MGT723 Research Proposal: Carbon Disclosure and Stakeholder Influence

VerifiedAdded on 2023/06/08

|7

|2378

|286

Report

AI Summary

This research proposal, prepared for MGT723, investigates the impact of stakeholder theory on corporate carbon emission disclosure. The study examines the influence of stakeholders, including consumers, on organizations' decisions to report carbon emissions and integrate climate change policies. It utilizes a descriptive research design and secondary data from the Carbon Disclosure Project (CDP) survey, analyzing 80 organizations. The research explores the relationship between climate change policy, financial implications, and voluntary disclosure levels, using both descriptive and inferential statistical analysis. The proposal outlines a conceptual model, hypotheses, and proxy measures, aiming to determine how stakeholder pressure, particularly from consumers, affects firms' carbon reporting behavior and whether financial gains influence emission reporting. The study acknowledges potential limitations, such as self-reporting bias and the exclusion of external factors, while seeking to understand the factors influencing carbon disclosure practices.

MGT723 Research Project

Semester 2 2018

Assessment Task 1: Research Proposal

Student Name: XXX

Draft Research Question: XXX

Title: XXX

Submission Date: XXX

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand that

the source of ideas must be referenced and that quotation marks and a reference are required when

directly quoting anyone else’s words.

Semester 2 2018

Assessment Task 1: Research Proposal

Student Name: XXX

Draft Research Question: XXX

Title: XXX

Submission Date: XXX

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand that

the source of ideas must be referenced and that quotation marks and a reference are required when

directly quoting anyone else’s words.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Literature Review - Summary

Motivation:

Industrial contribution to activities that have fuelled this fast change in ecological

conditions leading to catastrophic implications for the future generations have been since

then widely discussed and addressed across all spheres. Industrial role in curbing climate

change is therefore pose to be one of the prime challenges today (Liesen et al. 2015). Taking

into cognizance the social awareness as well as the real threat to the future implications,

companies have been drawing up strategic policies that work to curb activities which are

identified as the sources of the problem and committing to report on their activities as

checks to such behaviour (Bebbington and Larrinaga 2014). Greenhouse and carbon

emission are one of the main information that many organizations are expected and

encouraged to disclose as per of the carbon disclosure project (CDP). This is done with the

motivation to reveal the strategies and commitment of the firms to reduce their carbon

output which is one of the main avenues by which industries have affected climate (Hahn,

Reimsbach and Schiemann 2015). However not all the organizations have come on board

yet and the impact is yet to be significant. It is of interest to understand just what drives an

organization to commit to the cause to curb climate change. Stakeholder theory in this case

is a viable option. Stakeholders are those with whom organizations have aligned interests.

Influence of these groups can thus be expected to have an impact on organizational policies.

Theory

Stakeholder theory deals with the ethical aspect of the managerial division of a

business or any other organization. It is a conceptual frame work for policy making that

takes into account the moral accountability of the organization and its management (R

Edward freeman). According to stakeholder view, an organization’s strategy ought to

integrate with the market-based view and the resource-based view, a degree of socio-

political caution (Hörisch, Freeman and Schaltegger 2014). According to the normative

theory of identifying stakeholders, any person or a group of people or another organisation

who may or may not be an internal member of the organization with whom the

organization’s interest ally is a stakeholder. They include consumers, shareholders as well

as competitors and partners. The first people who come to mind when considering who

holds the stakes at an organization are the shareholders. However beside the obvious,

stakeholders include all whose actions and contributions influence company performance,

like employees, customers and business associates other than shareholders (Bridoux and

Stoelhorst 2014). These people hold the position to continuously challenge the organisation

in how they manage and allocate their resources thus influencing their operational policies

(Herold, Lee and Gunarathne 2018). The stakeholder salience theory speaks about how

stakeholders influence the management in their decision making process. They argue that

stakeholders such as the consumers, shareholders as well as competitors and partners who

may build pressure on certain issues could influence management to come up with the

disclosure data as a testament to their commitment (de Aguiar and Bebbington 2014). This

can be attributed to the fact that this issues touches all of society including the stakeholders

and the rising concern about climate change and the perceived accountability of the

2 | P a g e

Motivation:

Industrial contribution to activities that have fuelled this fast change in ecological

conditions leading to catastrophic implications for the future generations have been since

then widely discussed and addressed across all spheres. Industrial role in curbing climate

change is therefore pose to be one of the prime challenges today (Liesen et al. 2015). Taking

into cognizance the social awareness as well as the real threat to the future implications,

companies have been drawing up strategic policies that work to curb activities which are

identified as the sources of the problem and committing to report on their activities as

checks to such behaviour (Bebbington and Larrinaga 2014). Greenhouse and carbon

emission are one of the main information that many organizations are expected and

encouraged to disclose as per of the carbon disclosure project (CDP). This is done with the

motivation to reveal the strategies and commitment of the firms to reduce their carbon

output which is one of the main avenues by which industries have affected climate (Hahn,

Reimsbach and Schiemann 2015). However not all the organizations have come on board

yet and the impact is yet to be significant. It is of interest to understand just what drives an

organization to commit to the cause to curb climate change. Stakeholder theory in this case

is a viable option. Stakeholders are those with whom organizations have aligned interests.

Influence of these groups can thus be expected to have an impact on organizational policies.

Theory

Stakeholder theory deals with the ethical aspect of the managerial division of a

business or any other organization. It is a conceptual frame work for policy making that

takes into account the moral accountability of the organization and its management (R

Edward freeman). According to stakeholder view, an organization’s strategy ought to

integrate with the market-based view and the resource-based view, a degree of socio-

political caution (Hörisch, Freeman and Schaltegger 2014). According to the normative

theory of identifying stakeholders, any person or a group of people or another organisation

who may or may not be an internal member of the organization with whom the

organization’s interest ally is a stakeholder. They include consumers, shareholders as well

as competitors and partners. The first people who come to mind when considering who

holds the stakes at an organization are the shareholders. However beside the obvious,

stakeholders include all whose actions and contributions influence company performance,

like employees, customers and business associates other than shareholders (Bridoux and

Stoelhorst 2014). These people hold the position to continuously challenge the organisation

in how they manage and allocate their resources thus influencing their operational policies

(Herold, Lee and Gunarathne 2018). The stakeholder salience theory speaks about how

stakeholders influence the management in their decision making process. They argue that

stakeholders such as the consumers, shareholders as well as competitors and partners who

may build pressure on certain issues could influence management to come up with the

disclosure data as a testament to their commitment (de Aguiar and Bebbington 2014). This

can be attributed to the fact that this issues touches all of society including the stakeholders

and the rising concern about climate change and the perceived accountability of the

2 | P a g e

organizations by the stakeholders places certain expectations from stakeholders onto the

company. The organization in response to these expectations would give first priority to its

stakeholders and align their operational strategy along the interest of the stakeholders

(Herold, Lee, and Gunarathne 2018). Given the power that they hold on the company, the

stakeholders are in a position to put pressure to respond to their concerns by means of

environmental and social disclosure and this is supported by empirical evidence (Liesen et

al. 2015). Stakeholders thus have a key role to play in how the organization performs or

commits to perform on enforcing carbon friendly policies through their decisions and

reporting.

Stakeholder research is hence a significant aspect in business management studies. An

understanding of who the stakeholders of the firm are can help in giving insight about what

drives the organization and how they would act in various situations (Hörisch, Freeman and

Schaltegger 2014). The primary objective of the research methodology is then to identify

who the stakeholders are and the direction and magnitude of their influence on the many

levels of organizational activity. Environment disclosure is one of the most popular areas

that seems to have been benefitted by the influence of stakeholders and thus serve as a

validation of the stakeholder theory as a conceptual framework (Weber et al. 2016).

A number of literature is available which address the connection between carbon

disclosure and environmental impact. However none of those have been seen to be

consistent. Again, existing research, notable among which is Schreck and Raithel (2018)

shows that firms commit to reporting on emissions out of the belief that by doing so they

would establish image as environmentally conscious and therefore cater to the growing

environmentally conscious consumers in the market. Again, as per the Voluntary disclosure

theory, it is asserted that firms which are superior in terms of performance are more likely

to be aligned with environmental disclosure and thus this can form a basis to differentiate

the superior firms from the inferior ones (Birchall, Murphy and Milne 2015). Liesen (2015)

again showed that stakeholders have a significant impact on carbon disclosures of

organizations in Europe. Hence all these elements may be of significance when considering

the carbon disclosure by an organization. This study in particular makes use of stakeholder

theory and statistical data analysis to explore the problem using empirical research.

The study here then takes as the variable of interest the attribute of a company to

engage in voluntary disclosure as its relevance was explored by Lee, Park and Klassen

(2015). The integration of climate change in the firm’s policies is taken as a predictor or

independent variable (Weber et al. 2016). Additionally the analysis uses stakeholder

research to identify the factors that may influence carbon disclosure, that is, whether the

consumers as stakeholders in the firm have a hand in influencing firm’s disclosure

policies(Lee, Park, and Klassen 2015). A firm which feels obligated to cater to the growing

demand for environmental friendly policies from consumers would be able to capture

market advantage better than one which chooses to remain oblivious and this would

naturally lead to financial implications given the impact on its market. This factor is then

taken as control variables to the model. The following section shows the conceptual model

of the study. The control variable for this case focuses on the market pressures from

consumers that is experienced by the firms and how they may interact with the size of the

firm in how it responds to the carbon disclosure project objectives and its ensuing

performance.

3 | P a g e

company. The organization in response to these expectations would give first priority to its

stakeholders and align their operational strategy along the interest of the stakeholders

(Herold, Lee, and Gunarathne 2018). Given the power that they hold on the company, the

stakeholders are in a position to put pressure to respond to their concerns by means of

environmental and social disclosure and this is supported by empirical evidence (Liesen et

al. 2015). Stakeholders thus have a key role to play in how the organization performs or

commits to perform on enforcing carbon friendly policies through their decisions and

reporting.

Stakeholder research is hence a significant aspect in business management studies. An

understanding of who the stakeholders of the firm are can help in giving insight about what

drives the organization and how they would act in various situations (Hörisch, Freeman and

Schaltegger 2014). The primary objective of the research methodology is then to identify

who the stakeholders are and the direction and magnitude of their influence on the many

levels of organizational activity. Environment disclosure is one of the most popular areas

that seems to have been benefitted by the influence of stakeholders and thus serve as a

validation of the stakeholder theory as a conceptual framework (Weber et al. 2016).

A number of literature is available which address the connection between carbon

disclosure and environmental impact. However none of those have been seen to be

consistent. Again, existing research, notable among which is Schreck and Raithel (2018)

shows that firms commit to reporting on emissions out of the belief that by doing so they

would establish image as environmentally conscious and therefore cater to the growing

environmentally conscious consumers in the market. Again, as per the Voluntary disclosure

theory, it is asserted that firms which are superior in terms of performance are more likely

to be aligned with environmental disclosure and thus this can form a basis to differentiate

the superior firms from the inferior ones (Birchall, Murphy and Milne 2015). Liesen (2015)

again showed that stakeholders have a significant impact on carbon disclosures of

organizations in Europe. Hence all these elements may be of significance when considering

the carbon disclosure by an organization. This study in particular makes use of stakeholder

theory and statistical data analysis to explore the problem using empirical research.

The study here then takes as the variable of interest the attribute of a company to

engage in voluntary disclosure as its relevance was explored by Lee, Park and Klassen

(2015). The integration of climate change in the firm’s policies is taken as a predictor or

independent variable (Weber et al. 2016). Additionally the analysis uses stakeholder

research to identify the factors that may influence carbon disclosure, that is, whether the

consumers as stakeholders in the firm have a hand in influencing firm’s disclosure

policies(Lee, Park, and Klassen 2015). A firm which feels obligated to cater to the growing

demand for environmental friendly policies from consumers would be able to capture

market advantage better than one which chooses to remain oblivious and this would

naturally lead to financial implications given the impact on its market. This factor is then

taken as control variables to the model. The following section shows the conceptual model

of the study. The control variable for this case focuses on the market pressures from

consumers that is experienced by the firms and how they may interact with the size of the

firm in how it responds to the carbon disclosure project objectives and its ensuing

performance.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

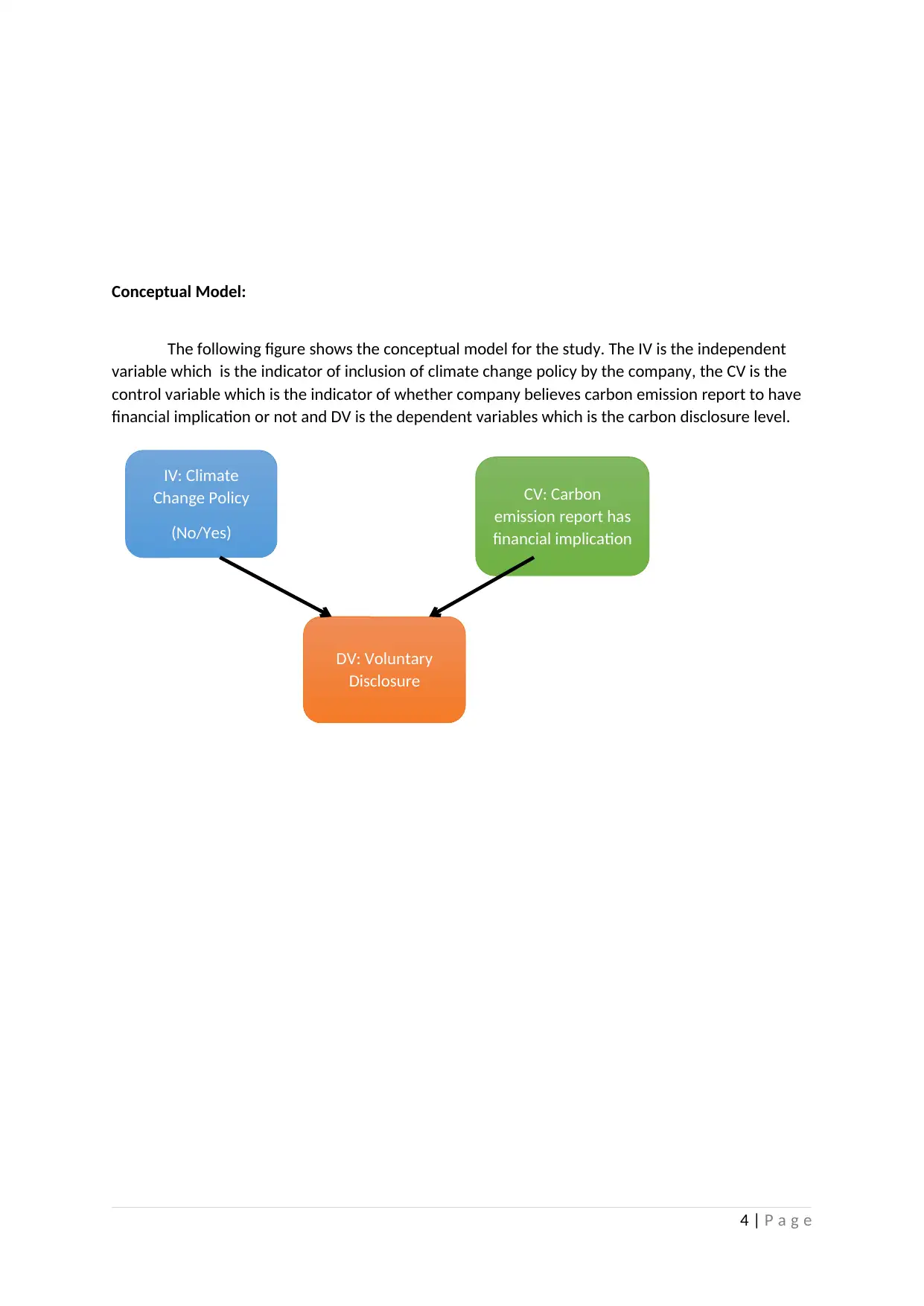

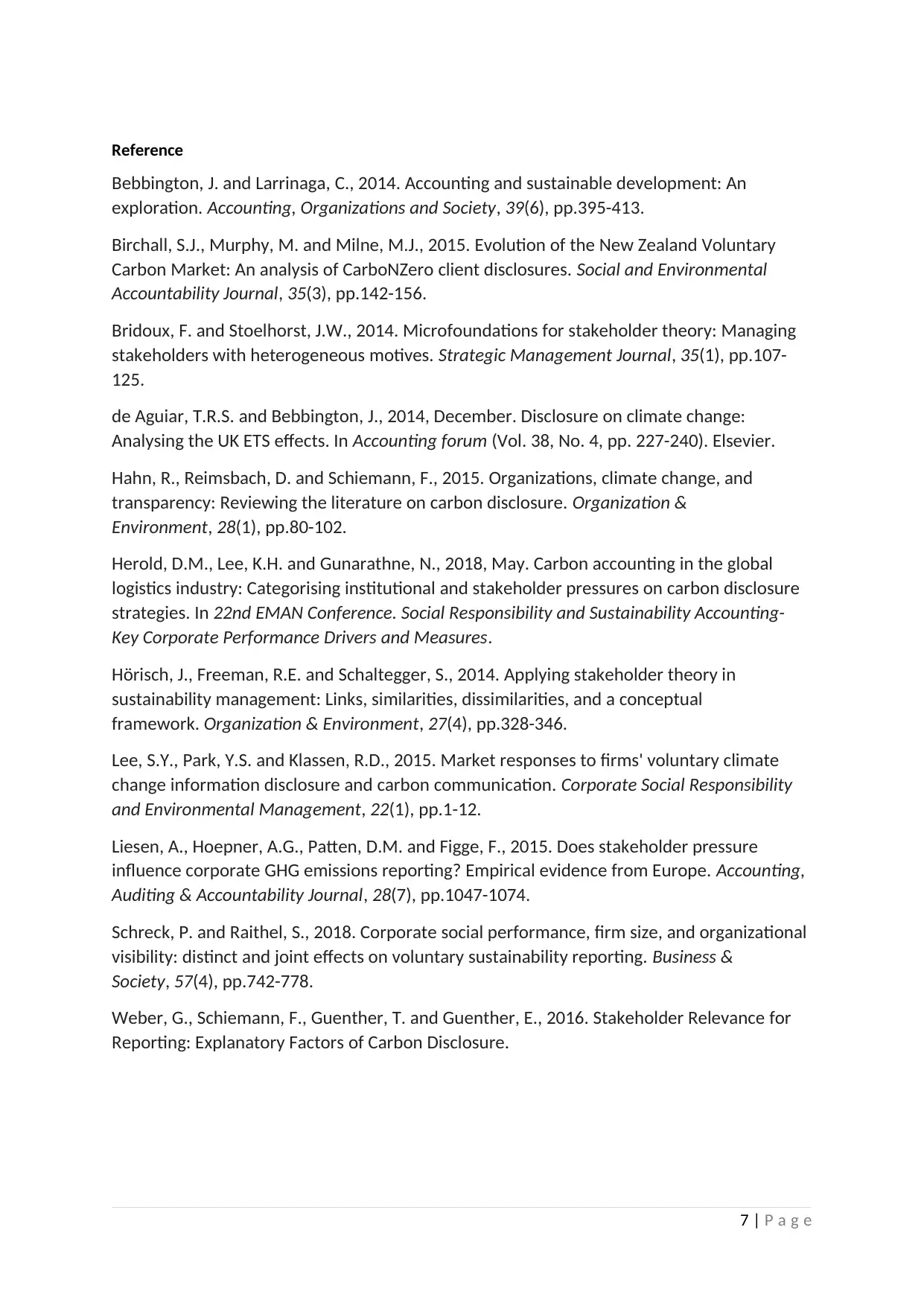

Conceptual Model:

The following figure shows the conceptual model for the study. The IV is the independent

variable which is the indicator of inclusion of climate change policy by the company, the CV is the

control variable which is the indicator of whether company believes carbon emission report to have

financial implication or not and DV is the dependent variables which is the carbon disclosure level.

4 | P a g e

IV: Climate

Change Policy

(No/Yes)

CV: Carbon

emission report has

financial implication

DV: Voluntary

Disclosure

The following figure shows the conceptual model for the study. The IV is the independent

variable which is the indicator of inclusion of climate change policy by the company, the CV is the

control variable which is the indicator of whether company believes carbon emission report to have

financial implication or not and DV is the dependent variables which is the carbon disclosure level.

4 | P a g e

IV: Climate

Change Policy

(No/Yes)

CV: Carbon

emission report has

financial implication

DV: Voluntary

Disclosure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hypothesis

H1: Financial gain on account of being market leader influences organization’s carbon

emission reporting.

H2: An organization that takes into account climate change into its business strategies

has lower reported carbon emissions.

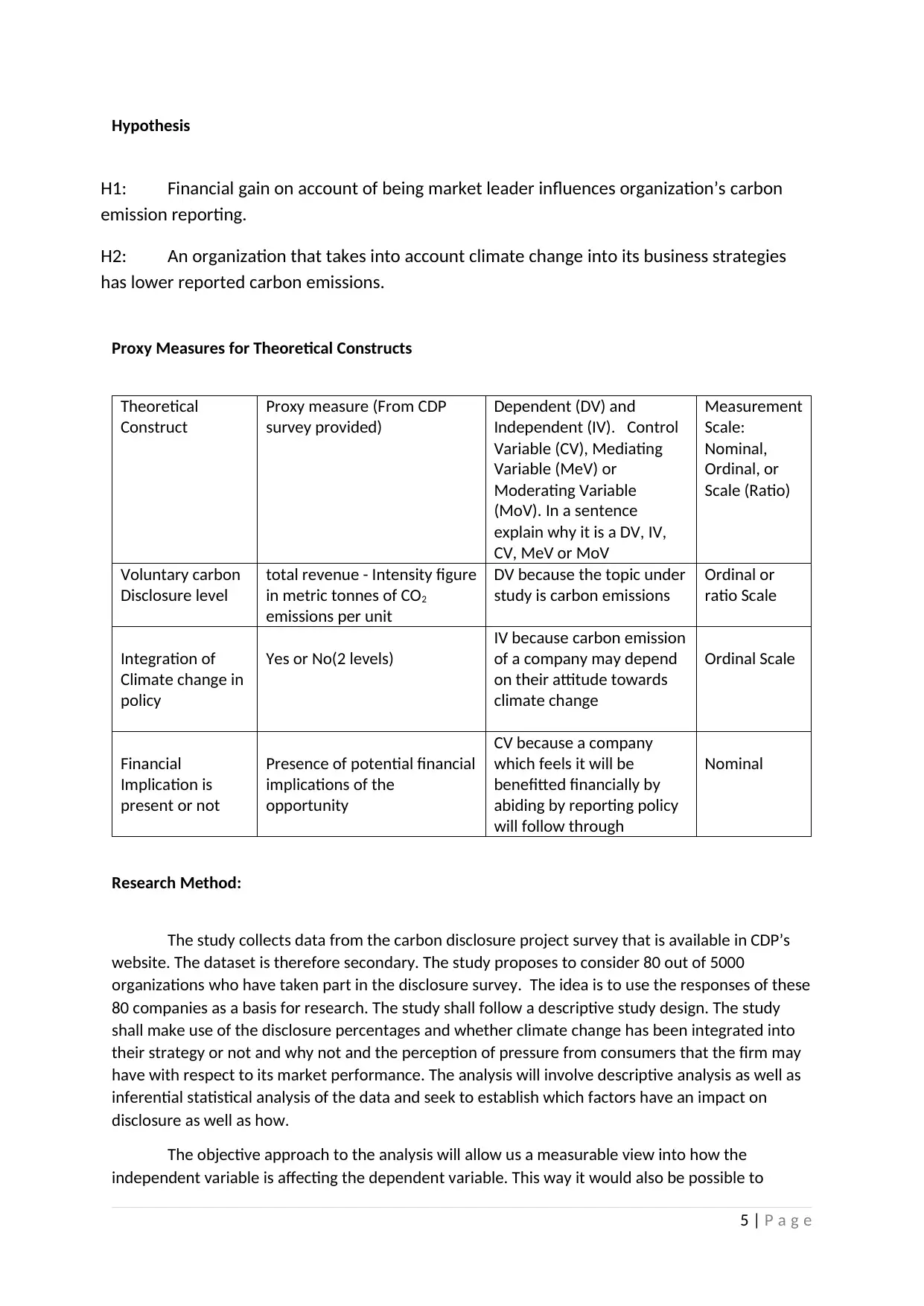

Proxy Measures for Theoretical Constructs

Theoretical

Construct

Proxy measure (From CDP

survey provided)

Dependent (DV) and

Independent (IV). Control

Variable (CV), Mediating

Variable (MeV) or

Moderating Variable

(MoV). In a sentence

explain why it is a DV, IV,

CV, MeV or MoV

Measurement

Scale:

Nominal,

Ordinal, or

Scale (Ratio)

Voluntary carbon

Disclosure level

total revenue - Intensity figure

in metric tonnes of CO2

emissions per unit

DV because the topic under

study is carbon emissions

Ordinal or

ratio Scale

Integration of

Climate change in

policy

Yes or No(2 levels)

IV because carbon emission

of a company may depend

on their attitude towards

climate change

Ordinal Scale

Financial

Implication is

present or not

Presence of potential financial

implications of the

opportunity

CV because a company

which feels it will be

benefitted financially by

abiding by reporting policy

will follow through

Nominal

Research Method:

The study collects data from the carbon disclosure project survey that is available in CDP’s

website. The dataset is therefore secondary. The study proposes to consider 80 out of 5000

organizations who have taken part in the disclosure survey. The idea is to use the responses of these

80 companies as a basis for research. The study shall follow a descriptive study design. The study

shall make use of the disclosure percentages and whether climate change has been integrated into

their strategy or not and why not and the perception of pressure from consumers that the firm may

have with respect to its market performance. The analysis will involve descriptive analysis as well as

inferential statistical analysis of the data and seek to establish which factors have an impact on

disclosure as well as how.

The objective approach to the analysis will allow us a measurable view into how the

independent variable is affecting the dependent variable. This way it would also be possible to

5 | P a g e

H1: Financial gain on account of being market leader influences organization’s carbon

emission reporting.

H2: An organization that takes into account climate change into its business strategies

has lower reported carbon emissions.

Proxy Measures for Theoretical Constructs

Theoretical

Construct

Proxy measure (From CDP

survey provided)

Dependent (DV) and

Independent (IV). Control

Variable (CV), Mediating

Variable (MeV) or

Moderating Variable

(MoV). In a sentence

explain why it is a DV, IV,

CV, MeV or MoV

Measurement

Scale:

Nominal,

Ordinal, or

Scale (Ratio)

Voluntary carbon

Disclosure level

total revenue - Intensity figure

in metric tonnes of CO2

emissions per unit

DV because the topic under

study is carbon emissions

Ordinal or

ratio Scale

Integration of

Climate change in

policy

Yes or No(2 levels)

IV because carbon emission

of a company may depend

on their attitude towards

climate change

Ordinal Scale

Financial

Implication is

present or not

Presence of potential financial

implications of the

opportunity

CV because a company

which feels it will be

benefitted financially by

abiding by reporting policy

will follow through

Nominal

Research Method:

The study collects data from the carbon disclosure project survey that is available in CDP’s

website. The dataset is therefore secondary. The study proposes to consider 80 out of 5000

organizations who have taken part in the disclosure survey. The idea is to use the responses of these

80 companies as a basis for research. The study shall follow a descriptive study design. The study

shall make use of the disclosure percentages and whether climate change has been integrated into

their strategy or not and why not and the perception of pressure from consumers that the firm may

have with respect to its market performance. The analysis will involve descriptive analysis as well as

inferential statistical analysis of the data and seek to establish which factors have an impact on

disclosure as well as how.

The objective approach to the analysis will allow us a measurable view into how the

independent variable is affecting the dependent variable. This way it would also be possible to

5 | P a g e

measure any possible errors in the assumptions. The concern involved in this approach is the validity

of the data. Since the companies have self-reported these statistics, it is speculated that the

performance and disclosure might be biased in favour of the company. Also there may be countless

other factors which are not being addressed in the model which cannot be easily measured such as

external social and political influences.

Overall it is expected that by the end of the survey the question that whether a company

which is larger in size is more likely to readily disclose their carbon emissions or not and whether a

company which actively includes climate change in its strategy model is likely to cause more

emissions or not could be answered.

6 | P a g e

of the data. Since the companies have self-reported these statistics, it is speculated that the

performance and disclosure might be biased in favour of the company. Also there may be countless

other factors which are not being addressed in the model which cannot be easily measured such as

external social and political influences.

Overall it is expected that by the end of the survey the question that whether a company

which is larger in size is more likely to readily disclose their carbon emissions or not and whether a

company which actively includes climate change in its strategy model is likely to cause more

emissions or not could be answered.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference

Bebbington, J. and Larrinaga, C., 2014. Accounting and sustainable development: An

exploration. Accounting, Organizations and Society, 39(6), pp.395-413.

Birchall, S.J., Murphy, M. and Milne, M.J., 2015. Evolution of the New Zealand Voluntary

Carbon Market: An analysis of CarboNZero client disclosures. Social and Environmental

Accountability Journal, 35(3), pp.142-156.

Bridoux, F. and Stoelhorst, J.W., 2014. Microfoundations for stakeholder theory: Managing

stakeholders with heterogeneous motives. Strategic Management Journal, 35(1), pp.107-

125.

de Aguiar, T.R.S. and Bebbington, J., 2014, December. Disclosure on climate change:

Analysing the UK ETS effects. In Accounting forum (Vol. 38, No. 4, pp. 227-240). Elsevier.

Hahn, R., Reimsbach, D. and Schiemann, F., 2015. Organizations, climate change, and

transparency: Reviewing the literature on carbon disclosure. Organization &

Environment, 28(1), pp.80-102.

Herold, D.M., Lee, K.H. and Gunarathne, N., 2018, May. Carbon accounting in the global

logistics industry: Categorising institutional and stakeholder pressures on carbon disclosure

strategies. In 22nd EMAN Conference. Social Responsibility and Sustainability Accounting-

Key Corporate Performance Drivers and Measures.

Hörisch, J., Freeman, R.E. and Schaltegger, S., 2014. Applying stakeholder theory in

sustainability management: Links, similarities, dissimilarities, and a conceptual

framework. Organization & Environment, 27(4), pp.328-346.

Lee, S.Y., Park, Y.S. and Klassen, R.D., 2015. Market responses to firms' voluntary climate

change information disclosure and carbon communication. Corporate Social Responsibility

and Environmental Management, 22(1), pp.1-12.

Liesen, A., Hoepner, A.G., Patten, D.M. and Figge, F., 2015. Does stakeholder pressure

influence corporate GHG emissions reporting? Empirical evidence from Europe. Accounting,

Auditing & Accountability Journal, 28(7), pp.1047-1074.

Schreck, P. and Raithel, S., 2018. Corporate social performance, firm size, and organizational

visibility: distinct and joint effects on voluntary sustainability reporting. Business &

Society, 57(4), pp.742-778.

Weber, G., Schiemann, F., Guenther, T. and Guenther, E., 2016. Stakeholder Relevance for

Reporting: Explanatory Factors of Carbon Disclosure.

7 | P a g e

Bebbington, J. and Larrinaga, C., 2014. Accounting and sustainable development: An

exploration. Accounting, Organizations and Society, 39(6), pp.395-413.

Birchall, S.J., Murphy, M. and Milne, M.J., 2015. Evolution of the New Zealand Voluntary

Carbon Market: An analysis of CarboNZero client disclosures. Social and Environmental

Accountability Journal, 35(3), pp.142-156.

Bridoux, F. and Stoelhorst, J.W., 2014. Microfoundations for stakeholder theory: Managing

stakeholders with heterogeneous motives. Strategic Management Journal, 35(1), pp.107-

125.

de Aguiar, T.R.S. and Bebbington, J., 2014, December. Disclosure on climate change:

Analysing the UK ETS effects. In Accounting forum (Vol. 38, No. 4, pp. 227-240). Elsevier.

Hahn, R., Reimsbach, D. and Schiemann, F., 2015. Organizations, climate change, and

transparency: Reviewing the literature on carbon disclosure. Organization &

Environment, 28(1), pp.80-102.

Herold, D.M., Lee, K.H. and Gunarathne, N., 2018, May. Carbon accounting in the global

logistics industry: Categorising institutional and stakeholder pressures on carbon disclosure

strategies. In 22nd EMAN Conference. Social Responsibility and Sustainability Accounting-

Key Corporate Performance Drivers and Measures.

Hörisch, J., Freeman, R.E. and Schaltegger, S., 2014. Applying stakeholder theory in

sustainability management: Links, similarities, dissimilarities, and a conceptual

framework. Organization & Environment, 27(4), pp.328-346.

Lee, S.Y., Park, Y.S. and Klassen, R.D., 2015. Market responses to firms' voluntary climate

change information disclosure and carbon communication. Corporate Social Responsibility

and Environmental Management, 22(1), pp.1-12.

Liesen, A., Hoepner, A.G., Patten, D.M. and Figge, F., 2015. Does stakeholder pressure

influence corporate GHG emissions reporting? Empirical evidence from Europe. Accounting,

Auditing & Accountability Journal, 28(7), pp.1047-1074.

Schreck, P. and Raithel, S., 2018. Corporate social performance, firm size, and organizational

visibility: distinct and joint effects on voluntary sustainability reporting. Business &

Society, 57(4), pp.742-778.

Weber, G., Schiemann, F., Guenther, T. and Guenther, E., 2016. Stakeholder Relevance for

Reporting: Explanatory Factors of Carbon Disclosure.

7 | P a g e

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.