Carbon Emissions Accounting: Current Practices and Financial Impact

VerifiedAdded on 2020/02/24

|12

|2663

|128

Report

AI Summary

This report provides a comprehensive overview of carbon emissions accounting, focusing on the nature of emission allowances within the European Emission Trading Scheme (EU ETS) and their legal and accounting characteristics. It delves into the relevant accounting standards, including IAS 2, IAS 20, IAS 37, IAS 38, and IAS 39, and discusses how carbon emissions are accounted for under both US GAAP and IFRS. The report examines the measurement of emission credits and allowances, highlighting the intangible asset model and the inventory model, detailing their respective accounting treatments, and the impact on financial statements. It also addresses the current accounting practices in the United States, the recognition of liabilities and gains, and the application of derivative accounting to emission credits. The analysis covers the effect of emission credits on financial statements, including reporting allowances as inventory or intangible assets, and the recognition of costs and liabilities. The report emphasizes the importance of understanding these accounting methods for effective financial reporting and compliance.

CARBON EMISSIONS ACCOUNTING 1

CARBON EMISSIONS

ACCOUNTING

CARBON EMISSIONS

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CARBON EMISSIONS ACCOUNTING 2

Nature of emission allowances:

Mainly the legal nature of the allowances for the emissions have been issued and also are

traded under the rules of the European emission Trading Scheme (EU ETS). This is though

has not been harmonised at the level of the EU.

The definition of the term allowances has been done under the Article 3(a) of the ETS

Directive wherein it has been prescribed that only one tonne of carbon dioxide shall be

emitted during any period. This would be valid in order to meet the requirements that have

been laid done under the ETS Directive. This would also be transferrable as per the

provisions of the ETC Directive. The notification issued in this regard reports on the

functioning of the carbon market of Europe. This accompanies the report on the

documentation which forms the part of the council. There has been a climate action progress

report that includes the functioning of the carbon market f Europe and also the report which

lays down its view of the Directive 2009/31/EC. This has been done on the geological storage

of the carbon dioxide as on the date of November 18, 2015. This describes the emission

allowances as the following:

Financial instruments

Intangible assets

Property rights

State property

Commodities (Emissions, 2017).

Accounting nature:

As per the IASB rules, wherein the accounting standards fail to apply on the company, then

the disclosure has to be made as per the IAS 8 Accounting Policies, Changes in accounting

Nature of emission allowances:

Mainly the legal nature of the allowances for the emissions have been issued and also are

traded under the rules of the European emission Trading Scheme (EU ETS). This is though

has not been harmonised at the level of the EU.

The definition of the term allowances has been done under the Article 3(a) of the ETS

Directive wherein it has been prescribed that only one tonne of carbon dioxide shall be

emitted during any period. This would be valid in order to meet the requirements that have

been laid done under the ETS Directive. This would also be transferrable as per the

provisions of the ETC Directive. The notification issued in this regard reports on the

functioning of the carbon market of Europe. This accompanies the report on the

documentation which forms the part of the council. There has been a climate action progress

report that includes the functioning of the carbon market f Europe and also the report which

lays down its view of the Directive 2009/31/EC. This has been done on the geological storage

of the carbon dioxide as on the date of November 18, 2015. This describes the emission

allowances as the following:

Financial instruments

Intangible assets

Property rights

State property

Commodities (Emissions, 2017).

Accounting nature:

As per the IASB rules, wherein the accounting standards fail to apply on the company, then

the disclosure has to be made as per the IAS 8 Accounting Policies, Changes in accounting

CARBON EMISSIONS ACCOUNTING 3

Estimates and Errors. This requires in the fact that the management must use their judgment

when it comes to the development and the application of the policy of accounting which

result in the information which is relevant and also reliable. This has to be done in

consultation with the auditors of the firm. The following are the accounting standards as per

which the accounting would take place:

International Accounting Standard (IAS) 2 Inventories;

IAS 20 Accounting for Government Grants and Disclosure of Government

Assistance;

IAS 37 Provisions, Contingent Liabilities and Contingent Assets;

IAS 38 Intangible Assets; and

IAS 39 Financial Instruments: Recognition and Measurement.

The carbon emissions are taken into account in accounts as per the Commodities, for

trading purposes etc.

Measurement:

Under the system, the producers of the electric power were given or also they had acquired in

the credits with regard to the free credits which covers up the SO2 and also the NOx

emissions but there is as such no accounting standard under the US GAAP which would

throw some light on the financial accounting for the programs of emissions. The FASB has

joined hands with the International Accounting standards Board or the IASB that would

address in the scheme of the carbon emissions for the purposes of accounting. There are some

more regulations that relates with the emissions that have been produced by the largest

sources of the nation. The EPA has been making it compulsory for the companies to report

the GHG levels (Hindu business line, 2017). There are many of the companies that would

account for the cap and trade activities which are connected with the program when there are

Estimates and Errors. This requires in the fact that the management must use their judgment

when it comes to the development and the application of the policy of accounting which

result in the information which is relevant and also reliable. This has to be done in

consultation with the auditors of the firm. The following are the accounting standards as per

which the accounting would take place:

International Accounting Standard (IAS) 2 Inventories;

IAS 20 Accounting for Government Grants and Disclosure of Government

Assistance;

IAS 37 Provisions, Contingent Liabilities and Contingent Assets;

IAS 38 Intangible Assets; and

IAS 39 Financial Instruments: Recognition and Measurement.

The carbon emissions are taken into account in accounts as per the Commodities, for

trading purposes etc.

Measurement:

Under the system, the producers of the electric power were given or also they had acquired in

the credits with regard to the free credits which covers up the SO2 and also the NOx

emissions but there is as such no accounting standard under the US GAAP which would

throw some light on the financial accounting for the programs of emissions. The FASB has

joined hands with the International Accounting standards Board or the IASB that would

address in the scheme of the carbon emissions for the purposes of accounting. There are some

more regulations that relates with the emissions that have been produced by the largest

sources of the nation. The EPA has been making it compulsory for the companies to report

the GHG levels (Hindu business line, 2017). There are many of the companies that would

account for the cap and trade activities which are connected with the program when there are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CARBON EMISSIONS ACCOUNTING 4

as such no specific authoritative guidance on the procedure. There are many of the companies

that are duty bound to report the impact of the change in the climate and the regulations of the

GHG emissions in their financial statements on Form 10 K. it is of an utmost importance that

the companies have the management strategy for carbon since those activities would help

them in complying and accounting for these stated activities but also the company will be

allowed to take the advantage of all of the credits and offset the same through the way of

strategic acquisition (ACCA global, 2017).

Current accounting practices:

There are many of the companies that have been operating in the United States and these

companies mostly belongs to the power and the utilities industry. These have been acquired

for the purposes of participating in the EPA, RGGI and other such programs related with such

carbon emissions and these have been associated since a long number of years. There are

many of the programs that have a cap and trade model as well. Since there is an absence of a

set standard in the US GAAP or in the (IFRS) which takes into account the emission credits,

renewable energy, emission offsets or such similar allowances, hence different practices are

being followed in this respect. Hence, there is an urgent need of providing a framework for

the purposes of accounting for the climatic changes, the one that could be applied to all of the

industries without any issue. The FASB and the IASB have joined in hands so as to work for

the emissions trading schemes since the year 2007 (PBR, 2017).

Current accounting for emissions credits or allowances:

as such no specific authoritative guidance on the procedure. There are many of the companies

that are duty bound to report the impact of the change in the climate and the regulations of the

GHG emissions in their financial statements on Form 10 K. it is of an utmost importance that

the companies have the management strategy for carbon since those activities would help

them in complying and accounting for these stated activities but also the company will be

allowed to take the advantage of all of the credits and offset the same through the way of

strategic acquisition (ACCA global, 2017).

Current accounting practices:

There are many of the companies that have been operating in the United States and these

companies mostly belongs to the power and the utilities industry. These have been acquired

for the purposes of participating in the EPA, RGGI and other such programs related with such

carbon emissions and these have been associated since a long number of years. There are

many of the programs that have a cap and trade model as well. Since there is an absence of a

set standard in the US GAAP or in the (IFRS) which takes into account the emission credits,

renewable energy, emission offsets or such similar allowances, hence different practices are

being followed in this respect. Hence, there is an urgent need of providing a framework for

the purposes of accounting for the climatic changes, the one that could be applied to all of the

industries without any issue. The FASB and the IASB have joined in hands so as to work for

the emissions trading schemes since the year 2007 (PBR, 2017).

Current accounting for emissions credits or allowances:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CARBON EMISSIONS ACCOUNTING 5

The companies that have been following the US GAAP today participate in the programs that

are related with the carbon emissions follow one of the two different accounting practices.

The first being the intangible asset model and the other being an inventory model.

Accounting of emission allowances:

Accounting under the intangible asset model:

Under this method, the companies measure the emission credits or the allowances that have

bene issued to then and the same have been acquired by them in the open market and values

them at cost. Hence, as and when the company issues the emissions credits or the allowances,

then it would have the nominal cost of 0. Also, there are many of the emission credits or the

allowances that have been purchased will have some cost associated with the same. When

commonly applied, under the model of the intangible asset accounting, it is also possible for

the company to indicate the emissions credit or the allowance that have been issued at their

fair value when the same have been received (Wordpress, 2017). On the basis of these

disclosures, the companies would not amortize the emissions credits since the economic

benefit of the same does not diminish till the time the same are consumed by the company.

Also, the costs of the credits would not be charged till the time the same are sold or have been

used. These emission credits or the allowances are subject to the accounting standard on

impairment. These are considered to be indefinite and would live as an intangible asset and

the same will be reported under the model of impairment or for the impairment model of the

fixed assets for the intangible assets that have certain life. This is in line with the amount that

the company would amortise in the credit of the emissions. These are the credits of the

emissions that would be considered to be of long term in nature and also would amortise the

credit of the emissions. These emission credits are termed as being long term in nature in the

balance sheet and the cash inflows and the cash outflows are connected with the emission

The companies that have been following the US GAAP today participate in the programs that

are related with the carbon emissions follow one of the two different accounting practices.

The first being the intangible asset model and the other being an inventory model.

Accounting of emission allowances:

Accounting under the intangible asset model:

Under this method, the companies measure the emission credits or the allowances that have

bene issued to then and the same have been acquired by them in the open market and values

them at cost. Hence, as and when the company issues the emissions credits or the allowances,

then it would have the nominal cost of 0. Also, there are many of the emission credits or the

allowances that have been purchased will have some cost associated with the same. When

commonly applied, under the model of the intangible asset accounting, it is also possible for

the company to indicate the emissions credit or the allowance that have been issued at their

fair value when the same have been received (Wordpress, 2017). On the basis of these

disclosures, the companies would not amortize the emissions credits since the economic

benefit of the same does not diminish till the time the same are consumed by the company.

Also, the costs of the credits would not be charged till the time the same are sold or have been

used. These emission credits or the allowances are subject to the accounting standard on

impairment. These are considered to be indefinite and would live as an intangible asset and

the same will be reported under the model of impairment or for the impairment model of the

fixed assets for the intangible assets that have certain life. This is in line with the amount that

the company would amortise in the credit of the emissions. These are the credits of the

emissions that would be considered to be of long term in nature and also would amortise the

credit of the emissions. These emission credits are termed as being long term in nature in the

balance sheet and the cash inflows and the cash outflows are connected with the emission

CARBON EMISSIONS ACCOUNTING 6

credits which are further classified as the investment activities in the statement of cash flows

of the financial statements of the company.

Accounting under the inventory model:

Under this model, the emission credits are measured at the weighted average costs. Each of

the emission credit as have been issued by the EPA or other such regulatory body would have

a 0 cost basis while when the same are purchased, then the emission credit’s would be valued

at the purchase price. The credits of the emission are valued using the weighted average cost

of the emission credits would be used for each one of the periods which is then to the fuel

costs or to the cost of sales. These credits are valued at the lower of cost of the market

approach to the impairment under the model of inventory accounting. These emission credits

are reported as inventory in the statement of financial position. The cash inflows and the

outflows as are connected with the emission credits are classified as the operating activities in

the statement of cash flows. The companies that trade in the emission credits would follow

this model. In case the company trades in the emission credits which is within the scope of

industry guidance for the broker dealer. These are considered to be the emission credits that

are held for sale ta their fair values at each of the reporting date (desai, 2017).

Accounting with liability and gain recognition:

Under both of the above stated models, the practice if that the obligation is recorded for the

purposes of delivering in the emission credits to the regulatory agency till the time actual

level of the emissions for any given period exceeds the credits that have been held in the

balance sheet. The gain which is recorded or is recognised in the period in which the

emission credits have been sold. But there is still a practise wherein there is a recognition of

credits which are further classified as the investment activities in the statement of cash flows

of the financial statements of the company.

Accounting under the inventory model:

Under this model, the emission credits are measured at the weighted average costs. Each of

the emission credit as have been issued by the EPA or other such regulatory body would have

a 0 cost basis while when the same are purchased, then the emission credit’s would be valued

at the purchase price. The credits of the emission are valued using the weighted average cost

of the emission credits would be used for each one of the periods which is then to the fuel

costs or to the cost of sales. These credits are valued at the lower of cost of the market

approach to the impairment under the model of inventory accounting. These emission credits

are reported as inventory in the statement of financial position. The cash inflows and the

outflows as are connected with the emission credits are classified as the operating activities in

the statement of cash flows. The companies that trade in the emission credits would follow

this model. In case the company trades in the emission credits which is within the scope of

industry guidance for the broker dealer. These are considered to be the emission credits that

are held for sale ta their fair values at each of the reporting date (desai, 2017).

Accounting with liability and gain recognition:

Under both of the above stated models, the practice if that the obligation is recorded for the

purposes of delivering in the emission credits to the regulatory agency till the time actual

level of the emissions for any given period exceeds the credits that have been held in the

balance sheet. The gain which is recorded or is recognised in the period in which the

emission credits have been sold. But there is still a practise wherein there is a recognition of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CARBON EMISSIONS ACCOUNTING 7

the gain since there are many of the companies that have adopted the stated accounting

policy. This further requires in the deferral of the gain in the case the emission credits have

been granted for the future vintage year but then are sold within the current year. In such a

case, the gain may not be termed a being realizable since the company is not bale to cover its

emission in the future vintage and this is mainly due to the sale of the emission credit’s that

were granted for the purposes of covering the future vintage year emissions.

Derivative accounting:

It is a common practise for these companies to enter into the future contracts, swaps and the

options that pertain to the emission credits. These are the arrangements that meets in the

definition of the derivative under the US GAAP. There are many of the forward contracts that

could be delivered physically wherein the net settlement would not take place and the same

will not be exposed to the normal amount of the purchases of the exemption of the normal

sales. These are the products that would settle in financially and are required to be accounted

at their fair values. Since these markets still continues to expand, more number of contracts

that could be covered within the stated scope would some under the definition of a derivative

(EY, 2017).

Effect on the financial statements:

The following are the impact of the emission credits on the financial statements:

The allowances of emissions are reported as inventory

The allowances for emissions are reported as the intangible assets

The amount of the allowance are recorded at nil cost when the same have been

received from the government since they are free. The difference between the cost and

the gain since there are many of the companies that have adopted the stated accounting

policy. This further requires in the deferral of the gain in the case the emission credits have

been granted for the future vintage year but then are sold within the current year. In such a

case, the gain may not be termed a being realizable since the company is not bale to cover its

emission in the future vintage and this is mainly due to the sale of the emission credit’s that

were granted for the purposes of covering the future vintage year emissions.

Derivative accounting:

It is a common practise for these companies to enter into the future contracts, swaps and the

options that pertain to the emission credits. These are the arrangements that meets in the

definition of the derivative under the US GAAP. There are many of the forward contracts that

could be delivered physically wherein the net settlement would not take place and the same

will not be exposed to the normal amount of the purchases of the exemption of the normal

sales. These are the products that would settle in financially and are required to be accounted

at their fair values. Since these markets still continues to expand, more number of contracts

that could be covered within the stated scope would some under the definition of a derivative

(EY, 2017).

Effect on the financial statements:

The following are the impact of the emission credits on the financial statements:

The allowances of emissions are reported as inventory

The allowances for emissions are reported as the intangible assets

The amount of the allowance are recorded at nil cost when the same have been

received from the government since they are free. The difference between the cost and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CARBON EMISSIONS ACCOUNTING 8

the fair value would be recognised on the liability side of the balance sheet

(Eureletrci, 2017).

The amount of the allowance are recognised at cost when the same are purchased by

the company

The amount of the allowances would be treated as an intangible asset when the same

is being treated on the cost revaluation model. In case, the revaluation model is

chosen, then the variations that arise in the fair value of the asset would be recognised

in equity. But in case, the cost model is chosen, then the asset would be depreciated

and this is mainly due to the reason that the same would go on to reduce its value by

its use in the process of production.

Further, the liability for the emission would be recognised on some linear basis but

the most recent practices for the recognition of the liability would occur.

Instead of being measuring this liability at its fair value, the guidance provides that

the allowances shall be carried forward at its market value.

The purchases of the forward of the allowances would be termed as being the

derivatives due to the use of the exemption. When this has been applied, then the

forward contract would entail the buying of the allowances of the emissions and the

same would be treated as the financial instruments which would then be measured at a

fair value. This would be considered as being a part of the fully performed contract

and its recognition in accounting would be postponed till the time the physical

delivery of the same takes place.

If these allowances are held for the trading purposes, then the holding or the purchase

of the allowances are not connected with the emissions, then the same would be

measured at their fair value and also the variations in the fair value would be charged

to the income (Law digital comms, 2017).

the fair value would be recognised on the liability side of the balance sheet

(Eureletrci, 2017).

The amount of the allowance are recognised at cost when the same are purchased by

the company

The amount of the allowances would be treated as an intangible asset when the same

is being treated on the cost revaluation model. In case, the revaluation model is

chosen, then the variations that arise in the fair value of the asset would be recognised

in equity. But in case, the cost model is chosen, then the asset would be depreciated

and this is mainly due to the reason that the same would go on to reduce its value by

its use in the process of production.

Further, the liability for the emission would be recognised on some linear basis but

the most recent practices for the recognition of the liability would occur.

Instead of being measuring this liability at its fair value, the guidance provides that

the allowances shall be carried forward at its market value.

The purchases of the forward of the allowances would be termed as being the

derivatives due to the use of the exemption. When this has been applied, then the

forward contract would entail the buying of the allowances of the emissions and the

same would be treated as the financial instruments which would then be measured at a

fair value. This would be considered as being a part of the fully performed contract

and its recognition in accounting would be postponed till the time the physical

delivery of the same takes place.

If these allowances are held for the trading purposes, then the holding or the purchase

of the allowances are not connected with the emissions, then the same would be

measured at their fair value and also the variations in the fair value would be charged

to the income (Law digital comms, 2017).

CARBON EMISSIONS ACCOUNTING 9

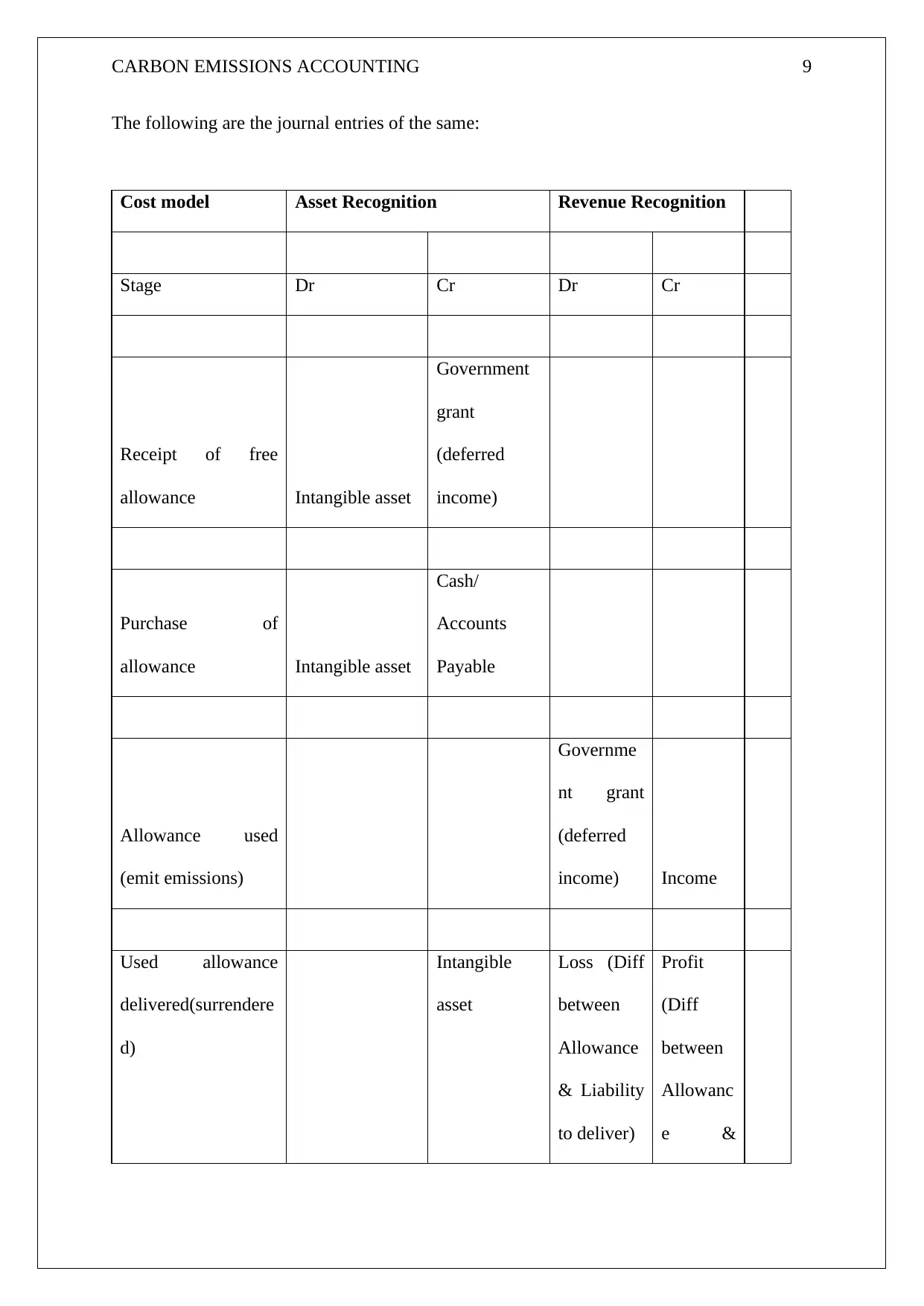

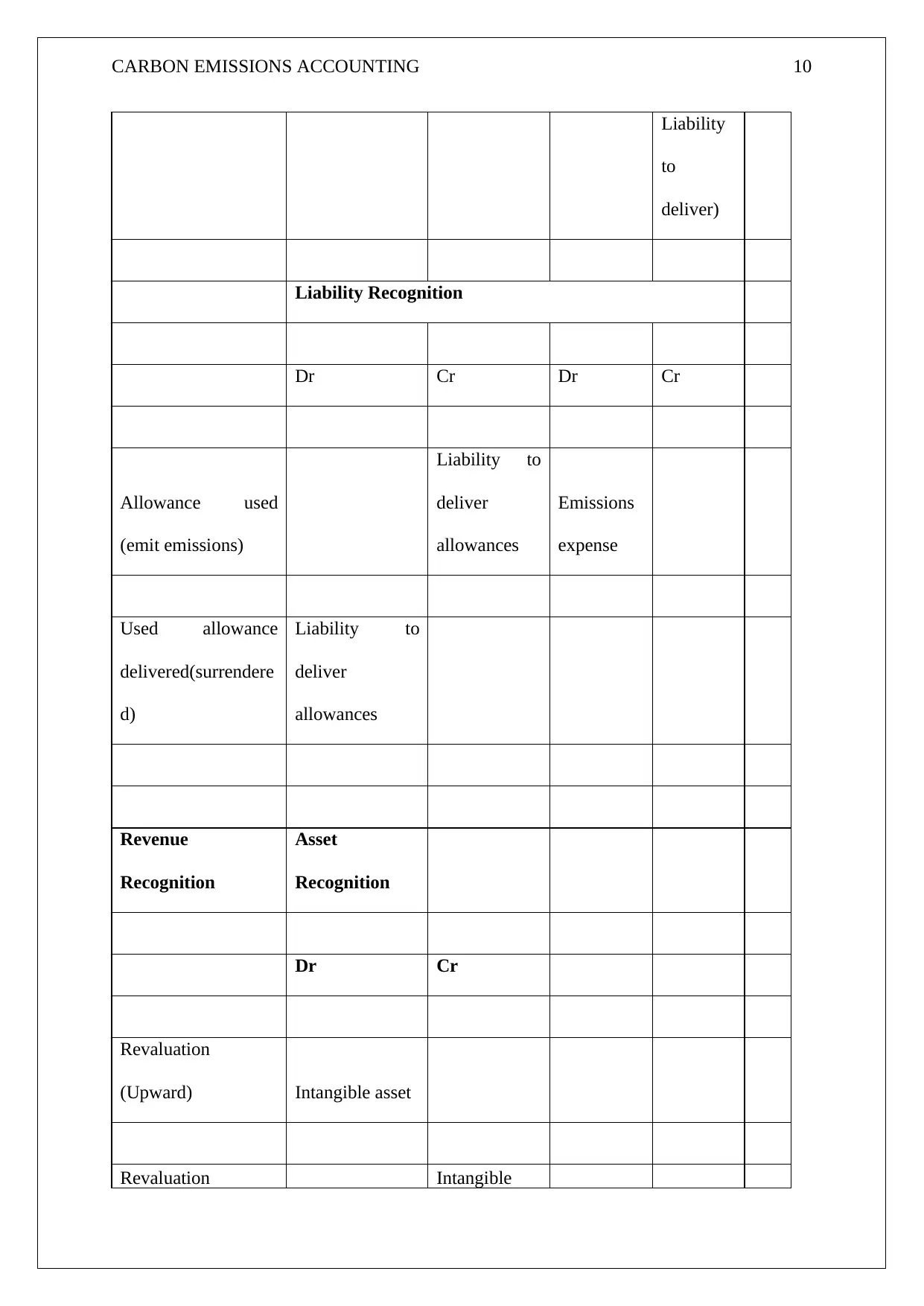

The following are the journal entries of the same:

Cost model Asset Recognition Revenue Recognition

Stage Dr Cr Dr Cr

Receipt of free

allowance Intangible asset

Government

grant

(deferred

income)

Purchase of

allowance Intangible asset

Cash/

Accounts

Payable

Allowance used

(emit emissions)

Governme

nt grant

(deferred

income) Income

Used allowance

delivered(surrendere

d)

Intangible

asset

Loss (Diff

between

Allowance

& Liability

to deliver)

Profit

(Diff

between

Allowanc

e &

The following are the journal entries of the same:

Cost model Asset Recognition Revenue Recognition

Stage Dr Cr Dr Cr

Receipt of free

allowance Intangible asset

Government

grant

(deferred

income)

Purchase of

allowance Intangible asset

Cash/

Accounts

Payable

Allowance used

(emit emissions)

Governme

nt grant

(deferred

income) Income

Used allowance

delivered(surrendere

d)

Intangible

asset

Loss (Diff

between

Allowance

& Liability

to deliver)

Profit

(Diff

between

Allowanc

e &

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CARBON EMISSIONS ACCOUNTING 10

Liability

to

deliver)

Liability Recognition

Dr Cr Dr Cr

Allowance used

(emit emissions)

Liability to

deliver

allowances

Emissions

expense

Used allowance

delivered(surrendere

d)

Liability to

deliver

allowances

Revenue

Recognition

Asset

Recognition

Dr Cr

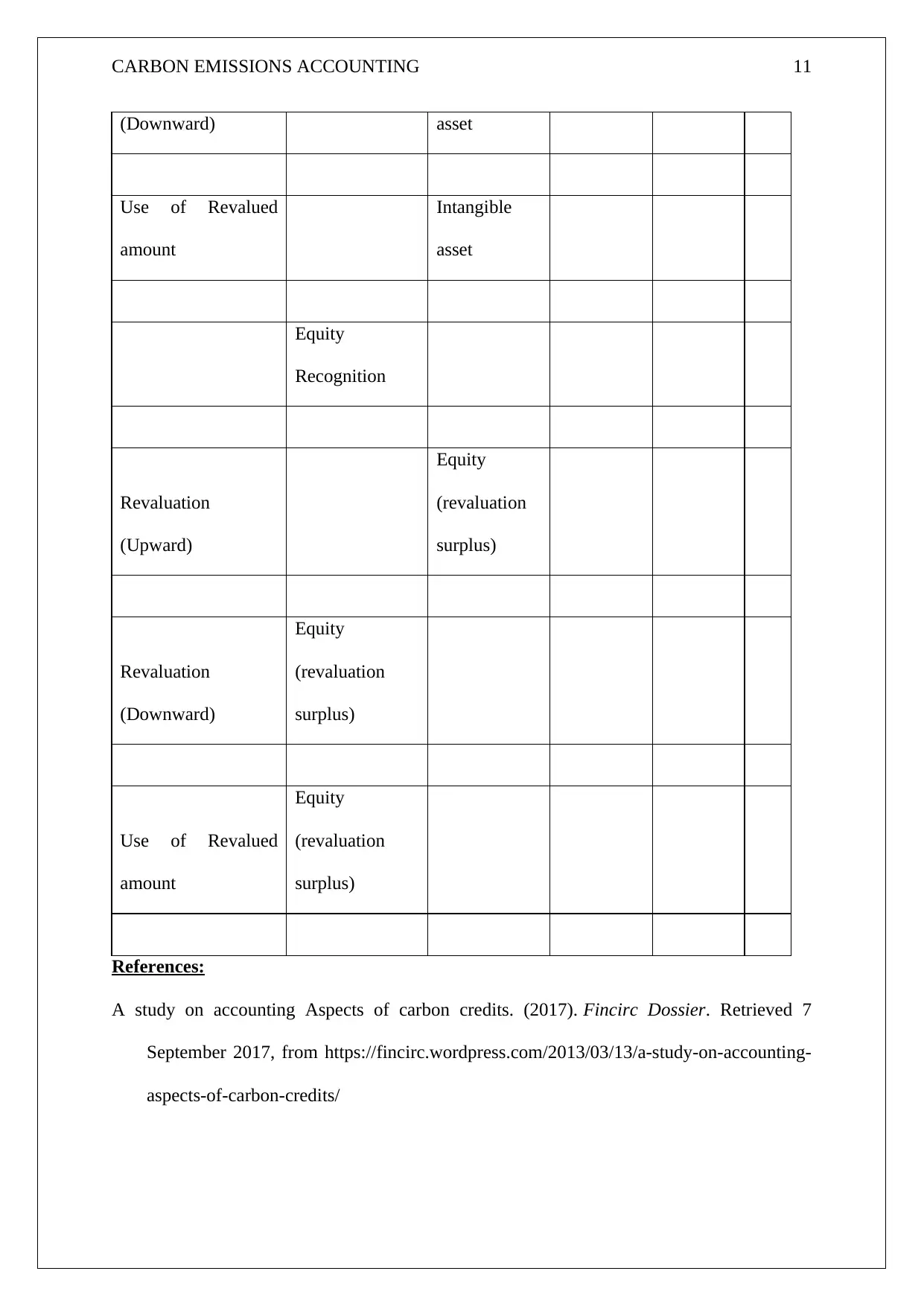

Revaluation

(Upward) Intangible asset

Revaluation Intangible

Liability

to

deliver)

Liability Recognition

Dr Cr Dr Cr

Allowance used

(emit emissions)

Liability to

deliver

allowances

Emissions

expense

Used allowance

delivered(surrendere

d)

Liability to

deliver

allowances

Revenue

Recognition

Asset

Recognition

Dr Cr

Revaluation

(Upward) Intangible asset

Revaluation Intangible

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CARBON EMISSIONS ACCOUNTING 11

(Downward) asset

Use of Revalued

amount

Intangible

asset

Equity

Recognition

Revaluation

(Upward)

Equity

(revaluation

surplus)

Revaluation

(Downward)

Equity

(revaluation

surplus)

Use of Revalued

amount

Equity

(revaluation

surplus)

References:

A study on accounting Aspects of carbon credits. (2017). Fincirc Dossier. Retrieved 7

September 2017, from https://fincirc.wordpress.com/2013/03/13/a-study-on-accounting-

aspects-of-carbon-credits/

(Downward) asset

Use of Revalued

amount

Intangible

asset

Equity

Recognition

Revaluation

(Upward)

Equity

(revaluation

surplus)

Revaluation

(Downward)

Equity

(revaluation

surplus)

Use of Revalued

amount

Equity

(revaluation

surplus)

References:

A study on accounting Aspects of carbon credits. (2017). Fincirc Dossier. Retrieved 7

September 2017, from https://fincirc.wordpress.com/2013/03/13/a-study-on-accounting-

aspects-of-carbon-credits/

CARBON EMISSIONS ACCOUNTING 12

Accounting for Carbon. (2017). www.accaglobal.com. Retrieved 7 September 2017, from

http://www.accaglobal.com/content/dam/acca/global/PDF-technical/climate-change/rr-

122-001.pdf

Accounting for carbon credits. (2017). The Hindu Business Line. Retrieved 7 September

2017, from http://www.thehindubusinessline.com/todays-paper/tp-opinion/accounting-

for-carbon-credits/article1057460.ece

Accounting guidance for emissions programs. (2017). Ey.com. Retrieved 7 September 2017,

from http://www.ey.com/us/en/industries/oil---gas/carbon-market-readiness---4---

accounting-guidance-for-emissions-programs

Carbon accounting – Effects on financial reporting. (2017). www.eurelectric.org. Retrieved 7

September 2017, from

http://www.eurelectric.org/media/71686/carbon_accounting_effects_-_final-2013-540-

0001-01-e.pdf

Carbon Credit Accounting. (2017). www.pbr.co.in. Retrieved 7 September 2017, from

http://www.pbr.co.in/September2015/15.pdf

Accounting for Emissions Trading: How Allowances Appear on Financial Statements Could

Influence the Effectiveness of Programs to Curb Pollution.

(2017). Lawdigitalcommons.bc.edu. Retrieved 9 September 2017, from

http://lawdigitalcommons.bc.edu/cgi/viewcontent.cgi?article=2084&context=ealr

Legal nature of emission allowances. (2017). Emissions-euets.com. Retrieved 7 September

2017, from https://www.emissions-euets.com/carbon-market-glossary/968-legal-nature-

of-emission-allowances

Accounting for Carbon. (2017). www.accaglobal.com. Retrieved 7 September 2017, from

http://www.accaglobal.com/content/dam/acca/global/PDF-technical/climate-change/rr-

122-001.pdf

Accounting for carbon credits. (2017). The Hindu Business Line. Retrieved 7 September

2017, from http://www.thehindubusinessline.com/todays-paper/tp-opinion/accounting-

for-carbon-credits/article1057460.ece

Accounting guidance for emissions programs. (2017). Ey.com. Retrieved 7 September 2017,

from http://www.ey.com/us/en/industries/oil---gas/carbon-market-readiness---4---

accounting-guidance-for-emissions-programs

Carbon accounting – Effects on financial reporting. (2017). www.eurelectric.org. Retrieved 7

September 2017, from

http://www.eurelectric.org/media/71686/carbon_accounting_effects_-_final-2013-540-

0001-01-e.pdf

Carbon Credit Accounting. (2017). www.pbr.co.in. Retrieved 7 September 2017, from

http://www.pbr.co.in/September2015/15.pdf

Accounting for Emissions Trading: How Allowances Appear on Financial Statements Could

Influence the Effectiveness of Programs to Curb Pollution.

(2017). Lawdigitalcommons.bc.edu. Retrieved 9 September 2017, from

http://lawdigitalcommons.bc.edu/cgi/viewcontent.cgi?article=2084&context=ealr

Legal nature of emission allowances. (2017). Emissions-euets.com. Retrieved 7 September

2017, from https://www.emissions-euets.com/carbon-market-glossary/968-legal-nature-

of-emission-allowances

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.