The Technology-Driven Shift in Card-Based Payments and Bank Accounts

VerifiedAdded on 2022/07/04

|14

|4805

|61

Report

AI Summary

This report examines the significant technology-driven transformation in card-based payments and bank accounts, highlighting the shift towards digital banking and smart payment systems. It explores the impact of mobile applications, contactless payments, and digital wallets on consumer behavior and financial efficiency. The report delves into technological disruptions, regulatory outcomes, and the advantages and challenges of contactless payments. It further analyzes the role of competition, the impact of the COVID-19 pandemic on digital banking, and the rise of fraud and cyber-security concerns. The analysis also includes insights into the global cashless payment trends, the evolution of payment systems, and the emergence of new payment models like buy-now-pay-later and cryptocurrencies, providing a comprehensive overview of the evolving financial landscape.

The technology-based shift in card-based payments and bank accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

With the immediate evolution of digital banking, the consumer is finding it more efficient for managing

their overall finance via online platforms. It is observed that people are now easily applying for loans,

opening new accounts and also investing in financial markets as it becomes simple and takes less time.

According to Wang v Ouyang (2019)1, previously people had to invest lots of time to conduct such

processes but because of digital marketing, it has become easy for them. Moreover, the mobile

application is allowing the consumer to implement a wide range of tasks with just some taps on their

mobile phones and therefore, creating an enjoyable as well as user-friendly experience for them.

Smart payments

In today’s era, technology is increasing at a very rapid pace, but a very drastic change in the payments

system. Smart payment is all one payment which reduces the friction during checkout, all apps are

provided in one where an individual can access the apps and pay to the different vendors these online

payments become a helping hand for the local business which plays an integral part in boosting the scale

of business as it saves them time and cost which is there if one uses the old conventional

method .however the rapid evolution of smart payment system has radically affected the need if having

payments card and even bank accounts (Zsarnoczky, 2018). 2These include debit cards, credit cards,

electronic fund transfer, direct cards, directs debt and e-commerce payment system payments should be

physical or electronic but each has its protocols and process. A different version of apps are available for

Android, iOS, smartphones depending on the system one can install and recommends version and easily

enjoy the process online payments system which surely curbing rye users to go to the bank and use their

facilities for the various purposes

Technological disruption and efficiency

The economy is the backbone of every country and to make it alive or to sustain the different aspects like

money laundering, parallel economy banks play many roles. “The core one consists of maturity

transformation and liquidity provision taking deposits” from the public to make them long term. The

information is preceded by the customers as borrowers and depositors are very sensitive, conventional

secretive (Moniruzzaman v Khezr, 20203). The electronic revolution has largely boosted the weightage of

modifiable communication and means which boost this is Artificial Intelligence Machine learning. Then

the system is more related to data such as payments, and transaction services will be more affected.

Digital disruption in the finance side is propelled by both supply and technological advancement. The

consumer expectation toward the usage of facilities has changed from the technological viewpoint the

1 Wang, S., Ouyang, L., Yuan, Y., Ni, X., Han, X. and Wang, F.Y., 2019. Blockchain-enabled smart contracts: architecture, applications, and future

trends. IEEE Transactions on Systems, Man, and Cybernetics: Systems, 49(11), pp.2266-2277.

2 Zsarnoczky, M., 2018. The digital future of the tourism & hospitality industry. Boston Hospitality Review, 6, pp.1-9.

3 Moniruzzaman, M., Khezr, S., Yassine, A. and Benlamri, R., 2020. Blockchain for smart homes: Review of current trends and research

challenges. Computers & Electrical Engineering, 83, p.106585.

1

With the immediate evolution of digital banking, the consumer is finding it more efficient for managing

their overall finance via online platforms. It is observed that people are now easily applying for loans,

opening new accounts and also investing in financial markets as it becomes simple and takes less time.

According to Wang v Ouyang (2019)1, previously people had to invest lots of time to conduct such

processes but because of digital marketing, it has become easy for them. Moreover, the mobile

application is allowing the consumer to implement a wide range of tasks with just some taps on their

mobile phones and therefore, creating an enjoyable as well as user-friendly experience for them.

Smart payments

In today’s era, technology is increasing at a very rapid pace, but a very drastic change in the payments

system. Smart payment is all one payment which reduces the friction during checkout, all apps are

provided in one where an individual can access the apps and pay to the different vendors these online

payments become a helping hand for the local business which plays an integral part in boosting the scale

of business as it saves them time and cost which is there if one uses the old conventional

method .however the rapid evolution of smart payment system has radically affected the need if having

payments card and even bank accounts (Zsarnoczky, 2018). 2These include debit cards, credit cards,

electronic fund transfer, direct cards, directs debt and e-commerce payment system payments should be

physical or electronic but each has its protocols and process. A different version of apps are available for

Android, iOS, smartphones depending on the system one can install and recommends version and easily

enjoy the process online payments system which surely curbing rye users to go to the bank and use their

facilities for the various purposes

Technological disruption and efficiency

The economy is the backbone of every country and to make it alive or to sustain the different aspects like

money laundering, parallel economy banks play many roles. “The core one consists of maturity

transformation and liquidity provision taking deposits” from the public to make them long term. The

information is preceded by the customers as borrowers and depositors are very sensitive, conventional

secretive (Moniruzzaman v Khezr, 20203). The electronic revolution has largely boosted the weightage of

modifiable communication and means which boost this is Artificial Intelligence Machine learning. Then

the system is more related to data such as payments, and transaction services will be more affected.

Digital disruption in the finance side is propelled by both supply and technological advancement. The

consumer expectation toward the usage of facilities has changed from the technological viewpoint the

1 Wang, S., Ouyang, L., Yuan, Y., Ni, X., Han, X. and Wang, F.Y., 2019. Blockchain-enabled smart contracts: architecture, applications, and future

trends. IEEE Transactions on Systems, Man, and Cybernetics: Systems, 49(11), pp.2266-2277.

2 Zsarnoczky, M., 2018. The digital future of the tourism & hospitality industry. Boston Hospitality Review, 6, pp.1-9.

3 Moniruzzaman, M., Khezr, S., Yassine, A. and Benlamri, R., 2020. Blockchain for smart homes: Review of current trends and research

challenges. Computers & Electrical Engineering, 83, p.106585.

1

“relevant factors are application programming interfaces, cloud computing, smartphones, digital

currencies and blockchain technology” (Hartawan v Putra, 20204).

Mobile phones become the second hand in the daily activities of the consumers as they provide financial

assistance to the users through different apps some are encouraging advice and others are helping in

regulating money transactions there are apps like money control that can supervise the finances of users.

The 3rd Party designers capture the customer interface and provide various functions like payments,

money transfers, online shopping (Zheng v Sang, 20185). Digital wallets become very popular among the

users as it is convenient and time friendly even though the old conventional system like visa master card

is still leading the market for the transaction it has been seen in western countries like Africa, Asia where

people at more likely to engaged with the online payment system rather having regular bank accounts

Traditional system

The digital currencies have deteriorated the old traditional system the traditional system of money has

advantages as it has proper a tire value unit of account many examples of digit currency like Alipay, wet

play in China as it is not awful to sit that ancestral payment system is better because Ut curbs the danger

of hacking controlling all the money (Karim v Haque, 20206). In the world of digitalization, some ample

hackers can hack the data and convert consumers' money into their accounts whereas the banking

payment system provides the full surety of confined information.

Competition and the role of regulations

What are the regulatory outcomes of digital disruption? “How should BigTech and FinTech firms be

regulated”? Guideline will impact the sort of contest among occupants and contestants. The primary issue

is whether guideline ought to focus on a level battleground or whether it ought to incline toward

contestants to work with rivalry.

The 2007–2009 financial crises have given rise to new approaches concerning competition in the

financial services sector. “A case in point is the 2015 UK reform in which the FCA gained concurrent

powers for enforcement of competition policy” (Singh v Miah, 2020) . 71 Supervisory authority of several

countries now holds some contest-associated powers. Synchronous abilities among bosses and

competition specialists introduce some complicatedness, yet it is positive that customer and financial

backer assurance in the monetary area are under a similar rooftop as rivalry, since purchaser

4 Hartawan, M.S., Putra, A.S. and Muktiono, A., 2020. Smart City Concept for Integrated Citizen Information Smart Card or ICISC in DKI

Jakarta. International Journal of Science, Technology & Management, 1(4), pp.364-370.

5 Zheng, P., Sang, Z., Zhong, R.Y., Liu, Y., Liu, C., Mubarok, K., Yu, S. and Xu, X., 2018. Smart manufacturing systems for Industry 4.0: Conceptual

framework, scenarios, and future perspectives. Frontiers of Mechanical Engineering, 13(2), pp.137-150.

6 Karim, M.W., Haque, A., Ulfy, M.A., Hossain, M.A. and Anis, M.Z., 2020. Factors influencing the use of E-wallet as a payment method among Malaysian

young adults. Journal of International Business and Management, 3(2), pp.01-12.

7 Singh, H. and Miah, S.J., 2020. Smart education literature: A theoretical analysis. Education and Information Technologies, 25(4), pp.3299-3328.

2

currencies and blockchain technology” (Hartawan v Putra, 20204).

Mobile phones become the second hand in the daily activities of the consumers as they provide financial

assistance to the users through different apps some are encouraging advice and others are helping in

regulating money transactions there are apps like money control that can supervise the finances of users.

The 3rd Party designers capture the customer interface and provide various functions like payments,

money transfers, online shopping (Zheng v Sang, 20185). Digital wallets become very popular among the

users as it is convenient and time friendly even though the old conventional system like visa master card

is still leading the market for the transaction it has been seen in western countries like Africa, Asia where

people at more likely to engaged with the online payment system rather having regular bank accounts

Traditional system

The digital currencies have deteriorated the old traditional system the traditional system of money has

advantages as it has proper a tire value unit of account many examples of digit currency like Alipay, wet

play in China as it is not awful to sit that ancestral payment system is better because Ut curbs the danger

of hacking controlling all the money (Karim v Haque, 20206). In the world of digitalization, some ample

hackers can hack the data and convert consumers' money into their accounts whereas the banking

payment system provides the full surety of confined information.

Competition and the role of regulations

What are the regulatory outcomes of digital disruption? “How should BigTech and FinTech firms be

regulated”? Guideline will impact the sort of contest among occupants and contestants. The primary issue

is whether guideline ought to focus on a level battleground or whether it ought to incline toward

contestants to work with rivalry.

The 2007–2009 financial crises have given rise to new approaches concerning competition in the

financial services sector. “A case in point is the 2015 UK reform in which the FCA gained concurrent

powers for enforcement of competition policy” (Singh v Miah, 2020) . 71 Supervisory authority of several

countries now holds some contest-associated powers. Synchronous abilities among bosses and

competition specialists introduce some complicatedness, yet it is positive that customer and financial

backer assurance in the monetary area are under a similar rooftop as rivalry, since purchaser

4 Hartawan, M.S., Putra, A.S. and Muktiono, A., 2020. Smart City Concept for Integrated Citizen Information Smart Card or ICISC in DKI

Jakarta. International Journal of Science, Technology & Management, 1(4), pp.364-370.

5 Zheng, P., Sang, Z., Zhong, R.Y., Liu, Y., Liu, C., Mubarok, K., Yu, S. and Xu, X., 2018. Smart manufacturing systems for Industry 4.0: Conceptual

framework, scenarios, and future perspectives. Frontiers of Mechanical Engineering, 13(2), pp.137-150.

6 Karim, M.W., Haque, A., Ulfy, M.A., Hossain, M.A. and Anis, M.Z., 2020. Factors influencing the use of E-wallet as a payment method among Malaysian

young adults. Journal of International Business and Management, 3(2), pp.01-12.

7 Singh, H. and Miah, S.J., 2020. Smart education literature: A theoretical analysis. Education and Information Technologies, 25(4), pp.3299-3328.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages of contactless payments

Easy to use - People always have hassle in punching their pin however contactless payments can

make the quicker transaction Safer technology- Tap to pay method of payment are far better than the other mode of payment

system The flexibility of the payment system – Unlike the banking system e payment are available 24/7 a

person can use the facilities any time with the easily accessible norms which are not present in the

traditional payments system

Challenges of contactless payment Limited acceptance –retailers and consumers who are not technology friendly can find it

difficult. Consumers will always be disappointed by the spotty coverage

Technical limitations- customers can face some problems because of technical glitches

such as hacking, no user-friendly apps and much more

Limited international availability- mobile contactless payment may not work

internationally. As there are some app which doesn’t support the online transaction

Critical analysis

The shift towards the digital realm has been accelerated due to the covid-19 pandemic. With lockdown

restrictions holding the typical bank-office development back from happening, and with social-isolating

measures further diminishing the open doors for in-person commitment, virtually all parts of the world

has seen the utilization of the web and portable “financial administrations soar since the beginning of the

infection toward the finish of the principal quarter” (Luna v Liebana, 20198). COVID-19, for example,

has "massively affected" advanced bank, with the end goal also that specialist has predicted that its whole

market would grow at a CAGR (compound annual growth rate) of 10% somewhere between 2019 and

2026, resulting in a pay of $1,702.4 million.

The research represents how vulnerable banks did become. A review distributed in January 2020 from

investigation firm FICO, for example, found that just about four of every five Asia-Pacific banks (78%)

accepted the presentation of constant instalment stages like P2P (shared) moves and portable instalments

had brought about expanded extortion misfortunes. Right around a quarter (22 per cent) said that they

anticipated misrepresentation to rise fundamentally over the accompanying year, while an extra 58 per

cent anticipated a moderate ascent in extortion (Wenner v Bram, 20189). "While the comfort of

8 Wenner, G., Bram, J.T., Marino, M., Obeysekare, E. and Mehta, K., 2018. Organizational models of mobile payment systems in low-resource

environments. Information Technology for Development, 24(4), pp.681-705.

9 de Luna, I.R., Liébana-Cabanillas, F., Sánchez-Fernández, J. and Muñoz-Leiva, F., 2019. Mobile payment is not all the same: The adoption of mobile

payment systems depending on the technology applied. Technological Forecasting and Social Change, 146, pp.931-944.

3

Easy to use - People always have hassle in punching their pin however contactless payments can

make the quicker transaction Safer technology- Tap to pay method of payment are far better than the other mode of payment

system The flexibility of the payment system – Unlike the banking system e payment are available 24/7 a

person can use the facilities any time with the easily accessible norms which are not present in the

traditional payments system

Challenges of contactless payment Limited acceptance –retailers and consumers who are not technology friendly can find it

difficult. Consumers will always be disappointed by the spotty coverage

Technical limitations- customers can face some problems because of technical glitches

such as hacking, no user-friendly apps and much more

Limited international availability- mobile contactless payment may not work

internationally. As there are some app which doesn’t support the online transaction

Critical analysis

The shift towards the digital realm has been accelerated due to the covid-19 pandemic. With lockdown

restrictions holding the typical bank-office development back from happening, and with social-isolating

measures further diminishing the open doors for in-person commitment, virtually all parts of the world

has seen the utilization of the web and portable “financial administrations soar since the beginning of the

infection toward the finish of the principal quarter” (Luna v Liebana, 20198). COVID-19, for example,

has "massively affected" advanced bank, with the end goal also that specialist has predicted that its whole

market would grow at a CAGR (compound annual growth rate) of 10% somewhere between 2019 and

2026, resulting in a pay of $1,702.4 million.

The research represents how vulnerable banks did become. A review distributed in January 2020 from

investigation firm FICO, for example, found that just about four of every five Asia-Pacific banks (78%)

accepted the presentation of constant instalment stages like P2P (shared) moves and portable instalments

had brought about expanded extortion misfortunes. Right around a quarter (22 per cent) said that they

anticipated misrepresentation to rise fundamentally over the accompanying year, while an extra 58 per

cent anticipated a moderate ascent in extortion (Wenner v Bram, 20189). "While the comfort of

8 Wenner, G., Bram, J.T., Marino, M., Obeysekare, E. and Mehta, K., 2018. Organizational models of mobile payment systems in low-resource

environments. Information Technology for Development, 24(4), pp.681-705.

9 de Luna, I.R., Liébana-Cabanillas, F., Sánchez-Fernández, J. and Muñoz-Leiva, F., 2019. Mobile payment is not all the same: The adoption of mobile

payment systems depending on the technology applied. Technological Forecasting and Social Change, 146, pp.931-944.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

continuous instalments is incredible information for clients, progressively, banks have no opportunity to

clear an exchange or instalment. Simulated intelligence can't dial back the clock, however, it can assist

with making frameworks that are fundamentally speedier to perceive an exchange that smells prone to be

deceitful," said Dan McConaghy, leader of FICO in Asia-Pacific. "Banks should move past passwords

and OTPs [one-time passwords] and add biometrics; gadget telemetry and client conduct investigation to

stay aware of the changing instalments scene."

As indicated by the “Consumer Sentinel Network”, which is completely maintained by the US purchaser

security body “the Federal Trade Commission (FTC), there were 3.2 million” buyer extortion and fraud

protests documented in 2019, either with government, state or nearby regulation authorization offices or

secretly (Lara v Villarejo, 202110). Of those filings, a powerful 651,000 were protests connected with

fraud, with Mastercard extortion the absolute most announced wholesale fraud grievance. Also, with

online retail turning out to be more essential to customers as time passes, those possessing taken Visa data

can purchase products over the web substantially more effectively than they would genuinely figure out

how to do in a shop.

Ought to digital aggressors have the option to hack into a bank's advanced foundation, data fraud turns

into a significant gamble for clients that is difficult to disregard. What's more, in later times, account

takeovers have become particularly famous (Dastan v Gurler, 201611). A sort of fraud, this digital danger

implies a terrible outsider accessing a client's record from which the lawbreaker can change the record

subtleties by acting as the client. With all resulting updates to the record being redirected to the crook's

contact address, the client is regularly unaware of the assault until it is past the point of no return.

Navigating the payments matrix

According to a research study, it was observed that near about 42% of the total population has increased

towards global cashless payment volumes. It is the main reason why 86% of the total population have

agreed that traditional payments providers would collaborate with fintech as well as technology givers as

their key innovation sources (Aydin v Burnaz, 201612). Based on the analysis, it is confirmed that 89% of

people have agreed that there will be an increase in the e-commerce site soon. Moreover, 42% of the total

population have strongly felt that there will be an inclination toward B2B, cross-currency and cross-

border payments in near future. As per the analysis, it is seen that over the next five years some areas

would be highly impacted by these regulatory changes.

10 Liébana-Cabanillas, F., Sánchez-Fernández, J. and Muñoz-Leiva, F., 2014. Antecedents of the adoption of the new mobile payment

systems: The moderating effect of age. Computers in Human Behavior, 35, pp.464-478.

11 Daştan, İ. and Gürler, C., 2016. Factors affecting the adoption of mobile payment systems: An empirical analysis. EMAJ: Emerging

Markets Journal, 6(1), pp.17-24.

12 Aydin, G. and Burnaz, S., 2016. Adoption of mobile payment systems: A study on mobile wallets. Journal of Business Economics and

Finance, 5(1), pp.73-92.

4

clear an exchange or instalment. Simulated intelligence can't dial back the clock, however, it can assist

with making frameworks that are fundamentally speedier to perceive an exchange that smells prone to be

deceitful," said Dan McConaghy, leader of FICO in Asia-Pacific. "Banks should move past passwords

and OTPs [one-time passwords] and add biometrics; gadget telemetry and client conduct investigation to

stay aware of the changing instalments scene."

As indicated by the “Consumer Sentinel Network”, which is completely maintained by the US purchaser

security body “the Federal Trade Commission (FTC), there were 3.2 million” buyer extortion and fraud

protests documented in 2019, either with government, state or nearby regulation authorization offices or

secretly (Lara v Villarejo, 202110). Of those filings, a powerful 651,000 were protests connected with

fraud, with Mastercard extortion the absolute most announced wholesale fraud grievance. Also, with

online retail turning out to be more essential to customers as time passes, those possessing taken Visa data

can purchase products over the web substantially more effectively than they would genuinely figure out

how to do in a shop.

Ought to digital aggressors have the option to hack into a bank's advanced foundation, data fraud turns

into a significant gamble for clients that is difficult to disregard. What's more, in later times, account

takeovers have become particularly famous (Dastan v Gurler, 201611). A sort of fraud, this digital danger

implies a terrible outsider accessing a client's record from which the lawbreaker can change the record

subtleties by acting as the client. With all resulting updates to the record being redirected to the crook's

contact address, the client is regularly unaware of the assault until it is past the point of no return.

Navigating the payments matrix

According to a research study, it was observed that near about 42% of the total population has increased

towards global cashless payment volumes. It is the main reason why 86% of the total population have

agreed that traditional payments providers would collaborate with fintech as well as technology givers as

their key innovation sources (Aydin v Burnaz, 201612). Based on the analysis, it is confirmed that 89% of

people have agreed that there will be an increase in the e-commerce site soon. Moreover, 42% of the total

population have strongly felt that there will be an inclination toward B2B, cross-currency and cross-

border payments in near future. As per the analysis, it is seen that over the next five years some areas

would be highly impacted by these regulatory changes.

10 Liébana-Cabanillas, F., Sánchez-Fernández, J. and Muñoz-Leiva, F., 2014. Antecedents of the adoption of the new mobile payment

systems: The moderating effect of age. Computers in Human Behavior, 35, pp.464-478.

11 Daştan, İ. and Gürler, C., 2016. Factors affecting the adoption of mobile payment systems: An empirical analysis. EMAJ: Emerging

Markets Journal, 6(1), pp.17-24.

12 Aydin, G. and Burnaz, S., 2016. Adoption of mobile payment systems: A study on mobile wallets. Journal of Business Economics and

Finance, 5(1), pp.73-92.

4

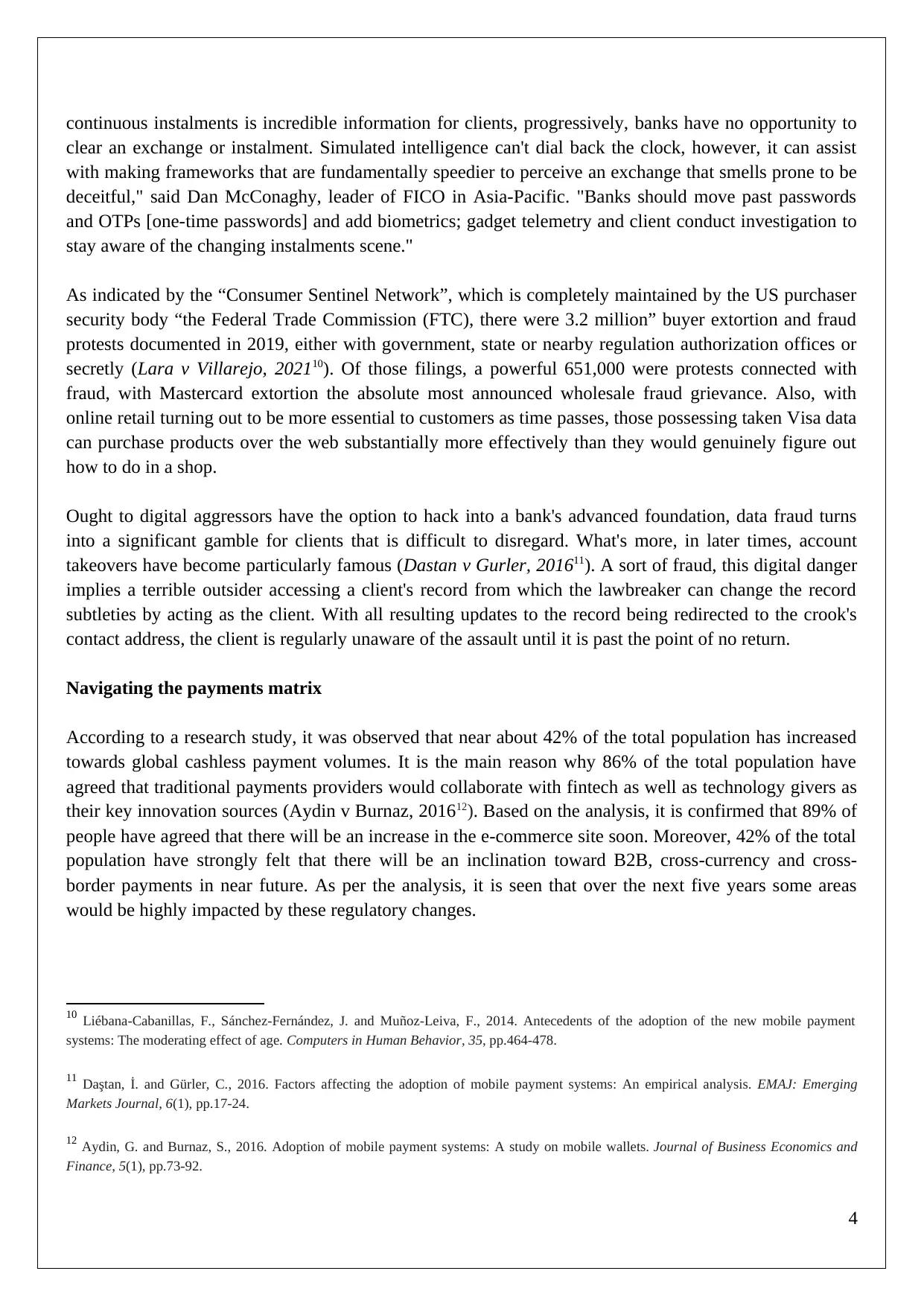

Particulars Percentage

1 Data privacy and cyber-security 48%

2 Digital identity authentication 31%

3 Use of new technology 30%

4 Local regulatory pressures – different regulations in different regions 30%

5 Environment and climate (ESG) 28%

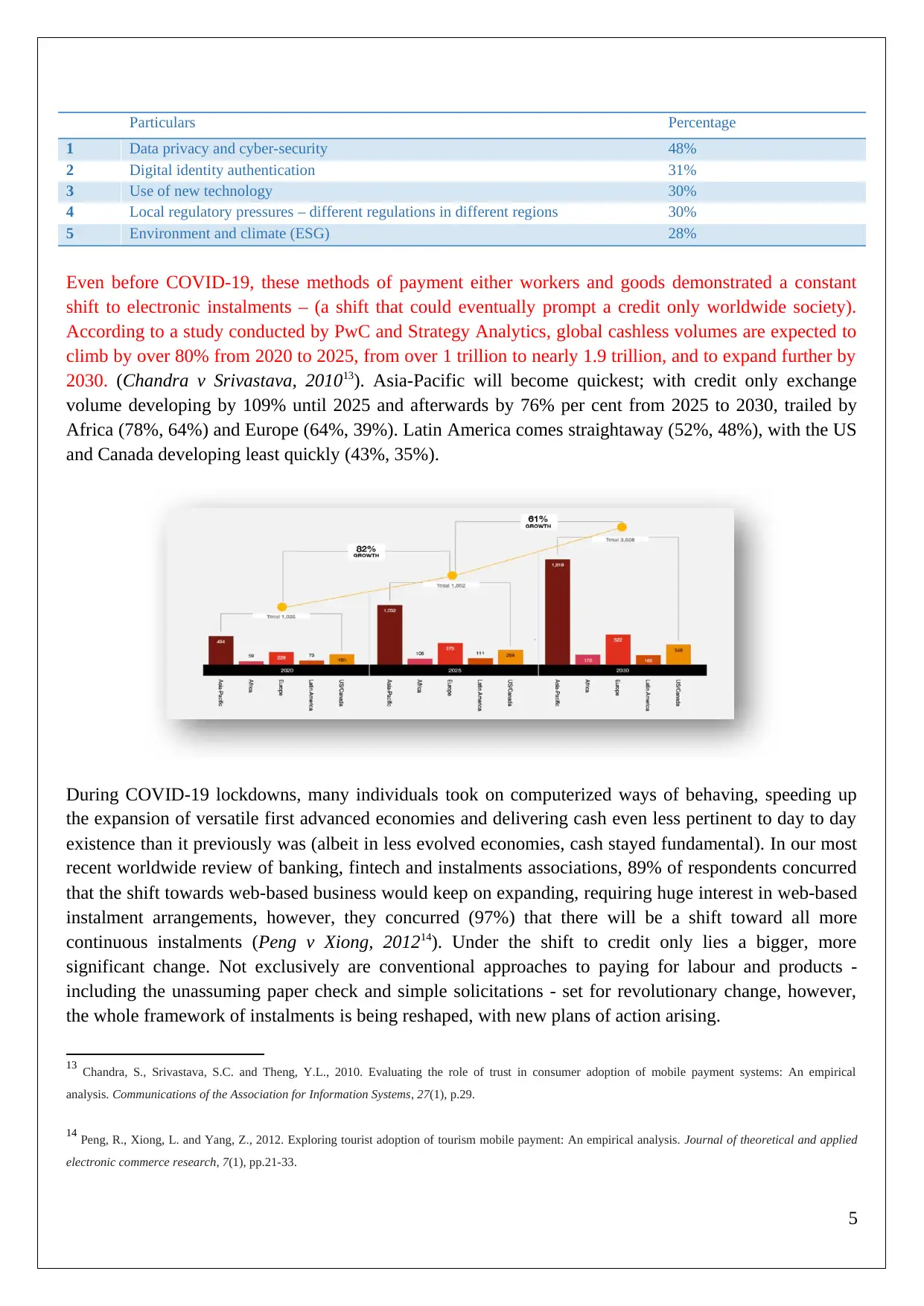

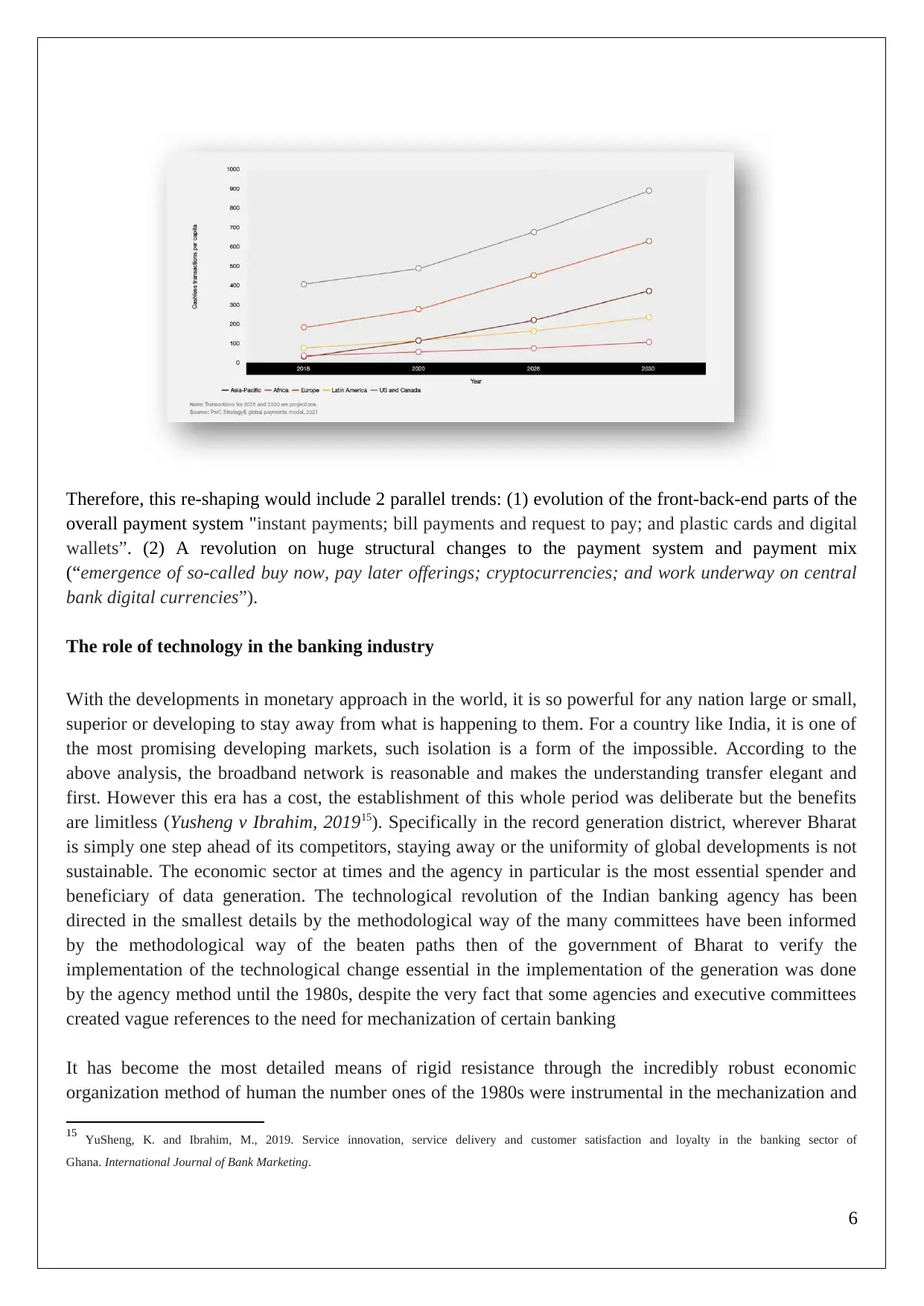

Even before COVID-19, these methods of payment either workers and goods demonstrated a constant

shift to electronic instalments – (a shift that could eventually prompt a credit only worldwide society).

According to a study conducted by PwC and Strategy Analytics, global cashless volumes are expected to

climb by over 80% from 2020 to 2025, from over 1 trillion to nearly 1.9 trillion, and to expand further by

2030. (Chandra v Srivastava, 201013). Asia-Pacific will become quickest; with credit only exchange

volume developing by 109% until 2025 and afterwards by 76% per cent from 2025 to 2030, trailed by

Africa (78%, 64%) and Europe (64%, 39%). Latin America comes straightaway (52%, 48%), with the US

and Canada developing least quickly (43%, 35%).

During COVID-19 lockdowns, many individuals took on computerized ways of behaving, speeding up

the expansion of versatile first advanced economies and delivering cash even less pertinent to day to day

existence than it previously was (albeit in less evolved economies, cash stayed fundamental). In our most

recent worldwide review of banking, fintech and instalments associations, 89% of respondents concurred

that the shift towards web-based business would keep on expanding, requiring huge interest in web-based

instalment arrangements, however, they concurred (97%) that there will be a shift toward all more

continuous instalments (Peng v Xiong, 201214). Under the shift to credit only lies a bigger, more

significant change. Not exclusively are conventional approaches to paying for labour and products -

including the unassuming paper check and simple solicitations - set for revolutionary change, however,

the whole framework of instalments is being reshaped, with new plans of action arising.

13 Chandra, S., Srivastava, S.C. and Theng, Y.L., 2010. Evaluating the role of trust in consumer adoption of mobile payment systems: An empirical

analysis. Communications of the Association for Information Systems, 27(1), p.29.

14 Peng, R., Xiong, L. and Yang, Z., 2012. Exploring tourist adoption of tourism mobile payment: An empirical analysis. Journal of theoretical and applied

electronic commerce research, 7(1), pp.21-33.

5

1 Data privacy and cyber-security 48%

2 Digital identity authentication 31%

3 Use of new technology 30%

4 Local regulatory pressures – different regulations in different regions 30%

5 Environment and climate (ESG) 28%

Even before COVID-19, these methods of payment either workers and goods demonstrated a constant

shift to electronic instalments – (a shift that could eventually prompt a credit only worldwide society).

According to a study conducted by PwC and Strategy Analytics, global cashless volumes are expected to

climb by over 80% from 2020 to 2025, from over 1 trillion to nearly 1.9 trillion, and to expand further by

2030. (Chandra v Srivastava, 201013). Asia-Pacific will become quickest; with credit only exchange

volume developing by 109% until 2025 and afterwards by 76% per cent from 2025 to 2030, trailed by

Africa (78%, 64%) and Europe (64%, 39%). Latin America comes straightaway (52%, 48%), with the US

and Canada developing least quickly (43%, 35%).

During COVID-19 lockdowns, many individuals took on computerized ways of behaving, speeding up

the expansion of versatile first advanced economies and delivering cash even less pertinent to day to day

existence than it previously was (albeit in less evolved economies, cash stayed fundamental). In our most

recent worldwide review of banking, fintech and instalments associations, 89% of respondents concurred

that the shift towards web-based business would keep on expanding, requiring huge interest in web-based

instalment arrangements, however, they concurred (97%) that there will be a shift toward all more

continuous instalments (Peng v Xiong, 201214). Under the shift to credit only lies a bigger, more

significant change. Not exclusively are conventional approaches to paying for labour and products -

including the unassuming paper check and simple solicitations - set for revolutionary change, however,

the whole framework of instalments is being reshaped, with new plans of action arising.

13 Chandra, S., Srivastava, S.C. and Theng, Y.L., 2010. Evaluating the role of trust in consumer adoption of mobile payment systems: An empirical

analysis. Communications of the Association for Information Systems, 27(1), p.29.

14 Peng, R., Xiong, L. and Yang, Z., 2012. Exploring tourist adoption of tourism mobile payment: An empirical analysis. Journal of theoretical and applied

electronic commerce research, 7(1), pp.21-33.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, this re-shaping would include 2 parallel trends: (1) evolution of the front-back-end parts of the

overall payment system "instant payments; bill payments and request to pay; and plastic cards and digital

wallets”. (2) A revolution on huge structural changes to the payment system and payment mix

(“emergence of so-called buy now, pay later offerings; cryptocurrencies; and work underway on central

bank digital currencies”).

The role of technology in the banking industry

With the developments in monetary approach in the world, it is so powerful for any nation large or small,

superior or developing to stay away from what is happening to them. For a country like India, it is one of

the most promising developing markets, such isolation is a form of the impossible. According to the

above analysis, the broadband network is reasonable and makes the understanding transfer elegant and

first. However this era has a cost, the establishment of this whole period was deliberate but the benefits

are limitless (Yusheng v Ibrahim, 201915). Specifically in the record generation district, wherever Bharat

is simply one step ahead of its competitors, staying away or the uniformity of global developments is not

sustainable. The economic sector at times and the agency in particular is the most essential spender and

beneficiary of data generation. The technological revolution of the Indian banking agency has been

directed in the smallest details by the methodological way of the many committees have been informed

by the methodological way of the beaten paths then of the government of Bharat to verify the

implementation of the technological change essential in the implementation of the generation was done

by the agency method until the 1980s, despite the very fact that some agencies and executive committees

created vague references to the need for mechanization of certain banking

It has become the most detailed means of rigid resistance through the incredibly robust economic

organization method of human the number ones of the 1980s were instrumental in the mechanization and

15 YuSheng, K. and Ibrahim, M., 2019. Service innovation, service delivery and customer satisfaction and loyalty in the banking sector of

Ghana. International Journal of Bank Marketing.

6

overall payment system "instant payments; bill payments and request to pay; and plastic cards and digital

wallets”. (2) A revolution on huge structural changes to the payment system and payment mix

(“emergence of so-called buy now, pay later offerings; cryptocurrencies; and work underway on central

bank digital currencies”).

The role of technology in the banking industry

With the developments in monetary approach in the world, it is so powerful for any nation large or small,

superior or developing to stay away from what is happening to them. For a country like India, it is one of

the most promising developing markets, such isolation is a form of the impossible. According to the

above analysis, the broadband network is reasonable and makes the understanding transfer elegant and

first. However this era has a cost, the establishment of this whole period was deliberate but the benefits

are limitless (Yusheng v Ibrahim, 201915). Specifically in the record generation district, wherever Bharat

is simply one step ahead of its competitors, staying away or the uniformity of global developments is not

sustainable. The economic sector at times and the agency in particular is the most essential spender and

beneficiary of data generation. The technological revolution of the Indian banking agency has been

directed in the smallest details by the methodological way of the many committees have been informed

by the methodological way of the beaten paths then of the government of Bharat to verify the

implementation of the technological change essential in the implementation of the generation was done

by the agency method until the 1980s, despite the very fact that some agencies and executive committees

created vague references to the need for mechanization of certain banking

It has become the most detailed means of rigid resistance through the incredibly robust economic

organization method of human the number ones of the 1980s were instrumental in the mechanization and

15 YuSheng, K. and Ibrahim, M., 2019. Service innovation, service delivery and customer satisfaction and loyalty in the banking sector of

Ghana. International Journal of Bank Marketing.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

mechanization aspect of Indian banks. Fact generation improved the performance and strength of

commercial agency methods for the length of the banking sector (Dalahmeh v Obeidat, 201816). The

Indian banking sector has made rapid progress in reforming itself in the competitive environment of

fashionable commercial agencies. Indian agency is inside associated computer revolution. Technological

infrastructure has become a necessary area of reform methodology within the banking window, with the

gradual development of responsive gadgets and improved market practices.

E-banking: It lets the financial institution offer its excessive quit customers handy services. With

the usage of Graphical User Interfaces (GUIs), banks have made their structures extra user-

pleasant for all customers, permitting human beings to get admission to their account info on their

personal computers, make bills from one account to another, print financial institution statements

and inquire approximately their economic Banks use a digital record alternate era called

Electronic Data Interchange (EDI) to switch commercial enterprise records among them and their

customers (Ali v Puah, 201817). This software program lets organizations get commercial

enterprise records in a layout that may be studied with the aid of using computers. In this case, the

consumer on the alternative quit can have smooth get admission to the information.

NRI Banking Services: The majority of the nations which have followed this generation are

India, the United States, and the United Arab Emirates. Because many humans relocate overseas

to work, they must guide themselves and their families. They have consequently been capable of

shipping cash to their cherished ones in a less difficult way to generate (Hammoud v Baba,

201818).

RURAL Banking: Unlike withinside the beyond whilst banking become centralized in city areas,

lately in new times it’s easier to establish banks in remote areas. For example: The Africa, they

now have the system of Mobile cash bank. The example talks about the person in the remote area

may have a bank account with a cell organization that is open for free. Where people deposit

money in the account thru a close to with the aid of using a cell cash working center. This cash

may be taken out as per depositor wish at any time and can also ship the money.

Plastic money: Credit card also known as ‘'VISA ELECTRON'' have made the banking system

greater bendy than before. It has a system known as credit score, a client can have access to a

16 YuSheng, K. and Ibrahim, M., 2019. Service innovation, service delivery and customer satisfaction and loyalty in the banking sector of

Ghana. International Journal of Bank Marketing.

17 Ali, M. and Puah, C.H., 2018. The internal determinants of bank profitability and stability: An insight from banking sector of Pakistan. Management

Research Review.

18 Hammoud, J., Bizri, R.M. and El Baba, I., 2018. The impact of e-banking service quality on customer satisfaction: Evidence from the Lebanese banking

sector. Sage Open, 8(3), p.2158244018790633.

7

commercial agency methods for the length of the banking sector (Dalahmeh v Obeidat, 201816). The

Indian banking sector has made rapid progress in reforming itself in the competitive environment of

fashionable commercial agencies. Indian agency is inside associated computer revolution. Technological

infrastructure has become a necessary area of reform methodology within the banking window, with the

gradual development of responsive gadgets and improved market practices.

E-banking: It lets the financial institution offer its excessive quit customers handy services. With

the usage of Graphical User Interfaces (GUIs), banks have made their structures extra user-

pleasant for all customers, permitting human beings to get admission to their account info on their

personal computers, make bills from one account to another, print financial institution statements

and inquire approximately their economic Banks use a digital record alternate era called

Electronic Data Interchange (EDI) to switch commercial enterprise records among them and their

customers (Ali v Puah, 201817). This software program lets organizations get commercial

enterprise records in a layout that may be studied with the aid of using computers. In this case, the

consumer on the alternative quit can have smooth get admission to the information.

NRI Banking Services: The majority of the nations which have followed this generation are

India, the United States, and the United Arab Emirates. Because many humans relocate overseas

to work, they must guide themselves and their families. They have consequently been capable of

shipping cash to their cherished ones in a less difficult way to generate (Hammoud v Baba,

201818).

RURAL Banking: Unlike withinside the beyond whilst banking become centralized in city areas,

lately in new times it’s easier to establish banks in remote areas. For example: The Africa, they

now have the system of Mobile cash bank. The example talks about the person in the remote area

may have a bank account with a cell organization that is open for free. Where people deposit

money in the account thru a close to with the aid of using a cell cash working center. This cash

may be taken out as per depositor wish at any time and can also ship the money.

Plastic money: Credit card also known as ‘'VISA ELECTRON'' have made the banking system

greater bendy than before. It has a system known as credit score, a client can have access to a

16 YuSheng, K. and Ibrahim, M., 2019. Service innovation, service delivery and customer satisfaction and loyalty in the banking sector of

Ghana. International Journal of Bank Marketing.

17 Ali, M. and Puah, C.H., 2018. The internal determinants of bank profitability and stability: An insight from banking sector of Pakistan. Management

Research Review.

18 Hammoud, J., Bizri, R.M. and El Baba, I., 2018. The impact of e-banking service quality on customer satisfaction: Evidence from the Lebanese banking

sector. Sage Open, 8(3), p.2158244018790633.

7

particular amount of cash from the bank to buy any element and then pay the amount at later

stage. In this case, they mustn't undergo the trouble of taking little money. Then with ''Smart

Cards'' also called visa electron, a customer can use that account to purchase for anything, and the

money is deposited directly from their bank debts; they can also use the same card to withdraw or

transfer money from their bank debts using an ATM.

Legal framework for oversight

According to the RBI, the payment and settlement Act (PSS Act) 2007 is unique and give the body the

right to modification and supervision of the payment system within the nation. The body carries out its

powers and perform the skills and showcase the obligation given to it less than the PSS act under the

"Board for Regulation and Supervision of Payment and Settlement Systems (BPSS)". It exerts its power

on the prescribed necessarily as suggested by the banks. For the transfer of the devices that encompasses

the cheques and have strong message delivery that stands from inside the SFMS (Structured Financial

Messaging System).

According to 'chapter III of the PSS acts, it says that "no legal entity aside from RBI will begin or

otherwise carry out a fee device exception beneath and by an authorization issued through manner of way

of the Reserve Bank beneath the provisions of this Act". It's very smooth that how every fee system

operational in India concerning fee duties due to reimbursement or payment of more than one type of fee

directives regarding securities, funds, or derivatives or foreign exchange or extraordinary transactions

need to have approval in the manner that RBI suggests. PSS Act moreover gives controls to banks to

problem authorization for strolling system of fee, and to change the authorization agreed by device

benefactors in case of infringements of any provisions of PSS Act, PSS Regulations, 2008, orders or

commands issued through a manner that RBI suggests for the operation of fee device is conflicting to the

conditions & terms scenario to which the authorization became allotted.

8

stage. In this case, they mustn't undergo the trouble of taking little money. Then with ''Smart

Cards'' also called visa electron, a customer can use that account to purchase for anything, and the

money is deposited directly from their bank debts; they can also use the same card to withdraw or

transfer money from their bank debts using an ATM.

Legal framework for oversight

According to the RBI, the payment and settlement Act (PSS Act) 2007 is unique and give the body the

right to modification and supervision of the payment system within the nation. The body carries out its

powers and perform the skills and showcase the obligation given to it less than the PSS act under the

"Board for Regulation and Supervision of Payment and Settlement Systems (BPSS)". It exerts its power

on the prescribed necessarily as suggested by the banks. For the transfer of the devices that encompasses

the cheques and have strong message delivery that stands from inside the SFMS (Structured Financial

Messaging System).

According to 'chapter III of the PSS acts, it says that "no legal entity aside from RBI will begin or

otherwise carry out a fee device exception beneath and by an authorization issued through manner of way

of the Reserve Bank beneath the provisions of this Act". It's very smooth that how every fee system

operational in India concerning fee duties due to reimbursement or payment of more than one type of fee

directives regarding securities, funds, or derivatives or foreign exchange or extraordinary transactions

need to have approval in the manner that RBI suggests. PSS Act moreover gives controls to banks to

problem authorization for strolling system of fee, and to change the authorization agreed by device

benefactors in case of infringements of any provisions of PSS Act, PSS Regulations, 2008, orders or

commands issued through a manner that RBI suggests for the operation of fee device is conflicting to the

conditions & terms scenario to which the authorization became allotted.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Since the worldwide monetary disaster of 2007-08, numerous traits happened, pushing the vital aid of

using the G20 for restructuring Over Counter (OTC) derivatives markets. At that time, TRS surfaced as a

pristine kind of FMI, especially within the OTC derivatives market. In line with the G20 dedication of

worldwide traits, the PSS Act became amended to consist of Trade Repository such as some other class of

charge the structure. The PSS Act additionally observed TR, which targeted as such with the support of

using the banks.

Similarly, chapter IV PSS Act and the diverse clauses offer Supervision and Regulation of such Payment

Systems. Power to supervise, adjust and compromise:

Segment 10: Power to decide and recommend norms - in regard of organization, size and state of

instalment directions, timings to be kept up with by instalment frameworks, way of asset moves,

measures of participation of instalment situation and their privileges and commitments, and issuance of

rules for viable administration of instalment frameworks.

Segment 11: Notice of progress in the Payment System - framework suppliers will not cause any

change influencing the construction and activity of the instalment framework without earlier endorsement

of banks.

Segment 12: Power to call for returns, archives or other data - engages banks to call for returns,

reports or other data from any framework supplier in regards to activities of instalment frameworks

worked by them.

Segment 13: Access to data - engages banks to get to any data connecting with any instalment

framework with the framework supplier and the framework members.

Segment 14: Power to enter and assess - engages banks to enter and review any premises where an

instalment framework is worked and any gear including any PC framework or different archives.

Segment 16: Power to complete review and assessment - enables banks to lead or get directed reviews

and examinations of an instalment framework or framework members

Segment 17: Power to give explicit bearing - engages banks to give headings to a framework supplier or

framework member to stop any demonstration, oversight or course of lead that would bring about

foundational dangers or influences the instalment framework, financial or credit strategy of the country.

9

using the G20 for restructuring Over Counter (OTC) derivatives markets. At that time, TRS surfaced as a

pristine kind of FMI, especially within the OTC derivatives market. In line with the G20 dedication of

worldwide traits, the PSS Act became amended to consist of Trade Repository such as some other class of

charge the structure. The PSS Act additionally observed TR, which targeted as such with the support of

using the banks.

Similarly, chapter IV PSS Act and the diverse clauses offer Supervision and Regulation of such Payment

Systems. Power to supervise, adjust and compromise:

Segment 10: Power to decide and recommend norms - in regard of organization, size and state of

instalment directions, timings to be kept up with by instalment frameworks, way of asset moves,

measures of participation of instalment situation and their privileges and commitments, and issuance of

rules for viable administration of instalment frameworks.

Segment 11: Notice of progress in the Payment System - framework suppliers will not cause any

change influencing the construction and activity of the instalment framework without earlier endorsement

of banks.

Segment 12: Power to call for returns, archives or other data - engages banks to call for returns,

reports or other data from any framework supplier in regards to activities of instalment frameworks

worked by them.

Segment 13: Access to data - engages banks to get to any data connecting with any instalment

framework with the framework supplier and the framework members.

Segment 14: Power to enter and assess - engages banks to enter and review any premises where an

instalment framework is worked and any gear including any PC framework or different archives.

Segment 16: Power to complete review and assessment - enables banks to lead or get directed reviews

and examinations of an instalment framework or framework members

Segment 17: Power to give explicit bearing - engages banks to give headings to a framework supplier or

framework member to stop any demonstration, oversight or course of lead that would bring about

foundational dangers or influences the instalment framework, financial or credit strategy of the country.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

Contactless payment is consciously carving out a place for itself, either as a convenience of practise or as

a transactional momentum. "The trend of utilising smart cards and smartphones is rising across

millennials," according to the report. Organizations are embracing this technological invention not only to

educate their customers, but also to make investments of their company. The money kept in a bank

account is safe and regulated if curb the weakness of keeping money at home because of robbery however

the rapid evolution of smart payments has radically affected the need of having payments cards and even

bank accounts

10

Contactless payment is consciously carving out a place for itself, either as a convenience of practise or as

a transactional momentum. "The trend of utilising smart cards and smartphones is rising across

millennials," according to the report. Organizations are embracing this technological invention not only to

educate their customers, but also to make investments of their company. The money kept in a bank

account is safe and regulated if curb the weakness of keeping money at home because of robbery however

the rapid evolution of smart payments has radically affected the need of having payments cards and even

bank accounts

10

Reference List

Al-dalahmeh, M., Khalaf, R. and Obeidat, B., 2018. The effect of employee engagement on

organizational performance via the mediating role of job satisfaction: The case of IT employees in

Jordanian banking sector. Modern Applied Science, 12(6), pp.17-43.

Ali, M. and Puah, C.H., 2018. The internal determinants of bank profitability and stability: An insight

from banking sector of Pakistan. Management Research Review.

Aydin, G. and Burnaz, S., 2016. Adoption of mobile payment systems: A study on mobile

wallets. Journal of Business Economics and Finance, 5(1), pp.73-92.

Chandra, S., Srivastava, S.C. and Theng, Y.L., 2010. Evaluating the role of trust in consumer adoption of

mobile payment systems: An empirical analysis. Communications of the Association for Information

Systems, 27(1), p.29.

Daştan, İ. and Gürler, C., 2016. Factors affecting the adoption of mobile payment systems: An empirical

analysis. EMAJ: Emerging Markets Journal, 6(1), pp.17-24.

de Luna, I.R., Liébana-Cabanillas, F., Sánchez-Fernández, J. and Muñoz-Leiva, F., 2019. Mobile

payment is not all the same: The adoption of mobile payment systems depending on the technology

applied. Technological Forecasting and Social Change, 146, pp.931-944.

Do, N., Tham, J., Khatibi, A. and Azam, S., 2019. An empirical analysis of Cambodian behavior intention

towards mobile payment. Management Science Letters, 9(12), pp.1941-1954.

Hammoud, J., Bizri, R.M. and El Baba, I., 2018. The impact of e-banking service quality on customer

satisfaction: Evidence from the Lebanese banking sector. Sage Open, 8(3), p.2158244018790633.

Hartawan, M.S., Putra, A.S. and Muktiono, A., 2020. Smart City Concept for Integrated Citizen

Information Smart Card or ICISC in DKI Jakarta. International Journal of Science, Technology &

Management, 1(4), pp.364-370.

11

Al-dalahmeh, M., Khalaf, R. and Obeidat, B., 2018. The effect of employee engagement on

organizational performance via the mediating role of job satisfaction: The case of IT employees in

Jordanian banking sector. Modern Applied Science, 12(6), pp.17-43.

Ali, M. and Puah, C.H., 2018. The internal determinants of bank profitability and stability: An insight

from banking sector of Pakistan. Management Research Review.

Aydin, G. and Burnaz, S., 2016. Adoption of mobile payment systems: A study on mobile

wallets. Journal of Business Economics and Finance, 5(1), pp.73-92.

Chandra, S., Srivastava, S.C. and Theng, Y.L., 2010. Evaluating the role of trust in consumer adoption of

mobile payment systems: An empirical analysis. Communications of the Association for Information

Systems, 27(1), p.29.

Daştan, İ. and Gürler, C., 2016. Factors affecting the adoption of mobile payment systems: An empirical

analysis. EMAJ: Emerging Markets Journal, 6(1), pp.17-24.

de Luna, I.R., Liébana-Cabanillas, F., Sánchez-Fernández, J. and Muñoz-Leiva, F., 2019. Mobile

payment is not all the same: The adoption of mobile payment systems depending on the technology

applied. Technological Forecasting and Social Change, 146, pp.931-944.

Do, N., Tham, J., Khatibi, A. and Azam, S., 2019. An empirical analysis of Cambodian behavior intention

towards mobile payment. Management Science Letters, 9(12), pp.1941-1954.

Hammoud, J., Bizri, R.M. and El Baba, I., 2018. The impact of e-banking service quality on customer

satisfaction: Evidence from the Lebanese banking sector. Sage Open, 8(3), p.2158244018790633.

Hartawan, M.S., Putra, A.S. and Muktiono, A., 2020. Smart City Concept for Integrated Citizen

Information Smart Card or ICISC in DKI Jakarta. International Journal of Science, Technology &

Management, 1(4), pp.364-370.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.