Corporate Governance and Ethical Failures: The Case of Carillion Plc

VerifiedAdded on 2022/12/26

|11

|3115

|41

Essay

AI Summary

This essay critically analyzes the corporate governance failures of Carillion Plc, a multinational construction services company in the UK. The analysis explores the ethical and financial mismanagement that led to the company's collapse, examining the roles of the board, shareholders, and auditors. The essay applies agency and stakeholder theories to understand the failures, highlighting issues such as over-optimistic reporting, reverse factoring, and the disregard for ethical conduct. It details how the board prioritized their rewards, failed to maintain transparency, and neglected risk management, leading to the company's demise. The analysis emphasizes the importance of ethical behavior, accountability, and adherence to corporate governance codes in preventing such failures, offering valuable lessons for businesses and stakeholders.

Corporate Governance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

There are various corporate failures which surprised everyone globally but along with

that highlighted the loopholes into the system. The major reason behind the events of corporate

failure is due to the corporate and ethical governance weaknesses. This essay critically analyses

the Carillion Plc as an example of failings which went from showing just £5.2bn revenue, and

£146.7m profit before tax, offering dividend to its shareholders with an order book of £16 billion

and £41.6 billion in pipeline in 2016. This essay provides an insight into the definition of ethics

and corporate governance followed by the theoretically understanding and analysing the failing

at the board level within an organization. For doing this, different theories have been put in place

for effectively understanding the failure.

Analysing the Carillion Plc failure

Carillion was the multinational organization into construction services in UK. Prior to its

demise, the company was having the liability of nearly £7 bn having 43000 individuals working

and the 28000 pension scheme members. The failure of the company resulted into delays and

cancellation of the projects in addition to the loss of jobs of its employees, pensioners, partner

etc. This case was an unsustainable dash for cash. Carillion's acquisition has lacking the coherent

strategy in terms of removing competitors from the market but it also failed to achieve or

generate the desired margins (Bhaskar and Flower, 2019). The purchases were funded by debts

which was rising which resulted into the creation of problem for the pension in the future. Even

though the company was facing the financial problem then too it worked on expanding into new

market along with exploiting its suppliers. The company wrong fully presented its accounts,

hiding the reality and increasing the dividends every year. The company mainly relied upon its

suppliers in respect to providing materials and support but then it treated them as contempt.

In between the year 2012 and 2017, the company paid out nearly £330 mn more in

respect to dividends in comparison to what it made through its business activities and the in

2009-18, the company owed a debt increased from £242 mn to approximately £1.3 bn. The most

surprising thing was that despite poor performance and weak financial situation, the board of the

company made a payment in millions pertaining to bonuses to its top executives in addition to

the salaries which was criticized by the shareholders (Sweet, 2018). The main reason behind the

collapse of Carillion is the lack of accountability and professionalism and inability to comply

with the governance and ethical code of conduct. The key participant into this collapse are the

that highlighted the loopholes into the system. The major reason behind the events of corporate

failure is due to the corporate and ethical governance weaknesses. This essay critically analyses

the Carillion Plc as an example of failings which went from showing just £5.2bn revenue, and

£146.7m profit before tax, offering dividend to its shareholders with an order book of £16 billion

and £41.6 billion in pipeline in 2016. This essay provides an insight into the definition of ethics

and corporate governance followed by the theoretically understanding and analysing the failing

at the board level within an organization. For doing this, different theories have been put in place

for effectively understanding the failure.

Analysing the Carillion Plc failure

Carillion was the multinational organization into construction services in UK. Prior to its

demise, the company was having the liability of nearly £7 bn having 43000 individuals working

and the 28000 pension scheme members. The failure of the company resulted into delays and

cancellation of the projects in addition to the loss of jobs of its employees, pensioners, partner

etc. This case was an unsustainable dash for cash. Carillion's acquisition has lacking the coherent

strategy in terms of removing competitors from the market but it also failed to achieve or

generate the desired margins (Bhaskar and Flower, 2019). The purchases were funded by debts

which was rising which resulted into the creation of problem for the pension in the future. Even

though the company was facing the financial problem then too it worked on expanding into new

market along with exploiting its suppliers. The company wrong fully presented its accounts,

hiding the reality and increasing the dividends every year. The company mainly relied upon its

suppliers in respect to providing materials and support but then it treated them as contempt.

In between the year 2012 and 2017, the company paid out nearly £330 mn more in

respect to dividends in comparison to what it made through its business activities and the in

2009-18, the company owed a debt increased from £242 mn to approximately £1.3 bn. The most

surprising thing was that despite poor performance and weak financial situation, the board of the

company made a payment in millions pertaining to bonuses to its top executives in addition to

the salaries which was criticized by the shareholders (Sweet, 2018). The main reason behind the

collapse of Carillion is the lack of accountability and professionalism and inability to comply

with the governance and ethical code of conduct. The key participant into this collapse are the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

board members, shareholders and the Big 4 firms which resulted into failure of the company to

meet with its ethical and corporate governance requirement.

Critical analysis from ethical and corporate governance perspective

In order to critically evaluate the case, from the perspective of corporate governance,

agency theory and the shareholder theory is being utilized. The agency theory basically defines

the relationship between the shareholders (principals) and the directors of the company (agents).

As per this theory, the agents are hired by the principals for the purpose of running the business.

The shareholders delegates the work pertaining to managing and running of business to its

directors along with the expectation that they will act in the betterment and interest of the

principal. But in contrast, there are chances that the agent might not act for the interest of the

principal. There are chances that there occurs a conflict of interest among the directors and

shareholders (Conway and Mor, 2018). Under the case of Carillion Plc made a joint venture

which it has achieved its financial close at £1.7 billion which is basically a public private

partnership. The JV was with the hospital infrastructure based out in Ontario, Canada. This

partnership was initially objected by the debt holders which was because of the reason that the

company already had a huge amount of financial crisis in the past 3 years. In addition to this, the

company merged with the GT rail maintenance in 2001 and also took-over the citex management

in 2002. It was also being observed that the company was operating in an aggressive way after its

demerger from its parent company in the year 2009. In addition to this, Carillion Plc also

acquired in the year 2008, company named Alfred McAlpine for amount of £572 million.

Therefore, the outcome of it can be seen that the Carillion Plc acquired a good market position

but has also impacted its performance during the time of financial downturn (Gallagher, Crinson

and Seeley, 2018). The directors provide bonuses to it top executives apart from the salary

despite knowing that the financial position of the company is not goods. Thus, it failed to comply

with the corporate governance pertaining to the betterment of the company and it shareholders.

Therefore, based upon this theory, it can be said that the managers in Carillion Plc were

interested in the remuneration and the benefits. Self-interest was the major factor and egoism key

concept underpinning this, which is the most prominent factor of ethical egoism.

The stakeholder theory incorporates the accountability of the management towards its

shareholders. Its shareholders involve the suppliers, employees, trade associations, government

and business partners. Pertaining to the Carillion Plc, it can be stated that the company even in

meet with its ethical and corporate governance requirement.

Critical analysis from ethical and corporate governance perspective

In order to critically evaluate the case, from the perspective of corporate governance,

agency theory and the shareholder theory is being utilized. The agency theory basically defines

the relationship between the shareholders (principals) and the directors of the company (agents).

As per this theory, the agents are hired by the principals for the purpose of running the business.

The shareholders delegates the work pertaining to managing and running of business to its

directors along with the expectation that they will act in the betterment and interest of the

principal. But in contrast, there are chances that the agent might not act for the interest of the

principal. There are chances that there occurs a conflict of interest among the directors and

shareholders (Conway and Mor, 2018). Under the case of Carillion Plc made a joint venture

which it has achieved its financial close at £1.7 billion which is basically a public private

partnership. The JV was with the hospital infrastructure based out in Ontario, Canada. This

partnership was initially objected by the debt holders which was because of the reason that the

company already had a huge amount of financial crisis in the past 3 years. In addition to this, the

company merged with the GT rail maintenance in 2001 and also took-over the citex management

in 2002. It was also being observed that the company was operating in an aggressive way after its

demerger from its parent company in the year 2009. In addition to this, Carillion Plc also

acquired in the year 2008, company named Alfred McAlpine for amount of £572 million.

Therefore, the outcome of it can be seen that the Carillion Plc acquired a good market position

but has also impacted its performance during the time of financial downturn (Gallagher, Crinson

and Seeley, 2018). The directors provide bonuses to it top executives apart from the salary

despite knowing that the financial position of the company is not goods. Thus, it failed to comply

with the corporate governance pertaining to the betterment of the company and it shareholders.

Therefore, based upon this theory, it can be said that the managers in Carillion Plc were

interested in the remuneration and the benefits. Self-interest was the major factor and egoism key

concept underpinning this, which is the most prominent factor of ethical egoism.

The stakeholder theory incorporates the accountability of the management towards its

shareholders. Its shareholders involve the suppliers, employees, trade associations, government

and business partners. Pertaining to the Carillion Plc, it can be stated that the company even in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the times of loss paid a huge amount of dividend to its shareholders and represented its annual

report showing that everything is going as expected, which was all false. In addition to this, it is

important to note that the big 4 firms were also involved in this collapse in some way. Deloitte

was engaged for some time as the internal auditor of the company along with its rival KPMG

which was appointed as its external auditor (VERSCHOOR, 2018). Besides this, EY was also

being involved in respect of providing advice to the company and restructuring the company as

per the committees. PwC was offering advice pertaining to the pension schemes along with govt.

on Carillion contract. The company paid dividend to its shareholders so that they can retain them

and avoid any situation of chaos but on the side, it treated its suppliers badly. It was a routine for

the company like paying late, quibbling of invoices and apart from this, delays in the reporting

period was all became the policy of the company. The arrangement made in regard to the

payment to suppliers opened a line of credit for the company which was systematically utilized

by the company in order to fragile its balance sheet irrespective of its supplier’s balance sheet.

Ethics are the moral principles which is being govern by the person’s behaviour within

the business. Under this, it is expected to cover thebroad social scope which is more than

economics. On reading out the Carillion’s 2016 report, there was no sign of the company in

difficult situation and were communicating their shareholders and investors about their ability to

minimize its cost along with improving efficiency which has resulted into increase in strong

profit margins.

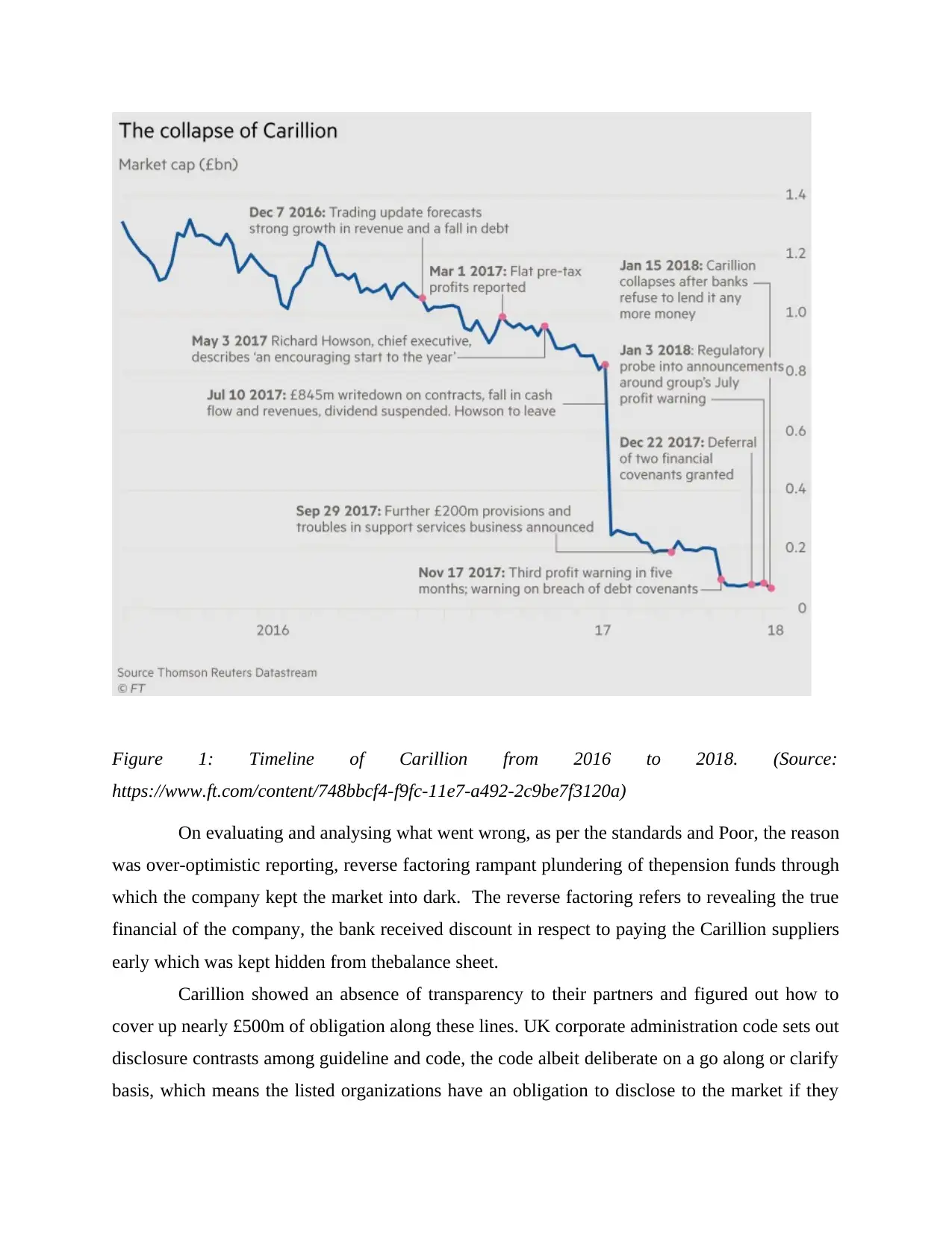

The figure below depicts how quickly the organization went from the strong and healthy

statement in 2016 to the 3 warnings pertaining to profits in the year 2017 leading to liquidation

in 2018.

report showing that everything is going as expected, which was all false. In addition to this, it is

important to note that the big 4 firms were also involved in this collapse in some way. Deloitte

was engaged for some time as the internal auditor of the company along with its rival KPMG

which was appointed as its external auditor (VERSCHOOR, 2018). Besides this, EY was also

being involved in respect of providing advice to the company and restructuring the company as

per the committees. PwC was offering advice pertaining to the pension schemes along with govt.

on Carillion contract. The company paid dividend to its shareholders so that they can retain them

and avoid any situation of chaos but on the side, it treated its suppliers badly. It was a routine for

the company like paying late, quibbling of invoices and apart from this, delays in the reporting

period was all became the policy of the company. The arrangement made in regard to the

payment to suppliers opened a line of credit for the company which was systematically utilized

by the company in order to fragile its balance sheet irrespective of its supplier’s balance sheet.

Ethics are the moral principles which is being govern by the person’s behaviour within

the business. Under this, it is expected to cover thebroad social scope which is more than

economics. On reading out the Carillion’s 2016 report, there was no sign of the company in

difficult situation and were communicating their shareholders and investors about their ability to

minimize its cost along with improving efficiency which has resulted into increase in strong

profit margins.

The figure below depicts how quickly the organization went from the strong and healthy

statement in 2016 to the 3 warnings pertaining to profits in the year 2017 leading to liquidation

in 2018.

Figure 1: Timeline of Carillion from 2016 to 2018. (Source:

https://www.ft.com/content/748bbcf4-f9fc-11e7-a492-2c9be7f3120a)

On evaluating and analysing what went wrong, as per the standards and Poor, the reason

was over-optimistic reporting, reverse factoring rampant plundering of thepension funds through

which the company kept the market into dark. The reverse factoring refers to revealing the true

financial of the company, the bank received discount in respect to paying the Carillion suppliers

early which was kept hidden from thebalance sheet.

Carillion showed an absence of transparency to their partners and figured out how to

cover up nearly £500m of obligation along these lines. UK corporate administration code sets out

disclosure contrasts among guideline and code, the code albeit deliberate on a go along or clarify

basis, which means the listed organizations have an obligation to disclose to the market if they

https://www.ft.com/content/748bbcf4-f9fc-11e7-a492-2c9be7f3120a)

On evaluating and analysing what went wrong, as per the standards and Poor, the reason

was over-optimistic reporting, reverse factoring rampant plundering of thepension funds through

which the company kept the market into dark. The reverse factoring refers to revealing the true

financial of the company, the bank received discount in respect to paying the Carillion suppliers

early which was kept hidden from thebalance sheet.

Carillion showed an absence of transparency to their partners and figured out how to

cover up nearly £500m of obligation along these lines. UK corporate administration code sets out

disclosure contrasts among guideline and code, the code albeit deliberate on a go along or clarify

basis, which means the listed organizations have an obligation to disclose to the market if they

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

are not following and in addition to this, it is also sets out that the directors ought to affirm that

they have completed a robust evaluation of the key risks confronting the organization – including

those that would undermine its plan of action, future execution, liquidity and solvency and that

Directors ought to state about those risks and clarify how they are being overseen or relieved

(Xiong, 2020). Unmistakably this didn't happen, and inside a half year when the organization

was in a difficult situation, with £845m esteem decrease in contracts, a fall in income and capital,

and a suspended profit.

The BOD failed to follow ethical code of conduct which some or the other way led to

the fall out of the company. The Board of Carillion changed the organization strategy in 2017 to

ensure their rewards, which means if the organization entered liquidation, they would in any case

be paid (Nordberg, 2020). The planned way this happened was unethical and egoistic in securing

their own advantage, Howson gathered £591,000 reward the time of 3 profit warnings and, on

liquidation in January 2018 he kept on being paid a compensation of £660,000, similarly as did

other board members. The compensation advisory group ought to have scrutinized the thought

processes of this adjustment in policy that repudiated the code, there was no such sensitivity

appeared to the large numbers who got jobless in Carillion's liquidation or those whose pension

was pillaged because of board failures.

The pension fund deficiency expanded from £249 million in the year 2010 to £805

million in the year 2016, practically similar sum as dividends paid to investors in that period. The

Pension trustees had long hard fights with Carillion board in attempting to execute increments to

the fund. It was alluded to the Pensions Regulator, (TPR) as no recuperation plan was set up that

was suggested by trustees, they undermined segment 231 powers to authorize this, it was

accounted for in the House of Commons government report that the key controllers, the FRC and

the TPR were weak in giving empty threats. There has been a lot of conversation over facing

intense meeting room characters, for example, Robert Maxwell or Enron's KenntheLay, even

Carillion's CFO and senior informant Emma Mercer discovered she 'was not tuned in to' by

board members.

Carillion were bidding for contracts no matter what, Howson said, “they needed to bid

and they needed to win”, realizing that the fact that the aggressive bidding was producing money

instead of benefit which depicts the reckless conduct, no perspective of the potential outcomes of

such activities, showing absence of good thinking. The profits were exaggerated, fixes to one

they have completed a robust evaluation of the key risks confronting the organization – including

those that would undermine its plan of action, future execution, liquidity and solvency and that

Directors ought to state about those risks and clarify how they are being overseen or relieved

(Xiong, 2020). Unmistakably this didn't happen, and inside a half year when the organization

was in a difficult situation, with £845m esteem decrease in contracts, a fall in income and capital,

and a suspended profit.

The BOD failed to follow ethical code of conduct which some or the other way led to

the fall out of the company. The Board of Carillion changed the organization strategy in 2017 to

ensure their rewards, which means if the organization entered liquidation, they would in any case

be paid (Nordberg, 2020). The planned way this happened was unethical and egoistic in securing

their own advantage, Howson gathered £591,000 reward the time of 3 profit warnings and, on

liquidation in January 2018 he kept on being paid a compensation of £660,000, similarly as did

other board members. The compensation advisory group ought to have scrutinized the thought

processes of this adjustment in policy that repudiated the code, there was no such sensitivity

appeared to the large numbers who got jobless in Carillion's liquidation or those whose pension

was pillaged because of board failures.

The pension fund deficiency expanded from £249 million in the year 2010 to £805

million in the year 2016, practically similar sum as dividends paid to investors in that period. The

Pension trustees had long hard fights with Carillion board in attempting to execute increments to

the fund. It was alluded to the Pensions Regulator, (TPR) as no recuperation plan was set up that

was suggested by trustees, they undermined segment 231 powers to authorize this, it was

accounted for in the House of Commons government report that the key controllers, the FRC and

the TPR were weak in giving empty threats. There has been a lot of conversation over facing

intense meeting room characters, for example, Robert Maxwell or Enron's KenntheLay, even

Carillion's CFO and senior informant Emma Mercer discovered she 'was not tuned in to' by

board members.

Carillion were bidding for contracts no matter what, Howson said, “they needed to bid

and they needed to win”, realizing that the fact that the aggressive bidding was producing money

instead of benefit which depicts the reckless conduct, no perspective of the potential outcomes of

such activities, showing absence of good thinking. The profits were exaggerated, fixes to one

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

hospital bringing about 12.7% losses were superseded by senior administration and was recorded

as 4.9% (£53 million) profit, there were 18 other similar agreements, also £294 million “traded

not certified” work not recorded accurately to increase the profit.

The Non-Executive Directors (NED) neglected to investigate or challenge reckless

practices, they failed in maintaining the code in guaranteeing and maintaining integrity of

monetary data and the risk management. The Tyson report (2003) had featured the requirement

for more thorough and more straightforward search measures for NEDs, obviously this wasn't

the situation with Philip Green, the dog that didn't bark alongside numerous others (Crilly, 2019).

The auditors were reprimanded for being absolutely smug, neglecting to practice appropriate

judgment over Carillion's records (The governance lessons of Carillion's collapse. 2018). KPMG

got £29million in more than 19 years, rotation of auditors has been a debated subject, with an

origination that time breeds commonality and isn't valuable to the independence required. The

review board ought to have been predominant in addressing auditor independence. In addition to

this, Deloitte also failed in their job of risk handling and interior controls while gathering £10 mn

as fees, the government report suggested reference of the statutory audit market to the

Competition and Markets as the trust and quality pertaining to audit had failed.

Carillion board sacrificed partners; the workers, pension holders and creditors and in

focusing on investor short-term interests. The BOD failed in its roles and duties, the association

was liquidated, investors got nothing. The Government inquiry stated that the board had

illustrated, carelessness, ravenousness and exploitations.

Untrustworthy and unethical behaviour within the company contrarily affects the

welfare of the society and questions the role among the ethics and administration however there

is an obligation and an ethical commitment to take care of the organization interests, which is a

duty of a good stewardship. Results inside Carillion being; firemen notified to dish out school

suppers to 18,000 schoolchildren in the event that Carillion's cooking staff didn't appear (they

did). The Government provided £150 mn to keep administrations running (The Collapse of

Carillion - a Failure of Ethical Standards? 2018). The societal impact of ineffective decision

making, puts costs to the detriment of people in general, the Government taking care of the

expenses of incomplete structures, thousands jobless, and the PPF who had endured its greatest

shot securing Carillion's pensions, and the loan providers (creditors) does not see any return of

over £2 billion owed. A consequentialist ethical system set up would have been deterrent, there

as 4.9% (£53 million) profit, there were 18 other similar agreements, also £294 million “traded

not certified” work not recorded accurately to increase the profit.

The Non-Executive Directors (NED) neglected to investigate or challenge reckless

practices, they failed in maintaining the code in guaranteeing and maintaining integrity of

monetary data and the risk management. The Tyson report (2003) had featured the requirement

for more thorough and more straightforward search measures for NEDs, obviously this wasn't

the situation with Philip Green, the dog that didn't bark alongside numerous others (Crilly, 2019).

The auditors were reprimanded for being absolutely smug, neglecting to practice appropriate

judgment over Carillion's records (The governance lessons of Carillion's collapse. 2018). KPMG

got £29million in more than 19 years, rotation of auditors has been a debated subject, with an

origination that time breeds commonality and isn't valuable to the independence required. The

review board ought to have been predominant in addressing auditor independence. In addition to

this, Deloitte also failed in their job of risk handling and interior controls while gathering £10 mn

as fees, the government report suggested reference of the statutory audit market to the

Competition and Markets as the trust and quality pertaining to audit had failed.

Carillion board sacrificed partners; the workers, pension holders and creditors and in

focusing on investor short-term interests. The BOD failed in its roles and duties, the association

was liquidated, investors got nothing. The Government inquiry stated that the board had

illustrated, carelessness, ravenousness and exploitations.

Untrustworthy and unethical behaviour within the company contrarily affects the

welfare of the society and questions the role among the ethics and administration however there

is an obligation and an ethical commitment to take care of the organization interests, which is a

duty of a good stewardship. Results inside Carillion being; firemen notified to dish out school

suppers to 18,000 schoolchildren in the event that Carillion's cooking staff didn't appear (they

did). The Government provided £150 mn to keep administrations running (The Collapse of

Carillion - a Failure of Ethical Standards? 2018). The societal impact of ineffective decision

making, puts costs to the detriment of people in general, the Government taking care of the

expenses of incomplete structures, thousands jobless, and the PPF who had endured its greatest

shot securing Carillion's pensions, and the loan providers (creditors) does not see any return of

over £2 billion owed. A consequentialist ethical system set up would have been deterrent, there

is no expectation for associations to show genuine philanthropy, however thought of results,

ought to have been an underlying economic thought. Honesty and integrity is considered to be

the same thing from thecorporate governance perspective but morality is crucial when one has

the responsibility of others. The board of Carillion plc failed in completing their obligation

towards its stakeholders and trust is important pertaining to business ethics which can be possible

through maintenance of transparency and disclosure. The board needed to be transparent in

regard to hiding of debt obligation and exaggerating benefits illustrating ignorance of the

outcomes, having an organization statement of purpose to say they are the 'confided in

accomplice' would be ludicrous if the results weren't so serious.

It can be inferred from the above that the Carillion collapse was the outcome of number

of mistakes in respect to the ethical and corporate governance which all together resulted into

damaging the firm. The company paid the dividend and the bonuses which were being paid to

the top executives and shareholders at a rate which was not affordable by the company. The

board were planned in changing policy around compensation showing adjusted interests

connected to reward might be inconvenient to moral authority (Sikka and et.al., 2018). An

absence of freedom appeared by those there to secure, for example, the NED's and auditors to the

point that the public authority advisory group need to see the changes and a complete negligence

of the suppliers. The board guaranteed they were remunerated for the failure in accepting

compensation and rewards long after the breakdown of the organization and showed no capable

authority towards representatives. Audit is the main part of corporate governance and absence of

effective audit results into affecting the trust in the process. The collapse of Carillion Plc has led

to creation of alert to FRC to respond quickly to the investigation pertaining to audit.

ought to have been an underlying economic thought. Honesty and integrity is considered to be

the same thing from thecorporate governance perspective but morality is crucial when one has

the responsibility of others. The board of Carillion plc failed in completing their obligation

towards its stakeholders and trust is important pertaining to business ethics which can be possible

through maintenance of transparency and disclosure. The board needed to be transparent in

regard to hiding of debt obligation and exaggerating benefits illustrating ignorance of the

outcomes, having an organization statement of purpose to say they are the 'confided in

accomplice' would be ludicrous if the results weren't so serious.

It can be inferred from the above that the Carillion collapse was the outcome of number

of mistakes in respect to the ethical and corporate governance which all together resulted into

damaging the firm. The company paid the dividend and the bonuses which were being paid to

the top executives and shareholders at a rate which was not affordable by the company. The

board were planned in changing policy around compensation showing adjusted interests

connected to reward might be inconvenient to moral authority (Sikka and et.al., 2018). An

absence of freedom appeared by those there to secure, for example, the NED's and auditors to the

point that the public authority advisory group need to see the changes and a complete negligence

of the suppliers. The board guaranteed they were remunerated for the failure in accepting

compensation and rewards long after the breakdown of the organization and showed no capable

authority towards representatives. Audit is the main part of corporate governance and absence of

effective audit results into affecting the trust in the process. The collapse of Carillion Plc has led

to creation of alert to FRC to respond quickly to the investigation pertaining to audit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bhaskar, K. and Flower, J., 2019. Financial failures and scandals: From Enron to Carillion.

Routledge.

Conway, L. and Mor, F., 2018. The collapse of Carillion. House of Commons Briefing Paper,

(08206). p.18.

Crilly, D. O. N. A. L., 2019. Behavioral stakeholder theory. The Cambridge Handbook of

Stakeholder Theory. p.250.

Gallagher, A., Crinson, K. and Seeley, R., 2018. Politicization of Corporate Failure. American

Bankruptcy Institute Journal. 37(9). pp.26-59.

Nordberg, D., 2020. Successes in Corporate Governance—Or Failures?. In The Cadbury Code

and Recurrent Crisis (pp. 1-14). Palgrave Macmillan, Cham.

Sikka, P., and et.al., 2018. Reforming the auditing industry. Report commissioned by the Shadow

Chancellor of the Exchequer, John McDonnell MP.

Sweet, R., 2018. Carillion’s “accounting tricks”: MPs’ damning verdict. Construction Research

and Innovation. 9(2). pp.48-50.

VERSCHOOR, C. C., 2018. CARILLION FAILURE RAISES QUESTIONS ABOUT

CONSULTING SERVICES. Strategic Finance.

Xiong, X. S., 2020. Time to Revisit Capital Maintenance on Profits Distribution: Lesson from

Carillion and Beyond. European Business Law Review. 31(2).

Online

The Collapse of Carillion - a Failure of Ethical Standards? 2018. [Online]. Available Through:<

https://cspl.blog.gov.uk/2018/02/01/the-collapse-of-carillion-a-failure-of-ethical-

standards/>.

The governance lessons of Carillion's collapse. 2018. [Online]. Available Through:<

https://www.accaglobal.com/uk/en/member/member/accounting-business/2018/04/

corporate/carillions-collapse.html>.

Books and Journals

Bhaskar, K. and Flower, J., 2019. Financial failures and scandals: From Enron to Carillion.

Routledge.

Conway, L. and Mor, F., 2018. The collapse of Carillion. House of Commons Briefing Paper,

(08206). p.18.

Crilly, D. O. N. A. L., 2019. Behavioral stakeholder theory. The Cambridge Handbook of

Stakeholder Theory. p.250.

Gallagher, A., Crinson, K. and Seeley, R., 2018. Politicization of Corporate Failure. American

Bankruptcy Institute Journal. 37(9). pp.26-59.

Nordberg, D., 2020. Successes in Corporate Governance—Or Failures?. In The Cadbury Code

and Recurrent Crisis (pp. 1-14). Palgrave Macmillan, Cham.

Sikka, P., and et.al., 2018. Reforming the auditing industry. Report commissioned by the Shadow

Chancellor of the Exchequer, John McDonnell MP.

Sweet, R., 2018. Carillion’s “accounting tricks”: MPs’ damning verdict. Construction Research

and Innovation. 9(2). pp.48-50.

VERSCHOOR, C. C., 2018. CARILLION FAILURE RAISES QUESTIONS ABOUT

CONSULTING SERVICES. Strategic Finance.

Xiong, X. S., 2020. Time to Revisit Capital Maintenance on Profits Distribution: Lesson from

Carillion and Beyond. European Business Law Review. 31(2).

Online

The Collapse of Carillion - a Failure of Ethical Standards? 2018. [Online]. Available Through:<

https://cspl.blog.gov.uk/2018/02/01/the-collapse-of-carillion-a-failure-of-ethical-

standards/>.

The governance lessons of Carillion's collapse. 2018. [Online]. Available Through:<

https://www.accaglobal.com/uk/en/member/member/accounting-business/2018/04/

corporate/carillions-collapse.html>.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Figure 2: (Source:

https://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_CLLN_2016.pdf)

Figure 2: (Source:

https://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_CLLN_2016.pdf)

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.