Taxation Report: Analysis of Carimin Petroleum Berhad Taxation

VerifiedAdded on 2021/01/02

|12

|3234

|72

Report

AI Summary

This report provides a comprehensive analysis of the taxation practices of Carimin Petroleum Berhad, an investment holding company in the energy sector. The report begins by explaining how to determine the basis period and year of assessment under Malaysian law, referencing the Income Tax Act 1967 and relevant sections. It then delves into the elements of computing chargeable income, including capital expenditure, capital gains, and capital losses, highlighting relevant tax incentives and regulations. The discussion on capital expenditure claimable by the organization covers initial and annual allowances for various qualifying assets, referencing the Inland Revenue Board of Malaysia's guidelines. The report uses the company's annual report data to illustrate the computations, capital expenditure, and capital allowances. The corporate structure of the company and its impact on taxation is also discussed. The report concludes by summarizing the key findings and providing references to the sources used.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................3

1. Describing on how to determine basis period and year of assessment...................................3

2. Explaining elements in computing the chargeable income.....................................................4

3. Discussion on capital expenditure claimable by organisation................................................6

4. Computation of tax payable with the help of annual report of company................................7

SUMMARY.....................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................3

1. Describing on how to determine basis period and year of assessment...................................3

2. Explaining elements in computing the chargeable income.....................................................4

3. Discussion on capital expenditure claimable by organisation................................................6

4. Computation of tax payable with the help of annual report of company................................7

SUMMARY.....................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

The nature of Carimin Petroleum Berhad is an investment holding company engaged in

energy sector. It was established in 1989 and evolved to become leading oil and gas companies

providing technical and engineering support services in Malaysian industry. Organisation

specialises in engineering, scheduled/work pack development, procurement, recommissioning

and commissioning activities. It also includes deploy marine vessels such as work barges,

accommodation vessels, crew boats, anchor handling tug supply vessels which are regarded as

part of marine spread activities. Business has steadily grown in recent years from just a

manpower service provider to dynamic and emerging contractor in integrated maintenance,

rejuvenation and hook-up and commissioning (HUC) of both offshore and onshore in oil and gas

support industries.

Till date, Carimin Petroleum Berhad had completed projects of more than RM1 billion

and has diversified portfolio of reputed clients. These clients include PETRONAS Carigali,

Murphy Oil, Repsol, Exxon Mobil and many other clients. The corporate structure of company is

drawn below-

1

The nature of Carimin Petroleum Berhad is an investment holding company engaged in

energy sector. It was established in 1989 and evolved to become leading oil and gas companies

providing technical and engineering support services in Malaysian industry. Organisation

specialises in engineering, scheduled/work pack development, procurement, recommissioning

and commissioning activities. It also includes deploy marine vessels such as work barges,

accommodation vessels, crew boats, anchor handling tug supply vessels which are regarded as

part of marine spread activities. Business has steadily grown in recent years from just a

manpower service provider to dynamic and emerging contractor in integrated maintenance,

rejuvenation and hook-up and commissioning (HUC) of both offshore and onshore in oil and gas

support industries.

Till date, Carimin Petroleum Berhad had completed projects of more than RM1 billion

and has diversified portfolio of reputed clients. These clients include PETRONAS Carigali,

Murphy Oil, Repsol, Exxon Mobil and many other clients. The corporate structure of company is

drawn below-

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

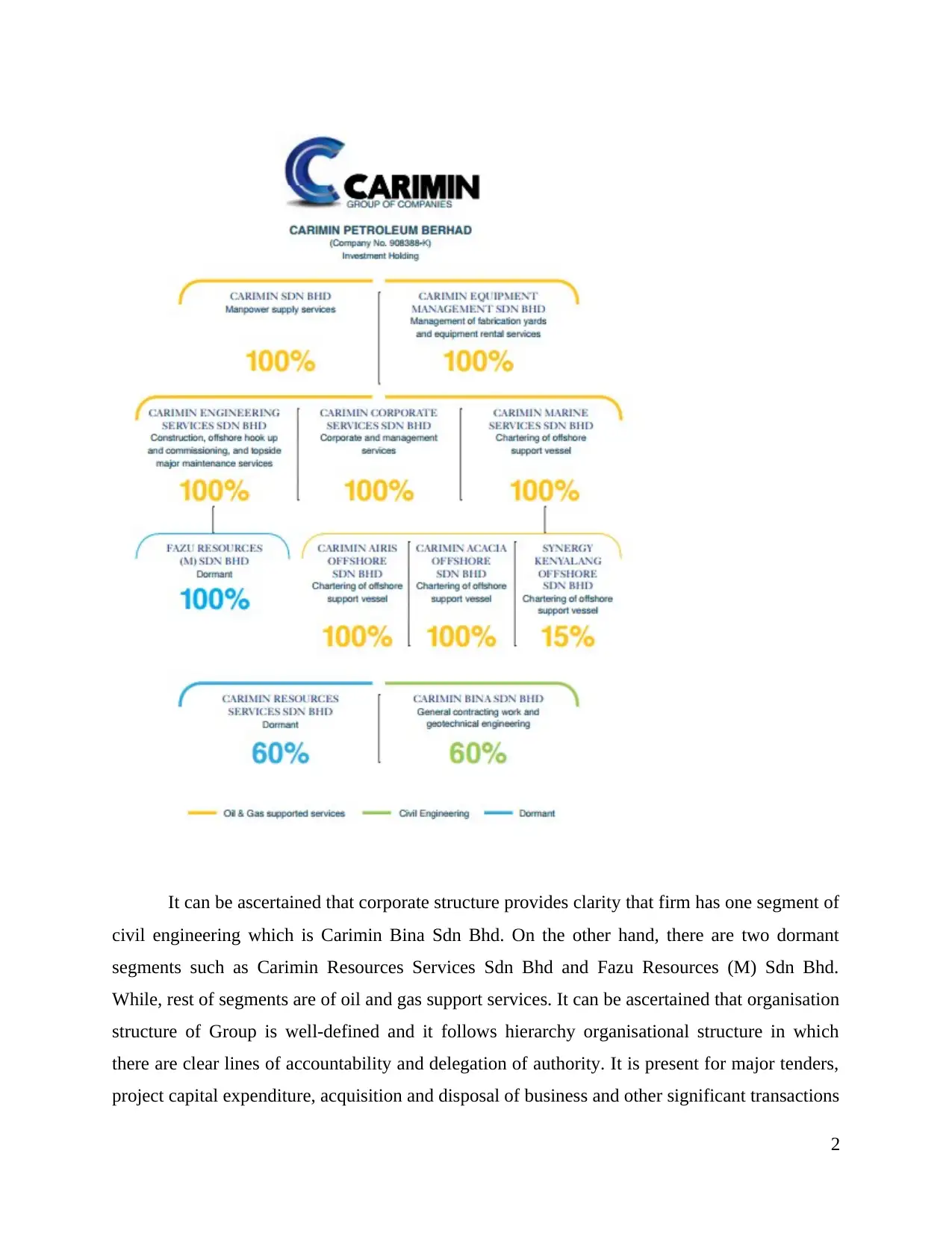

It can be ascertained that corporate structure provides clarity that firm has one segment of

civil engineering which is Carimin Bina Sdn Bhd. On the other hand, there are two dormant

segments such as Carimin Resources Services Sdn Bhd and Fazu Resources (M) Sdn Bhd.

While, rest of segments are of oil and gas support services. It can be ascertained that organisation

structure of Group is well-defined and it follows hierarchy organisational structure in which

there are clear lines of accountability and delegation of authority. It is present for major tenders,

project capital expenditure, acquisition and disposal of business and other significant transactions

2

civil engineering which is Carimin Bina Sdn Bhd. On the other hand, there are two dormant

segments such as Carimin Resources Services Sdn Bhd and Fazu Resources (M) Sdn Bhd.

While, rest of segments are of oil and gas support services. It can be ascertained that organisation

structure of Group is well-defined and it follows hierarchy organisational structure in which

there are clear lines of accountability and delegation of authority. It is present for major tenders,

project capital expenditure, acquisition and disposal of business and other significant transactions

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

requiring approval of Board. Management team is effectively led Managing Director and assisted

by Executive Directors with particular heads of departments. Responsible and competent

personnel is recruited for overseeing better operational functions.

The Group has clearly defined policies and procedures along with limit of authority under

each head. This has led to attain and promote transparency, responsibility, operational efficiency

and better corporate governance in the best manner possible. It can be said that business provides

variety of support services to clients in the industry and management is liable to perform

adequately so that better results may be attained. Moreover, management structure of Carimin

Petroleum Berhad is well-defined and responsibilities are effectively delegated to employees by

Board of Directors.

MAIN BODY

1. Describing on how to determine basis period and year of assessment

The income tax computation under the Malaysian law prescribed by MASB (Malaysian

Accounting Standards Board) can be used for identifying and determining basis period.

Company that have qualified for group relief may surrender maximum of 70 % of its adjusted

loss for year of assessment to either one or more than one companies (Faizal & et.al., 2017).

With the effect of year of assessment 2019, period in which organisation may surrender its

adjusted loss is limited to starting 3 consecutive years of assessment after completion of its first

12-month basis period from commencement of operational activities of organisation.

The basis period is termed as the time period for which company pays out tax each year.

The basis period is however the same as its accounting year (Kiow, Salleh & Kassim, 2017).

Carimin Petroleum Berhad is one of the largest company engaged in energy sector listed on

Bursa Malaysia also determines basis period. Financial year of 2018 has been ended on 30 June

2018. In relation to this, basis period is determined from 1 May 2017 to 30 June 2018. This is

evident from the Section 21A of Income Tax Act 1967 which is used for company, limited

liability partnership (LLP), trust or cooperative soceity. According to Subsection (2) of Section

21A, where set of accounts have been made for the period of 12 months ending on day other than

31 December, such period is to be constituted as basis period for YA (Year of Assessment).

According to Subsection (4) which has been in effect from YA 2014 has simplified

determination of basis periods upon commencement of operations. When an entity set its first

3

by Executive Directors with particular heads of departments. Responsible and competent

personnel is recruited for overseeing better operational functions.

The Group has clearly defined policies and procedures along with limit of authority under

each head. This has led to attain and promote transparency, responsibility, operational efficiency

and better corporate governance in the best manner possible. It can be said that business provides

variety of support services to clients in the industry and management is liable to perform

adequately so that better results may be attained. Moreover, management structure of Carimin

Petroleum Berhad is well-defined and responsibilities are effectively delegated to employees by

Board of Directors.

MAIN BODY

1. Describing on how to determine basis period and year of assessment

The income tax computation under the Malaysian law prescribed by MASB (Malaysian

Accounting Standards Board) can be used for identifying and determining basis period.

Company that have qualified for group relief may surrender maximum of 70 % of its adjusted

loss for year of assessment to either one or more than one companies (Faizal & et.al., 2017).

With the effect of year of assessment 2019, period in which organisation may surrender its

adjusted loss is limited to starting 3 consecutive years of assessment after completion of its first

12-month basis period from commencement of operational activities of organisation.

The basis period is termed as the time period for which company pays out tax each year.

The basis period is however the same as its accounting year (Kiow, Salleh & Kassim, 2017).

Carimin Petroleum Berhad is one of the largest company engaged in energy sector listed on

Bursa Malaysia also determines basis period. Financial year of 2018 has been ended on 30 June

2018. In relation to this, basis period is determined from 1 May 2017 to 30 June 2018. This is

evident from the Section 21A of Income Tax Act 1967 which is used for company, limited

liability partnership (LLP), trust or cooperative soceity. According to Subsection (2) of Section

21A, where set of accounts have been made for the period of 12 months ending on day other than

31 December, such period is to be constituted as basis period for YA (Year of Assessment).

According to Subsection (4) which has been in effect from YA 2014 has simplified

determination of basis periods upon commencement of operations. When an entity set its first

3

accounts which falls in first, second or third year YA after date of commencement, period

covered by accounts is accepted as basis period for first applicable YA. In addition to this, YA's

before that YA will then deemed to have no basis periods. On the other hand, YA can be

determined as per the company's choice as Companies Act 2016 does not make specification

regarding date in which financial year may be commenced or end. Directors of company is

obliged to prepare financial statements within 18 months after incorporation of organisation.

Moreover, in subsequent 6 months of financial year-end for submitting reports with Companies

Commission of Malaysia. It should be determined by looking on business cycle and taxation

period as there are complications especially when closing falls in March, June, September and

December because audit fees are not easy to be negotiated.

2. Explaining elements in computing the chargeable income

1. Capital expenditure

The capital expenditure is termed as funds which are being invested or used by

organisation in maintaining or acquiring fixed assets like land and buildings, equipments. In

accordance to Malaysia, deductions are allowed under chargeable income for any revenue

expenditure incurred on wholly or exclusively in production of income (Malaysia Publishes

Guidance on Qualifying Expenditure and Computation of Capital Allowances. 2015). However,

no deduction is allowed under preliminary costs, capital expenditure, floatation costs registration,

winding up or liquidation of corporation unless specifically permitted by Income Tax Act 1967

or order by Malaysian Ministries. However, tax incentives would be provided for encouraging

transformation to IoT, robots and big data analytics by manufacturing and service sector (Pui

Yee, Moorthy & Choo Keng Soon, 2017). Capital allowances will be provided on first RM 10

million of qualifying capital expenditure incurred during YA 2018 to 2020 with fully claimable

within two YA.

Plans are underway for developing five-acre yard into integrated facility that will include

better blasting and painting activities leading to enhance capability of Carimin Petroleum Berhad

in the best manner possible. Capital expenditure for this purpose will be financed on partial basis

from listing proceeds. On the other hand, Carimin Petroleum Berhad uses segment capital

expenditure for acquiring plant and equipment and which does not include goodwill.

2. Capital gain

4

covered by accounts is accepted as basis period for first applicable YA. In addition to this, YA's

before that YA will then deemed to have no basis periods. On the other hand, YA can be

determined as per the company's choice as Companies Act 2016 does not make specification

regarding date in which financial year may be commenced or end. Directors of company is

obliged to prepare financial statements within 18 months after incorporation of organisation.

Moreover, in subsequent 6 months of financial year-end for submitting reports with Companies

Commission of Malaysia. It should be determined by looking on business cycle and taxation

period as there are complications especially when closing falls in March, June, September and

December because audit fees are not easy to be negotiated.

2. Explaining elements in computing the chargeable income

1. Capital expenditure

The capital expenditure is termed as funds which are being invested or used by

organisation in maintaining or acquiring fixed assets like land and buildings, equipments. In

accordance to Malaysia, deductions are allowed under chargeable income for any revenue

expenditure incurred on wholly or exclusively in production of income (Malaysia Publishes

Guidance on Qualifying Expenditure and Computation of Capital Allowances. 2015). However,

no deduction is allowed under preliminary costs, capital expenditure, floatation costs registration,

winding up or liquidation of corporation unless specifically permitted by Income Tax Act 1967

or order by Malaysian Ministries. However, tax incentives would be provided for encouraging

transformation to IoT, robots and big data analytics by manufacturing and service sector (Pui

Yee, Moorthy & Choo Keng Soon, 2017). Capital allowances will be provided on first RM 10

million of qualifying capital expenditure incurred during YA 2018 to 2020 with fully claimable

within two YA.

Plans are underway for developing five-acre yard into integrated facility that will include

better blasting and painting activities leading to enhance capability of Carimin Petroleum Berhad

in the best manner possible. Capital expenditure for this purpose will be financed on partial basis

from listing proceeds. On the other hand, Carimin Petroleum Berhad uses segment capital

expenditure for acquiring plant and equipment and which does not include goodwill.

2. Capital gain

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is known as the rise in the value of capital asset (investment or real estate) that gives

higher worth than the purchase price of capital asset. Gain is never realised unless it is sold.

Capital gain may be of short-term ranging to one year or long-term of more than one year. It is

required to get claim on income taxes. However, Malaysia does not charge or tax capital gains

from the sale of capital assets or investments other than land and buildings. In relation to this,

real property gains tax applies to sale of land in Malaysia only. It includes gains from the sale of

shares in controlled company whose holdings of real property or shares amount to at least 75 %

of more of its tangible assets (Hamzah, Tokimatsu & Yoshikawa, 2017.).

The rate for disposals of real property is 30 % and that too made within 3 years of

acquisition date. Moreover, such rates are reduced subsequently after 3 years. This is evident

from the fact that rates stipulated are 20 % in fourth year and is 15 % for disposals after five

years of acquisition which is further decreased to 5 % after sixth year post-acquisition. This

means that Malaysia does not have provision for capital gains tax but it is made to real property

of some classes.

3. Capital loss

The capital losses are those which are opposite of capital gains. In simple words, when

purchase price of capital asset is more than its selling price, loss is occurred for the entity. This

highlights that business is required to make proper evaluation regarding disposals in order to

avoid losses up to a major extent. On the other hand, treatment of capital losses arising from sale

of real property can be used for offsetting against capital gains earned from such sales with ease.

Gains resulting from such real property disposal acquired are mandatorily exempted from the tax

as are asset transfer by domestic companies of Malaysia approved under restructuring scheme.

Carimin Petroleum Berhad falls under title of domestic company.

Capital losses can be effectively offset as against capital gains made by company. It can

be ascertained that Carimin Petroleum Berhad with reference to financial assets has made clear

in annual report. The financial assets at fair value through profit or loss are stated at fair value

only with any gains or losses arising on remeasurement recognised in profit or loss (Bong &

et.al., 2017). Gains or losses arising from sale of financial assets are recognised in

comprehensive income and accumulated in fair value reserve. While, on de-recognition,

cumulative gain or loss already accumulated in such reserve is reclassified from equity into profit

or loss.

5

higher worth than the purchase price of capital asset. Gain is never realised unless it is sold.

Capital gain may be of short-term ranging to one year or long-term of more than one year. It is

required to get claim on income taxes. However, Malaysia does not charge or tax capital gains

from the sale of capital assets or investments other than land and buildings. In relation to this,

real property gains tax applies to sale of land in Malaysia only. It includes gains from the sale of

shares in controlled company whose holdings of real property or shares amount to at least 75 %

of more of its tangible assets (Hamzah, Tokimatsu & Yoshikawa, 2017.).

The rate for disposals of real property is 30 % and that too made within 3 years of

acquisition date. Moreover, such rates are reduced subsequently after 3 years. This is evident

from the fact that rates stipulated are 20 % in fourth year and is 15 % for disposals after five

years of acquisition which is further decreased to 5 % after sixth year post-acquisition. This

means that Malaysia does not have provision for capital gains tax but it is made to real property

of some classes.

3. Capital loss

The capital losses are those which are opposite of capital gains. In simple words, when

purchase price of capital asset is more than its selling price, loss is occurred for the entity. This

highlights that business is required to make proper evaluation regarding disposals in order to

avoid losses up to a major extent. On the other hand, treatment of capital losses arising from sale

of real property can be used for offsetting against capital gains earned from such sales with ease.

Gains resulting from such real property disposal acquired are mandatorily exempted from the tax

as are asset transfer by domestic companies of Malaysia approved under restructuring scheme.

Carimin Petroleum Berhad falls under title of domestic company.

Capital losses can be effectively offset as against capital gains made by company. It can

be ascertained that Carimin Petroleum Berhad with reference to financial assets has made clear

in annual report. The financial assets at fair value through profit or loss are stated at fair value

only with any gains or losses arising on remeasurement recognised in profit or loss (Bong &

et.al., 2017). Gains or losses arising from sale of financial assets are recognised in

comprehensive income and accumulated in fair value reserve. While, on de-recognition,

cumulative gain or loss already accumulated in such reserve is reclassified from equity into profit

or loss.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

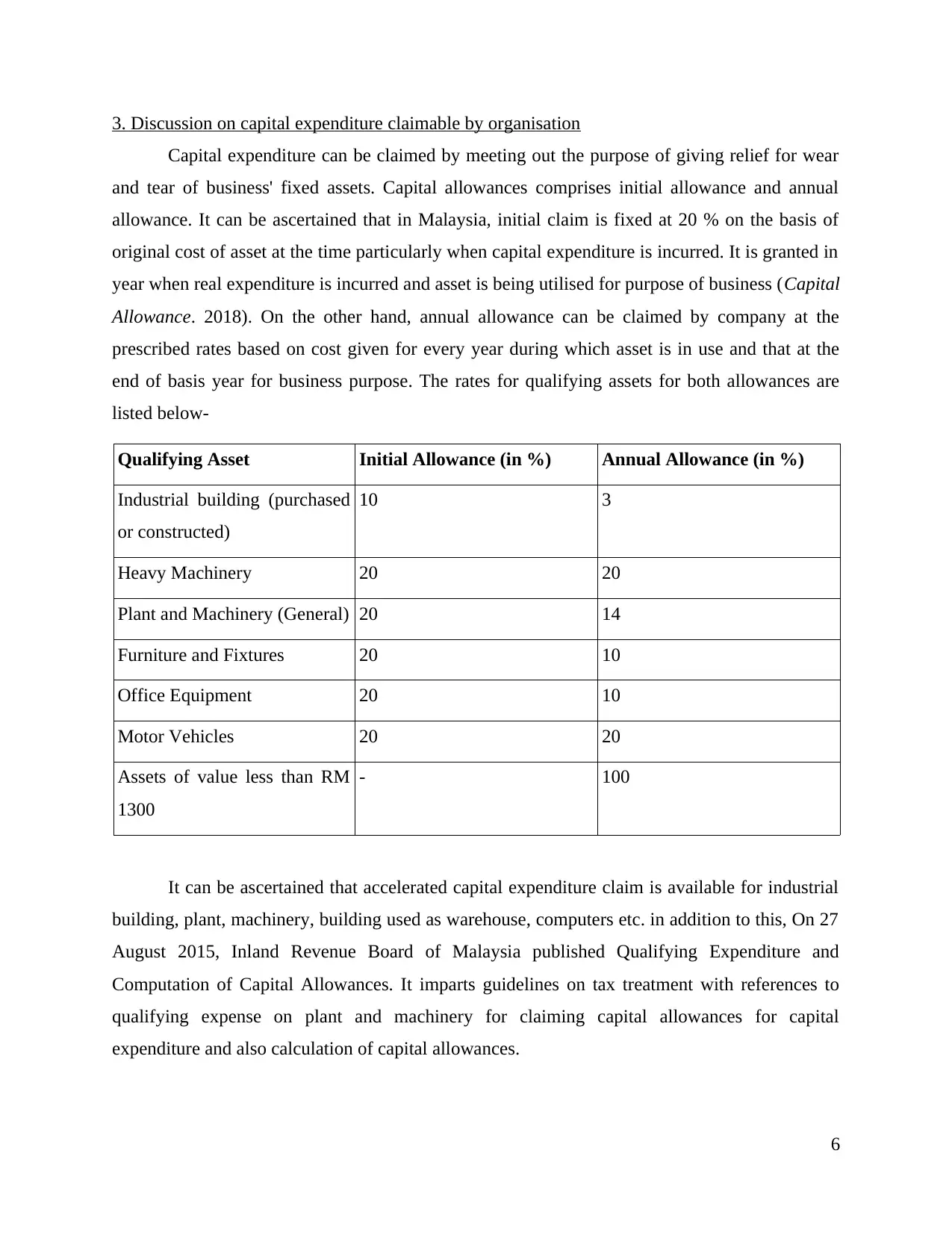

3. Discussion on capital expenditure claimable by organisation

Capital expenditure can be claimed by meeting out the purpose of giving relief for wear

and tear of business' fixed assets. Capital allowances comprises initial allowance and annual

allowance. It can be ascertained that in Malaysia, initial claim is fixed at 20 % on the basis of

original cost of asset at the time particularly when capital expenditure is incurred. It is granted in

year when real expenditure is incurred and asset is being utilised for purpose of business (Capital

Allowance. 2018). On the other hand, annual allowance can be claimed by company at the

prescribed rates based on cost given for every year during which asset is in use and that at the

end of basis year for business purpose. The rates for qualifying assets for both allowances are

listed below-

Qualifying Asset Initial Allowance (in %) Annual Allowance (in %)

Industrial building (purchased

or constructed)

10 3

Heavy Machinery 20 20

Plant and Machinery (General) 20 14

Furniture and Fixtures 20 10

Office Equipment 20 10

Motor Vehicles 20 20

Assets of value less than RM

1300

- 100

It can be ascertained that accelerated capital expenditure claim is available for industrial

building, plant, machinery, building used as warehouse, computers etc. in addition to this, On 27

August 2015, Inland Revenue Board of Malaysia published Qualifying Expenditure and

Computation of Capital Allowances. It imparts guidelines on tax treatment with references to

qualifying expense on plant and machinery for claiming capital allowances for capital

expenditure and also calculation of capital allowances.

6

Capital expenditure can be claimed by meeting out the purpose of giving relief for wear

and tear of business' fixed assets. Capital allowances comprises initial allowance and annual

allowance. It can be ascertained that in Malaysia, initial claim is fixed at 20 % on the basis of

original cost of asset at the time particularly when capital expenditure is incurred. It is granted in

year when real expenditure is incurred and asset is being utilised for purpose of business (Capital

Allowance. 2018). On the other hand, annual allowance can be claimed by company at the

prescribed rates based on cost given for every year during which asset is in use and that at the

end of basis year for business purpose. The rates for qualifying assets for both allowances are

listed below-

Qualifying Asset Initial Allowance (in %) Annual Allowance (in %)

Industrial building (purchased

or constructed)

10 3

Heavy Machinery 20 20

Plant and Machinery (General) 20 14

Furniture and Fixtures 20 10

Office Equipment 20 10

Motor Vehicles 20 20

Assets of value less than RM

1300

- 100

It can be ascertained that accelerated capital expenditure claim is available for industrial

building, plant, machinery, building used as warehouse, computers etc. in addition to this, On 27

August 2015, Inland Revenue Board of Malaysia published Qualifying Expenditure and

Computation of Capital Allowances. It imparts guidelines on tax treatment with references to

qualifying expense on plant and machinery for claiming capital allowances for capital

expenditure and also calculation of capital allowances.

6

Major areas covered under the publication with examples are qualifying expenditure

which include details for incidental expenditures, vehicles, hire purchase assets, assets used

previously for non-official purposes. It also includes detail for asset installation services,

expenditure on dismantling and removing assets, foreign exchange differences which arises from

abroad loans for providing funding for purchase of plant and machinery. Another area is persons

eligible for claiming capital allowances when qualifying expenditure is incurred. Moreover, rules

for assets with expected life of below two years.

The operating segments of Carimin Petroleum Berhad consists of MPS (Manpower

Services) and CHUCTMM (Construction, Hook Up and Commissioning as well as Topside

Major Maintenance) which are two main customers of Group. The capital expenditure is PPE

(Property, Plant and Equipment) which was RM 59000 for MPS and RM 113000 for

CHUCTMM. While, MS (Marine Services) consists of capital expenditure of RM 253000 and

others are RM 23000 making it total to RM 448000 of whole Group (Annual Report of Carimin

Petroleum Berhad. 2018). For the year ended 2018, CC (Civil Construction) is not incurred

heading towards expenditure.

The capital expenditure starting from YA 2001, limitation amount for qualifying plant

expenditure for motor vehicle has been increased from RM 50,000 to RM 100,000 on condition

that motor vehicle bought is new one and on road price of purchase does not exceed RM 150,000

(Taxation and Investment in Malaysia 2018. 2018). It can be referred to example that when new

truck is purchased by Carimin Petroleum Berhad at cost of RM 40,000 which increases book

value of assets to the same amount. This amount has to recorded under cash flow statement as

capital expenditure under investing activities, then gradually truck depreciates over the years.

Thus, as per the law, truck which is acquired at a cost of RM 40,000 does not qualify as claim

under capital expenditure.

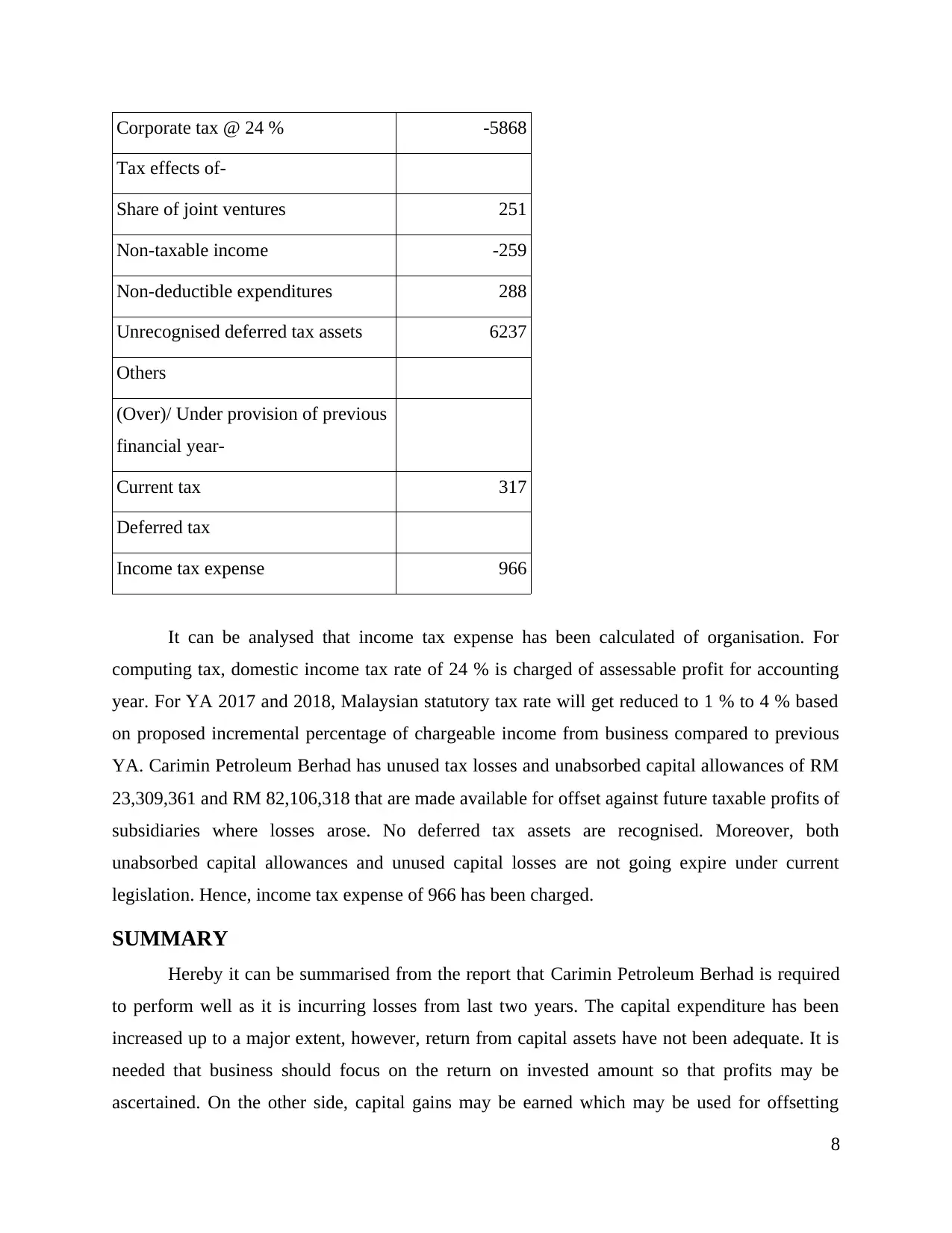

4. Computation of tax payable with the help of annual report of company

Computation of income tax payable by Carimin Petroleum Berhad

Particulars

2018

(In RM'000)

(Loss)/ Profit before tax -24452

7

which include details for incidental expenditures, vehicles, hire purchase assets, assets used

previously for non-official purposes. It also includes detail for asset installation services,

expenditure on dismantling and removing assets, foreign exchange differences which arises from

abroad loans for providing funding for purchase of plant and machinery. Another area is persons

eligible for claiming capital allowances when qualifying expenditure is incurred. Moreover, rules

for assets with expected life of below two years.

The operating segments of Carimin Petroleum Berhad consists of MPS (Manpower

Services) and CHUCTMM (Construction, Hook Up and Commissioning as well as Topside

Major Maintenance) which are two main customers of Group. The capital expenditure is PPE

(Property, Plant and Equipment) which was RM 59000 for MPS and RM 113000 for

CHUCTMM. While, MS (Marine Services) consists of capital expenditure of RM 253000 and

others are RM 23000 making it total to RM 448000 of whole Group (Annual Report of Carimin

Petroleum Berhad. 2018). For the year ended 2018, CC (Civil Construction) is not incurred

heading towards expenditure.

The capital expenditure starting from YA 2001, limitation amount for qualifying plant

expenditure for motor vehicle has been increased from RM 50,000 to RM 100,000 on condition

that motor vehicle bought is new one and on road price of purchase does not exceed RM 150,000

(Taxation and Investment in Malaysia 2018. 2018). It can be referred to example that when new

truck is purchased by Carimin Petroleum Berhad at cost of RM 40,000 which increases book

value of assets to the same amount. This amount has to recorded under cash flow statement as

capital expenditure under investing activities, then gradually truck depreciates over the years.

Thus, as per the law, truck which is acquired at a cost of RM 40,000 does not qualify as claim

under capital expenditure.

4. Computation of tax payable with the help of annual report of company

Computation of income tax payable by Carimin Petroleum Berhad

Particulars

2018

(In RM'000)

(Loss)/ Profit before tax -24452

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate tax @ 24 % -5868

Tax effects of-

Share of joint ventures 251

Non-taxable income -259

Non-deductible expenditures 288

Unrecognised deferred tax assets 6237

Others

(Over)/ Under provision of previous

financial year-

Current tax 317

Deferred tax

Income tax expense 966

It can be analysed that income tax expense has been calculated of organisation. For

computing tax, domestic income tax rate of 24 % is charged of assessable profit for accounting

year. For YA 2017 and 2018, Malaysian statutory tax rate will get reduced to 1 % to 4 % based

on proposed incremental percentage of chargeable income from business compared to previous

YA. Carimin Petroleum Berhad has unused tax losses and unabsorbed capital allowances of RM

23,309,361 and RM 82,106,318 that are made available for offset against future taxable profits of

subsidiaries where losses arose. No deferred tax assets are recognised. Moreover, both

unabsorbed capital allowances and unused capital losses are not going expire under current

legislation. Hence, income tax expense of 966 has been charged.

SUMMARY

Hereby it can be summarised from the report that Carimin Petroleum Berhad is required

to perform well as it is incurring losses from last two years. The capital expenditure has been

increased up to a major extent, however, return from capital assets have not been adequate. It is

needed that business should focus on the return on invested amount so that profits may be

ascertained. On the other side, capital gains may be earned which may be used for offsetting

8

Tax effects of-

Share of joint ventures 251

Non-taxable income -259

Non-deductible expenditures 288

Unrecognised deferred tax assets 6237

Others

(Over)/ Under provision of previous

financial year-

Current tax 317

Deferred tax

Income tax expense 966

It can be analysed that income tax expense has been calculated of organisation. For

computing tax, domestic income tax rate of 24 % is charged of assessable profit for accounting

year. For YA 2017 and 2018, Malaysian statutory tax rate will get reduced to 1 % to 4 % based

on proposed incremental percentage of chargeable income from business compared to previous

YA. Carimin Petroleum Berhad has unused tax losses and unabsorbed capital allowances of RM

23,309,361 and RM 82,106,318 that are made available for offset against future taxable profits of

subsidiaries where losses arose. No deferred tax assets are recognised. Moreover, both

unabsorbed capital allowances and unused capital losses are not going expire under current

legislation. Hence, income tax expense of 966 has been charged.

SUMMARY

Hereby it can be summarised from the report that Carimin Petroleum Berhad is required

to perform well as it is incurring losses from last two years. The capital expenditure has been

increased up to a major extent, however, return from capital assets have not been adequate. It is

needed that business should focus on the return on invested amount so that profits may be

ascertained. On the other side, capital gains may be earned which may be used for offsetting

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capital losses in a better manner. Carimin Petroleum Berhad is largest and oldest petroleum

company engaged in energy sector. All of its subsidiaries and operational segments are required

to be performed adequately in order to maximise profits and minimise losses. Furthermore, it is

needed that business may be able to attain higher growth and expand itself by acquiring more oil

and gas organisations.

Income tax computation at Malaysian statutory rate of 24 % has been applied and RM

966 has been charged. However, company has incurred loss requires implementing higher

strategies and newer business model for eradicating losses. Basis period and YA both have been

determined which is used for tax computation by corporate. Elements such as capital

expenditure, capital loss and capital gain have been explained along with treatment for attaining

chargeable income. Capital expenditure claimable by Carimin Petroleum Berhad has also been

analysed. Thus, it can be summarised that tax computation is one of the important element which

is required to be done in coherent manner by referring to MASB provisions and Income Tax Act

1967 so that correct computation may be made. Furthermore, deductions and incentives if any

can also be adjusted with the help of abiding by law. Hence, proper tax computation is the

liability of business and make proper filing to income tax authority of Malaysia.

9

company engaged in energy sector. All of its subsidiaries and operational segments are required

to be performed adequately in order to maximise profits and minimise losses. Furthermore, it is

needed that business may be able to attain higher growth and expand itself by acquiring more oil

and gas organisations.

Income tax computation at Malaysian statutory rate of 24 % has been applied and RM

966 has been charged. However, company has incurred loss requires implementing higher

strategies and newer business model for eradicating losses. Basis period and YA both have been

determined which is used for tax computation by corporate. Elements such as capital

expenditure, capital loss and capital gain have been explained along with treatment for attaining

chargeable income. Capital expenditure claimable by Carimin Petroleum Berhad has also been

analysed. Thus, it can be summarised that tax computation is one of the important element which

is required to be done in coherent manner by referring to MASB provisions and Income Tax Act

1967 so that correct computation may be made. Furthermore, deductions and incentives if any

can also be adjusted with the help of abiding by law. Hence, proper tax computation is the

liability of business and make proper filing to income tax authority of Malaysia.

9

REFERENCES

Books and Journals

Bong, C.P.C & et.al., 2017. Review on the renewable energy and solid waste management

policies towards biogas development in Malaysia. Renewable and Sustainable Energy

Reviews. 70. pp.988-998.

Faizal, S. M & et.al., 2017. Perception on justice, trust and tax compliance behavior in

Malaysia. Kasetsart Journal of Social Sciences. 38(3). pp.226-232.

Hamzah, N., Tokimatsu, K. & Yoshikawa, K., 2017. Prospective for power generation of solid

fuel from hydrothermal treatment of biomass and waste in Malaysia.Energy Procedia. 142.

pp.369-373.

Kiow, T. S., Salleh, M.F.M. & Kassim, A.A.B.M., 2017. The determinants of individual

taxpayers’ tax compliance behaviour in peninsular malaysia. International Business and

Accounting Research Journal. 1(1). pp.26-43.

Pui Yee, C., Moorthy, K. & Choo Keng Soon, W., 2017. Taxpayers’ perceptions on tax evasion

behaviour: an empirical study in Malaysia. International Journal of Law and

Management. 59(3). pp.413-429.

Online

Annual Report of Carimin Petroleum Berhad. 2018 [PDF]. Available Through:

<http://disclosure.bursamalaysia.com/FileAccess/apbursaweb/download?

id=190080&name=EA_DS_ATTACHMENTS>.

Capital Allowance. 2018 [Online]. Available Through:

<http://taxsummaries.pwc.com/ID/Malaysia-Corporate-Deductions>.

Malaysia Publishes Guidance on Qualifying Expenditure and Computation of Capital

Allowances. 2015 [Online]. Available Through:

<https://www.orbitax.com/news/archive.php/Malaysia-Publishes-Guidance-on-18808>.

Taxation and Investment in Malaysia 2018. 2018 [PDF]. Available Through:

<https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

malaysiaguide-2018.pdf>.

10

Books and Journals

Bong, C.P.C & et.al., 2017. Review on the renewable energy and solid waste management

policies towards biogas development in Malaysia. Renewable and Sustainable Energy

Reviews. 70. pp.988-998.

Faizal, S. M & et.al., 2017. Perception on justice, trust and tax compliance behavior in

Malaysia. Kasetsart Journal of Social Sciences. 38(3). pp.226-232.

Hamzah, N., Tokimatsu, K. & Yoshikawa, K., 2017. Prospective for power generation of solid

fuel from hydrothermal treatment of biomass and waste in Malaysia.Energy Procedia. 142.

pp.369-373.

Kiow, T. S., Salleh, M.F.M. & Kassim, A.A.B.M., 2017. The determinants of individual

taxpayers’ tax compliance behaviour in peninsular malaysia. International Business and

Accounting Research Journal. 1(1). pp.26-43.

Pui Yee, C., Moorthy, K. & Choo Keng Soon, W., 2017. Taxpayers’ perceptions on tax evasion

behaviour: an empirical study in Malaysia. International Journal of Law and

Management. 59(3). pp.413-429.

Online

Annual Report of Carimin Petroleum Berhad. 2018 [PDF]. Available Through:

<http://disclosure.bursamalaysia.com/FileAccess/apbursaweb/download?

id=190080&name=EA_DS_ATTACHMENTS>.

Capital Allowance. 2018 [Online]. Available Through:

<http://taxsummaries.pwc.com/ID/Malaysia-Corporate-Deductions>.

Malaysia Publishes Guidance on Qualifying Expenditure and Computation of Capital

Allowances. 2015 [Online]. Available Through:

<https://www.orbitax.com/news/archive.php/Malaysia-Publishes-Guidance-on-18808>.

Taxation and Investment in Malaysia 2018. 2018 [PDF]. Available Through:

<https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

malaysiaguide-2018.pdf>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.