Financial Analysis and Auditing of Carnarvon Petroleum (2019)

VerifiedAdded on 2022/09/26

|13

|2293

|15

Report

AI Summary

This report analyzes the audit of Carnarvon Petroleum, focusing on the 2019 annual report. It examines the concept of materiality, detailing the levels used by the auditor, Ernst & Young, and its application to Carnarvon Petroleum's financial statements. The report includes a financial statement analysis, measuring profitability, solvency, and efficiency ratios from 2016 to 2019 to assess the company's financial position. It also reviews the cash flow statements, highlighting significant inflows and outflows, particularly in investment activities. The analysis reveals the company's financial challenges, including reduced profit margins and below-average financial leverage, and discusses the auditor's assertions regarding completeness, existence, and valuations. The report concludes by emphasizing the importance of the auditor's role in safeguarding stakeholder interests, given the company's financial performance.

Running head: AUDITUING AND ASSURANCE

AUDITUING AND ASSURANCE

Name of Student

Name of University

Author’s Note

AUDITUING AND ASSURANCE

Name of Student

Name of University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITUING AND ASSURANCE

AUDITUING AND ASSURANCE

2

AUDITUING AND ASSURANCE

INTRODUCTION:

The report discusses about the level of materiality that Australian petroleum and oil and

Gas Company, Carnarvon Petroleum uses in representing their 2019 annual report. In order to

identify the financial positions of the company various financial ratios are also being

incorporated. The report also indicates the total amount of cash inflows and total amount of cash

outflows from the financial statements of the company.

Carnarvon Petroleum is an Australian company which was founded in late 1983. The

company mainly deals with petroleum, oil and gas. The company is famous for innovating new

products that suffice the demand of oil and petroleum. The company spends considerable amount

of investments in technological development, so that they can discover more new products. The

company is a listed company in the Australian Stock Exchange under the name CVN. As per the

2018 annual report the company gained total $14.25 million. Though certain uncertain

circumstances the income turned into loss in the year 2019. In spite of facing loss the company

still possess current assets of $74,667,000. In order to identify more on the financial positions of

the company financial ratios are being measured.

MATERIALITY OF CARNARVON PETROLEUM:

Materiality is considered as the concept of convention in auditing and accounting. The

convention of auditing is mainly related to the transaction or any kind of discrepancies of the

amount. Materiality of auditing comes into play when the auditor checks the financial statements

of the company (Cohen & Simnett, 2015). There are several levels of materiality that auditor

mainly uses to measures the materiality present in the financial statements of the company. The

first and foremost level of materiality is the planning materiality. In this level the auditor needs

AUDITUING AND ASSURANCE

INTRODUCTION:

The report discusses about the level of materiality that Australian petroleum and oil and

Gas Company, Carnarvon Petroleum uses in representing their 2019 annual report. In order to

identify the financial positions of the company various financial ratios are also being

incorporated. The report also indicates the total amount of cash inflows and total amount of cash

outflows from the financial statements of the company.

Carnarvon Petroleum is an Australian company which was founded in late 1983. The

company mainly deals with petroleum, oil and gas. The company is famous for innovating new

products that suffice the demand of oil and petroleum. The company spends considerable amount

of investments in technological development, so that they can discover more new products. The

company is a listed company in the Australian Stock Exchange under the name CVN. As per the

2018 annual report the company gained total $14.25 million. Though certain uncertain

circumstances the income turned into loss in the year 2019. In spite of facing loss the company

still possess current assets of $74,667,000. In order to identify more on the financial positions of

the company financial ratios are being measured.

MATERIALITY OF CARNARVON PETROLEUM:

Materiality is considered as the concept of convention in auditing and accounting. The

convention of auditing is mainly related to the transaction or any kind of discrepancies of the

amount. Materiality of auditing comes into play when the auditor checks the financial statements

of the company (Cohen & Simnett, 2015). There are several levels of materiality that auditor

mainly uses to measures the materiality present in the financial statements of the company. The

first and foremost level of materiality is the planning materiality. In this level the auditor needs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITUING AND ASSURANCE

to assume that the financial statements that the company has to offer contain some fraud or

unknown error, which can affect the decisions of the financial statement user. Thus, the primary

level of materiality guides the auditor to create a specific design of auditing procedures. The

second form of materiality is the performance materiality. In this step the auditor determines the

allowance for known and unknown error and fraud that is present in the financial statements of

the company. The auditor also multiplies the percentage of risks that presents in the financial

statements of the company with planning materiality. Thus, in this way the auditor can tolerable

misstatement. It can also be stated that 50% to 70% of planning materiality are mainly based on

the moderate risk at the financial statements level. The lower misstatement in the financial

statements enables the auditor to conduct the auditing by 100%. In case of Carnarvon Petroleum

the same thing happened.

As per the declaration made by the auditor, Ernst & Young, the materiality in the 2019

annual report of Carnarvon Petroleum is zero. The auditor checked the materiality of the

financial statements of Carnarvon Petroleum based on AASB 101 Presentation of Financial

Statements and AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors. In

order to identify the materiality of the financial statements of Carnarvon Petroleum, Ernst &

Young firstly uses planning materiality. In this step the auditor designed the auditing procedure

for analysing any kind of materiality in the financial statements of the company (Brown et al.,

2019). In the next step the auditor tries to identify the performance materiality, which in this case

was nowhere to be found. These are the reasons due to which the auditor of Carnarvon

Petroleum, Ernst and Young passed an unqualified audit report. As per auditor’s report of 2019

annual report of Carnarvon Petroleum, there was no act played by the company that may

compromises the auditor’s independence requirements, as mentioned in Corporations Act 2001.

AUDITUING AND ASSURANCE

to assume that the financial statements that the company has to offer contain some fraud or

unknown error, which can affect the decisions of the financial statement user. Thus, the primary

level of materiality guides the auditor to create a specific design of auditing procedures. The

second form of materiality is the performance materiality. In this step the auditor determines the

allowance for known and unknown error and fraud that is present in the financial statements of

the company. The auditor also multiplies the percentage of risks that presents in the financial

statements of the company with planning materiality. Thus, in this way the auditor can tolerable

misstatement. It can also be stated that 50% to 70% of planning materiality are mainly based on

the moderate risk at the financial statements level. The lower misstatement in the financial

statements enables the auditor to conduct the auditing by 100%. In case of Carnarvon Petroleum

the same thing happened.

As per the declaration made by the auditor, Ernst & Young, the materiality in the 2019

annual report of Carnarvon Petroleum is zero. The auditor checked the materiality of the

financial statements of Carnarvon Petroleum based on AASB 101 Presentation of Financial

Statements and AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors. In

order to identify the materiality of the financial statements of Carnarvon Petroleum, Ernst &

Young firstly uses planning materiality. In this step the auditor designed the auditing procedure

for analysing any kind of materiality in the financial statements of the company (Brown et al.,

2019). In the next step the auditor tries to identify the performance materiality, which in this case

was nowhere to be found. These are the reasons due to which the auditor of Carnarvon

Petroleum, Ernst and Young passed an unqualified audit report. As per auditor’s report of 2019

annual report of Carnarvon Petroleum, there was no act played by the company that may

compromises the auditor’s independence requirements, as mentioned in Corporations Act 2001.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITUING AND ASSURANCE

The auditor’s report of financial statements of Carnarvon Petroleum states that it has very less or

negligible risks and it does not contain any kind of performance materiality.

FINANCIAL STATEMENT ANALYSIS:

In order to identify the financial positions of Carnarvon Petroleum, 2019, 2018, 2017 and

2016 annual report has analysed. Both income statement and balance sheet ratios are being

measured. The ratios like profitability ratio, solvency ratio, efficiency ratio and turnover ratios

are being measured. The detailed analyses are mentioned below:

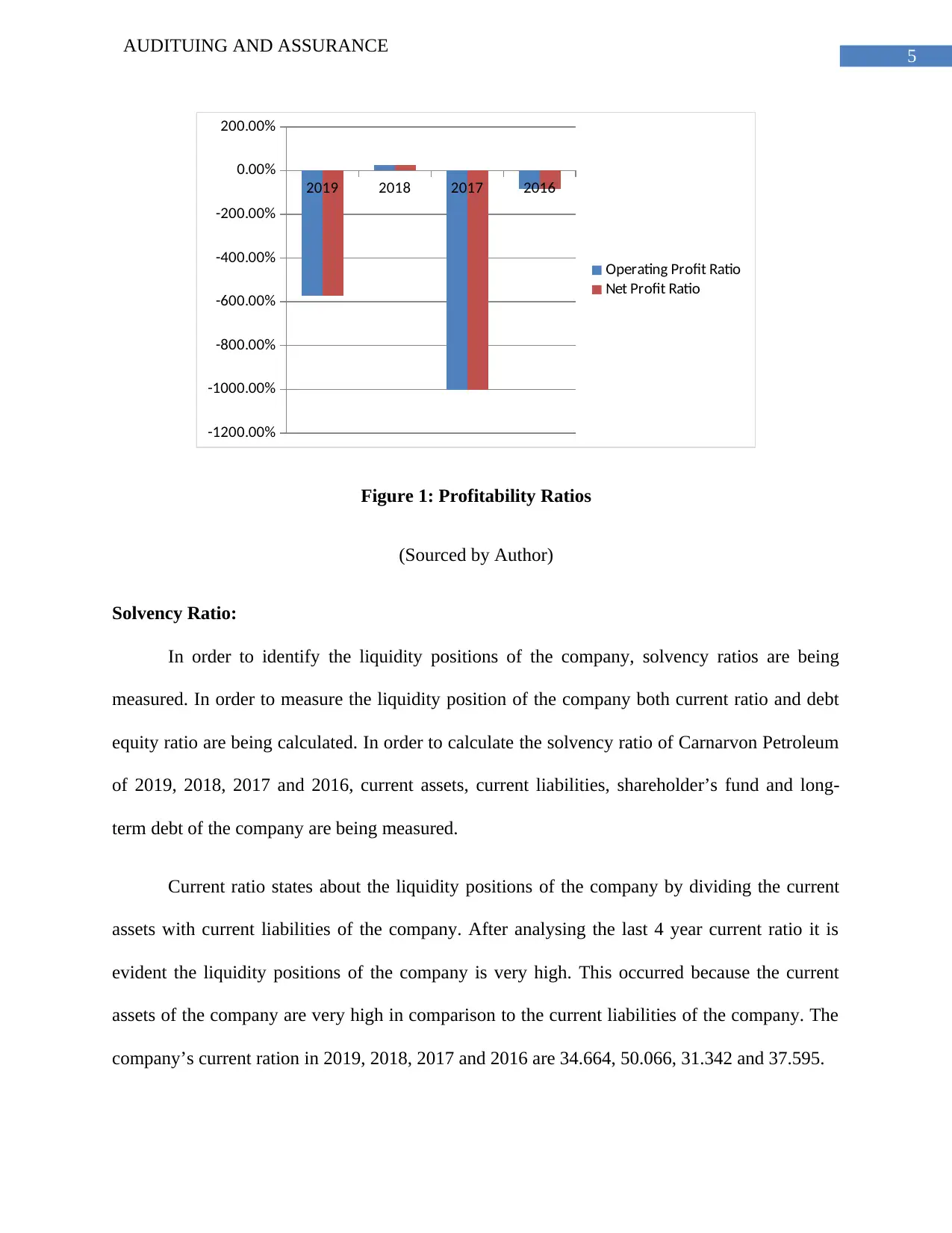

Profitability Ratio:

In order to identify the profitability of the company two profitability ratios are being

measured. They are operating profit ratio and net profit ratio. The operating profit ratio and net

profit both states the profit generating ability of the company. In order to measure the profit

generating ability of Carnarvon Petroleum the operating profit ratio and net profit ratio are being

measured from 2019 to 2016.

After analysing the operating profit ratio from 2019 to 2016, it can be stated that the

profit margin of the company reduced by considerable percentage. In 2019, the operating profit

of company is in negative whereas in 2018 it represents a high operating profit margin. In 2018

the operating profit margin was 25.15%. It is the only year in last 5 years where company was

successfully able to generate profit from the market. In 2017 and 2016 the company also fetched

loss from the market. Net profit margin ratio also shows same type of results. Thus, indicating

that the company’s financial positions are very poor and the management of the company needs

to implement several policies to increase the financial positions of the company.

AUDITUING AND ASSURANCE

The auditor’s report of financial statements of Carnarvon Petroleum states that it has very less or

negligible risks and it does not contain any kind of performance materiality.

FINANCIAL STATEMENT ANALYSIS:

In order to identify the financial positions of Carnarvon Petroleum, 2019, 2018, 2017 and

2016 annual report has analysed. Both income statement and balance sheet ratios are being

measured. The ratios like profitability ratio, solvency ratio, efficiency ratio and turnover ratios

are being measured. The detailed analyses are mentioned below:

Profitability Ratio:

In order to identify the profitability of the company two profitability ratios are being

measured. They are operating profit ratio and net profit ratio. The operating profit ratio and net

profit both states the profit generating ability of the company. In order to measure the profit

generating ability of Carnarvon Petroleum the operating profit ratio and net profit ratio are being

measured from 2019 to 2016.

After analysing the operating profit ratio from 2019 to 2016, it can be stated that the

profit margin of the company reduced by considerable percentage. In 2019, the operating profit

of company is in negative whereas in 2018 it represents a high operating profit margin. In 2018

the operating profit margin was 25.15%. It is the only year in last 5 years where company was

successfully able to generate profit from the market. In 2017 and 2016 the company also fetched

loss from the market. Net profit margin ratio also shows same type of results. Thus, indicating

that the company’s financial positions are very poor and the management of the company needs

to implement several policies to increase the financial positions of the company.

5

AUDITUING AND ASSURANCE

2019 2018 2017 2016

-1200.00%

-1000.00%

-800.00%

-600.00%

-400.00%

-200.00%

0.00%

200.00%

Operating Profit Ratio

Net Profit Ratio

Figure 1: Profitability Ratios

(Sourced by Author)

Solvency Ratio:

In order to identify the liquidity positions of the company, solvency ratios are being

measured. In order to measure the liquidity position of the company both current ratio and debt

equity ratio are being calculated. In order to calculate the solvency ratio of Carnarvon Petroleum

of 2019, 2018, 2017 and 2016, current assets, current liabilities, shareholder’s fund and long-

term debt of the company are being measured.

Current ratio states about the liquidity positions of the company by dividing the current

assets with current liabilities of the company. After analysing the last 4 year current ratio it is

evident the liquidity positions of the company is very high. This occurred because the current

assets of the company are very high in comparison to the current liabilities of the company. The

company’s current ration in 2019, 2018, 2017 and 2016 are 34.664, 50.066, 31.342 and 37.595.

AUDITUING AND ASSURANCE

2019 2018 2017 2016

-1200.00%

-1000.00%

-800.00%

-600.00%

-400.00%

-200.00%

0.00%

200.00%

Operating Profit Ratio

Net Profit Ratio

Figure 1: Profitability Ratios

(Sourced by Author)

Solvency Ratio:

In order to identify the liquidity positions of the company, solvency ratios are being

measured. In order to measure the liquidity position of the company both current ratio and debt

equity ratio are being calculated. In order to calculate the solvency ratio of Carnarvon Petroleum

of 2019, 2018, 2017 and 2016, current assets, current liabilities, shareholder’s fund and long-

term debt of the company are being measured.

Current ratio states about the liquidity positions of the company by dividing the current

assets with current liabilities of the company. After analysing the last 4 year current ratio it is

evident the liquidity positions of the company is very high. This occurred because the current

assets of the company are very high in comparison to the current liabilities of the company. The

company’s current ration in 2019, 2018, 2017 and 2016 are 34.664, 50.066, 31.342 and 37.595.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITUING AND ASSURANCE

2019 2018 2017 2016

-1200.00%

-1000.00%

-800.00%

-600.00%

-400.00%

-200.00%

0.00%

200.00%

Operating Profit Ratio

Net Profit Ratio

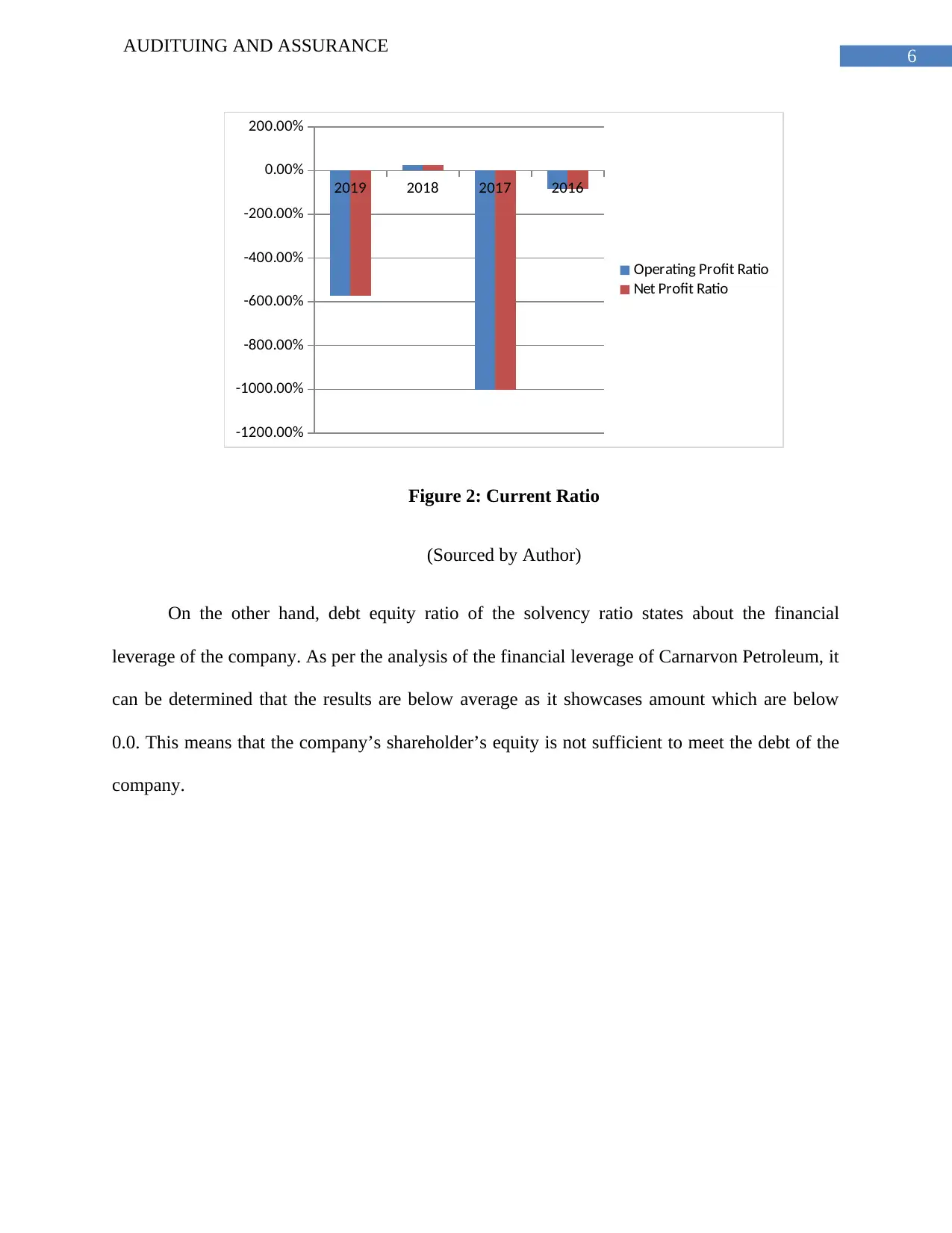

Figure 2: Current Ratio

(Sourced by Author)

On the other hand, debt equity ratio of the solvency ratio states about the financial

leverage of the company. As per the analysis of the financial leverage of Carnarvon Petroleum, it

can be determined that the results are below average as it showcases amount which are below

0.0. This means that the company’s shareholder’s equity is not sufficient to meet the debt of the

company.

AUDITUING AND ASSURANCE

2019 2018 2017 2016

-1200.00%

-1000.00%

-800.00%

-600.00%

-400.00%

-200.00%

0.00%

200.00%

Operating Profit Ratio

Net Profit Ratio

Figure 2: Current Ratio

(Sourced by Author)

On the other hand, debt equity ratio of the solvency ratio states about the financial

leverage of the company. As per the analysis of the financial leverage of Carnarvon Petroleum, it

can be determined that the results are below average as it showcases amount which are below

0.0. This means that the company’s shareholder’s equity is not sufficient to meet the debt of the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITUING AND ASSURANCE

2019 2018 2017 2016

0.000

0.005

0.010

0.015

0.020

0.025

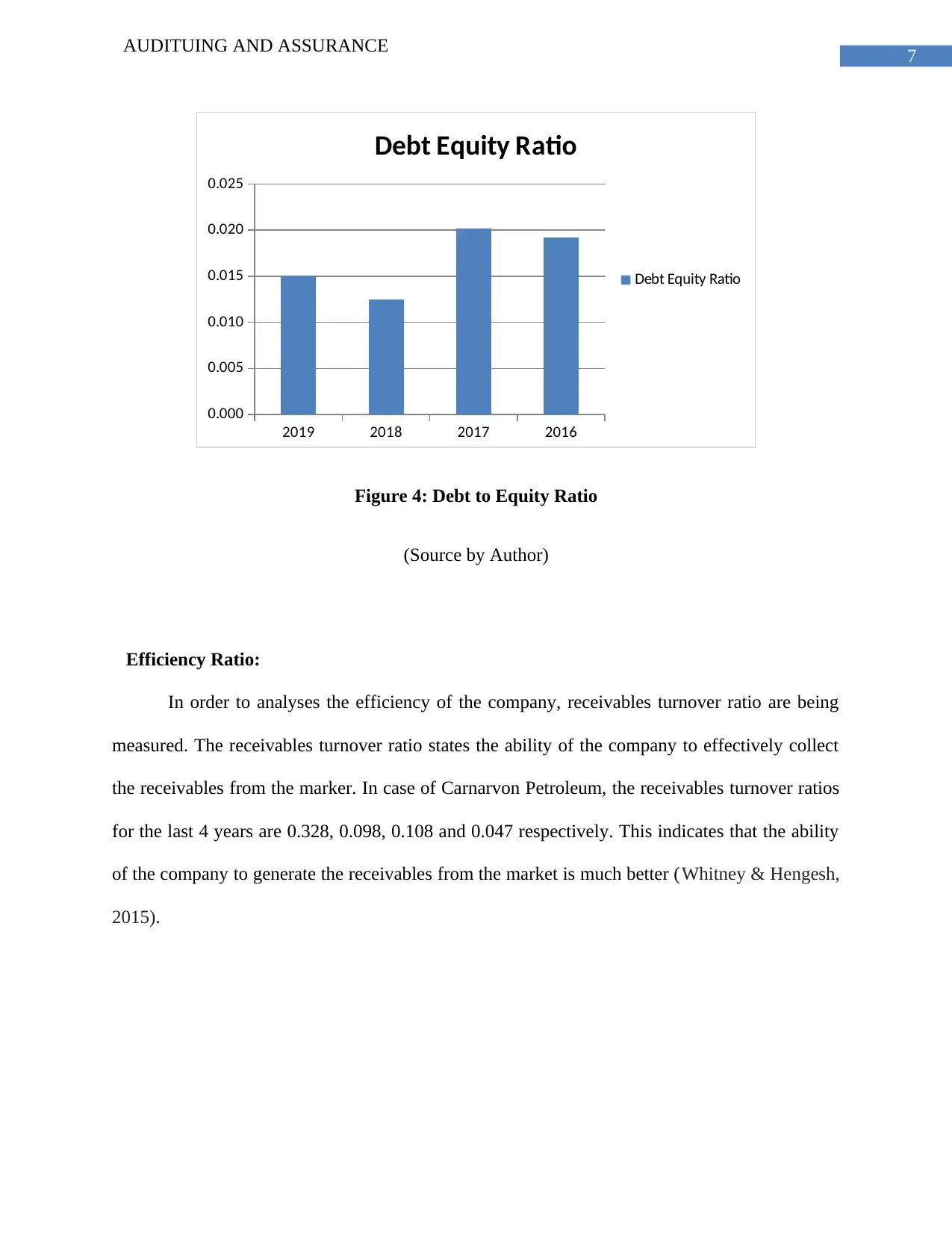

Debt Equity Ratio

Debt Equity Ratio

Figure 4: Debt to Equity Ratio

(Source by Author)

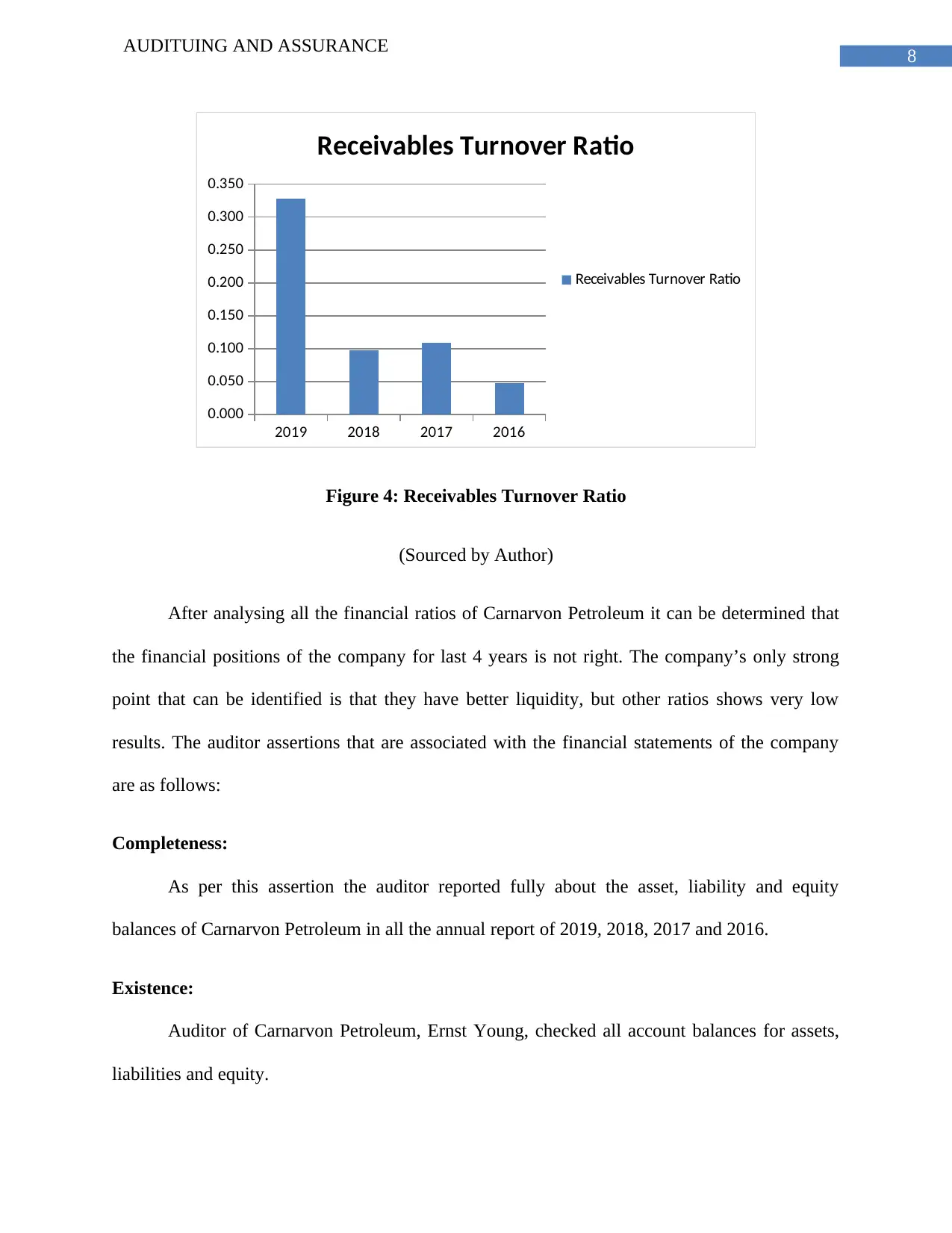

Efficiency Ratio:

In order to analyses the efficiency of the company, receivables turnover ratio are being

measured. The receivables turnover ratio states the ability of the company to effectively collect

the receivables from the marker. In case of Carnarvon Petroleum, the receivables turnover ratios

for the last 4 years are 0.328, 0.098, 0.108 and 0.047 respectively. This indicates that the ability

of the company to generate the receivables from the market is much better (Whitney & Hengesh,

2015).

AUDITUING AND ASSURANCE

2019 2018 2017 2016

0.000

0.005

0.010

0.015

0.020

0.025

Debt Equity Ratio

Debt Equity Ratio

Figure 4: Debt to Equity Ratio

(Source by Author)

Efficiency Ratio:

In order to analyses the efficiency of the company, receivables turnover ratio are being

measured. The receivables turnover ratio states the ability of the company to effectively collect

the receivables from the marker. In case of Carnarvon Petroleum, the receivables turnover ratios

for the last 4 years are 0.328, 0.098, 0.108 and 0.047 respectively. This indicates that the ability

of the company to generate the receivables from the market is much better (Whitney & Hengesh,

2015).

8

AUDITUING AND ASSURANCE

2019 2018 2017 2016

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

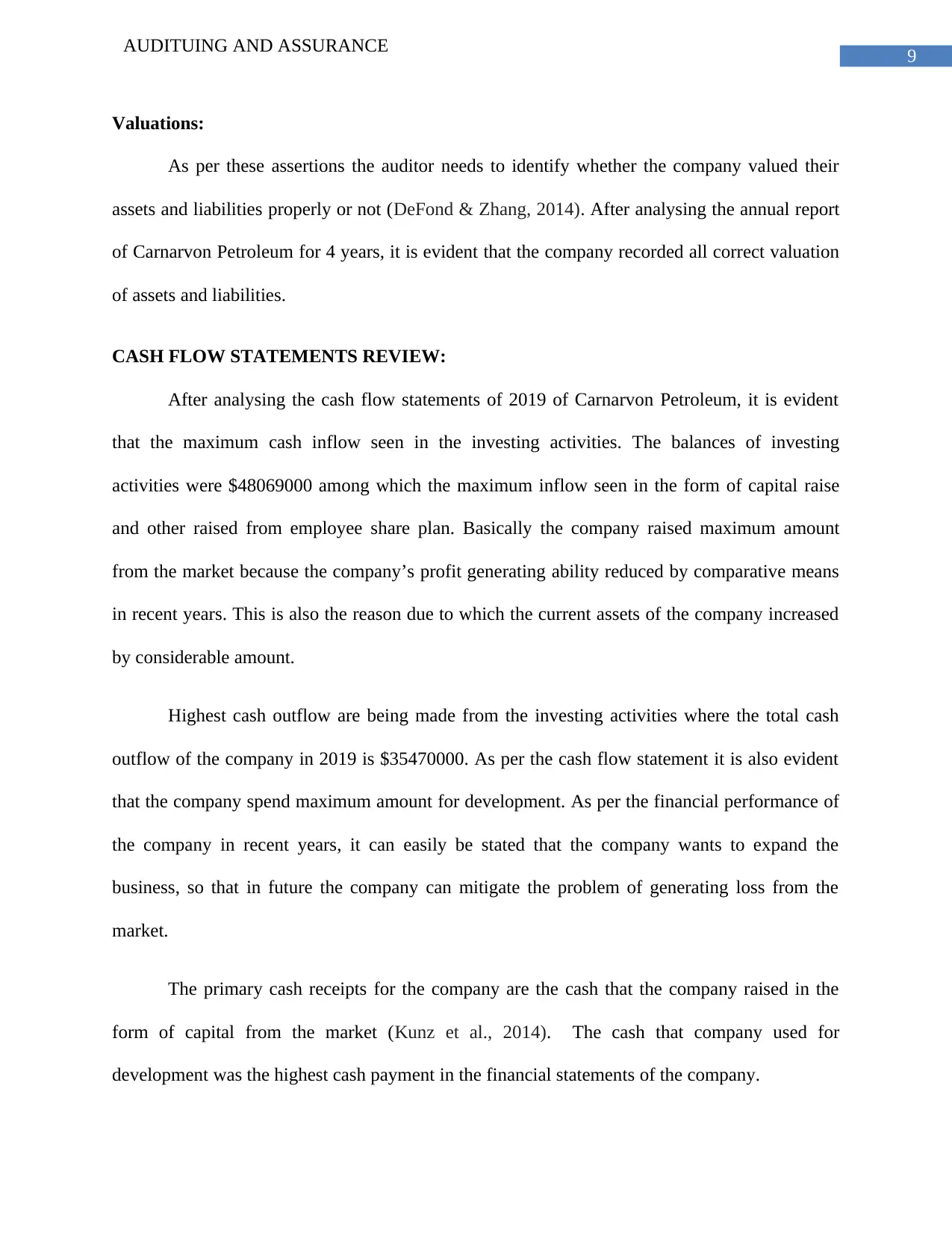

Receivables Turnover Ratio

Receivables Turnover Ratio

Figure 4: Receivables Turnover Ratio

(Sourced by Author)

After analysing all the financial ratios of Carnarvon Petroleum it can be determined that

the financial positions of the company for last 4 years is not right. The company’s only strong

point that can be identified is that they have better liquidity, but other ratios shows very low

results. The auditor assertions that are associated with the financial statements of the company

are as follows:

Completeness:

As per this assertion the auditor reported fully about the asset, liability and equity

balances of Carnarvon Petroleum in all the annual report of 2019, 2018, 2017 and 2016.

Existence:

Auditor of Carnarvon Petroleum, Ernst Young, checked all account balances for assets,

liabilities and equity.

AUDITUING AND ASSURANCE

2019 2018 2017 2016

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

Receivables Turnover Ratio

Receivables Turnover Ratio

Figure 4: Receivables Turnover Ratio

(Sourced by Author)

After analysing all the financial ratios of Carnarvon Petroleum it can be determined that

the financial positions of the company for last 4 years is not right. The company’s only strong

point that can be identified is that they have better liquidity, but other ratios shows very low

results. The auditor assertions that are associated with the financial statements of the company

are as follows:

Completeness:

As per this assertion the auditor reported fully about the asset, liability and equity

balances of Carnarvon Petroleum in all the annual report of 2019, 2018, 2017 and 2016.

Existence:

Auditor of Carnarvon Petroleum, Ernst Young, checked all account balances for assets,

liabilities and equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITUING AND ASSURANCE

Valuations:

As per these assertions the auditor needs to identify whether the company valued their

assets and liabilities properly or not (DeFond & Zhang, 2014). After analysing the annual report

of Carnarvon Petroleum for 4 years, it is evident that the company recorded all correct valuation

of assets and liabilities.

CASH FLOW STATEMENTS REVIEW:

After analysing the cash flow statements of 2019 of Carnarvon Petroleum, it is evident

that the maximum cash inflow seen in the investing activities. The balances of investing

activities were $48069000 among which the maximum inflow seen in the form of capital raise

and other raised from employee share plan. Basically the company raised maximum amount

from the market because the company’s profit generating ability reduced by comparative means

in recent years. This is also the reason due to which the current assets of the company increased

by considerable amount.

Highest cash outflow are being made from the investing activities where the total cash

outflow of the company in 2019 is $35470000. As per the cash flow statement it is also evident

that the company spend maximum amount for development. As per the financial performance of

the company in recent years, it can easily be stated that the company wants to expand the

business, so that in future the company can mitigate the problem of generating loss from the

market.

The primary cash receipts for the company are the cash that the company raised in the

form of capital from the market (Kunz et al., 2014). The cash that company used for

development was the highest cash payment in the financial statements of the company.

AUDITUING AND ASSURANCE

Valuations:

As per these assertions the auditor needs to identify whether the company valued their

assets and liabilities properly or not (DeFond & Zhang, 2014). After analysing the annual report

of Carnarvon Petroleum for 4 years, it is evident that the company recorded all correct valuation

of assets and liabilities.

CASH FLOW STATEMENTS REVIEW:

After analysing the cash flow statements of 2019 of Carnarvon Petroleum, it is evident

that the maximum cash inflow seen in the investing activities. The balances of investing

activities were $48069000 among which the maximum inflow seen in the form of capital raise

and other raised from employee share plan. Basically the company raised maximum amount

from the market because the company’s profit generating ability reduced by comparative means

in recent years. This is also the reason due to which the current assets of the company increased

by considerable amount.

Highest cash outflow are being made from the investing activities where the total cash

outflow of the company in 2019 is $35470000. As per the cash flow statement it is also evident

that the company spend maximum amount for development. As per the financial performance of

the company in recent years, it can easily be stated that the company wants to expand the

business, so that in future the company can mitigate the problem of generating loss from the

market.

The primary cash receipts for the company are the cash that the company raised in the

form of capital from the market (Kunz et al., 2014). The cash that company used for

development was the highest cash payment in the financial statements of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITUING AND ASSURANCE

The cash used by the company for the development was the main non-cash and investing

activities. The company also spend certain amount of cash for acquisitions of property, plant and

equipment. The company spend $44000 in 2019 for the acquisitions of property, plant and

equipment.

After analysing the financial performance of Carnarvon Petroleum, it is evident that the

going concern of the company is at stake. The main reason behind such problem is due to the

company’s low financial performance in recent years. Thus, the auditor needs to state the

material uncertainty in the auditor’s report, so that the auditor can safeguard the stakeholder’s

interests. In this way the auditor could easily maintain the shareholder’s interests (Ackers &

Eccles, 2015). In this way the auditor can mitigate the risks and even safeguard the shareholder’s

interests.

AUDITUING AND ASSURANCE

The cash used by the company for the development was the main non-cash and investing

activities. The company also spend certain amount of cash for acquisitions of property, plant and

equipment. The company spend $44000 in 2019 for the acquisitions of property, plant and

equipment.

After analysing the financial performance of Carnarvon Petroleum, it is evident that the

going concern of the company is at stake. The main reason behind such problem is due to the

company’s low financial performance in recent years. Thus, the auditor needs to state the

material uncertainty in the auditor’s report, so that the auditor can safeguard the stakeholder’s

interests. In this way the auditor could easily maintain the shareholder’s interests (Ackers &

Eccles, 2015). In this way the auditor can mitigate the risks and even safeguard the shareholder’s

interests.

11

AUDITUING AND ASSURANCE

REFERENCES:

Cohen, J. R., & Simnett, R. (2015). CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), 59-74.

Brown, V. L., Coram, P. J., Dennis, S. A., Dickins, D., Earley, C. E., Higgs, J. L., ... & Tatum,

K. W. (2019). Comments of the Auditing Standards Committee of the Auditing Section of the

American Accounting Association on International Auditing and Assurance Standards Board

Exposure Draft, Proposed International Standard on Auditing 315 (Revised): Identifying and

Assessing the Risks of Material Misstatement and Proposed Consequential and Conforming

Amendments to Other ISAs. Current Issues in Auditing, 13(1), C1-C9.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of accounting

and economics, 58(2-3), 275-326.

Ackers, B., & Eccles, N. S. (2015). Mandatory corporate social responsibility assurance

practices. Accounting, Auditing & Accountability Journal.

Kunz, R., Josset, D., Scholtz, H., Motholo, V., O'Reilly, G., Penning, G., & Rudman, R. (2014).

Auditing & Assurance: Principles & Practice. OUP Catalogue.

Kunz, R., Josset, D., Scholtz, H., Motholo, V., O'Reilly, G., Penning, G., & Rudman, R. (2014).

Auditing & Assurance: Principles & Practice. OUP Catalogue.

Whitney, B. B., & Hengesh, J. V. (2015). Geomorphological evidence of neotectonic

deformation in the Carnarvon Basin, Western Australia. Geomorphology, 228, 579-596.

AUDITUING AND ASSURANCE

REFERENCES:

Cohen, J. R., & Simnett, R. (2015). CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), 59-74.

Brown, V. L., Coram, P. J., Dennis, S. A., Dickins, D., Earley, C. E., Higgs, J. L., ... & Tatum,

K. W. (2019). Comments of the Auditing Standards Committee of the Auditing Section of the

American Accounting Association on International Auditing and Assurance Standards Board

Exposure Draft, Proposed International Standard on Auditing 315 (Revised): Identifying and

Assessing the Risks of Material Misstatement and Proposed Consequential and Conforming

Amendments to Other ISAs. Current Issues in Auditing, 13(1), C1-C9.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of accounting

and economics, 58(2-3), 275-326.

Ackers, B., & Eccles, N. S. (2015). Mandatory corporate social responsibility assurance

practices. Accounting, Auditing & Accountability Journal.

Kunz, R., Josset, D., Scholtz, H., Motholo, V., O'Reilly, G., Penning, G., & Rudman, R. (2014).

Auditing & Assurance: Principles & Practice. OUP Catalogue.

Kunz, R., Josset, D., Scholtz, H., Motholo, V., O'Reilly, G., Penning, G., & Rudman, R. (2014).

Auditing & Assurance: Principles & Practice. OUP Catalogue.

Whitney, B. B., & Hengesh, J. V. (2015). Geomorphological evidence of neotectonic

deformation in the Carnarvon Basin, Western Australia. Geomorphology, 228, 579-596.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.