Travel Finance: Analysis of Carnival Corporation & PLC & Dalata Group

VerifiedAdded on 2024/04/26

|20

|5077

|84

Report

AI Summary

This report delves into the crucial aspects of finance and funding within the travel and tourism industry, primarily focusing on Carnival Corporation & Plc and Dalata Hotel Group Plc. It begins by examining the significance of cost and volume in financial management, using Carnival Corporation as a case study to understand how these elements influence pricing and profitability. The report analyzes various pricing methods employed in the travel sector, drawing examples from different cruise brands under Carnival Corporation. Furthermore, it investigates the factors that impact profit for travel and tourism businesses, again using Carnival Corporation's cruise brands as a reference. A detailed interpretation of the financial accounts of Dalata Hotel Group Plc for the year ended 2016 provides insights into their financial performance. Lastly, the report explores the sources and distribution of funding for capital projects associated with tourism, offering a comprehensive overview of financial strategies and considerations within the industry. Desklib provides a platform to access similar solved assignments and past papers.

1

UNIT 2 -

Finance and

Funding in

the Travel

and Tourism

Sector

UNIT 2 -

Finance and

Funding in

the Travel

and Tourism

Sector

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.....................................................................................................................................2

TASK 1 – WRITTEN REPORT...................................................................................................................3

1.1 IMPORTANCE OF COSTS AND VOLUME IN FINANCIAL MANAGEMENT OF TRAVEL AND

TOURISM BUSINESSES USING CARNIVAL CORPORATION & PLC AS A CASE STUDY...........................3

1.2 ANALYSE PRICING METHODS USED IN THE TRAVEL AND TOURISM SECTOR AND USING

RELEVANT EXAMPLES FROM DIFFERENT CRUISE BRANDS OF CARNIVAL CORPORATION & PLC.......6

1.3 ANALYSE FACTORS INFLUENCING PROFIT FOR TRAVEL AND TOURISM BUSINESSES USING

CARNIVAL CORPORATION & PLC CRUISE BRANDS AS A CASE STUDY................................................8

TASK 3 - WRITTEN REPORT ON THE FINANCIAL PERFORMANCE OF DALATA HOTEL GROUP PLC.......10

3.1 INTERPRETATION OF FINANCIAL ACCOUNTS OF DALATA HOTEL GROUP PLC FOR THE YEAR

ENDED 31ST DECEMBER 2016...........................................................................................................10

TASK 4 – LEAFLETS...............................................................................................................................14

4.1 ANALYSE SOURCES AND DISTRIBUTION OF FUNDING FOR THE DEVELOPMENT OF CAPITAL

PROJECTS ASSOCIATED WITH TOURISM..........................................................................................14

CONCLUSION.........................................................................................................................................0

REFERENCES..........................................................................................................................................1

INTRODUCTION.....................................................................................................................................2

TASK 1 – WRITTEN REPORT...................................................................................................................3

1.1 IMPORTANCE OF COSTS AND VOLUME IN FINANCIAL MANAGEMENT OF TRAVEL AND

TOURISM BUSINESSES USING CARNIVAL CORPORATION & PLC AS A CASE STUDY...........................3

1.2 ANALYSE PRICING METHODS USED IN THE TRAVEL AND TOURISM SECTOR AND USING

RELEVANT EXAMPLES FROM DIFFERENT CRUISE BRANDS OF CARNIVAL CORPORATION & PLC.......6

1.3 ANALYSE FACTORS INFLUENCING PROFIT FOR TRAVEL AND TOURISM BUSINESSES USING

CARNIVAL CORPORATION & PLC CRUISE BRANDS AS A CASE STUDY................................................8

TASK 3 - WRITTEN REPORT ON THE FINANCIAL PERFORMANCE OF DALATA HOTEL GROUP PLC.......10

3.1 INTERPRETATION OF FINANCIAL ACCOUNTS OF DALATA HOTEL GROUP PLC FOR THE YEAR

ENDED 31ST DECEMBER 2016...........................................................................................................10

TASK 4 – LEAFLETS...............................................................................................................................14

4.1 ANALYSE SOURCES AND DISTRIBUTION OF FUNDING FOR THE DEVELOPMENT OF CAPITAL

PROJECTS ASSOCIATED WITH TOURISM..........................................................................................14

CONCLUSION.........................................................................................................................................0

REFERENCES..........................................................................................................................................1

INTRODUCTION

Travel and tourism industry is growing with a considerable pace contributing to the nation’s

economy. The finance and funding in travel and tourism is said to be very critical for their

growth and sustainability (Tribe, 2015). In this report the factors contributing the financial

performance of the Travel business is been analysed in context with the Carnival

Corporation & Plc analysing the importance of cost and volume with other related cost and

factors. In the next part of the report an analysis has been made in context with the Dalata

Hotel Group Plc for evaluating the financial performance of the business by comparing the

data of the two years. At last an understanding about the funding and capital projects are

discussed in terms of development and improvement of tourism sector.

Travel and tourism industry is growing with a considerable pace contributing to the nation’s

economy. The finance and funding in travel and tourism is said to be very critical for their

growth and sustainability (Tribe, 2015). In this report the factors contributing the financial

performance of the Travel business is been analysed in context with the Carnival

Corporation & Plc analysing the importance of cost and volume with other related cost and

factors. In the next part of the report an analysis has been made in context with the Dalata

Hotel Group Plc for evaluating the financial performance of the business by comparing the

data of the two years. At last an understanding about the funding and capital projects are

discussed in terms of development and improvement of tourism sector.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1 – WRITTEN REPORT

Travel and tourism business also requires managing their finances and working on their

financial management. For this, the different terminologies and an assessment of different

financial terms have to be done by the companies (Heizer, 2016). As per the case of Carnival

Corporation & plc, a report has been made for understanding the important financial terms

such as cost, volume and different pricing methods and factors influencing the profit margin

of the company (Carnival Corporation & PLC, 2018). This will be helping the company in

analysing and taking effective management and financial decision making.

1.1 IMPORTANCE OF COSTS AND VOLUME IN FINANCIAL MANAGEMENT OF

TRAVEL AND TOURISM BUSINESSES USING CARNIVAL CORPORATION & PLC

AS A CASE STUDY.

COST is termed as the number of expenses or expenditure incurred by the company say for

acquiring the resources and material for producing the required output and selling it

respectively. In monetary terms the cost is assessed as per the charges against efforts,

material, time and utilities consumed, risk incurred, resources and opportunity forgone.

Cost is termed as an important element in the financial management of a business as it

affects the pricing of product and services with various other costs as well. There are

different types of cost depending on the type of resources and services (Eldenburg, et al.

2016). This classification of the cost is necessary for taking the three important business

decision i.e. product costing, management control and decision making.

Travel and tourism business also requires managing their finances and working on their

financial management. For this, the different terminologies and an assessment of different

financial terms have to be done by the companies (Heizer, 2016). As per the case of Carnival

Corporation & plc, a report has been made for understanding the important financial terms

such as cost, volume and different pricing methods and factors influencing the profit margin

of the company (Carnival Corporation & PLC, 2018). This will be helping the company in

analysing and taking effective management and financial decision making.

1.1 IMPORTANCE OF COSTS AND VOLUME IN FINANCIAL MANAGEMENT OF

TRAVEL AND TOURISM BUSINESSES USING CARNIVAL CORPORATION & PLC

AS A CASE STUDY.

COST is termed as the number of expenses or expenditure incurred by the company say for

acquiring the resources and material for producing the required output and selling it

respectively. In monetary terms the cost is assessed as per the charges against efforts,

material, time and utilities consumed, risk incurred, resources and opportunity forgone.

Cost is termed as an important element in the financial management of a business as it

affects the pricing of product and services with various other costs as well. There are

different types of cost depending on the type of resources and services (Eldenburg, et al.

2016). This classification of the cost is necessary for taking the three important business

decision i.e. product costing, management control and decision making.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct cost is traced as direct expenses incurred by the organisation and company

for delivering its services or manufacturing product (Shepherd, 2015). Example the

Carnival Corporation and plc, the travel and tourism company have their direct cost

in way of offering to client’s spas, hotels and food etc. which can be directly

consumable.

Indirect cost is an expense that cannot be directly traced but forms a part of the final

product or services (Shepherd, 2015). Example the Carnival Corporation the indirect

cost may be in the form of administrative expenses such as salaries and overhead

expenses like rent and other utilities.

Fixed cost is the expenses that are not hindered by any fluctuation in the activity or

functioning and remains fixed during the operations. It does not change as per the

number of services and product produced or sold (Lanen, 2016). Example the

Carnival Corporation has its fixed cost of maintenance of the Cruise and salaries to

top management and other costs like distribution and marketing regardless of the

number of passengers and operation of the company.

Variable cost is termed as the changes in the cost directly proportionate to the

change in the activity level or production output and varies over the time (Schmidt,

2016). The example in Carnival Corporation the variable cost ascertained are such as

freight and other charges, commissions and production supplies etc.

COST

DIRECT

LABOUR OVERHEADS MATERIALS

INDIRECT

ADMINISTRATIVE

EXPENSES

SELLING

EXPENSES

VARIABLE FIXED

for delivering its services or manufacturing product (Shepherd, 2015). Example the

Carnival Corporation and plc, the travel and tourism company have their direct cost

in way of offering to client’s spas, hotels and food etc. which can be directly

consumable.

Indirect cost is an expense that cannot be directly traced but forms a part of the final

product or services (Shepherd, 2015). Example the Carnival Corporation the indirect

cost may be in the form of administrative expenses such as salaries and overhead

expenses like rent and other utilities.

Fixed cost is the expenses that are not hindered by any fluctuation in the activity or

functioning and remains fixed during the operations. It does not change as per the

number of services and product produced or sold (Lanen, 2016). Example the

Carnival Corporation has its fixed cost of maintenance of the Cruise and salaries to

top management and other costs like distribution and marketing regardless of the

number of passengers and operation of the company.

Variable cost is termed as the changes in the cost directly proportionate to the

change in the activity level or production output and varies over the time (Schmidt,

2016). The example in Carnival Corporation the variable cost ascertained are such as

freight and other charges, commissions and production supplies etc.

COST

DIRECT

LABOUR OVERHEADS MATERIALS

INDIRECT

ADMINISTRATIVE

EXPENSES

SELLING

EXPENSES

VARIABLE FIXED

VOLUME is the quantity produced or generated by the business of the product and services

to be delivered. The volume initialises the profit margin of the company and its position in

the market (He, et al. 2016). Example the Carnival Corporation the volume is the packages

of tours and travel that are sold and the services delivered with the number of available

stocks and resources.

Break-even analysis is said to be the point where there is no profit or loss i.e.

operating income is zero, for the company. The BEP is important for assessing the

number of product units to be sold by the company to cover all its cost. It is

important for the Carnival Corporation & plc for ensuring the balance of total cost

and total gains in terms of the business volume to reach the breakeven point

(Schmidt, 2016).

Economies of scale are gained or achieved in context with the minimum input

delivering maximum output generating a higher amount of volume. This ensures the

profitability and sustainability of the firm with increased output at a decreased cost

(Holtz-Eakin and Lovely, 2017). And its vice versa Diseconomies of scale is termed as

lowering the volume of production with increased cost. This affects the functioning

and profitability of the firm resulting in an increase in per unit cost of the services

and product delivered.

ALLOCATION AND APPORTIONMENT are termed as the distribution or attributing the cost

for the given task and generating the output effectively. This is done by the Carnival

Corporation by way of distributing its cost especially the overhead cost as per the activities

or services delivered to the customers. This provides the company with an edge to adjust its

expenses and cut down extra cost that hampers the profitability of the firm (Patiar, 2016).

Apportionment of cost helps the Carnival Corporation & plc to streamline its expenditure

and funding required by the business for future growth and covering all central cost like

salaries, overhead expenses etc.

Cost and Volume are important for the Carnival Corporation & plc as both determines the

financial and competitive position of the business in the travel and tourism sector. The cost

assesses the operating cost and another related cost which helps the firm to determine and

compare its current position with the competitors. The volume generated and delivered

to be delivered. The volume initialises the profit margin of the company and its position in

the market (He, et al. 2016). Example the Carnival Corporation the volume is the packages

of tours and travel that are sold and the services delivered with the number of available

stocks and resources.

Break-even analysis is said to be the point where there is no profit or loss i.e.

operating income is zero, for the company. The BEP is important for assessing the

number of product units to be sold by the company to cover all its cost. It is

important for the Carnival Corporation & plc for ensuring the balance of total cost

and total gains in terms of the business volume to reach the breakeven point

(Schmidt, 2016).

Economies of scale are gained or achieved in context with the minimum input

delivering maximum output generating a higher amount of volume. This ensures the

profitability and sustainability of the firm with increased output at a decreased cost

(Holtz-Eakin and Lovely, 2017). And its vice versa Diseconomies of scale is termed as

lowering the volume of production with increased cost. This affects the functioning

and profitability of the firm resulting in an increase in per unit cost of the services

and product delivered.

ALLOCATION AND APPORTIONMENT are termed as the distribution or attributing the cost

for the given task and generating the output effectively. This is done by the Carnival

Corporation by way of distributing its cost especially the overhead cost as per the activities

or services delivered to the customers. This provides the company with an edge to adjust its

expenses and cut down extra cost that hampers the profitability of the firm (Patiar, 2016).

Apportionment of cost helps the Carnival Corporation & plc to streamline its expenditure

and funding required by the business for future growth and covering all central cost like

salaries, overhead expenses etc.

Cost and Volume are important for the Carnival Corporation & plc as both determines the

financial and competitive position of the business in the travel and tourism sector. The cost

assesses the operating cost and another related cost which helps the firm to determine and

compare its current position with the competitors. The volume generated and delivered

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determines the sales as well as marketing capacity of the firm depending on its demand.

Both this also helps the firm to forecast the pricing based on the cost and volume to be

generated. The requirement of funds and other essential items to be acquired by the

business is also determined as per the expenses and needs of the customer as per the sales

(Barr, et al. 2018). The sales volume and expenses help the Carnival Corporation to assess

the customer's needs, package improvement or any other arrangement needed to increase

the profitability or sales margin. The variable cost and breakeven analysis helps the Carnival

Corporation to deal and regulate the changes as per the market and meet out the demand

in terms of hotel and cruise booking, tickets pricing and overhead expenses etc.

Both this also helps the firm to forecast the pricing based on the cost and volume to be

generated. The requirement of funds and other essential items to be acquired by the

business is also determined as per the expenses and needs of the customer as per the sales

(Barr, et al. 2018). The sales volume and expenses help the Carnival Corporation to assess

the customer's needs, package improvement or any other arrangement needed to increase

the profitability or sales margin. The variable cost and breakeven analysis helps the Carnival

Corporation to deal and regulate the changes as per the market and meet out the demand

in terms of hotel and cruise booking, tickets pricing and overhead expenses etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 ANALYSE PRICING METHODS USED IN THE TRAVEL AND TOURISM

SECTOR AND USING RELEVANT EXAMPLES FROM DIFFERENT CRUISE

BRANDS OF CARNIVAL CORPORATION & PLC.

Pricing methods are considered as one of the most important and crucial decision to be

taken by any business or firm. The decision lies in many factors and assessing these factors

will help the firm to effectively take their pricing decision while considering all the facts and

figures. The different pricing methods that can be used by the travel and tourism industry in

context with the Carnival Corporation are as follows:

Cost-Led Pricing: in this method, the prices are set as per the cost and volume to be

generated by the firm or organisation. For accurately determining the prices breakeven

point is calculated to ascertain the profitability position of the firm in regards to the

investment made and set the prices accordingly. High level of profit is there if the prices are

set above the breakeven point (Salim and Bala, 2017). Example the Costa Cruises of Carnival

Corporation is determining the prices above as per there cost and volume. This is effectively

helping them in generating a fruitful return on the investment made in terms of profit. The

cost led method approaches the firm effectively in deciding the promotional offers and

discounts with strategising the recovery of total cost and achieving profit margin.

Market-Led Pricing: this method determines the prices of product and services as per the

customers need and willingness to pay. The pricing to be set is ascertained in context with

the changing market dynamics and according to the prevailing market condition, choosing

the pricing strategies to say skimming and penetration pricing (Piercy, 2016). In penetration,

the prices are set lower for attracting more customers and other than in skimming the prices

are set higher as per the strong position of the company to gain competitive advantage.

Example Carnival UK (Cunard Line and P&O Cruises) uses this method to strategise their

pricing for packages and tours. This method helps the firm to ascertain the best pricing by

discriminating different segments and charging them according to the different groups of

customers.

Cost-Plus Pricing: it is a method in which the sales price is determined on the basis of total

product cost plus adding the markup percentage of profit to the final products or service.

The final pricing also includes opportunity cost with the other related costs such as direct

SECTOR AND USING RELEVANT EXAMPLES FROM DIFFERENT CRUISE

BRANDS OF CARNIVAL CORPORATION & PLC.

Pricing methods are considered as one of the most important and crucial decision to be

taken by any business or firm. The decision lies in many factors and assessing these factors

will help the firm to effectively take their pricing decision while considering all the facts and

figures. The different pricing methods that can be used by the travel and tourism industry in

context with the Carnival Corporation are as follows:

Cost-Led Pricing: in this method, the prices are set as per the cost and volume to be

generated by the firm or organisation. For accurately determining the prices breakeven

point is calculated to ascertain the profitability position of the firm in regards to the

investment made and set the prices accordingly. High level of profit is there if the prices are

set above the breakeven point (Salim and Bala, 2017). Example the Costa Cruises of Carnival

Corporation is determining the prices above as per there cost and volume. This is effectively

helping them in generating a fruitful return on the investment made in terms of profit. The

cost led method approaches the firm effectively in deciding the promotional offers and

discounts with strategising the recovery of total cost and achieving profit margin.

Market-Led Pricing: this method determines the prices of product and services as per the

customers need and willingness to pay. The pricing to be set is ascertained in context with

the changing market dynamics and according to the prevailing market condition, choosing

the pricing strategies to say skimming and penetration pricing (Piercy, 2016). In penetration,

the prices are set lower for attracting more customers and other than in skimming the prices

are set higher as per the strong position of the company to gain competitive advantage.

Example Carnival UK (Cunard Line and P&O Cruises) uses this method to strategise their

pricing for packages and tours. This method helps the firm to ascertain the best pricing by

discriminating different segments and charging them according to the different groups of

customers.

Cost-Plus Pricing: it is a method in which the sales price is determined on the basis of total

product cost plus adding the markup percentage of profit to the final products or service.

The final pricing also includes opportunity cost with the other related costs such as direct

and indirect cost. This all includes the cost of raw material procured, cost of labour and

overhead cost; also known as cost elements (Nagle, et al. 2016). Example Carnival Cruise

Line uses this for ascertaining the prices of its tickets and packages. This is useful for them to

secure its profitability by a fixed markup percentage to avoid from the fluctuations of the

travel and tourism industry. This also determines the variable cost and ensures the

unexpected changes in the cost of effectively determining the packages and tickets. The

disadvantage is that this method does not consider the ongoing competition in the market

and ignores the role of customers and pricing strategies followed by the competitors.

Formula for setting price: P = AVC + AVC (M)

Where AVC= Average Variable Cost

M = Markup percentage

AVC (m) = Gross profit margin

Marginal Costing Pricing: this method majorly focuses on the variable cost such as material

cost and wages etc. The fixed and indirect costs are not considerably used by the firm to

assess the prices of the packages and tickets. Such as the AIDA Cruises a brand of Carnival

Corporation does not use fixed and indirect cost as a basis for calculating the pricing of its

services and product. AIDA is deciding the pricing by marginal costing method which allows

them to have a control over the demand fluctuations and variability in the season (Kotas,

2014). This method is appropriate for the company as it is easy and considerably uses the

spares capacity of the firm for generating more profitability say in terms of effective use of

resources. Allows the lower segment travellers with lower pricing and also makes the frim to

remain in the competition with a price sensitive approach.

overhead cost; also known as cost elements (Nagle, et al. 2016). Example Carnival Cruise

Line uses this for ascertaining the prices of its tickets and packages. This is useful for them to

secure its profitability by a fixed markup percentage to avoid from the fluctuations of the

travel and tourism industry. This also determines the variable cost and ensures the

unexpected changes in the cost of effectively determining the packages and tickets. The

disadvantage is that this method does not consider the ongoing competition in the market

and ignores the role of customers and pricing strategies followed by the competitors.

Formula for setting price: P = AVC + AVC (M)

Where AVC= Average Variable Cost

M = Markup percentage

AVC (m) = Gross profit margin

Marginal Costing Pricing: this method majorly focuses on the variable cost such as material

cost and wages etc. The fixed and indirect costs are not considerably used by the firm to

assess the prices of the packages and tickets. Such as the AIDA Cruises a brand of Carnival

Corporation does not use fixed and indirect cost as a basis for calculating the pricing of its

services and product. AIDA is deciding the pricing by marginal costing method which allows

them to have a control over the demand fluctuations and variability in the season (Kotas,

2014). This method is appropriate for the company as it is easy and considerably uses the

spares capacity of the firm for generating more profitability say in terms of effective use of

resources. Allows the lower segment travellers with lower pricing and also makes the frim to

remain in the competition with a price sensitive approach.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.3 ANALYSE FACTORS INFLUENCING PROFIT FOR TRAVEL AND TOURISM

BUSINESSES USING CARNIVAL CORPORATION & PLC CRUISE BRANDS AS A

CASE STUDY.

There are many factors that can affect the firm’s profitability and productivity and may also

have an influence on its services and product delivered. The major factor that may

influences the profit of travel and tourism business of Carnival Corporation & plc are as

follows:

Political conditions: government involvement and updation in the rules and policies

affect the profitability of the travel and tourism sector. Example the Carnival

Corporation will be greatly impacted in terms of profit and productivity if the

government follows anti-tourism policy. This will lower down the travel rate and

immigration from the different countries (Mason, 2015). Also, the taxation and other

charges levied down by the government affects the profitability of the visitors and

company both with will have to incur high charges and cost for acquiring the

services.

Terrorism: safety and security are one of the major factors that attract the tourists

to visit a place and the frequent terrorist attacks restrict them from visiting the

places or cities. Carnival Corporation’s profit is also influenced by this as it makes the

company suffer losses and gives a negative image of the place (Brondoni, 2016). The

assurance of the security and safety in the UK gives a profitable edge to the company

with an increase in visitors or tourists.

Climatic conditions: changing weather conditions and natural calamities often

impact the tour and travel business. The natural sceneries and pleasant atmosphere

attracts more travellers and tourist resulting in a higher profit margin and increases

the productivity of the business (Shakeela and Becken, 2015). On the other hand, if

any disastrous or catastrophic condition is there, affects the profit of the travel and

tourism as the tourists avoid to visit such places or areas.

Seasonality: in travel and tourism industry seasonality impacts more on the

profitability; as there are peak and troughs in the seasonal business, like of Carnival

Corporation & plc. Example, in the season of Christmas due to holidays the travel

business of Carnival Corporation is at its peak and vice-versa faces a trough in the

BUSINESSES USING CARNIVAL CORPORATION & PLC CRUISE BRANDS AS A

CASE STUDY.

There are many factors that can affect the firm’s profitability and productivity and may also

have an influence on its services and product delivered. The major factor that may

influences the profit of travel and tourism business of Carnival Corporation & plc are as

follows:

Political conditions: government involvement and updation in the rules and policies

affect the profitability of the travel and tourism sector. Example the Carnival

Corporation will be greatly impacted in terms of profit and productivity if the

government follows anti-tourism policy. This will lower down the travel rate and

immigration from the different countries (Mason, 2015). Also, the taxation and other

charges levied down by the government affects the profitability of the visitors and

company both with will have to incur high charges and cost for acquiring the

services.

Terrorism: safety and security are one of the major factors that attract the tourists

to visit a place and the frequent terrorist attacks restrict them from visiting the

places or cities. Carnival Corporation’s profit is also influenced by this as it makes the

company suffer losses and gives a negative image of the place (Brondoni, 2016). The

assurance of the security and safety in the UK gives a profitable edge to the company

with an increase in visitors or tourists.

Climatic conditions: changing weather conditions and natural calamities often

impact the tour and travel business. The natural sceneries and pleasant atmosphere

attracts more travellers and tourist resulting in a higher profit margin and increases

the productivity of the business (Shakeela and Becken, 2015). On the other hand, if

any disastrous or catastrophic condition is there, affects the profit of the travel and

tourism as the tourists avoid to visit such places or areas.

Seasonality: in travel and tourism industry seasonality impacts more on the

profitability; as there are peak and troughs in the seasonal business, like of Carnival

Corporation & plc. Example, in the season of Christmas due to holidays the travel

business of Carnival Corporation is at its peak and vice-versa faces a trough in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

off-season say during the summer days (Shakeela and Becken, 2015). This majorly

impacts the productivity in the offseason and lowers the utilisation of the resources

and therefore decreases the profitability of the firm.

Economic stability: changing micro and macro factors affect the business of travel

and tourism; say the interest rates, currency rates etc. Carnival Corporation & plc is

impacted by this changes and which all the way affects the profitability and

productivity of the firm (Smeral, 2017). Example currency rate changes lower downs

the profit margin as the changing rate differs from country to country and various

tourists travel from different countries.

impacts the productivity in the offseason and lowers the utilisation of the resources

and therefore decreases the profitability of the firm.

Economic stability: changing micro and macro factors affect the business of travel

and tourism; say the interest rates, currency rates etc. Carnival Corporation & plc is

impacted by this changes and which all the way affects the profitability and

productivity of the firm (Smeral, 2017). Example currency rate changes lower downs

the profit margin as the changing rate differs from country to country and various

tourists travel from different countries.

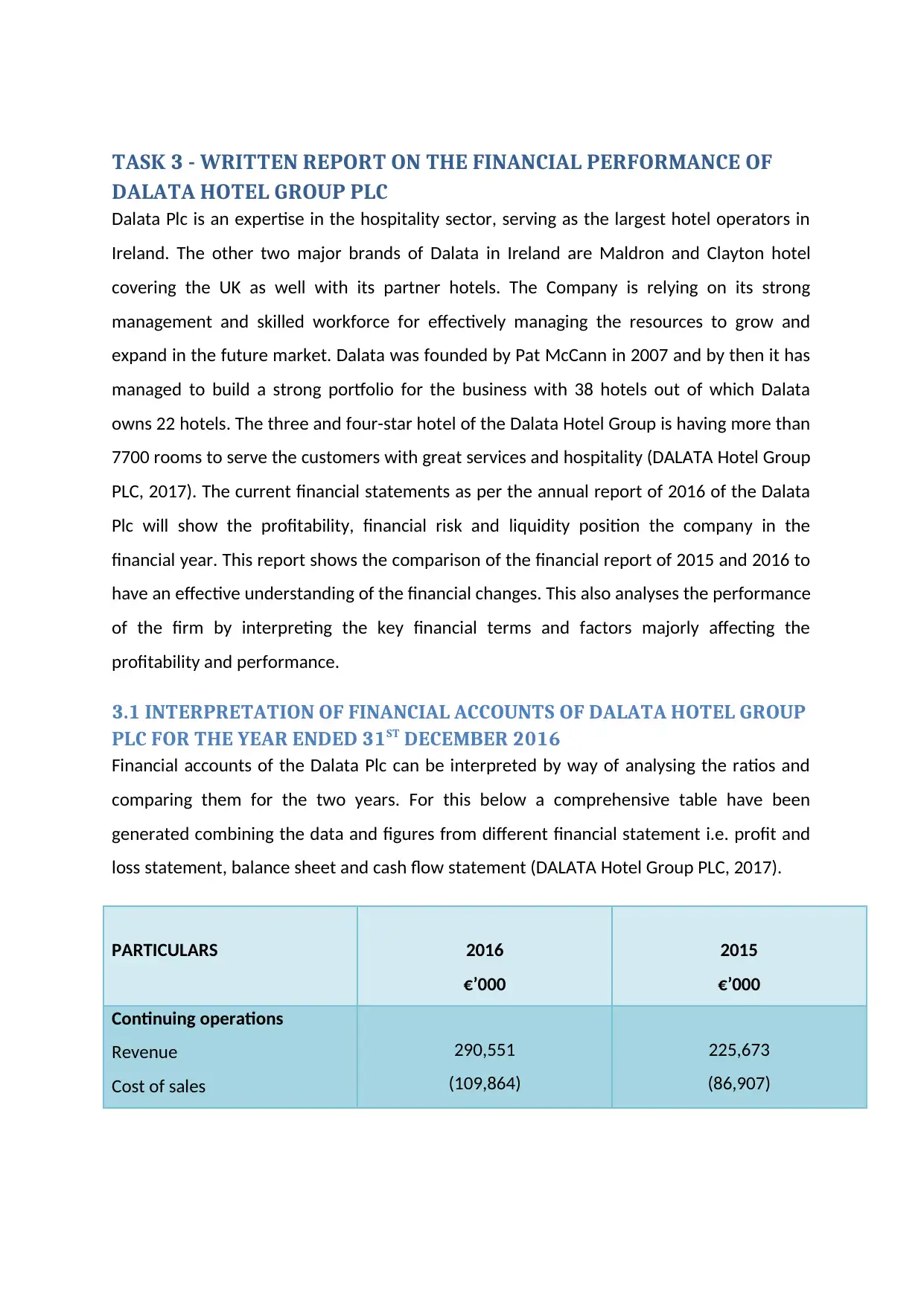

TASK 3 - WRITTEN REPORT ON THE FINANCIAL PERFORMANCE OF

DALATA HOTEL GROUP PLC

Dalata Plc is an expertise in the hospitality sector, serving as the largest hotel operators in

Ireland. The other two major brands of Dalata in Ireland are Maldron and Clayton hotel

covering the UK as well with its partner hotels. The Company is relying on its strong

management and skilled workforce for effectively managing the resources to grow and

expand in the future market. Dalata was founded by Pat McCann in 2007 and by then it has

managed to build a strong portfolio for the business with 38 hotels out of which Dalata

owns 22 hotels. The three and four-star hotel of the Dalata Hotel Group is having more than

7700 rooms to serve the customers with great services and hospitality (DALATA Hotel Group

PLC, 2017). The current financial statements as per the annual report of 2016 of the Dalata

Plc will show the profitability, financial risk and liquidity position the company in the

financial year. This report shows the comparison of the financial report of 2015 and 2016 to

have an effective understanding of the financial changes. This also analyses the performance

of the firm by interpreting the key financial terms and factors majorly affecting the

profitability and performance.

3.1 INTERPRETATION OF FINANCIAL ACCOUNTS OF DALATA HOTEL GROUP

PLC FOR THE YEAR ENDED 31ST DECEMBER 2016

Financial accounts of the Dalata Plc can be interpreted by way of analysing the ratios and

comparing them for the two years. For this below a comprehensive table have been

generated combining the data and figures from different financial statement i.e. profit and

loss statement, balance sheet and cash flow statement (DALATA Hotel Group PLC, 2017).

PARTICULARS 2016

€’000

2015

€’000

Continuing operations

Revenue

Cost of sales

290,551

(109,864)

225,673

(86,907)

DALATA HOTEL GROUP PLC

Dalata Plc is an expertise in the hospitality sector, serving as the largest hotel operators in

Ireland. The other two major brands of Dalata in Ireland are Maldron and Clayton hotel

covering the UK as well with its partner hotels. The Company is relying on its strong

management and skilled workforce for effectively managing the resources to grow and

expand in the future market. Dalata was founded by Pat McCann in 2007 and by then it has

managed to build a strong portfolio for the business with 38 hotels out of which Dalata

owns 22 hotels. The three and four-star hotel of the Dalata Hotel Group is having more than

7700 rooms to serve the customers with great services and hospitality (DALATA Hotel Group

PLC, 2017). The current financial statements as per the annual report of 2016 of the Dalata

Plc will show the profitability, financial risk and liquidity position the company in the

financial year. This report shows the comparison of the financial report of 2015 and 2016 to

have an effective understanding of the financial changes. This also analyses the performance

of the firm by interpreting the key financial terms and factors majorly affecting the

profitability and performance.

3.1 INTERPRETATION OF FINANCIAL ACCOUNTS OF DALATA HOTEL GROUP

PLC FOR THE YEAR ENDED 31ST DECEMBER 2016

Financial accounts of the Dalata Plc can be interpreted by way of analysing the ratios and

comparing them for the two years. For this below a comprehensive table have been

generated combining the data and figures from different financial statement i.e. profit and

loss statement, balance sheet and cash flow statement (DALATA Hotel Group PLC, 2017).

PARTICULARS 2016

€’000

2015

€’000

Continuing operations

Revenue

Cost of sales

290,551

(109,864)

225,673

(86,907)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.