International Accounting: Carrefour & Disney Financial Analysis Report

VerifiedAdded on 2022/08/23

|9

|1610

|21

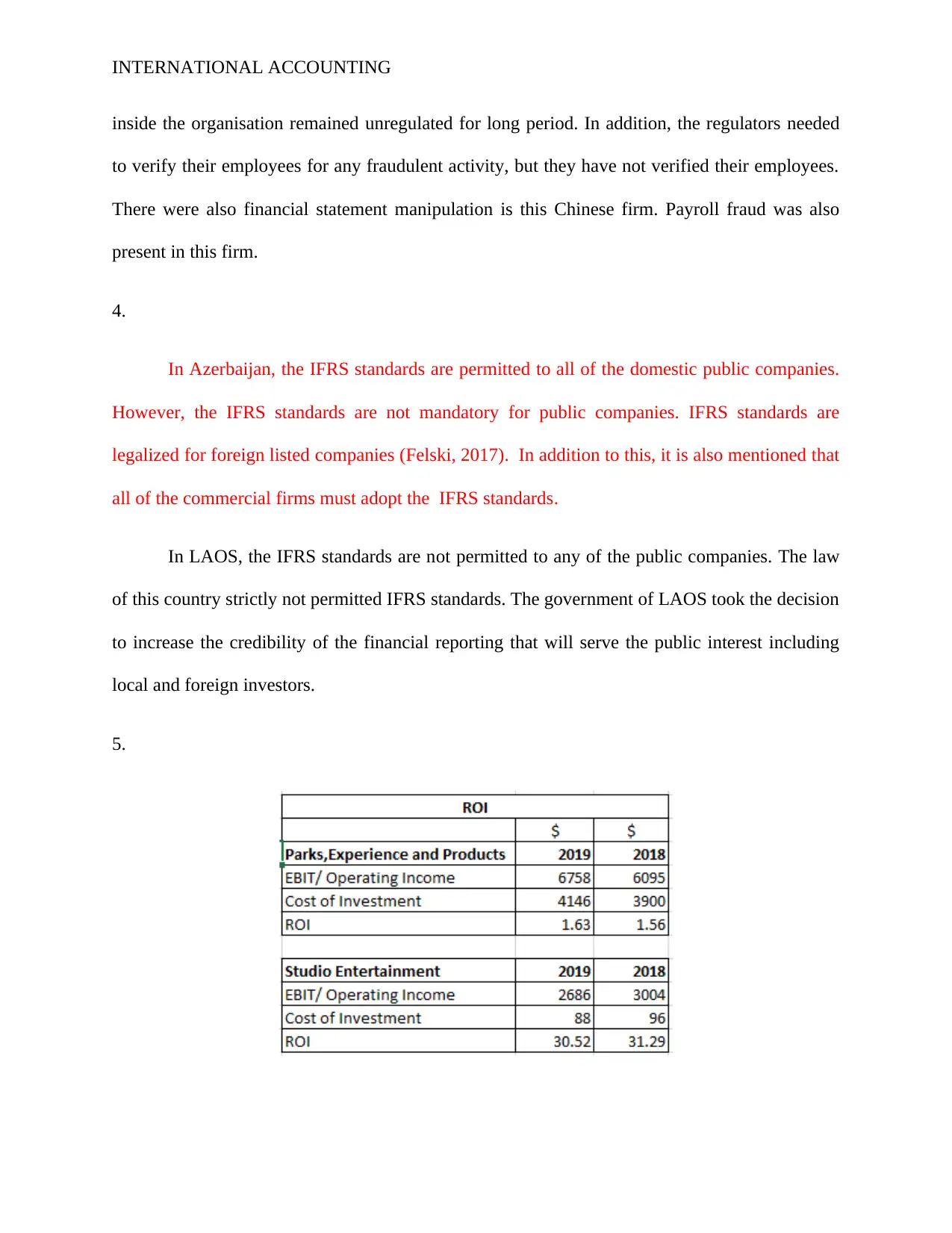

Report

AI Summary

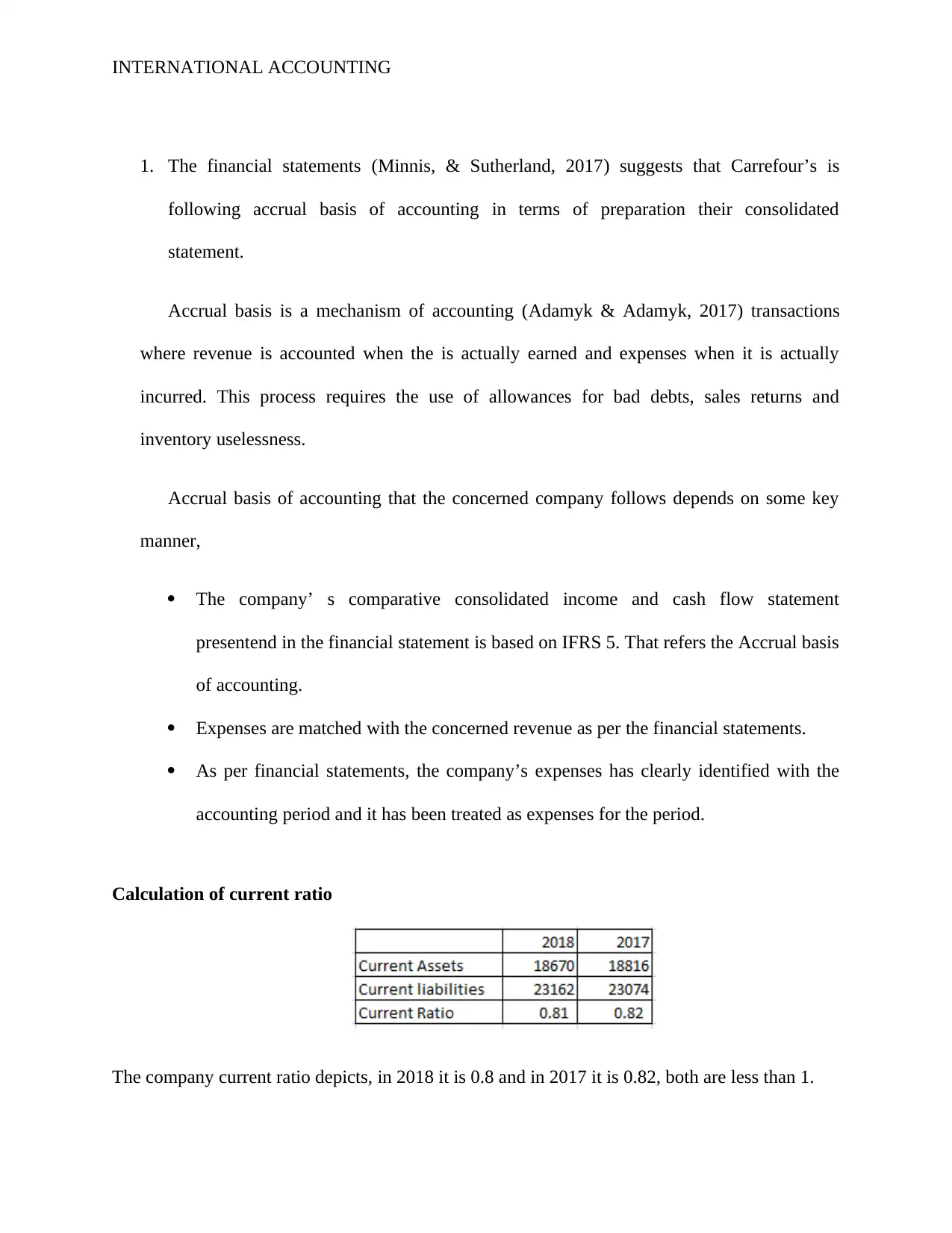

This report analyzes international accounting principles, focusing on Carrefour and Disney's financial statements. It examines the basis of accounting used by Carrefour, calculates its current ratio, and explains harmonization and convergence of accounting standards. The report discusses arguments for and against the U.S. adopting convergence, and identifies the standard-setting bodies. It also explores issues related to the China Agritech fraud, the adoption status of IFRS in Azerbaijan and Laos, and calculates the Return on Investment (ROI) for Disney's segments. Furthermore, it addresses the differences between GAAP and IFRS, consolidation, and the Foreign Corrupt Practices Act (FCPA). The analysis incorporates references to relevant academic literature and financial statements to support the findings. The report also covers reportable segments as defined by IFRS 8.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.