HA3032 Auditing Report: Developing Audit Program for Carsales.com

VerifiedAdded on 2022/11/15

|16

|3919

|325

Report

AI Summary

This report provides an in-depth analysis of the auditing process for Carsales.com. It begins with an introduction to auditing and its significance in verifying financial statements, followed by a background and industry analysis of Carsales.com. The report then examines the company's financial statements, identifying potential risks, and analyzing key financial ratios like liquidity, efficiency, profitability, and leverage. A crucial aspect is the estimation of planning materiality, essential for determining the scope of the audit. The report further details audit assertions and planning, outlining specific audit work steps, and sampling methods for various account balances like trade receivables and inventory. The conclusion summarizes the key findings and the overall audit approach, making it a comprehensive guide to understanding the Carsales.com auditing process.

Running head: Auditing

Auditing

Name of the Student

Name of the University

Author Note

Auditing

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Auditing

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Background and Industry Analysis........................................................................................4

Analysis of Financial Statement of the Business...................................................................5

Analytical Review of the Company.......................................................................................7

Estimation of Planning Materiality........................................................................................8

Audit Assertions and Planning.............................................................................................10

Conclusion................................................................................................................................14

Reference..................................................................................................................................15

Auditing

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Background and Industry Analysis........................................................................................4

Analysis of Financial Statement of the Business...................................................................5

Analytical Review of the Company.......................................................................................7

Estimation of Planning Materiality........................................................................................8

Audit Assertions and Planning.............................................................................................10

Conclusion................................................................................................................................14

Reference..................................................................................................................................15

2

Auditing

Introduction

Audit is a process which is been carried upon the financial statement of the

company. Auditing is been carried out by the external person termed as auditor. Auditor carry

many process in the company so that it able to get the sufficient information about the

company financial statement and give it view that whether the company statement are sowing

true and fair view or not (Beck and Mauldin 2014). The auditor check whether the financial

statement are made in accordance of the auditing standard and different principle listed for

the preparation of the financial statement. The auditor also check the company account does

not have any material misstatement in the financial account and it is been showing all the

correct figure of all the account (Bell, Causholli and Knechel 2015). It also checks the

company internal control system to know whether the company is able to control the entire

internal problem and how they maintain their inventory system of the company.

The report is based upon the company name Carsales.com. The purpose of this report

is to analysis the business of the company which provide its service in many countries.

Carsales.com operate in online market place which deals with the product likes motorcycle,

automotive and marine business. The report show the analysis of the different risk which the

company is facing in day to day transaction. The analysis is been based upon the financial

ration of the company which show the real performance of the company. The auditor have

consider three years ratio for analysing the company risk. In addition of that it all contain the

details of the materiality which the company financial statement contains. The auditor have

also shown the accounts which are affected by the material misstatement of the company. It

also the plan of sampling the auditor have used in regards of the audit process of the

company.

Auditing

Introduction

Audit is a process which is been carried upon the financial statement of the

company. Auditing is been carried out by the external person termed as auditor. Auditor carry

many process in the company so that it able to get the sufficient information about the

company financial statement and give it view that whether the company statement are sowing

true and fair view or not (Beck and Mauldin 2014). The auditor check whether the financial

statement are made in accordance of the auditing standard and different principle listed for

the preparation of the financial statement. The auditor also check the company account does

not have any material misstatement in the financial account and it is been showing all the

correct figure of all the account (Bell, Causholli and Knechel 2015). It also checks the

company internal control system to know whether the company is able to control the entire

internal problem and how they maintain their inventory system of the company.

The report is based upon the company name Carsales.com. The purpose of this report

is to analysis the business of the company which provide its service in many countries.

Carsales.com operate in online market place which deals with the product likes motorcycle,

automotive and marine business. The report show the analysis of the different risk which the

company is facing in day to day transaction. The analysis is been based upon the financial

ration of the company which show the real performance of the company. The auditor have

consider three years ratio for analysing the company risk. In addition of that it all contain the

details of the materiality which the company financial statement contains. The auditor have

also shown the accounts which are affected by the material misstatement of the company. It

also the plan of sampling the auditor have used in regards of the audit process of the

company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Auditing

Discussion

Background and Industry Analysis

The report is been based upon the Carsales.com which is a online based industry and

carry its business in regards of automobile . As per the financial statement of the company it

can be said that the company is doing good in the market and able to increase its customer on

a regular basis. As per the above statement it can be said the company is working in a

growing industry and as a result it able to get more amount of profit from the business. As per

the account of the company it can be seen that the company is having an increase in the net

profit of the company so this show that the company have a very good position in the market.

As there will be a risk to business so the risk which the company face while carrying their

business activities are discuss below:

o Liquidity Conditions: This is one of the primary risk which each company have to

face as it is necessary for the company to hold some amount of cash in the business as

it will help them to do the working cycle of the company and also company should

have some cash for paying any current obligation which can be occurred in the

company business so to overcome such situation the company need to have liquidity

in the financial statement of the company (Chen et al., 2015).

o Competitor in the Industry: The company have to face this risk also as each

industry have some amount of competitors and due to these the company is not able to

get the whole market of the industry (Chou 2015). It also happens that they not able to

get increase in sales as the competitors is able to get an edge over the market.

Company should able to make their marketing strategy taking the competitors into

consideration.

o Unfavourable Economic Conditions: The company have to face such risk and it not

able to avoided by the company as it may happen that the government change some

Auditing

Discussion

Background and Industry Analysis

The report is been based upon the Carsales.com which is a online based industry and

carry its business in regards of automobile . As per the financial statement of the company it

can be said that the company is doing good in the market and able to increase its customer on

a regular basis. As per the above statement it can be said the company is working in a

growing industry and as a result it able to get more amount of profit from the business. As per

the account of the company it can be seen that the company is having an increase in the net

profit of the company so this show that the company have a very good position in the market.

As there will be a risk to business so the risk which the company face while carrying their

business activities are discuss below:

o Liquidity Conditions: This is one of the primary risk which each company have to

face as it is necessary for the company to hold some amount of cash in the business as

it will help them to do the working cycle of the company and also company should

have some cash for paying any current obligation which can be occurred in the

company business so to overcome such situation the company need to have liquidity

in the financial statement of the company (Chen et al., 2015).

o Competitor in the Industry: The company have to face this risk also as each

industry have some amount of competitors and due to these the company is not able to

get the whole market of the industry (Chou 2015). It also happens that they not able to

get increase in sales as the competitors is able to get an edge over the market.

Company should able to make their marketing strategy taking the competitors into

consideration.

o Unfavourable Economic Conditions: The company have to face such risk and it not

able to avoided by the company as it may happen that the government change some

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Auditing

policy and due to the change it affect the financial position of the company

(Christensen et al., 2016). As it may happen the government have increase the interest

rate so that can lead to increase the interest cost of the company and it will also

decrease the overall profit of the company.

Analysis of Financial Statement of the Business

The analysis of the company is been done by considering the annual report of 2018

and it show the judgement which the company have made in the financial statement are

proper or not. As per the income statement of the company it is clear that the gross profit

have been decrease in percentage so it show the company is not to increase the sale in respect

of the increase in cost of the goods of the company (Shareholder.carsales.com.au 2019). The

income statement also show that there is an increase in both the revenue and the cost so it can

be consider as a risk as the company may have overstate to show a better financial position of

the company. As the result of the overstate the company financial statement will have a

material misstatement so it will affect the principle of true and fair view of the financial

statement. As there is one misstatement situation so the auditor should be very careful while

checking other accounts as it may happen that the company financial statement may have

more account misstated.

The risk that the company face while doing their business is been classified as control

and inherent risk. The company may have material misstatement in the financial statement as

it may happen due to some omission and error so this type of risk is been defined as inherent

risk. The company internal control may have some amount of weakness and due to these

which risk are occur are termed as control risk of the company. The auditor have to carry its

audit process in the company Carsales.com so that it able to identity both inherent and control

risk of the company. The management should apply the audit risk model so that it will able to

identify the risk in the business which are been classified in above lines of the report. The

Auditing

policy and due to the change it affect the financial position of the company

(Christensen et al., 2016). As it may happen the government have increase the interest

rate so that can lead to increase the interest cost of the company and it will also

decrease the overall profit of the company.

Analysis of Financial Statement of the Business

The analysis of the company is been done by considering the annual report of 2018

and it show the judgement which the company have made in the financial statement are

proper or not. As per the income statement of the company it is clear that the gross profit

have been decrease in percentage so it show the company is not to increase the sale in respect

of the increase in cost of the goods of the company (Shareholder.carsales.com.au 2019). The

income statement also show that there is an increase in both the revenue and the cost so it can

be consider as a risk as the company may have overstate to show a better financial position of

the company. As the result of the overstate the company financial statement will have a

material misstatement so it will affect the principle of true and fair view of the financial

statement. As there is one misstatement situation so the auditor should be very careful while

checking other accounts as it may happen that the company financial statement may have

more account misstated.

The risk that the company face while doing their business is been classified as control

and inherent risk. The company may have material misstatement in the financial statement as

it may happen due to some omission and error so this type of risk is been defined as inherent

risk. The company internal control may have some amount of weakness and due to these

which risk are occur are termed as control risk of the company. The auditor have to carry its

audit process in the company Carsales.com so that it able to identity both inherent and control

risk of the company. The management should apply the audit risk model so that it will able to

identify the risk in the business which are been classified in above lines of the report. The

5

Auditing

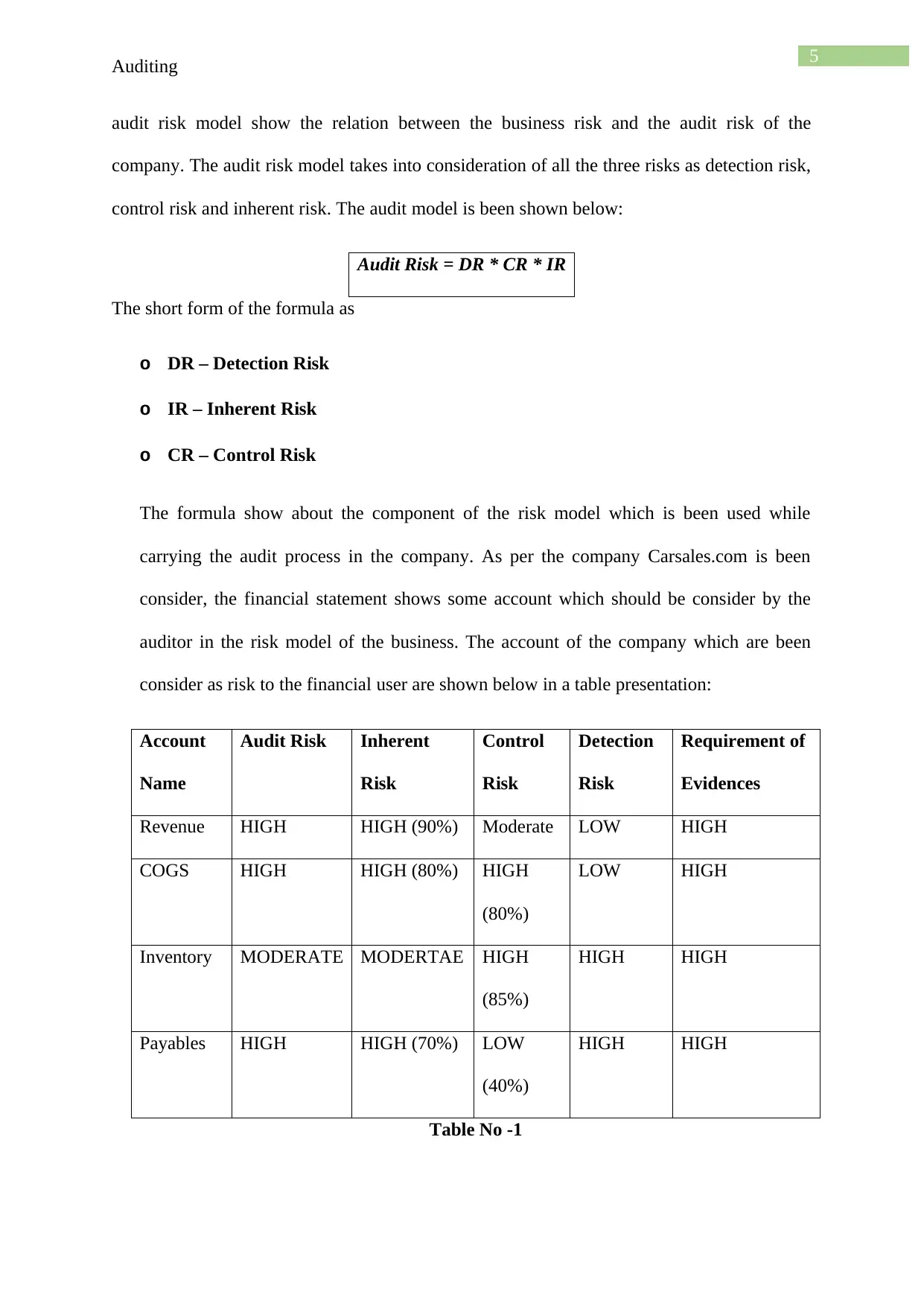

audit risk model show the relation between the business risk and the audit risk of the

company. The audit risk model takes into consideration of all the three risks as detection risk,

control risk and inherent risk. The audit model is been shown below:

Audit Risk = DR * CR * IR

The short form of the formula as

o DR – Detection Risk

o IR – Inherent Risk

o CR – Control Risk

The formula show about the component of the risk model which is been used while

carrying the audit process in the company. As per the company Carsales.com is been

consider, the financial statement shows some account which should be consider by the

auditor in the risk model of the business. The account of the company which are been

consider as risk to the financial user are shown below in a table presentation:

Account

Name

Audit Risk Inherent

Risk

Control

Risk

Detection

Risk

Requirement of

Evidences

Revenue HIGH HIGH (90%) Moderate LOW HIGH

COGS HIGH HIGH (80%) HIGH

(80%)

LOW HIGH

Inventory MODERATE MODERTAE HIGH

(85%)

HIGH HIGH

Payables HIGH HIGH (70%) LOW

(40%)

HIGH HIGH

Table No -1

Auditing

audit risk model show the relation between the business risk and the audit risk of the

company. The audit risk model takes into consideration of all the three risks as detection risk,

control risk and inherent risk. The audit model is been shown below:

Audit Risk = DR * CR * IR

The short form of the formula as

o DR – Detection Risk

o IR – Inherent Risk

o CR – Control Risk

The formula show about the component of the risk model which is been used while

carrying the audit process in the company. As per the company Carsales.com is been

consider, the financial statement shows some account which should be consider by the

auditor in the risk model of the business. The account of the company which are been

consider as risk to the financial user are shown below in a table presentation:

Account

Name

Audit Risk Inherent

Risk

Control

Risk

Detection

Risk

Requirement of

Evidences

Revenue HIGH HIGH (90%) Moderate LOW HIGH

COGS HIGH HIGH (80%) HIGH

(80%)

LOW HIGH

Inventory MODERATE MODERTAE HIGH

(85%)

HIGH HIGH

Payables HIGH HIGH (70%) LOW

(40%)

HIGH HIGH

Table No -1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Auditing

Source – Author

Analytical Review of the Company

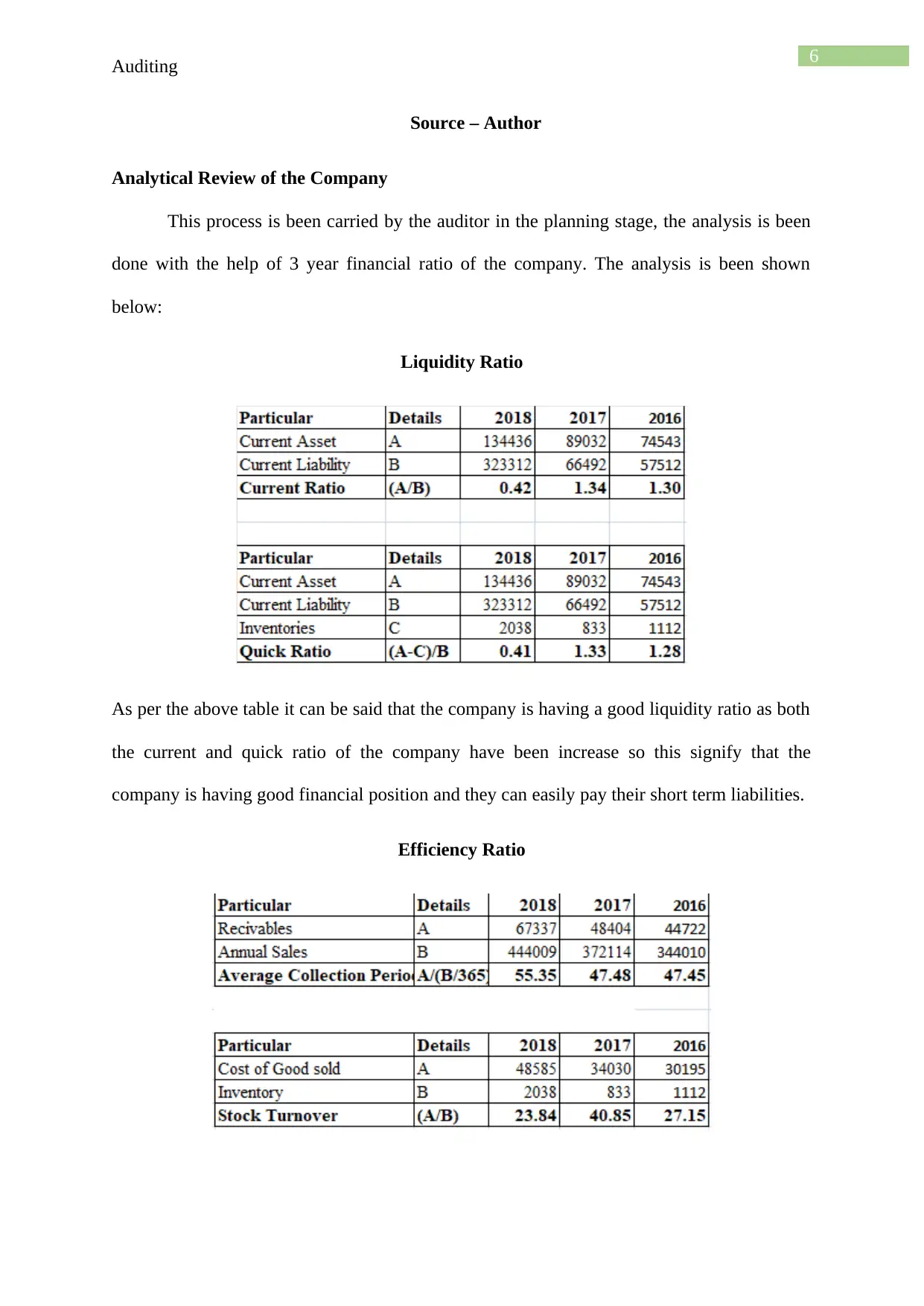

This process is been carried by the auditor in the planning stage, the analysis is been

done with the help of 3 year financial ratio of the company. The analysis is been shown

below:

Liquidity Ratio

As per the above table it can be said that the company is having a good liquidity ratio as both

the current and quick ratio of the company have been increase so this signify that the

company is having good financial position and they can easily pay their short term liabilities.

Efficiency Ratio

Auditing

Source – Author

Analytical Review of the Company

This process is been carried by the auditor in the planning stage, the analysis is been

done with the help of 3 year financial ratio of the company. The analysis is been shown

below:

Liquidity Ratio

As per the above table it can be said that the company is having a good liquidity ratio as both

the current and quick ratio of the company have been increase so this signify that the

company is having good financial position and they can easily pay their short term liabilities.

Efficiency Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Auditing

It can be seen that these ratio have also been increase so it show that the company is bale to

fuller utilization of its asset and able to earn more amount of profit in the business.

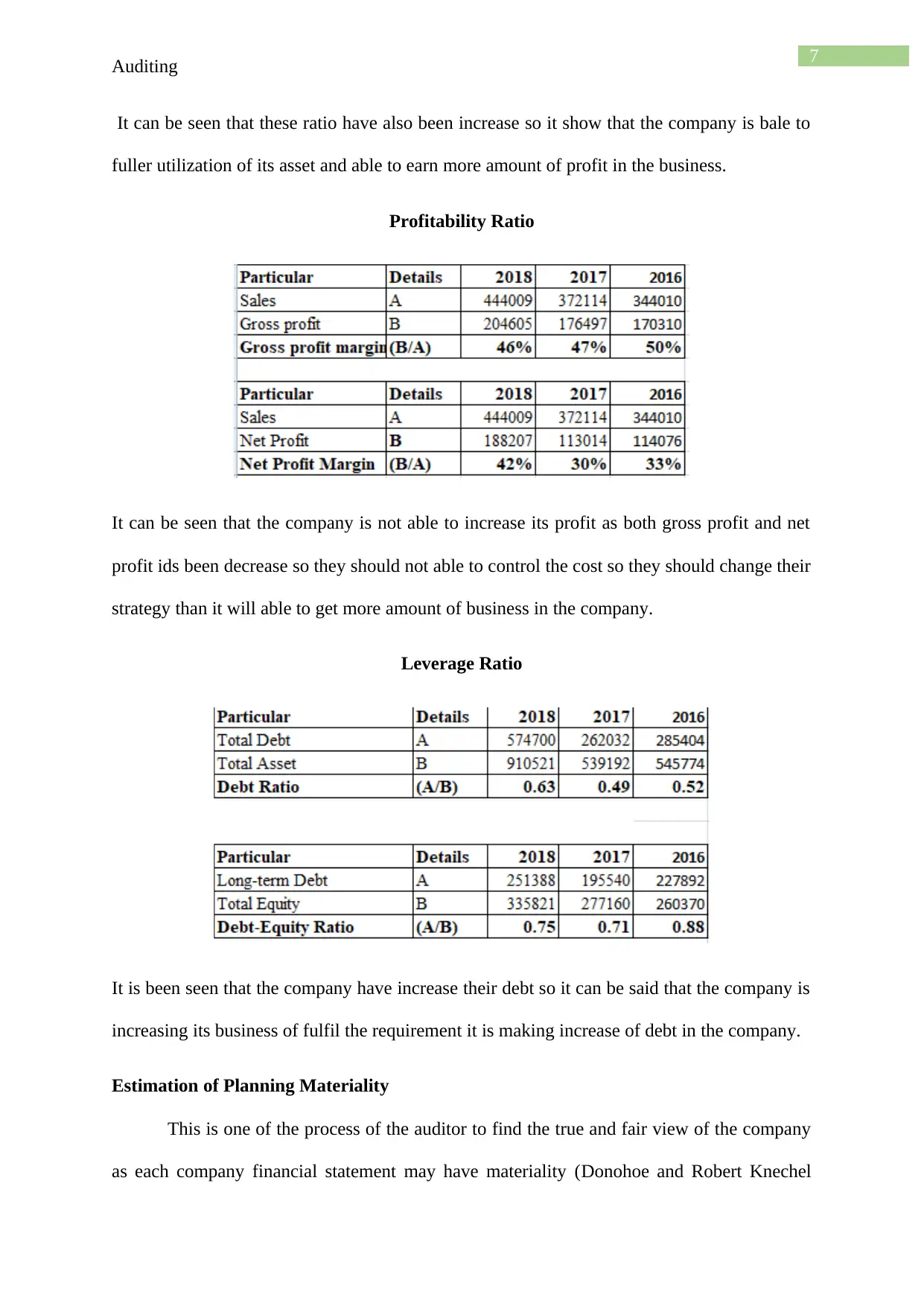

Profitability Ratio

It can be seen that the company is not able to increase its profit as both gross profit and net

profit ids been decrease so they should not able to control the cost so they should change their

strategy than it will able to get more amount of business in the company.

Leverage Ratio

It is been seen that the company have increase their debt so it can be said that the company is

increasing its business of fulfil the requirement it is making increase of debt in the company.

Estimation of Planning Materiality

This is one of the process of the auditor to find the true and fair view of the company

as each company financial statement may have materiality (Donohoe and Robert Knechel

Auditing

It can be seen that these ratio have also been increase so it show that the company is bale to

fuller utilization of its asset and able to earn more amount of profit in the business.

Profitability Ratio

It can be seen that the company is not able to increase its profit as both gross profit and net

profit ids been decrease so they should not able to control the cost so they should change their

strategy than it will able to get more amount of business in the company.

Leverage Ratio

It is been seen that the company have increase their debt so it can be said that the company is

increasing its business of fulfil the requirement it is making increase of debt in the company.

Estimation of Planning Materiality

This is one of the process of the auditor to find the true and fair view of the company

as each company financial statement may have materiality (Donohoe and Robert Knechel

8

Auditing

2014). The auditor each item of the company with the help of materiality concept and gives it

opinion that whether the account is been overvalued or undervalued by the company or not.

This help the auditor to know the estimation and the judgement of the company in regards of

the account and also show the nature and complexity associated with the account. The

analysis which is been done of the company Caresales.com it is been found out by the auditor

the material misstatement is been in the revenue, net profit , current asset and the cost of

goods of the company and also some items in regards of the nature of the business (Ettredge,

Fuerherm and Li 2014.).

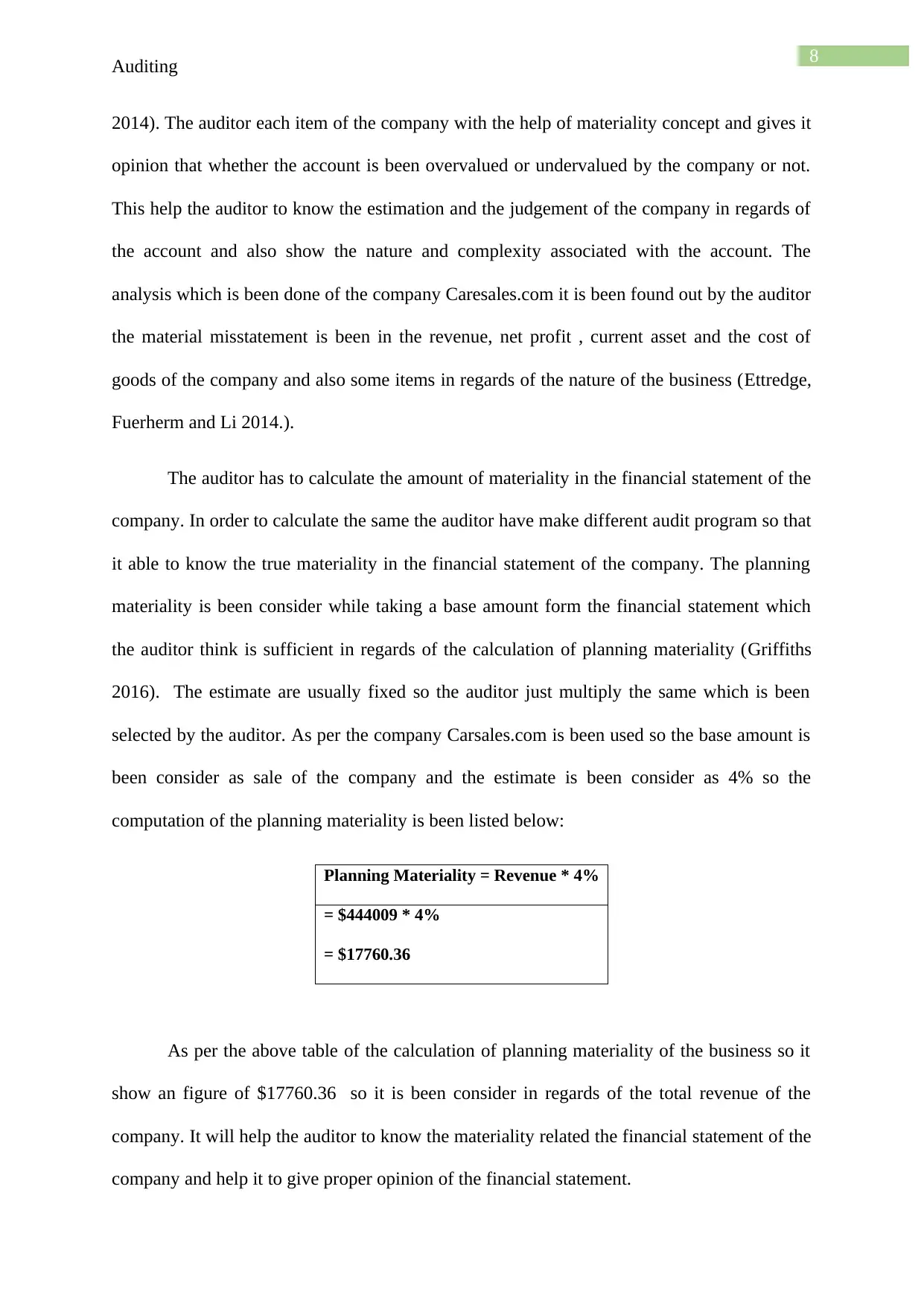

The auditor has to calculate the amount of materiality in the financial statement of the

company. In order to calculate the same the auditor have make different audit program so that

it able to know the true materiality in the financial statement of the company. The planning

materiality is been consider while taking a base amount form the financial statement which

the auditor think is sufficient in regards of the calculation of planning materiality (Griffiths

2016). The estimate are usually fixed so the auditor just multiply the same which is been

selected by the auditor. As per the company Carsales.com is been used so the base amount is

been consider as sale of the company and the estimate is been consider as 4% so the

computation of the planning materiality is been listed below:

Planning Materiality = Revenue * 4%

= $444009 * 4%

= $17760.36

As per the above table of the calculation of planning materiality of the business so it

show an figure of $17760.36 so it is been consider in regards of the total revenue of the

company. It will help the auditor to know the materiality related the financial statement of the

company and help it to give proper opinion of the financial statement.

Auditing

2014). The auditor each item of the company with the help of materiality concept and gives it

opinion that whether the account is been overvalued or undervalued by the company or not.

This help the auditor to know the estimation and the judgement of the company in regards of

the account and also show the nature and complexity associated with the account. The

analysis which is been done of the company Caresales.com it is been found out by the auditor

the material misstatement is been in the revenue, net profit , current asset and the cost of

goods of the company and also some items in regards of the nature of the business (Ettredge,

Fuerherm and Li 2014.).

The auditor has to calculate the amount of materiality in the financial statement of the

company. In order to calculate the same the auditor have make different audit program so that

it able to know the true materiality in the financial statement of the company. The planning

materiality is been consider while taking a base amount form the financial statement which

the auditor think is sufficient in regards of the calculation of planning materiality (Griffiths

2016). The estimate are usually fixed so the auditor just multiply the same which is been

selected by the auditor. As per the company Carsales.com is been used so the base amount is

been consider as sale of the company and the estimate is been consider as 4% so the

computation of the planning materiality is been listed below:

Planning Materiality = Revenue * 4%

= $444009 * 4%

= $17760.36

As per the above table of the calculation of planning materiality of the business so it

show an figure of $17760.36 so it is been consider in regards of the total revenue of the

company. It will help the auditor to know the materiality related the financial statement of the

company and help it to give proper opinion of the financial statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Auditing

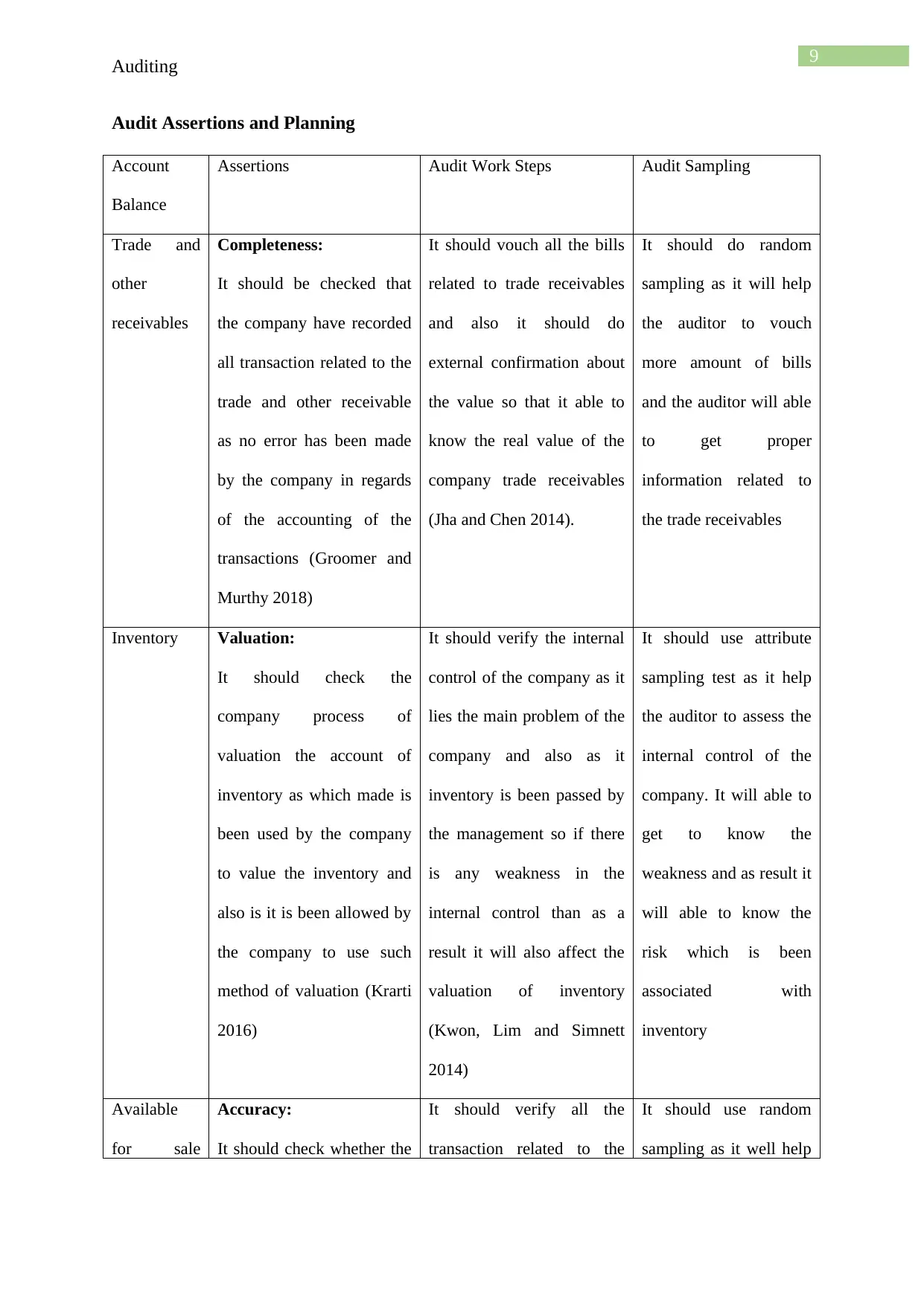

Audit Assertions and Planning

Account

Balance

Assertions Audit Work Steps Audit Sampling

Trade and

other

receivables

Completeness:

It should be checked that

the company have recorded

all transaction related to the

trade and other receivable

as no error has been made

by the company in regards

of the accounting of the

transactions (Groomer and

Murthy 2018)

It should vouch all the bills

related to trade receivables

and also it should do

external confirmation about

the value so that it able to

know the real value of the

company trade receivables

(Jha and Chen 2014).

It should do random

sampling as it will help

the auditor to vouch

more amount of bills

and the auditor will able

to get proper

information related to

the trade receivables

Inventory Valuation:

It should check the

company process of

valuation the account of

inventory as which made is

been used by the company

to value the inventory and

also is it is been allowed by

the company to use such

method of valuation (Krarti

2016)

It should verify the internal

control of the company as it

lies the main problem of the

company and also as it

inventory is been passed by

the management so if there

is any weakness in the

internal control than as a

result it will also affect the

valuation of inventory

(Kwon, Lim and Simnett

2014)

It should use attribute

sampling test as it help

the auditor to assess the

internal control of the

company. It will able to

get to know the

weakness and as result it

will able to know the

risk which is been

associated with

inventory

Available

for sale

Accuracy:

It should check whether the

It should verify all the

transaction related to the

It should use random

sampling as it well help

Auditing

Audit Assertions and Planning

Account

Balance

Assertions Audit Work Steps Audit Sampling

Trade and

other

receivables

Completeness:

It should be checked that

the company have recorded

all transaction related to the

trade and other receivable

as no error has been made

by the company in regards

of the accounting of the

transactions (Groomer and

Murthy 2018)

It should vouch all the bills

related to trade receivables

and also it should do

external confirmation about

the value so that it able to

know the real value of the

company trade receivables

(Jha and Chen 2014).

It should do random

sampling as it will help

the auditor to vouch

more amount of bills

and the auditor will able

to get proper

information related to

the trade receivables

Inventory Valuation:

It should check the

company process of

valuation the account of

inventory as which made is

been used by the company

to value the inventory and

also is it is been allowed by

the company to use such

method of valuation (Krarti

2016)

It should verify the internal

control of the company as it

lies the main problem of the

company and also as it

inventory is been passed by

the management so if there

is any weakness in the

internal control than as a

result it will also affect the

valuation of inventory

(Kwon, Lim and Simnett

2014)

It should use attribute

sampling test as it help

the auditor to assess the

internal control of the

company. It will able to

get to know the

weakness and as result it

will able to know the

risk which is been

associated with

inventory

Available

for sale

Accuracy:

It should check whether the

It should verify all the

transaction related to the

It should use random

sampling as it well help

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Auditing

financial

assets

company have properly

calculated the value of the

asset as it may happen that

there is some calculation

mistake in the account and

as a result it affect the

financial statement of the

company (Lennox, Wu and

Zhang 2014)

asset and also should verify

the amount so it will be

clear that the company have

not done any material

misstatement in the account

(Pizzini, Lin and Ziegenfuss

2014).

it to do verification of

many transaction as the

transaction is very big

so increase number of

sample size will help to

get more accurate

information of the

company account.

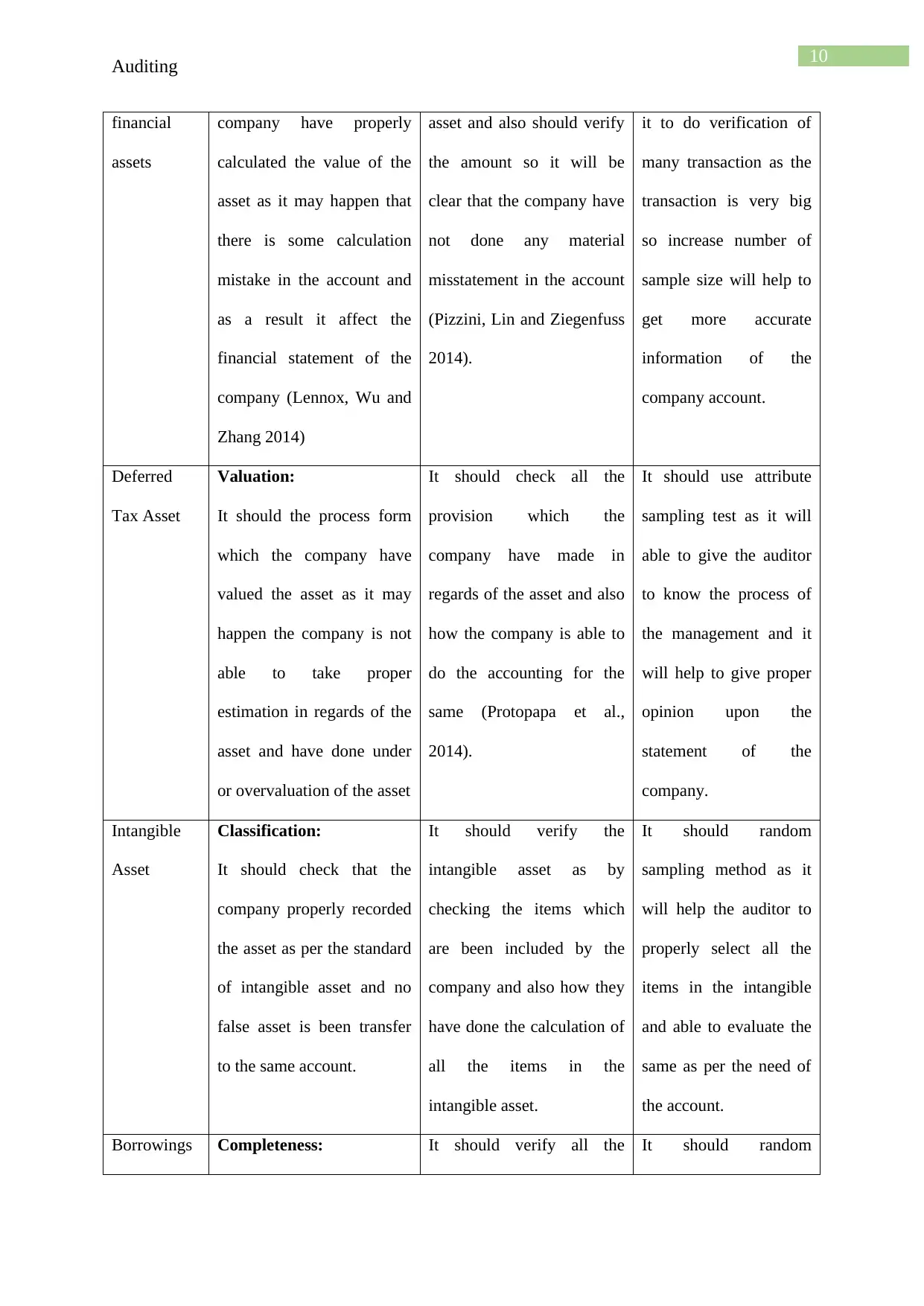

Deferred

Tax Asset

Valuation:

It should the process form

which the company have

valued the asset as it may

happen the company is not

able to take proper

estimation in regards of the

asset and have done under

or overvaluation of the asset

It should check all the

provision which the

company have made in

regards of the asset and also

how the company is able to

do the accounting for the

same (Protopapa et al.,

2014).

It should use attribute

sampling test as it will

able to give the auditor

to know the process of

the management and it

will help to give proper

opinion upon the

statement of the

company.

Intangible

Asset

Classification:

It should check that the

company properly recorded

the asset as per the standard

of intangible asset and no

false asset is been transfer

to the same account.

It should verify the

intangible asset as by

checking the items which

are been included by the

company and also how they

have done the calculation of

all the items in the

intangible asset.

It should random

sampling method as it

will help the auditor to

properly select all the

items in the intangible

and able to evaluate the

same as per the need of

the account.

Borrowings Completeness: It should verify all the It should random

Auditing

financial

assets

company have properly

calculated the value of the

asset as it may happen that

there is some calculation

mistake in the account and

as a result it affect the

financial statement of the

company (Lennox, Wu and

Zhang 2014)

asset and also should verify

the amount so it will be

clear that the company have

not done any material

misstatement in the account

(Pizzini, Lin and Ziegenfuss

2014).

it to do verification of

many transaction as the

transaction is very big

so increase number of

sample size will help to

get more accurate

information of the

company account.

Deferred

Tax Asset

Valuation:

It should the process form

which the company have

valued the asset as it may

happen the company is not

able to take proper

estimation in regards of the

asset and have done under

or overvaluation of the asset

It should check all the

provision which the

company have made in

regards of the asset and also

how the company is able to

do the accounting for the

same (Protopapa et al.,

2014).

It should use attribute

sampling test as it will

able to give the auditor

to know the process of

the management and it

will help to give proper

opinion upon the

statement of the

company.

Intangible

Asset

Classification:

It should check that the

company properly recorded

the asset as per the standard

of intangible asset and no

false asset is been transfer

to the same account.

It should verify the

intangible asset as by

checking the items which

are been included by the

company and also how they

have done the calculation of

all the items in the

intangible asset.

It should random

sampling method as it

will help the auditor to

properly select all the

items in the intangible

and able to evaluate the

same as per the need of

the account.

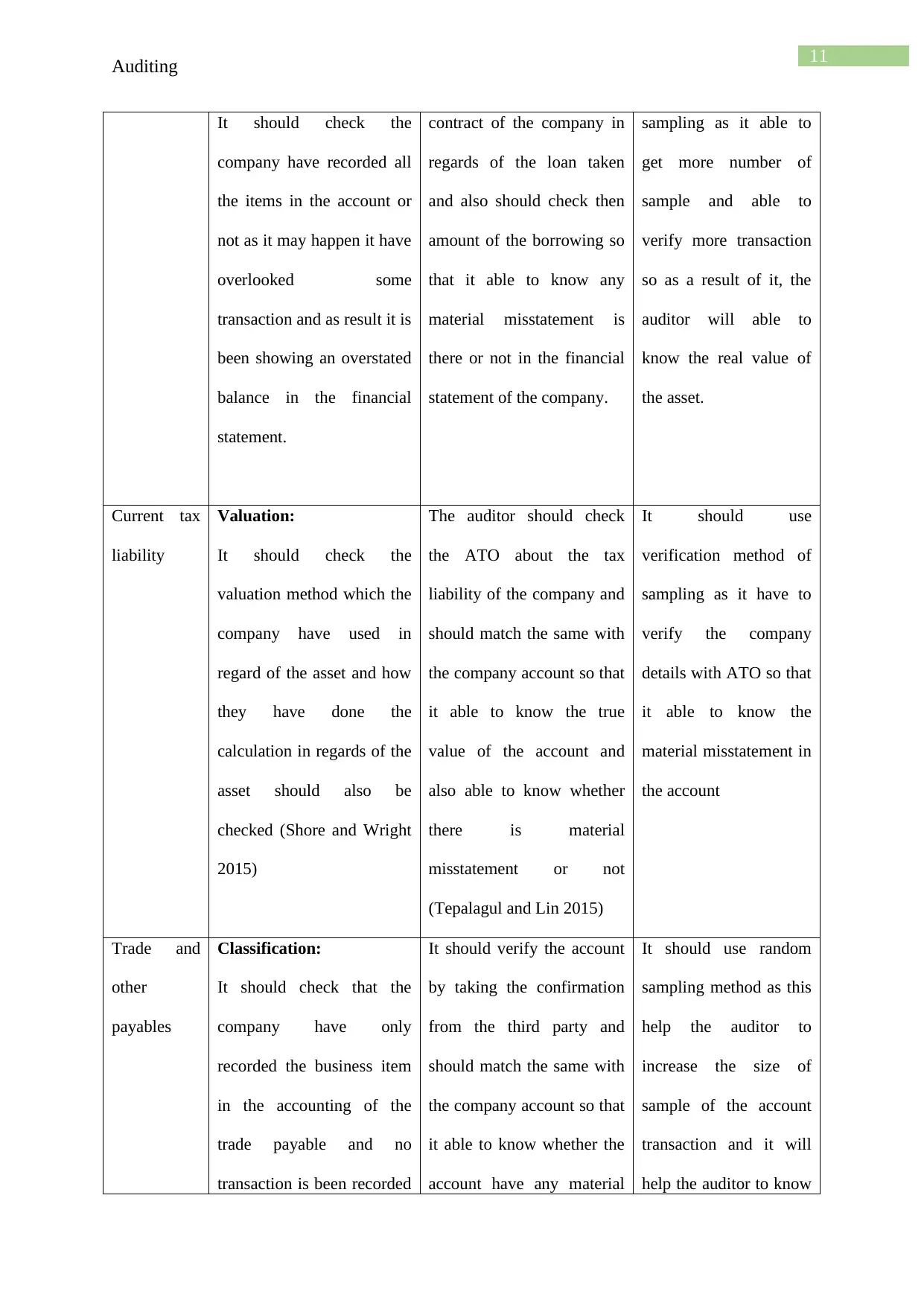

Borrowings Completeness: It should verify all the It should random

11

Auditing

It should check the

company have recorded all

the items in the account or

not as it may happen it have

overlooked some

transaction and as result it is

been showing an overstated

balance in the financial

statement.

contract of the company in

regards of the loan taken

and also should check then

amount of the borrowing so

that it able to know any

material misstatement is

there or not in the financial

statement of the company.

sampling as it able to

get more number of

sample and able to

verify more transaction

so as a result of it, the

auditor will able to

know the real value of

the asset.

Current tax

liability

Valuation:

It should check the

valuation method which the

company have used in

regard of the asset and how

they have done the

calculation in regards of the

asset should also be

checked (Shore and Wright

2015)

The auditor should check

the ATO about the tax

liability of the company and

should match the same with

the company account so that

it able to know the true

value of the account and

also able to know whether

there is material

misstatement or not

(Tepalagul and Lin 2015)

It should use

verification method of

sampling as it have to

verify the company

details with ATO so that

it able to know the

material misstatement in

the account

Trade and

other

payables

Classification:

It should check that the

company have only

recorded the business item

in the accounting of the

trade payable and no

transaction is been recorded

It should verify the account

by taking the confirmation

from the third party and

should match the same with

the company account so that

it able to know whether the

account have any material

It should use random

sampling method as this

help the auditor to

increase the size of

sample of the account

transaction and it will

help the auditor to know

Auditing

It should check the

company have recorded all

the items in the account or

not as it may happen it have

overlooked some

transaction and as result it is

been showing an overstated

balance in the financial

statement.

contract of the company in

regards of the loan taken

and also should check then

amount of the borrowing so

that it able to know any

material misstatement is

there or not in the financial

statement of the company.

sampling as it able to

get more number of

sample and able to

verify more transaction

so as a result of it, the

auditor will able to

know the real value of

the asset.

Current tax

liability

Valuation:

It should check the

valuation method which the

company have used in

regard of the asset and how

they have done the

calculation in regards of the

asset should also be

checked (Shore and Wright

2015)

The auditor should check

the ATO about the tax

liability of the company and

should match the same with

the company account so that

it able to know the true

value of the account and

also able to know whether

there is material

misstatement or not

(Tepalagul and Lin 2015)

It should use

verification method of

sampling as it have to

verify the company

details with ATO so that

it able to know the

material misstatement in

the account

Trade and

other

payables

Classification:

It should check that the

company have only

recorded the business item

in the accounting of the

trade payable and no

transaction is been recorded

It should verify the account

by taking the confirmation

from the third party and

should match the same with

the company account so that

it able to know whether the

account have any material

It should use random

sampling method as this

help the auditor to

increase the size of

sample of the account

transaction and it will

help the auditor to know

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.