Managerial Accounting: Cost-Volume-Profit Analysis and Budgeting Cases

VerifiedAdded on 2023/06/15

|16

|2947

|398

Case Study

AI Summary

This document presents solutions to several case studies in managerial accounting, covering topics such as cost analysis, profit maximization, and budgeting. The first case examines the profitability of a catering company's standard cocktail party and explores bidding strategies for a charity event. The second case analyzes sales commission structures and evaluates the financial implications of employing a dedicated sales force versus using independent agents, including breakeven point calculations and operating income projections. The final case focuses on the impact of new machinery on overhead rates and job costing, assessing the cost implications and managerial concerns associated with the changes. The analysis and solutions are presented with detailed calculations and justifications.

Running head: MANAGERIAL ACCOUNT

Managerial Account

Name of the Student:

Name of the University:

Author Note

Managerial Account

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGERIAL ACCOUNT

Table of Contents

Answer to Case 3-20........................................................................................................................2

Answer to Requirement 1............................................................................................................2

Answer to Requirement 2............................................................................................................3

Answer to Requirement 3............................................................................................................3

Answer to Case 4-34........................................................................................................................4

Answer to Requirement 1............................................................................................................4

Answer to Requirement 2............................................................................................................4

Answer to Requirement 3............................................................................................................5

Answer to Requirement 4............................................................................................................6

Answer to Requirement 5............................................................................................................6

Answer to Requirement 6............................................................................................................7

Answer to Case 5-30........................................................................................................................9

Answer to Requirement 1............................................................................................................9

Answer to Requirement 2..........................................................................................................10

Answer to Requirement 3..........................................................................................................10

Answer to Requirement 4..........................................................................................................10

References and Bibliography:........................................................................................................12

MANAGERIAL ACCOUNT

Table of Contents

Answer to Case 3-20........................................................................................................................2

Answer to Requirement 1............................................................................................................2

Answer to Requirement 2............................................................................................................3

Answer to Requirement 3............................................................................................................3

Answer to Case 4-34........................................................................................................................4

Answer to Requirement 1............................................................................................................4

Answer to Requirement 2............................................................................................................4

Answer to Requirement 3............................................................................................................5

Answer to Requirement 4............................................................................................................6

Answer to Requirement 5............................................................................................................6

Answer to Requirement 6............................................................................................................7

Answer to Case 5-30........................................................................................................................9

Answer to Requirement 1............................................................................................................9

Answer to Requirement 2..........................................................................................................10

Answer to Requirement 3..........................................................................................................10

Answer to Requirement 4..........................................................................................................10

References and Bibliography:........................................................................................................12

2

MANAGERIAL ACCOUNT

MANAGERIAL ACCOUNT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGERIAL ACCOUNT

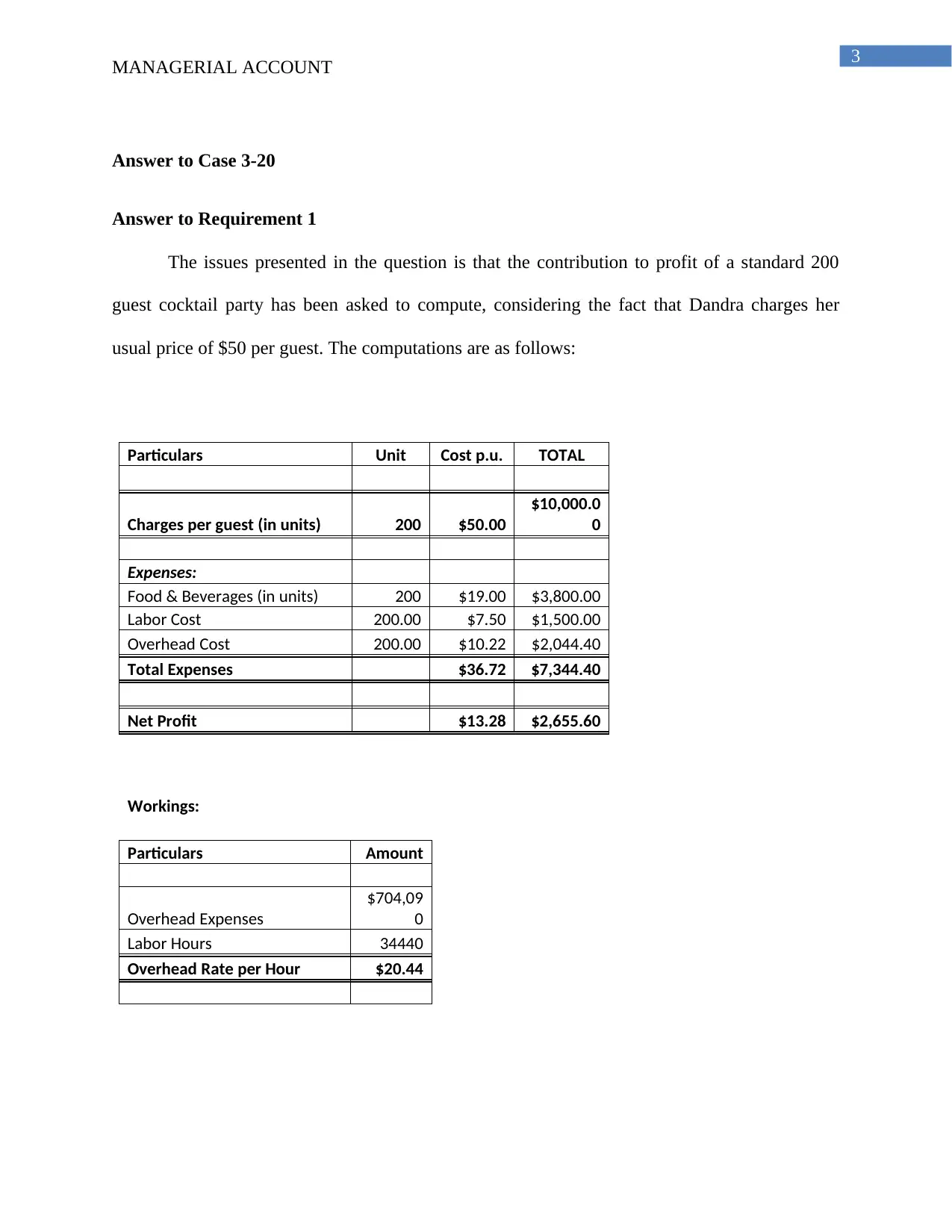

Answer to Case 3-20

Answer to Requirement 1

The issues presented in the question is that the contribution to profit of a standard 200

guest cocktail party has been asked to compute, considering the fact that Dandra charges her

usual price of $50 per guest. The computations are as follows:

Particulars Unit Cost p.u. TOTAL

Charges per guest (in units) 200 $50.00

$10,000.0

0

Expenses:

Food & Beverages (in units) 200 $19.00 $3,800.00

Labor Cost 200.00 $7.50 $1,500.00

Overhead Cost 200.00 $10.22 $2,044.40

Total Expenses $36.72 $7,344.40

Net Profit $13.28 $2,655.60

Workings:

Particulars Amount

Overhead Expenses

$704,09

0

Labor Hours 34440

Overhead Rate per Hour $20.44

MANAGERIAL ACCOUNT

Answer to Case 3-20

Answer to Requirement 1

The issues presented in the question is that the contribution to profit of a standard 200

guest cocktail party has been asked to compute, considering the fact that Dandra charges her

usual price of $50 per guest. The computations are as follows:

Particulars Unit Cost p.u. TOTAL

Charges per guest (in units) 200 $50.00

$10,000.0

0

Expenses:

Food & Beverages (in units) 200 $19.00 $3,800.00

Labor Cost 200.00 $7.50 $1,500.00

Overhead Cost 200.00 $10.22 $2,044.40

Total Expenses $36.72 $7,344.40

Net Profit $13.28 $2,655.60

Workings:

Particulars Amount

Overhead Expenses

$704,09

0

Labor Hours 34440

Overhead Rate per Hour $20.44

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGERIAL ACCOUNT

Answer to Requirement 2

In the answer to requirement 1, the table shows the charges per guest that is $50.00 per

unit. However, the total expenses that have been computed amount up to $36.72. This means that

the net profit that has been deduced from the business venture amounts to $13.28 per unit and

$2,655.60 in total. Now, the issues that have been presented in this particular question is the exct

way in which Dandra could bid for the charity event in terms of price per guest and still not lose

money on the event itself. Thus, as apparent from the above table Dandra could bid any price in

terms of per guest, above or equal to $39. A price of $39 or above it would ascertain the fact that

Dandra deals in profit and not lose money on the event itself (Barr & McClellan, 2018).

Answer to Requirement 3

The issue presented in this particular question is that the organizer of the charity’s

fundraising event has pointed out the singular fact that there has been already a receipt of a bid

under $45 from another catering company. As discussed in the above question Dandra bidding

anything above or equal to 39$ in terms of price per guest would result in a profit. However, the

profit margin has to be kept in mind by the owner of the catering company. A price per guest of

$50 would fetch a profit of $13.28. However, lowering the price per guest would result in the

lowering of the profit margin but Dandra could bid for an amount lower than $45, which would

still result in a profit. Therefore, Dandra should bid below her normal $50 per guest price for the

charity event, which would fetch lower but substantial profit to the catering company and

increase the chances of Dandra winning the bid (Chikoto & Neely, 2014).

MANAGERIAL ACCOUNT

Answer to Requirement 2

In the answer to requirement 1, the table shows the charges per guest that is $50.00 per

unit. However, the total expenses that have been computed amount up to $36.72. This means that

the net profit that has been deduced from the business venture amounts to $13.28 per unit and

$2,655.60 in total. Now, the issues that have been presented in this particular question is the exct

way in which Dandra could bid for the charity event in terms of price per guest and still not lose

money on the event itself. Thus, as apparent from the above table Dandra could bid any price in

terms of per guest, above or equal to $39. A price of $39 or above it would ascertain the fact that

Dandra deals in profit and not lose money on the event itself (Barr & McClellan, 2018).

Answer to Requirement 3

The issue presented in this particular question is that the organizer of the charity’s

fundraising event has pointed out the singular fact that there has been already a receipt of a bid

under $45 from another catering company. As discussed in the above question Dandra bidding

anything above or equal to 39$ in terms of price per guest would result in a profit. However, the

profit margin has to be kept in mind by the owner of the catering company. A price per guest of

$50 would fetch a profit of $13.28. However, lowering the price per guest would result in the

lowering of the profit margin but Dandra could bid for an amount lower than $45, which would

still result in a profit. Therefore, Dandra should bid below her normal $50 per guest price for the

charity event, which would fetch lower but substantial profit to the catering company and

increase the chances of Dandra winning the bid (Chikoto & Neely, 2014).

5

MANAGERIAL ACCOUNT

Answer to Case 4-34

Answer to Requirement 1

Particulars

Sales

Commission @

19%

Sales

Commission @

22%

Own Sales

Force

Sales $15,000,000 $15,000,000 $15,000,000

Cost of Goods Sold:

Fixed -$8,400,000 -$8,400,000 -$8,400,000

Variable -$1,400,000 -$1,400,000 -$1,400,000

Total Cost of Goods Sold -$9,800,000 -$9,800,000 -$9,800,000

Gross Margin $5,200,000 $5,200,000 $5,200,000

Selling & Administrative

Expenses:

Commissions -$2,850,000 -$3,300,000 -$1,800,000

Travel & Entertainment Expenses -$200,000

Fixed Advertising Expenses -$400,000 -$400,000 -$650,000

Fixed Administrative Expenses -$1,600,000 -$1,600,000 -$1,600,000

Fixed Payroll Expenses of Sales

People -$350,000

Fixed Payroll Expenses of Sales

Manager & Support Staffs -$100,000

Total Selling & Administrative

Expenses -$4,850,000 -$5,300,000 -$4,700,000

Operating Income $350,000 -$100,000 $500,000

Answer to Requirement 2

Particulars

Sales

Commission @

19%

Sales

Commission @

22%

Own Sales

Force

Sales $15,000,000 $15,000,000 $15,000,000

Variable Expenses:

MANAGERIAL ACCOUNT

Answer to Case 4-34

Answer to Requirement 1

Particulars

Sales

Commission @

19%

Sales

Commission @

22%

Own Sales

Force

Sales $15,000,000 $15,000,000 $15,000,000

Cost of Goods Sold:

Fixed -$8,400,000 -$8,400,000 -$8,400,000

Variable -$1,400,000 -$1,400,000 -$1,400,000

Total Cost of Goods Sold -$9,800,000 -$9,800,000 -$9,800,000

Gross Margin $5,200,000 $5,200,000 $5,200,000

Selling & Administrative

Expenses:

Commissions -$2,850,000 -$3,300,000 -$1,800,000

Travel & Entertainment Expenses -$200,000

Fixed Advertising Expenses -$400,000 -$400,000 -$650,000

Fixed Administrative Expenses -$1,600,000 -$1,600,000 -$1,600,000

Fixed Payroll Expenses of Sales

People -$350,000

Fixed Payroll Expenses of Sales

Manager & Support Staffs -$100,000

Total Selling & Administrative

Expenses -$4,850,000 -$5,300,000 -$4,700,000

Operating Income $350,000 -$100,000 $500,000

Answer to Requirement 2

Particulars

Sales

Commission @

19%

Sales

Commission @

22%

Own Sales

Force

Sales $15,000,000 $15,000,000 $15,000,000

Variable Expenses:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGERIAL ACCOUNT

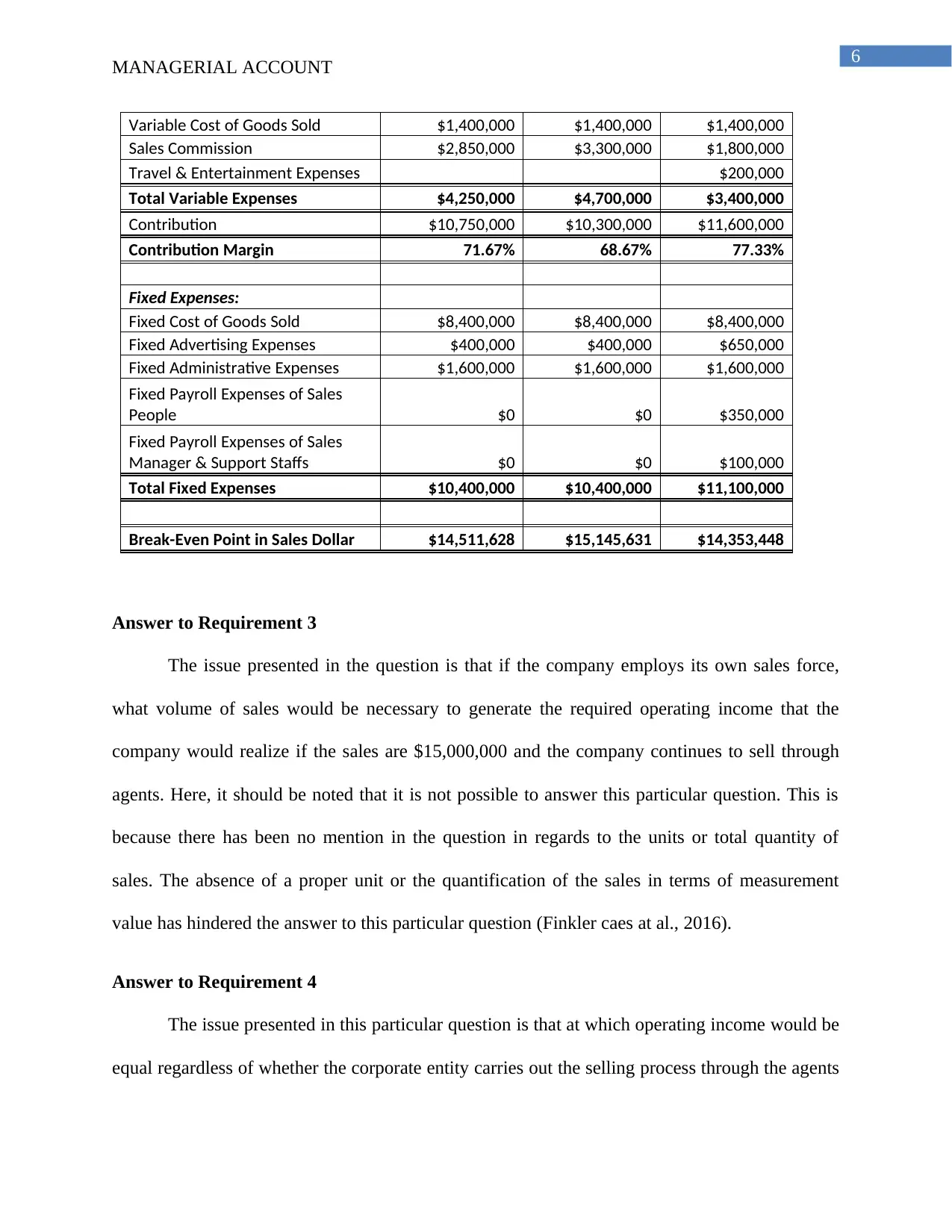

Variable Cost of Goods Sold $1,400,000 $1,400,000 $1,400,000

Sales Commission $2,850,000 $3,300,000 $1,800,000

Travel & Entertainment Expenses $200,000

Total Variable Expenses $4,250,000 $4,700,000 $3,400,000

Contribution $10,750,000 $10,300,000 $11,600,000

Contribution Margin 71.67% 68.67% 77.33%

Fixed Expenses:

Fixed Cost of Goods Sold $8,400,000 $8,400,000 $8,400,000

Fixed Advertising Expenses $400,000 $400,000 $650,000

Fixed Administrative Expenses $1,600,000 $1,600,000 $1,600,000

Fixed Payroll Expenses of Sales

People $0 $0 $350,000

Fixed Payroll Expenses of Sales

Manager & Support Staffs $0 $0 $100,000

Total Fixed Expenses $10,400,000 $10,400,000 $11,100,000

Break-Even Point in Sales Dollar $14,511,628 $15,145,631 $14,353,448

Answer to Requirement 3

The issue presented in the question is that if the company employs its own sales force,

what volume of sales would be necessary to generate the required operating income that the

company would realize if the sales are $15,000,000 and the company continues to sell through

agents. Here, it should be noted that it is not possible to answer this particular question. This is

because there has been no mention in the question in regards to the units or total quantity of

sales. The absence of a proper unit or the quantification of the sales in terms of measurement

value has hindered the answer to this particular question (Finkler caes at al., 2016).

Answer to Requirement 4

The issue presented in this particular question is that at which operating income would be

equal regardless of whether the corporate entity carries out the selling process through the agents

MANAGERIAL ACCOUNT

Variable Cost of Goods Sold $1,400,000 $1,400,000 $1,400,000

Sales Commission $2,850,000 $3,300,000 $1,800,000

Travel & Entertainment Expenses $200,000

Total Variable Expenses $4,250,000 $4,700,000 $3,400,000

Contribution $10,750,000 $10,300,000 $11,600,000

Contribution Margin 71.67% 68.67% 77.33%

Fixed Expenses:

Fixed Cost of Goods Sold $8,400,000 $8,400,000 $8,400,000

Fixed Advertising Expenses $400,000 $400,000 $650,000

Fixed Administrative Expenses $1,600,000 $1,600,000 $1,600,000

Fixed Payroll Expenses of Sales

People $0 $0 $350,000

Fixed Payroll Expenses of Sales

Manager & Support Staffs $0 $0 $100,000

Total Fixed Expenses $10,400,000 $10,400,000 $11,100,000

Break-Even Point in Sales Dollar $14,511,628 $15,145,631 $14,353,448

Answer to Requirement 3

The issue presented in the question is that if the company employs its own sales force,

what volume of sales would be necessary to generate the required operating income that the

company would realize if the sales are $15,000,000 and the company continues to sell through

agents. Here, it should be noted that it is not possible to answer this particular question. This is

because there has been no mention in the question in regards to the units or total quantity of

sales. The absence of a proper unit or the quantification of the sales in terms of measurement

value has hindered the answer to this particular question (Finkler caes at al., 2016).

Answer to Requirement 4

The issue presented in this particular question is that at which operating income would be

equal regardless of whether the corporate entity carries out the selling process through the agents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGERIAL ACCOUNT

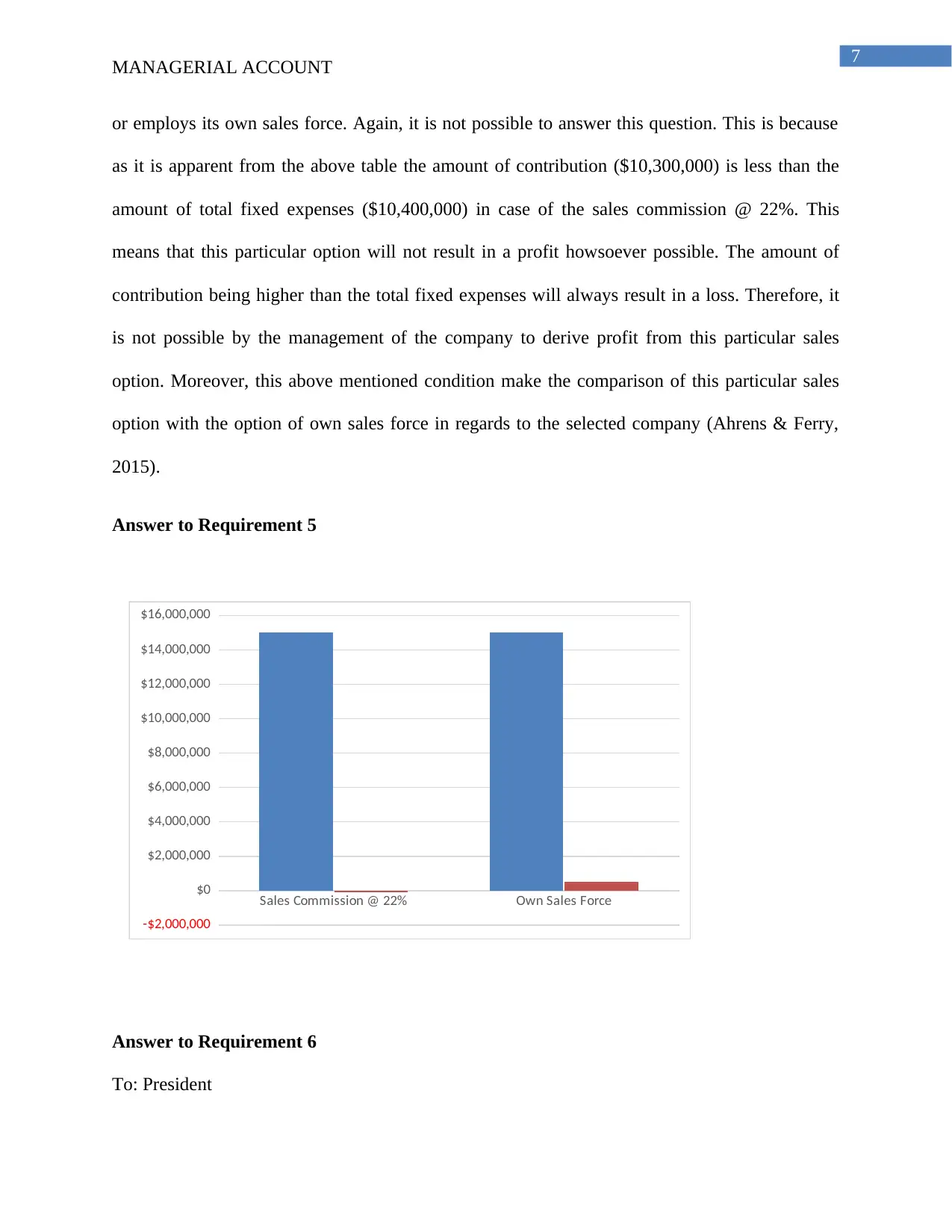

or employs its own sales force. Again, it is not possible to answer this question. This is because

as it is apparent from the above table the amount of contribution ($10,300,000) is less than the

amount of total fixed expenses ($10,400,000) in case of the sales commission @ 22%. This

means that this particular option will not result in a profit howsoever possible. The amount of

contribution being higher than the total fixed expenses will always result in a loss. Therefore, it

is not possible by the management of the company to derive profit from this particular sales

option. Moreover, this above mentioned condition make the comparison of this particular sales

option with the option of own sales force in regards to the selected company (Ahrens & Ferry,

2015).

Answer to Requirement 5

Answer to Requirement 6

To: President

Sales Commission @ 22% Own Sales Force

-$2,000,000

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

MANAGERIAL ACCOUNT

or employs its own sales force. Again, it is not possible to answer this question. This is because

as it is apparent from the above table the amount of contribution ($10,300,000) is less than the

amount of total fixed expenses ($10,400,000) in case of the sales commission @ 22%. This

means that this particular option will not result in a profit howsoever possible. The amount of

contribution being higher than the total fixed expenses will always result in a loss. Therefore, it

is not possible by the management of the company to derive profit from this particular sales

option. Moreover, this above mentioned condition make the comparison of this particular sales

option with the option of own sales force in regards to the selected company (Ahrens & Ferry,

2015).

Answer to Requirement 5

Answer to Requirement 6

To: President

Sales Commission @ 22% Own Sales Force

-$2,000,000

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

8

MANAGERIAL ACCOUNT

Date: February 20, 2018

Subject: Business recommendation in regards to the sales option that the company should use

Sir,

This is to inform you that your corporation has been of recognizable repute and has been

working brilliantly throughout the past financial years. This means that the company has been

distributing products of genuine quality and has earned goodwill and trust of its both commercial

and business clients. However, as mentioned in the case report, the current issue that the

company is facing in regards to the sales and distribution of its photocopiers have been as

follows:

The current commission rate that the independent sales agents are paid is already high.

This means that the independent sales agents are paid a 19% sales commission, which

invariably decreases the net revenue that has been derived by the firm. Moreover, this has

also increased the cost of goods sold that has ultimately decreased the projected sales of

the firm

The recent news has been that the sales agents have been demanding an increase in the

total rate of commission that they receive as a part of sales. This is, as reported by the

management of the corporate entity the third increase in commissions that has been

demanded by the sales agents in five years. Therefore, it can be well predicted here that

the independent sales agents would again demand for a hike in the rate of sales

commission in the near future and this would in turn gradually decrease the total profit

derived by the company from the sale of photocopying machines.

MANAGERIAL ACCOUNT

Date: February 20, 2018

Subject: Business recommendation in regards to the sales option that the company should use

Sir,

This is to inform you that your corporation has been of recognizable repute and has been

working brilliantly throughout the past financial years. This means that the company has been

distributing products of genuine quality and has earned goodwill and trust of its both commercial

and business clients. However, as mentioned in the case report, the current issue that the

company is facing in regards to the sales and distribution of its photocopiers have been as

follows:

The current commission rate that the independent sales agents are paid is already high.

This means that the independent sales agents are paid a 19% sales commission, which

invariably decreases the net revenue that has been derived by the firm. Moreover, this has

also increased the cost of goods sold that has ultimately decreased the projected sales of

the firm

The recent news has been that the sales agents have been demanding an increase in the

total rate of commission that they receive as a part of sales. This is, as reported by the

management of the corporate entity the third increase in commissions that has been

demanded by the sales agents in five years. Therefore, it can be well predicted here that

the independent sales agents would again demand for a hike in the rate of sales

commission in the near future and this would in turn gradually decrease the total profit

derived by the company from the sale of photocopying machines.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGERIAL ACCOUNT

This has resulted in the management of the corporate entity to think about the

development of a group of highly motivated and ambitious sales team that would be

personally owned by the company so that they can cut back on the costs in regards to

sales commission and focus more on enhancing and expanding the sales of the product.

The budgets in regards to the payroll of these sales employees have also been preparfed

and the total number of sales staff that should be appointed in order to cover for the

current business market area has been fixed at six.

Now, the particular recommendation in the case that whether Crescent Corporation

should continue selling the products via the independent sales agents or should develop its own

sales team has been justified by the following facts:

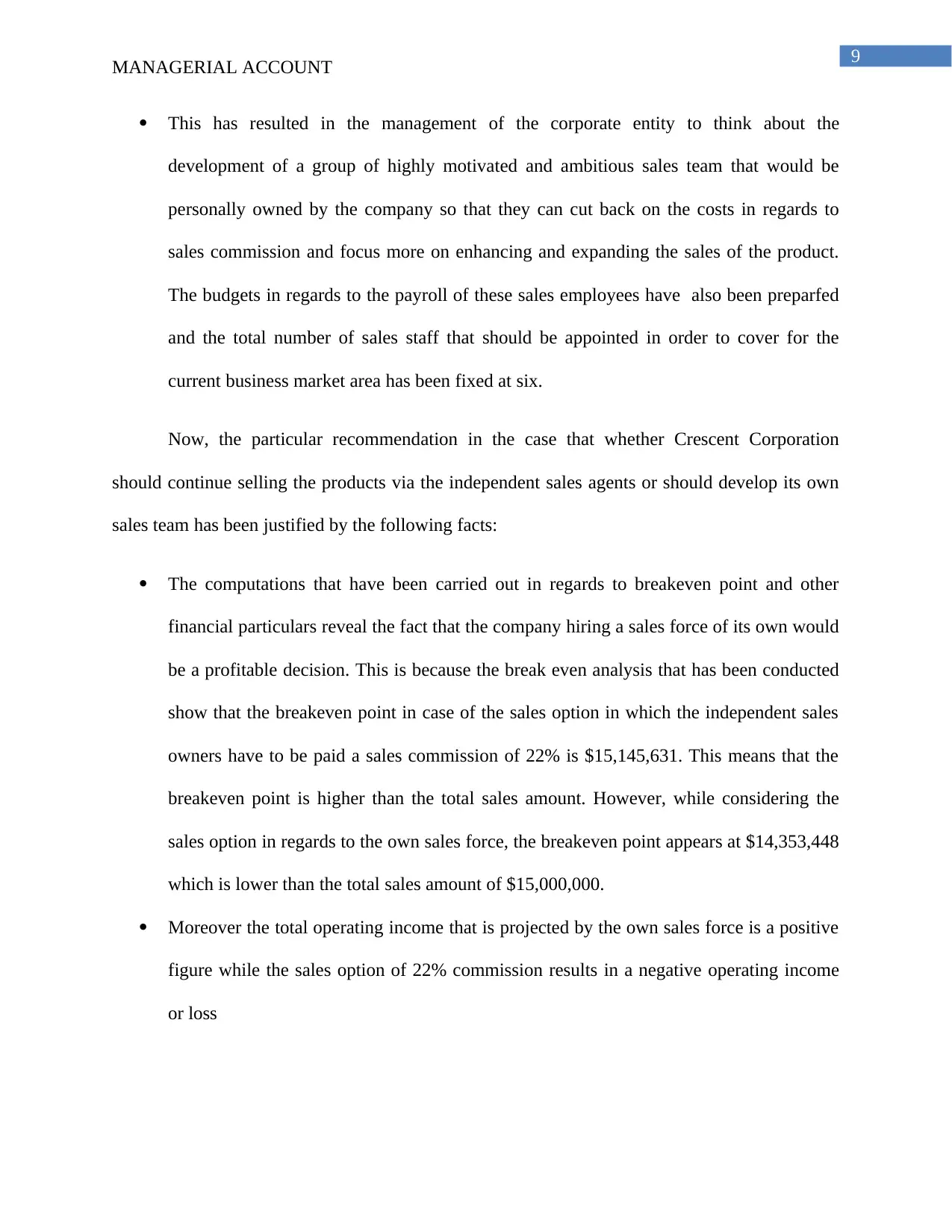

The computations that have been carried out in regards to breakeven point and other

financial particulars reveal the fact that the company hiring a sales force of its own would

be a profitable decision. This is because the break even analysis that has been conducted

show that the breakeven point in case of the sales option in which the independent sales

owners have to be paid a sales commission of 22% is $15,145,631. This means that the

breakeven point is higher than the total sales amount. However, while considering the

sales option in regards to the own sales force, the breakeven point appears at $14,353,448

which is lower than the total sales amount of $15,000,000.

Moreover the total operating income that is projected by the own sales force is a positive

figure while the sales option of 22% commission results in a negative operating income

or loss

MANAGERIAL ACCOUNT

This has resulted in the management of the corporate entity to think about the

development of a group of highly motivated and ambitious sales team that would be

personally owned by the company so that they can cut back on the costs in regards to

sales commission and focus more on enhancing and expanding the sales of the product.

The budgets in regards to the payroll of these sales employees have also been preparfed

and the total number of sales staff that should be appointed in order to cover for the

current business market area has been fixed at six.

Now, the particular recommendation in the case that whether Crescent Corporation

should continue selling the products via the independent sales agents or should develop its own

sales team has been justified by the following facts:

The computations that have been carried out in regards to breakeven point and other

financial particulars reveal the fact that the company hiring a sales force of its own would

be a profitable decision. This is because the break even analysis that has been conducted

show that the breakeven point in case of the sales option in which the independent sales

owners have to be paid a sales commission of 22% is $15,145,631. This means that the

breakeven point is higher than the total sales amount. However, while considering the

sales option in regards to the own sales force, the breakeven point appears at $14,353,448

which is lower than the total sales amount of $15,000,000.

Moreover the total operating income that is projected by the own sales force is a positive

figure while the sales option of 22% commission results in a negative operating income

or loss

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGERIAL ACCOUNT

Thus, it is highly recommended that the company opt for selling its photocopier machines

via the personally developed sales team. This means that the corporate entity should acquire all

the rights from the independent sales agents and give them to the sales team that has been

planned to hire and built. It should be noted here that the initial phase of such a brand new sales

structure might be tough. This is because the newly developed sales team might need some time

in order to understand the tricks of the trade and achieve the desired or projected sales revenue.

However, with the passage of time and the gaining of the required experience will make the sales

team competent enough in order to derive the projected revenues that will be higher than the

current revenue gained by the company.

Best Regards,

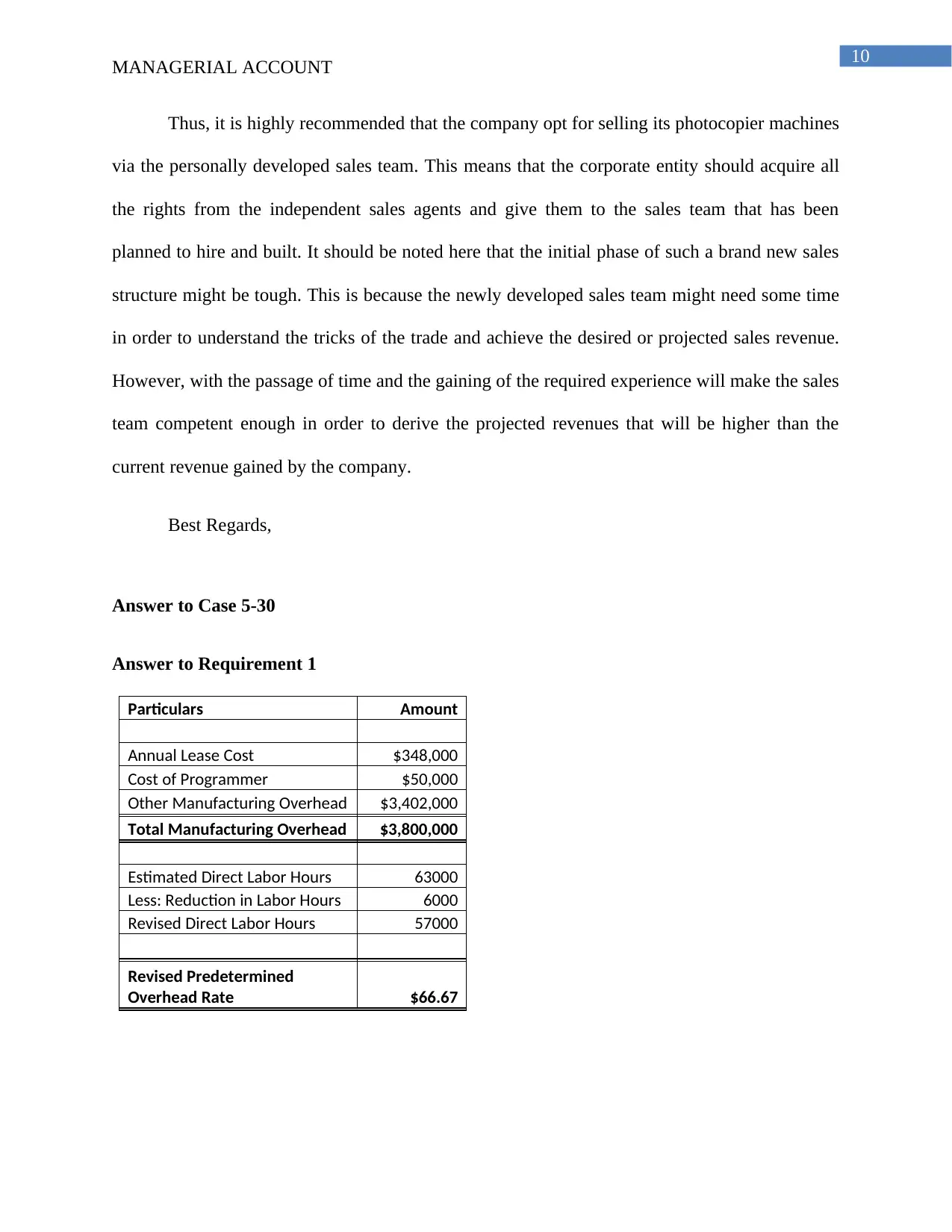

Answer to Case 5-30

Answer to Requirement 1

Particulars Amount

Annual Lease Cost $348,000

Cost of Programmer $50,000

Other Manufacturing Overhead $3,402,000

Total Manufacturing Overhead $3,800,000

Estimated Direct Labor Hours 63000

Less: Reduction in Labor Hours 6000

Revised Direct Labor Hours 57000

Revised Predetermined

Overhead Rate $66.67

MANAGERIAL ACCOUNT

Thus, it is highly recommended that the company opt for selling its photocopier machines

via the personally developed sales team. This means that the corporate entity should acquire all

the rights from the independent sales agents and give them to the sales team that has been

planned to hire and built. It should be noted here that the initial phase of such a brand new sales

structure might be tough. This is because the newly developed sales team might need some time

in order to understand the tricks of the trade and achieve the desired or projected sales revenue.

However, with the passage of time and the gaining of the required experience will make the sales

team competent enough in order to derive the projected revenues that will be higher than the

current revenue gained by the company.

Best Regards,

Answer to Case 5-30

Answer to Requirement 1

Particulars Amount

Annual Lease Cost $348,000

Cost of Programmer $50,000

Other Manufacturing Overhead $3,402,000

Total Manufacturing Overhead $3,800,000

Estimated Direct Labor Hours 63000

Less: Reduction in Labor Hours 6000

Revised Direct Labor Hours 57000

Revised Predetermined

Overhead Rate $66.67

11

MANAGERIAL ACCOUNT

The new predetermined overhead rate is higher than the previous rate. This is because

this rate includes the indirect costs that have been included due to the installation of the new

machine. The annual lease cost is one such cost.

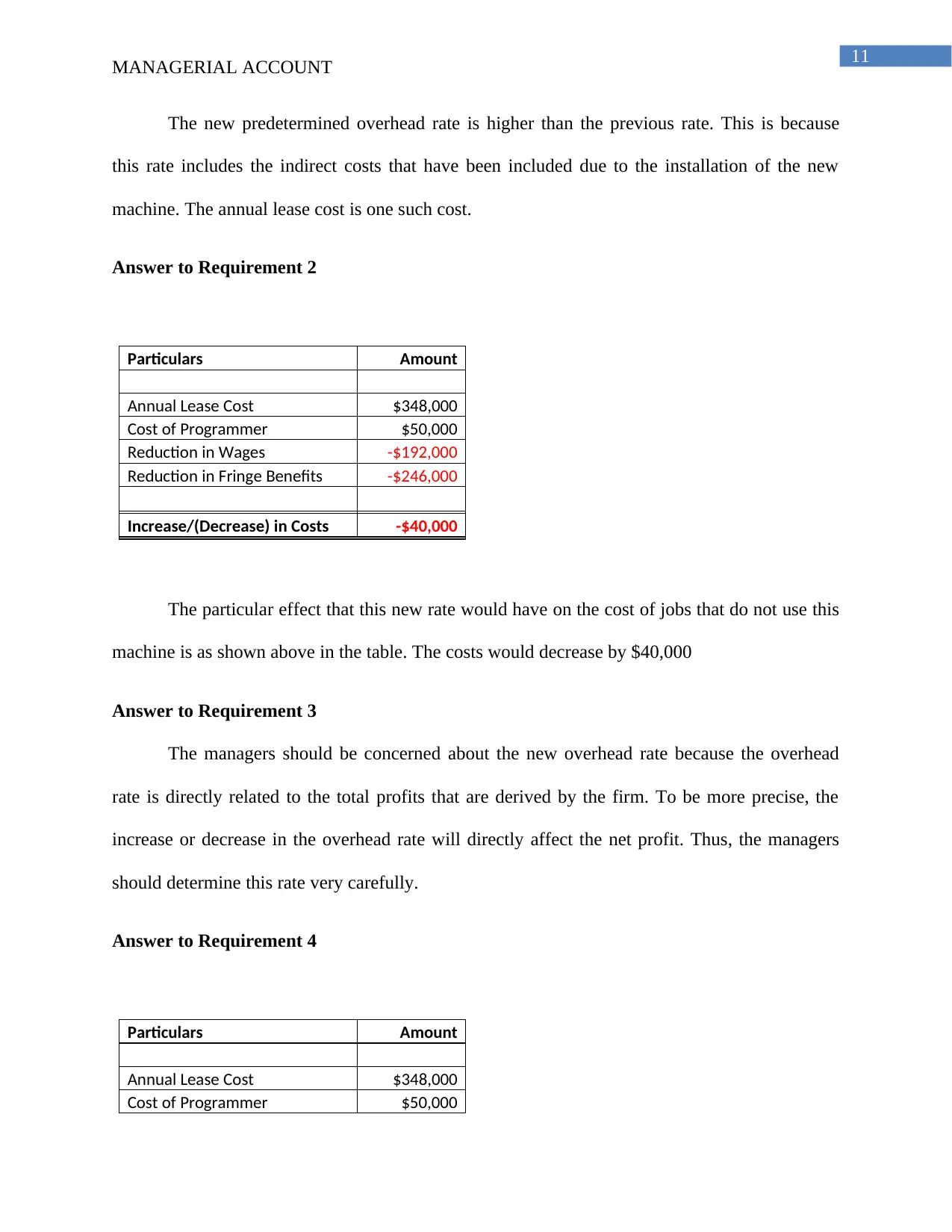

Answer to Requirement 2

Particulars Amount

Annual Lease Cost $348,000

Cost of Programmer $50,000

Reduction in Wages -$192,000

Reduction in Fringe Benefits -$246,000

Increase/(Decrease) in Costs -$40,000

The particular effect that this new rate would have on the cost of jobs that do not use this

machine is as shown above in the table. The costs would decrease by $40,000

Answer to Requirement 3

The managers should be concerned about the new overhead rate because the overhead

rate is directly related to the total profits that are derived by the firm. To be more precise, the

increase or decrease in the overhead rate will directly affect the net profit. Thus, the managers

should determine this rate very carefully.

Answer to Requirement 4

Particulars Amount

Annual Lease Cost $348,000

Cost of Programmer $50,000

MANAGERIAL ACCOUNT

The new predetermined overhead rate is higher than the previous rate. This is because

this rate includes the indirect costs that have been included due to the installation of the new

machine. The annual lease cost is one such cost.

Answer to Requirement 2

Particulars Amount

Annual Lease Cost $348,000

Cost of Programmer $50,000

Reduction in Wages -$192,000

Reduction in Fringe Benefits -$246,000

Increase/(Decrease) in Costs -$40,000

The particular effect that this new rate would have on the cost of jobs that do not use this

machine is as shown above in the table. The costs would decrease by $40,000

Answer to Requirement 3

The managers should be concerned about the new overhead rate because the overhead

rate is directly related to the total profits that are derived by the firm. To be more precise, the

increase or decrease in the overhead rate will directly affect the net profit. Thus, the managers

should determine this rate very carefully.

Answer to Requirement 4

Particulars Amount

Annual Lease Cost $348,000

Cost of Programmer $50,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.