Financial Accounting Statements: Case Study Analysis and Ratios

VerifiedAdded on 2023/01/13

|16

|2534

|26

Case Study

AI Summary

This case study analyzes financial accounting statements, focusing on the key concepts and terms, and how adjustments are applied. It examines the financial performance of River Island and Matalan Ltd. through ratio analysis, covering profitability, liquidity, solvency, and efficiency ratios. The study interprets the results of these ratios, identifies business performance strategies, and discusses the importance of year-end adjustments, their effects on financial statements, and the uses and limitations of ratio analysis. The case study also includes financial data, ratio calculations, and interpretations to assess the financial health and performance of the companies.

Case study on a set of

accounting statements

accounting statements

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX ...................................................................................................................................13

1. River Island ..........................................................................................................................13

2. Matalan Ltd...........................................................................................................................15

INTRODUCTION...........................................................................................................................3

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX ...................................................................................................................................13

1. River Island ..........................................................................................................................13

2. Matalan Ltd...........................................................................................................................15

INTRODUCTION

Financial accounting statement is considered to be as the summary of various

accounting transactions which in turn is occurred over the specific period of the time (Granof

and et.al., 2016). This study will highlight on understanding the various key terms and concepts

which in turn is considered to be very relevant for understanding financial accounting

statements. This study also effectively examines how the adjustments are applied within the

financial accounting statements. Furthermore, this study also understands the role and

limitations associated with the ratios in order to effectively analyse the business performance.

Lastly, this study determines the use of ratio analysis which in turn helps in analysing the

business performance.

Examining appropriate accounting concepts and terms.

Accounting terms

Accounting is an appropriate procedure to record various financial activities which is

useful in assessing the financial position of the business.

Accounting period is a span of time that tends to cover by various set of financial

statements.

Business entity is referred to as the legal structure of the business where all operations

will be carried out.

Financial statements are in turn referred to as reports which is prepared by the

management of the organisation in order to analyse the financial position of the company for a

given span of time (Jollands and Quinn, 2017).

Accounting concept

Accounting concepts is referred to as the basic assumption which in turn is based on

certain rules and principles which in turn tends to work on basis of recording various set of

financial business transactions.

Financial accounting statement is considered to be as the summary of various

accounting transactions which in turn is occurred over the specific period of the time (Granof

and et.al., 2016). This study will highlight on understanding the various key terms and concepts

which in turn is considered to be very relevant for understanding financial accounting

statements. This study also effectively examines how the adjustments are applied within the

financial accounting statements. Furthermore, this study also understands the role and

limitations associated with the ratios in order to effectively analyse the business performance.

Lastly, this study determines the use of ratio analysis which in turn helps in analysing the

business performance.

Examining appropriate accounting concepts and terms.

Accounting terms

Accounting is an appropriate procedure to record various financial activities which is

useful in assessing the financial position of the business.

Accounting period is a span of time that tends to cover by various set of financial

statements.

Business entity is referred to as the legal structure of the business where all operations

will be carried out.

Financial statements are in turn referred to as reports which is prepared by the

management of the organisation in order to analyse the financial position of the company for a

given span of time (Jollands and Quinn, 2017).

Accounting concept

Accounting concepts is referred to as the basic assumption which in turn is based on

certain rules and principles which in turn tends to work on basis of recording various set of

financial business transactions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business entity concept: This means business and its owner tends to have separate legal

identity.

Money measurement concept: Only those financial transaction are recorder in

statements which can be valued and measured in monetary terms.

Going concern concept: This means business will carry out its operations for the

foreseeable future (Cannon, 2019).

Accounting period concept: This means accounting transactions are recorded for

ascertaining profit or loss for specific period of time.

Historical cost concept: It states all assets of the company are recorded at original

purchase price.

Dual aspect concept: Every financial transaction has affects on two accounts on

opposite side.

Realisation concept: The revenue generated from business transaction is recorded only

at the time of its realisation. Consistency concept: It states that, the accounting practices of the company must

remain consistent for several years.

Interpretation of financial accounting statements from provided data.

Financial accounting statements of River Island clothing company represents that it is

performing well in the market. Company is having a turnover of 877.7 million with the gross

profits of 107.1 million. The profits and turnover of the company has shown a decrease from

last year. The operating profit of company has declined to half from last year. The income

statements of company for year 2018 shows that profit for the financial year is only 37. The

cost of sales has increased of company where the revenues has declined. The balance sheet

presenting the position of company shows that net assets of company have decreased from last

year which were 581.6 to 341.5. The reserves and capital of company has also declined.

Financial statements of company are prepared using the accounting standards and complying

identity.

Money measurement concept: Only those financial transaction are recorder in

statements which can be valued and measured in monetary terms.

Going concern concept: This means business will carry out its operations for the

foreseeable future (Cannon, 2019).

Accounting period concept: This means accounting transactions are recorded for

ascertaining profit or loss for specific period of time.

Historical cost concept: It states all assets of the company are recorded at original

purchase price.

Dual aspect concept: Every financial transaction has affects on two accounts on

opposite side.

Realisation concept: The revenue generated from business transaction is recorded only

at the time of its realisation. Consistency concept: It states that, the accounting practices of the company must

remain consistent for several years.

Interpretation of financial accounting statements from provided data.

Financial accounting statements of River Island clothing company represents that it is

performing well in the market. Company is having a turnover of 877.7 million with the gross

profits of 107.1 million. The profits and turnover of the company has shown a decrease from

last year. The operating profit of company has declined to half from last year. The income

statements of company for year 2018 shows that profit for the financial year is only 37. The

cost of sales has increased of company where the revenues has declined. The balance sheet

presenting the position of company shows that net assets of company have decreased from last

year which were 581.6 to 341.5. The reserves and capital of company has also declined.

Financial statements of company are prepared using the accounting standards and complying

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with the requirements of company law. Company is required to address these changes as early

as possible adopting the new strategies that will help company in regaining its share and

market share. Cost of sales is required to be controlled by the organisation using cost control

measures. It can take part in better negotiations and reduce its costs. The turnover of company

has reduced from previous year but the expenses of company has remained same.

Administration expenses of company have increased. Income from interests and other

receivables is reduced further declining the profit level. Company is required to take better

marketing and strategic measures for increasing the sales and profits of company (Yashwanth

and Yaragol, 2018). Continuous declining trend can cause the company to shut down.

Importance of making year- end adjustments to financial accounting statements

The financial statements are prepared at the end of financial year and at that time many

mistakes and some transaction which were left unrecorded needs to be adjusted. This is known

as year end adjustment which are done at time of preparing the financial statements (Ojala and

et.al., 2019). These are named as year- end because of these are made at time of preparing

financial statements. These are some additional entries which needs to be adjusted in order to

adjust some unrecorded transactions or some entries which have earlier being missed by

accountant and now they need to be adjusted in order to calculate accurate profit or loss.

These adjustments are made because the accounting system follows the principles of revenue

recognition and matching concept.

The major importance of these year- end adjustments is that this help the company in

knowing the true and actual financial position of company. The reason underlying this

importance is that even a single transaction which is not adjusted can impact the profits of

business to a great extent.

Another importance of these adjustment is that this system helps in identifying any

mistake or error which have been earlier made and it can be now rectified and solved with help

of these adjustments.

as possible adopting the new strategies that will help company in regaining its share and

market share. Cost of sales is required to be controlled by the organisation using cost control

measures. It can take part in better negotiations and reduce its costs. The turnover of company

has reduced from previous year but the expenses of company has remained same.

Administration expenses of company have increased. Income from interests and other

receivables is reduced further declining the profit level. Company is required to take better

marketing and strategic measures for increasing the sales and profits of company (Yashwanth

and Yaragol, 2018). Continuous declining trend can cause the company to shut down.

Importance of making year- end adjustments to financial accounting statements

The financial statements are prepared at the end of financial year and at that time many

mistakes and some transaction which were left unrecorded needs to be adjusted. This is known

as year end adjustment which are done at time of preparing the financial statements (Ojala and

et.al., 2019). These are named as year- end because of these are made at time of preparing

financial statements. These are some additional entries which needs to be adjusted in order to

adjust some unrecorded transactions or some entries which have earlier being missed by

accountant and now they need to be adjusted in order to calculate accurate profit or loss.

These adjustments are made because the accounting system follows the principles of revenue

recognition and matching concept.

The major importance of these year- end adjustments is that this help the company in

knowing the true and actual financial position of company. The reason underlying this

importance is that even a single transaction which is not adjusted can impact the profits of

business to a great extent.

Another importance of these adjustment is that this system helps in identifying any

mistake or error which have been earlier made and it can be now rectified and solved with help

of these adjustments.

Also, another importance of this adjustment entries is that this help company in

analysing the fact that all accounting records have been made in accordance with the

accounting principles which are followed by company.

Moreover year- end adjusting entries are important for company as they help in

rechecking and reconciling all the transaction which are financial in nature and oversee that all

transaction have been recorded.

Another importance is that these year- end entries are based on matching principles

that is it records all cost of carrying on business at the same time all revenues are being

recorded (Maynard, 2017). Thus, this help the accountant in providing more accurate and

correct information relating to profitability of business.

Effect of year end adjustments

The execution of year- end adjustment entries is very good and positive over the

financial statements. This is majorly because of the reason that after these adjusting entries

only true financial position of company will be outlined and assessed. Thus, these entries need

to be made so that actual balance of cash and other assets can be outlined in good and

effective manner.

Another major effect of these year- end adjusting transaction is that this will help the

accountant in easily assessing all mistakes which could have been made if these entries would

not be corrected. Thus, this ensures and increases trustworthiness of investors over the

company and accountant (Florou, Morricone and Pope, 2019).

Another major effect will be that by making this adjustment entries the company will

earn a goodwill and it will be enhanced as now the stakeholder will like that company is making

adjustment and recording all transaction which have been left earlier. Due to this market value

of company will increase and so as its goodwill.

Understanding meaning of various accounting ratios.

Accounting ratios are referred to as the comparison between various financial data in

order analyse the financial statements of the organization.

analysing the fact that all accounting records have been made in accordance with the

accounting principles which are followed by company.

Moreover year- end adjusting entries are important for company as they help in

rechecking and reconciling all the transaction which are financial in nature and oversee that all

transaction have been recorded.

Another importance is that these year- end entries are based on matching principles

that is it records all cost of carrying on business at the same time all revenues are being

recorded (Maynard, 2017). Thus, this help the accountant in providing more accurate and

correct information relating to profitability of business.

Effect of year end adjustments

The execution of year- end adjustment entries is very good and positive over the

financial statements. This is majorly because of the reason that after these adjusting entries

only true financial position of company will be outlined and assessed. Thus, these entries need

to be made so that actual balance of cash and other assets can be outlined in good and

effective manner.

Another major effect of these year- end adjusting transaction is that this will help the

accountant in easily assessing all mistakes which could have been made if these entries would

not be corrected. Thus, this ensures and increases trustworthiness of investors over the

company and accountant (Florou, Morricone and Pope, 2019).

Another major effect will be that by making this adjustment entries the company will

earn a goodwill and it will be enhanced as now the stakeholder will like that company is making

adjustment and recording all transaction which have been left earlier. Due to this market value

of company will increase and so as its goodwill.

Understanding meaning of various accounting ratios.

Accounting ratios are referred to as the comparison between various financial data in

order analyse the financial statements of the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability ratios: This method is used to analyze how well the business is generating

profits by carrying out its business operations. Liquidity ratio analysis: It is very useful in measuring the self sufficiency of the business

in order to pay off the short term liabilities for the specific period (Accounting Ratios,

2019). Solvency ratio analysis: It helps in measuring the ability of the organization to pay off its

long term debts and interest in order to assess the financial health of company. Efficiency ratio analysis: These ratios tend to indicate the return which in turn has been

generated from sale of any assets. This helps in examining how effectively assets has

been utilized within organization.

profits by carrying out its business operations. Liquidity ratio analysis: It is very useful in measuring the self sufficiency of the business

in order to pay off the short term liabilities for the specific period (Accounting Ratios,

2019). Solvency ratio analysis: It helps in measuring the ability of the organization to pay off its

long term debts and interest in order to assess the financial health of company. Efficiency ratio analysis: These ratios tend to indicate the return which in turn has been

generated from sale of any assets. This helps in examining how effectively assets has

been utilized within organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Uses and limitation of ratio analysis

It is the technique used in analysing and interpreting the financial statements and to

take decisions but these are also affected by its limitations which are stated below.

Uses:

Ratio analysis helps in examining the financial performance of the business which helps

in taking better decisions which are beneficial for the business. Not only the company but also

the external users are interested in knowing the ratio analysis of the company as they are one's

who invest in the company (Lessambo, 2018). It summarizes the report into various figures that

helps in comparing the financial position of the organization and results of the decision taken. It

simplifies the complex into simple ratios which helps in knowing the operating and financial

efficiency of the business and long term positioning.

Limitations:

Sometimes companies changes some of its figures of its financial statement to improve

their financial ratios and show show better performance. This results in window dressing and

wrong decision making. Ratios ignores the inflation factors and ratios are calculated using

historical data and does not include changes in the price level. This leads to wrong reflection of

financial situation (Mei and et.al, 2018). These financial ratios do not consider any of the

qualitative aspects which is its major limitation. There no standard definition or formula of the

ratios. Some companies uses different formula to calculate ratios. For example, while

calculating current ratio, some companies considers all current liabilities while others exclude

bank overdraft. Also, A single ratio does not create any sense, so to create a clear picture

several ratios needs to be calculated.

Using appropriate ratios in order to analyse the financial business performance.

Ratio analysis of River Island and Matalan Ltd is enumerated below:

Profitability ratios

River Island Matalan Ltd

Particulars 2017 2018 2017 2018

It is the technique used in analysing and interpreting the financial statements and to

take decisions but these are also affected by its limitations which are stated below.

Uses:

Ratio analysis helps in examining the financial performance of the business which helps

in taking better decisions which are beneficial for the business. Not only the company but also

the external users are interested in knowing the ratio analysis of the company as they are one's

who invest in the company (Lessambo, 2018). It summarizes the report into various figures that

helps in comparing the financial position of the organization and results of the decision taken. It

simplifies the complex into simple ratios which helps in knowing the operating and financial

efficiency of the business and long term positioning.

Limitations:

Sometimes companies changes some of its figures of its financial statement to improve

their financial ratios and show show better performance. This results in window dressing and

wrong decision making. Ratios ignores the inflation factors and ratios are calculated using

historical data and does not include changes in the price level. This leads to wrong reflection of

financial situation (Mei and et.al, 2018). These financial ratios do not consider any of the

qualitative aspects which is its major limitation. There no standard definition or formula of the

ratios. Some companies uses different formula to calculate ratios. For example, while

calculating current ratio, some companies considers all current liabilities while others exclude

bank overdraft. Also, A single ratio does not create any sense, so to create a clear picture

several ratios needs to be calculated.

Using appropriate ratios in order to analyse the financial business performance.

Ratio analysis of River Island and Matalan Ltd is enumerated below:

Profitability ratios

River Island Matalan Ltd

Particulars 2017 2018 2017 2018

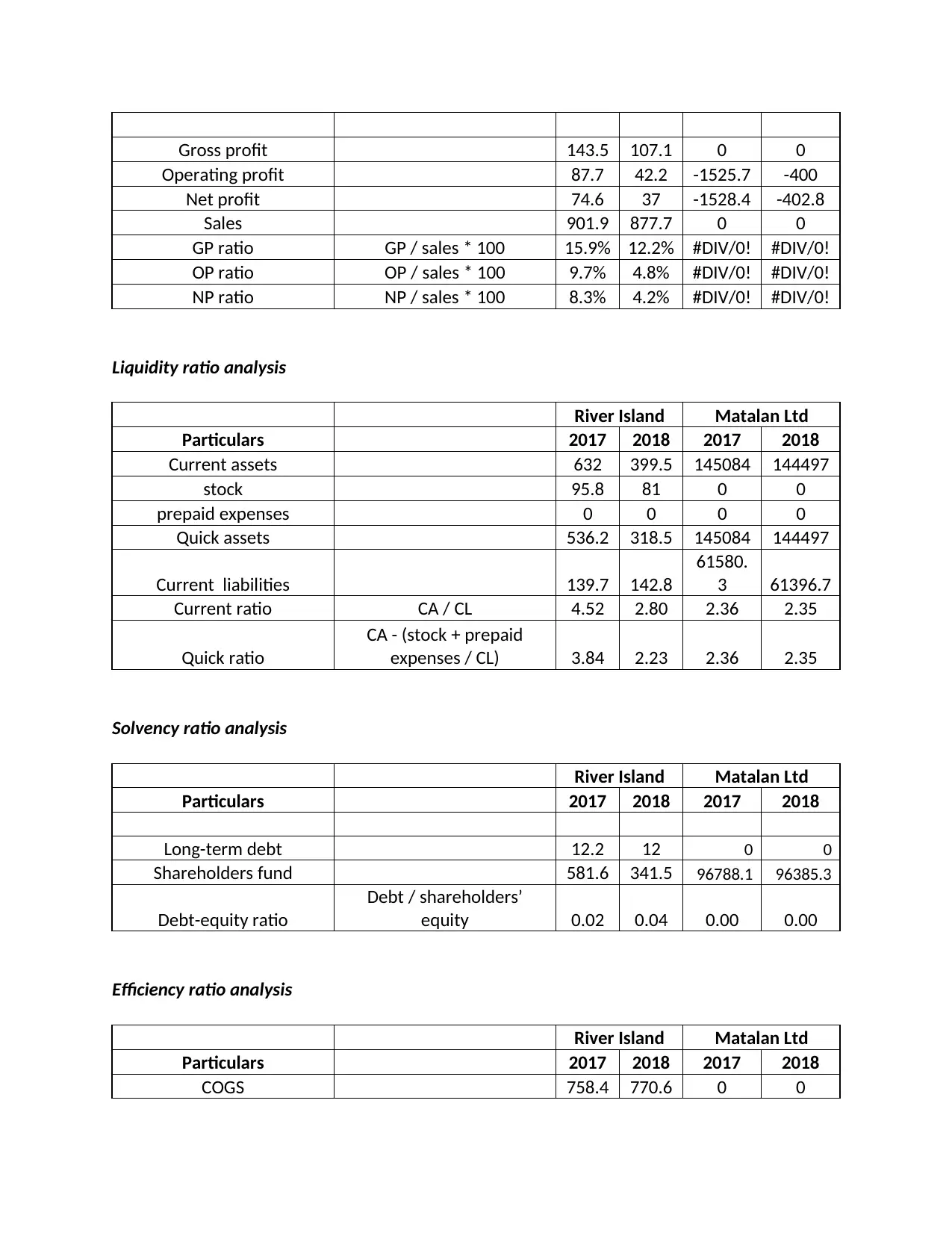

Gross profit 143.5 107.1 0 0

Operating profit 87.7 42.2 -1525.7 -400

Net profit 74.6 37 -1528.4 -402.8

Sales 901.9 877.7 0 0

GP ratio GP / sales * 100 15.9% 12.2% #DIV/0! #DIV/0!

OP ratio OP / sales * 100 9.7% 4.8% #DIV/0! #DIV/0!

NP ratio NP / sales * 100 8.3% 4.2% #DIV/0! #DIV/0!

Liquidity ratio analysis

River Island Matalan Ltd

Particulars 2017 2018 2017 2018

Current assets 632 399.5 145084 144497

stock 95.8 81 0 0

prepaid expenses 0 0 0 0

Quick assets 536.2 318.5 145084 144497

Current liabilities 139.7 142.8

61580.

3 61396.7

Current ratio CA / CL 4.52 2.80 2.36 2.35

Quick ratio

CA - (stock + prepaid

expenses / CL) 3.84 2.23 2.36 2.35

Solvency ratio analysis

River Island Matalan Ltd

Particulars 2017 2018 2017 2018

Long-term debt 12.2 12 0 0

Shareholders fund 581.6 341.5 96788.1 96385.3

Debt-equity ratio

Debt / shareholders’

equity 0.02 0.04 0.00 0.00

Efficiency ratio analysis

River Island Matalan Ltd

Particulars 2017 2018 2017 2018

COGS 758.4 770.6 0 0

Operating profit 87.7 42.2 -1525.7 -400

Net profit 74.6 37 -1528.4 -402.8

Sales 901.9 877.7 0 0

GP ratio GP / sales * 100 15.9% 12.2% #DIV/0! #DIV/0!

OP ratio OP / sales * 100 9.7% 4.8% #DIV/0! #DIV/0!

NP ratio NP / sales * 100 8.3% 4.2% #DIV/0! #DIV/0!

Liquidity ratio analysis

River Island Matalan Ltd

Particulars 2017 2018 2017 2018

Current assets 632 399.5 145084 144497

stock 95.8 81 0 0

prepaid expenses 0 0 0 0

Quick assets 536.2 318.5 145084 144497

Current liabilities 139.7 142.8

61580.

3 61396.7

Current ratio CA / CL 4.52 2.80 2.36 2.35

Quick ratio

CA - (stock + prepaid

expenses / CL) 3.84 2.23 2.36 2.35

Solvency ratio analysis

River Island Matalan Ltd

Particulars 2017 2018 2017 2018

Long-term debt 12.2 12 0 0

Shareholders fund 581.6 341.5 96788.1 96385.3

Debt-equity ratio

Debt / shareholders’

equity 0.02 0.04 0.00 0.00

Efficiency ratio analysis

River Island Matalan Ltd

Particulars 2017 2018 2017 2018

COGS 758.4 770.6 0 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

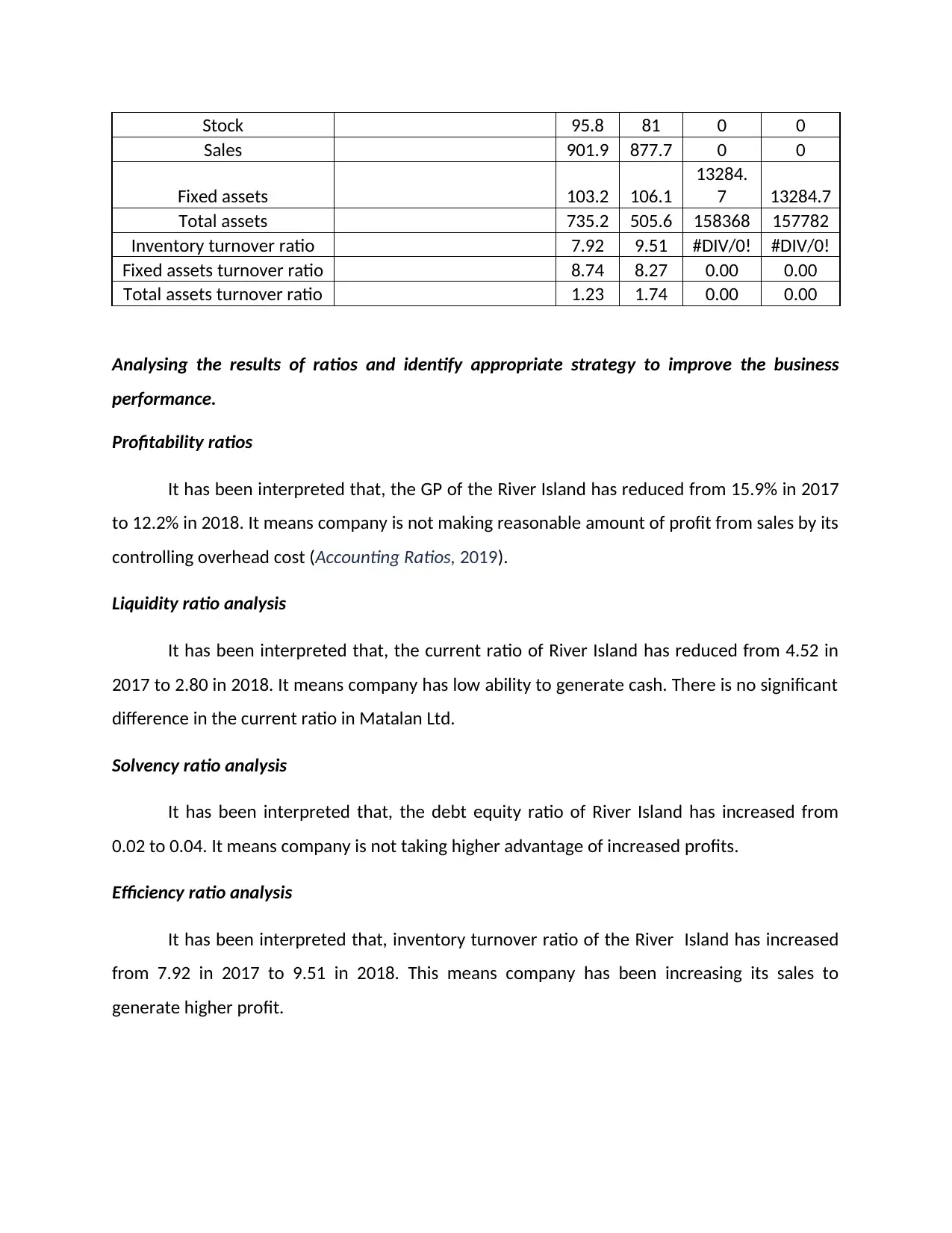

Stock 95.8 81 0 0

Sales 901.9 877.7 0 0

Fixed assets 103.2 106.1

13284.

7 13284.7

Total assets 735.2 505.6 158368 157782

Inventory turnover ratio 7.92 9.51 #DIV/0! #DIV/0!

Fixed assets turnover ratio 8.74 8.27 0.00 0.00

Total assets turnover ratio 1.23 1.74 0.00 0.00

Analysing the results of ratios and identify appropriate strategy to improve the business

performance.

Profitability ratios

It has been interpreted that, the GP of the River Island has reduced from 15.9% in 2017

to 12.2% in 2018. It means company is not making reasonable amount of profit from sales by its

controlling overhead cost (Accounting Ratios, 2019).

Liquidity ratio analysis

It has been interpreted that, the current ratio of River Island has reduced from 4.52 in

2017 to 2.80 in 2018. It means company has low ability to generate cash. There is no significant

difference in the current ratio in Matalan Ltd.

Solvency ratio analysis

It has been interpreted that, the debt equity ratio of River Island has increased from

0.02 to 0.04. It means company is not taking higher advantage of increased profits.

Efficiency ratio analysis

It has been interpreted that, inventory turnover ratio of the River Island has increased

from 7.92 in 2017 to 9.51 in 2018. This means company has been increasing its sales to

generate higher profit.

Sales 901.9 877.7 0 0

Fixed assets 103.2 106.1

13284.

7 13284.7

Total assets 735.2 505.6 158368 157782

Inventory turnover ratio 7.92 9.51 #DIV/0! #DIV/0!

Fixed assets turnover ratio 8.74 8.27 0.00 0.00

Total assets turnover ratio 1.23 1.74 0.00 0.00

Analysing the results of ratios and identify appropriate strategy to improve the business

performance.

Profitability ratios

It has been interpreted that, the GP of the River Island has reduced from 15.9% in 2017

to 12.2% in 2018. It means company is not making reasonable amount of profit from sales by its

controlling overhead cost (Accounting Ratios, 2019).

Liquidity ratio analysis

It has been interpreted that, the current ratio of River Island has reduced from 4.52 in

2017 to 2.80 in 2018. It means company has low ability to generate cash. There is no significant

difference in the current ratio in Matalan Ltd.

Solvency ratio analysis

It has been interpreted that, the debt equity ratio of River Island has increased from

0.02 to 0.04. It means company is not taking higher advantage of increased profits.

Efficiency ratio analysis

It has been interpreted that, inventory turnover ratio of the River Island has increased

from 7.92 in 2017 to 9.51 in 2018. This means company has been increasing its sales to

generate higher profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

This study concludes that, ratios helps in analysing the financial position of the

company. Accounting is useful for summarizing the accounting information to ascertain better

decision making.

This study concludes that, ratios helps in analysing the financial position of the

company. Accounting is useful for summarizing the accounting information to ascertain better

decision making.

REFERENCES

Books and Journals

Cannon, M.L., 2019. An Exploration of Key Accounting Concepts Through Case Studies.

Florou, A., Morricone, S. and Pope, P.F., 2019. Proactive Financial Reporting Enforcement: Audit

Fees and Financial Reporting Quality Effects. The Accounting Review.

Granof, M.H and et.al., 2016. Government and not-for-profit accounting: Concepts and

practices. John Wiley & Sons.

Jollands, S. and Quinn, M., 2017. Politicising the sustaining of water supply in Ireland–the role

of accounting concepts. Accounting, Auditing & Accountability Journal.

Lessambo, F. I., 2018. Financial Ratios Analysis. In Financial Statements (pp. 207-247). Palgrave

Macmillan, Cham.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Mei, Z., and et.al, 2018, June. Limitations of the DuPont Financial Index System and Its

Improvement. In International Conference on Intelligent and Interactive Systems and

Applications (pp. 985-993). Springer, Cham.

Ojala, H., and et.al., 2019. What Turns the Taxman On? Tax Aggressiveness, Financial Statement

Audits and Tax Return Adjustments in Small Private Companies. International Journal of

Accounting, Forthcoming.

Yashwanth, K.J. and Yaragol, B.P., 2018. A Study on Financial Performance Analysis of Prequate

Consultants Private Limited, Bangalore.

Online

Accounting Ratios. 2019. [Online]. Available through:<https://cleartax.in/s/accounting-ratio>

Books and Journals

Cannon, M.L., 2019. An Exploration of Key Accounting Concepts Through Case Studies.

Florou, A., Morricone, S. and Pope, P.F., 2019. Proactive Financial Reporting Enforcement: Audit

Fees and Financial Reporting Quality Effects. The Accounting Review.

Granof, M.H and et.al., 2016. Government and not-for-profit accounting: Concepts and

practices. John Wiley & Sons.

Jollands, S. and Quinn, M., 2017. Politicising the sustaining of water supply in Ireland–the role

of accounting concepts. Accounting, Auditing & Accountability Journal.

Lessambo, F. I., 2018. Financial Ratios Analysis. In Financial Statements (pp. 207-247). Palgrave

Macmillan, Cham.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Mei, Z., and et.al, 2018, June. Limitations of the DuPont Financial Index System and Its

Improvement. In International Conference on Intelligent and Interactive Systems and

Applications (pp. 985-993). Springer, Cham.

Ojala, H., and et.al., 2019. What Turns the Taxman On? Tax Aggressiveness, Financial Statement

Audits and Tax Return Adjustments in Small Private Companies. International Journal of

Accounting, Forthcoming.

Yashwanth, K.J. and Yaragol, B.P., 2018. A Study on Financial Performance Analysis of Prequate

Consultants Private Limited, Bangalore.

Online

Accounting Ratios. 2019. [Online]. Available through:<https://cleartax.in/s/accounting-ratio>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.