Case Study in Finance

VerifiedAdded on 2020/03/16

|10

|1539

|52

Case Study

AI Summary

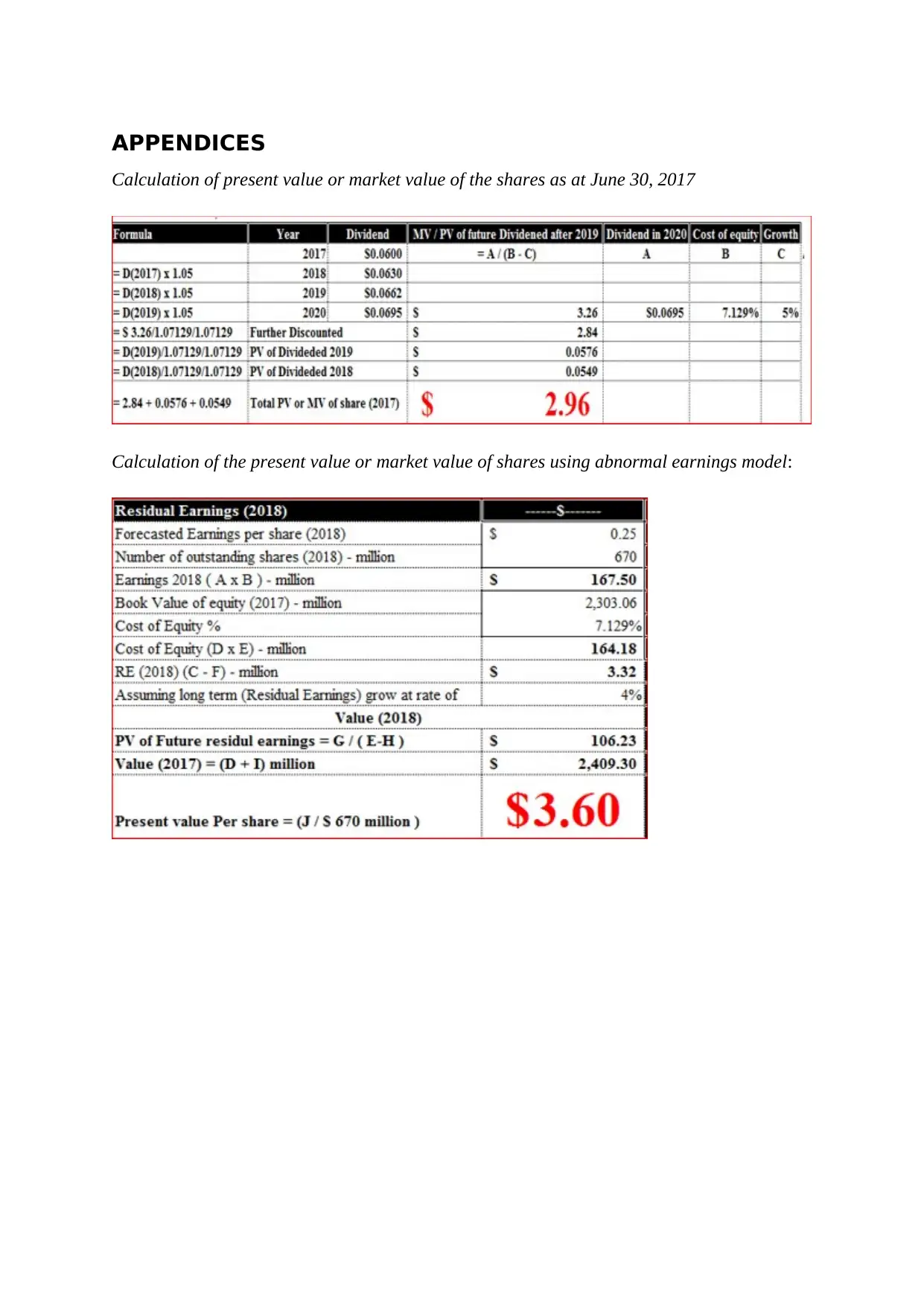

This case study presents a comprehensive financial analysis of the acquisition proposal by Kohlberg Kravis Roberts & Co. (KKR) for Vocus Group. It evaluates the financial viability, operational efficiency, and profitability of Vocus Group through detailed assessments of financial statements and market values. The analysis concludes that accepting the offer would result in a loss for shareholders, as the proposed price per share is lower than its market value. The report includes various financial metrics, comparisons, and references to support its findings.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.