Marks & Spencer Financial Analysis: Cash Budget, Equation, Listing

VerifiedAdded on 2023/06/18

|11

|3053

|349

Report

AI Summary

This report provides a financial analysis of Marks and Spencer, focusing on key accounting principles and practices. It identifies transactions relevant to a cash budget and prepares a three-month budget, highlighting the importance of cash inflows and outflows. The report defines the accounting equation (Assets = Equity + Liabilities) and explains its consistent application, supported by examples. Furthermore, it discusses the benefits of listing shares on the stock exchange, identifies significant stakeholders in large listed companies like Marks and Spencer, and evaluates whether profit is a reliable indicator of cash balance, differentiating between cash and profit. This comprehensive analysis offers insights into Marks and Spencer's financial management and stakeholder relationships.

Question

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK- 1...........................................................................................................................................3

Identify the transactions that can be included in cash budget. Also prepare the one for three

months....................................................................................................................................3

TASK- 2...........................................................................................................................................5

Define Accounting equation along with explaining the reason behind its correct application

for every single time. Also, give example..............................................................................5

List down the benefits of listing shares in stock exchange....................................................6

Detect the possible stakeholders in large listed companies like Marks and Spenser.............7

Is the profit a reliable indicator of cash balance. Also give difference between cash and profit.

................................................................................................................................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION ..........................................................................................................................3

TASK- 1...........................................................................................................................................3

Identify the transactions that can be included in cash budget. Also prepare the one for three

months....................................................................................................................................3

TASK- 2...........................................................................................................................................5

Define Accounting equation along with explaining the reason behind its correct application

for every single time. Also, give example..............................................................................5

List down the benefits of listing shares in stock exchange....................................................6

Detect the possible stakeholders in large listed companies like Marks and Spenser.............7

Is the profit a reliable indicator of cash balance. Also give difference between cash and profit.

................................................................................................................................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Accounting stands for the procedure of recording all the financial transactions linked to

the business. There are two aspects of this process. First one is cash basis in which only those

items are given importance that have taken place in cash. The other is accrual basis. In this

system, the firm records all the proceeding of the firm whether they are on cash or credit. It

keeps track on all the profits, expenses and losses along with the assets and liabilities (Ingles,

2019). The company chosen in this report is Marks and Spencer. It is a UK based retailer dealing

in home, food and clothing products. The report is divided into two parts. First part identifies the

items of cash budget along with its preparation. The second part providing explanation of

accounting equation along with its working. It also ascertains the stakeholders of given company

and checks whether a profit is a reliable indicator of cash or not along with its difference.

TASK- 1

Identify the transactions that can be included in cash budget. Also prepare the one for three

months.

Cash budget is a statement prepared by company for anticipating all the possible inflows

and outflows of cash in a particular time period. It record only those entries which could happen

in cash and that too at that time at which it will actually incurred in money. Below are

explanations of which transaction are included or not in the statement.

1. Amount invested in business attracts the inflow of money in business, so it is a part of

cash budget.

2. A plan for drawing a fixed amount on every personal purchase would account for

recording in only that case when the it will buy any thing for itself.

3. Here, the computer is bought for personal use, the amount related t this would not be

recorded. But the planned figure of £ 800 will be treated as drawings.

4. Purchase of computer for business demands an outflow of business money so, it is also

included .

5. Buying motorcycle will also be recorded as office expense.

6. Sales limited to 30 % will be recorded in the same month and remaining would be

received in coming month, so it will recorded as receipt in that period.

Accounting stands for the procedure of recording all the financial transactions linked to

the business. There are two aspects of this process. First one is cash basis in which only those

items are given importance that have taken place in cash. The other is accrual basis. In this

system, the firm records all the proceeding of the firm whether they are on cash or credit. It

keeps track on all the profits, expenses and losses along with the assets and liabilities (Ingles,

2019). The company chosen in this report is Marks and Spencer. It is a UK based retailer dealing

in home, food and clothing products. The report is divided into two parts. First part identifies the

items of cash budget along with its preparation. The second part providing explanation of

accounting equation along with its working. It also ascertains the stakeholders of given company

and checks whether a profit is a reliable indicator of cash or not along with its difference.

TASK- 1

Identify the transactions that can be included in cash budget. Also prepare the one for three

months.

Cash budget is a statement prepared by company for anticipating all the possible inflows

and outflows of cash in a particular time period. It record only those entries which could happen

in cash and that too at that time at which it will actually incurred in money. Below are

explanations of which transaction are included or not in the statement.

1. Amount invested in business attracts the inflow of money in business, so it is a part of

cash budget.

2. A plan for drawing a fixed amount on every personal purchase would account for

recording in only that case when the it will buy any thing for itself.

3. Here, the computer is bought for personal use, the amount related t this would not be

recorded. But the planned figure of £ 800 will be treated as drawings.

4. Purchase of computer for business demands an outflow of business money so, it is also

included .

5. Buying motorcycle will also be recorded as office expense.

6. Sales limited to 30 % will be recorded in the same month and remaining would be

received in coming month, so it will recorded as receipt in that period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

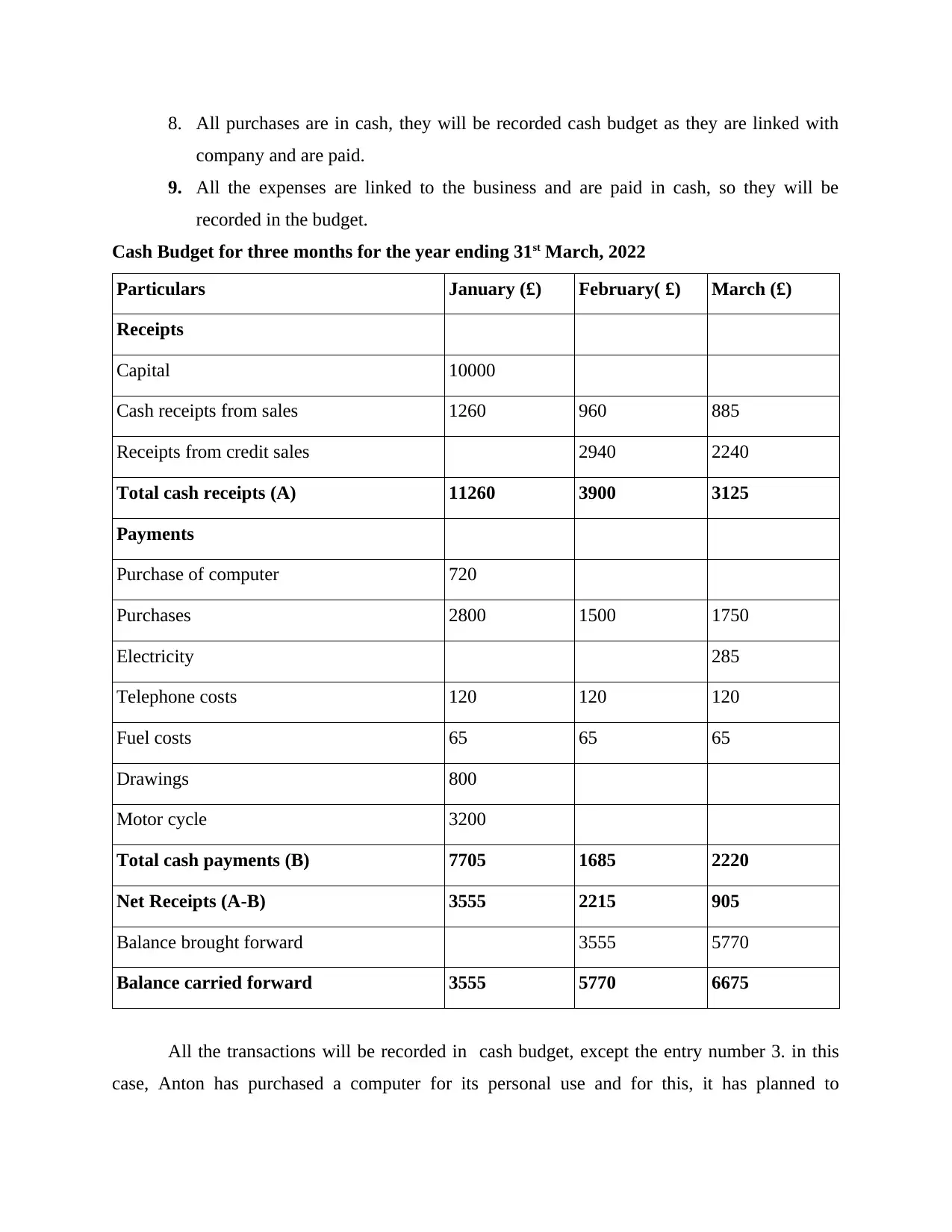

8. All purchases are in cash, they will be recorded cash budget as they are linked with

company and are paid.

9. All the expenses are linked to the business and are paid in cash, so they will be

recorded in the budget.

Cash Budget for three months for the year ending 31st March, 2022

Particulars January (£) February( £) March (£)

Receipts

Capital 10000

Cash receipts from sales 1260 960 885

Receipts from credit sales 2940 2240

Total cash receipts (A) 11260 3900 3125

Payments

Purchase of computer 720

Purchases 2800 1500 1750

Electricity 285

Telephone costs 120 120 120

Fuel costs 65 65 65

Drawings 800

Motor cycle 3200

Total cash payments (B) 7705 1685 2220

Net Receipts (A-B) 3555 2215 905

Balance brought forward 3555 5770

Balance carried forward 3555 5770 6675

All the transactions will be recorded in cash budget, except the entry number 3. in this

case, Anton has purchased a computer for its personal use and for this, it has planned to

company and are paid.

9. All the expenses are linked to the business and are paid in cash, so they will be

recorded in the budget.

Cash Budget for three months for the year ending 31st March, 2022

Particulars January (£) February( £) March (£)

Receipts

Capital 10000

Cash receipts from sales 1260 960 885

Receipts from credit sales 2940 2240

Total cash receipts (A) 11260 3900 3125

Payments

Purchase of computer 720

Purchases 2800 1500 1750

Electricity 285

Telephone costs 120 120 120

Fuel costs 65 65 65

Drawings 800

Motor cycle 3200

Total cash payments (B) 7705 1685 2220

Net Receipts (A-B) 3555 2215 905

Balance brought forward 3555 5770

Balance carried forward 3555 5770 6675

All the transactions will be recorded in cash budget, except the entry number 3. in this

case, Anton has purchased a computer for its personal use and for this, it has planned to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

withdraw £ 800. The effect of drawings has been projected in plan, so there is no requirement for

recording this personal purchase in the books of company.

Working Notes:

As given, 30 % of the sales are on cash while the money for remaining 70 % would be

received in coming next month.

January,

Sales = £ 4200

on cash = 4200 * 30 % = £ 1260

On credit = 4200 – 1260 = £ 2940 ( to be received in next month)

February,

Sales = £ 3200

on cash = 3200 * 30 % = £ 960

On credit = 3200 – 960 = £ 2240 ( Due after this month)

March,

Sales = £ 2950

on cash = 2950 * 30 % = £ 885

On credit = 2950 * 70 % = £ 2065 ( Receivable in April)

TASK- 2

Define Accounting equation along with explaining the reason behind its correct application for

every single time. Also, give example.

Accounting equation is a sort of formula which creates relationship among the assets,

liabilities and capital of the business. It is a base of book keeping through which the whole

system of double entry works. According to this, all the debits must be equal to credits. This

means that for every entry, the sum total of assets will be equal to the summation of liabilities

and capital (Béland and et. al., 2018).

Assets = Equity + Liabilities

It is observed that Accounting equation always satisfy. This is because, it works on the

double entry system. This means that each and every transaction would have two side effect

which helps in maintaining balance at every stage. Every entry tends to put its impact on at least

two accounts which helps in creating its balance (Nyitrai and Virág, 2019).

recording this personal purchase in the books of company.

Working Notes:

As given, 30 % of the sales are on cash while the money for remaining 70 % would be

received in coming next month.

January,

Sales = £ 4200

on cash = 4200 * 30 % = £ 1260

On credit = 4200 – 1260 = £ 2940 ( to be received in next month)

February,

Sales = £ 3200

on cash = 3200 * 30 % = £ 960

On credit = 3200 – 960 = £ 2240 ( Due after this month)

March,

Sales = £ 2950

on cash = 2950 * 30 % = £ 885

On credit = 2950 * 70 % = £ 2065 ( Receivable in April)

TASK- 2

Define Accounting equation along with explaining the reason behind its correct application for

every single time. Also, give example.

Accounting equation is a sort of formula which creates relationship among the assets,

liabilities and capital of the business. It is a base of book keeping through which the whole

system of double entry works. According to this, all the debits must be equal to credits. This

means that for every entry, the sum total of assets will be equal to the summation of liabilities

and capital (Béland and et. al., 2018).

Assets = Equity + Liabilities

It is observed that Accounting equation always satisfy. This is because, it works on the

double entry system. This means that each and every transaction would have two side effect

which helps in maintaining balance at every stage. Every entry tends to put its impact on at least

two accounts which helps in creating its balance (Nyitrai and Virág, 2019).

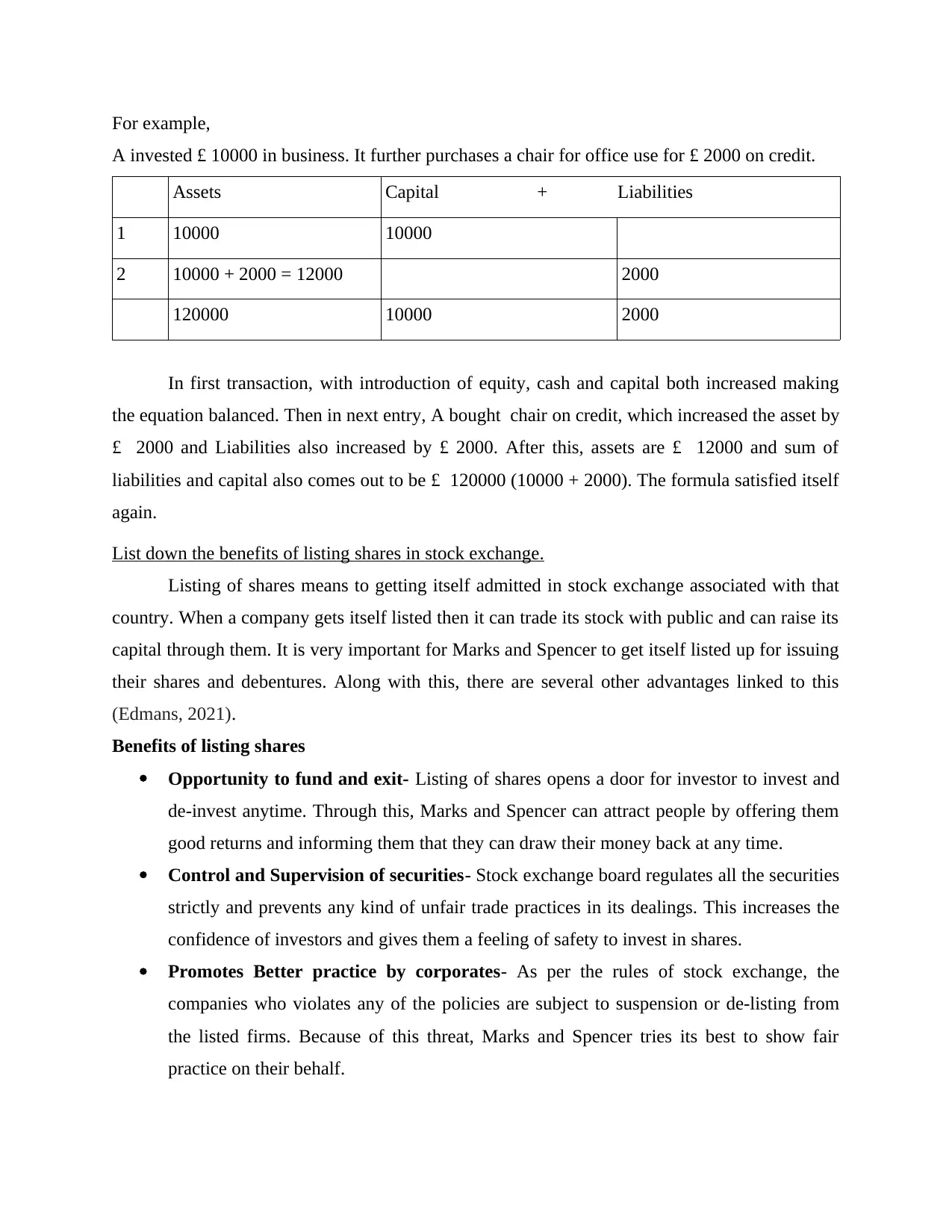

For example,

A invested £ 10000 in business. It further purchases a chair for office use for £ 2000 on credit.

Assets Capital + Liabilities

1 10000 10000

2 10000 + 2000 = 12000 2000

120000 10000 2000

In first transaction, with introduction of equity, cash and capital both increased making

the equation balanced. Then in next entry, A bought chair on credit, which increased the asset by

£ 2000 and Liabilities also increased by £ 2000. After this, assets are £ 12000 and sum of

liabilities and capital also comes out to be £ 120000 (10000 + 2000). The formula satisfied itself

again.

List down the benefits of listing shares in stock exchange.

Listing of shares means to getting itself admitted in stock exchange associated with that

country. When a company gets itself listed then it can trade its stock with public and can raise its

capital through them. It is very important for Marks and Spencer to get itself listed up for issuing

their shares and debentures. Along with this, there are several other advantages linked to this

(Edmans, 2021).

Benefits of listing shares

Opportunity to fund and exit- Listing of shares opens a door for investor to invest and

de-invest anytime. Through this, Marks and Spencer can attract people by offering them

good returns and informing them that they can draw their money back at any time.

Control and Supervision of securities- Stock exchange board regulates all the securities

strictly and prevents any kind of unfair trade practices in its dealings. This increases the

confidence of investors and gives them a feeling of safety to invest in shares.

Promotes Better practice by corporates- As per the rules of stock exchange, the

companies who violates any of the policies are subject to suspension or de-listing from

the listed firms. Because of this threat, Marks and Spencer tries its best to show fair

practice on their behalf.

A invested £ 10000 in business. It further purchases a chair for office use for £ 2000 on credit.

Assets Capital + Liabilities

1 10000 10000

2 10000 + 2000 = 12000 2000

120000 10000 2000

In first transaction, with introduction of equity, cash and capital both increased making

the equation balanced. Then in next entry, A bought chair on credit, which increased the asset by

£ 2000 and Liabilities also increased by £ 2000. After this, assets are £ 12000 and sum of

liabilities and capital also comes out to be £ 120000 (10000 + 2000). The formula satisfied itself

again.

List down the benefits of listing shares in stock exchange.

Listing of shares means to getting itself admitted in stock exchange associated with that

country. When a company gets itself listed then it can trade its stock with public and can raise its

capital through them. It is very important for Marks and Spencer to get itself listed up for issuing

their shares and debentures. Along with this, there are several other advantages linked to this

(Edmans, 2021).

Benefits of listing shares

Opportunity to fund and exit- Listing of shares opens a door for investor to invest and

de-invest anytime. Through this, Marks and Spencer can attract people by offering them

good returns and informing them that they can draw their money back at any time.

Control and Supervision of securities- Stock exchange board regulates all the securities

strictly and prevents any kind of unfair trade practices in its dealings. This increases the

confidence of investors and gives them a feeling of safety to invest in shares.

Promotes Better practice by corporates- As per the rules of stock exchange, the

companies who violates any of the policies are subject to suspension or de-listing from

the listed firms. Because of this threat, Marks and Spencer tries its best to show fair

practice on their behalf.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Timely and accurate disclosure of information- The listed companies are required to

file up their financial statements with the stock exchange in the limited time period and

with correct information. This will bring transparency and builds the confidence of

investor. This reliability will help the Marks and Spencer in attracting more shareholders

towards it (Shen and Qian, 2021).

Ensures Liquidity – Listing of shares helps in recognising the liquidity position of the

firm. This will further help Marks and Spencer in sharing risk with its shareholders and

providing them benefits when the firm is earning profits.

Thus, the companies must list their shares with the stock exchange for getting confidence

of investors and arranging its funds from public. It will also help it in trading itself according to

rules.

Detect the possible stakeholders in large listed companies like Marks and Spenser.

Stakeholders are the persons who are associated with the company in one way or the

other. They are influenced with the operations and profits or losses of the business. These

persons are interested in the success and financial statements of the firm. Various stakeholders

for the firm such as Marks and Spenser are as follows:

Employees- These are the persons who devote their time to the organisation by working

over their. They works in Marks and Spencer for earning their livelihood. Their are

around 70000 employees working in the company. They are interested in knowing that

whether their jobs and salary are secured or not. These individuals are eager to know the

profits earned as they are the people who are working for generating that profit (Kang,

Hwang and Song, 2018).

Customers- They are the buyers of the product. They desire their good and service both

of good quality and with a wide variety at reasonable price. Marks and Spencer keeps a

track on the movement of goods and tries to anticipate the choices and demands. Through

this, they try to manufacture the product as per their desire. They also maintains contact

with buyers through their customer service facility. Thus, they are very important

stakeholders for the organisation.

Government- These authorities provides for the rules related to the business. Marks and

Spencer has to work according to these regulations only. They make sure that all the laws

like company act, health regularities and other frameworks must are adapted in the

file up their financial statements with the stock exchange in the limited time period and

with correct information. This will bring transparency and builds the confidence of

investor. This reliability will help the Marks and Spencer in attracting more shareholders

towards it (Shen and Qian, 2021).

Ensures Liquidity – Listing of shares helps in recognising the liquidity position of the

firm. This will further help Marks and Spencer in sharing risk with its shareholders and

providing them benefits when the firm is earning profits.

Thus, the companies must list their shares with the stock exchange for getting confidence

of investors and arranging its funds from public. It will also help it in trading itself according to

rules.

Detect the possible stakeholders in large listed companies like Marks and Spenser.

Stakeholders are the persons who are associated with the company in one way or the

other. They are influenced with the operations and profits or losses of the business. These

persons are interested in the success and financial statements of the firm. Various stakeholders

for the firm such as Marks and Spenser are as follows:

Employees- These are the persons who devote their time to the organisation by working

over their. They works in Marks and Spencer for earning their livelihood. Their are

around 70000 employees working in the company. They are interested in knowing that

whether their jobs and salary are secured or not. These individuals are eager to know the

profits earned as they are the people who are working for generating that profit (Kang,

Hwang and Song, 2018).

Customers- They are the buyers of the product. They desire their good and service both

of good quality and with a wide variety at reasonable price. Marks and Spencer keeps a

track on the movement of goods and tries to anticipate the choices and demands. Through

this, they try to manufacture the product as per their desire. They also maintains contact

with buyers through their customer service facility. Thus, they are very important

stakeholders for the organisation.

Government- These authorities provides for the rules related to the business. Marks and

Spencer has to work according to these regulations only. They make sure that all the laws

like company act, health regularities and other frameworks must are adapted in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

environment of business properly. Government is interested in company for ensuring that

company is adhering to all its rules and also that are paying all their expenses properly

(Erjiang, Yu and Peng, 2021).

Suppliers- They provides raw material or goods to the company. Marks and Spencer

avail its suppliers from multiple firms globally. So, they demands the contracts which are

safe and can provide good quality items at lower price. So, it is important for the business

to maintain good relation with these persons. Any conflict with these parties can make

bad impact on its supplies.

Shareholders- Those people who invest their money in company by purchasing its

shares are considered to be its shareholders. These persons are very important for Marks

and Spencer as they are the individuals on whose money the whole firm functions. They

are interested in the profits and growth if business. So, they keen to analyse the financial

performance of firm. Marks and Spencer also makes it sure that it provides desired

dividend to them. If the shareholders feel that company is performing well, then they can

ask it to change its policies and procedures. Firm also conducts meetings and AGMs

with them (McStay, 2018).

Local communities- These authorities check out for some legalities like whether a store

can be located at particular location or not. Marks and Spencer maintains good relations

with these by conducting meetings, deals or some joint projects. They holds the power to

tarnish the reputation of company so, firm always informs all these things to these

authorities and works according to its rules and regulations.

Above are the persons who are the important stakeholders of Marks and Spencer. The

firm has to make sure that all these are properly satisfied and they is no conflict in relations with

them. These persons are interested in the accounting reports and profit generation capacity of

business (Lu, 2020).

Is the profit a reliable indicator of cash balance. Also give difference between cash and profit.

No, profits are not the reliable indicator of the cash balance. Money refers to the amount

in hands of the company in physical form and kept in bank. It is available to the business through

investment received, sales and incomes and it deceases with expenses, purchases and payments.

When all these things happen in cash or is realised in cash then, they are involved in money.

Whereas, talking about Profits, it is no dependent on cash. The profit in accrual system does not

company is adhering to all its rules and also that are paying all their expenses properly

(Erjiang, Yu and Peng, 2021).

Suppliers- They provides raw material or goods to the company. Marks and Spencer

avail its suppliers from multiple firms globally. So, they demands the contracts which are

safe and can provide good quality items at lower price. So, it is important for the business

to maintain good relation with these persons. Any conflict with these parties can make

bad impact on its supplies.

Shareholders- Those people who invest their money in company by purchasing its

shares are considered to be its shareholders. These persons are very important for Marks

and Spencer as they are the individuals on whose money the whole firm functions. They

are interested in the profits and growth if business. So, they keen to analyse the financial

performance of firm. Marks and Spencer also makes it sure that it provides desired

dividend to them. If the shareholders feel that company is performing well, then they can

ask it to change its policies and procedures. Firm also conducts meetings and AGMs

with them (McStay, 2018).

Local communities- These authorities check out for some legalities like whether a store

can be located at particular location or not. Marks and Spencer maintains good relations

with these by conducting meetings, deals or some joint projects. They holds the power to

tarnish the reputation of company so, firm always informs all these things to these

authorities and works according to its rules and regulations.

Above are the persons who are the important stakeholders of Marks and Spencer. The

firm has to make sure that all these are properly satisfied and they is no conflict in relations with

them. These persons are interested in the accounting reports and profit generation capacity of

business (Lu, 2020).

Is the profit a reliable indicator of cash balance. Also give difference between cash and profit.

No, profits are not the reliable indicator of the cash balance. Money refers to the amount

in hands of the company in physical form and kept in bank. It is available to the business through

investment received, sales and incomes and it deceases with expenses, purchases and payments.

When all these things happen in cash or is realised in cash then, they are involved in money.

Whereas, talking about Profits, it is no dependent on cash. The profit in accrual system does not

depends on whether the things has happened in cash or not. It just gives importance to the fact

that transaction should be related to that period and is relevant to be recorded in records. The

entries which are related to cash but are not incurred in money are also accounted in it.

According to mathematical expression, profits is equal to income minus expenses. But is

does not introspect that whether all these expenses and incomes have taken place in real

monetary form or not. So, profits made by business is not a reliable indicator of cash holdings of

business. This means that firm showing high level of gains, may hot be having much amount of

money resources. This is solely due to the nature of profits to consider non-cash transactions into

it.

Difference between cash and profits

Cash balance involves the amount held by firm after paying and receiving of money from

all activities – investing, operating as well as financing. While profits deals in only

operating actions.

Profits includes all cash and non-cash items, while cash includes only those entries that

has took place in money only (Peng, Wang, and Chan, 2019).

Profits does not shows the actual liquidity of business, but cash shows and presents the

money holdings of business and helps in interpreting its actual position.

On the whole, it a can be said that a business cannot rely totally on its net income, it has

to give equal importance to cash flow of its business. Ignoring this aspect can make a big distress

in the company.

CONCLUSION

From the above report, it can be concluded that dual entry system has managed the

recording of all the financial items very efficiently. It helps the companies in analysing the two

way aspects of the entries. The cash budget made under this system helps in evaluating all the

transactions which can be included in it and which not. The listing of shares helps a firm in

arranging its funds from the general public and stakeholders in ascertaining the financial position

of the business. This is because for the listed companies, it is important to file their financial

statements with the stock exchange and disclose their complete relevant information. It is also

observed that cash and profits are not one and the same thing. There is a lot of difference in both

these concepts and major one is the recording of non cash transactions in income statement.

that transaction should be related to that period and is relevant to be recorded in records. The

entries which are related to cash but are not incurred in money are also accounted in it.

According to mathematical expression, profits is equal to income minus expenses. But is

does not introspect that whether all these expenses and incomes have taken place in real

monetary form or not. So, profits made by business is not a reliable indicator of cash holdings of

business. This means that firm showing high level of gains, may hot be having much amount of

money resources. This is solely due to the nature of profits to consider non-cash transactions into

it.

Difference between cash and profits

Cash balance involves the amount held by firm after paying and receiving of money from

all activities – investing, operating as well as financing. While profits deals in only

operating actions.

Profits includes all cash and non-cash items, while cash includes only those entries that

has took place in money only (Peng, Wang, and Chan, 2019).

Profits does not shows the actual liquidity of business, but cash shows and presents the

money holdings of business and helps in interpreting its actual position.

On the whole, it a can be said that a business cannot rely totally on its net income, it has

to give equal importance to cash flow of its business. Ignoring this aspect can make a big distress

in the company.

CONCLUSION

From the above report, it can be concluded that dual entry system has managed the

recording of all the financial items very efficiently. It helps the companies in analysing the two

way aspects of the entries. The cash budget made under this system helps in evaluating all the

transactions which can be included in it and which not. The listing of shares helps a firm in

arranging its funds from the general public and stakeholders in ascertaining the financial position

of the business. This is because for the listed companies, it is important to file their financial

statements with the stock exchange and disclose their complete relevant information. It is also

observed that cash and profits are not one and the same thing. There is a lot of difference in both

these concepts and major one is the recording of non cash transactions in income statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Béland, D. and et. al., 2018. Instrument constituencies and transnational policy diffusion: The

case of conditional cash transfers. Review of International Political Economy. 25(4).

pp.463-482.

Edmans, A., 2021. Grow the Pie: How Great Companies Deliver Both Purpose and Profit–

Updated and Revised. Cambridge University Press.

Erjiang, E., Yu, M. and Peng, G., 2021. Intermediation in reward-based crowdfunding: a cash

deposit mechanism to reduce moral hazard. Electronic Commerce Research, pp.1-22.

Ingles, D., 2019. Improving cash flow corporate taxation (CFCT) and the Z-tax (ZT)

approach. Tax and Transfer Policy Institute-Working paper, 7.

Kang, S., Hwang, I. and Song, S., 2018. Cash hoarding: Vice or virtue. Journal of International

Financial Markets, Institutions and Money. 53. pp.94-116.

Lu, L., 2020. The regulation of the dual-class share structure in China: a comparative

perspective. Capital Markets Law Journal.

McStay, K., 2018. The Efficiency of New Issue Markets. Routledge.

Nyitrai, T. and Virág, M., 2019. The effects of handling outliers on the performance of

bankruptcy prediction models. Socio-Economic Planning Sciences. 67. pp.34-42.

Peng, X., Wang, X. and Chan, K.C., 2019. Does customer concentration disclosure affect IPO

pricing?. Finance Research Letters. 28. pp.363-369.

Shen, J. and Qian, J., 2021. The impact of insufficient cash flow on payment term and supply

chain contracts. International Journal of Systems Science: Operations & Logistics,

pp.1-17.

Books and Journals

Béland, D. and et. al., 2018. Instrument constituencies and transnational policy diffusion: The

case of conditional cash transfers. Review of International Political Economy. 25(4).

pp.463-482.

Edmans, A., 2021. Grow the Pie: How Great Companies Deliver Both Purpose and Profit–

Updated and Revised. Cambridge University Press.

Erjiang, E., Yu, M. and Peng, G., 2021. Intermediation in reward-based crowdfunding: a cash

deposit mechanism to reduce moral hazard. Electronic Commerce Research, pp.1-22.

Ingles, D., 2019. Improving cash flow corporate taxation (CFCT) and the Z-tax (ZT)

approach. Tax and Transfer Policy Institute-Working paper, 7.

Kang, S., Hwang, I. and Song, S., 2018. Cash hoarding: Vice or virtue. Journal of International

Financial Markets, Institutions and Money. 53. pp.94-116.

Lu, L., 2020. The regulation of the dual-class share structure in China: a comparative

perspective. Capital Markets Law Journal.

McStay, K., 2018. The Efficiency of New Issue Markets. Routledge.

Nyitrai, T. and Virág, M., 2019. The effects of handling outliers on the performance of

bankruptcy prediction models. Socio-Economic Planning Sciences. 67. pp.34-42.

Peng, X., Wang, X. and Chan, K.C., 2019. Does customer concentration disclosure affect IPO

pricing?. Finance Research Letters. 28. pp.363-369.

Shen, J. and Qian, J., 2021. The impact of insufficient cash flow on payment term and supply

chain contracts. International Journal of Systems Science: Operations & Logistics,

pp.1-17.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.