Management Accounting Analysis: Cash Budget, BEP, and Overhead Cost

VerifiedAdded on 2023/06/18

|16

|3777

|83

Report

AI Summary

This management accounting report provides a detailed analysis of cash budgeting, break-even point (BEP), and overhead cost allocation. It includes a six-month cash budget, highlighting the company's poor cash position and suggesting improvements through better credit term management. The report calculates the break-even point, margin of safety, and profitability at different sales levels using marginal costing techniques. It also addresses behavioral aspects of budgeting that can lead to problems within a business entity, such as dysfunctional behavior, lack of subordinate participation, budgetary slack, and excessive budgeting pressures. Furthermore, the report calculates overhead cost rates and total production costs, comparing single rate versus departmental rate methods for overhead absorption, offering strategic recommendations for improving financial performance. Desklib offers a range of solved assignments and study resources for students.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

QUESTION- 1...........................................................................................................................................3

a) Cash budget.........................................................................................................................................3

b) Cash position in the business and what can be done to improve the cash flows..................................5

c) Behavioral aspects of budgeting that may lead to the problems in business entity.............................5

QUESTION- 2...........................................................................................................................................6

a) Calculation of the contribution........................................................................................................8

b) Calculation of the break-even point and the margin of safety..........................................................8

c) Calculation of the profit...................................................................................................................9

d) Calculation of the number of electric kettles to be sold to gain profit of 90000...............................9

e) Calculation of the selling price at which 53000 electric kettles are to be sold for profit of 90000. 10

f) Recommendation for a good strategy............................................................................................11

g) Assumptions of breakeven model..................................................................................................12

QUESTION- 3.........................................................................................................................................13

a) Calculation of the overhead cost rate based on the labor hours......................................................13

b) Calculation of the total production cost of 10 units of the soft stool..............................................14

c) Representing the advantages and disadvantages of using the single rate for absorption of

overheads as compared to the departmental rates..................................................................................15

CONCLUSION........................................................................................................................................15

REFERENCES........................................................................................................................................16

Departmental and Manufacturing Overhead Vs. Single Overhead Rates. 2021. [Online] Available

through: < https://smallbusiness.chron.com/departmental-manufacturing-overhead-vs-single-overhead-

rates-36198.html>......................................................................................................................................17

Behavioural Implications of Budgeting (6 Implications). 2021. [Online] Available through: <

https://www.yourarticlelibrary.com/accounting/budgeting-accounting/behavioural-implications-of-

budgeting-6-implications/52800>..............................................................................................................17

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

QUESTION- 1...........................................................................................................................................3

a) Cash budget.........................................................................................................................................3

b) Cash position in the business and what can be done to improve the cash flows..................................5

c) Behavioral aspects of budgeting that may lead to the problems in business entity.............................5

QUESTION- 2...........................................................................................................................................6

a) Calculation of the contribution........................................................................................................8

b) Calculation of the break-even point and the margin of safety..........................................................8

c) Calculation of the profit...................................................................................................................9

d) Calculation of the number of electric kettles to be sold to gain profit of 90000...............................9

e) Calculation of the selling price at which 53000 electric kettles are to be sold for profit of 90000. 10

f) Recommendation for a good strategy............................................................................................11

g) Assumptions of breakeven model..................................................................................................12

QUESTION- 3.........................................................................................................................................13

a) Calculation of the overhead cost rate based on the labor hours......................................................13

b) Calculation of the total production cost of 10 units of the soft stool..............................................14

c) Representing the advantages and disadvantages of using the single rate for absorption of

overheads as compared to the departmental rates..................................................................................15

CONCLUSION........................................................................................................................................15

REFERENCES........................................................................................................................................16

Departmental and Manufacturing Overhead Vs. Single Overhead Rates. 2021. [Online] Available

through: < https://smallbusiness.chron.com/departmental-manufacturing-overhead-vs-single-overhead-

rates-36198.html>......................................................................................................................................17

Behavioural Implications of Budgeting (6 Implications). 2021. [Online] Available through: <

https://www.yourarticlelibrary.com/accounting/budgeting-accounting/behavioural-implications-of-

budgeting-6-implications/52800>..............................................................................................................17

INTRODUCTION

In the current times, business units lay high level of emphasis on undertaking

management accounting tools and techniques for taking appropriate business decisions.

Managerial accounting implies for the process of identifying, analyzing, interpreting and

communicating information associated with business aspects. By using such information

manager can develop competent strategic policy framework that contributes in the achievement

of organizational goals. The present report is based on the different case scenarios which will

provide deeper insight about the concept of cash budget and how it helps in analyzing business

performance. Along with this, report will also develop understanding about BEP and its

significance within business context. Further, it presents how variance analysis technique can be

used to identify deviations. It also highlights different types of budget which are prepared and

analyzed for meeting organizational goals.

MAIN BODY

QUESTION- 1

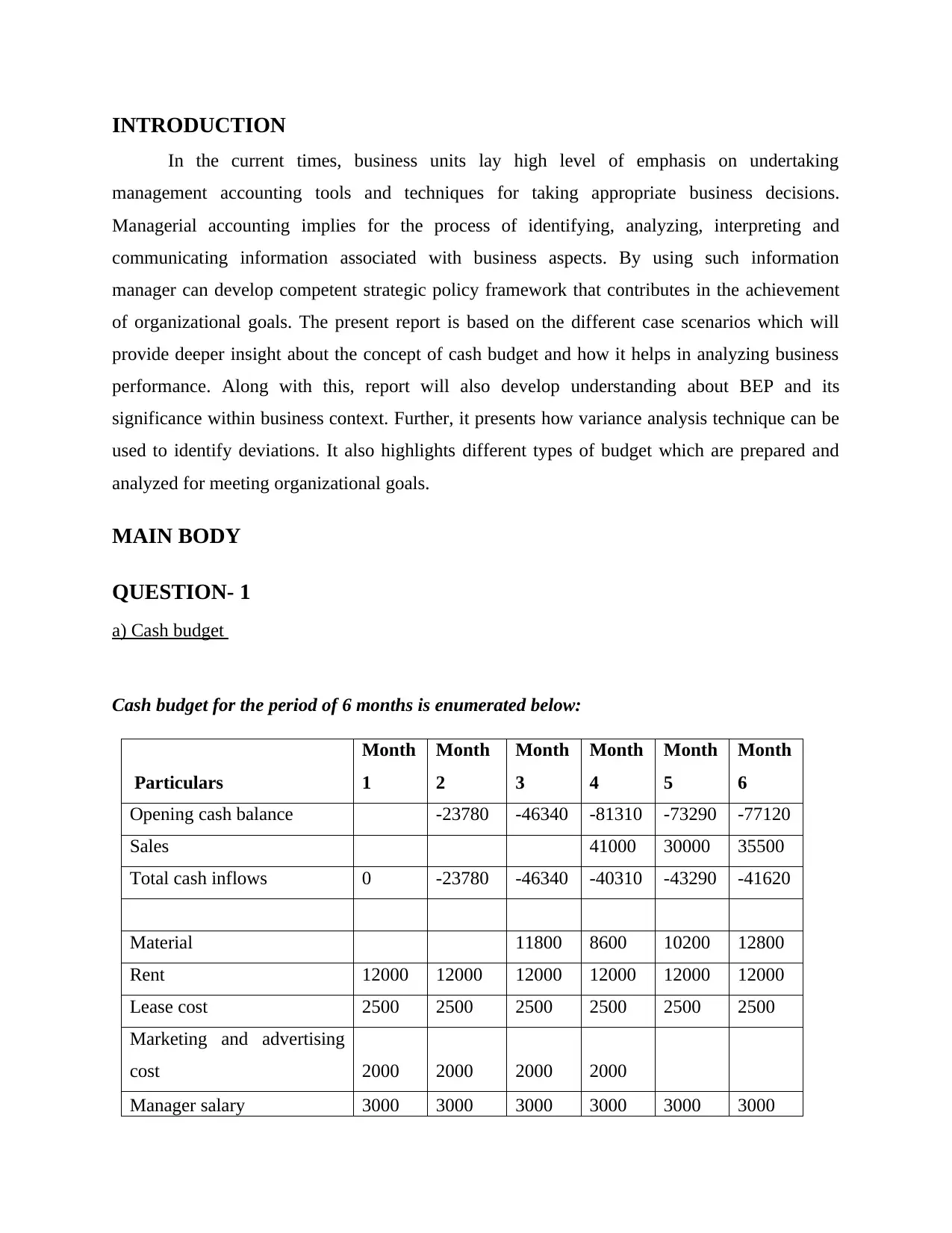

a) Cash budget

Cash budget for the period of 6 months is enumerated below:

Particulars

Month

1

Month

2

Month

3

Month

4

Month

5

Month

6

Opening cash balance -23780 -46340 -81310 -73290 -77120

Sales 41000 30000 35500

Total cash inflows 0 -23780 -46340 -40310 -43290 -41620

Material 11800 8600 10200 12800

Rent 12000 12000 12000 12000 12000 12000

Lease cost 2500 2500 2500 2500 2500 2500

Marketing and advertising

cost 2000 2000 2000 2000

Manager salary 3000 3000 3000 3000 3000 3000

In the current times, business units lay high level of emphasis on undertaking

management accounting tools and techniques for taking appropriate business decisions.

Managerial accounting implies for the process of identifying, analyzing, interpreting and

communicating information associated with business aspects. By using such information

manager can develop competent strategic policy framework that contributes in the achievement

of organizational goals. The present report is based on the different case scenarios which will

provide deeper insight about the concept of cash budget and how it helps in analyzing business

performance. Along with this, report will also develop understanding about BEP and its

significance within business context. Further, it presents how variance analysis technique can be

used to identify deviations. It also highlights different types of budget which are prepared and

analyzed for meeting organizational goals.

MAIN BODY

QUESTION- 1

a) Cash budget

Cash budget for the period of 6 months is enumerated below:

Particulars

Month

1

Month

2

Month

3

Month

4

Month

5

Month

6

Opening cash balance -23780 -46340 -81310 -73290 -77120

Sales 41000 30000 35500

Total cash inflows 0 -23780 -46340 -40310 -43290 -41620

Material 11800 8600 10200 12800

Rent 12000 12000 12000 12000 12000 12000

Lease cost 2500 2500 2500 2500 2500 2500

Marketing and advertising

cost 2000 2000 2000 2000

Manager salary 3000 3000 3000 3000 3000 3000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

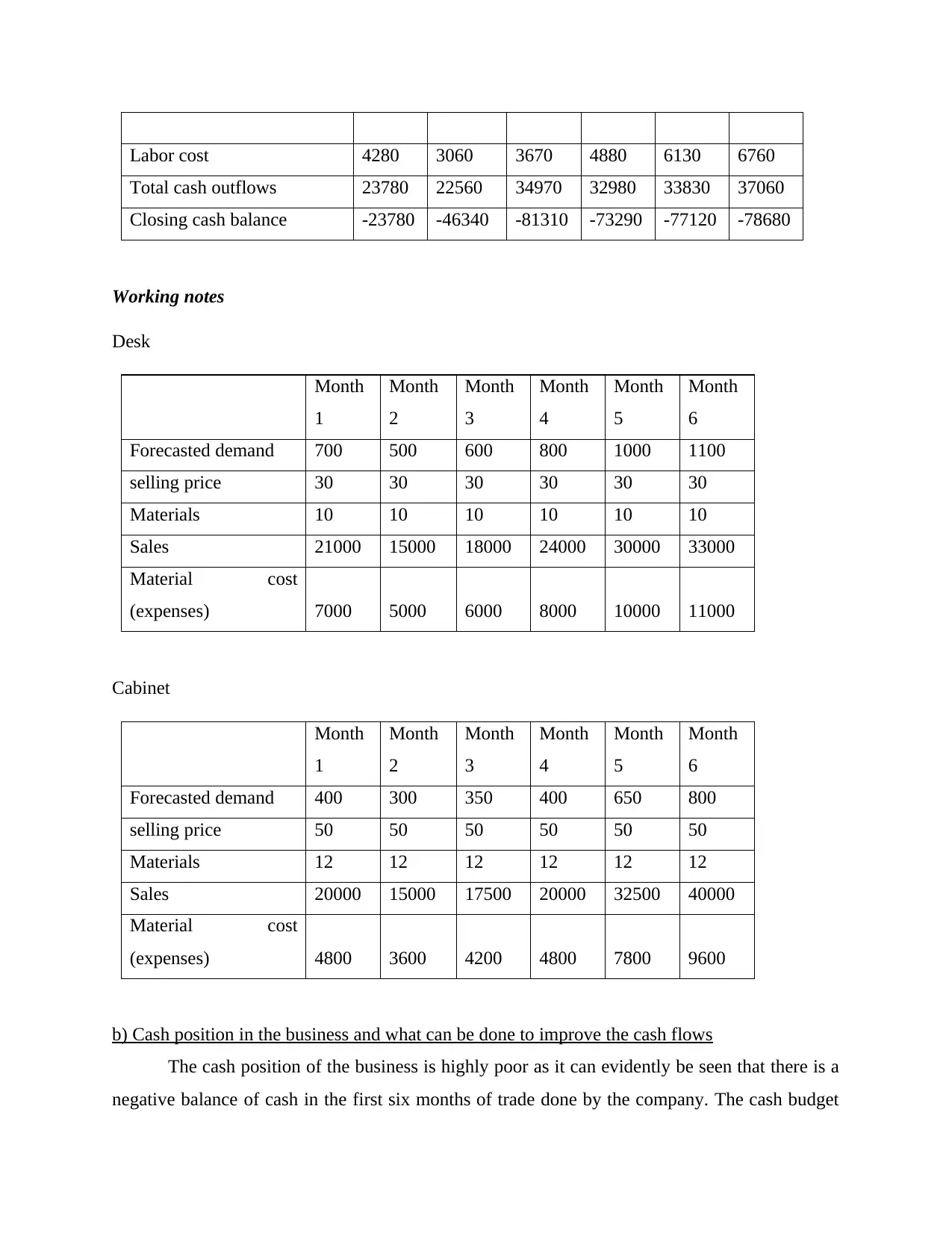

Labor cost 4280 3060 3670 4880 6130 6760

Total cash outflows 23780 22560 34970 32980 33830 37060

Closing cash balance -23780 -46340 -81310 -73290 -77120 -78680

Working notes

Desk

Month

1

Month

2

Month

3

Month

4

Month

5

Month

6

Forecasted demand 700 500 600 800 1000 1100

selling price 30 30 30 30 30 30

Materials 10 10 10 10 10 10

Sales 21000 15000 18000 24000 30000 33000

Material cost

(expenses) 7000 5000 6000 8000 10000 11000

Cabinet

Month

1

Month

2

Month

3

Month

4

Month

5

Month

6

Forecasted demand 400 300 350 400 650 800

selling price 50 50 50 50 50 50

Materials 12 12 12 12 12 12

Sales 20000 15000 17500 20000 32500 40000

Material cost

(expenses) 4800 3600 4200 4800 7800 9600

b) Cash position in the business and what can be done to improve the cash flows

The cash position of the business is highly poor as it can evidently be seen that there is a

negative balance of cash in the first six months of trade done by the company. The cash budget

Total cash outflows 23780 22560 34970 32980 33830 37060

Closing cash balance -23780 -46340 -81310 -73290 -77120 -78680

Working notes

Desk

Month

1

Month

2

Month

3

Month

4

Month

5

Month

6

Forecasted demand 700 500 600 800 1000 1100

selling price 30 30 30 30 30 30

Materials 10 10 10 10 10 10

Sales 21000 15000 18000 24000 30000 33000

Material cost

(expenses) 7000 5000 6000 8000 10000 11000

Cabinet

Month

1

Month

2

Month

3

Month

4

Month

5

Month

6

Forecasted demand 400 300 350 400 650 800

selling price 50 50 50 50 50 50

Materials 12 12 12 12 12 12

Sales 20000 15000 17500 20000 32500 40000

Material cost

(expenses) 4800 3600 4200 4800 7800 9600

b) Cash position in the business and what can be done to improve the cash flows

The cash position of the business is highly poor as it can evidently be seen that there is a

negative balance of cash in the first six months of trade done by the company. The cash budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that is prepared above shows that in each month the business is incurring the cash deficits

wherein the outflow of cash is greater than the inflows leading to the shortage of the same. It can

be seen that the cash management policies of the company are very poor through which it has

been able to generate the negative liquidity position which is further contributing to pushing the

company in the tighter liquidity spot.

This creates a tough position wherein the company shall not be able to even meet the

short term obligations of the business and this shall make them lose their credibility. Further cash

flows of the business can be improved through the better arrangement of the credit terms of the

receivables and the payables of the company (Turner and et.al., 2017). The first and foremost

necessary thing is that the company keep the receivables and the payable days equivalent which

shall be leading to the smooth flow of the working capital cycle of the business. Since the

company is working on the ordering basis so initially it must frame the policy of dealing only on

cash basis until it manages to generate the funds from outside. Apart from that also the

receivables policy must be maintained equivalent to the payables policy so that the lag does not

come and accordingly it is able to create better position of cash.

c) Behavioral aspects of budgeting that may lead to the problems in business entity

There are several behavioral aspects of budgeting that may create problems for the entity

which are:-

Dysfunctional behavior- The budgets are being prepared by the top management who

generally maintain the goal congruence between the organizational objectives and the

managerial goals. But this sometimes affects the overall budget through the unrealistic

expectations of the management. This shall be leading to the negative behavior among

the subordinates impacting their overall motivation and zeal to perform their jobs

efficiently.

Participation of the subordinates in the budgeting- Generally it can be noticed that the

budgets are authoritative in nature whereby the top management shall be imposing the

decisions over all the employees regarding the future operations (Azudin and Mansor

2018). On the contrary some business may involve employee engagement but certainly is

the pseudo participation that further impacts the employees negatively. This shall be

generating behavioral problems in the entity in the process of creating the budgets.

wherein the outflow of cash is greater than the inflows leading to the shortage of the same. It can

be seen that the cash management policies of the company are very poor through which it has

been able to generate the negative liquidity position which is further contributing to pushing the

company in the tighter liquidity spot.

This creates a tough position wherein the company shall not be able to even meet the

short term obligations of the business and this shall make them lose their credibility. Further cash

flows of the business can be improved through the better arrangement of the credit terms of the

receivables and the payables of the company (Turner and et.al., 2017). The first and foremost

necessary thing is that the company keep the receivables and the payable days equivalent which

shall be leading to the smooth flow of the working capital cycle of the business. Since the

company is working on the ordering basis so initially it must frame the policy of dealing only on

cash basis until it manages to generate the funds from outside. Apart from that also the

receivables policy must be maintained equivalent to the payables policy so that the lag does not

come and accordingly it is able to create better position of cash.

c) Behavioral aspects of budgeting that may lead to the problems in business entity

There are several behavioral aspects of budgeting that may create problems for the entity

which are:-

Dysfunctional behavior- The budgets are being prepared by the top management who

generally maintain the goal congruence between the organizational objectives and the

managerial goals. But this sometimes affects the overall budget through the unrealistic

expectations of the management. This shall be leading to the negative behavior among

the subordinates impacting their overall motivation and zeal to perform their jobs

efficiently.

Participation of the subordinates in the budgeting- Generally it can be noticed that the

budgets are authoritative in nature whereby the top management shall be imposing the

decisions over all the employees regarding the future operations (Azudin and Mansor

2018). On the contrary some business may involve employee engagement but certainly is

the pseudo participation that further impacts the employees negatively. This shall be

generating behavioral problems in the entity in the process of creating the budgets.

Budgetary slack- The budgetary slack is created when the management who is preparing

the budgets shall be less optimistic and conservative by underestimating the revenues,

overestimating the costs and thereby generating the requirements of arrangement of

funds. This shall be leading to the deviations in between the budgets and the original

level of activity that is being undertaken in the company (Behavioural Implications of

Budgeting (6 Implications), 2021).

Excessive budgeting pressures- The other aspect of budgeting that shall be leading to the

negative impacts on the business are the excessive pressure and the directing that is

provided by the budgets in the company. It can be known that this restrict the freedom of

taking the initiatives in the business such that the employees are forced to follow each

and every element of the budget. Also this shall further be leading to the development of

the inter departmental conflicts in the organization affecting the operational efficiency of

the business.

QUESTION- 2

Break-even analysis- The break-even model is the technique which is used for the assessment of

the profitability at the different level of sales. The break-even point is at the level of sales where

the total revenues generated are equivalent to the total costs that are incurred in the operations.

This means that at this level there is zero profitability and the revenues are sufficient to cover the

costs of the company (Kostyukova and et.al., 2018). Apart from that it can be identified that this

is the minimum level wherein the company can just survive by covering the costs, as below this

they shall be incorporating the losses. This analysis shall be helping in the ascertainment of the

future optimum level of operations in the company that shall be leading to the fulfilment of the

organizational objectives.

Margin of safety- The margin of safety shall be representing the difference between the intrinsic

value of the stock and its market price that is currently prevailing in the market. It is the margin

that the company is having over the break-even point of the business. It also indicates that the

higher is the difference between the actual and the break-even sales the better it is for the

business as this shall be leading to the increase in the profitability of the business. The safety

margin shall be preventing the company from any sort of losses even if the demand decreases to

some extent.

the budgets shall be less optimistic and conservative by underestimating the revenues,

overestimating the costs and thereby generating the requirements of arrangement of

funds. This shall be leading to the deviations in between the budgets and the original

level of activity that is being undertaken in the company (Behavioural Implications of

Budgeting (6 Implications), 2021).

Excessive budgeting pressures- The other aspect of budgeting that shall be leading to the

negative impacts on the business are the excessive pressure and the directing that is

provided by the budgets in the company. It can be known that this restrict the freedom of

taking the initiatives in the business such that the employees are forced to follow each

and every element of the budget. Also this shall further be leading to the development of

the inter departmental conflicts in the organization affecting the operational efficiency of

the business.

QUESTION- 2

Break-even analysis- The break-even model is the technique which is used for the assessment of

the profitability at the different level of sales. The break-even point is at the level of sales where

the total revenues generated are equivalent to the total costs that are incurred in the operations.

This means that at this level there is zero profitability and the revenues are sufficient to cover the

costs of the company (Kostyukova and et.al., 2018). Apart from that it can be identified that this

is the minimum level wherein the company can just survive by covering the costs, as below this

they shall be incorporating the losses. This analysis shall be helping in the ascertainment of the

future optimum level of operations in the company that shall be leading to the fulfilment of the

organizational objectives.

Margin of safety- The margin of safety shall be representing the difference between the intrinsic

value of the stock and its market price that is currently prevailing in the market. It is the margin

that the company is having over the break-even point of the business. It also indicates that the

higher is the difference between the actual and the break-even sales the better it is for the

business as this shall be leading to the increase in the profitability of the business. The safety

margin shall be preventing the company from any sort of losses even if the demand decreases to

some extent.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

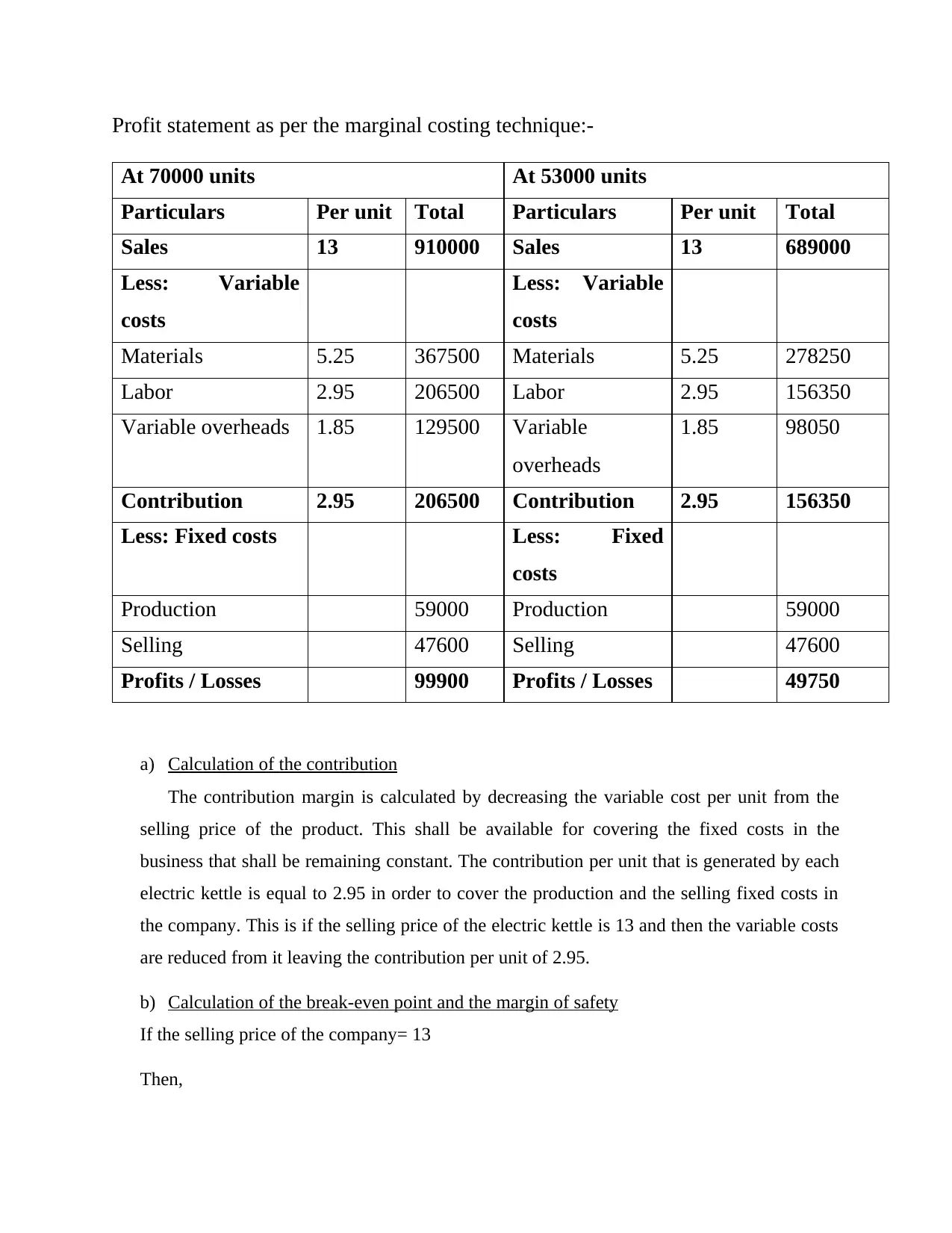

Profit statement as per the marginal costing technique:-

At 70000 units At 53000 units

Particulars Per unit Total Particulars Per unit Total

Sales 13 910000 Sales 13 689000

Less: Variable

costs

Less: Variable

costs

Materials 5.25 367500 Materials 5.25 278250

Labor 2.95 206500 Labor 2.95 156350

Variable overheads 1.85 129500 Variable

overheads

1.85 98050

Contribution 2.95 206500 Contribution 2.95 156350

Less: Fixed costs Less: Fixed

costs

Production 59000 Production 59000

Selling 47600 Selling 47600

Profits / Losses 99900 Profits / Losses 49750

a) Calculation of the contribution

The contribution margin is calculated by decreasing the variable cost per unit from the

selling price of the product. This shall be available for covering the fixed costs in the

business that shall be remaining constant. The contribution per unit that is generated by each

electric kettle is equal to 2.95 in order to cover the production and the selling fixed costs in

the company. This is if the selling price of the electric kettle is 13 and then the variable costs

are reduced from it leaving the contribution per unit of 2.95.

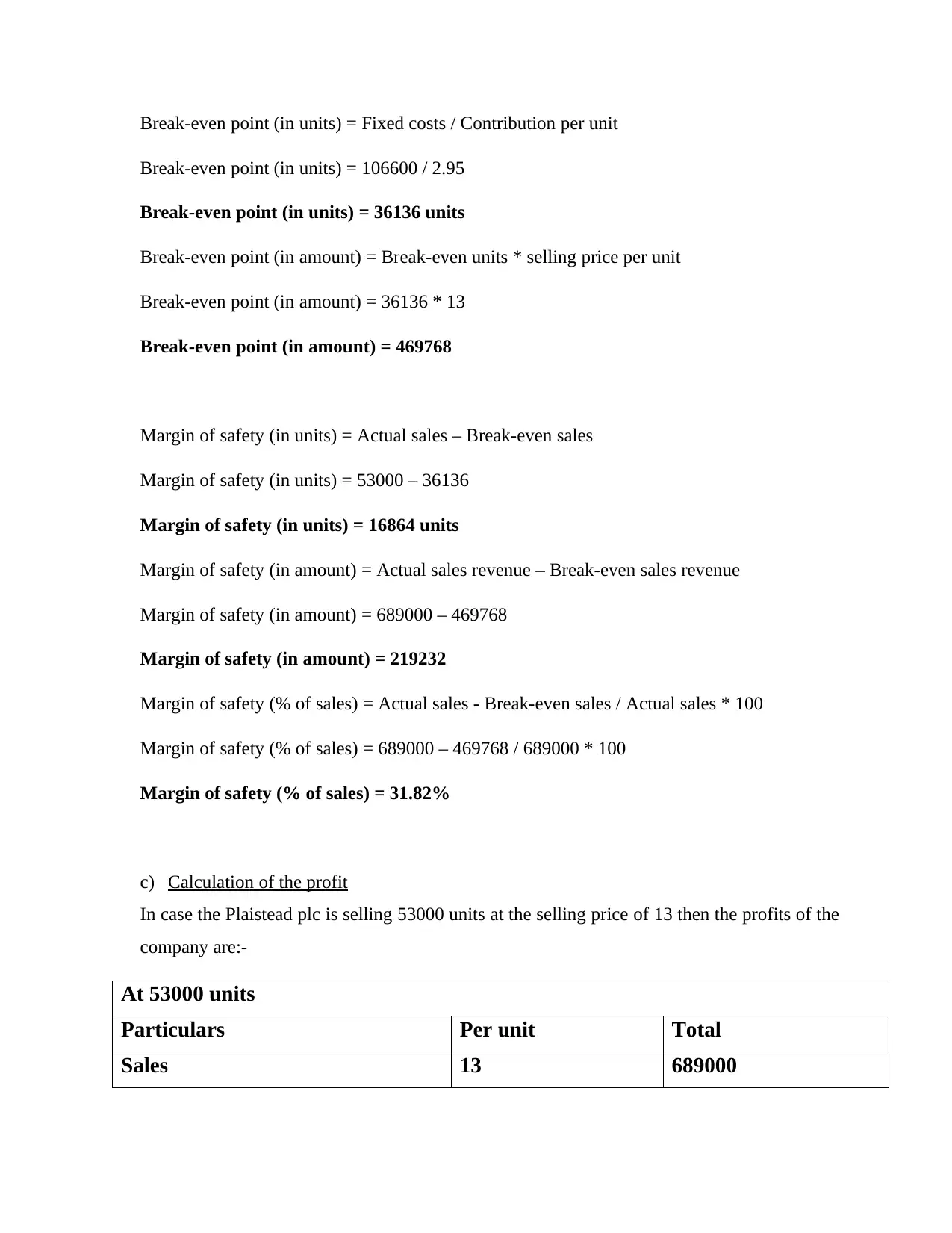

b) Calculation of the break-even point and the margin of safety

If the selling price of the company= 13

Then,

At 70000 units At 53000 units

Particulars Per unit Total Particulars Per unit Total

Sales 13 910000 Sales 13 689000

Less: Variable

costs

Less: Variable

costs

Materials 5.25 367500 Materials 5.25 278250

Labor 2.95 206500 Labor 2.95 156350

Variable overheads 1.85 129500 Variable

overheads

1.85 98050

Contribution 2.95 206500 Contribution 2.95 156350

Less: Fixed costs Less: Fixed

costs

Production 59000 Production 59000

Selling 47600 Selling 47600

Profits / Losses 99900 Profits / Losses 49750

a) Calculation of the contribution

The contribution margin is calculated by decreasing the variable cost per unit from the

selling price of the product. This shall be available for covering the fixed costs in the

business that shall be remaining constant. The contribution per unit that is generated by each

electric kettle is equal to 2.95 in order to cover the production and the selling fixed costs in

the company. This is if the selling price of the electric kettle is 13 and then the variable costs

are reduced from it leaving the contribution per unit of 2.95.

b) Calculation of the break-even point and the margin of safety

If the selling price of the company= 13

Then,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Break-even point (in units) = Fixed costs / Contribution per unit

Break-even point (in units) = 106600 / 2.95

Break-even point (in units) = 36136 units

Break-even point (in amount) = Break-even units * selling price per unit

Break-even point (in amount) = 36136 * 13

Break-even point (in amount) = 469768

Margin of safety (in units) = Actual sales – Break-even sales

Margin of safety (in units) = 53000 – 36136

Margin of safety (in units) = 16864 units

Margin of safety (in amount) = Actual sales revenue – Break-even sales revenue

Margin of safety (in amount) = 689000 – 469768

Margin of safety (in amount) = 219232

Margin of safety (% of sales) = Actual sales - Break-even sales / Actual sales * 100

Margin of safety (% of sales) = 689000 – 469768 / 689000 * 100

Margin of safety (% of sales) = 31.82%

c) Calculation of the profit

In case the Plaistead plc is selling 53000 units at the selling price of 13 then the profits of the

company are:-

At 53000 units

Particulars Per unit Total

Sales 13 689000

Break-even point (in units) = 106600 / 2.95

Break-even point (in units) = 36136 units

Break-even point (in amount) = Break-even units * selling price per unit

Break-even point (in amount) = 36136 * 13

Break-even point (in amount) = 469768

Margin of safety (in units) = Actual sales – Break-even sales

Margin of safety (in units) = 53000 – 36136

Margin of safety (in units) = 16864 units

Margin of safety (in amount) = Actual sales revenue – Break-even sales revenue

Margin of safety (in amount) = 689000 – 469768

Margin of safety (in amount) = 219232

Margin of safety (% of sales) = Actual sales - Break-even sales / Actual sales * 100

Margin of safety (% of sales) = 689000 – 469768 / 689000 * 100

Margin of safety (% of sales) = 31.82%

c) Calculation of the profit

In case the Plaistead plc is selling 53000 units at the selling price of 13 then the profits of the

company are:-

At 53000 units

Particulars Per unit Total

Sales 13 689000

Less: Variable costs

Materials 5.25 278250

Labor 2.95 156350

Variable overheads 1.85 98050

Contribution 2.95 156350

Less: Fixed costs

Production 59000

Selling 47600

Profits / Losses 49750

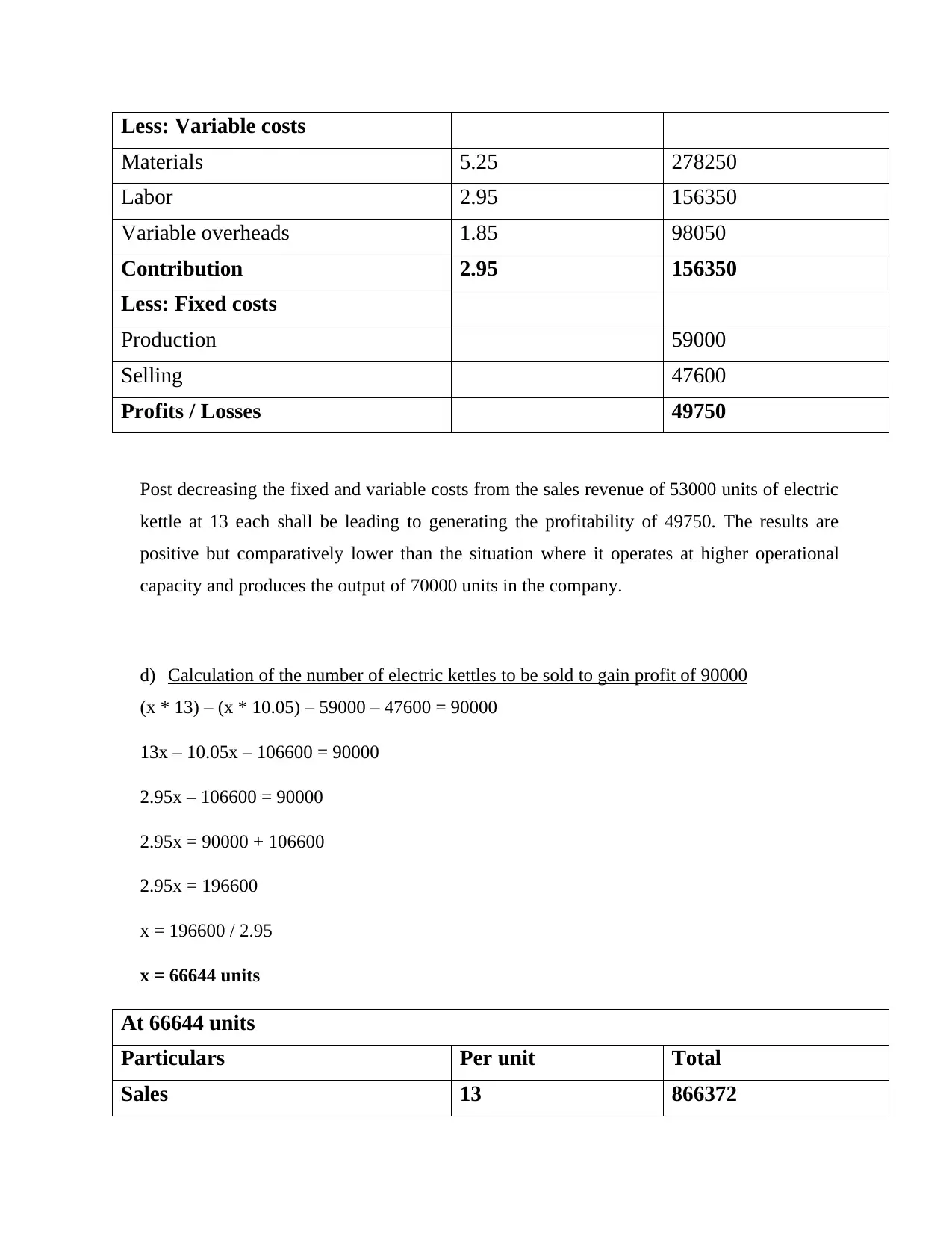

Post decreasing the fixed and variable costs from the sales revenue of 53000 units of electric

kettle at 13 each shall be leading to generating the profitability of 49750. The results are

positive but comparatively lower than the situation where it operates at higher operational

capacity and produces the output of 70000 units in the company.

d) Calculation of the number of electric kettles to be sold to gain profit of 90000

(x * 13) – (x * 10.05) – 59000 – 47600 = 90000

13x – 10.05x – 106600 = 90000

2.95x – 106600 = 90000

2.95x = 90000 + 106600

2.95x = 196600

x = 196600 / 2.95

x = 66644 units

At 66644 units

Particulars Per unit Total

Sales 13 866372

Materials 5.25 278250

Labor 2.95 156350

Variable overheads 1.85 98050

Contribution 2.95 156350

Less: Fixed costs

Production 59000

Selling 47600

Profits / Losses 49750

Post decreasing the fixed and variable costs from the sales revenue of 53000 units of electric

kettle at 13 each shall be leading to generating the profitability of 49750. The results are

positive but comparatively lower than the situation where it operates at higher operational

capacity and produces the output of 70000 units in the company.

d) Calculation of the number of electric kettles to be sold to gain profit of 90000

(x * 13) – (x * 10.05) – 59000 – 47600 = 90000

13x – 10.05x – 106600 = 90000

2.95x – 106600 = 90000

2.95x = 90000 + 106600

2.95x = 196600

x = 196600 / 2.95

x = 66644 units

At 66644 units

Particulars Per unit Total

Sales 13 866372

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Variable costs

Materials 5.25 349881

Labor 2.95 196600

Variable overheads 1.85 123291

Contribution 2.95 196600

Less: Fixed costs

Production 59000

Selling 47600

Profits / Losses 90000

In order to generate the profits of up-to 90000 the Plaistead plc shall be selling 66644 units of

electric kettles at the selling price of 13 keeping the variable costs per unit and the fixed costs

remain constant. The selling of 66644 units shall be leading to the generation of 90000 units

(Hiebl and Richter, 2018).

e) Calculation of the selling price at which 53000 electric kettles are to be sold for profit of

90000

(53000 * x) – (53000 * 10.05) – 59000 – 47600 = 90000

53000x – 532650 – 59000 – 47600 = 90000

53000x – 639250 = 90000

53000x = 90000 + 639250

53000x = 729250

x = 729250 / 53000

x = 13.76

At 53000 units

Particulars Per unit Total

Sales 13.76 729280

Materials 5.25 349881

Labor 2.95 196600

Variable overheads 1.85 123291

Contribution 2.95 196600

Less: Fixed costs

Production 59000

Selling 47600

Profits / Losses 90000

In order to generate the profits of up-to 90000 the Plaistead plc shall be selling 66644 units of

electric kettles at the selling price of 13 keeping the variable costs per unit and the fixed costs

remain constant. The selling of 66644 units shall be leading to the generation of 90000 units

(Hiebl and Richter, 2018).

e) Calculation of the selling price at which 53000 electric kettles are to be sold for profit of

90000

(53000 * x) – (53000 * 10.05) – 59000 – 47600 = 90000

53000x – 532650 – 59000 – 47600 = 90000

53000x – 639250 = 90000

53000x = 90000 + 639250

53000x = 729250

x = 729250 / 53000

x = 13.76

At 53000 units

Particulars Per unit Total

Sales 13.76 729280

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: Variable costs

Materials 5.25 278250

Labor 2.95 156350

Variable overheads 1.85 98050

Contribution 3.71 196630

Less: Fixed costs

Production 59000

Selling 47600

Profits / Losses 90000

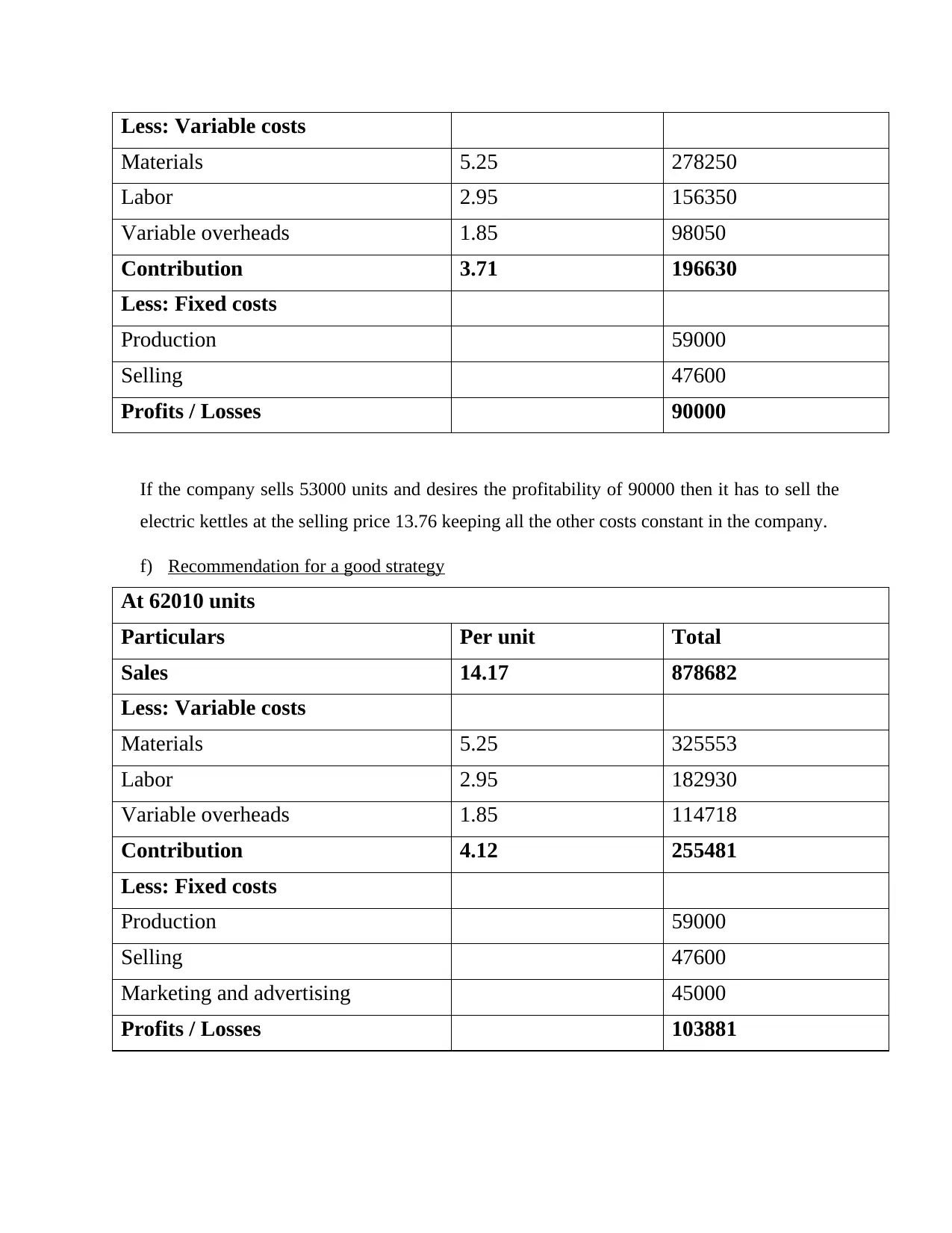

If the company sells 53000 units and desires the profitability of 90000 then it has to sell the

electric kettles at the selling price 13.76 keeping all the other costs constant in the company.

f) Recommendation for a good strategy

At 62010 units

Particulars Per unit Total

Sales 14.17 878682

Less: Variable costs

Materials 5.25 325553

Labor 2.95 182930

Variable overheads 1.85 114718

Contribution 4.12 255481

Less: Fixed costs

Production 59000

Selling 47600

Marketing and advertising 45000

Profits / Losses 103881

Materials 5.25 278250

Labor 2.95 156350

Variable overheads 1.85 98050

Contribution 3.71 196630

Less: Fixed costs

Production 59000

Selling 47600

Profits / Losses 90000

If the company sells 53000 units and desires the profitability of 90000 then it has to sell the

electric kettles at the selling price 13.76 keeping all the other costs constant in the company.

f) Recommendation for a good strategy

At 62010 units

Particulars Per unit Total

Sales 14.17 878682

Less: Variable costs

Materials 5.25 325553

Labor 2.95 182930

Variable overheads 1.85 114718

Contribution 4.12 255481

Less: Fixed costs

Production 59000

Selling 47600

Marketing and advertising 45000

Profits / Losses 103881

Yes, this is definitely a good strategy as the above table shows that the company is earning a

profitability up-to double than that of earlier when it was selling the 53000 units at 13 per

unit of electric kettle. Now the company is selling 62010 units at 14.17 per unit with an

additional marketing cost of 45000 that is generating profits of 103881 as compared to before

profits of 49750.

g) Assumptions of breakeven model

There are several assumptions that are pertaining to the break-even model which makes the

technique unrealistic for the real life applicability. These are some major assumptions:-

The first and the foremost assumption is that the selling price of the company shall

remain constant over the period (Rikhardsson and Yigitbasioglu, 2018).

The other assumption is that all the other components of the cost like the variable

costs per unit and the fixed costs of operations shall be remaining constant for the

company.

It can be assessed that the prices of the factors shall also be remaining constant for

the period.

Apart from that it can be identified that as per the model the efficiency of the

company in terms of technology and the manpower shall also be remaining constant

for the company.

It is assumed that the cost and revenues function shall be linear.

The assumption is that the units produced are equal to the units sold which means

that there is no scope for the closing stock.

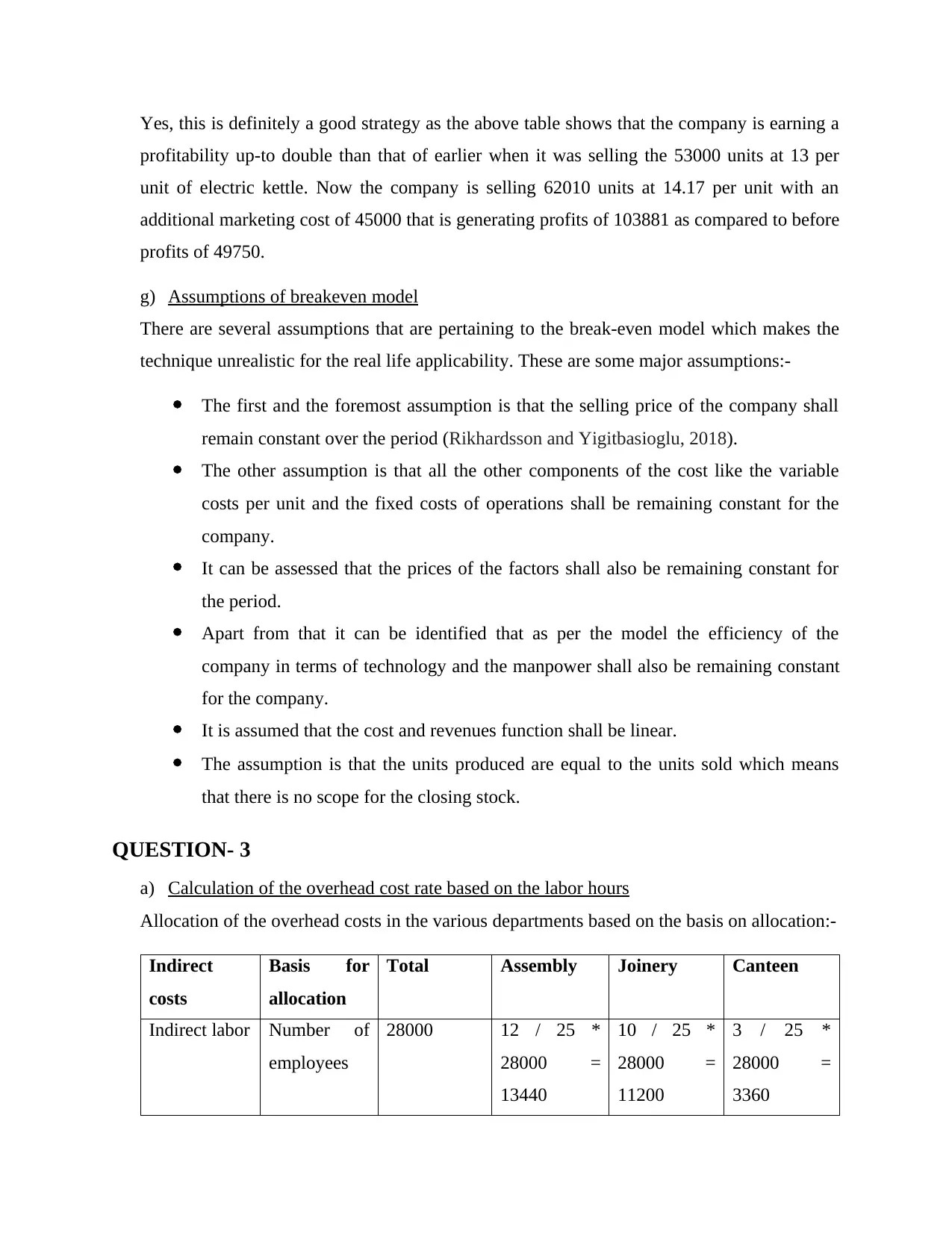

QUESTION- 3

a) Calculation of the overhead cost rate based on the labor hours

Allocation of the overhead costs in the various departments based on the basis on allocation:-

Indirect

costs

Basis for

allocation

Total Assembly Joinery Canteen

Indirect labor Number of

employees

28000 12 / 25 *

28000 =

13440

10 / 25 *

28000 =

11200

3 / 25 *

28000 =

3360

profitability up-to double than that of earlier when it was selling the 53000 units at 13 per

unit of electric kettle. Now the company is selling 62010 units at 14.17 per unit with an

additional marketing cost of 45000 that is generating profits of 103881 as compared to before

profits of 49750.

g) Assumptions of breakeven model

There are several assumptions that are pertaining to the break-even model which makes the

technique unrealistic for the real life applicability. These are some major assumptions:-

The first and the foremost assumption is that the selling price of the company shall

remain constant over the period (Rikhardsson and Yigitbasioglu, 2018).

The other assumption is that all the other components of the cost like the variable

costs per unit and the fixed costs of operations shall be remaining constant for the

company.

It can be assessed that the prices of the factors shall also be remaining constant for

the period.

Apart from that it can be identified that as per the model the efficiency of the

company in terms of technology and the manpower shall also be remaining constant

for the company.

It is assumed that the cost and revenues function shall be linear.

The assumption is that the units produced are equal to the units sold which means

that there is no scope for the closing stock.

QUESTION- 3

a) Calculation of the overhead cost rate based on the labor hours

Allocation of the overhead costs in the various departments based on the basis on allocation:-

Indirect

costs

Basis for

allocation

Total Assembly Joinery Canteen

Indirect labor Number of

employees

28000 12 / 25 *

28000 =

13440

10 / 25 *

28000 =

11200

3 / 25 *

28000 =

3360

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.