Financial Analysis: Cash Budgeting, Accounting Equation & M&S

VerifiedAdded on 2023/06/17

|10

|2820

|199

Report

AI Summary

This finance report provides a detailed analysis of cash budgeting, the accounting equation, and stakeholder identification, particularly in the context of large listed companies like Marks and Spencer. The report includes a three-month cash budget, highlighting transactions that impact cash flow, and explains the fundamental accounting equation, emphasizing its balance through the double-entry system. It further explores the benefits of listing shares on a stock exchange and identifies key stakeholders in a large corporation, examining their interests and impact. The report concludes by evaluating the reliability of profits as an indicator of cash balance, differentiating between the two concepts and clarifying that profit includes both cash and credit transactions, while cash balance reflects actual money available to the company. Desklib provides this document, among many others, as a valuable resource for students seeking to enhance their understanding of financial concepts and practices.

Finance (Distinction)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK- 1...........................................................................................................................................3

Detect the transactions which can be involved in cash budget. Also produce it for three

months....................................................................................................................................3

TASK- 2...........................................................................................................................................5

Explain Accounting equation. Also explain the reason of its correct application every time.

Also, give example.................................................................................................................5

Mention the benefits of listing down the shares in stock exchange.......................................5

Identify the stakeholders in large listed companies like Marks and Spencer........................6

Can profits be considered as a reliable indicator of the cash balance. Evaluate along with

providing the difference among them.....................................................................................8

REFERENCES..............................................................................................................................10

TASK- 1...........................................................................................................................................3

Detect the transactions which can be involved in cash budget. Also produce it for three

months....................................................................................................................................3

TASK- 2...........................................................................................................................................5

Explain Accounting equation. Also explain the reason of its correct application every time.

Also, give example.................................................................................................................5

Mention the benefits of listing down the shares in stock exchange.......................................5

Identify the stakeholders in large listed companies like Marks and Spencer........................6

Can profits be considered as a reliable indicator of the cash balance. Evaluate along with

providing the difference among them.....................................................................................8

REFERENCES..............................................................................................................................10

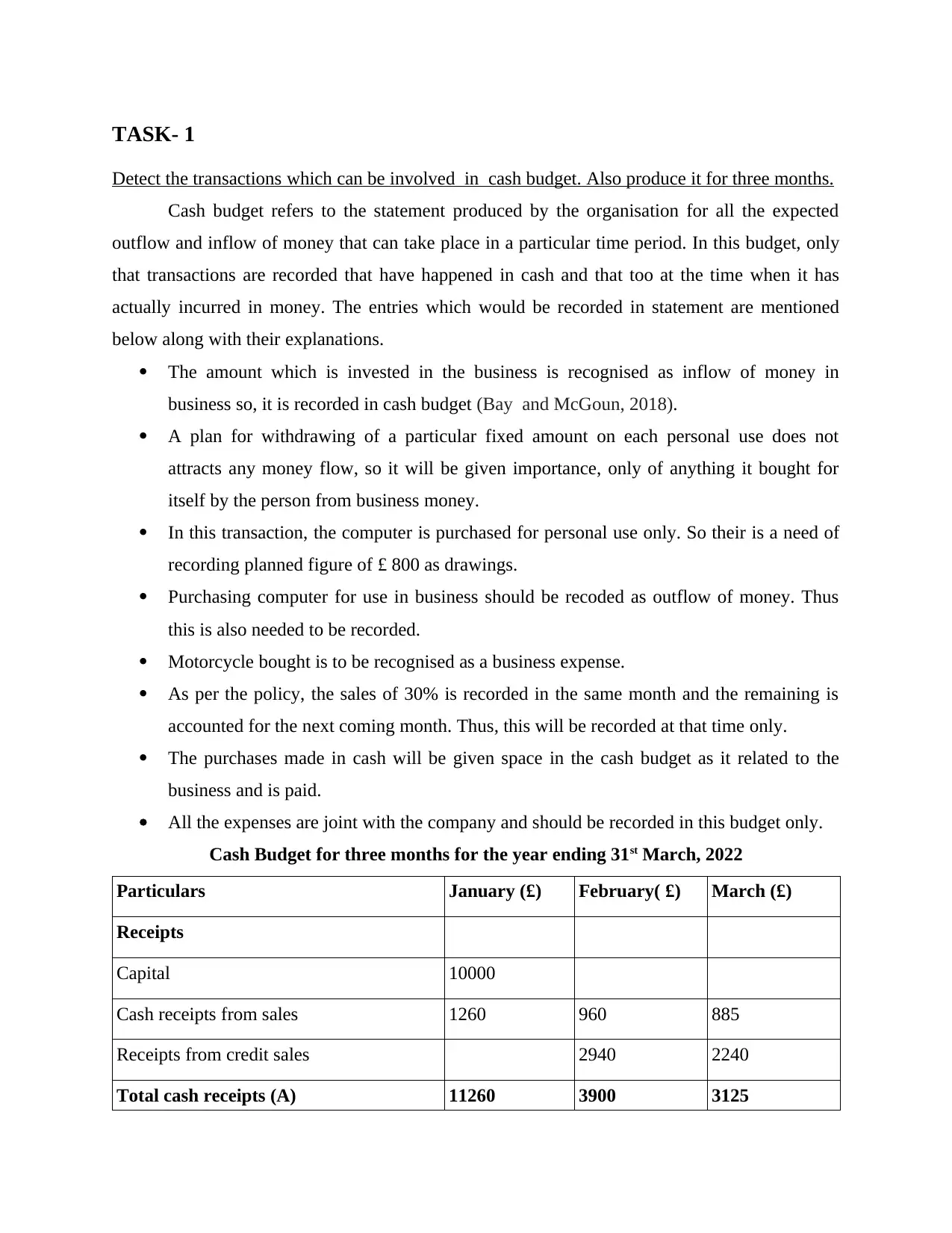

TASK- 1

Detect the transactions which can be involved in cash budget. Also produce it for three months.

Cash budget refers to the statement produced by the organisation for all the expected

outflow and inflow of money that can take place in a particular time period. In this budget, only

that transactions are recorded that have happened in cash and that too at the time when it has

actually incurred in money. The entries which would be recorded in statement are mentioned

below along with their explanations.

The amount which is invested in the business is recognised as inflow of money in

business so, it is recorded in cash budget (Bay and McGoun, 2018).

A plan for withdrawing of a particular fixed amount on each personal use does not

attracts any money flow, so it will be given importance, only of anything it bought for

itself by the person from business money.

In this transaction, the computer is purchased for personal use only. So their is a need of

recording planned figure of £ 800 as drawings.

Purchasing computer for use in business should be recoded as outflow of money. Thus

this is also needed to be recorded.

Motorcycle bought is to be recognised as a business expense.

As per the policy, the sales of 30% is recorded in the same month and the remaining is

accounted for the next coming month. Thus, this will be recorded at that time only.

The purchases made in cash will be given space in the cash budget as it related to the

business and is paid.

All the expenses are joint with the company and should be recorded in this budget only.

Cash Budget for three months for the year ending 31st March, 2022

Particulars January (£) February( £) March (£)

Receipts

Capital 10000

Cash receipts from sales 1260 960 885

Receipts from credit sales 2940 2240

Total cash receipts (A) 11260 3900 3125

Detect the transactions which can be involved in cash budget. Also produce it for three months.

Cash budget refers to the statement produced by the organisation for all the expected

outflow and inflow of money that can take place in a particular time period. In this budget, only

that transactions are recorded that have happened in cash and that too at the time when it has

actually incurred in money. The entries which would be recorded in statement are mentioned

below along with their explanations.

The amount which is invested in the business is recognised as inflow of money in

business so, it is recorded in cash budget (Bay and McGoun, 2018).

A plan for withdrawing of a particular fixed amount on each personal use does not

attracts any money flow, so it will be given importance, only of anything it bought for

itself by the person from business money.

In this transaction, the computer is purchased for personal use only. So their is a need of

recording planned figure of £ 800 as drawings.

Purchasing computer for use in business should be recoded as outflow of money. Thus

this is also needed to be recorded.

Motorcycle bought is to be recognised as a business expense.

As per the policy, the sales of 30% is recorded in the same month and the remaining is

accounted for the next coming month. Thus, this will be recorded at that time only.

The purchases made in cash will be given space in the cash budget as it related to the

business and is paid.

All the expenses are joint with the company and should be recorded in this budget only.

Cash Budget for three months for the year ending 31st March, 2022

Particulars January (£) February( £) March (£)

Receipts

Capital 10000

Cash receipts from sales 1260 960 885

Receipts from credit sales 2940 2240

Total cash receipts (A) 11260 3900 3125

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

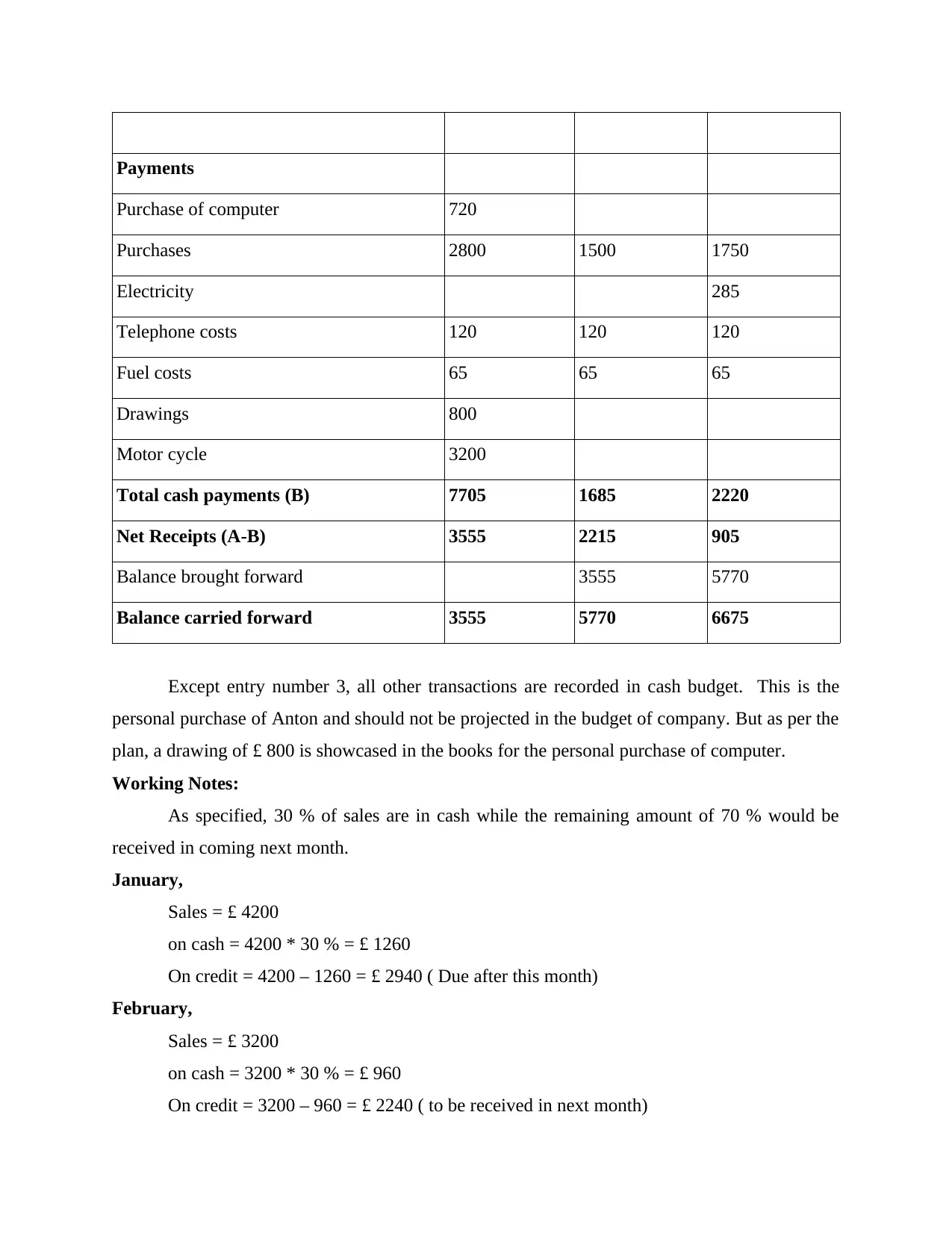

Payments

Purchase of computer 720

Purchases 2800 1500 1750

Electricity 285

Telephone costs 120 120 120

Fuel costs 65 65 65

Drawings 800

Motor cycle 3200

Total cash payments (B) 7705 1685 2220

Net Receipts (A-B) 3555 2215 905

Balance brought forward 3555 5770

Balance carried forward 3555 5770 6675

Except entry number 3, all other transactions are recorded in cash budget. This is the

personal purchase of Anton and should not be projected in the budget of company. But as per the

plan, a drawing of £ 800 is showcased in the books for the personal purchase of computer.

Working Notes:

As specified, 30 % of sales are in cash while the remaining amount of 70 % would be

received in coming next month.

January,

Sales = £ 4200

on cash = 4200 * 30 % = £ 1260

On credit = 4200 – 1260 = £ 2940 ( Due after this month)

February,

Sales = £ 3200

on cash = 3200 * 30 % = £ 960

On credit = 3200 – 960 = £ 2240 ( to be received in next month)

Purchase of computer 720

Purchases 2800 1500 1750

Electricity 285

Telephone costs 120 120 120

Fuel costs 65 65 65

Drawings 800

Motor cycle 3200

Total cash payments (B) 7705 1685 2220

Net Receipts (A-B) 3555 2215 905

Balance brought forward 3555 5770

Balance carried forward 3555 5770 6675

Except entry number 3, all other transactions are recorded in cash budget. This is the

personal purchase of Anton and should not be projected in the budget of company. But as per the

plan, a drawing of £ 800 is showcased in the books for the personal purchase of computer.

Working Notes:

As specified, 30 % of sales are in cash while the remaining amount of 70 % would be

received in coming next month.

January,

Sales = £ 4200

on cash = 4200 * 30 % = £ 1260

On credit = 4200 – 1260 = £ 2940 ( Due after this month)

February,

Sales = £ 3200

on cash = 3200 * 30 % = £ 960

On credit = 3200 – 960 = £ 2240 ( to be received in next month)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

March,

Sales = £ 2950

on cash = 2950 * 30 % = £ 885

On credit = 2950 * 70 % = £ 2065 ( Receivable in April)

TASK- 2

Explain Accounting equation. Also explain the reason of its correct application every time. Also,

give example.

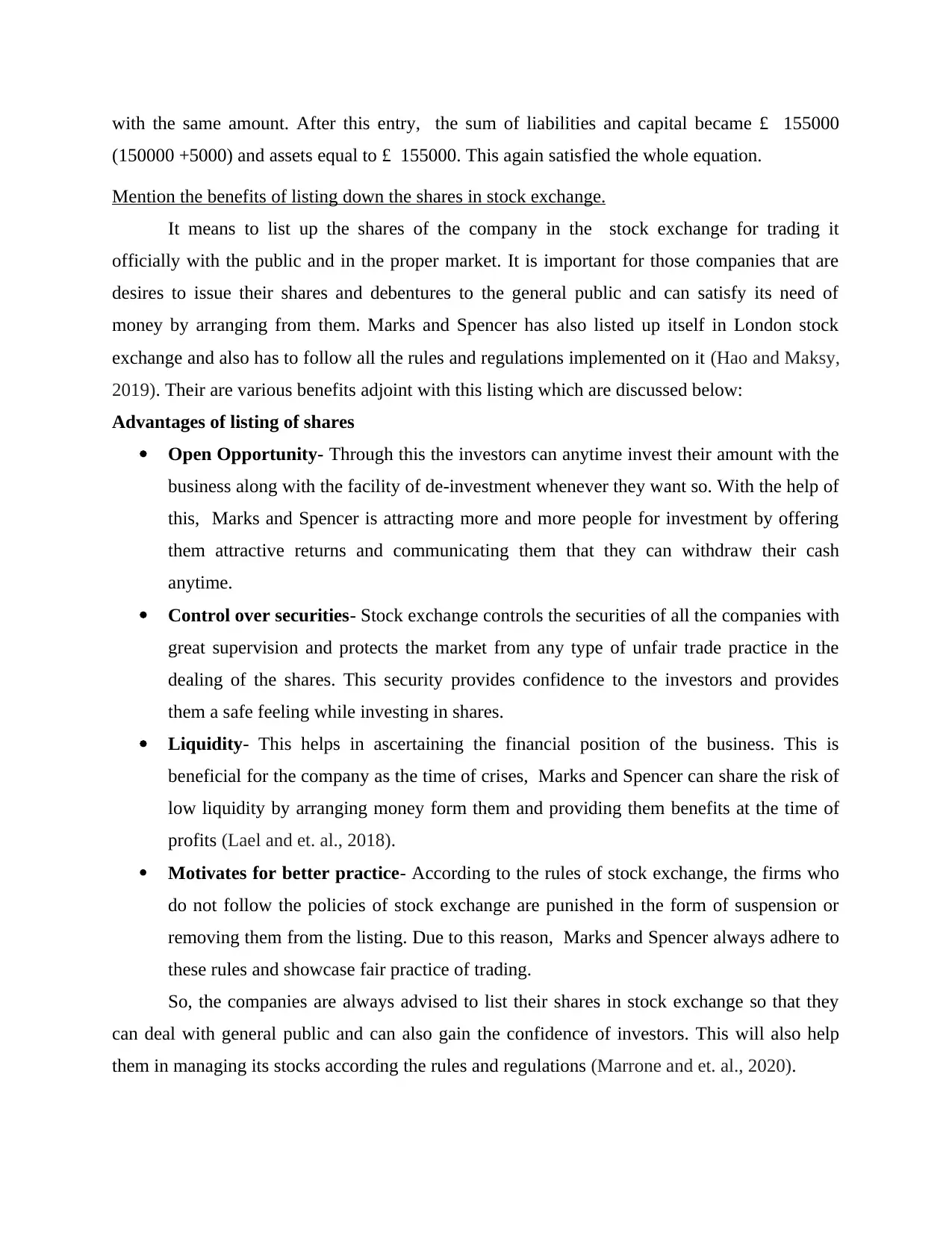

Accounting equation can be defined as a type of formula that helps in creating relation

among the capital, liabilities and assets of the corporation. It is the ground on which the system

of double entry are performed. As per this, it is necessary that the amounts of debit is equal to

the value credited. This simply means that the total of assets must be equal to the addition of

equity and debts (Gupta and Kumar, 2020).

Assets = Equity + Liabilities

This is analysed that the accounting equation always satisfy. The reason behind this

conformance is that it is processed according to the basic principle of double entry. All the

transactions in this process has two sided effect which helps in maintaining the balance for every

single entry. This means that all the entries have affect on minimum tow accounts which aids in

nurturing this balance (Bond and et. al., 2021).

For instance,

John invested £ 150000 in business. It then purchased furniture for office use amounting £ 5000

on credit.

Assets Capital + Liabilities

1 150000 150000

2 150000 + 5000 = 155000 5000

155000 150000 5000

In beginning, the investment made by John brought cash in the business and it also

increased the capital in the firm. Rise in both assets and equity balanced the equation. In next

entry, purchase of furniture on credit, raised the holding of assets by £5000 and liabilities too

Sales = £ 2950

on cash = 2950 * 30 % = £ 885

On credit = 2950 * 70 % = £ 2065 ( Receivable in April)

TASK- 2

Explain Accounting equation. Also explain the reason of its correct application every time. Also,

give example.

Accounting equation can be defined as a type of formula that helps in creating relation

among the capital, liabilities and assets of the corporation. It is the ground on which the system

of double entry are performed. As per this, it is necessary that the amounts of debit is equal to

the value credited. This simply means that the total of assets must be equal to the addition of

equity and debts (Gupta and Kumar, 2020).

Assets = Equity + Liabilities

This is analysed that the accounting equation always satisfy. The reason behind this

conformance is that it is processed according to the basic principle of double entry. All the

transactions in this process has two sided effect which helps in maintaining the balance for every

single entry. This means that all the entries have affect on minimum tow accounts which aids in

nurturing this balance (Bond and et. al., 2021).

For instance,

John invested £ 150000 in business. It then purchased furniture for office use amounting £ 5000

on credit.

Assets Capital + Liabilities

1 150000 150000

2 150000 + 5000 = 155000 5000

155000 150000 5000

In beginning, the investment made by John brought cash in the business and it also

increased the capital in the firm. Rise in both assets and equity balanced the equation. In next

entry, purchase of furniture on credit, raised the holding of assets by £5000 and liabilities too

with the same amount. After this entry, the sum of liabilities and capital became £ 155000

(150000 +5000) and assets equal to £ 155000. This again satisfied the whole equation.

Mention the benefits of listing down the shares in stock exchange.

It means to list up the shares of the company in the stock exchange for trading it

officially with the public and in the proper market. It is important for those companies that are

desires to issue their shares and debentures to the general public and can satisfy its need of

money by arranging from them. Marks and Spencer has also listed up itself in London stock

exchange and also has to follow all the rules and regulations implemented on it (Hao and Maksy,

2019). Their are various benefits adjoint with this listing which are discussed below:

Advantages of listing of shares

Open Opportunity- Through this the investors can anytime invest their amount with the

business along with the facility of de-investment whenever they want so. With the help of

this, Marks and Spencer is attracting more and more people for investment by offering

them attractive returns and communicating them that they can withdraw their cash

anytime.

Control over securities- Stock exchange controls the securities of all the companies with

great supervision and protects the market from any type of unfair trade practice in the

dealing of the shares. This security provides confidence to the investors and provides

them a safe feeling while investing in shares.

Liquidity- This helps in ascertaining the financial position of the business. This is

beneficial for the company as the time of crises, Marks and Spencer can share the risk of

low liquidity by arranging money form them and providing them benefits at the time of

profits (Lael and et. al., 2018).

Motivates for better practice- According to the rules of stock exchange, the firms who

do not follow the policies of stock exchange are punished in the form of suspension or

removing them from the listing. Due to this reason, Marks and Spencer always adhere to

these rules and showcase fair practice of trading.

So, the companies are always advised to list their shares in stock exchange so that they

can deal with general public and can also gain the confidence of investors. This will also help

them in managing its stocks according the rules and regulations (Marrone and et. al., 2020).

(150000 +5000) and assets equal to £ 155000. This again satisfied the whole equation.

Mention the benefits of listing down the shares in stock exchange.

It means to list up the shares of the company in the stock exchange for trading it

officially with the public and in the proper market. It is important for those companies that are

desires to issue their shares and debentures to the general public and can satisfy its need of

money by arranging from them. Marks and Spencer has also listed up itself in London stock

exchange and also has to follow all the rules and regulations implemented on it (Hao and Maksy,

2019). Their are various benefits adjoint with this listing which are discussed below:

Advantages of listing of shares

Open Opportunity- Through this the investors can anytime invest their amount with the

business along with the facility of de-investment whenever they want so. With the help of

this, Marks and Spencer is attracting more and more people for investment by offering

them attractive returns and communicating them that they can withdraw their cash

anytime.

Control over securities- Stock exchange controls the securities of all the companies with

great supervision and protects the market from any type of unfair trade practice in the

dealing of the shares. This security provides confidence to the investors and provides

them a safe feeling while investing in shares.

Liquidity- This helps in ascertaining the financial position of the business. This is

beneficial for the company as the time of crises, Marks and Spencer can share the risk of

low liquidity by arranging money form them and providing them benefits at the time of

profits (Lael and et. al., 2018).

Motivates for better practice- According to the rules of stock exchange, the firms who

do not follow the policies of stock exchange are punished in the form of suspension or

removing them from the listing. Due to this reason, Marks and Spencer always adhere to

these rules and showcase fair practice of trading.

So, the companies are always advised to list their shares in stock exchange so that they

can deal with general public and can also gain the confidence of investors. This will also help

them in managing its stocks according the rules and regulations (Marrone and et. al., 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Identify the stakeholders in large listed companies like Marks and Spencer.

These people are linked with the organisation either directly or indirectly. They are

affected by the incomes, losses and operations of the business. They takes high interest in the

financial reports and the success of the company. Their are number of stakeholders of Marks

and Spencer which are discussed below:

Employees- They give their own time to the firm by working their for the purpose of

earning salary and increasing their reputation. Their are near about 70000 workers in

Marks and Spencer. These people are interested in generating information about the

profits earned by the firm, through which they can assure that of their jobs are secure

with the company. They also wants to know that whether their efforts are generating

profits for the corporation or not.

Customers- These are the consumers of the products sold by Marks and Spencer. They

want the firm to provide them good service and products with high quality along with

reasonable prices. Business keeps an eye on the movement of goods and attempts to

guess out the change in demand and choices of the customers. This helps them in

constructing the good as per the desired of the client along with maintaining contacts with

them. This also helps them in providing better after sale services (McMillan and Casey,,

2018).

Government- they are the regulating authorities that specifies the rules related to the

concerned business. Marks and Spencer is required to perform as per these rules. They

keeps this thing in mind that they follow all the regulations mentioned in health

regularities, company act and all the other frameworks in the business. Government also

seeks to know that the organisation is accomplishing with all the rules and paying its

taxes correctly without any evasion.

Suppliers- These are the people who sells goods and raw material to Marks and Spencer .

Their are number of suppliers for the company at global level. So, the company is in

desire of such contractors who can avail them good quality product at reasonable price

and with full safety. Thus, it is mandatory for them to maintain quality relations with

these persons or businesses. They holds the power of affecting the business at large scale

for it tries to avoid any kind of conflict with them (Ng, 2018).

These people are linked with the organisation either directly or indirectly. They are

affected by the incomes, losses and operations of the business. They takes high interest in the

financial reports and the success of the company. Their are number of stakeholders of Marks

and Spencer which are discussed below:

Employees- They give their own time to the firm by working their for the purpose of

earning salary and increasing their reputation. Their are near about 70000 workers in

Marks and Spencer. These people are interested in generating information about the

profits earned by the firm, through which they can assure that of their jobs are secure

with the company. They also wants to know that whether their efforts are generating

profits for the corporation or not.

Customers- These are the consumers of the products sold by Marks and Spencer. They

want the firm to provide them good service and products with high quality along with

reasonable prices. Business keeps an eye on the movement of goods and attempts to

guess out the change in demand and choices of the customers. This helps them in

constructing the good as per the desired of the client along with maintaining contacts with

them. This also helps them in providing better after sale services (McMillan and Casey,,

2018).

Government- they are the regulating authorities that specifies the rules related to the

concerned business. Marks and Spencer is required to perform as per these rules. They

keeps this thing in mind that they follow all the regulations mentioned in health

regularities, company act and all the other frameworks in the business. Government also

seeks to know that the organisation is accomplishing with all the rules and paying its

taxes correctly without any evasion.

Suppliers- These are the people who sells goods and raw material to Marks and Spencer .

Their are number of suppliers for the company at global level. So, the company is in

desire of such contractors who can avail them good quality product at reasonable price

and with full safety. Thus, it is mandatory for them to maintain quality relations with

these persons or businesses. They holds the power of affecting the business at large scale

for it tries to avoid any kind of conflict with them (Ng, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholders- They are the investors of Marks and Spencer on whose money the whole

firm runs its operations. They purchase the shares of the firm so they are interested in

knowing that whether the business is earning profits or facing losses. They desire that the

company earns more and more profits so that they can earn dividend from them. Marks

and Spencer makes sure that they distribute adequate amount of profits because on the

basis of this, further investors decide that whether they should invest in the organisation

or not. The company also conduct meeting with these shareholders and makes

discussions about the changes required in the business.

All the persons mentioned above are equally important stakeholders for Marks and

Spencer. The firm has to satisfy all of them by addressing to their demands and maintaining good

relation with them. All these stakeholders are very much interested in the financial statements of

the company so they have to they present the report without any type of error or fraud, so that

correct decision can be taken by users of these reports.

Can profits be considered as a reliable indicator of the cash balance. Evaluate along with

providing the difference among them.

No, profits are never the trustful indicator of cash hold by the company. Money is defined

as the amount present with the firm in its physical format or in the bank. It is received by the

business through sales, investment made in the business or any other income and decrease

through payment made for expenses and purchases. But these things are included in cash only at

the time when they are actually realised in money format. But when talking about the profits, it

does not depends on cash. This is because, profits includes all the transactions whether they have

taken place in cash or credit basis. The profits works on the accrual system where income earned

but not received is also included in it, while it is not considered in cash calculation. The profits

gives importance to all the transactions which took place in that accounting year irrespective of

the fact that it is realised in money or not (Secinaro and et. al., 2021).

Looking at the mathematical expression, profit is the difference between the incomes and

expenses. But it does not go in detail that whether that entries have happened in monetary format

or not. Thus, it is very much clear that the profit earned by business is not a reliable indicator of

the cash possess by the firm. It also means that if the firm is earning high level of profits, then it

will also be having hold on huge level of cash. This is because of the nature of profits to

recognise non cash transactions in it.

firm runs its operations. They purchase the shares of the firm so they are interested in

knowing that whether the business is earning profits or facing losses. They desire that the

company earns more and more profits so that they can earn dividend from them. Marks

and Spencer makes sure that they distribute adequate amount of profits because on the

basis of this, further investors decide that whether they should invest in the organisation

or not. The company also conduct meeting with these shareholders and makes

discussions about the changes required in the business.

All the persons mentioned above are equally important stakeholders for Marks and

Spencer. The firm has to satisfy all of them by addressing to their demands and maintaining good

relation with them. All these stakeholders are very much interested in the financial statements of

the company so they have to they present the report without any type of error or fraud, so that

correct decision can be taken by users of these reports.

Can profits be considered as a reliable indicator of the cash balance. Evaluate along with

providing the difference among them.

No, profits are never the trustful indicator of cash hold by the company. Money is defined

as the amount present with the firm in its physical format or in the bank. It is received by the

business through sales, investment made in the business or any other income and decrease

through payment made for expenses and purchases. But these things are included in cash only at

the time when they are actually realised in money format. But when talking about the profits, it

does not depends on cash. This is because, profits includes all the transactions whether they have

taken place in cash or credit basis. The profits works on the accrual system where income earned

but not received is also included in it, while it is not considered in cash calculation. The profits

gives importance to all the transactions which took place in that accounting year irrespective of

the fact that it is realised in money or not (Secinaro and et. al., 2021).

Looking at the mathematical expression, profit is the difference between the incomes and

expenses. But it does not go in detail that whether that entries have happened in monetary format

or not. Thus, it is very much clear that the profit earned by business is not a reliable indicator of

the cash possess by the firm. It also means that if the firm is earning high level of profits, then it

will also be having hold on huge level of cash. This is because of the nature of profits to

recognise non cash transactions in it.

Comparison among the cash and profits

Cash comprises of money held the business after settling down all its debts and expenses

and receiving money form operating, financing and investing activities. On the other

hand, profits accounts for only operating activities.

Profits comprises of cash as well as non cash entries while cash does not involve any

transaction which has not happened on money in actual.

The later one does not holds the power to show the liquidity position of the firm but the

former one represents the cash held by it which helps in knowing the liquidity condition

and analysing the performance of the firm.

On the whole, it can be concluded that the business should never rely only on profits for

checking the cash balance available with it.

Cash comprises of money held the business after settling down all its debts and expenses

and receiving money form operating, financing and investing activities. On the other

hand, profits accounts for only operating activities.

Profits comprises of cash as well as non cash entries while cash does not involve any

transaction which has not happened on money in actual.

The later one does not holds the power to show the liquidity position of the firm but the

former one represents the cash held by it which helps in knowing the liquidity condition

and analysing the performance of the firm.

On the whole, it can be concluded that the business should never rely only on profits for

checking the cash balance available with it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Badu, B. and Appiah, K.O., 2018. Value relevance of accounting information: an emerging

country perspective. Journal of Accounting & Organizational Change.

Bay, T. and McGoun, S., 2018. Critical Finance Studies–Editorial. Critical Perspectives on

Accounting. 52. pp.1-3.

Bond, D. and et. al., 2021. Research productivity of Australian accounting

academics. Accounting & Finance. 61(1). pp.1081-1104.

Gupta, C.M. and Kumar, D., 2020. Creative accounting a tool for financial crime: a review of the

techniques and its effects. Journal of Financial Crime.

Hao, Q. and Maksy, M.M., 2019. Factors Associated with Student Performance in Advanced

Accounting: An Empirical Study at a US Residential Public University. Journal of

Accounting and Finance. 19(4). pp.162-180.

Laela, S.F. and et. al., 2018. Management accounting-strategy coalignment in Islamic

banking. International Journal of Islamic and Middle Eastern Finance and

Management.

Marrone, M. and et. al., 2020. Trends in environmental accounting research within and outside of

the accounting discipline. Accounting, Auditing & Accountability Journal.

McMillan, G.S. and Casey, D.L., 2018. Examining the scope of the accounting literature: a

bibliometric review of a decade of research. International Journal of Bibliometrics in

Business and Management. 1(2). pp.147-159.

Ng, A.W., 2018. From sustainability accounting to a green financing system: Institutional

legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner

Production. 195. pp.585-592.

Secinaro, S. and et. al., 2021. Blockchain in the accounting, auditing and accountability fields: a

bibliometric and coding analysis. Accounting, Auditing & Accountability Journal.

Books and Journals

Badu, B. and Appiah, K.O., 2018. Value relevance of accounting information: an emerging

country perspective. Journal of Accounting & Organizational Change.

Bay, T. and McGoun, S., 2018. Critical Finance Studies–Editorial. Critical Perspectives on

Accounting. 52. pp.1-3.

Bond, D. and et. al., 2021. Research productivity of Australian accounting

academics. Accounting & Finance. 61(1). pp.1081-1104.

Gupta, C.M. and Kumar, D., 2020. Creative accounting a tool for financial crime: a review of the

techniques and its effects. Journal of Financial Crime.

Hao, Q. and Maksy, M.M., 2019. Factors Associated with Student Performance in Advanced

Accounting: An Empirical Study at a US Residential Public University. Journal of

Accounting and Finance. 19(4). pp.162-180.

Laela, S.F. and et. al., 2018. Management accounting-strategy coalignment in Islamic

banking. International Journal of Islamic and Middle Eastern Finance and

Management.

Marrone, M. and et. al., 2020. Trends in environmental accounting research within and outside of

the accounting discipline. Accounting, Auditing & Accountability Journal.

McMillan, G.S. and Casey, D.L., 2018. Examining the scope of the accounting literature: a

bibliometric review of a decade of research. International Journal of Bibliometrics in

Business and Management. 1(2). pp.147-159.

Ng, A.W., 2018. From sustainability accounting to a green financing system: Institutional

legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner

Production. 195. pp.585-592.

Secinaro, S. and et. al., 2021. Blockchain in the accounting, auditing and accountability fields: a

bibliometric and coding analysis. Accounting, Auditing & Accountability Journal.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.