Comprehensive Finance Report: Cash Budgeting and Financial Concepts

VerifiedAdded on 2023/06/08

|10

|2646

|54

Report

AI Summary

This finance assignment provides a detailed analysis of cash budgeting for Surya Trading, covering a six-month period ending December 31, 2022. It includes the preparation of a cash budget, explanation of the differences between cash and profits, and differentiation between capital and revenue expenditure, expenses and drawings, gross profit and net profit, cash budget and cash flow statements, and accrual and prepayments. The assignment also explains various financial concepts such as assets, liabilities, ordinary shares, preference shares, dividends, stock exchange, venture capital, budget, capital income, and company. It further delves into business transactions that do not involve immediate cash movement and the implications of these concepts on financial decision-making.

FINANCE (PASS

CRITERIA)

CRITERIA)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1.1.........................................................................................................................................3

Prepare Cash budget for Surya trading for six months ending on 31st December 2022.........3

TASK 2.1.........................................................................................................................................5

A. Explain if cash and profits similar. Can there be any business transactions which does not

consider an immediate movement of cash..............................................................................5

B. Differentiate between.........................................................................................................6

C. Explain the following.........................................................................................................7

REFERENCES..............................................................................................................................10

TASK 1.1.........................................................................................................................................3

Prepare Cash budget for Surya trading for six months ending on 31st December 2022.........3

TASK 2.1.........................................................................................................................................5

A. Explain if cash and profits similar. Can there be any business transactions which does not

consider an immediate movement of cash..............................................................................5

B. Differentiate between.........................................................................................................6

C. Explain the following.........................................................................................................7

REFERENCES..............................................................................................................................10

TASK 1.1

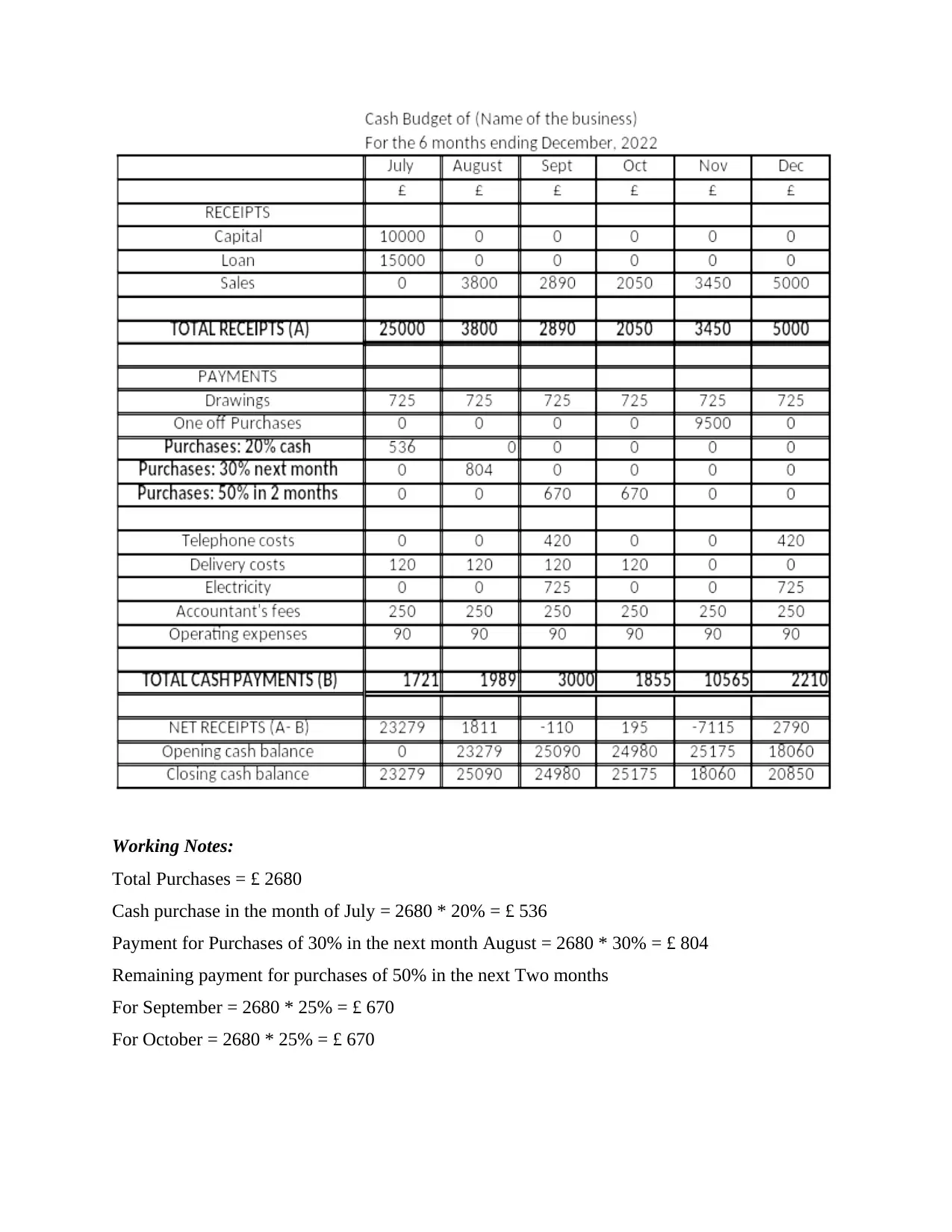

Prepare Cash budget for Surya trading for six months ending on 31st December 2022.

Cash budget: Cash budget can be explained as an estimation of cash flow of a business

over a certain time period. It could be for a month, year or on quarter basis as well. Such budgets

are useful In examining whether the business is having adequate funds available for managing

and continuing operational activities for a given time frame (Amos and et.al, 2021). A company's

cash budget is an essential metric which would help in maintaining financial stability, it helps the

company to compute a variety of range for several planning purposes as well. The primary

objective and aim of a cash budget is to forecast futuristic cash balance in relation to identify and

find potential surpluses and deficits.

Prepare Cash budget for Surya trading for six months ending on 31st December 2022.

Cash budget: Cash budget can be explained as an estimation of cash flow of a business

over a certain time period. It could be for a month, year or on quarter basis as well. Such budgets

are useful In examining whether the business is having adequate funds available for managing

and continuing operational activities for a given time frame (Amos and et.al, 2021). A company's

cash budget is an essential metric which would help in maintaining financial stability, it helps the

company to compute a variety of range for several planning purposes as well. The primary

objective and aim of a cash budget is to forecast futuristic cash balance in relation to identify and

find potential surpluses and deficits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working Notes:

Total Purchases = £ 2680

Cash purchase in the month of July = 2680 * 20% = £ 536

Payment for Purchases of 30% in the next month August = 2680 * 30% = £ 804

Remaining payment for purchases of 50% in the next Two months

For September = 2680 * 25% = £ 670

For October = 2680 * 25% = £ 670

Total Purchases = £ 2680

Cash purchase in the month of July = 2680 * 20% = £ 536

Payment for Purchases of 30% in the next month August = 2680 * 30% = £ 804

Remaining payment for purchases of 50% in the next Two months

For September = 2680 * 25% = £ 670

For October = 2680 * 25% = £ 670

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2.1

A. Explain if cash and profits similar. Can there be any business transactions which does not

consider an immediate movement of cash.

No, cash and profits are not similar they have some basic differences which helps to have

a better understanding as where they stand apart from each other. The term Cash and profits can

be explained as under:

Cash: Cash can be explained as a movement of funds which a company or business would send

and receive. Cash flow defines money inflow and outflow of funds in a company, but doesn't

count other aspects of the financial picture.

Profits: Profit can be stated as positive financial difference among a firm's revenue and their

operating expenses as well as current liabilities too. At the end of a financial time span, a

company would be looking after income generated from cash flow, having a look at total

revenues, subtracting the outflow of cash or expenditures would help to compute profit earned by

the company.

Difference between Cash and profits:

The main difference which can be explained among the two terms taken into account is

that profit clearly indicates the quantity of money which is left over after all expenses

have been covered whereas cash flow indicates the net flow of funds which are taking

place in a business.

Profit is a type of revenue which helps to cover unpredictable and unseen risks/ losses as

well. It is considered as a helping hand in making the business run for a longer span and

contribute in carrying out its functions and operations in a more efficient and effective

manner as well. In case of cash it is only accountable for the functions where it has been

used for covering the payments and debts of a company. It also indicates the level of

liquidity the business is managing and in what ways it would help in settling loans and

insurances as well (Amos and et.al, 2021).

Cash flow and net profit are helpful in measuring different things. While profit’s

ultimate goal is to reflect financial health of the business whereas in case of cash it is the

lifeblood of firm which would help in keeping operations ticking over on a regular basis.

Yes, there are business transactions which does not demand for immediate movement of

cash from business such as purchasing goods from vendor on credit basis. In such cases, cash is

A. Explain if cash and profits similar. Can there be any business transactions which does not

consider an immediate movement of cash.

No, cash and profits are not similar they have some basic differences which helps to have

a better understanding as where they stand apart from each other. The term Cash and profits can

be explained as under:

Cash: Cash can be explained as a movement of funds which a company or business would send

and receive. Cash flow defines money inflow and outflow of funds in a company, but doesn't

count other aspects of the financial picture.

Profits: Profit can be stated as positive financial difference among a firm's revenue and their

operating expenses as well as current liabilities too. At the end of a financial time span, a

company would be looking after income generated from cash flow, having a look at total

revenues, subtracting the outflow of cash or expenditures would help to compute profit earned by

the company.

Difference between Cash and profits:

The main difference which can be explained among the two terms taken into account is

that profit clearly indicates the quantity of money which is left over after all expenses

have been covered whereas cash flow indicates the net flow of funds which are taking

place in a business.

Profit is a type of revenue which helps to cover unpredictable and unseen risks/ losses as

well. It is considered as a helping hand in making the business run for a longer span and

contribute in carrying out its functions and operations in a more efficient and effective

manner as well. In case of cash it is only accountable for the functions where it has been

used for covering the payments and debts of a company. It also indicates the level of

liquidity the business is managing and in what ways it would help in settling loans and

insurances as well (Amos and et.al, 2021).

Cash flow and net profit are helpful in measuring different things. While profit’s

ultimate goal is to reflect financial health of the business whereas in case of cash it is the

lifeblood of firm which would help in keeping operations ticking over on a regular basis.

Yes, there are business transactions which does not demand for immediate movement of

cash from business such as purchasing goods from vendor on credit basis. In such cases, cash is

not involved at the time of transaction, the consideration is being paid and covered after a certain

time period. In such situations goods are being purchased from the seller and amount is paid on

due date or a future date which is being decided well in advance. Here, it becomes easier for the

enterprise to focus on other areas and have ample of time available for covering costs incurred

over a period of time. Another transaction can be internal based transactions which does not

consider or involve any external parties and such transaction even doesn't include any exchange

in value with other external party example could be reducing valuation of fixed assets. One more

transaction which could be explained is buying or purchasing insurance from a insurer (Burlacu

and et.al, 2019). It explains in what ways insurance can provide protection towards the purchased

and acquired goods and services. In such cases the insurance amount is paid after the premium

starts and not on immediate basis.

B. Differentiate between

a) Capital expenditure and revenue expenditure

Capital expenditure expenditures contribute to the revenue earning capacity of a business

over more than one accounting period. These expenditures are shown in balance sheet. The

examples of capital expenditure are purchase of machinery, manufacturing equipment.

Revenue expenditure are incurred to generate revenue for a particular accounting period.

These expenditures are shown in profit and loss account. The examples of revenue expenditure

are wages and salary expenses. It can be fully tax deducted in the same accounting period. These

expenditures are incurred for short term that are used in running daily business operations.

b) Expenses and drawings

Expenses is spent to generate income for the business. These expenditures can be classified

into two parts revenue and capital expenditure. Revenue expenditures are shown in profit and

loss account and capital expenditures are shown in profit and loss account. The expenses can

have recorded in two methods of accounting such as cash basis or accrual basis.

Drawings means owner of the money take money for the personal purpose. It reduces the

capital of a business. Drawings are shown in balance sheet as liability side by reducing the

capital. It is not a business expenses.

c) Gross profit and net profit

Gross profit is determined by reducing cost of goods sold from the total revenue of the

company. Cost of goods sold means how much money has spent for making the product. It

time period. In such situations goods are being purchased from the seller and amount is paid on

due date or a future date which is being decided well in advance. Here, it becomes easier for the

enterprise to focus on other areas and have ample of time available for covering costs incurred

over a period of time. Another transaction can be internal based transactions which does not

consider or involve any external parties and such transaction even doesn't include any exchange

in value with other external party example could be reducing valuation of fixed assets. One more

transaction which could be explained is buying or purchasing insurance from a insurer (Burlacu

and et.al, 2019). It explains in what ways insurance can provide protection towards the purchased

and acquired goods and services. In such cases the insurance amount is paid after the premium

starts and not on immediate basis.

B. Differentiate between

a) Capital expenditure and revenue expenditure

Capital expenditure expenditures contribute to the revenue earning capacity of a business

over more than one accounting period. These expenditures are shown in balance sheet. The

examples of capital expenditure are purchase of machinery, manufacturing equipment.

Revenue expenditure are incurred to generate revenue for a particular accounting period.

These expenditures are shown in profit and loss account. The examples of revenue expenditure

are wages and salary expenses. It can be fully tax deducted in the same accounting period. These

expenditures are incurred for short term that are used in running daily business operations.

b) Expenses and drawings

Expenses is spent to generate income for the business. These expenditures can be classified

into two parts revenue and capital expenditure. Revenue expenditures are shown in profit and

loss account and capital expenditures are shown in profit and loss account. The expenses can

have recorded in two methods of accounting such as cash basis or accrual basis.

Drawings means owner of the money take money for the personal purpose. It reduces the

capital of a business. Drawings are shown in balance sheet as liability side by reducing the

capital. It is not a business expenses.

c) Gross profit and net profit

Gross profit is determined by reducing cost of goods sold from the total revenue of the

company. Cost of goods sold means how much money has spent for making the product. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shows in income statement account. Cost of goods sold includes direct labour, direct wages and

direct raw of materials.

Net profit is determined by reducing all operating expenses includes interest and taxes

from the gross profit. It helps to make business decision and create accurate financial statements.

It includes indirect expenses salary, rent, printing and stationery. Before calculating net profit,

the company must know gross profit (Swamy and et.al, 2019).

d) Cash budget and cash flow statements.

Cash budget determines the cash flow of a business for a specific time. It can be prepared

monthly, quarterly and annually. The objective of cash budget to determine whether the entity

has sufficient cash to continue the business for a long term. It can be viewed for short term and

long term.

Cash flow statement provides information about the changes in cash and cash equivalents

of an enterprises. The main objective is to explain the cash movements between two points that

is sources of funds and applications of funds. It can be viewed for long term period (Timperley,

2021).

e) Accrual and prepayments

Accrual means those expenses which are due in current accounting period but were not in

current accounting period. It shows in balance sheet as a liability side. It is a liability for the

company. Example is outstanding wages.

Prepayments means those expenses which will due in next accounting period but paid in

current accounting period. It shows in balance sheet as asset side. Prepayment expenses are asset

for the company. Examples are prepaid bills and loan repayment before the due date (Vasileiou,

2021).

C. Explain the following

a) Asset

Asset is a resource of the company, Individual and others owns with the purpose of that it

will give a future economic benefit. It is shown on a company's balance sheet. An Asset can be

divided as tangible, intangible, current and financial (He and Li, 2021). Current assets are those

assets which can be converted to cash such as debtor and inventory. It is retained in the company

to increases company growth. An asset is to generate cash flow, increases sales and increases

company value (Jung and et.al, 2020).

direct raw of materials.

Net profit is determined by reducing all operating expenses includes interest and taxes

from the gross profit. It helps to make business decision and create accurate financial statements.

It includes indirect expenses salary, rent, printing and stationery. Before calculating net profit,

the company must know gross profit (Swamy and et.al, 2019).

d) Cash budget and cash flow statements.

Cash budget determines the cash flow of a business for a specific time. It can be prepared

monthly, quarterly and annually. The objective of cash budget to determine whether the entity

has sufficient cash to continue the business for a long term. It can be viewed for short term and

long term.

Cash flow statement provides information about the changes in cash and cash equivalents

of an enterprises. The main objective is to explain the cash movements between two points that

is sources of funds and applications of funds. It can be viewed for long term period (Timperley,

2021).

e) Accrual and prepayments

Accrual means those expenses which are due in current accounting period but were not in

current accounting period. It shows in balance sheet as a liability side. It is a liability for the

company. Example is outstanding wages.

Prepayments means those expenses which will due in next accounting period but paid in

current accounting period. It shows in balance sheet as asset side. Prepayment expenses are asset

for the company. Examples are prepaid bills and loan repayment before the due date (Vasileiou,

2021).

C. Explain the following

a) Asset

Asset is a resource of the company, Individual and others owns with the purpose of that it

will give a future economic benefit. It is shown on a company's balance sheet. An Asset can be

divided as tangible, intangible, current and financial (He and Li, 2021). Current assets are those

assets which can be converted to cash such as debtor and inventory. It is retained in the company

to increases company growth. An asset is to generate cash flow, increases sales and increases

company value (Jung and et.al, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Liability

It is something that is owed by the company which is recorded in the balance sheet.

Liabilities are both non-current and current. Non-current liability means that liability which are

due for long period for example, debenture. Current liabilities mean those liabilities which are

due for one accounting period examples are trade payables and outstanding expenses. It is

obligations that are rising out of previous transaction which is paid by the company through the

revenue generated by the company.

c) Ordinary shares

Total capital of the company is divided into the two parts ordinary shares and preference

share. It is also known as equity shares. Buyers of these stocks are the actual owners of the

company. The owner of ordinary shares is not fixed a dividend. If company earns more profit in

any financial year then company distributes surplus profit to the equity share holder (Khan and

et.al, 2021).

d) Preference share

The people who acquire preference shares known as preference share holder. They are

assured of a fixed dividend rate. In the case of winding up of the company they have right to be

paid in the first capital and dividend. Preference shareholders do not have voting right in the

company (Kouvelis and et.al, 2018).

e) Dividend

It means distribution of a company earning to its shareholders. The dividend payment

amounts are determined by the board of directors. If company earns more profit, then surplus

amount does not distribute to its shareholder and retain earnings to be invested back into the

company.

f) Stock exchange

Securities exchange means those place where the traders can sell and buy the shares and

securities. It also gives the facilities for the issuer and redemption of the shares. The stock

exchange is controlled by the regulatory authority. It is the primary market where the companies

float shares to the general public in an initial public offering to raise the capital (Li and et.al,

2020).

g) Venture capital

It is something that is owed by the company which is recorded in the balance sheet.

Liabilities are both non-current and current. Non-current liability means that liability which are

due for long period for example, debenture. Current liabilities mean those liabilities which are

due for one accounting period examples are trade payables and outstanding expenses. It is

obligations that are rising out of previous transaction which is paid by the company through the

revenue generated by the company.

c) Ordinary shares

Total capital of the company is divided into the two parts ordinary shares and preference

share. It is also known as equity shares. Buyers of these stocks are the actual owners of the

company. The owner of ordinary shares is not fixed a dividend. If company earns more profit in

any financial year then company distributes surplus profit to the equity share holder (Khan and

et.al, 2021).

d) Preference share

The people who acquire preference shares known as preference share holder. They are

assured of a fixed dividend rate. In the case of winding up of the company they have right to be

paid in the first capital and dividend. Preference shareholders do not have voting right in the

company (Kouvelis and et.al, 2018).

e) Dividend

It means distribution of a company earning to its shareholders. The dividend payment

amounts are determined by the board of directors. If company earns more profit, then surplus

amount does not distribute to its shareholder and retain earnings to be invested back into the

company.

f) Stock exchange

Securities exchange means those place where the traders can sell and buy the shares and

securities. It also gives the facilities for the issuer and redemption of the shares. The stock

exchange is controlled by the regulatory authority. It is the primary market where the companies

float shares to the general public in an initial public offering to raise the capital (Li and et.al,

2020).

g) Venture capital

It is the part of private equity. Before the start-up of the business the owner required fund

as a venture capital of investors. It provides to small company for the quickly grown. It can be

provided the fund after evaluation of the company. It is different from the other private equity

because it focuses on emerging companies seeking substantial funds for the first time. After the

introduce of venture capital the result is change in venture capital ecosystem.

h) Budget

A budget is tool of management which is used in planning, programming and controlling

the business activity. It can be prepared monthly quarterly and yearly. It needs to be change and

corrected every time when change in business situations. It is prepared on the basis of past data.

The budget result is to compared with the actual result and if there is any deficiency found there

then it prepared again or corrected.

i) Capital Income

It is also known as capital gain. It is those profit which is earns on the sale of long term

assets. Long term assets include shares and fixed assets. If the selling price of the asset exceed of

the purchase price, then difference between both prices are known as capital gain. It is increase

the value of capital asset (Ma and et.al, 2019).

j) Company

The company is incorporated under the company’s act. Company is a legal entity formed

by a group of individual. The company can be two types (Macchiavello and et.al, 2022).

1. Private company- It means a company having a minimum paid up share capital. It

prohibits any invitation to the public.

2. Public company- It is not a private company. It has a minimum paid up share capital as

may have prescribed in company prospectus.

as a venture capital of investors. It provides to small company for the quickly grown. It can be

provided the fund after evaluation of the company. It is different from the other private equity

because it focuses on emerging companies seeking substantial funds for the first time. After the

introduce of venture capital the result is change in venture capital ecosystem.

h) Budget

A budget is tool of management which is used in planning, programming and controlling

the business activity. It can be prepared monthly quarterly and yearly. It needs to be change and

corrected every time when change in business situations. It is prepared on the basis of past data.

The budget result is to compared with the actual result and if there is any deficiency found there

then it prepared again or corrected.

i) Capital Income

It is also known as capital gain. It is those profit which is earns on the sale of long term

assets. Long term assets include shares and fixed assets. If the selling price of the asset exceed of

the purchase price, then difference between both prices are known as capital gain. It is increase

the value of capital asset (Ma and et.al, 2019).

j) Company

The company is incorporated under the company’s act. Company is a legal entity formed

by a group of individual. The company can be two types (Macchiavello and et.al, 2022).

1. Private company- It means a company having a minimum paid up share capital. It

prohibits any invitation to the public.

2. Public company- It is not a private company. It has a minimum paid up share capital as

may have prescribed in company prospectus.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Amos and et.al, 2021. The mediating effects of finance on the performance of hospital facilities

management services. Journal of Building Engineering, 34, p.101899.

Burlacu and et.al, 2019. Impact of demography on the public finance of the European

Union. Quality-Access to Success, 20.

He, Q. and Li, X., 2021. The failure of Chinese peer-to-peer lending platforms: Finance and

politics. Journal of Corporate Finance, 66, p.101852.

Jung and et.al, 2020. Public finance responses to COVID-19 in Korea. National Tax

Journal, 73(3), pp.879-900.

Khan and et.al, 2021. Artificial intelligence and NLP-based chatbot for islamic banking and

finance. International Journal of Information Retrieval Research (IJIRR), 11(3), pp.65-77.

Kouvelis and et.al, 2018. Who should finance the supply chain? Impact of credit ratings on

supply chain decisions. Manufacturing & Service Operations Management, 20(1), pp.19-

35.

Li and et.al, 2020. Blockchain-enabled logistics finance execution platform for capital-

constrained E-commerce retail. Robotics and Computer-Integrated Manufacturing, 65,

p.101962.

Ma and et.al, 2019. Financial credit risk prediction in internet finance driven by machine

learning. Neural Computing and Applications, 31(12), pp.8359-8367.

Macchiavello and et.al, 2022. Sustainable Finance and Fintech: Can Technology Contribute to

Achieving Environmental Goals? A Preliminary Assessment of ‘Green Fintech’and

‘Sustainable Digital Finance’. European Company and Financial Law Review, 19(1),

pp.128-174.

Swamy and et.al, 2019. The dynamics of finance-growth nexus in advanced

economies. International Review of Economics & Finance, 64, pp.122-146.

Timperley, J., 2021. How to fix the broken promises of climate finance. Nature, pp.400-402.

Vasileiou, E., 2021. Behavioral finance and market efficiency in the time of the COVID-19

pandemic: does fear drive the market?. International Review of Applied Economics, 35(2),

pp.224-241.

Books and Journals

Amos and et.al, 2021. The mediating effects of finance on the performance of hospital facilities

management services. Journal of Building Engineering, 34, p.101899.

Burlacu and et.al, 2019. Impact of demography on the public finance of the European

Union. Quality-Access to Success, 20.

He, Q. and Li, X., 2021. The failure of Chinese peer-to-peer lending platforms: Finance and

politics. Journal of Corporate Finance, 66, p.101852.

Jung and et.al, 2020. Public finance responses to COVID-19 in Korea. National Tax

Journal, 73(3), pp.879-900.

Khan and et.al, 2021. Artificial intelligence and NLP-based chatbot for islamic banking and

finance. International Journal of Information Retrieval Research (IJIRR), 11(3), pp.65-77.

Kouvelis and et.al, 2018. Who should finance the supply chain? Impact of credit ratings on

supply chain decisions. Manufacturing & Service Operations Management, 20(1), pp.19-

35.

Li and et.al, 2020. Blockchain-enabled logistics finance execution platform for capital-

constrained E-commerce retail. Robotics and Computer-Integrated Manufacturing, 65,

p.101962.

Ma and et.al, 2019. Financial credit risk prediction in internet finance driven by machine

learning. Neural Computing and Applications, 31(12), pp.8359-8367.

Macchiavello and et.al, 2022. Sustainable Finance and Fintech: Can Technology Contribute to

Achieving Environmental Goals? A Preliminary Assessment of ‘Green Fintech’and

‘Sustainable Digital Finance’. European Company and Financial Law Review, 19(1),

pp.128-174.

Swamy and et.al, 2019. The dynamics of finance-growth nexus in advanced

economies. International Review of Economics & Finance, 64, pp.122-146.

Timperley, J., 2021. How to fix the broken promises of climate finance. Nature, pp.400-402.

Vasileiou, E., 2021. Behavioral finance and market efficiency in the time of the COVID-19

pandemic: does fear drive the market?. International Review of Applied Economics, 35(2),

pp.224-241.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.