Evaluating Financial Health: Cash Cycle, Risks, and Project Viability

VerifiedAdded on 2023/04/04

|6

|1140

|437

Report

AI Summary

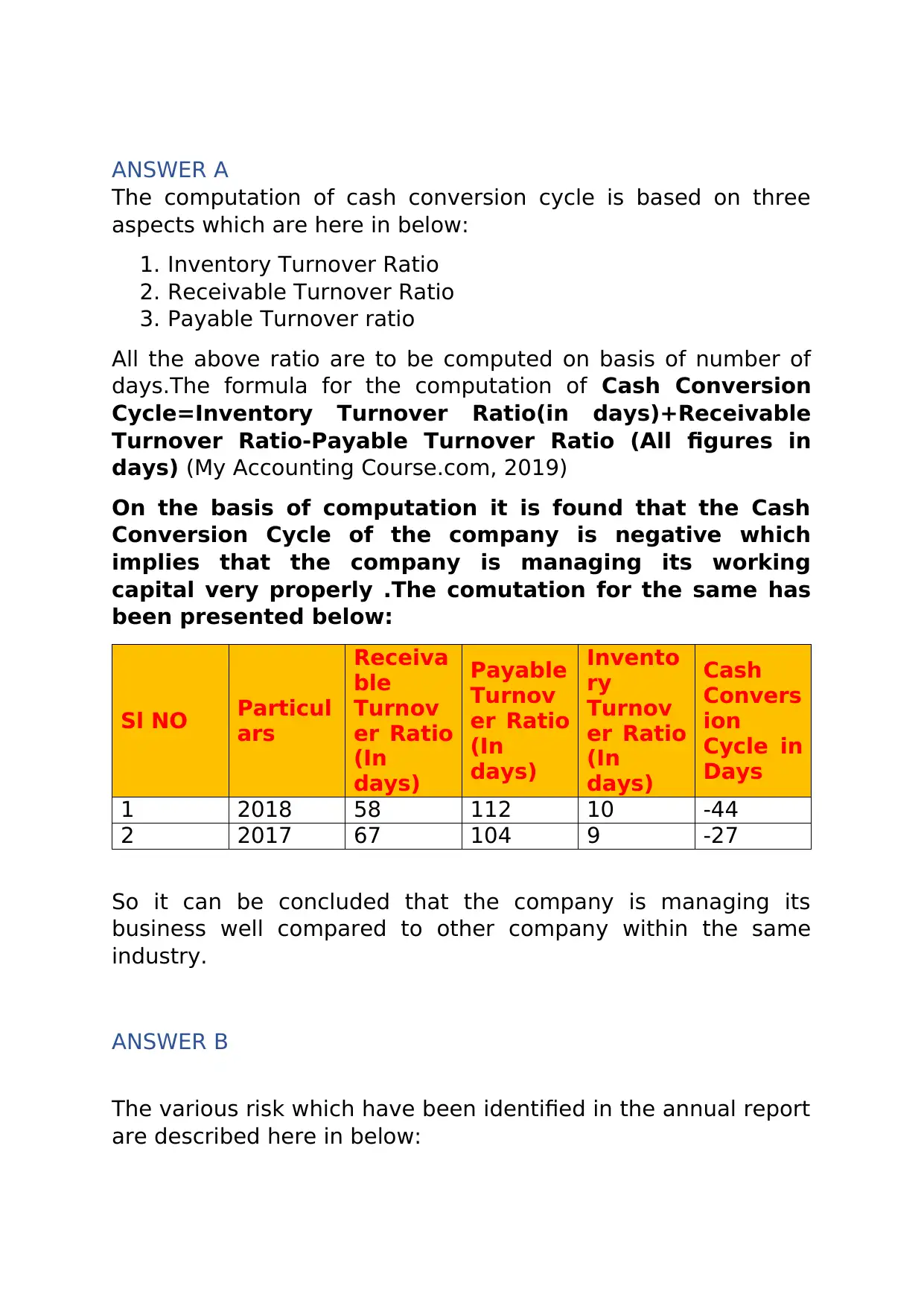

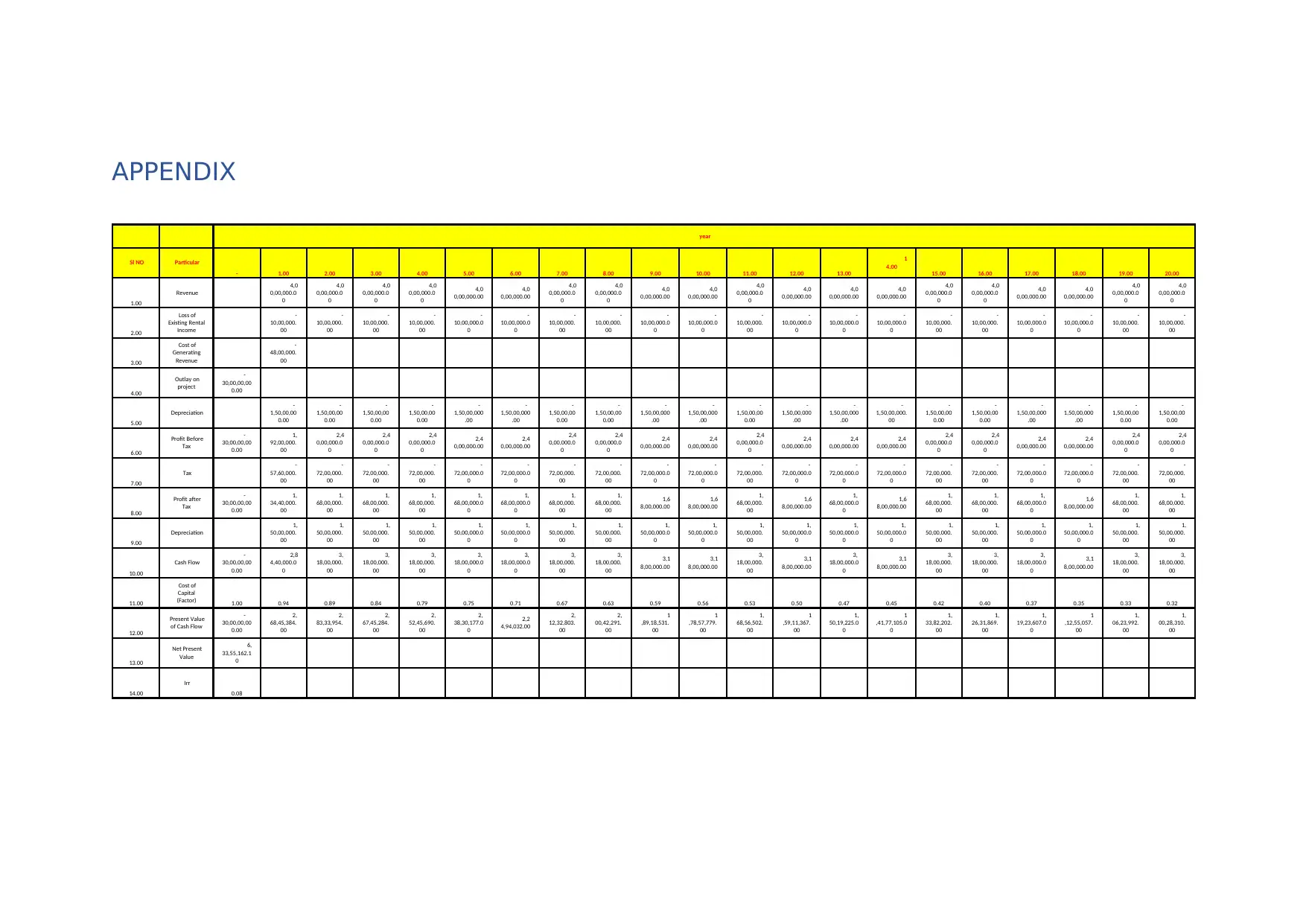

This report provides a financial analysis, beginning with an examination of the cash conversion cycle, revealing a negative cycle indicating efficient working capital management. It identifies systematic market risk, technological risk, supply chain risk, foreign exchange fluctuation risk, and interest rate risk. The analysis includes an assessment of a share's performance against market indices, noting an increase in company debt. Bond valuation calculations are performed with and without interest payments. Furthermore, the report evaluates a project using Net Present Value (NPV) analysis, concluding that the project should be undertaken based on its positive NPV and an Internal Rate of Return (IRR) of 8%, which exceeds the cost of capital. The free cash flow calculations supporting the NPV analysis are appended to the report. Desklib offers similar solved assignments and study tools for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.