FINANCE 5: Analysis of Toyota's Cash Conversion Cycle Report

VerifiedAdded on 2022/10/18

|7

|1230

|25

Report

AI Summary

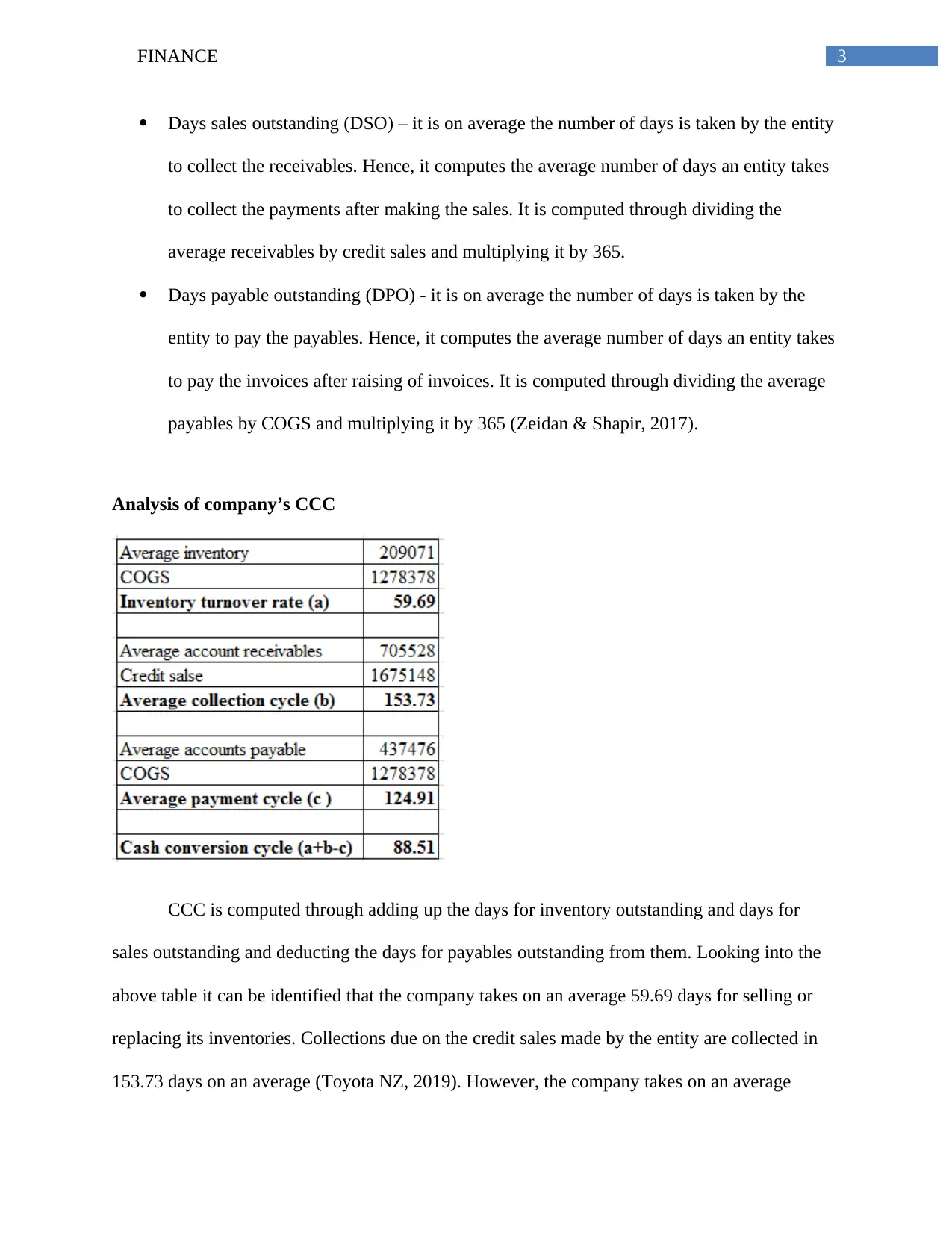

This report provides a comprehensive analysis of Toyota's cash conversion cycle (CCC). It begins by defining the importance and purpose of the CCC, which measures the time it takes for a company to convert its investments in inventory into cash. The report then details the three key components of the CCC: Days Inventory Outstanding (DIO), Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO). Using data from Toyota NZ (2019), the report calculates and analyzes Toyota's CCC, revealing that the company takes approximately 88.51 days to convert its working capital into cash. Several strategies are suggested to improve Toyota's CCC, including reducing inventory holding time, accelerating receivables collection, and optimizing payment terms with creditors. The report also emphasizes the significance of cash flow projections for new products, highlighting their role in assessing financial viability and ensuring adequate funds for covering costs. References from academic sources support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.