HI5020 Corporate Accounting: Analysis of Cash Flow Statements Report

VerifiedAdded on 2023/03/29

|23

|4524

|145

Report

AI Summary

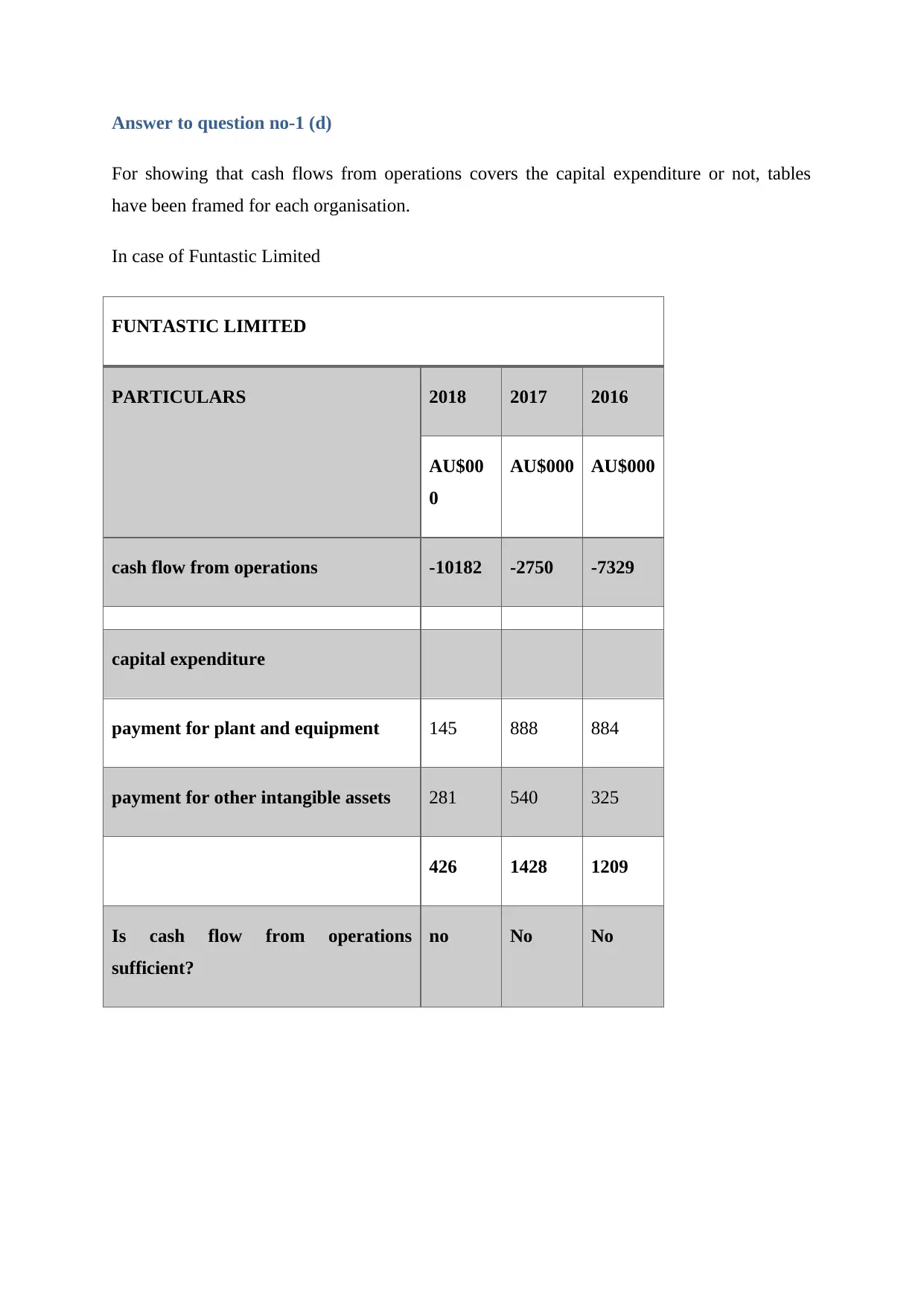

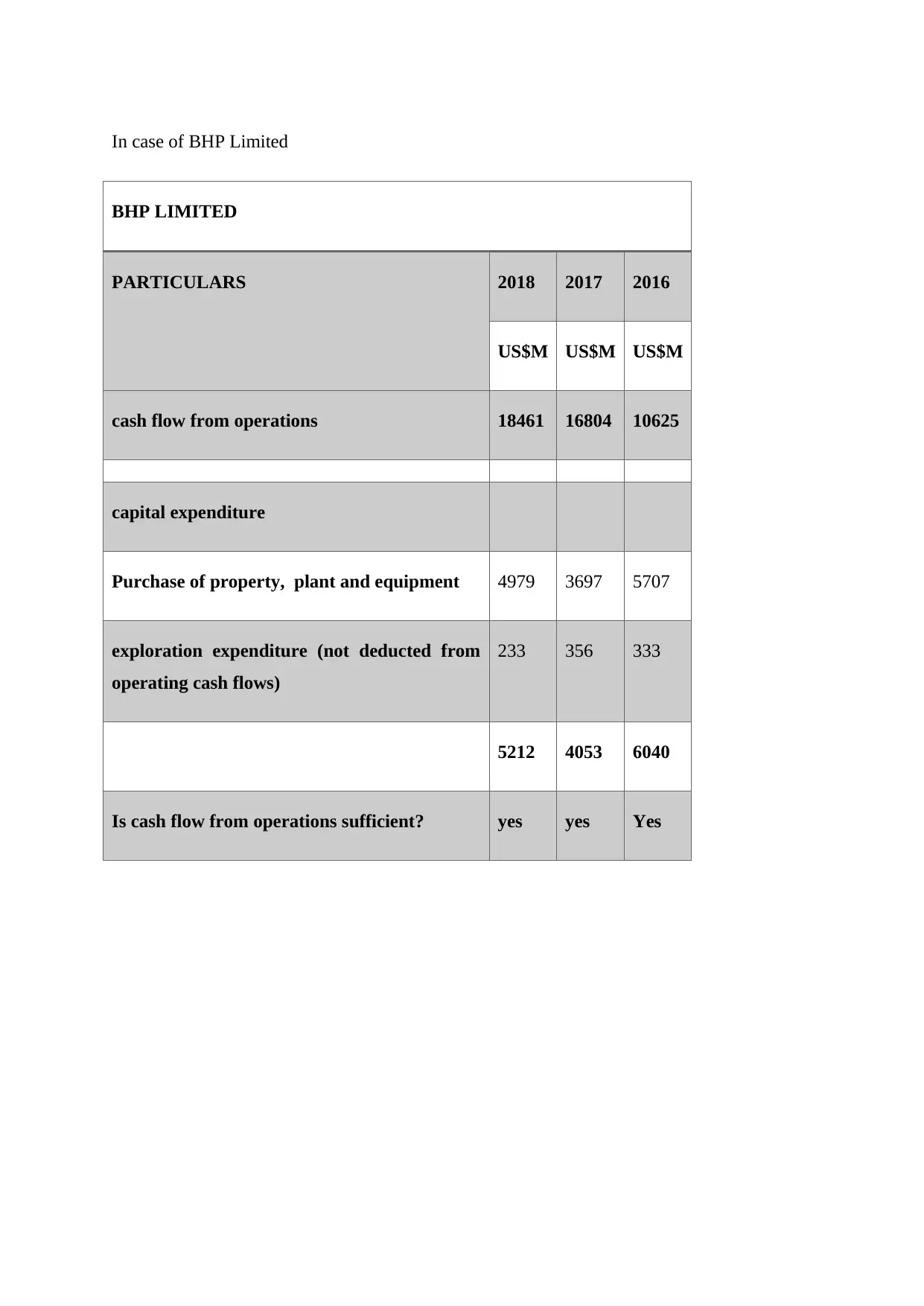

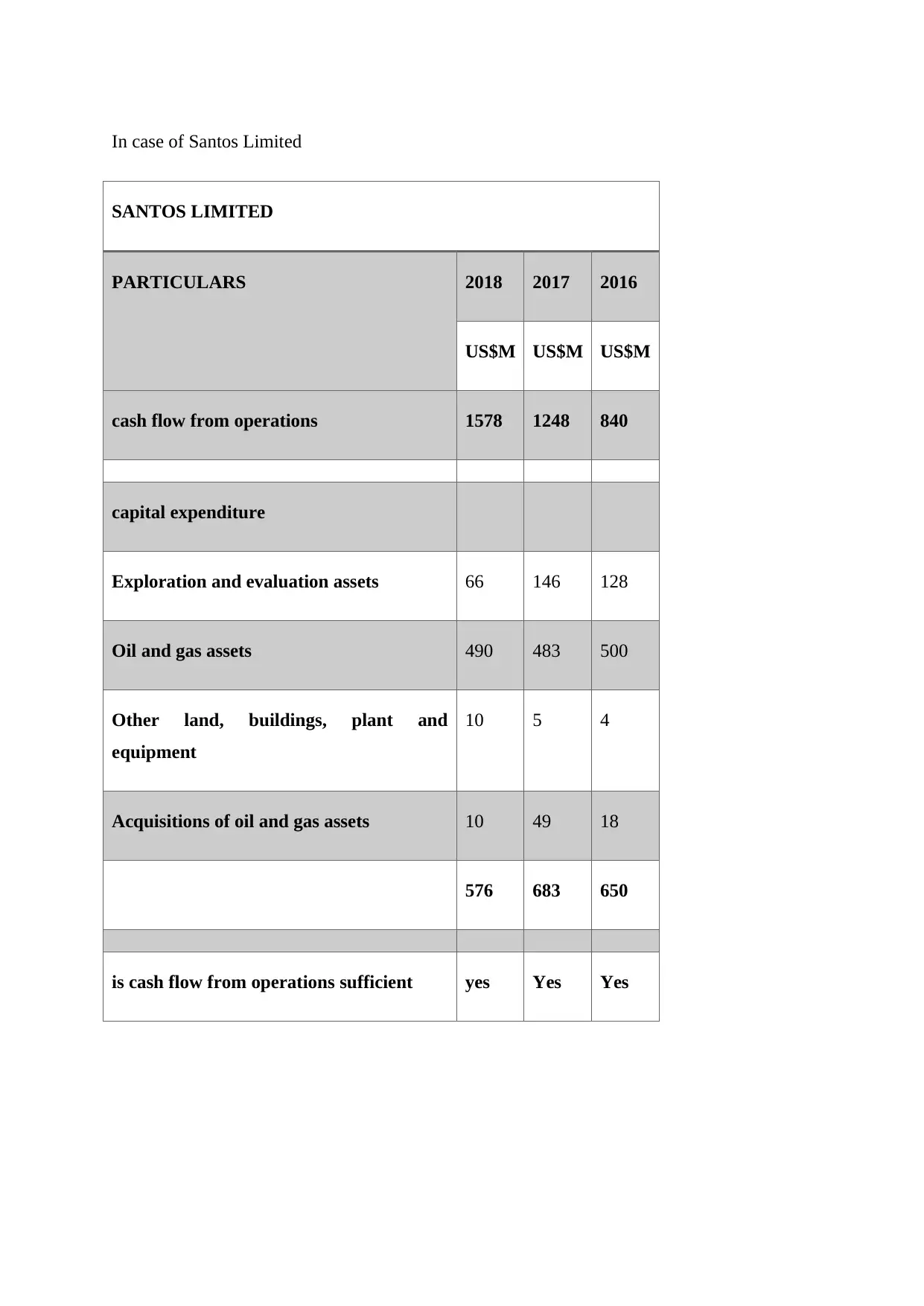

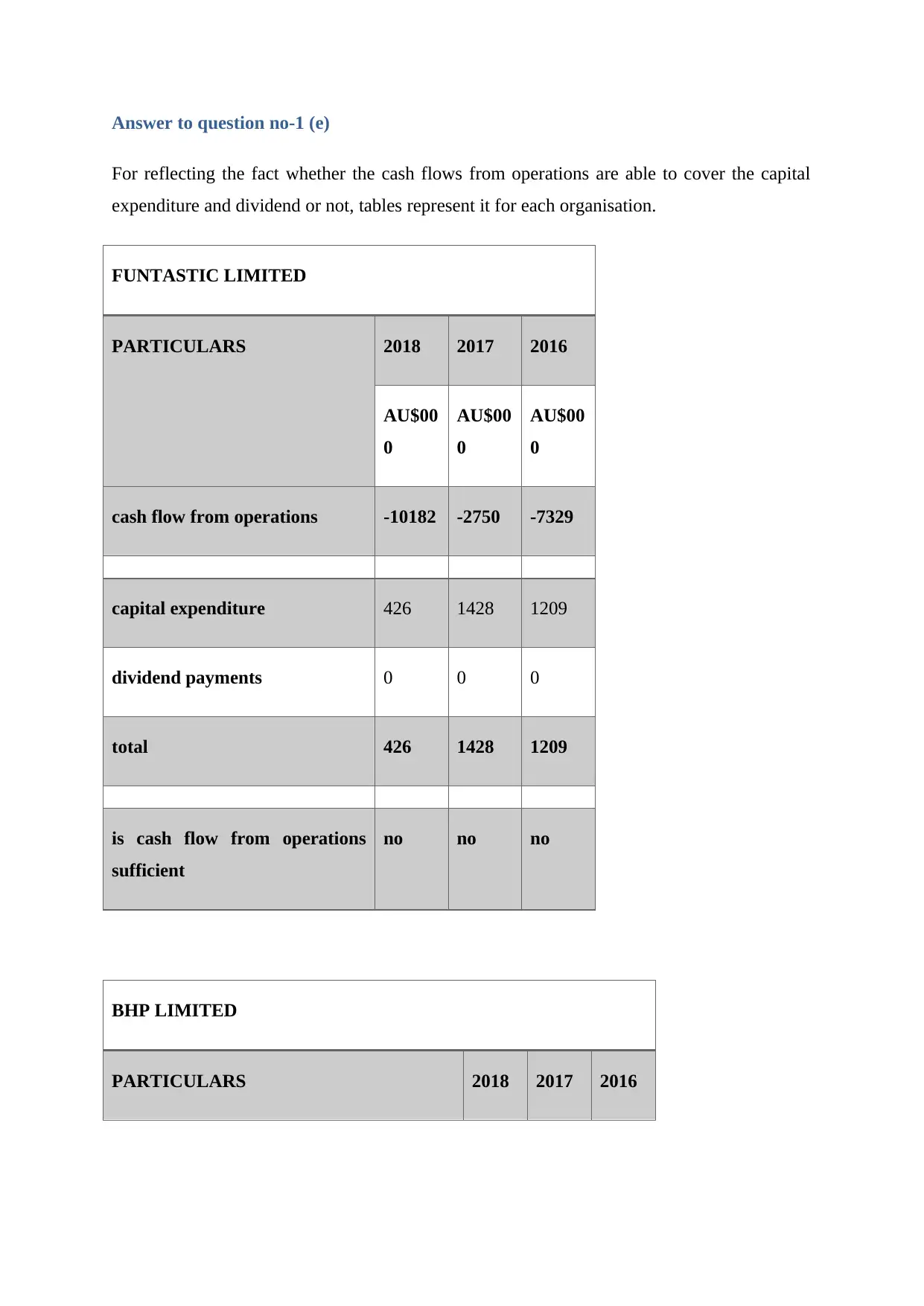

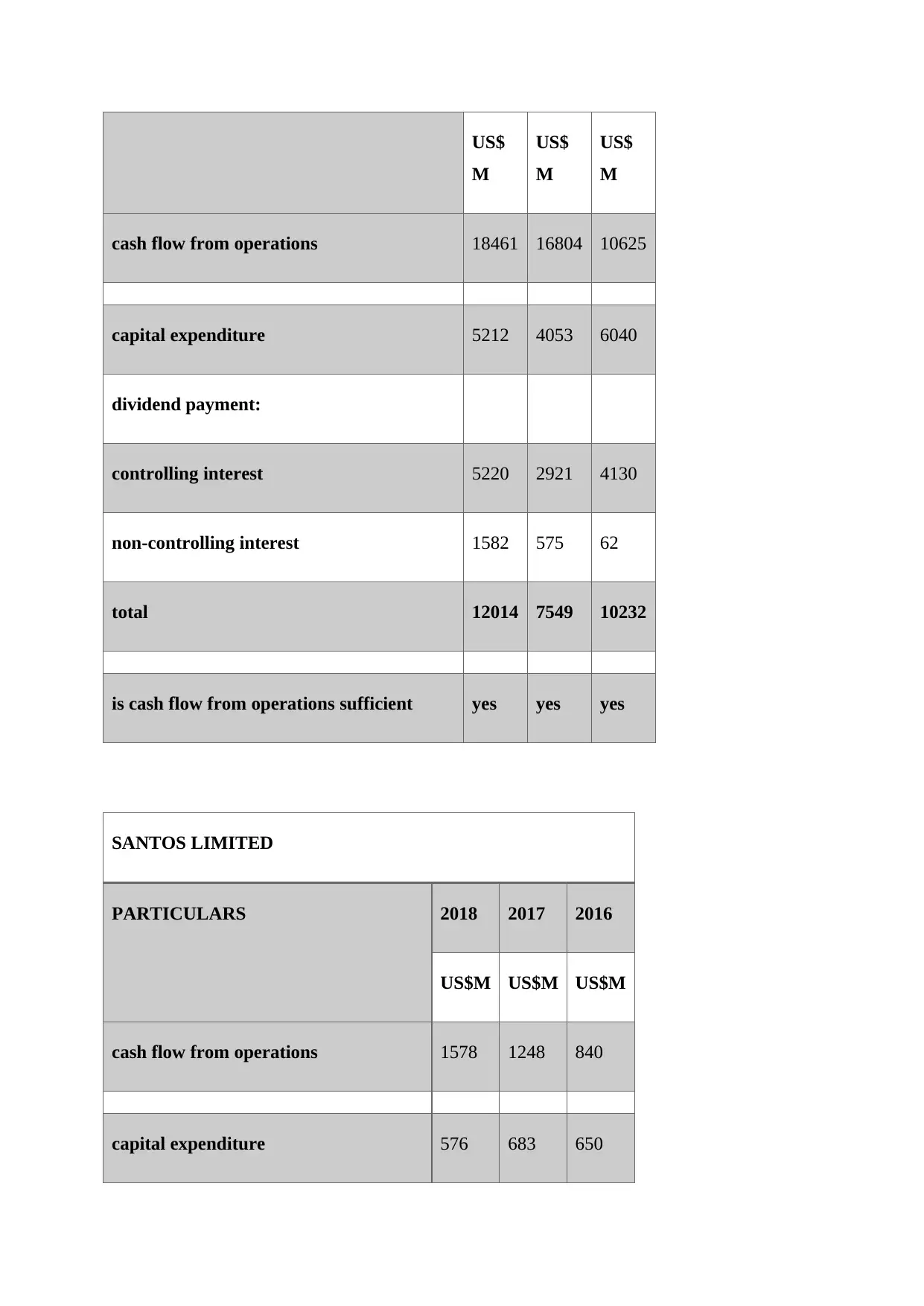

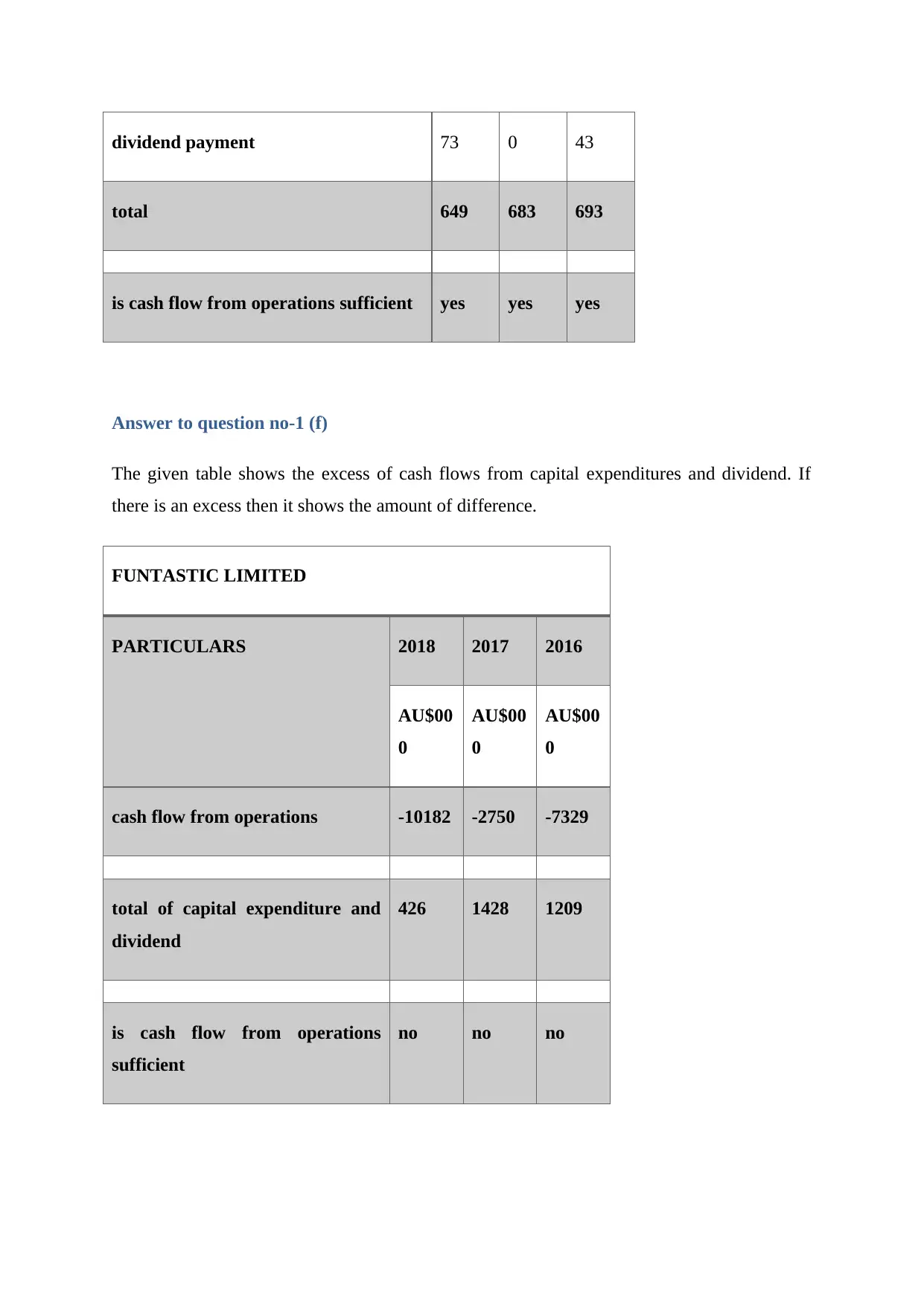

This report delves into the analysis of cash flow statements, focusing on the financial performance of companies and the importance of cash management. The report examines the usefulness of cash flow statements and income statements, highlighting how they reflect a company's financial health. It analyzes the cash inflows and outflows of three companies: Funtastic Limited, BHP Limited, and Santos Limited, assessing their operational cash flows, capital expenditures, and dividend payments. The report investigates whether cash flows from operations cover capital expenditure and dividends, and examines how working capital accounts are utilized. The analysis provides a detailed understanding of how companies generate and use cash, offering insights into their financial strategies and potential risks. The report also includes an abstract, introduction, table of contents, and conclusion, providing a structured overview of the findings and analysis. The report further provides answers to various questions related to cash flow statements, including the sources and uses of cash, trends in cash flows, and the sufficiency of cash flows to cover capital expenditures and dividends.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.