ACC00724: Accounting for Managers, S2 2018 - Assignment 2 Report

VerifiedAdded on 2023/06/08

|13

|2171

|438

Report

AI Summary

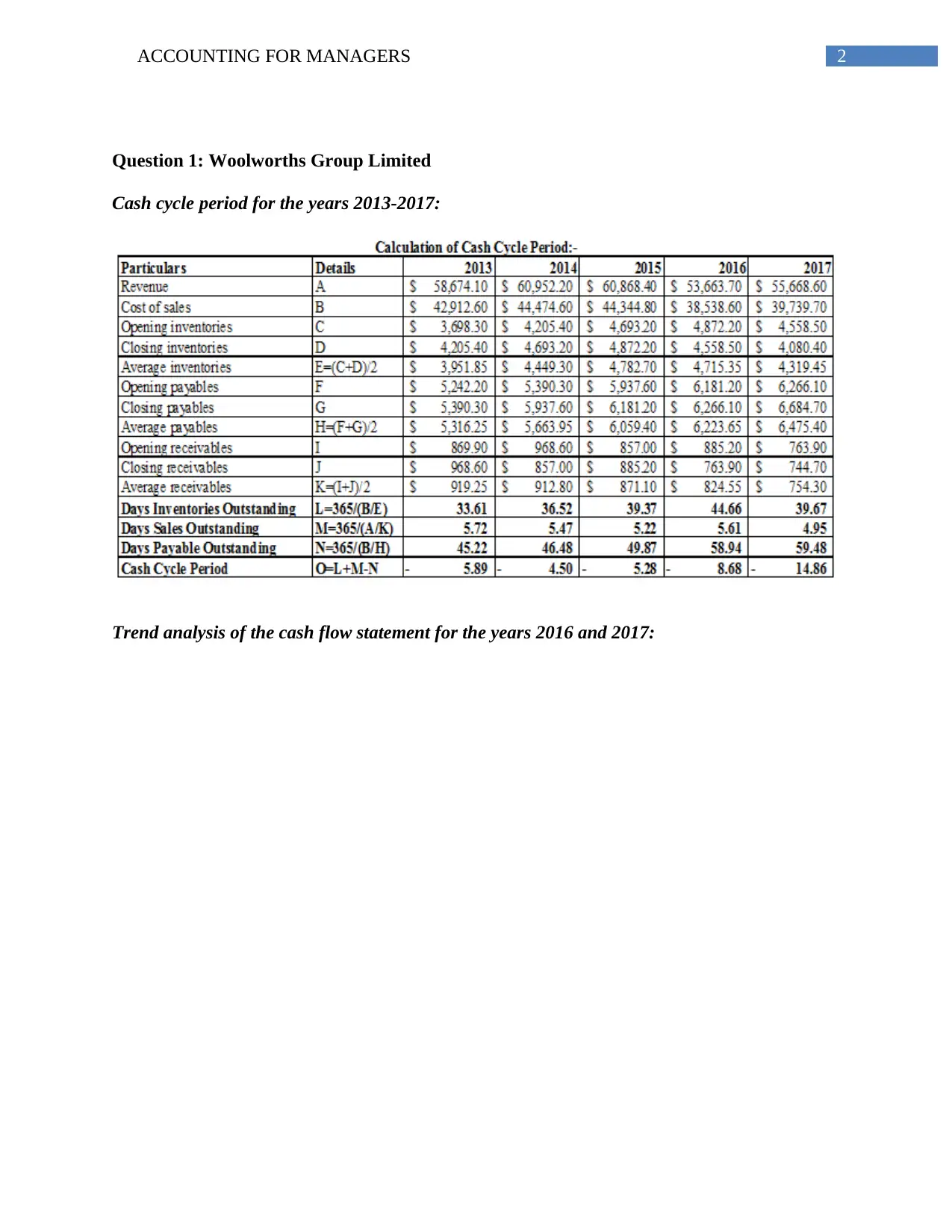

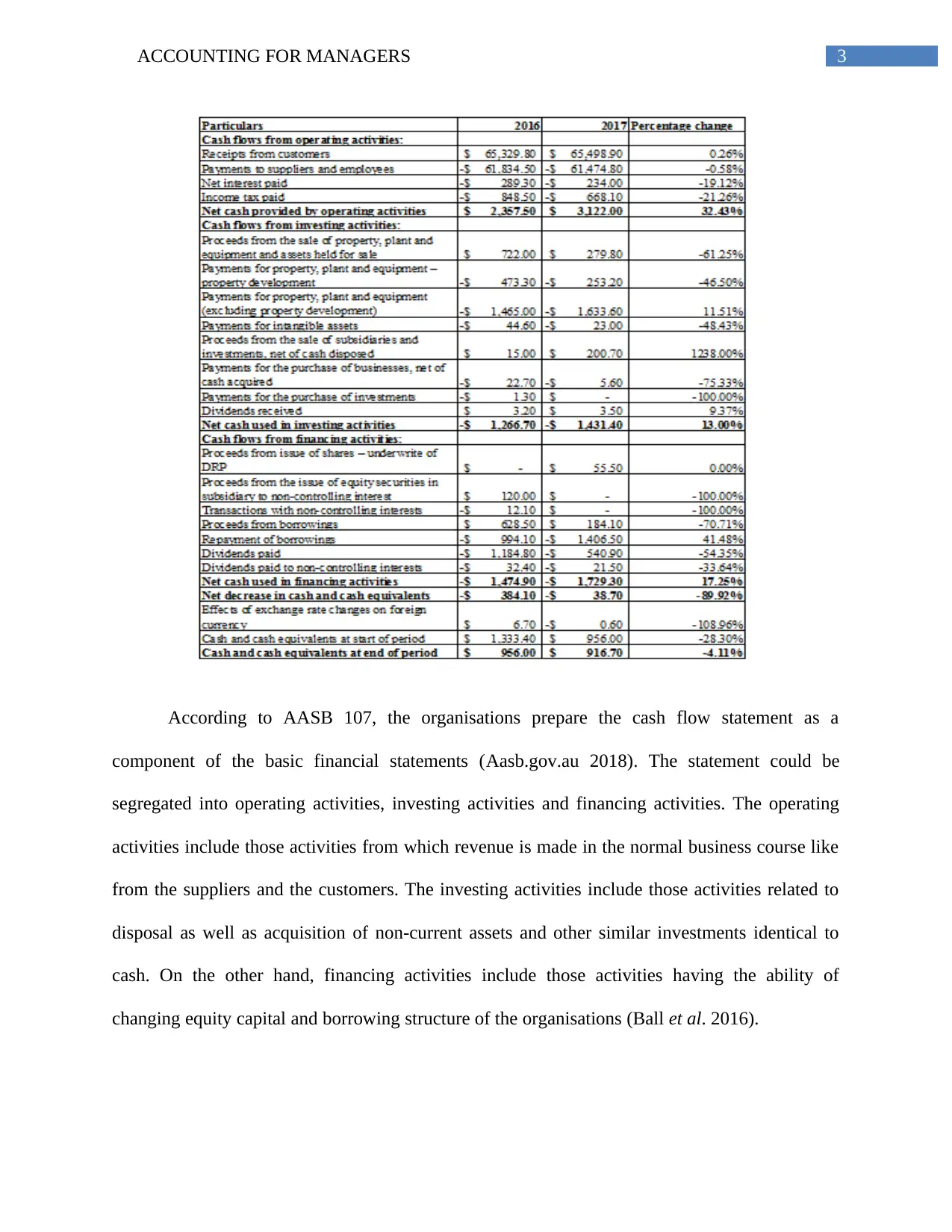

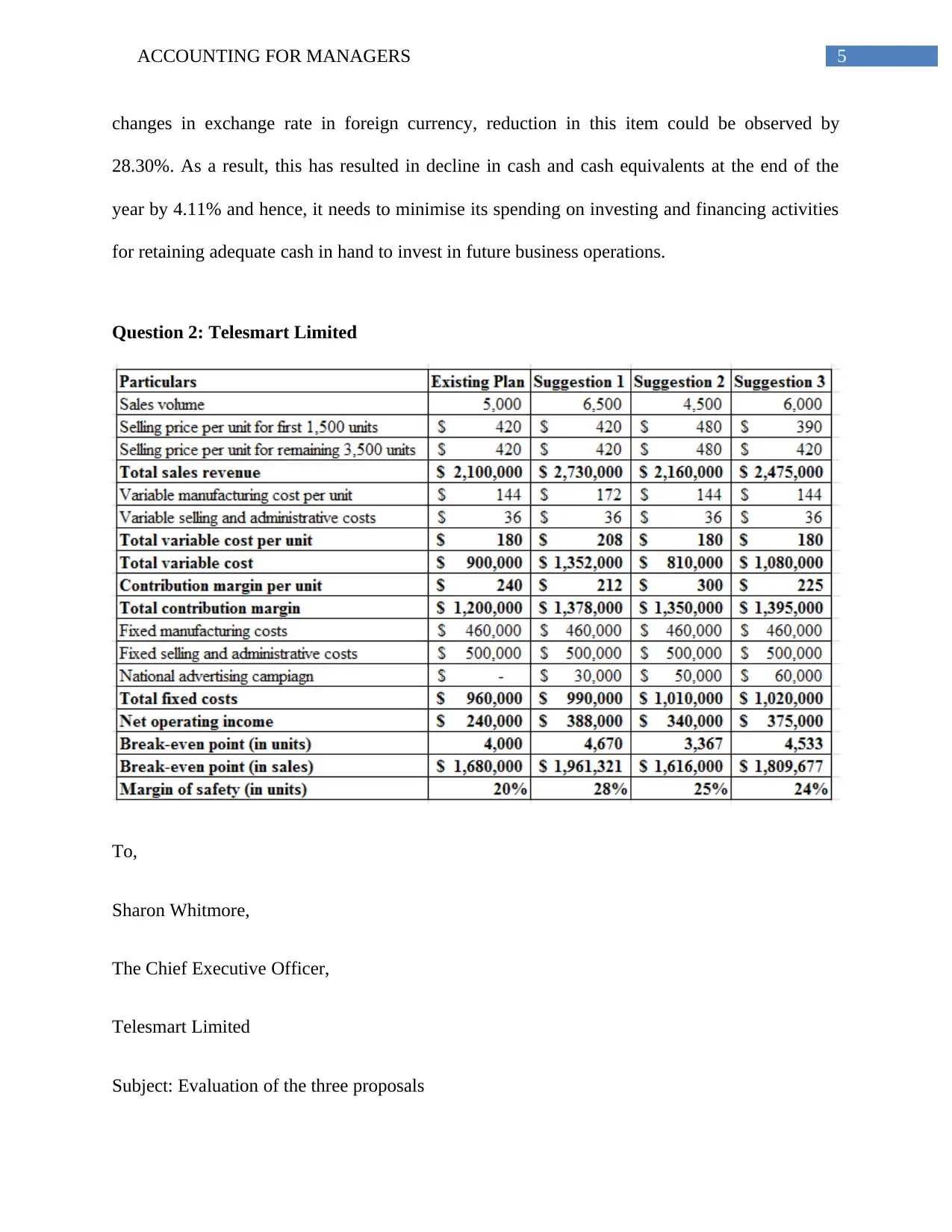

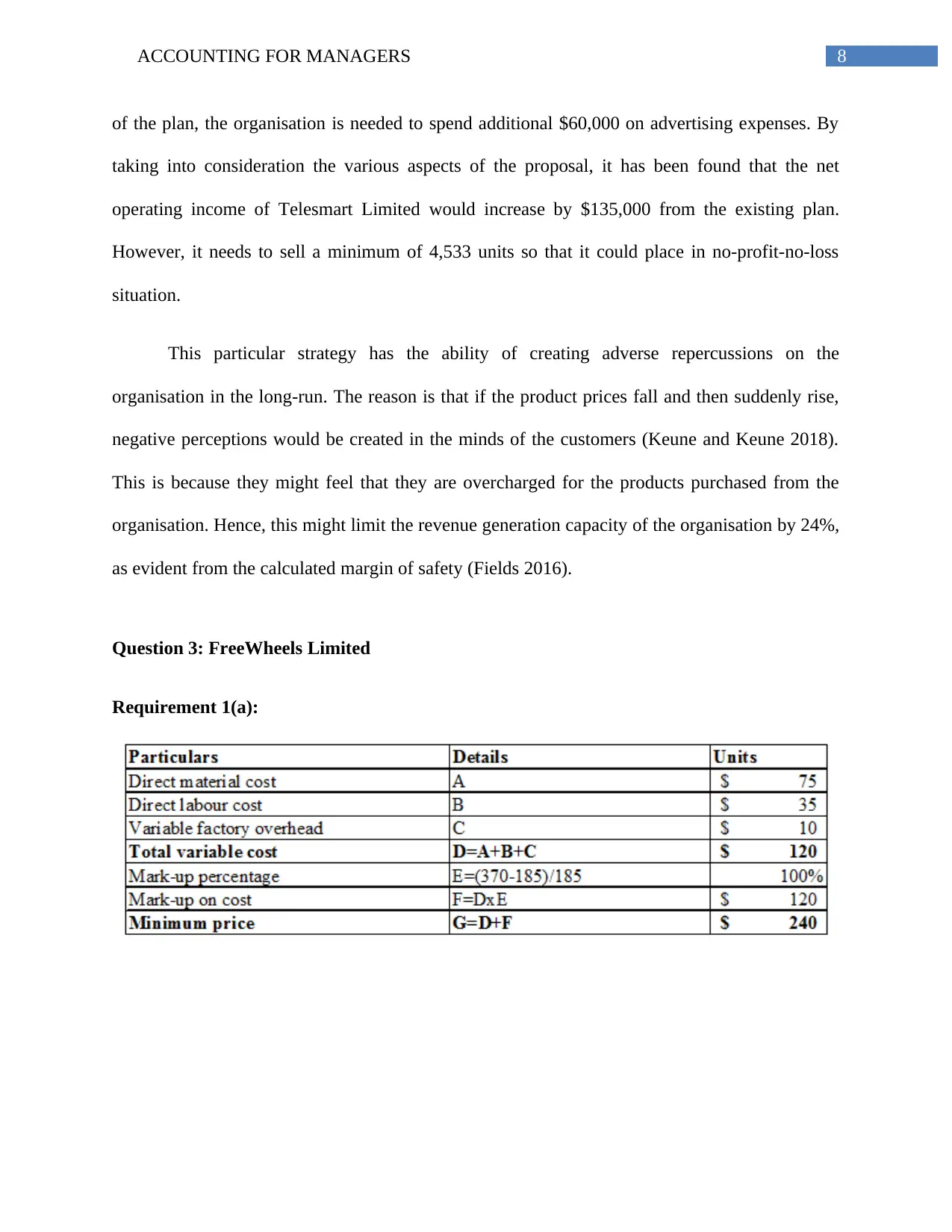

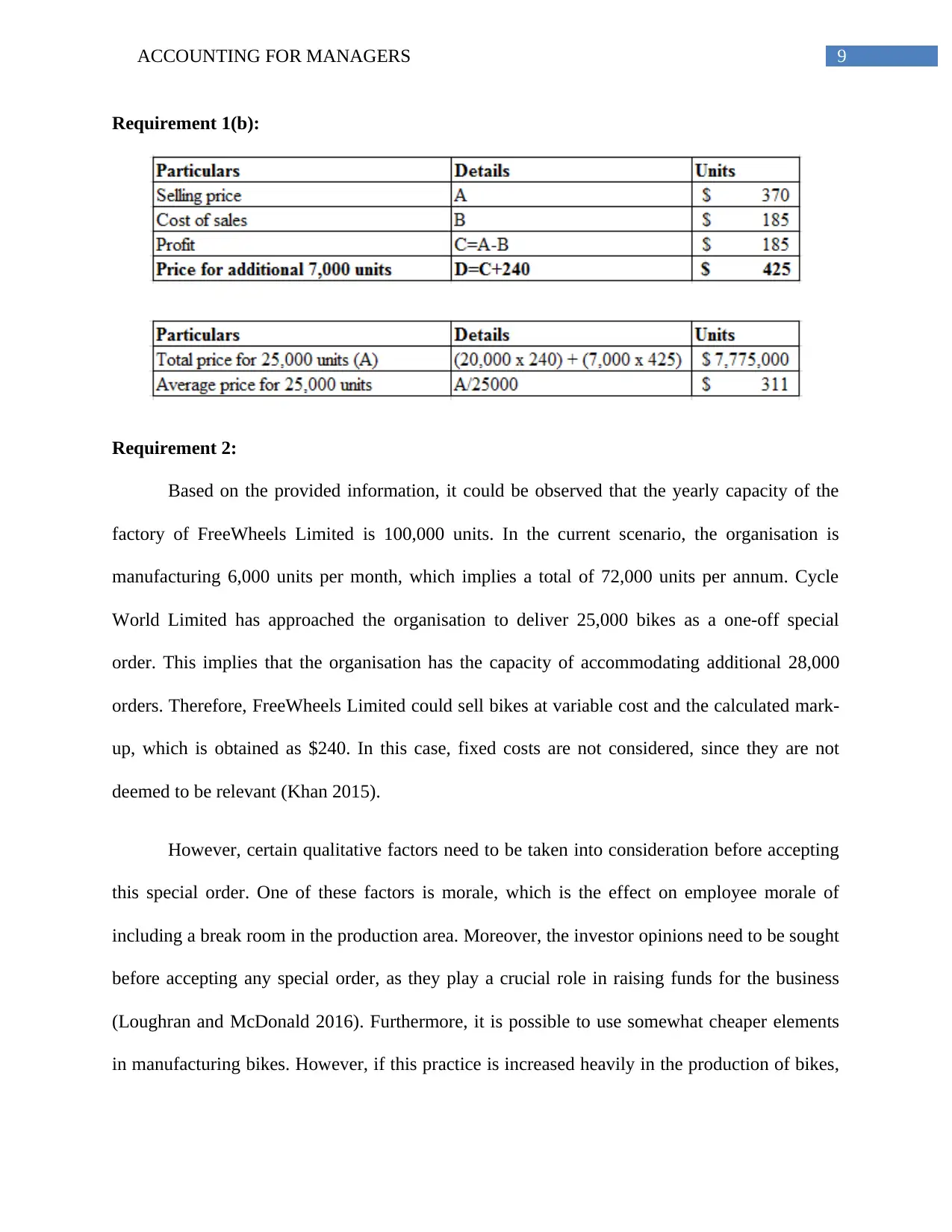

This report provides a comprehensive analysis of accounting principles and financial statements, focusing on three companies: Woolworths Group Limited, Telesmart Limited, and FreeWheels Limited. The first section calculates the cash cycle period for Woolworths from 2013 to 2017 and evaluates the trends in its cash flow statements for 2016 and 2017, highlighting operating, investing, and financing activities. The second section evaluates three proposals from Telesmart's managers to increase profitability, considering factors like sales volume, pricing, and advertising expenses. The third section analyzes FreeWheels Limited's manufacturing capacity and evaluates a special order from Cycle World Limited, considering variable costs, fixed costs, and qualitative factors such as employee morale and investor opinions. The report provides detailed financial data, calculations, and evaluations to support its conclusions, offering valuable insights into financial management and decision-making.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.