Financial Analysis: Cash Flow Statement of Two Australian Companies

VerifiedAdded on 2020/05/28

|7

|2081

|91

Report

AI Summary

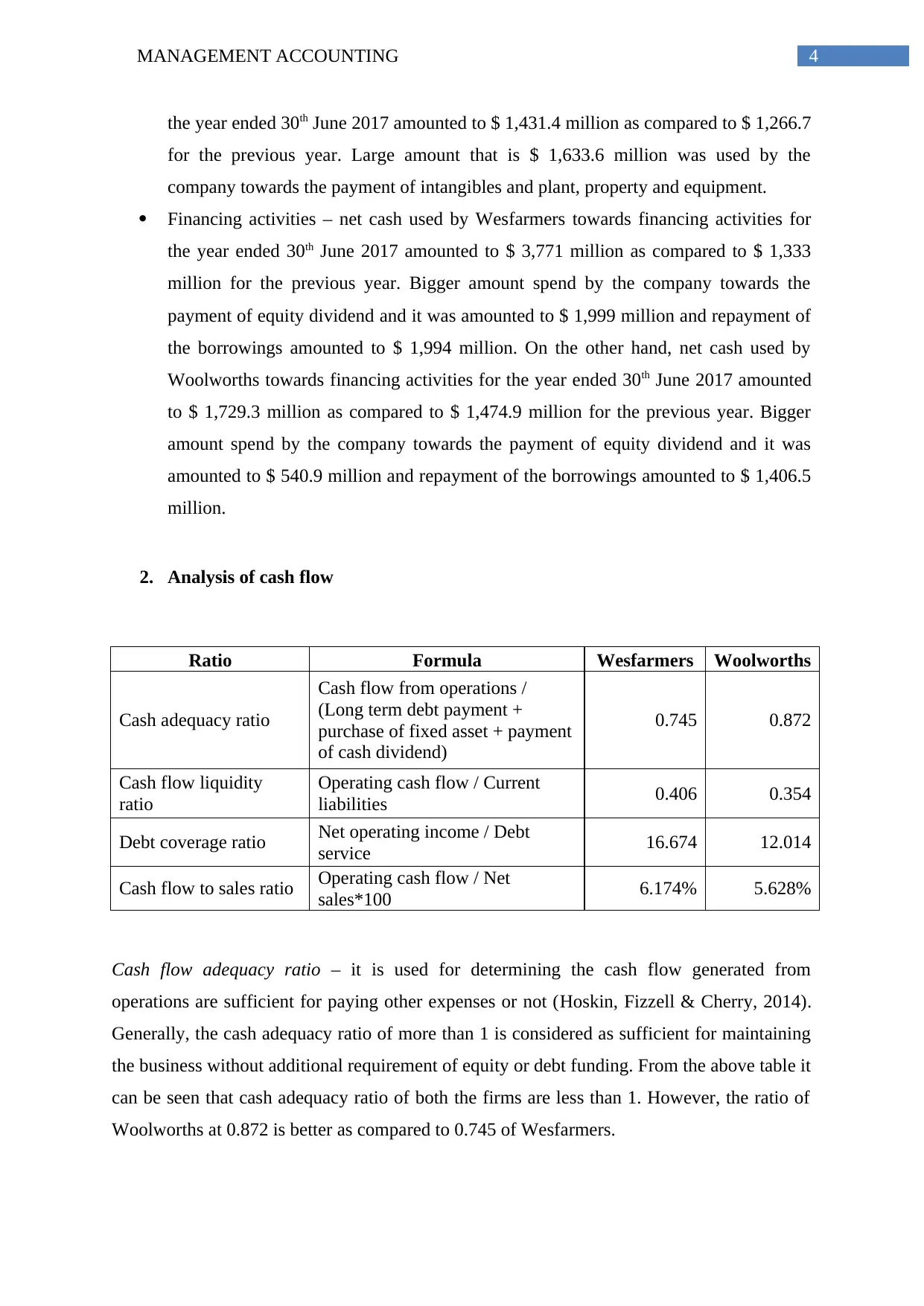

This report provides a comprehensive analysis of the cash flow statements of two major Australian companies, Wesfarmers and Woolworths. It begins by outlining the methods used in preparing cash flow statements, differentiating between the direct and indirect methods and explaining how cash flows are categorized into operating, investing, and financing activities. The report then delves into the specifics of each company's cash flow statements, detailing the cash flows from different activities for the year ended 30th June 2017. A comparative analysis of the two companies is presented, including key cash flow ratios such as cash adequacy ratio, cash flow liquidity ratio, debt coverage ratio, and cash flow to sales ratio. The analysis reveals insights into each company's financial health, liquidity, and solvency. The conclusion highlights Wesfarmers' stronger position in terms of debt coverage and ability to generate cash from sales, while recommending that Woolworths focus on minimizing operating expenses to improve its long-term sustainability. The report utilizes financial data and reconciliations to provide a clear understanding of each company's financial performance and offers valuable insights for financial analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.