Analyzing Cash Holding Determinants in UK Firms Post-Crisis

VerifiedAdded on 2023/03/29

|115

|24325

|188

Report

AI Summary

This report investigates the determinants of cash holding decisions among UK firms listed on the FTSE 350, focusing on the period after the 2008 financial crisis. It examines firm-specific variables over a twelve-year period (2004-2015), divided into three sub-periods: pre-crisis (2004-2006), during-crisis (2007-2009), and post-crisis (2010-2015). The study explores the theoretical underpinnings of cash holding, including the trade-off theory, pecking order theory, and free cash flow theory, as well as motives such as transaction, precautionary, tax, and agency considerations. The empirical analysis reveals a positive relationship between cash holding and net working capital, cash flow, and a negative relationship with leverage and firm size, with variations observed across the three sub-periods. The report concludes by highlighting the importance of understanding these determinants for effective corporate financial management.

The Determinants of Cash Holding In the UK after Financial

Crisis

1

Crisis

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract..................................................................................................3

1- Introduction........................................................................................4

Cash holding

theories…………………………………………………………………………....…..

…..….5

Cash holding motives……………………..

…………………………………………………...…………....7

Problem Statement...............................................................................22

Aims and Objectives.............................................................................18

Structure of the Paper...........................................................................27

2- Literature Review.............................................................................29

3- Methodology....................................................................................38

Sample Selection..................................................................................40

Variable Measurement..........................................................................41

4- Empirical Specification.....................................................................51

Descriptive statistics pre-crisis period (2004-2006).............................53

Regression pre-crisis period…………………………………………………….…..

………………..55

Descriptive statistics during-crisis period.............................................57

Regression during-crisis period............................................................60

Descriptive statistics after-crisis period................................................62

Regression after-crisis period...............................................................63

5- Cash holding overall

pattern………………………………………………………….…………….....66

2

1- Introduction........................................................................................4

Cash holding

theories…………………………………………………………………………....…..

…..….5

Cash holding motives……………………..

…………………………………………………...…………....7

Problem Statement...............................................................................22

Aims and Objectives.............................................................................18

Structure of the Paper...........................................................................27

2- Literature Review.............................................................................29

3- Methodology....................................................................................38

Sample Selection..................................................................................40

Variable Measurement..........................................................................41

4- Empirical Specification.....................................................................51

Descriptive statistics pre-crisis period (2004-2006).............................53

Regression pre-crisis period…………………………………………………….…..

………………..55

Descriptive statistics during-crisis period.............................................57

Regression during-crisis period............................................................60

Descriptive statistics after-crisis period................................................62

Regression after-crisis period...............................................................63

5- Cash holding overall

pattern………………………………………………………….…………….....66

2

6- Overall regression analysis………………………………………..

……………………………………67

7- Conclusion........................................................................................72

References………………………………………………………………………………

……………………….….76

Table of Figures

Table 1. Sample used in the

analysis……………………………………………..………………..….40

Table 2 prediction of the

correlation………………………………………………….………………51

Table3. Summary statistics of period 2004-2006……………….

……………………………….54

Table 4. Correlation matrix of period 2004-

2006………………………………………………..54

Table5. Estimation result of period 2004-2006……………………..

……………………………56

Table 6. Summary statistics of period 2007-

2009…………………………………...…………..57

3

……………………………………67

7- Conclusion........................................................................................72

References………………………………………………………………………………

……………………….….76

Table of Figures

Table 1. Sample used in the

analysis……………………………………………..………………..….40

Table 2 prediction of the

correlation………………………………………………….………………51

Table3. Summary statistics of period 2004-2006……………….

……………………………….54

Table 4. Correlation matrix of period 2004-

2006………………………………………………..54

Table5. Estimation result of period 2004-2006……………………..

……………………………56

Table 6. Summary statistics of period 2007-

2009…………………………………...…………..57

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table 7. Correlation matrix of period 2007-

2009………………………………………………..59

Table 8. Estimation results for period 2007-2009…………………………..

…………………..60

Table 9. Summary statistics of period 2010-

2015…………………………………………...…..62

Table 10. Correlation matrix of period 2010-

2015…………………………………………..…63

Table 11. Estimation results for period 2010-

2015…………………………………………….64

Table 12. Cash holding

overall…………………………………………………………………..………66

Appendix 1: DataStream variables

code………………………………………………………..……87

4

2009………………………………………………..59

Table 8. Estimation results for period 2007-2009…………………………..

…………………..60

Table 9. Summary statistics of period 2010-

2015…………………………………………...…..62

Table 10. Correlation matrix of period 2010-

2015…………………………………………..…63

Table 11. Estimation results for period 2010-

2015…………………………………………….64

Table 12. Cash holding

overall…………………………………………………………………..………66

Appendix 1: DataStream variables

code………………………………………………………..……87

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The determinants of corporate Cash holding in the UK after

financial crisis

Abstract

Cash holding decision is one of the major choices taken by the

management of the company. The decision not only depends on

academic vision but also the firm' s role in the market and sensitivity to

macro variables. This study aims to determine what variables play

major role in taking cash holding decision by firm. For case purpose we

have considered firms from UK that are listed in FTSE 350. The data set

contains twelve years (2004-2015) data of firm specific variables.

The study time period was divided into three sub periods -before crisis

from 2004 to 2006, the second period is the period from 2007 to2009

and post-crisis period is 2010 -2015. Macroeconomic variables have

not discussed here. The results show there is a positive and significant

relationship between cash holding and net working capital, cash flow

and a negative relationship with leverage and size. The determinants

have different relationships during the three sup-periods.

Keywords: Cash Holdings, Liquidity, Capital structure theories, Firm-

specific variables, Motives

1- Introduction

Liquid assets holding become the prior requirement of UK companies after the

5

financial crisis

Abstract

Cash holding decision is one of the major choices taken by the

management of the company. The decision not only depends on

academic vision but also the firm' s role in the market and sensitivity to

macro variables. This study aims to determine what variables play

major role in taking cash holding decision by firm. For case purpose we

have considered firms from UK that are listed in FTSE 350. The data set

contains twelve years (2004-2015) data of firm specific variables.

The study time period was divided into three sub periods -before crisis

from 2004 to 2006, the second period is the period from 2007 to2009

and post-crisis period is 2010 -2015. Macroeconomic variables have

not discussed here. The results show there is a positive and significant

relationship between cash holding and net working capital, cash flow

and a negative relationship with leverage and size. The determinants

have different relationships during the three sup-periods.

Keywords: Cash Holdings, Liquidity, Capital structure theories, Firm-

specific variables, Motives

1- Introduction

Liquid assets holding become the prior requirement of UK companies after the

5

period of financial crisis. Moreover, due to the financial crisis in the period of 2008

several companies were forced to shut down their business operations and functions. On

the other side, other companies that survived during this period are facing difficulty in

obtaining funds because external financing becomes more expensive. In reference to all

such aspects it becomes vital for the firms to enhance their cash holdings which in turn

helps them in coping up with the liquidity crunch. Hence, after the period of financial

crisis, UK firms tend to make more focus on employing conservative financing and low

investment policy. Further, there are mainly three theories that are highly associated with

the determinants of cash holdings namely trade off, pecking order and agency.

From assessment, it has been identified that real GDP growth declined from 3.6%

to 1.3% respectively. Condition of financial crisis has placed high level of impact on the

economic growth as well as development of the companies. With the motive to cope up

with such situation UK business units started to employ the strategy of cash holding.

Further, tables and graphs depicted below clearly shows that cash holding of companies

including both financial and non-financial increased significantly. The main motives of

UK firms behind such increasing holding include the aspects like transaction,

precautionary, tax and agency. Thus, the present dissertation will provide deeper insight

about the determinants of cash holdings considered by UK firms after the period of

financial crisis 2007-2008.

6

several companies were forced to shut down their business operations and functions. On

the other side, other companies that survived during this period are facing difficulty in

obtaining funds because external financing becomes more expensive. In reference to all

such aspects it becomes vital for the firms to enhance their cash holdings which in turn

helps them in coping up with the liquidity crunch. Hence, after the period of financial

crisis, UK firms tend to make more focus on employing conservative financing and low

investment policy. Further, there are mainly three theories that are highly associated with

the determinants of cash holdings namely trade off, pecking order and agency.

From assessment, it has been identified that real GDP growth declined from 3.6%

to 1.3% respectively. Condition of financial crisis has placed high level of impact on the

economic growth as well as development of the companies. With the motive to cope up

with such situation UK business units started to employ the strategy of cash holding.

Further, tables and graphs depicted below clearly shows that cash holding of companies

including both financial and non-financial increased significantly. The main motives of

UK firms behind such increasing holding include the aspects like transaction,

precautionary, tax and agency. Thus, the present dissertation will provide deeper insight

about the determinants of cash holdings considered by UK firms after the period of

financial crisis 2007-2008.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

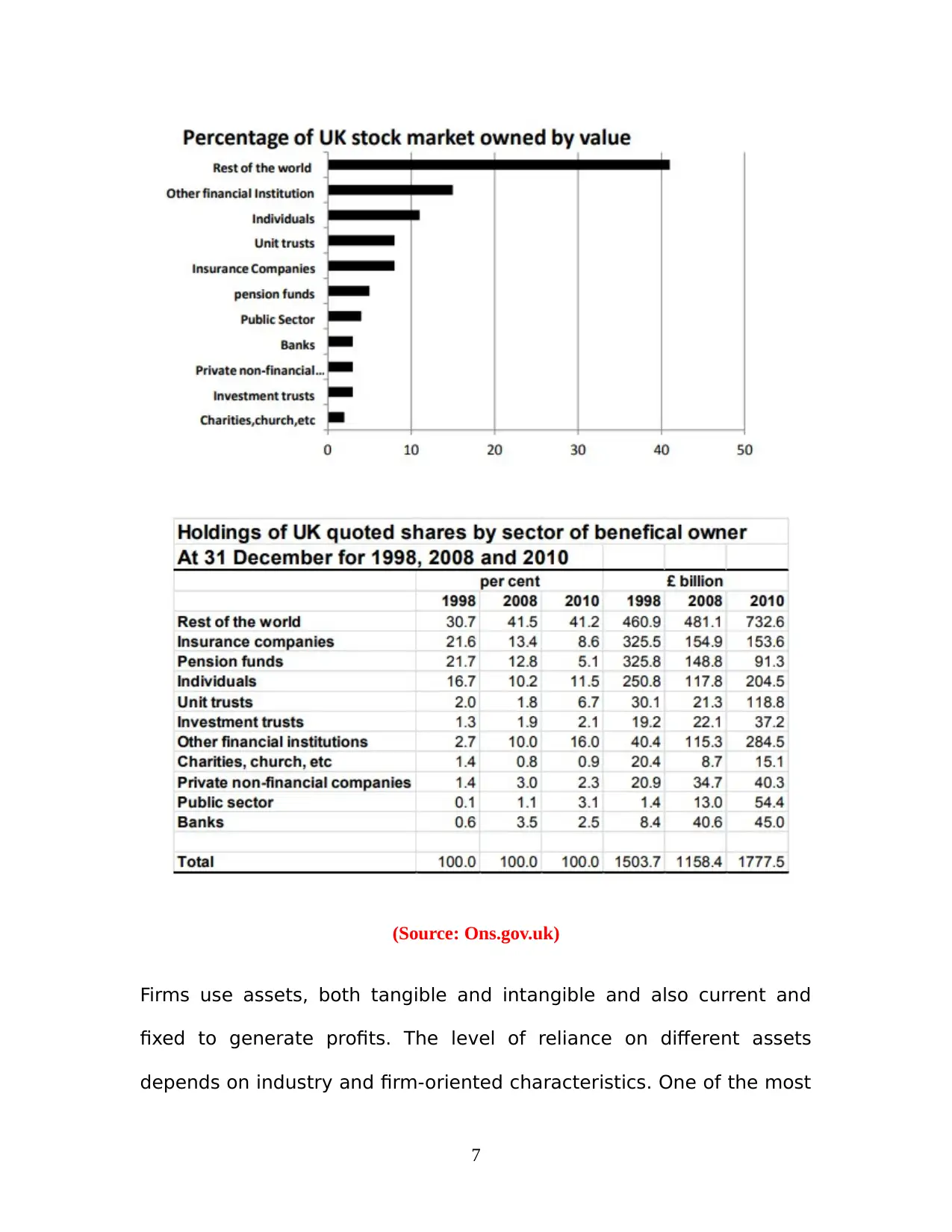

(Source: Ons.gov.uk)

Firms use assets, both tangible and intangible and also current and

fixed to generate profits. The level of reliance on different assets

depends on industry and firm-oriented characteristics. One of the most

7

Firms use assets, both tangible and intangible and also current and

fixed to generate profits. The level of reliance on different assets

depends on industry and firm-oriented characteristics. One of the most

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

controversial issues related to management of assets is the optimal

amount of cash that a firm should hold at any point in time. Cash and

cash equivalents are integral in the ability of a firm to meet its

obligations.There are many definitions for cash holding. According to

Gill and Shah (2012) cash holding is “cash in hand or readily available

for investment in physical assets and to distribute to investors.

According to Peicuti (2014), in addition to the obligations, there are

emergent opportunities in the market that are only available in the

short-run. In some instances, these cash and cash equivalents are

utilised in exploiting opportunities that originate from changes in the

market dynamics, such as investment in physical assets, distribution in

the form of dividends (Gill and Shah, 2011). Cash reserves provide a

valuable source of funds that is used to exploit investment

opportunities (Opler, 1999 and Bates et al., 2009) under two scenarios.

First, when current internally generated cash flows are low or volatile

are insufficient; such resources are deployed towards the most

necessary destinations as indicated by Denis and Sibilkov, (2010). In

this accord, the cash holdings hedge against the financial shocks from

changes in economic projections (Chen and Chang, 2012), and serve

as a tool for solving the challenges facing firms in the form of

unfulfilled expectations (Sufi, 2009). Secondly, the available cash can

be used in mergers and acquisitions. For instance, Harford (1999)

8

amount of cash that a firm should hold at any point in time. Cash and

cash equivalents are integral in the ability of a firm to meet its

obligations.There are many definitions for cash holding. According to

Gill and Shah (2012) cash holding is “cash in hand or readily available

for investment in physical assets and to distribute to investors.

According to Peicuti (2014), in addition to the obligations, there are

emergent opportunities in the market that are only available in the

short-run. In some instances, these cash and cash equivalents are

utilised in exploiting opportunities that originate from changes in the

market dynamics, such as investment in physical assets, distribution in

the form of dividends (Gill and Shah, 2011). Cash reserves provide a

valuable source of funds that is used to exploit investment

opportunities (Opler, 1999 and Bates et al., 2009) under two scenarios.

First, when current internally generated cash flows are low or volatile

are insufficient; such resources are deployed towards the most

necessary destinations as indicated by Denis and Sibilkov, (2010). In

this accord, the cash holdings hedge against the financial shocks from

changes in economic projections (Chen and Chang, 2012), and serve

as a tool for solving the challenges facing firms in the form of

unfulfilled expectations (Sufi, 2009). Secondly, the available cash can

be used in mergers and acquisitions. For instance, Harford (1999)

8

found that rich-cash US’s firms are more likely to attempt acquisition

than less cash holding firms.

The global financial crisis in 2008 had a significant impact on the world

economy and thus the corporations severely effected which let many

of them out of the markets or made poor profits. The crisis created a

shock to the supply of credit to all firms (Gorton, 2010). Due to this

crisis, institutions have bee heavily deleveraged complying with the

new financial regulations. Since then corporations around the world

have paid profound attention on cash holding’sdecision. According to

Capita Asset Services (2014): the total net cash of FTSE100 reached to

53.5bn in 2013.(http://www.capitaassetservices.com/).

We assume that the recent financial crisis has influenced firm’s

manager to be more cautions about the amount of cash on their hands

and raised their awareness about be prepared for any potential

financial crisis and thus the difficulties to obtain external funds.

According to this assumption we predict to have higher cash holding

ration in both periods duringand post financial crisis compared to pre

financial crisis.

For all above, the cash holding appear to be an essential factor to be

understood.

Theoretical Consideration:

9

than less cash holding firms.

The global financial crisis in 2008 had a significant impact on the world

economy and thus the corporations severely effected which let many

of them out of the markets or made poor profits. The crisis created a

shock to the supply of credit to all firms (Gorton, 2010). Due to this

crisis, institutions have bee heavily deleveraged complying with the

new financial regulations. Since then corporations around the world

have paid profound attention on cash holding’sdecision. According to

Capita Asset Services (2014): the total net cash of FTSE100 reached to

53.5bn in 2013.(http://www.capitaassetservices.com/).

We assume that the recent financial crisis has influenced firm’s

manager to be more cautions about the amount of cash on their hands

and raised their awareness about be prepared for any potential

financial crisis and thus the difficulties to obtain external funds.

According to this assumption we predict to have higher cash holding

ration in both periods duringand post financial crisis compared to pre

financial crisis.

For all above, the cash holding appear to be an essential factor to be

understood.

Theoretical Consideration:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash in the balance sheet is the important part in the assets. In the

theoretical point and based on past studies, there are 3 types of

theoretical models: the trade-off theory, the pecking order theory, cash

flow theory.

Trade-off theory

Trade-off theory based on the sample assumption: there is an optimum

level of cash. This value calculated based on the trade off between the

marginal benefits and costs of holding liquid assets. The aim is to

maximise the firm’s value by maximise the shareholder’s wealth. The

costs of holding cash represent on the opportunity cost of idle capital

and agency costs, whereas the benefits include avoiding transaction

costa to borrow, alleviating agency costs arising from external funds

and asymmetry information (Opler, 1999).

According to Kensy (1936) there are two motives of holding cash

precautionary motive and transaction minimization. In relation to the

former, it argues that firms hold cash due to the effect of asymmetric

information when comes to raise funds. This suggests that firms are

more reluctant to raise funds from capital markets either because of

their excessively cost (Myers and Majluf, 1984). or due to varies issues

related to the markets (Al-Najjar, 2013). The transaction minimization

motive suggests that firms stockpile cash when the raising-costs and

the opportunity-costs (due to cash deficits)are high(Dittmar et al.,

10

theoretical point and based on past studies, there are 3 types of

theoretical models: the trade-off theory, the pecking order theory, cash

flow theory.

Trade-off theory

Trade-off theory based on the sample assumption: there is an optimum

level of cash. This value calculated based on the trade off between the

marginal benefits and costs of holding liquid assets. The aim is to

maximise the firm’s value by maximise the shareholder’s wealth. The

costs of holding cash represent on the opportunity cost of idle capital

and agency costs, whereas the benefits include avoiding transaction

costa to borrow, alleviating agency costs arising from external funds

and asymmetry information (Opler, 1999).

According to Kensy (1936) there are two motives of holding cash

precautionary motive and transaction minimization. In relation to the

former, it argues that firms hold cash due to the effect of asymmetric

information when comes to raise funds. This suggests that firms are

more reluctant to raise funds from capital markets either because of

their excessively cost (Myers and Majluf, 1984). or due to varies issues

related to the markets (Al-Najjar, 2013). The transaction minimization

motive suggests that firms stockpile cash when the raising-costs and

the opportunity-costs (due to cash deficits)are high(Dittmar et al.,

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2003;Miller&Orr, 1966;Tobin 1956) and to avoid liquidate assets to

make payments (Ferreiraand Vilela (2004). Opler’s (1999) model shows

the optimal level of holding cash to be where the marginal cost of

holding liquid assets equals to the marginal cost of liquid assets

shortage. The study has shown that there is a simple trade off

managing between higher cash and lower debt in the firm. Moreover,

the correlation between cash flow and future investment opportunities

is low.

Packing order theory

This theory argues that there is nooptimal level of cash holdings for a

firm. However, the firm can find an optimum level of cash holding

because they use cash to balance the retained earnings and

investment opportunities. The key factor of this theory is that the

management possesses deeper knowledge about the firm value that

the potential investors and follow pecking order of financing to

minimize the cost of asymmetric information (Myers and Majluf, 1984).

Moreover, the hierarchical model reports the trend that firms prefer

internal funding as a safety sources that may include previously raised

capital or retained earnings. However, in the case of lack internal cash

resources firms can turn to debt orissue equities as a final

11

make payments (Ferreiraand Vilela (2004). Opler’s (1999) model shows

the optimal level of holding cash to be where the marginal cost of

holding liquid assets equals to the marginal cost of liquid assets

shortage. The study has shown that there is a simple trade off

managing between higher cash and lower debt in the firm. Moreover,

the correlation between cash flow and future investment opportunities

is low.

Packing order theory

This theory argues that there is nooptimal level of cash holdings for a

firm. However, the firm can find an optimum level of cash holding

because they use cash to balance the retained earnings and

investment opportunities. The key factor of this theory is that the

management possesses deeper knowledge about the firm value that

the potential investors and follow pecking order of financing to

minimize the cost of asymmetric information (Myers and Majluf, 1984).

Moreover, the hierarchical model reports the trend that firms prefer

internal funding as a safety sources that may include previously raised

capital or retained earnings. However, in the case of lack internal cash

resources firms can turn to debt orissue equities as a final

11

resourceresort (Ferreira and Vilela (2004).This theory states that the

existence of asymmetric information increases the cost of external

financing, with equity source being the highest degree of asymmetric

information compare to issuing debts (Myers,1984).Therefore, the cash

holding can be used as buffer between the retained earning and the

investment’s needs. Firms with enough internal resources will prefer to

use its cash for investments purpose then meet their debts obligations

and pay dividends. Only after that, firms can accumulate cash.

In this theory, there is a negative correlation between cash holdings

and leverage.

Free cash flow theory

In third model cash holdings are used for reducing the pressure on

managers, to improve the working activities and give a growth

opportunity. According to Jensen (1986) “Free cash flow is cash flow in

excess of that required to fund all projects that have positive net

present value, when discounting at the relevant cost of capital”. In

another words, the manager collects more cash flows for investments

and asset growth.Managers tend to reserve cash to get more assets

under control in order accept new projects without asking a permission

from the stockholders and avoiding banks loans (Ali, 2013). As result,

12

existence of asymmetric information increases the cost of external

financing, with equity source being the highest degree of asymmetric

information compare to issuing debts (Myers,1984).Therefore, the cash

holding can be used as buffer between the retained earning and the

investment’s needs. Firms with enough internal resources will prefer to

use its cash for investments purpose then meet their debts obligations

and pay dividends. Only after that, firms can accumulate cash.

In this theory, there is a negative correlation between cash holdings

and leverage.

Free cash flow theory

In third model cash holdings are used for reducing the pressure on

managers, to improve the working activities and give a growth

opportunity. According to Jensen (1986) “Free cash flow is cash flow in

excess of that required to fund all projects that have positive net

present value, when discounting at the relevant cost of capital”. In

another words, the manager collects more cash flows for investments

and asset growth.Managers tend to reserve cash to get more assets

under control in order accept new projects without asking a permission

from the stockholders and avoiding banks loans (Ali, 2013). As result,

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 115

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.