Comprehensive Report on Cash Management and Capital Budgeting

VerifiedAdded on 2020/04/21

|13

|3888

|249

Report

AI Summary

This report provides a comprehensive overview of cash management and capital budgeting. It begins by differentiating between profit and cash flow, explaining the importance of working capital, and illustrating how changes in working capital impact cash flow. The report then delves into strategies for improving cash flow, including forecasting, debt collection, and risk management. The second part of the report focuses on capital budgeting, outlining its purpose, process, and various investment appraisal methods like Payback Period, Net Present Value (NPV), and Internal Rate of Return (IRR). It discusses the advantages and disadvantages of each method and provides hypothetical illustrations to aid in decision-making. The report concludes with recommendations for optimizing cash management and capital budgeting practices within a business context, offering a detailed analysis of financial planning and investment strategies.

Running Head: CASH MANAGEMENT AND CAPITAL BUDGETING

Cash Management and Capital Budgeting

Cash Management and Capital Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash management and capital budgeting 2

Contents

Executive summary...............................................................................................................................2

Profit......................................................................................................................................................3

Cash flow..............................................................................................................................................3

Difference between profit and cash flow:..............................................................................................3

Working Capital....................................................................................................................................3

Receivables............................................................................................................................................3

Payables.................................................................................................................................................3

Inventory...............................................................................................................................................4

Changes in working capital affect cash flow.........................................................................................4

Hypothetical Illustration........................................................................................................................4

Recommendations.................................................................................................................................5

Capital budgeting..................................................................................................................................5

Purpose of Capital Budgeting................................................................................................................6

Process of capital budgeting..................................................................................................................6

Investment appraisal methods................................................................................................................7

Payback period:.................................................................................................................................7

Net Present Value:.............................................................................................................................7

Internal Rate of Return:.....................................................................................................................7

Advantages and disadvantages of methods............................................................................................8

Hypothetical illustration........................................................................................................................8

Recommendations...............................................................................................................................11

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

Contents

Executive summary...............................................................................................................................2

Profit......................................................................................................................................................3

Cash flow..............................................................................................................................................3

Difference between profit and cash flow:..............................................................................................3

Working Capital....................................................................................................................................3

Receivables............................................................................................................................................3

Payables.................................................................................................................................................3

Inventory...............................................................................................................................................4

Changes in working capital affect cash flow.........................................................................................4

Hypothetical Illustration........................................................................................................................4

Recommendations.................................................................................................................................5

Capital budgeting..................................................................................................................................5

Purpose of Capital Budgeting................................................................................................................6

Process of capital budgeting..................................................................................................................6

Investment appraisal methods................................................................................................................7

Payback period:.................................................................................................................................7

Net Present Value:.............................................................................................................................7

Internal Rate of Return:.....................................................................................................................7

Advantages and disadvantages of methods............................................................................................8

Hypothetical illustration........................................................................................................................8

Recommendations...............................................................................................................................11

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

Cash management and capital budgeting 3

Executive summary

The summary includes the concise knowledge about the management of cash and working

capital with illustration. It also provides the understanding of capital budgeting process and

its methods. The part 1 of the report shows the difference between cash and profit and gives

the reason for the shortage of cash in the business, despite of earning profits. It explains the

definition of working capital and also the effects of change in it. Methods to improve

company’s cash flow are also stated in part 1.

Part 2 of the report includes the introduction of capital budgeting, its purpose and process.

Investment appraisal methods (NPV, IRR, Payback Period) used for taking investment

decisions are also discussed in part 2. Their advantages and disadvantages and illustrative

examples are given to know which investment proposal is best suitable for the company. All

this is included in part 2. Overall analysis of cash management and capital budgeting is done

in this report.

Profit: it is a surplus left after deducting total cost from the total revenue. A company earns

profits when there is a reduction in its liabilities and debts and an increase in its assets, sales

and owners’ equity (Knight, 2012).

Cash flow: it means the amount of cash flowing in and out of the business. If there is an

increase in cash equivalents than it is called an inflow and if there is a decrease than it is

considered as outflow. (Periasamy, 2009).

Difference between profit and cash flow:

S.N

o.

Profit Cash flow

1. The revenue earned from the sale of

products and services

The inside and outside movement of cash

in the business

2. Earned after paying all the expenses

from the income earned.

Shows the availability of cash in the

business to make various payments.

3. Income statement is prepared on accrual

basis,

Cash flow statement is prepared on cash

basis

4. Gives the information about the

profitability of the firm.

Gives the idea about liquidity and

solvency of the firm.

5. A simple accounting difference between

total revenue and total expenditure.

A movement of cash in operating,

investing and financing activities of

business.

Working Capital: it is the capital required for day to day operations. According to ICAI,

“working capital shows the surplus of current assets over current liabilities which also

include short term loans. It refers to the funds available with the company for its daily

operations” (ICAI, 2017).

The total amount of current assets refers to the gross working capital and net working capital

means the excess of current assets over current liabilities (Sagner, 2010).

Receivables: accounts receivable are none other than the debtors of the company. They are

those people to whom company provides its goods and services on credit. Receivables are

Executive summary

The summary includes the concise knowledge about the management of cash and working

capital with illustration. It also provides the understanding of capital budgeting process and

its methods. The part 1 of the report shows the difference between cash and profit and gives

the reason for the shortage of cash in the business, despite of earning profits. It explains the

definition of working capital and also the effects of change in it. Methods to improve

company’s cash flow are also stated in part 1.

Part 2 of the report includes the introduction of capital budgeting, its purpose and process.

Investment appraisal methods (NPV, IRR, Payback Period) used for taking investment

decisions are also discussed in part 2. Their advantages and disadvantages and illustrative

examples are given to know which investment proposal is best suitable for the company. All

this is included in part 2. Overall analysis of cash management and capital budgeting is done

in this report.

Profit: it is a surplus left after deducting total cost from the total revenue. A company earns

profits when there is a reduction in its liabilities and debts and an increase in its assets, sales

and owners’ equity (Knight, 2012).

Cash flow: it means the amount of cash flowing in and out of the business. If there is an

increase in cash equivalents than it is called an inflow and if there is a decrease than it is

considered as outflow. (Periasamy, 2009).

Difference between profit and cash flow:

S.N

o.

Profit Cash flow

1. The revenue earned from the sale of

products and services

The inside and outside movement of cash

in the business

2. Earned after paying all the expenses

from the income earned.

Shows the availability of cash in the

business to make various payments.

3. Income statement is prepared on accrual

basis,

Cash flow statement is prepared on cash

basis

4. Gives the information about the

profitability of the firm.

Gives the idea about liquidity and

solvency of the firm.

5. A simple accounting difference between

total revenue and total expenditure.

A movement of cash in operating,

investing and financing activities of

business.

Working Capital: it is the capital required for day to day operations. According to ICAI,

“working capital shows the surplus of current assets over current liabilities which also

include short term loans. It refers to the funds available with the company for its daily

operations” (ICAI, 2017).

The total amount of current assets refers to the gross working capital and net working capital

means the excess of current assets over current liabilities (Sagner, 2010).

Receivables: accounts receivable are none other than the debtors of the company. They are

those people to whom company provides its goods and services on credit. Receivables are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash management and capital budgeting 4

part of the firm’s current assets. The customers who purchases on credit are required to pay

back the desired amount within the given time and date.

Payables: Account payables are the creditors of the company. They are those people from

whom, company purchase the material on credit. They are shown at the liability side of the

balance sheet. The creditors lend their goods and services to the company and get an

desirable amount in return.

Inventory: it is basically an asset of the firm. It means the stock of goods held with the

organisation for the purpose of sale. It includes the item purchased by the company for the

purpose of resale. There are three categories of it, which are:

Raw materials: these include those products which are required at the initial stage of

production.

Work-in-progress: unfinished items which are still in production process are known as

work-in-progress. These items are partially finished and are not ready for sale.

Finished goods: all the items or materials which have gone through the whole process

of production and are ready for sale to the customers in the market are known as

finished goods.

Inventory is termed as a current asset because it gets converted in cash within one year (Wild,

2017).

Changes in working capital affect cash flow.

The changes in the capital, directly affect the firm’s cash flow. An increase in it means the

current assets has raised through investing the resources which will reduce the flow of cash in

business (Icmai.in, 2017). On the other hand, decrease in capital means that firm’s current

liabilities has increased. Rise in current liabilities is considered as net cash inflow which

means, the company has more cash available with it to use for other projects. It is very

important to analyse the changes in working capital as they affect cash flow as well as the

overall performance of the business (Faulkender, et al., 2012).

Hypothetical Illustration

Cash Flow Statement Amount (£)

A Cash flow from Operating activities

Cash received from customers 70000

cash paid -50000

Increase/Decrease in Working Capital

Increase in Creditors 10000

Increase in Debtors -5000

Cash flow from Operating activities 25000

B Cash flow from Investing activities

receipts from sale of vehicle 10000

equipment purchase -15000

Cash used in investing activities -5000

C Cash flow from Financing activities

Payment of Loan -40000

part of the firm’s current assets. The customers who purchases on credit are required to pay

back the desired amount within the given time and date.

Payables: Account payables are the creditors of the company. They are those people from

whom, company purchase the material on credit. They are shown at the liability side of the

balance sheet. The creditors lend their goods and services to the company and get an

desirable amount in return.

Inventory: it is basically an asset of the firm. It means the stock of goods held with the

organisation for the purpose of sale. It includes the item purchased by the company for the

purpose of resale. There are three categories of it, which are:

Raw materials: these include those products which are required at the initial stage of

production.

Work-in-progress: unfinished items which are still in production process are known as

work-in-progress. These items are partially finished and are not ready for sale.

Finished goods: all the items or materials which have gone through the whole process

of production and are ready for sale to the customers in the market are known as

finished goods.

Inventory is termed as a current asset because it gets converted in cash within one year (Wild,

2017).

Changes in working capital affect cash flow.

The changes in the capital, directly affect the firm’s cash flow. An increase in it means the

current assets has raised through investing the resources which will reduce the flow of cash in

business (Icmai.in, 2017). On the other hand, decrease in capital means that firm’s current

liabilities has increased. Rise in current liabilities is considered as net cash inflow which

means, the company has more cash available with it to use for other projects. It is very

important to analyse the changes in working capital as they affect cash flow as well as the

overall performance of the business (Faulkender, et al., 2012).

Hypothetical Illustration

Cash Flow Statement Amount (£)

A Cash flow from Operating activities

Cash received from customers 70000

cash paid -50000

Increase/Decrease in Working Capital

Increase in Creditors 10000

Increase in Debtors -5000

Cash flow from Operating activities 25000

B Cash flow from Investing activities

receipts from sale of vehicle 10000

equipment purchase -15000

Cash used in investing activities -5000

C Cash flow from Financing activities

Payment of Loan -40000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash management and capital budgeting 5

Cash used in Financing activities -40000

Net decrease in cash -20000

From the above example it can be seen that even if the company is earning profit, but still its

position of liquidity is not stable as it does not have enough cash to pay its debt. Increase in

creditors will make the inflow of cash but increase in debtors means that the cash is flowing

out of the business and the collection from the debtors is not done timely. Not only from

sales, company need to derive cash from investing and financing activities also. These are the

reasons for the net decrease in cash which is shown in the statement.

Recommendations

There is a need to improve company’s cash flow through better working capital management.

If the working capital is properly managed, it will automatically have positive impact on the

inflow and outflow of the cash (Aktas, Croci and Petmezas, 2015). Certain steps are involved

for improving a cash flow, which are:

Forecast: the first step is to know about the current position of the cash flow and to

make the forecast about its position in future. The company should perform a good

forecast during the year. Forecasting will help the business to be aware about the

future cash inflow and outflow.

Improving debt collection: GRL’s trouble cash flow shows that its customers and

suppliers are not properly balanced. The debts are increasing and the cash is been hold

by the debtors. The company should focus on improving its receivables term. The

collections from debtors should be on time so that, availability of cash will be there to

pay other debts.

Segmentation of customers, suppliers and inventory: Proper categorization of the

customer should be done by the company on the basis of the probability of the

payments done by them. Dividing the suppliers into the category of regular ones and

from whom the company frequently purchases. Segregation of the inventory is also

important because sometimes the companies end up having lot of money tied up in

form of inventory which is not as per the customer requirement. Segmentation of all

these items also improves the cash flow of the company.

Risk management: company should adopt the process of risk management in order to

deal with the contingencies. The procedure should be based on the role of working

capital.

Everyone’s Priority: improvement of cash flow also includes that all the employees

should have a proper understanding about the cash flow. They should feel motivated

by the targets which are set for them. Effective and efficient performance by the staff

will eventually help the company to raise its cash flow.

Capital budgeting

It refers to the process of choosing a better investment proposal . It is considered as tool used

by companies to maximise their profits. It is one of the most challenging task for the

management because it includes decision about investments which deals with allocation of

Cash used in Financing activities -40000

Net decrease in cash -20000

From the above example it can be seen that even if the company is earning profit, but still its

position of liquidity is not stable as it does not have enough cash to pay its debt. Increase in

creditors will make the inflow of cash but increase in debtors means that the cash is flowing

out of the business and the collection from the debtors is not done timely. Not only from

sales, company need to derive cash from investing and financing activities also. These are the

reasons for the net decrease in cash which is shown in the statement.

Recommendations

There is a need to improve company’s cash flow through better working capital management.

If the working capital is properly managed, it will automatically have positive impact on the

inflow and outflow of the cash (Aktas, Croci and Petmezas, 2015). Certain steps are involved

for improving a cash flow, which are:

Forecast: the first step is to know about the current position of the cash flow and to

make the forecast about its position in future. The company should perform a good

forecast during the year. Forecasting will help the business to be aware about the

future cash inflow and outflow.

Improving debt collection: GRL’s trouble cash flow shows that its customers and

suppliers are not properly balanced. The debts are increasing and the cash is been hold

by the debtors. The company should focus on improving its receivables term. The

collections from debtors should be on time so that, availability of cash will be there to

pay other debts.

Segmentation of customers, suppliers and inventory: Proper categorization of the

customer should be done by the company on the basis of the probability of the

payments done by them. Dividing the suppliers into the category of regular ones and

from whom the company frequently purchases. Segregation of the inventory is also

important because sometimes the companies end up having lot of money tied up in

form of inventory which is not as per the customer requirement. Segmentation of all

these items also improves the cash flow of the company.

Risk management: company should adopt the process of risk management in order to

deal with the contingencies. The procedure should be based on the role of working

capital.

Everyone’s Priority: improvement of cash flow also includes that all the employees

should have a proper understanding about the cash flow. They should feel motivated

by the targets which are set for them. Effective and efficient performance by the staff

will eventually help the company to raise its cash flow.

Capital budgeting

It refers to the process of choosing a better investment proposal . It is considered as tool used

by companies to maximise their profits. It is one of the most challenging task for the

management because it includes decision about investments which deals with allocation of

Cash management and capital budgeting 6

the funds to the projects over a period of time in order to achieve the predetermined goals and

objectives (Parrino, Kidwell and Bates, 2011).

Capital budgeting generally include calculations of the accounting profit that can be derived

from each of the projects in future, the present values of the cash flows, the time taken to

recover the initial investment, risk assessments and other factors (Morris and Daley, 2017).

Purpose of Capital Budgeting

Capital budgeting is done to achieve certain objectives of the company. The purposes of

doing it are as follows:

To identify the most profitable capital expenditure.

To check that whether replacing any existing fixed asset will provide more returns or

not.

Selection of a specified project.

Find out the quantity of finance require funding the capital expenditure.

To identify the sources of fund for doing the expenditure.

To choose the best project proposal.

Decisions taken regarding capital budgeting are very crucial, important and critical. It is

very important for the firm to take correct and proper decision concerning with the

investment so to avail the profits in the long run. As these decisions are for the long time

period so they affect the overall growth of the business. (Baker and English, 2011).

Process of capital budgeting

The process is the steps which include identification, analysis, review, estimates, selection

and implementation of the best proposal. Capital budgeting process is dynamic because the

changes which take place in organisation’s environment can affect the current or selected

project (Abor, 2016). The stages involved in the process are:

Identification of project proposal: a preliminary screening of the proposals is done.

Projects are identified by the management team of the firm and after the

identification; evaluation and screening is done.

Estimation of the cash flow: the second stage involves preparation of a capital budget

for the selected proposals. The budget shows the estimated amount required for

investment.

Approval: after estimating funds for the selected projects, they are been authorized

and approved. Projects having small expenditure are approved in a short period of

time, whereas process of authorization and approval is used on projects involving

huge expenditures.

Evaluation: Incremental cash flows of projects are evaluated to know about their

ability to give proper results and profits.

Implementation: After passing above stages, the project is finally implemented in this

stage, to work upon.

Project tracking: all the implemented projects are tracked in this stage. Reports

regarding the expenses incurred and revenues earned are been made by the managers.

Post completion audit: comparison of the actual cash flow with the budgeted one is

done time to time. The audit is done to have an idea about that whether to continue the

the funds to the projects over a period of time in order to achieve the predetermined goals and

objectives (Parrino, Kidwell and Bates, 2011).

Capital budgeting generally include calculations of the accounting profit that can be derived

from each of the projects in future, the present values of the cash flows, the time taken to

recover the initial investment, risk assessments and other factors (Morris and Daley, 2017).

Purpose of Capital Budgeting

Capital budgeting is done to achieve certain objectives of the company. The purposes of

doing it are as follows:

To identify the most profitable capital expenditure.

To check that whether replacing any existing fixed asset will provide more returns or

not.

Selection of a specified project.

Find out the quantity of finance require funding the capital expenditure.

To identify the sources of fund for doing the expenditure.

To choose the best project proposal.

Decisions taken regarding capital budgeting are very crucial, important and critical. It is

very important for the firm to take correct and proper decision concerning with the

investment so to avail the profits in the long run. As these decisions are for the long time

period so they affect the overall growth of the business. (Baker and English, 2011).

Process of capital budgeting

The process is the steps which include identification, analysis, review, estimates, selection

and implementation of the best proposal. Capital budgeting process is dynamic because the

changes which take place in organisation’s environment can affect the current or selected

project (Abor, 2016). The stages involved in the process are:

Identification of project proposal: a preliminary screening of the proposals is done.

Projects are identified by the management team of the firm and after the

identification; evaluation and screening is done.

Estimation of the cash flow: the second stage involves preparation of a capital budget

for the selected proposals. The budget shows the estimated amount required for

investment.

Approval: after estimating funds for the selected projects, they are been authorized

and approved. Projects having small expenditure are approved in a short period of

time, whereas process of authorization and approval is used on projects involving

huge expenditures.

Evaluation: Incremental cash flows of projects are evaluated to know about their

ability to give proper results and profits.

Implementation: After passing above stages, the project is finally implemented in this

stage, to work upon.

Project tracking: all the implemented projects are tracked in this stage. Reports

regarding the expenses incurred and revenues earned are been made by the managers.

Post completion audit: comparison of the actual cash flow with the budgeted one is

done time to time. The audit is done to have an idea about that whether to continue the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash management and capital budgeting 7

project or not. It also shows how well the company manages its cash flows (Agarwal,

2013).

Investment appraisal methods

It is very important for the organisation to know about the financial viability of each

investment proposal (Damodaran, 2010). Evaluation of the proposal by using various

methods such as payback period, NPV, IRR and ARR is known as investment appraisal

(McLaney and Atrill, 2014). Following methods are:

Payback period:

In simpler form, it means number of years taken to recoup the primary investment. It is very

important to calculate this period to know that whether to continue the project or not.

Generally, projects having longer payback periods are not advisable (Ahmed, 2013).

Formula:

Initial Investment

Annual cash inflow

Net Present Value:

It is equals to PV of cash inflow minus PV of outflow. It is calculated to know about the

profitability of the project in which investment is done (Bierman and Smidt, 2012). If,

NPV>0 = accepted

NPV<0 = rejected

NPV=0 = selected on the basis of criteria other than NPV.

Formula:

NPV =∑

i=1

T Ci

(1+r )i −C0

C0 = Initial Investment

C = Cash Flow

r = rate of discount

T = Time

Internal Rate of Return:

It is that rate at which present value of all cash inflows of a project is equal to the initial

investment. The project having high IRR value is desirable (Brealey, et al., 2012).

Formula:

NPV = 0; PV of cash inflow – cash outflow; or

[ C1

( 1+r )1 + C2

(1+r )2 + C3

( 1+ r )3 +… ]−Initial Investment =0

C1 = cash inflow of first year

C2 = cash inflow of second year

project or not. It also shows how well the company manages its cash flows (Agarwal,

2013).

Investment appraisal methods

It is very important for the organisation to know about the financial viability of each

investment proposal (Damodaran, 2010). Evaluation of the proposal by using various

methods such as payback period, NPV, IRR and ARR is known as investment appraisal

(McLaney and Atrill, 2014). Following methods are:

Payback period:

In simpler form, it means number of years taken to recoup the primary investment. It is very

important to calculate this period to know that whether to continue the project or not.

Generally, projects having longer payback periods are not advisable (Ahmed, 2013).

Formula:

Initial Investment

Annual cash inflow

Net Present Value:

It is equals to PV of cash inflow minus PV of outflow. It is calculated to know about the

profitability of the project in which investment is done (Bierman and Smidt, 2012). If,

NPV>0 = accepted

NPV<0 = rejected

NPV=0 = selected on the basis of criteria other than NPV.

Formula:

NPV =∑

i=1

T Ci

(1+r )i −C0

C0 = Initial Investment

C = Cash Flow

r = rate of discount

T = Time

Internal Rate of Return:

It is that rate at which present value of all cash inflows of a project is equal to the initial

investment. The project having high IRR value is desirable (Brealey, et al., 2012).

Formula:

NPV = 0; PV of cash inflow – cash outflow; or

[ C1

( 1+r )1 + C2

(1+r )2 + C3

( 1+ r )3 +… ]−Initial Investment =0

C1 = cash inflow of first year

C2 = cash inflow of second year

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash management and capital budgeting 8

C3 =cash inflow of third year, and so on...

r = internal rate of return

Advantages and disadvantages of methods

S.No. Methods Advantages Disadvantages

1 Payback

period

Simple and popular

method.

Widely used to make the

quick evaluation of the

projects.

Unlike IRR, it is not concern with

the time value of money.

Give more importance to liquidity

rather than profitability.

2 Net Present

Value.

Helps in increasing the

value of firm.

Risk and profitability of

the project are

calculated.

It is difficult to find out suitable

discount rate.

Does not provide right decisions

for the projects having unequal

investments.

3 Internal Rate

of Return.

True profitability of the

proposal is calculated.

No need to determine the

cost of capital in

advance.

Monotonous calculations.

Assumption made while

calculating IRR may prove to be

wrong.

(Shim, Siegel and Shim, 2011).

Hypothetical illustration

A company wants to make an investment in a project. There are two options available and

company can invest in either of them. The managers of the company wants to know the

profitability of the projects and risk associated with them, so that they can take the correct

decision. The options are:

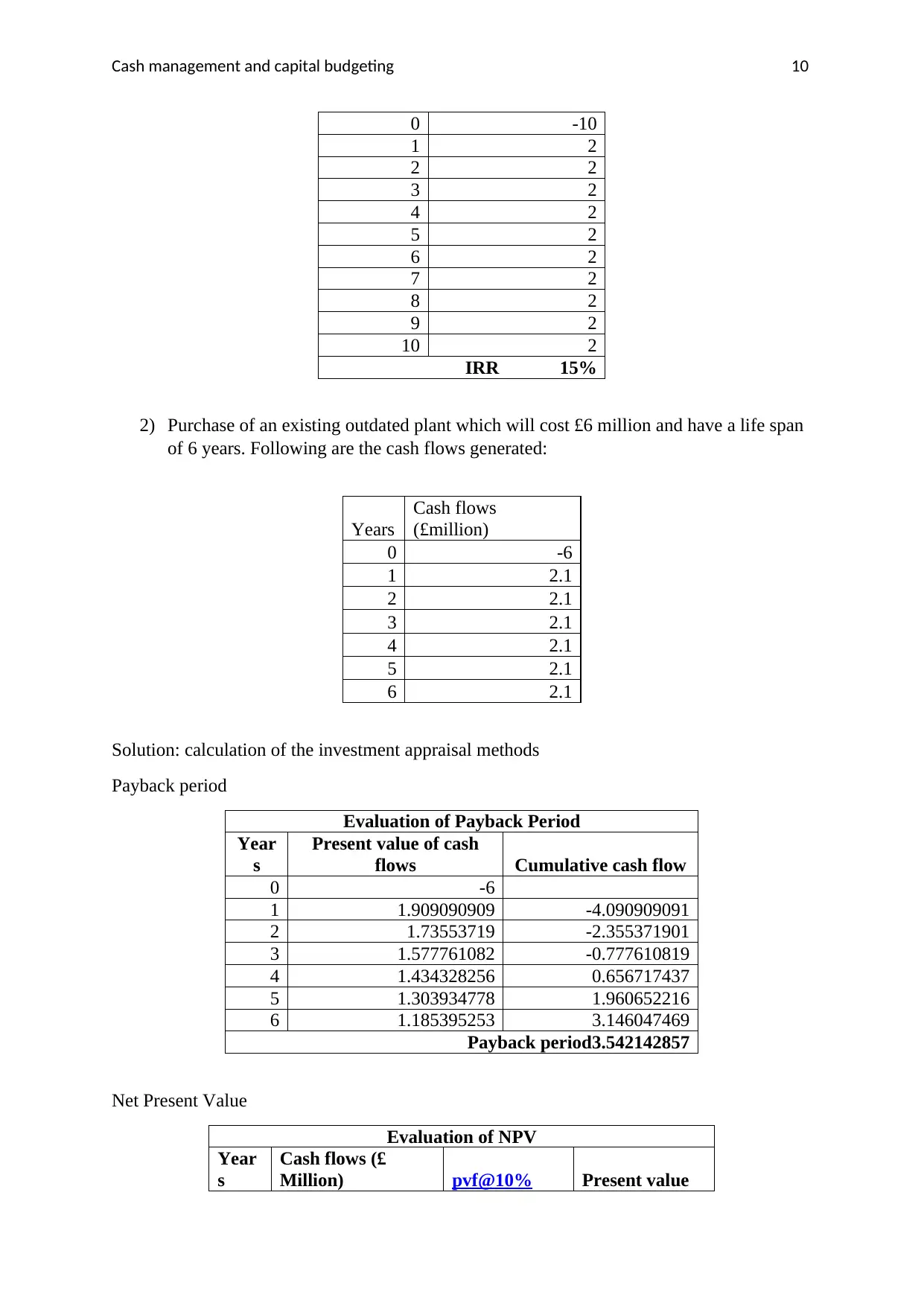

1) Construction of a plant which requires an initial outlay of £10 million and the life of

the plant is estimated to be 10 years. Following cash inflows are generated:

Years

Cash flows

(£ Million)

0 -10

1 2

2 2

3 2

4 2

5 2

6 2

7 2

8 2

9 2

10 2

C3 =cash inflow of third year, and so on...

r = internal rate of return

Advantages and disadvantages of methods

S.No. Methods Advantages Disadvantages

1 Payback

period

Simple and popular

method.

Widely used to make the

quick evaluation of the

projects.

Unlike IRR, it is not concern with

the time value of money.

Give more importance to liquidity

rather than profitability.

2 Net Present

Value.

Helps in increasing the

value of firm.

Risk and profitability of

the project are

calculated.

It is difficult to find out suitable

discount rate.

Does not provide right decisions

for the projects having unequal

investments.

3 Internal Rate

of Return.

True profitability of the

proposal is calculated.

No need to determine the

cost of capital in

advance.

Monotonous calculations.

Assumption made while

calculating IRR may prove to be

wrong.

(Shim, Siegel and Shim, 2011).

Hypothetical illustration

A company wants to make an investment in a project. There are two options available and

company can invest in either of them. The managers of the company wants to know the

profitability of the projects and risk associated with them, so that they can take the correct

decision. The options are:

1) Construction of a plant which requires an initial outlay of £10 million and the life of

the plant is estimated to be 10 years. Following cash inflows are generated:

Years

Cash flows

(£ Million)

0 -10

1 2

2 2

3 2

4 2

5 2

6 2

7 2

8 2

9 2

10 2

Cash management and capital budgeting 9

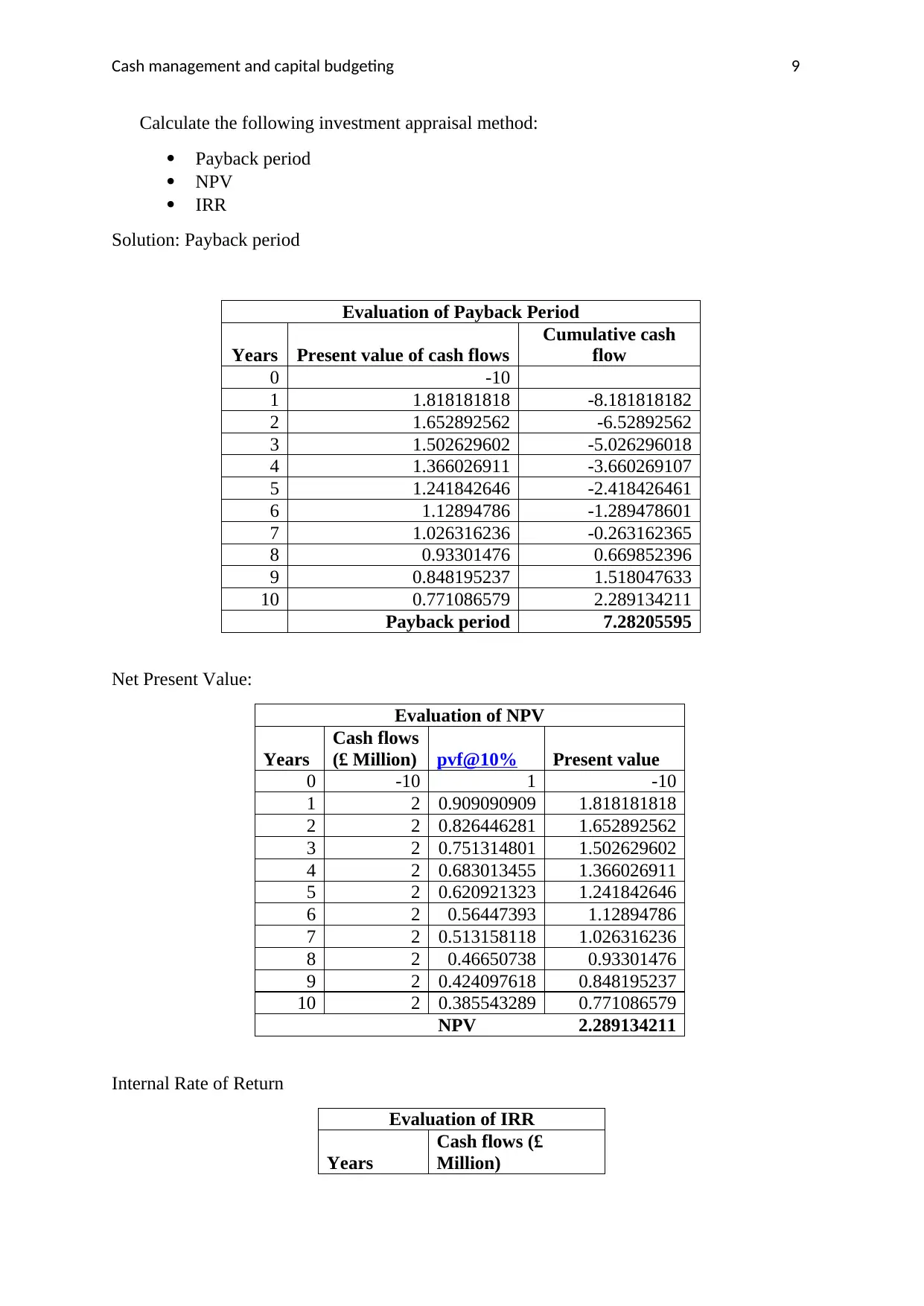

Calculate the following investment appraisal method:

Payback period

NPV

IRR

Solution: Payback period

Evaluation of Payback Period

Years Present value of cash flows

Cumulative cash

flow

0 -10

1 1.818181818 -8.181818182

2 1.652892562 -6.52892562

3 1.502629602 -5.026296018

4 1.366026911 -3.660269107

5 1.241842646 -2.418426461

6 1.12894786 -1.289478601

7 1.026316236 -0.263162365

8 0.93301476 0.669852396

9 0.848195237 1.518047633

10 0.771086579 2.289134211

Payback period 7.28205595

Net Present Value:

Evaluation of NPV

Years

Cash flows

(£ Million) pvf@10% Present value

0 -10 1 -10

1 2 0.909090909 1.818181818

2 2 0.826446281 1.652892562

3 2 0.751314801 1.502629602

4 2 0.683013455 1.366026911

5 2 0.620921323 1.241842646

6 2 0.56447393 1.12894786

7 2 0.513158118 1.026316236

8 2 0.46650738 0.93301476

9 2 0.424097618 0.848195237

10 2 0.385543289 0.771086579

NPV 2.289134211

Internal Rate of Return

Evaluation of IRR

Years

Cash flows (£

Million)

Calculate the following investment appraisal method:

Payback period

NPV

IRR

Solution: Payback period

Evaluation of Payback Period

Years Present value of cash flows

Cumulative cash

flow

0 -10

1 1.818181818 -8.181818182

2 1.652892562 -6.52892562

3 1.502629602 -5.026296018

4 1.366026911 -3.660269107

5 1.241842646 -2.418426461

6 1.12894786 -1.289478601

7 1.026316236 -0.263162365

8 0.93301476 0.669852396

9 0.848195237 1.518047633

10 0.771086579 2.289134211

Payback period 7.28205595

Net Present Value:

Evaluation of NPV

Years

Cash flows

(£ Million) pvf@10% Present value

0 -10 1 -10

1 2 0.909090909 1.818181818

2 2 0.826446281 1.652892562

3 2 0.751314801 1.502629602

4 2 0.683013455 1.366026911

5 2 0.620921323 1.241842646

6 2 0.56447393 1.12894786

7 2 0.513158118 1.026316236

8 2 0.46650738 0.93301476

9 2 0.424097618 0.848195237

10 2 0.385543289 0.771086579

NPV 2.289134211

Internal Rate of Return

Evaluation of IRR

Years

Cash flows (£

Million)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash management and capital budgeting 10

0 -10

1 2

2 2

3 2

4 2

5 2

6 2

7 2

8 2

9 2

10 2

IRR 15%

2) Purchase of an existing outdated plant which will cost £6 million and have a life span

of 6 years. Following are the cash flows generated:

Years

Cash flows

(£million)

0 -6

1 2.1

2 2.1

3 2.1

4 2.1

5 2.1

6 2.1

Solution: calculation of the investment appraisal methods

Payback period

Evaluation of Payback Period

Year

s

Present value of cash

flows Cumulative cash flow

0 -6

1 1.909090909 -4.090909091

2 1.73553719 -2.355371901

3 1.577761082 -0.777610819

4 1.434328256 0.656717437

5 1.303934778 1.960652216

6 1.185395253 3.146047469

Payback period3.542142857

Net Present Value

Evaluation of NPV

Year

s

Cash flows (£

Million) pvf@10% Present value

0 -10

1 2

2 2

3 2

4 2

5 2

6 2

7 2

8 2

9 2

10 2

IRR 15%

2) Purchase of an existing outdated plant which will cost £6 million and have a life span

of 6 years. Following are the cash flows generated:

Years

Cash flows

(£million)

0 -6

1 2.1

2 2.1

3 2.1

4 2.1

5 2.1

6 2.1

Solution: calculation of the investment appraisal methods

Payback period

Evaluation of Payback Period

Year

s

Present value of cash

flows Cumulative cash flow

0 -6

1 1.909090909 -4.090909091

2 1.73553719 -2.355371901

3 1.577761082 -0.777610819

4 1.434328256 0.656717437

5 1.303934778 1.960652216

6 1.185395253 3.146047469

Payback period3.542142857

Net Present Value

Evaluation of NPV

Year

s

Cash flows (£

Million) pvf@10% Present value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash management and capital budgeting 11

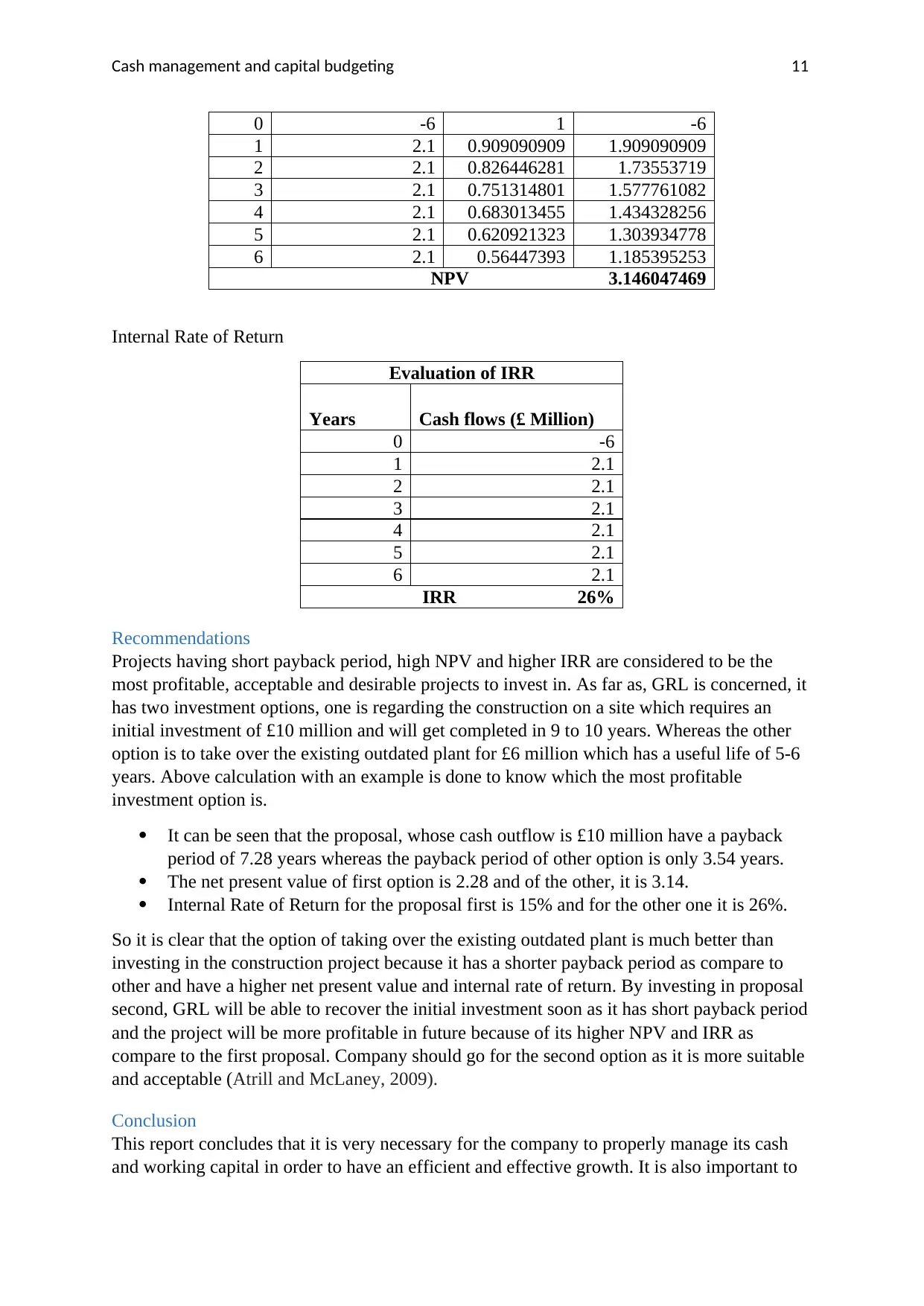

0 -6 1 -6

1 2.1 0.909090909 1.909090909

2 2.1 0.826446281 1.73553719

3 2.1 0.751314801 1.577761082

4 2.1 0.683013455 1.434328256

5 2.1 0.620921323 1.303934778

6 2.1 0.56447393 1.185395253

NPV 3.146047469

Internal Rate of Return

Evaluation of IRR

Years Cash flows (£ Million)

0 -6

1 2.1

2 2.1

3 2.1

4 2.1

5 2.1

6 2.1

IRR 26%

Recommendations

Projects having short payback period, high NPV and higher IRR are considered to be the

most profitable, acceptable and desirable projects to invest in. As far as, GRL is concerned, it

has two investment options, one is regarding the construction on a site which requires an

initial investment of £10 million and will get completed in 9 to 10 years. Whereas the other

option is to take over the existing outdated plant for £6 million which has a useful life of 5-6

years. Above calculation with an example is done to know which the most profitable

investment option is.

It can be seen that the proposal, whose cash outflow is £10 million have a payback

period of 7.28 years whereas the payback period of other option is only 3.54 years.

The net present value of first option is 2.28 and of the other, it is 3.14.

Internal Rate of Return for the proposal first is 15% and for the other one it is 26%.

So it is clear that the option of taking over the existing outdated plant is much better than

investing in the construction project because it has a shorter payback period as compare to

other and have a higher net present value and internal rate of return. By investing in proposal

second, GRL will be able to recover the initial investment soon as it has short payback period

and the project will be more profitable in future because of its higher NPV and IRR as

compare to the first proposal. Company should go for the second option as it is more suitable

and acceptable (Atrill and McLaney, 2009).

Conclusion

This report concludes that it is very necessary for the company to properly manage its cash

and working capital in order to have an efficient and effective growth. It is also important to

0 -6 1 -6

1 2.1 0.909090909 1.909090909

2 2.1 0.826446281 1.73553719

3 2.1 0.751314801 1.577761082

4 2.1 0.683013455 1.434328256

5 2.1 0.620921323 1.303934778

6 2.1 0.56447393 1.185395253

NPV 3.146047469

Internal Rate of Return

Evaluation of IRR

Years Cash flows (£ Million)

0 -6

1 2.1

2 2.1

3 2.1

4 2.1

5 2.1

6 2.1

IRR 26%

Recommendations

Projects having short payback period, high NPV and higher IRR are considered to be the

most profitable, acceptable and desirable projects to invest in. As far as, GRL is concerned, it

has two investment options, one is regarding the construction on a site which requires an

initial investment of £10 million and will get completed in 9 to 10 years. Whereas the other

option is to take over the existing outdated plant for £6 million which has a useful life of 5-6

years. Above calculation with an example is done to know which the most profitable

investment option is.

It can be seen that the proposal, whose cash outflow is £10 million have a payback

period of 7.28 years whereas the payback period of other option is only 3.54 years.

The net present value of first option is 2.28 and of the other, it is 3.14.

Internal Rate of Return for the proposal first is 15% and for the other one it is 26%.

So it is clear that the option of taking over the existing outdated plant is much better than

investing in the construction project because it has a shorter payback period as compare to

other and have a higher net present value and internal rate of return. By investing in proposal

second, GRL will be able to recover the initial investment soon as it has short payback period

and the project will be more profitable in future because of its higher NPV and IRR as

compare to the first proposal. Company should go for the second option as it is more suitable

and acceptable (Atrill and McLaney, 2009).

Conclusion

This report concludes that it is very necessary for the company to properly manage its cash

and working capital in order to have an efficient and effective growth. It is also important to

Cash management and capital budgeting 12

take appropriate investment decision with the use of capital budgeting methods so that

profitability can be maintained. Proper investment appraisal methods should be calculate to

know the risk associated with a particular investment project. All this analysis will eventually

help the company to prosper and to earn profits.

References

Periasamy, P. (2009). Financial Management. 2nd ed. New Delhi: Tata McGraw-Hill

Education Pvt. Ltd.

Abor, J.Y., 2016. Entrepreneurial Finance for MSMEs: A Managerial Approach for

Developing Markets. Springer.

Agarwal, V., 2013. Managerial Economics. Pearson Education India.

Ahmed, I.E., 2013. Factors determining the selection of capital budgeting

techniques. Journal of Finance and Investment Analysis, 2(2), pp.77-88.

Aktas, N., Croci, E. and Petmezas, D., 2015. Is working capital management value-

enhancing? Evidence from firm performance and investments. Journal of Corporate

Finance, 30, pp.98-113.

Atrill, P. and McLaney, E., 2009. Management accounting for decision makers. Pearson

Education.

Baker, H.K. and English, P., 2011. Capital budgeting valuation: Financial analysis for

today's investment projects (Vol. 13). John Wiley & Sons.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Brealey, R.A., Myers, S.C., Allen, F. and Mohanty, P., 2012. Principles of corporate finance.

Tata McGraw-Hill Education.

Damodaran, A., 2010. Applied corporate finance. John Wiley & Sons.

Faulkender, M., Flannery, M.J., Hankins, K.W. and Smith, J.M., 2012. Cash flows and

leverage adjustments. Journal of Financial Economics, 103(3), pp.632-646.

ICAI. (2017). ICAI - The Institute of Chartered Accountants of India. [online] Available at:

https://www.icai.org/post.html?post_id=12431 [Accessed 11 Nov. 2017].

Icmai.in. (2017). Student Home. [online] Available at: http://icmai.in/studentswebsite/

[Accessed 11 Nov. 2017].

Knight, F.H., 2012. Risk, uncertainty and profit. Courier Corporation.

McLaney, E.J. and Atrill, P., 2014. Accounting and Finance: An Introduction. Pearson.

take appropriate investment decision with the use of capital budgeting methods so that

profitability can be maintained. Proper investment appraisal methods should be calculate to

know the risk associated with a particular investment project. All this analysis will eventually

help the company to prosper and to earn profits.

References

Periasamy, P. (2009). Financial Management. 2nd ed. New Delhi: Tata McGraw-Hill

Education Pvt. Ltd.

Abor, J.Y., 2016. Entrepreneurial Finance for MSMEs: A Managerial Approach for

Developing Markets. Springer.

Agarwal, V., 2013. Managerial Economics. Pearson Education India.

Ahmed, I.E., 2013. Factors determining the selection of capital budgeting

techniques. Journal of Finance and Investment Analysis, 2(2), pp.77-88.

Aktas, N., Croci, E. and Petmezas, D., 2015. Is working capital management value-

enhancing? Evidence from firm performance and investments. Journal of Corporate

Finance, 30, pp.98-113.

Atrill, P. and McLaney, E., 2009. Management accounting for decision makers. Pearson

Education.

Baker, H.K. and English, P., 2011. Capital budgeting valuation: Financial analysis for

today's investment projects (Vol. 13). John Wiley & Sons.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Brealey, R.A., Myers, S.C., Allen, F. and Mohanty, P., 2012. Principles of corporate finance.

Tata McGraw-Hill Education.

Damodaran, A., 2010. Applied corporate finance. John Wiley & Sons.

Faulkender, M., Flannery, M.J., Hankins, K.W. and Smith, J.M., 2012. Cash flows and

leverage adjustments. Journal of Financial Economics, 103(3), pp.632-646.

ICAI. (2017). ICAI - The Institute of Chartered Accountants of India. [online] Available at:

https://www.icai.org/post.html?post_id=12431 [Accessed 11 Nov. 2017].

Icmai.in. (2017). Student Home. [online] Available at: http://icmai.in/studentswebsite/

[Accessed 11 Nov. 2017].

Knight, F.H., 2012. Risk, uncertainty and profit. Courier Corporation.

McLaney, E.J. and Atrill, P., 2014. Accounting and Finance: An Introduction. Pearson.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.