Organizational Change: Cashless Banking Impact on Australian Banks

VerifiedAdded on 2021/06/18

|17

|4460

|14

Report

AI Summary

This report provides a comprehensive analysis of the impact of cashless banking on organizational changes within the Australian banking industry. It begins by exploring the increasing preference for electronic payment methods and the declining use of cash, highlighting the role of the Reserve Bank of Australia and the New Payments Platform. The report then delves into the technological innovations and globalization that drive these changes, emphasizing the shift from traditional banking models to digital platforms. Key areas of focus include the implications for monetary policy, efficiency gains, increased profitability, business growth, and enhanced customer relationships. The analysis considers the benefits of cashless systems, such as reduced costs and increased efficiency, while also addressing potential challenges. The report also examines the Reserve Bank's role in a cashless economy, focusing on its regulatory and supervisory functions. Ultimately, the report provides insights into the future of financial transactions and the ongoing evolution of the banking sector in Australia.

Impact of Cashless Banking in Australia 1

IMPACT OF CASHLESS BANKING ON ORGANIZATIONAL CHANGE OF BANKING

INDUSTRY OF AUSTRALIA

Name

University

Course

Tutor

Date

IMPACT OF CASHLESS BANKING ON ORGANIZATIONAL CHANGE OF BANKING

INDUSTRY OF AUSTRALIA

Name

University

Course

Tutor

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impact of Cashless Banking in Australia 2

Table of Contents

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................3

The monetary policy implications...................................................................................................9

Efficiency in the Monetary Policy.................................................................................................10

The increase in profitability...........................................................................................................11

Growth of the Business..................................................................................................................12

Deeper customer relation...............................................................................................................13

Increased Quality Service..............................................................................................................13

List of References..........................................................................................................................15

Table of Contents

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................3

The monetary policy implications...................................................................................................9

Efficiency in the Monetary Policy.................................................................................................10

The increase in profitability...........................................................................................................11

Growth of the Business..................................................................................................................12

Deeper customer relation...............................................................................................................13

Increased Quality Service..............................................................................................................13

List of References..........................................................................................................................15

Impact of Cashless Banking in Australia 3

Executive Summary

The preference of using electronic payment methods over cash has increased among consumers

in Australian. Despite this, the demand for cash for non-transactions purposes and as a way of

wealth storage remains strong. The use of cashless bank services for transactions has increased

over the decades. The economy uses both the cash and cashless system to make payments for

different services and products. Cash is still preferred as people believe it is a secure means of

payment and storage of wealth purposes. Until the full transition to the cashless transaction

system, the Reserve Bank maintains public confidence in providing high-quality notes for cash

transactions and free from counterfeiting. The trend in using cash for the transactions has

changed to the cashless system with the continuous use of mobile banking, internet transfers and

other electronic methods of transfers. The Reserved Bank of Australia came up with the New

Payments Platform to oversee the extinction of cash transactions in Australia.

Introduction

With the introduction of globalization, organizations have undergone constant changes, and it

has become an accepted phenomenon in all industries (Humphrey, Kim & Vale 2011, p. 222).

Technological innovations, the creation of new market conditions, environmental, and political

factors have led organizations to change. Banking industry is not an exception and it has become

a common phenomenon (Clary & Wandersee 2013, p. 68). Organizations adjust their operations

and adopt the innovations to be in line with market changes. Competition is also another factor

that has led to change initiative as other organizations set standards and to remain relevant and

competitive in the market, the organization has to adopt the new market conditions created. The

Executive Summary

The preference of using electronic payment methods over cash has increased among consumers

in Australian. Despite this, the demand for cash for non-transactions purposes and as a way of

wealth storage remains strong. The use of cashless bank services for transactions has increased

over the decades. The economy uses both the cash and cashless system to make payments for

different services and products. Cash is still preferred as people believe it is a secure means of

payment and storage of wealth purposes. Until the full transition to the cashless transaction

system, the Reserve Bank maintains public confidence in providing high-quality notes for cash

transactions and free from counterfeiting. The trend in using cash for the transactions has

changed to the cashless system with the continuous use of mobile banking, internet transfers and

other electronic methods of transfers. The Reserved Bank of Australia came up with the New

Payments Platform to oversee the extinction of cash transactions in Australia.

Introduction

With the introduction of globalization, organizations have undergone constant changes, and it

has become an accepted phenomenon in all industries (Humphrey, Kim & Vale 2011, p. 222).

Technological innovations, the creation of new market conditions, environmental, and political

factors have led organizations to change. Banking industry is not an exception and it has become

a common phenomenon (Clary & Wandersee 2013, p. 68). Organizations adjust their operations

and adopt the innovations to be in line with market changes. Competition is also another factor

that has led to change initiative as other organizations set standards and to remain relevant and

competitive in the market, the organization has to adopt the new market conditions created. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impact of Cashless Banking in Australia 4

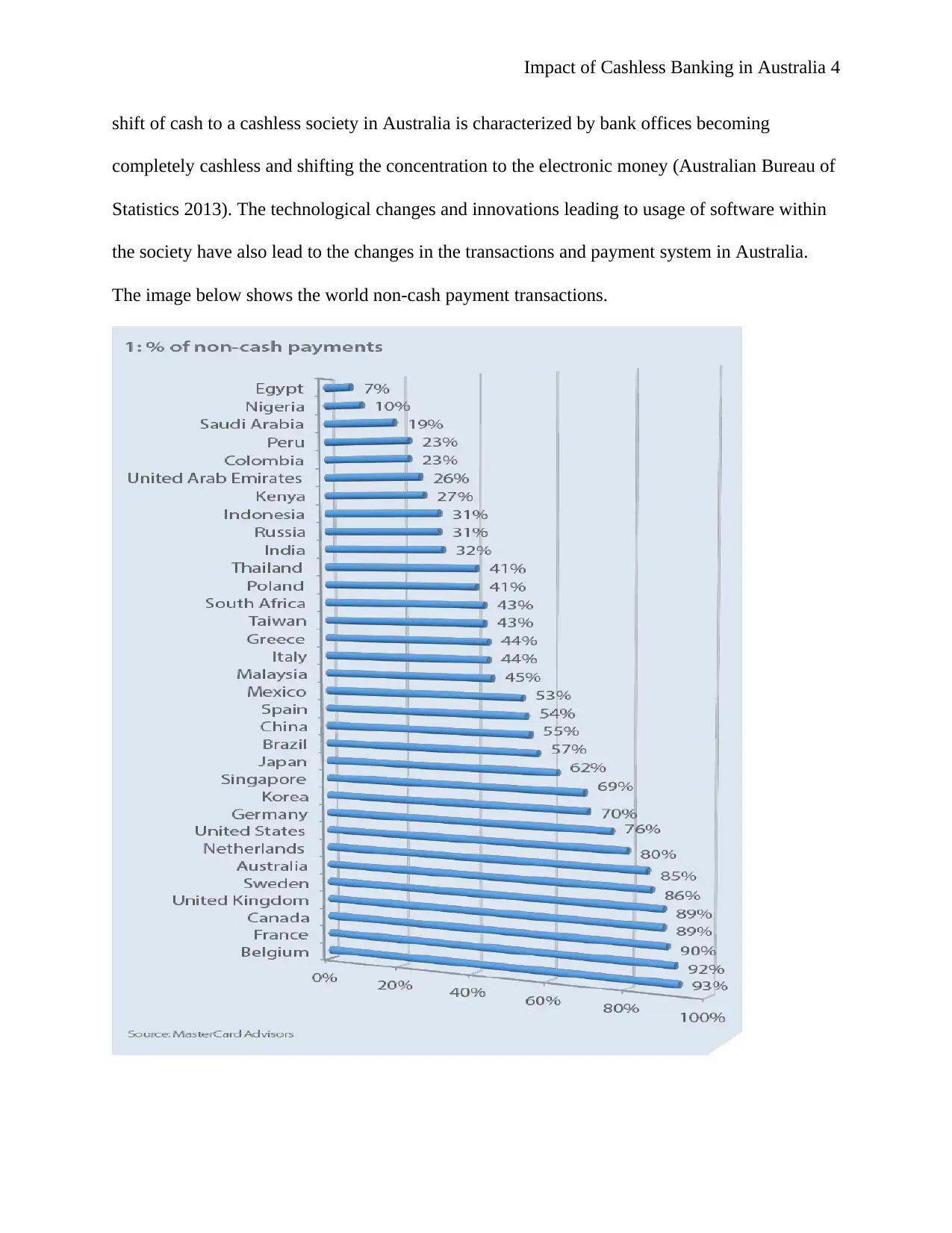

shift of cash to a cashless society in Australia is characterized by bank offices becoming

completely cashless and shifting the concentration to the electronic money (Australian Bureau of

Statistics 2013). The technological changes and innovations leading to usage of software within

the society have also lead to the changes in the transactions and payment system in Australia.

The image below shows the world non-cash payment transactions.

shift of cash to a cashless society in Australia is characterized by bank offices becoming

completely cashless and shifting the concentration to the electronic money (Australian Bureau of

Statistics 2013). The technological changes and innovations leading to usage of software within

the society have also lead to the changes in the transactions and payment system in Australia.

The image below shows the world non-cash payment transactions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impact of Cashless Banking in Australia 5

The Reserve Bank of Australia the country’s top financial institution released data showing proof

that the ATM cash withdrawals plunged down to its lowest in the 15 years. The share of cash in

consumer payments went down to 39% from 70% over nine year period (RBA, 2012).

The financial sector globally has undergone many changes due to innovations and the increasing

demand for services by customers (Segendorf & Wretman 2015, p. 51). Also, the need to

facilitate easy in production and trade of services and products has led to the organization

changes in the banking industries. The ease of convenience and accessibilities of services led to

constant technological innovations to meet the needs of customers. For example, a study done by

the MasterCard showed that Australians regard your business negatively if your only method of

payment is cash.

People’s engagement in transactions has led to these changes. Banks have traditionally been

viewed as stores for cash storages since the inventions of money. However, globalization, new

methods of handling money and new information systems have led to the increase in

development of financial systems. It led to the change in the bank-customer relationship and the

services customers expect from the bank. The banks are no longer viewed as only a cash store,

but also a service advisory system.

The technological and communication advancements have contributed highly to the changes in

the behavioral changes of the customers and the banks (Bagnall, Chong & Smith 2011, p.9).

Innovations of cashless products such as banking over the internet, use of e-cards and the ease of

accessibility during transactions changed the banking organizations product and services to offer.

Traditionally, the banking services were accessed at the working hours, but the changes have

now led to 24-hour access to services. Services such as transfer of money, making savings,

purchasing goods have become cashless, and one can perform any transaction without going to

The Reserve Bank of Australia the country’s top financial institution released data showing proof

that the ATM cash withdrawals plunged down to its lowest in the 15 years. The share of cash in

consumer payments went down to 39% from 70% over nine year period (RBA, 2012).

The financial sector globally has undergone many changes due to innovations and the increasing

demand for services by customers (Segendorf & Wretman 2015, p. 51). Also, the need to

facilitate easy in production and trade of services and products has led to the organization

changes in the banking industries. The ease of convenience and accessibilities of services led to

constant technological innovations to meet the needs of customers. For example, a study done by

the MasterCard showed that Australians regard your business negatively if your only method of

payment is cash.

People’s engagement in transactions has led to these changes. Banks have traditionally been

viewed as stores for cash storages since the inventions of money. However, globalization, new

methods of handling money and new information systems have led to the increase in

development of financial systems. It led to the change in the bank-customer relationship and the

services customers expect from the bank. The banks are no longer viewed as only a cash store,

but also a service advisory system.

The technological and communication advancements have contributed highly to the changes in

the behavioral changes of the customers and the banks (Bagnall, Chong & Smith 2011, p.9).

Innovations of cashless products such as banking over the internet, use of e-cards and the ease of

accessibility during transactions changed the banking organizations product and services to offer.

Traditionally, the banking services were accessed at the working hours, but the changes have

now led to 24-hour access to services. Services such as transfer of money, making savings,

purchasing goods have become cashless, and one can perform any transaction without going to

Impact of Cashless Banking in Australia 6

the bank. The increased knowledge in managing internet banking, automated teller machines has

led to customers’ independence and teller bank services not required. The bank card, internet

banking, and the automated teller machines have led to cashless services. These have led to

different impacts on the organization change of banking industries.

Changes in customer behavior and perceptions towards cash services at the banks led to the

innovation of cashless banking. Cashless bank services refer to banks relying on the use of

electronic means rather than cash when conducting monetary transactions. The introduction and

widespread use of electronic cards, mobiles and internet banking in early 2000 led to the cashless

banking concept. The cards are loaded with credits from the banks for customers to transact, and

when the money is used up, they are recharged. The cashless system is used largely over the

world in the finance system. Most transactions in Australia have changed to the cashless system,

and only 7% are using cash. It has led to the debate on whether Australia will follow Sweden and

adopt the cashless banking system entirely (Segendorf & Wretman 2015, p. 51). The trend in

lower usage of cash in transactions shows that the future is cashless banking system.

Cashless banking system led to increased benefits and reduction in the cost of the operations.

The role of the Reserve Bank is to focus on the implications of monetary policies in the economy

of Australia. It is debatable that the cashless society would lead to Reserve Bank losing their

independence and making the monetary policies less efficient. Cashless society refers to no

distribution or circulation of coins and notes by the cent Reserve Bank. Private institutions issue

all the money and the Reserve Bank has no monopoly on the issue of money. There will be no

physical medium of exchange of money. The cashless banking system will reduce the chances of

banks run in the presence of negative interest rates. Customers would not withdraw bank

deposits in case of an expected bank failure. It will only encourage customers to withdraw to

the bank. The increased knowledge in managing internet banking, automated teller machines has

led to customers’ independence and teller bank services not required. The bank card, internet

banking, and the automated teller machines have led to cashless services. These have led to

different impacts on the organization change of banking industries.

Changes in customer behavior and perceptions towards cash services at the banks led to the

innovation of cashless banking. Cashless bank services refer to banks relying on the use of

electronic means rather than cash when conducting monetary transactions. The introduction and

widespread use of electronic cards, mobiles and internet banking in early 2000 led to the cashless

banking concept. The cards are loaded with credits from the banks for customers to transact, and

when the money is used up, they are recharged. The cashless system is used largely over the

world in the finance system. Most transactions in Australia have changed to the cashless system,

and only 7% are using cash. It has led to the debate on whether Australia will follow Sweden and

adopt the cashless banking system entirely (Segendorf & Wretman 2015, p. 51). The trend in

lower usage of cash in transactions shows that the future is cashless banking system.

Cashless banking system led to increased benefits and reduction in the cost of the operations.

The role of the Reserve Bank is to focus on the implications of monetary policies in the economy

of Australia. It is debatable that the cashless society would lead to Reserve Bank losing their

independence and making the monetary policies less efficient. Cashless society refers to no

distribution or circulation of coins and notes by the cent Reserve Bank. Private institutions issue

all the money and the Reserve Bank has no monopoly on the issue of money. There will be no

physical medium of exchange of money. The cashless banking system will reduce the chances of

banks run in the presence of negative interest rates. Customers would not withdraw bank

deposits in case of an expected bank failure. It will only encourage customers to withdraw to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impact of Cashless Banking in Australia 7

avoid interest fees that may be caused by negative interest rates. In the negative interest rates, the

cashless society may strengthen the Reserve Bank power to conduct the monetary policies

(Bagnall, Chong & Smith 2011, p.9).

If the negative interest rates are carried over to the private households, the banks will benefit and

the possibilities of experiencing bank run are lower in the cashless banking society. A good

percentage is not using cash anymore, and the highly developed electronic payment system is

less likely to experience bank run. People will have to visit the banks to deposit their cash as the

cash transactions cannot take place without visiting the banking halls. People cannot pay bills

over the internet or use of cards without loading the cards. The people will stop visiting banks to

withdraw money and then deposit it again (Humphrey, Kim & Vale 2011, p. 222).

Another benefit of cashless banking is the different cost structures for the card payments. The

card payments compared to cash are cheaper. The use of debit cards is a cheaper form of

payments compared to cash or use of credit cards. The use of debit cards in transactions has

increased the efficiency of the payment system in the cashless banking system (Humphrey, Kim

& Vale 2011, p. 218). Transaction handling, customer service, information technology and

communication, authorization of payment, and control of checks are some of the cost of debit

cards. While for cash, costs include the deposits, personnel costs such as cash counting and

handling every day, withdrawals, printing costs, transportation, time for transactions and

servicing fee and other fees by the banks (Segendorf & Wretman 2015, p. 49). Other costs such

as work time, administration information, safety costs, insurances in handling cash and risk of

robbery are also involved in cash transactions, unlike cashless transactions. The banks bear

major costs for cash transactions and suffer losses. The cashless transactions assist banks in

minimizing losses and focussing more on its customers. Reducing cash payments and using the

avoid interest fees that may be caused by negative interest rates. In the negative interest rates, the

cashless society may strengthen the Reserve Bank power to conduct the monetary policies

(Bagnall, Chong & Smith 2011, p.9).

If the negative interest rates are carried over to the private households, the banks will benefit and

the possibilities of experiencing bank run are lower in the cashless banking society. A good

percentage is not using cash anymore, and the highly developed electronic payment system is

less likely to experience bank run. People will have to visit the banks to deposit their cash as the

cash transactions cannot take place without visiting the banking halls. People cannot pay bills

over the internet or use of cards without loading the cards. The people will stop visiting banks to

withdraw money and then deposit it again (Humphrey, Kim & Vale 2011, p. 222).

Another benefit of cashless banking is the different cost structures for the card payments. The

card payments compared to cash are cheaper. The use of debit cards is a cheaper form of

payments compared to cash or use of credit cards. The use of debit cards in transactions has

increased the efficiency of the payment system in the cashless banking system (Humphrey, Kim

& Vale 2011, p. 218). Transaction handling, customer service, information technology and

communication, authorization of payment, and control of checks are some of the cost of debit

cards. While for cash, costs include the deposits, personnel costs such as cash counting and

handling every day, withdrawals, printing costs, transportation, time for transactions and

servicing fee and other fees by the banks (Segendorf & Wretman 2015, p. 49). Other costs such

as work time, administration information, safety costs, insurances in handling cash and risk of

robbery are also involved in cash transactions, unlike cashless transactions. The banks bear

major costs for cash transactions and suffer losses. The cashless transactions assist banks in

minimizing losses and focussing more on its customers. Reducing cash payments and using the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impact of Cashless Banking in Australia 8

cashless system make the purchasing and transactions more efficient. The use of debit cards in

most transactions benefits the society as they would use the credit cards less which costs are also

on the higher side (Sorman 2011, p.190).

The desire to adopt the use of electronic payment methods over cash has increased among

consumers in many parts of the world. However, the demand for cash for non-transactions

purposes and as a way of wealth storage is very stable and adopted from one organization to

another. The use of cashless bank services for transactions has increased over the decades. The

economy uses both the cash and cashless system to make payments for different services and

products (OECD Economic Surveys Australia', 2014, p.62). On the other hand, the use of cash is

still preferred as people believe it is a secure means of payment and storage of wealth purposes.

The trend in using cash for the transactions has changed to the cashless system with the

continuous use of mobile banking, internet transfers and other electronic methods of transfers.

Until the full transition to the cashless transaction system, the Reserve Bank maintains public

confidence in providing high-quality notes for cash transactions and free from counterfeiting.

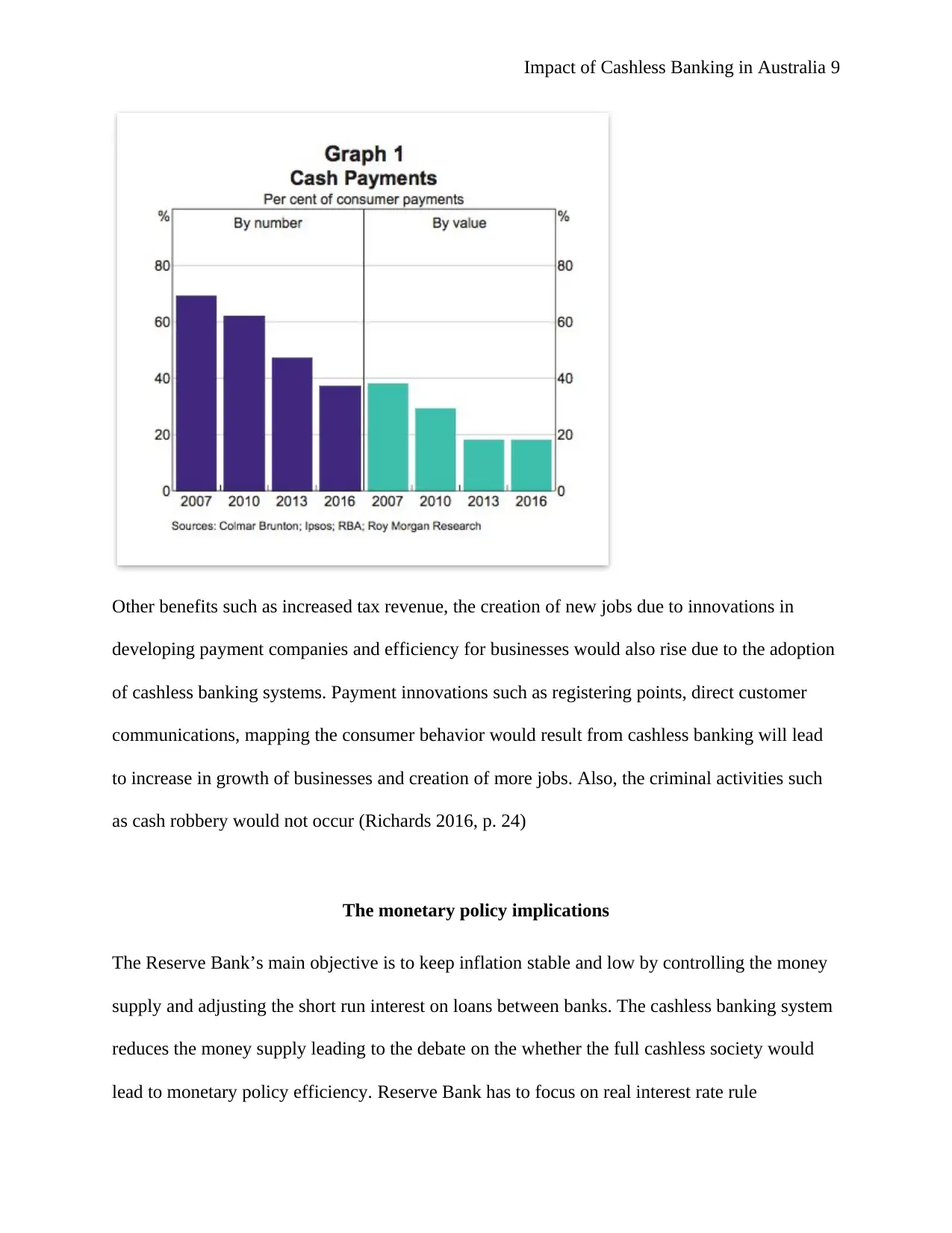

The graph below shows the trends of cash payment from 2007 to the year 2016 in Australia.

cashless system make the purchasing and transactions more efficient. The use of debit cards in

most transactions benefits the society as they would use the credit cards less which costs are also

on the higher side (Sorman 2011, p.190).

The desire to adopt the use of electronic payment methods over cash has increased among

consumers in many parts of the world. However, the demand for cash for non-transactions

purposes and as a way of wealth storage is very stable and adopted from one organization to

another. The use of cashless bank services for transactions has increased over the decades. The

economy uses both the cash and cashless system to make payments for different services and

products (OECD Economic Surveys Australia', 2014, p.62). On the other hand, the use of cash is

still preferred as people believe it is a secure means of payment and storage of wealth purposes.

The trend in using cash for the transactions has changed to the cashless system with the

continuous use of mobile banking, internet transfers and other electronic methods of transfers.

Until the full transition to the cashless transaction system, the Reserve Bank maintains public

confidence in providing high-quality notes for cash transactions and free from counterfeiting.

The graph below shows the trends of cash payment from 2007 to the year 2016 in Australia.

Impact of Cashless Banking in Australia 9

Other benefits such as increased tax revenue, the creation of new jobs due to innovations in

developing payment companies and efficiency for businesses would also rise due to the adoption

of cashless banking systems. Payment innovations such as registering points, direct customer

communications, mapping the consumer behavior would result from cashless banking will lead

to increase in growth of businesses and creation of more jobs. Also, the criminal activities such

as cash robbery would not occur (Richards 2016, p. 24)

The monetary policy implications

The Reserve Bank’s main objective is to keep inflation stable and low by controlling the money

supply and adjusting the short run interest on loans between banks. The cashless banking system

reduces the money supply leading to the debate on the whether the full cashless society would

lead to monetary policy efficiency. Reserve Bank has to focus on real interest rate rule

Other benefits such as increased tax revenue, the creation of new jobs due to innovations in

developing payment companies and efficiency for businesses would also rise due to the adoption

of cashless banking systems. Payment innovations such as registering points, direct customer

communications, mapping the consumer behavior would result from cashless banking will lead

to increase in growth of businesses and creation of more jobs. Also, the criminal activities such

as cash robbery would not occur (Richards 2016, p. 24)

The monetary policy implications

The Reserve Bank’s main objective is to keep inflation stable and low by controlling the money

supply and adjusting the short run interest on loans between banks. The cashless banking system

reduces the money supply leading to the debate on the whether the full cashless society would

lead to monetary policy efficiency. Reserve Bank has to focus on real interest rate rule

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impact of Cashless Banking in Australia 10

manipulating the short-run interest rate on loans between banks meaning the money supply in the

banking system will not affect the cashless system will not affect monetary policy (Liu,

Margaritis & Tourani-Rad 2010, p.507). According to Stix et al. (2014, p. 2014), the process of

adjusting the short-term loan interest rate will enable the transition to a cashless society not to

interfere with the monetary policy. Other tools can also be used by the Reserve Bank to control

inflations in cashless society; these include reserving the cash requirements, rationing open

market operations and moral suasion (Odior et al. 2012, p. 13). The role of the Reserve Bank will

have to be revised in a cashless economy and focus more on regulatory and supervision of the

institutions issuing money. The Central Bank will have to increase its regulation role, tax

overview and integrity protection (Cowling & Howlett 2012, p.72).

Efficiency in the Monetary Policy

According to a study done by Odior (2012, p 14), the development of cashless society would see

monetary policies more efficient with less cash in circulation. The reduction in cash transactions

will lead to the payment system more efficient and reduction in robbery cases and cost of

transactions. Australia focusing more on market operations and reserve requirements will help

reduce inflation. The costs of not printing currency will balance some of the losses that may

occur. The cashless banking system will increase the rate of circulation of currency in the long

run which stimulates trade and commercial activities (Claessens, Dem & Cock 2012, p. 258).

The role of Reserve Bank would be revised into taking a supervisory role in controlling the

cashless money issued by private institutions. They will have to control inflation and to impose

legal reserve requirement to remain independent.

manipulating the short-run interest rate on loans between banks meaning the money supply in the

banking system will not affect the cashless system will not affect monetary policy (Liu,

Margaritis & Tourani-Rad 2010, p.507). According to Stix et al. (2014, p. 2014), the process of

adjusting the short-term loan interest rate will enable the transition to a cashless society not to

interfere with the monetary policy. Other tools can also be used by the Reserve Bank to control

inflations in cashless society; these include reserving the cash requirements, rationing open

market operations and moral suasion (Odior et al. 2012, p. 13). The role of the Reserve Bank will

have to be revised in a cashless economy and focus more on regulatory and supervision of the

institutions issuing money. The Central Bank will have to increase its regulation role, tax

overview and integrity protection (Cowling & Howlett 2012, p.72).

Efficiency in the Monetary Policy

According to a study done by Odior (2012, p 14), the development of cashless society would see

monetary policies more efficient with less cash in circulation. The reduction in cash transactions

will lead to the payment system more efficient and reduction in robbery cases and cost of

transactions. Australia focusing more on market operations and reserve requirements will help

reduce inflation. The costs of not printing currency will balance some of the losses that may

occur. The cashless banking system will increase the rate of circulation of currency in the long

run which stimulates trade and commercial activities (Claessens, Dem & Cock 2012, p. 258).

The role of Reserve Bank would be revised into taking a supervisory role in controlling the

cashless money issued by private institutions. They will have to control inflation and to impose

legal reserve requirement to remain independent.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impact of Cashless Banking in Australia 11

The Reserve Bank will most likely revise its role in the cashless society in the cases of the

transaction in the cashless society. They will have to take a regulatory role. The ability of the

Reserve Bank to target the repo rates will be unaffected hence not interfering with the monetary

policy which will remain effective in the cashless society. Measures such as open market

operations, reserve requirements and liquidity ratios will be used to control inflations.

The increase in profitability

The cashless mode of transactions characterized by the use of credit card, ATM card, telephonic

and electronic transfer of funds, internet and mobile banking has seen the increase in profitability

for the organizations and banks at large (Gruen, 2015, p. 206).. The banks who introduced the

ATM early have a high market share as people joined these banks due to the conveniences in

accesses the services provided by the banks. It gave the banks competitive advantages due to

low-cost reduction and increased profits. The cashless banking has also lead to increased

efficiency in operations by increasing revenue and cost reduction (Bagnall & Flood 2011, p.57)

A study done by the MasterCard showed that Australians regard your business negatively if your

only method of payment is cash (Balnaves, 2012, p. 138).

The introduction of the e-banking and reduction in the traditional measure such as market share

and bank size let to increased profitability. The use of cashless banking system significantly

increases the profitability of the banking industries (Al-Smadi & Al-Wabel 2011, p. 6). The

internet-based transactions have few costs and increase the profits. The cashless banking system

increases the flow of deposits as people deposit the cash they have to access the money through

card or internet or mobile transfers. The traditional way where most operations took place

through cash exchange saw many people store their cash and use them during transactions. The

The Reserve Bank will most likely revise its role in the cashless society in the cases of the

transaction in the cashless society. They will have to take a regulatory role. The ability of the

Reserve Bank to target the repo rates will be unaffected hence not interfering with the monetary

policy which will remain effective in the cashless society. Measures such as open market

operations, reserve requirements and liquidity ratios will be used to control inflations.

The increase in profitability

The cashless mode of transactions characterized by the use of credit card, ATM card, telephonic

and electronic transfer of funds, internet and mobile banking has seen the increase in profitability

for the organizations and banks at large (Gruen, 2015, p. 206).. The banks who introduced the

ATM early have a high market share as people joined these banks due to the conveniences in

accesses the services provided by the banks. It gave the banks competitive advantages due to

low-cost reduction and increased profits. The cashless banking has also lead to increased

efficiency in operations by increasing revenue and cost reduction (Bagnall & Flood 2011, p.57)

A study done by the MasterCard showed that Australians regard your business negatively if your

only method of payment is cash (Balnaves, 2012, p. 138).

The introduction of the e-banking and reduction in the traditional measure such as market share

and bank size let to increased profitability. The use of cashless banking system significantly

increases the profitability of the banking industries (Al-Smadi & Al-Wabel 2011, p. 6). The

internet-based transactions have few costs and increase the profits. The cashless banking system

increases the flow of deposits as people deposit the cash they have to access the money through

card or internet or mobile transfers. The traditional way where most operations took place

through cash exchange saw many people store their cash and use them during transactions. The

Impact of Cashless Banking in Australia 12

increase in the flow of money also increases profitability to the banks (Valadkhani, Anwar &

Arjomandi 2014, p. 56) The use of phone banking and ATMs has improved the efficiency of the

banks too. It has also enabled customers to access information on their accounts and the products

and services the banks are offering to increase the marketing rates for banks at low costs. Most of

the expenses involved in cashless transactions reduce over the time and the banks only make

profits (Meredith, Kenney & Hatzvi 2014, p. 46).

Growth of the Business

The use of cashless banking system has also led to the growth of businesses. There is a flow of

money and easy access for purchasing services as one can transact over the phone or internet and

get the product without making withdrawals at the banks (Schwartz, Fabo, Bailey & Carter 2012

p. 92). Businesses are also able to gather information on the habits of purchase of their

customers. Leading to increased support to customers and understanding their consumer

behavior. Most consumers/customers in Australia already prefer the use of the cashless system

and a good percentage is already using the cashless financial system to make purchases and

different transactions.

The investment by banks in the cashless banking services to their conveniences at low possible

costs has ensured profitability for the banking industries. The cashless innovations aim at

providing the banking services to customers without cash (Fox, Liu & Martz 2016, p. 8). The

increase in this services leads to increase profitability for the banks as it reduces the use of

resources and time spent in handling cash. Hence profitability increases for the banking industry

in the introduction of the cashless banking system. The reduction in operation cost leads to the

increase in the flow of money also increases profitability to the banks (Valadkhani, Anwar &

Arjomandi 2014, p. 56) The use of phone banking and ATMs has improved the efficiency of the

banks too. It has also enabled customers to access information on their accounts and the products

and services the banks are offering to increase the marketing rates for banks at low costs. Most of

the expenses involved in cashless transactions reduce over the time and the banks only make

profits (Meredith, Kenney & Hatzvi 2014, p. 46).

Growth of the Business

The use of cashless banking system has also led to the growth of businesses. There is a flow of

money and easy access for purchasing services as one can transact over the phone or internet and

get the product without making withdrawals at the banks (Schwartz, Fabo, Bailey & Carter 2012

p. 92). Businesses are also able to gather information on the habits of purchase of their

customers. Leading to increased support to customers and understanding their consumer

behavior. Most consumers/customers in Australia already prefer the use of the cashless system

and a good percentage is already using the cashless financial system to make purchases and

different transactions.

The investment by banks in the cashless banking services to their conveniences at low possible

costs has ensured profitability for the banking industries. The cashless innovations aim at

providing the banking services to customers without cash (Fox, Liu & Martz 2016, p. 8). The

increase in this services leads to increase profitability for the banks as it reduces the use of

resources and time spent in handling cash. Hence profitability increases for the banking industry

in the introduction of the cashless banking system. The reduction in operation cost leads to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.