Analysis of Management Accounting at Caunton Engineering Limited

VerifiedAdded on 2021/02/21

|19

|5822

|47

Report

AI Summary

This report delves into the realm of management accounting, exploring its systems, techniques, and planning tools within the context of Caunton Engineering Limited, a prominent UK steelwork engineering firm. The report commences with an introduction to management accounting, emphasizing its role in decision-making through the provision of relevant financial and non-financial information. It then examines various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, highlighting their applications within Caunton Engineering. Furthermore, the report analyzes management accounting reports such as accounts receivable reports, budget reports, inventory management reports, and performance reports, assessing their advantages and disadvantages. The evaluation of integration of the system and reporting of management accounting with the process of the company is also included. The report explores the application of planning tools for effective budgetary control and their role in preparing budgets. It compares how organizations use management accounting systems to address financial problems and emphasizes the importance of responding to organizational and financial issues for achieving sustainable success. The report concludes with an evaluation of planning tools for responding to financial problems.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

FIRST ACTIVITY...........................................................................................................................1

Management accounting systems:...................................................................................................1

Management Accounting Reports:.........................................................................................3

Evaluation of integration of system and reporting of management accounting with process of

company:................................................................................................................................5

Costs calculated using appropriate techniques of cost analysis to frame income statement:.6

Applicability of range of management accounting techniques:.............................................9

Interpretation of Income statement:........................................................................................9

SECOND ACTIVITY....................................................................................................................10

Description of application of planning tool used to establish effective budgetary control:. 10

Uses of planning tools in preparation of budgets:................................................................14

Comparison of manner by which organisations are using management accounting systems to

respond financial problems:.................................................................................................14

Responding to organisational and financial problems leads to sustainability in success:....16

Evaluating planning tools for responding to financial problems:........................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

FIRST ACTIVITY...........................................................................................................................1

Management accounting systems:...................................................................................................1

Management Accounting Reports:.........................................................................................3

Evaluation of integration of system and reporting of management accounting with process of

company:................................................................................................................................5

Costs calculated using appropriate techniques of cost analysis to frame income statement:.6

Applicability of range of management accounting techniques:.............................................9

Interpretation of Income statement:........................................................................................9

SECOND ACTIVITY....................................................................................................................10

Description of application of planning tool used to establish effective budgetary control:. 10

Uses of planning tools in preparation of budgets:................................................................14

Comparison of manner by which organisations are using management accounting systems to

respond financial problems:.................................................................................................14

Responding to organisational and financial problems leads to sustainability in success:....16

Evaluating planning tools for responding to financial problems:........................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting term is combination of accounting and management.

Accounting implies to systematic classification and recording of quantitative aspects, whereas

management combines planning, control, organising things and making decisions. Management

accounting covers all aspects whether quantitative or qualitative with aim to provide reliable and

relevant results and information for taking momentous decisions (Lavia López and Hiebl, 2014).

Managers are responsible for effective implementation and adoption of systems of management

accounting. This report helps to enhance the understanding of management accounting and its

different aspects. This report explains management accounting systems, techniques and planning

tools to respond financial problems in context of engineering company named “Caunton

Engineering Limited”. It is leading steelwork engineering company of UK. Company is famous

for its fabrication quality, best designs and structural steelwork. It has approx. more than 41

years’ experience in this industry and providing services and support to real estate and

construction companies.

FIRST ACTIVITY

Management accounting systems:

Management accounting: It is process that consisted elaborated planning regarding the

crucial financial business action and overall management performance in state to analyse,

monitor, control the business affairs so that productivity and profitability can be increased. It is

basically a simple process that facilitates to the management of the company in decision making

process by providing the general business records and financial transaction (Hopper and Bui,

2016). Management accounting is combination of two aspect accounting and management, as it

considers business systems that combines all the financial and non monetary components.

Management accounting system: Management accounting systems mentioned that

systematic usage of the business accounting transaction and information in order to generate the

financial statement with accuracy so that they can make the decision regarding long term objects

and defined organisational policies or regulation. These system of the management accounting

are the elementary business exercise that is significant for the development of the goods and

service providing industry. These sort of management accounting system that are prepared by the

head of the individual business section and suggested to the management of the company so that

1

Management accounting term is combination of accounting and management.

Accounting implies to systematic classification and recording of quantitative aspects, whereas

management combines planning, control, organising things and making decisions. Management

accounting covers all aspects whether quantitative or qualitative with aim to provide reliable and

relevant results and information for taking momentous decisions (Lavia López and Hiebl, 2014).

Managers are responsible for effective implementation and adoption of systems of management

accounting. This report helps to enhance the understanding of management accounting and its

different aspects. This report explains management accounting systems, techniques and planning

tools to respond financial problems in context of engineering company named “Caunton

Engineering Limited”. It is leading steelwork engineering company of UK. Company is famous

for its fabrication quality, best designs and structural steelwork. It has approx. more than 41

years’ experience in this industry and providing services and support to real estate and

construction companies.

FIRST ACTIVITY

Management accounting systems:

Management accounting: It is process that consisted elaborated planning regarding the

crucial financial business action and overall management performance in state to analyse,

monitor, control the business affairs so that productivity and profitability can be increased. It is

basically a simple process that facilitates to the management of the company in decision making

process by providing the general business records and financial transaction (Hopper and Bui,

2016). Management accounting is combination of two aspect accounting and management, as it

considers business systems that combines all the financial and non monetary components.

Management accounting system: Management accounting systems mentioned that

systematic usage of the business accounting transaction and information in order to generate the

financial statement with accuracy so that they can make the decision regarding long term objects

and defined organisational policies or regulation. These system of the management accounting

are the elementary business exercise that is significant for the development of the goods and

service providing industry. These sort of management accounting system that are prepared by the

head of the individual business section and suggested to the management of the company so that

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they can make daily business decision to run the business. Caunton Engineering Limited

formulate the business strategies in the short run to betterment of the organisation. Different type

of management accounting system are followed by the company in order to collect the business

information measure the business decision and financial growth. Some of them are described as

under:

Cost accounting system: It is detailed framework that is used in business to identify the

absolute cost of goods and services that are produced and provided to its respective customer.

This system is totally focused on the analysis and determines the cost and its techniques

(Wickramasinghe and Alawattage, 2012). In context to Caunton Engineering Limited,

management of the company use this system to assist the function and process of the production

cost to evaluating the cost like finishing, developing, designing and other process. This system

comprises of cost accounting techniques that are used by the company to determine the actual

cost of the designed goods and services with ascertaining the profit along with cost at assorted

degree of manufacture. With the help of this system, management can understand the cost

structure and cost process of the organisation so that they can make the business decision by

considering goals and objectives. This system also helpful in making the cost related strategies,

cost sheet structure and annual budget of the business.

Inventory management system: It is a process that consolidate application with

structure of production to assure the availability of stocked goods that comprises at different

level of processing raw material, work in progress and complete goods to further ensure their

availability at exact needs with predefined standard quality. It plays a pivotal role in deciding the

price tag of goods and services by assessing value of closing stock. Management of Caunton

Engineering Limited handles the broad range of its material and finished production of the steel

by influencing the amount of material. Company uses this method to control the cost of stores

material and better flow of the goods to help them in provide the standard goods and services.

There are different concepts to determines the value of goods such as FIFO, LIFO and weighted

average. For company this system is essential to manage its stocks and minimise excessive costs.

Job costing system: This system directed on allocating costs to categorized task and

batches. It assists to measure different activities and processes of business to improve the

efficiency and productivity. It describes as assigning total manufacturing cost over the particular

unit of output. It is cost accounting method that related to the manufacturing unit where

2

formulate the business strategies in the short run to betterment of the organisation. Different type

of management accounting system are followed by the company in order to collect the business

information measure the business decision and financial growth. Some of them are described as

under:

Cost accounting system: It is detailed framework that is used in business to identify the

absolute cost of goods and services that are produced and provided to its respective customer.

This system is totally focused on the analysis and determines the cost and its techniques

(Wickramasinghe and Alawattage, 2012). In context to Caunton Engineering Limited,

management of the company use this system to assist the function and process of the production

cost to evaluating the cost like finishing, developing, designing and other process. This system

comprises of cost accounting techniques that are used by the company to determine the actual

cost of the designed goods and services with ascertaining the profit along with cost at assorted

degree of manufacture. With the help of this system, management can understand the cost

structure and cost process of the organisation so that they can make the business decision by

considering goals and objectives. This system also helpful in making the cost related strategies,

cost sheet structure and annual budget of the business.

Inventory management system: It is a process that consolidate application with

structure of production to assure the availability of stocked goods that comprises at different

level of processing raw material, work in progress and complete goods to further ensure their

availability at exact needs with predefined standard quality. It plays a pivotal role in deciding the

price tag of goods and services by assessing value of closing stock. Management of Caunton

Engineering Limited handles the broad range of its material and finished production of the steel

by influencing the amount of material. Company uses this method to control the cost of stores

material and better flow of the goods to help them in provide the standard goods and services.

There are different concepts to determines the value of goods such as FIFO, LIFO and weighted

average. For company this system is essential to manage its stocks and minimise excessive costs.

Job costing system: This system directed on allocating costs to categorized task and

batches. It assists to measure different activities and processes of business to improve the

efficiency and productivity. It describes as assigning total manufacturing cost over the particular

unit of output. It is cost accounting method that related to the manufacturing unit where

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production is normally estimating on number of completed process and projects (Plumb and

et.al., 2017). Caunton Engineering Limited use this system to evaluate the total production costs

in a pre-arranged manner by dividing it under direct material, direct labour and expenses costs by

individually estimating its actual cost. Company can use this system to assess cost of its specific

products by considering it a specific job. Company can use some other techniques of the cost to

evaluate the production like process costing, batch costing.

Price optimisation system: It is practical approaches where an administrator can

ascertain that how costumers will respond to different costs of product and services by definite

channels. Companies can shape their prices and markets of goods and services by applying this

method. This system focus on the measuring the goods prices by shrinking the price in order to

control the current profit ratio. Caunton Engineering Limited is analysing the different price

strategies in order to decide the price tag of the goods and services so that they can dwindle the

competitor in the market. This system measures the factor which leads to increase in price of

goods. With the help of this system modification in price of product and services must match the

requirement of the business organisation objects.

Management Accounting Reports:

Management accounting reporting: It is process that concern about aggregation of

business information and structured data by management of an organisation in order to make

operational decisions. These are periodic reports that consider different types of business

decision taken by head of units and furnish the all basic detail to enterprise management. In the

Caunton Engineering Limited, management reporting is key activity where a numerous kind of

information is transmitted to top management for taking enterprise related decisions. Following

are the reports that are yield by the management, as described below:

Account receivable reports: This is a collection report that is generated by those

industries which are commercially dealing with the customer on credit basis. This report shows

how much amount yet to be received from the debtors and provides the detail summary

regarding the due amount from the customers. Caunton Engineering Limited's management

prepares this report to track the sum of outstanding amount from its clients, interest on overdue

payment, expected amount receivable, provisions for bad debts and other basic detail about the

customers. It is beneficial for the company as it may help to tighten up the credit policy by

examine outstanding amount from debtors.

3

et.al., 2017). Caunton Engineering Limited use this system to evaluate the total production costs

in a pre-arranged manner by dividing it under direct material, direct labour and expenses costs by

individually estimating its actual cost. Company can use this system to assess cost of its specific

products by considering it a specific job. Company can use some other techniques of the cost to

evaluate the production like process costing, batch costing.

Price optimisation system: It is practical approaches where an administrator can

ascertain that how costumers will respond to different costs of product and services by definite

channels. Companies can shape their prices and markets of goods and services by applying this

method. This system focus on the measuring the goods prices by shrinking the price in order to

control the current profit ratio. Caunton Engineering Limited is analysing the different price

strategies in order to decide the price tag of the goods and services so that they can dwindle the

competitor in the market. This system measures the factor which leads to increase in price of

goods. With the help of this system modification in price of product and services must match the

requirement of the business organisation objects.

Management Accounting Reports:

Management accounting reporting: It is process that concern about aggregation of

business information and structured data by management of an organisation in order to make

operational decisions. These are periodic reports that consider different types of business

decision taken by head of units and furnish the all basic detail to enterprise management. In the

Caunton Engineering Limited, management reporting is key activity where a numerous kind of

information is transmitted to top management for taking enterprise related decisions. Following

are the reports that are yield by the management, as described below:

Account receivable reports: This is a collection report that is generated by those

industries which are commercially dealing with the customer on credit basis. This report shows

how much amount yet to be received from the debtors and provides the detail summary

regarding the due amount from the customers. Caunton Engineering Limited's management

prepares this report to track the sum of outstanding amount from its clients, interest on overdue

payment, expected amount receivable, provisions for bad debts and other basic detail about the

customers. It is beneficial for the company as it may help to tighten up the credit policy by

examine outstanding amount from debtors.

3

Budget report: This report is the fundamental report of a company that created to

compare projected standard data with actual performance of the enterprises. It is an internal

representation that is mainly used by the managers in order to assess that business is able to meet

its objectives and goal (Hilton and Platt, 2013). In Caunton Engineering Limited, internal

shareholder of the company determines the particular reports to analyses deviation in the

budgeted data and actual result in order to make proper decision in the firm. If the result displays

more difference, it requires to take fast action against those business activities that are not

fulfilling the need of managers regarding to make some suitable decision. So that they can able

to cover the difference the result for the betterment of the organization.

Inventory management Report: This report discloses that real time inward and outward

of the inventory during the financial year in a manufacturing unit. This report leads the actual

output of the production, inward material at stores, inventory details and its level. This report

alleviates in tracking and supervising various type of stocks to assess the stock movement from

the center of the warehouse and its requirement to make product. Caunton Engineering Limited

created this report on monthly basis to track the real time assessment of movement of the goods

at the manufacturing stores. This management report helps in decision making process regarding

to valuation of stock at the end of the year. There are the several methods for valuation of the

inventory like weighted average method, LIFO and FIFO to determination the value of the

closing inventory.

Performance Report: The key concept for producing this report is assessment of

individual performance of labours or employees together with overall performance of the

organisation. Management can use this report to setup crucial regulation, standard, measurements

and targets and make a comparison with actual and previous performance of organisation by

improving efficiency of employees. In this report, manager of the Caunton Engineering Limited

targets to financial goals that required to be complete in the financial year. Employee skill

development programs are conducted by managers in order to develop the skill and abilities of

inefficient employees and efficient employees are honoured. Company can measure the Market

acknowledgment by maintaining report. It beneficial for the organization in order to provide the

guidance to the managers to analyzing that enterprises are performing well or not in the

engineering sector.

Analysis of advantages and disadvantages of management accounting systems and applications:

4

compare projected standard data with actual performance of the enterprises. It is an internal

representation that is mainly used by the managers in order to assess that business is able to meet

its objectives and goal (Hilton and Platt, 2013). In Caunton Engineering Limited, internal

shareholder of the company determines the particular reports to analyses deviation in the

budgeted data and actual result in order to make proper decision in the firm. If the result displays

more difference, it requires to take fast action against those business activities that are not

fulfilling the need of managers regarding to make some suitable decision. So that they can able

to cover the difference the result for the betterment of the organization.

Inventory management Report: This report discloses that real time inward and outward

of the inventory during the financial year in a manufacturing unit. This report leads the actual

output of the production, inward material at stores, inventory details and its level. This report

alleviates in tracking and supervising various type of stocks to assess the stock movement from

the center of the warehouse and its requirement to make product. Caunton Engineering Limited

created this report on monthly basis to track the real time assessment of movement of the goods

at the manufacturing stores. This management report helps in decision making process regarding

to valuation of stock at the end of the year. There are the several methods for valuation of the

inventory like weighted average method, LIFO and FIFO to determination the value of the

closing inventory.

Performance Report: The key concept for producing this report is assessment of

individual performance of labours or employees together with overall performance of the

organisation. Management can use this report to setup crucial regulation, standard, measurements

and targets and make a comparison with actual and previous performance of organisation by

improving efficiency of employees. In this report, manager of the Caunton Engineering Limited

targets to financial goals that required to be complete in the financial year. Employee skill

development programs are conducted by managers in order to develop the skill and abilities of

inefficient employees and efficient employees are honoured. Company can measure the Market

acknowledgment by maintaining report. It beneficial for the organization in order to provide the

guidance to the managers to analyzing that enterprises are performing well or not in the

engineering sector.

Analysis of advantages and disadvantages of management accounting systems and applications:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

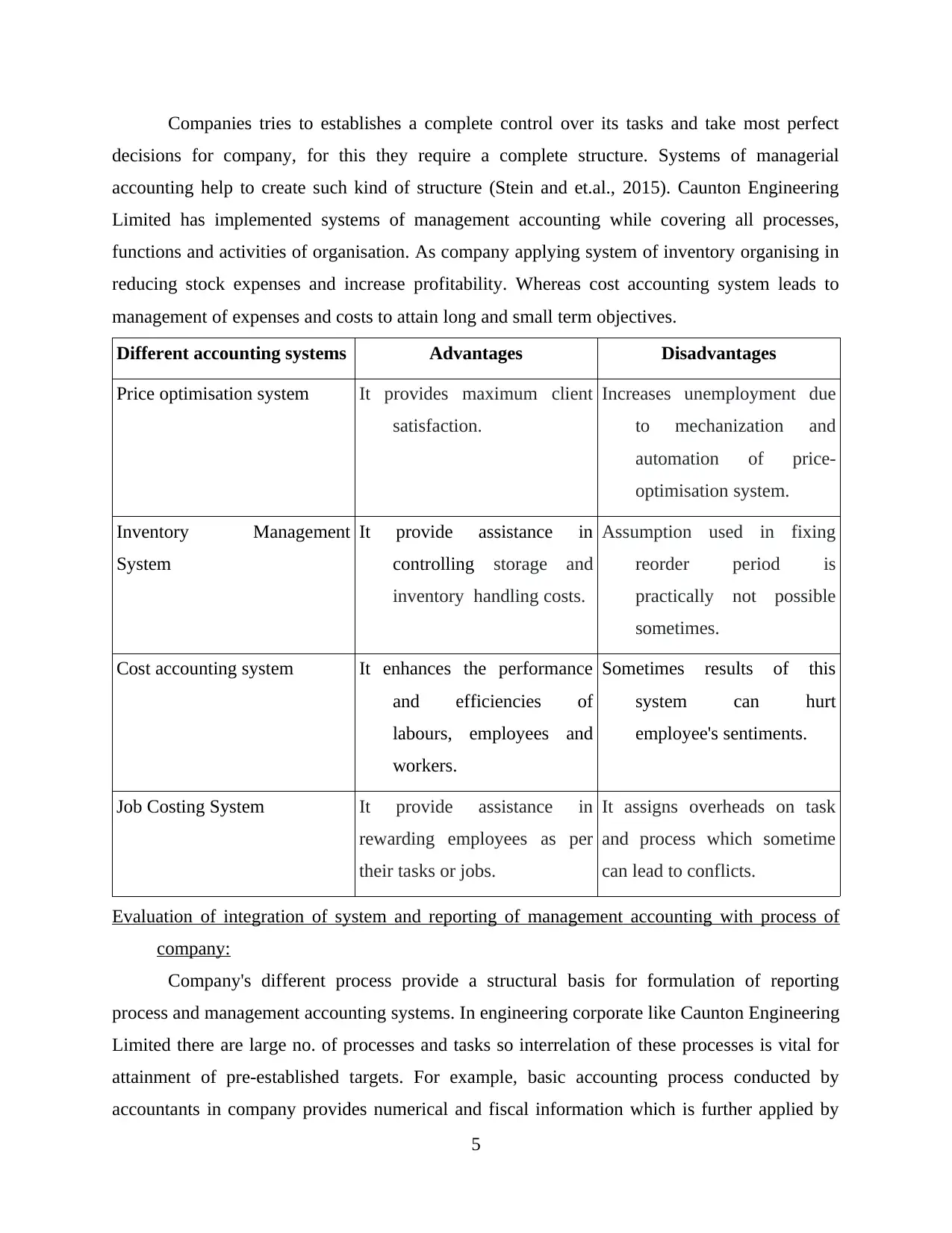

Companies tries to establishes a complete control over its tasks and take most perfect

decisions for company, for this they require a complete structure. Systems of managerial

accounting help to create such kind of structure (Stein and et.al., 2015). Caunton Engineering

Limited has implemented systems of management accounting while covering all processes,

functions and activities of organisation. As company applying system of inventory organising in

reducing stock expenses and increase profitability. Whereas cost accounting system leads to

management of expenses and costs to attain long and small term objectives.

Different accounting systems Advantages Disadvantages

Price optimisation system It provides maximum client

satisfaction.

Increases unemployment due

to mechanization and

automation of price-

optimisation system.

Inventory Management

System

It provide assistance in

controlling storage and

inventory handling costs.

Assumption used in fixing

reorder period is

practically not possible

sometimes.

Cost accounting system It enhances the performance

and efficiencies of

labours, employees and

workers.

Sometimes results of this

system can hurt

employee's sentiments.

Job Costing System It provide assistance in

rewarding employees as per

their tasks or jobs.

It assigns overheads on task

and process which sometime

can lead to conflicts.

Evaluation of integration of system and reporting of management accounting with process of

company:

Company's different process provide a structural basis for formulation of reporting

process and management accounting systems. In engineering corporate like Caunton Engineering

Limited there are large no. of processes and tasks so interrelation of these processes is vital for

attainment of pre-established targets. For example, basic accounting process conducted by

accountants in company provides numerical and fiscal information which is further applied by

5

decisions for company, for this they require a complete structure. Systems of managerial

accounting help to create such kind of structure (Stein and et.al., 2015). Caunton Engineering

Limited has implemented systems of management accounting while covering all processes,

functions and activities of organisation. As company applying system of inventory organising in

reducing stock expenses and increase profitability. Whereas cost accounting system leads to

management of expenses and costs to attain long and small term objectives.

Different accounting systems Advantages Disadvantages

Price optimisation system It provides maximum client

satisfaction.

Increases unemployment due

to mechanization and

automation of price-

optimisation system.

Inventory Management

System

It provide assistance in

controlling storage and

inventory handling costs.

Assumption used in fixing

reorder period is

practically not possible

sometimes.

Cost accounting system It enhances the performance

and efficiencies of

labours, employees and

workers.

Sometimes results of this

system can hurt

employee's sentiments.

Job Costing System It provide assistance in

rewarding employees as per

their tasks or jobs.

It assigns overheads on task

and process which sometime

can lead to conflicts.

Evaluation of integration of system and reporting of management accounting with process of

company:

Company's different process provide a structural basis for formulation of reporting

process and management accounting systems. In engineering corporate like Caunton Engineering

Limited there are large no. of processes and tasks so interrelation of these processes is vital for

attainment of pre-established targets. For example, basic accounting process conducted by

accountants in company provides numerical and fiscal information which is further applied by

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

higher management for reporting and in systems of management accounting (Turban, Volonino

and Wood, 2015).

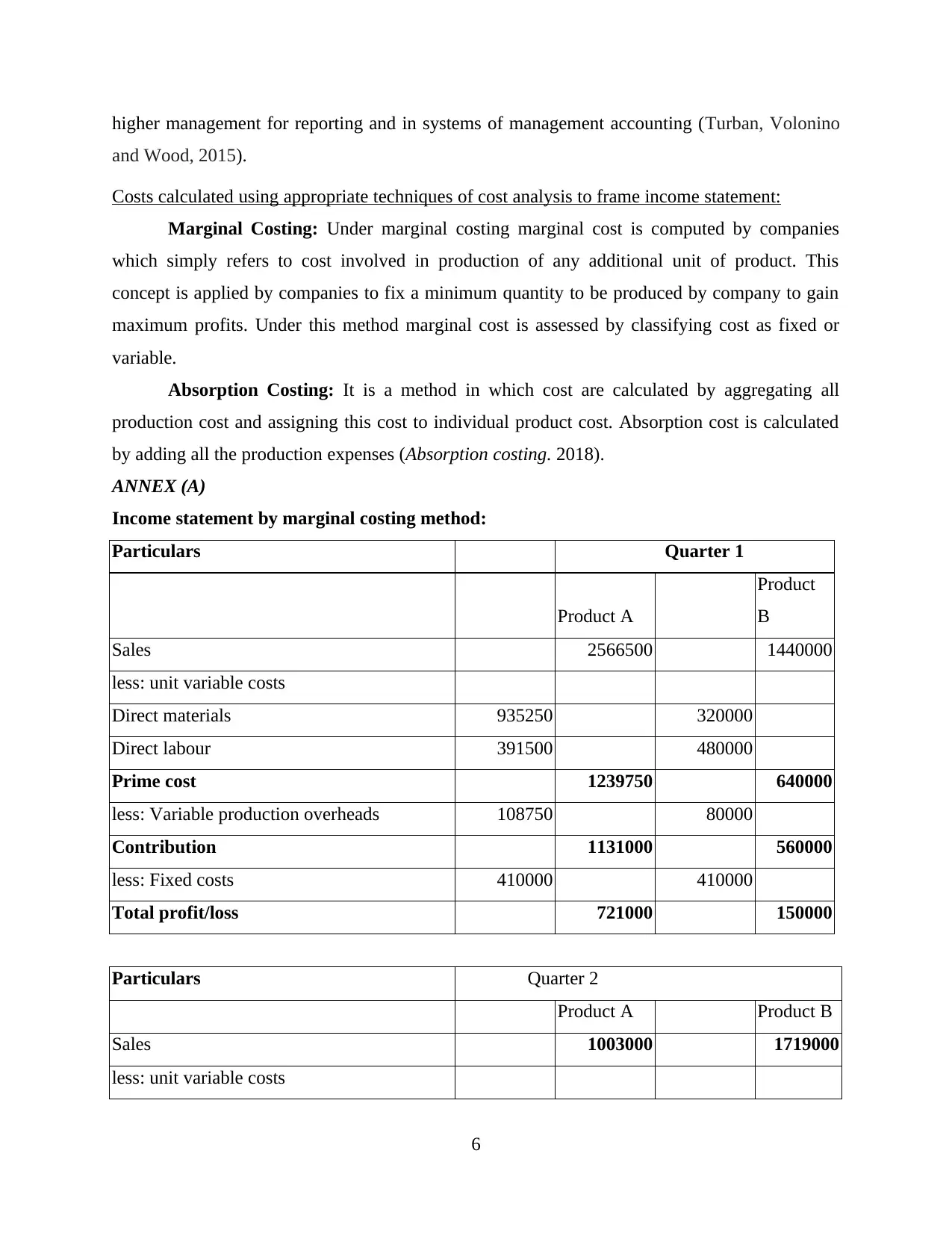

Costs calculated using appropriate techniques of cost analysis to frame income statement:

Marginal Costing: Under marginal costing marginal cost is computed by companies

which simply refers to cost involved in production of any additional unit of product. This

concept is applied by companies to fix a minimum quantity to be produced by company to gain

maximum profits. Under this method marginal cost is assessed by classifying cost as fixed or

variable.

Absorption Costing: It is a method in which cost are calculated by aggregating all

production cost and assigning this cost to individual product cost. Absorption cost is calculated

by adding all the production expenses (Absorption costing. 2018).

ANNEX (A)

Income statement by marginal costing method:

Particulars Quarter 1

Product A

Product

B

Sales 2566500 1440000

less: unit variable costs

Direct materials 935250 320000

Direct labour 391500 480000

Prime cost 1239750 640000

less: Variable production overheads 108750 80000

Contribution 1131000 560000

less: Fixed costs 410000 410000

Total profit/loss 721000 150000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: unit variable costs

6

and Wood, 2015).

Costs calculated using appropriate techniques of cost analysis to frame income statement:

Marginal Costing: Under marginal costing marginal cost is computed by companies

which simply refers to cost involved in production of any additional unit of product. This

concept is applied by companies to fix a minimum quantity to be produced by company to gain

maximum profits. Under this method marginal cost is assessed by classifying cost as fixed or

variable.

Absorption Costing: It is a method in which cost are calculated by aggregating all

production cost and assigning this cost to individual product cost. Absorption cost is calculated

by adding all the production expenses (Absorption costing. 2018).

ANNEX (A)

Income statement by marginal costing method:

Particulars Quarter 1

Product A

Product

B

Sales 2566500 1440000

less: unit variable costs

Direct materials 935250 320000

Direct labour 391500 480000

Prime cost 1239750 640000

less: Variable production overheads 108750 80000

Contribution 1131000 560000

less: Fixed costs 410000 410000

Total profit/loss 721000 150000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: unit variable costs

6

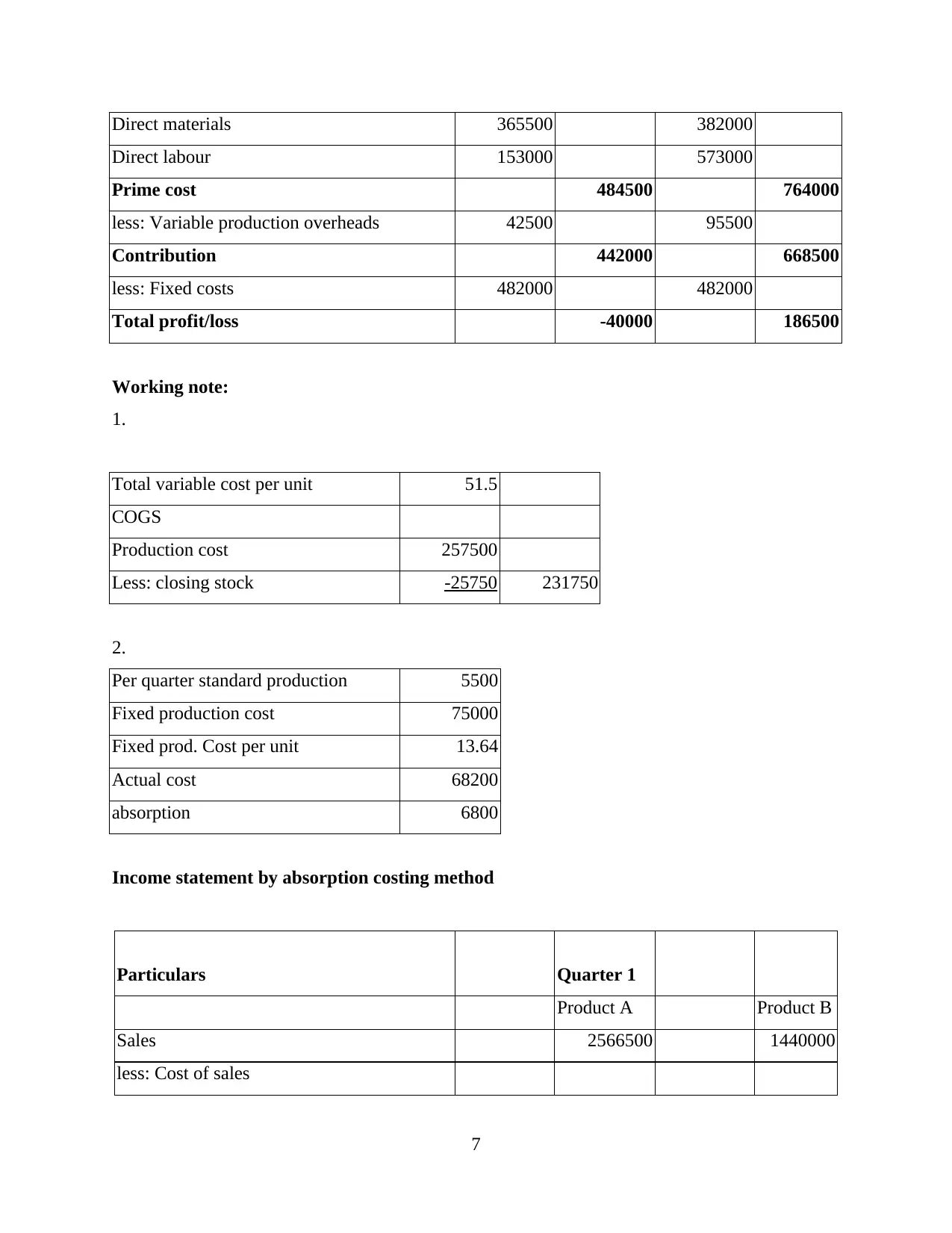

Direct materials 365500 382000

Direct labour 153000 573000

Prime cost 484500 764000

less: Variable production overheads 42500 95500

Contribution 442000 668500

less: Fixed costs 482000 482000

Total profit/loss -40000 186500

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method

Particulars Quarter 1

Product A Product B

Sales 2566500 1440000

less: Cost of sales

7

Direct labour 153000 573000

Prime cost 484500 764000

less: Variable production overheads 42500 95500

Contribution 442000 668500

less: Fixed costs 482000 482000

Total profit/loss -40000 186500

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method

Particulars Quarter 1

Product A Product B

Sales 2566500 1440000

less: Cost of sales

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

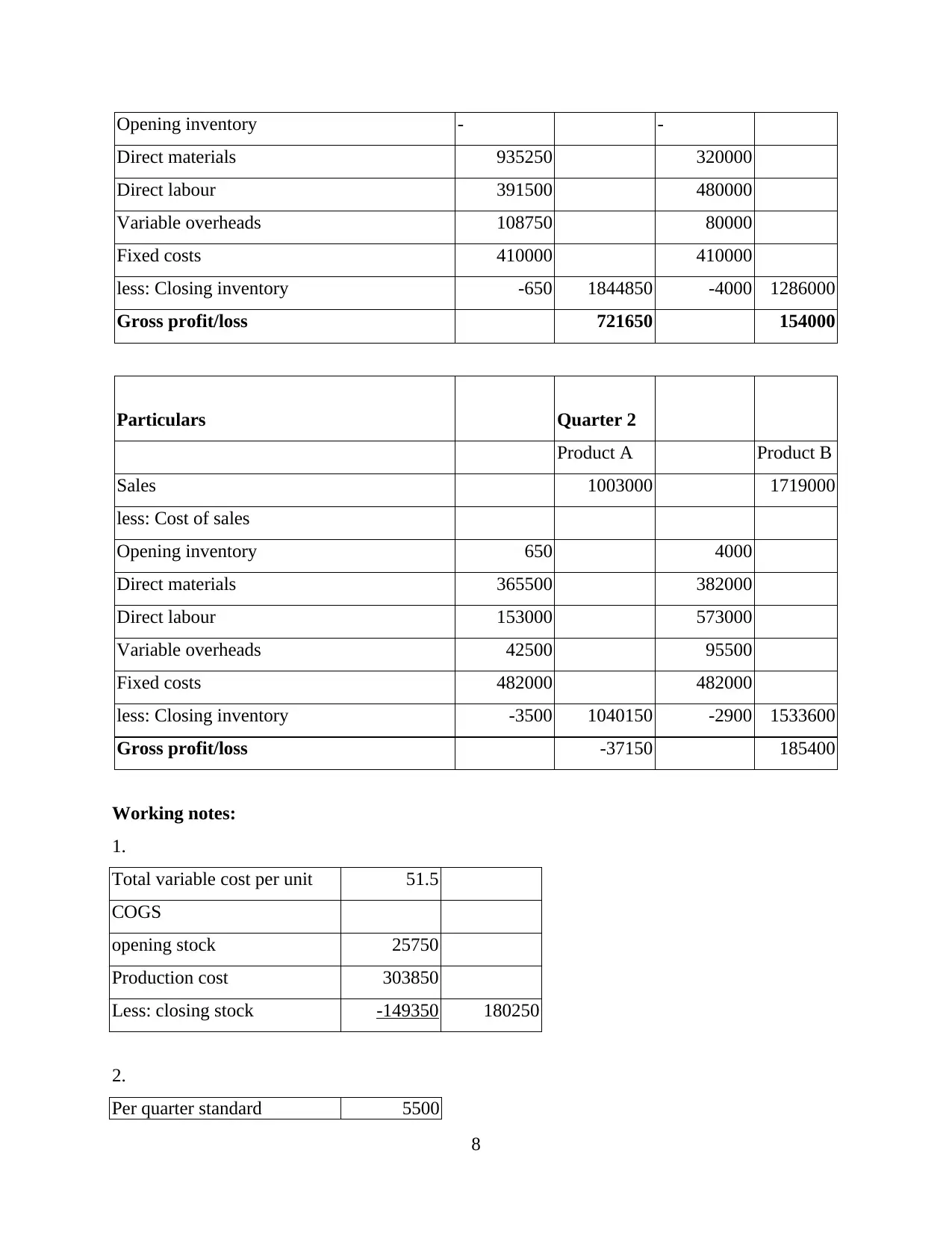

Opening inventory - -

Direct materials 935250 320000

Direct labour 391500 480000

Variable overheads 108750 80000

Fixed costs 410000 410000

less: Closing inventory -650 1844850 -4000 1286000

Gross profit/loss 721650 154000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: Cost of sales

Opening inventory 650 4000

Direct materials 365500 382000

Direct labour 153000 573000

Variable overheads 42500 95500

Fixed costs 482000 482000

less: Closing inventory -3500 1040150 -2900 1533600

Gross profit/loss -37150 185400

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard 5500

8

Direct materials 935250 320000

Direct labour 391500 480000

Variable overheads 108750 80000

Fixed costs 410000 410000

less: Closing inventory -650 1844850 -4000 1286000

Gross profit/loss 721650 154000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: Cost of sales

Opening inventory 650 4000

Direct materials 365500 382000

Direct labour 153000 573000

Variable overheads 42500 95500

Fixed costs 482000 482000

less: Closing inventory -3500 1040150 -2900 1533600

Gross profit/loss -37150 185400

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard 5500

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

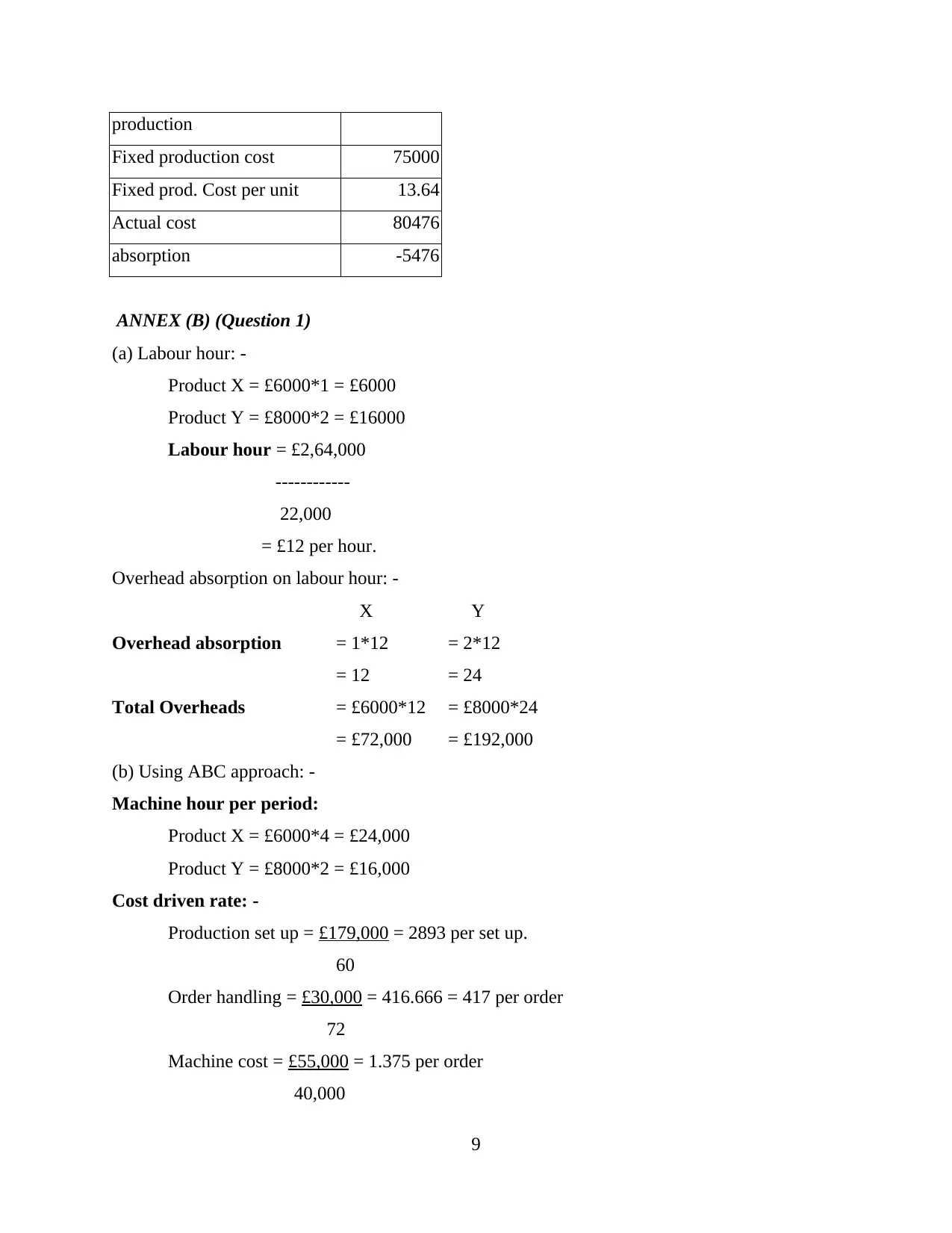

production

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B) (Question 1)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

9

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B) (Question 1)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

9

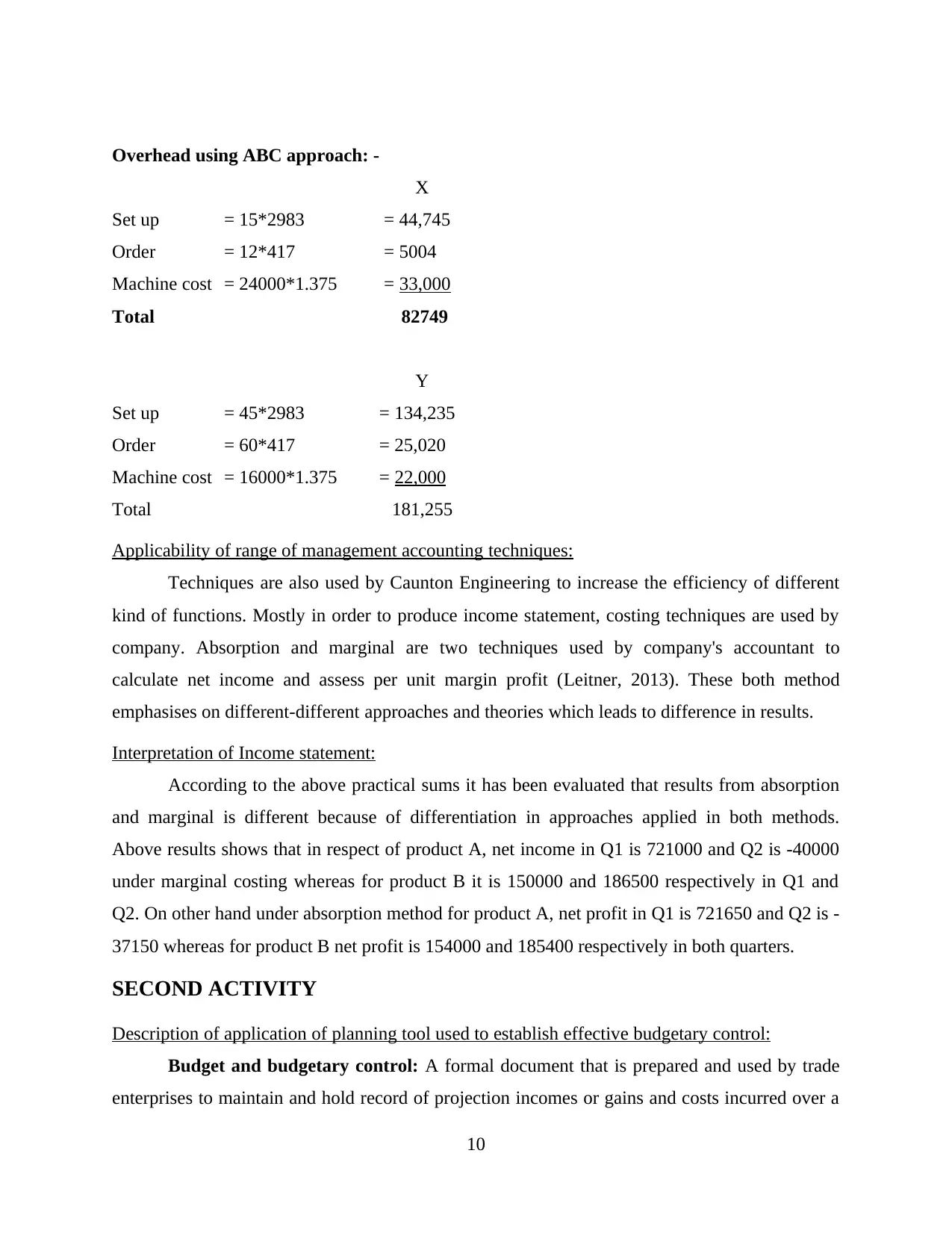

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Applicability of range of management accounting techniques:

Techniques are also used by Caunton Engineering to increase the efficiency of different

kind of functions. Mostly in order to produce income statement, costing techniques are used by

company. Absorption and marginal are two techniques used by company's accountant to

calculate net income and assess per unit margin profit (Leitner, 2013). These both method

emphasises on different-different approaches and theories which leads to difference in results.

Interpretation of Income statement:

According to the above practical sums it has been evaluated that results from absorption

and marginal is different because of differentiation in approaches applied in both methods.

Above results shows that in respect of product A, net income in Q1 is 721000 and Q2 is -40000

under marginal costing whereas for product B it is 150000 and 186500 respectively in Q1 and

Q2. On other hand under absorption method for product A, net profit in Q1 is 721650 and Q2 is -

37150 whereas for product B net profit is 154000 and 185400 respectively in both quarters.

SECOND ACTIVITY

Description of application of planning tool used to establish effective budgetary control:

Budget and budgetary control: A formal document that is prepared and used by trade

enterprises to maintain and hold record of projection incomes or gains and costs incurred over a

10

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Applicability of range of management accounting techniques:

Techniques are also used by Caunton Engineering to increase the efficiency of different

kind of functions. Mostly in order to produce income statement, costing techniques are used by

company. Absorption and marginal are two techniques used by company's accountant to

calculate net income and assess per unit margin profit (Leitner, 2013). These both method

emphasises on different-different approaches and theories which leads to difference in results.

Interpretation of Income statement:

According to the above practical sums it has been evaluated that results from absorption

and marginal is different because of differentiation in approaches applied in both methods.

Above results shows that in respect of product A, net income in Q1 is 721000 and Q2 is -40000

under marginal costing whereas for product B it is 150000 and 186500 respectively in Q1 and

Q2. On other hand under absorption method for product A, net profit in Q1 is 721650 and Q2 is -

37150 whereas for product B net profit is 154000 and 185400 respectively in both quarters.

SECOND ACTIVITY

Description of application of planning tool used to establish effective budgetary control:

Budget and budgetary control: A formal document that is prepared and used by trade

enterprises to maintain and hold record of projection incomes or gains and costs incurred over a

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.