Analysis & Change Management: CCIC's Agricultural Business in Europe

VerifiedAdded on 2023/06/14

|20

|4976

|74

Report

AI Summary

This report provides an analysis of CCIC's change management strategies for expanding its staple agricultural products business in Europe. It begins with a background of CCIC, highlighting its global presence and limited market share in the European port inspection market compared to competitors like SGS, BV, and Intertek. The analysis covers the status quo of the export market for staple agricultural products in Europe, focusing on key exporting countries such as Ukraine, France, Romania, and the Netherlands. It assesses CCIC's current situation in Europe regarding market promotion, customer exploitation, and core competitiveness, identifying challenges such as a lack of brand awareness, insufficient understanding of the local market, and unqualified inspectors. The report includes a business analysis of existing and potential customers, using COFCO as an example to illustrate the potential for business cooperation. A competitive analysis examines CCIC's position relative to its competitors and considers the bargaining power of suppliers and customers, as well as the threat of substitution. Finally, the report offers recommendations for improving CCIC's competitiveness and expanding its presence in the European agricultural products market.

Internal

CHANGE

MANAGEMENT

CHANGE

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

BACKGROUND OF CCIC........................................................................................2

INTRODUCTION...................................................................................................2

ANALYSIS............................................................................................................2

The status quo of the export market of staple agricultural products in Europe...................2

The current situation Analysis of CCIC in Europe......................................................5

Business analysis of existing and potential customers.................................................6

COMPETITIVE ANALYSIS OF CCIC.........................................................................9

The competitors:...............................................................................................9

Bargaining power of suppliers:...........................................................................10

Bargaining power of customers:..........................................................................11

Threat of substitution:.......................................................................................11

RECOMMENDATION...........................................................................................13

SUMMARY.........................................................................................................15

REFERENCES.....................................................................................................17

BACKGROUND OF CCIC........................................................................................2

INTRODUCTION...................................................................................................2

ANALYSIS............................................................................................................2

The status quo of the export market of staple agricultural products in Europe...................2

The current situation Analysis of CCIC in Europe......................................................5

Business analysis of existing and potential customers.................................................6

COMPETITIVE ANALYSIS OF CCIC.........................................................................9

The competitors:...............................................................................................9

Bargaining power of suppliers:...........................................................................10

Bargaining power of customers:..........................................................................11

Threat of substitution:.......................................................................................11

RECOMMENDATION...........................................................................................13

SUMMARY.........................................................................................................15

REFERENCES.....................................................................................................17

BACKGROUND OF CCIC

At present, the company I work for is a multinational inspection and certification

institution, which mainly serves the consulting of China's import and export trade,

inspection and testing of ports, food and milk powder, and so on. The company was

established in 1980 and had more than 40 years (Atkin and Brooks, 2021). There are

more than 40 companies in China, more than 300 branches and offices worldwide,

and the total number of employees is 25,000. In the EU region, we have 6 branches

companies, and the main business is government authorized business, such as

inspecting the second-hand machine and recycling raw materials.

Compared with the other international inspection companies and the competitors

in the same industry, such as SGS, BV, Intertek, our share market share of port

inspection in the European market is minimal.

Recently, the head office wants us to change the marketing strategy and direction

to develop more new business and improve our competitiveness. However, due to

lacking a deep understanding of the local business from the management team and

conservative management and decision-making model, business advancement is

relatively slow, and practical progress has not been achieved yet.

INTRODUCTION

CCIC has expanded many new businesses currently, and as a result, it can't be

stated one by one. Therefore, we would select and focus on the staple Agricultural

Products business development (Al-Haddad and Kotnour, 2015). Aligned with this

objective, we would collect and analyse the current market situation, competitiveness,

existing and potential customers. Finally, the related solution will be provided

according to this collected information and analysis.

At present, the company I work for is a multinational inspection and certification

institution, which mainly serves the consulting of China's import and export trade,

inspection and testing of ports, food and milk powder, and so on. The company was

established in 1980 and had more than 40 years (Atkin and Brooks, 2021). There are

more than 40 companies in China, more than 300 branches and offices worldwide,

and the total number of employees is 25,000. In the EU region, we have 6 branches

companies, and the main business is government authorized business, such as

inspecting the second-hand machine and recycling raw materials.

Compared with the other international inspection companies and the competitors

in the same industry, such as SGS, BV, Intertek, our share market share of port

inspection in the European market is minimal.

Recently, the head office wants us to change the marketing strategy and direction

to develop more new business and improve our competitiveness. However, due to

lacking a deep understanding of the local business from the management team and

conservative management and decision-making model, business advancement is

relatively slow, and practical progress has not been achieved yet.

INTRODUCTION

CCIC has expanded many new businesses currently, and as a result, it can't be

stated one by one. Therefore, we would select and focus on the staple Agricultural

Products business development (Al-Haddad and Kotnour, 2015). Aligned with this

objective, we would collect and analyse the current market situation, competitiveness,

existing and potential customers. Finally, the related solution will be provided

according to this collected information and analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

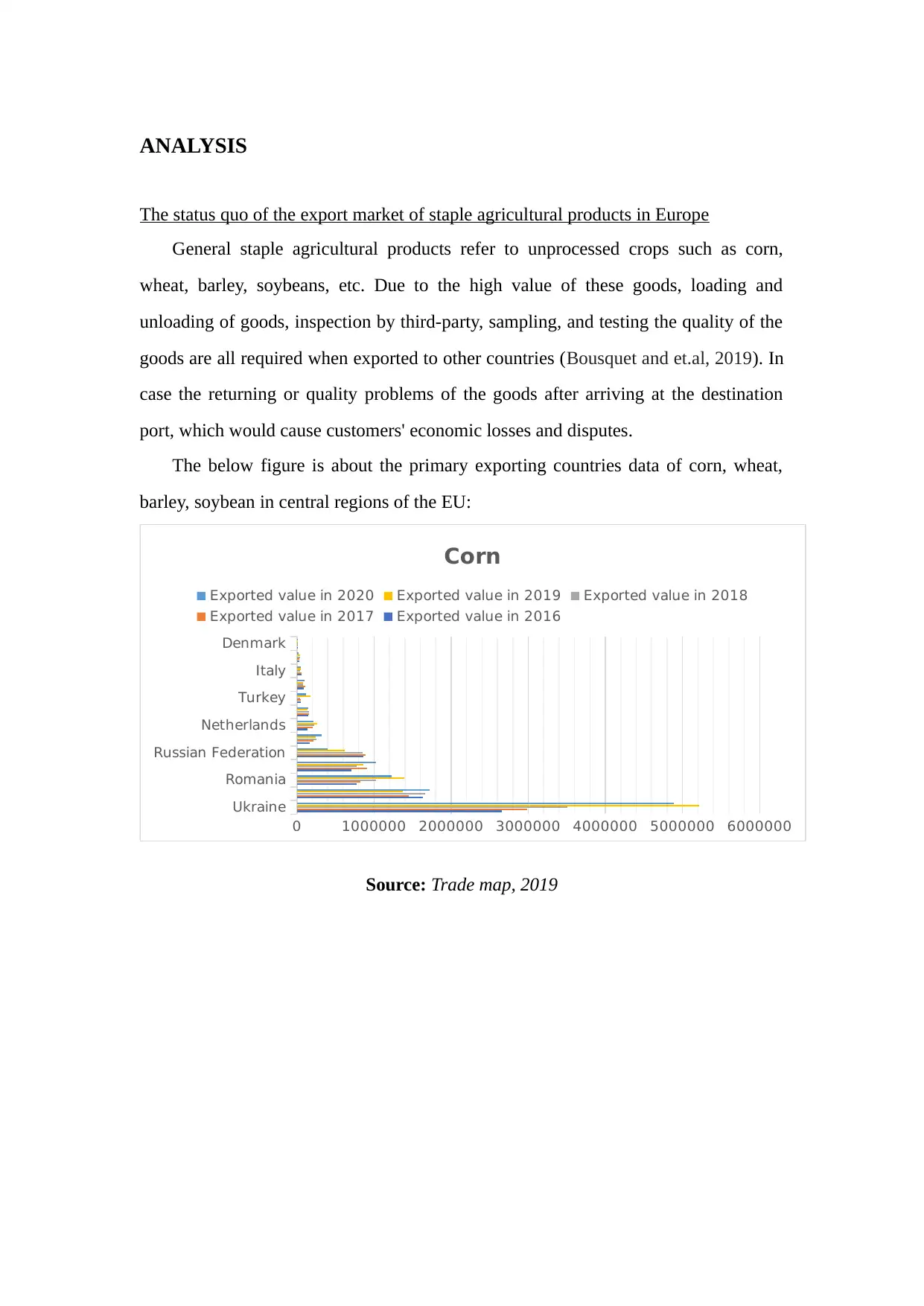

ANALYSIS

The status quo of the export market of staple agricultural products in Europe

General staple agricultural products refer to unprocessed crops such as corn,

wheat, barley, soybeans, etc. Due to the high value of these goods, loading and

unloading of goods, inspection by third-party, sampling, and testing the quality of the

goods are all required when exported to other countries (Bousquet and et.al, 2019). In

case the returning or quality problems of the goods after arriving at the destination

port, which would cause customers' economic losses and disputes.

The below figure is about the primary exporting countries data of corn, wheat,

barley, soybean in central regions of the EU:

Ukraine

Romania

Russian Federation

Netherlands

Turkey

Italy

Denmark

0 1000000 2000000 3000000 4000000 5000000 6000000

Corn

Exported value in 2020 Exported value in 2019 Exported value in 2018

Exported value in 2017 Exported value in 2016

Source: Trade map, 2019

The status quo of the export market of staple agricultural products in Europe

General staple agricultural products refer to unprocessed crops such as corn,

wheat, barley, soybeans, etc. Due to the high value of these goods, loading and

unloading of goods, inspection by third-party, sampling, and testing the quality of the

goods are all required when exported to other countries (Bousquet and et.al, 2019). In

case the returning or quality problems of the goods after arriving at the destination

port, which would cause customers' economic losses and disputes.

The below figure is about the primary exporting countries data of corn, wheat,

barley, soybean in central regions of the EU:

Ukraine

Romania

Russian Federation

Netherlands

Turkey

Italy

Denmark

0 1000000 2000000 3000000 4000000 5000000 6000000

Corn

Exported value in 2020 Exported value in 2019 Exported value in 2018

Exported value in 2017 Exported value in 2016

Source: Trade map, 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ukraine

Netherlands

Russian Federation

France

Romania

Belgium

Hungary

Germany

Italy

Moldova, Republic of

Portugal

Spain

Denmark

0

600000

1200000

Soya beans

Exported value in 2016 Exported value in 2017 Exported value in 2018

Exported value in 2019 Exported value in 2020

Source: Trade map, 2019

Russian Federation

Ukraine

Poland

Hungary

Denmark

Netherlands

Italy

0 2000000 4000000 6000000 8000000 10000000

Wheat

Exported value in 2020 Exported value in 2019 Exported value in 2018

Exported value in 2017 Exported value in 2016

Source: Trade map, 2019

Netherlands

Russian Federation

France

Romania

Belgium

Hungary

Germany

Italy

Moldova, Republic of

Portugal

Spain

Denmark

0

600000

1200000

Soya beans

Exported value in 2016 Exported value in 2017 Exported value in 2018

Exported value in 2019 Exported value in 2020

Source: Trade map, 2019

Russian Federation

Ukraine

Poland

Hungary

Denmark

Netherlands

Italy

0 2000000 4000000 6000000 8000000 10000000

Wheat

Exported value in 2020 Exported value in 2019 Exported value in 2018

Exported value in 2017 Exported value in 2016

Source: Trade map, 2019

France

Ukraine

Romania

Hungary

Finland

Netherlands

Portugal

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

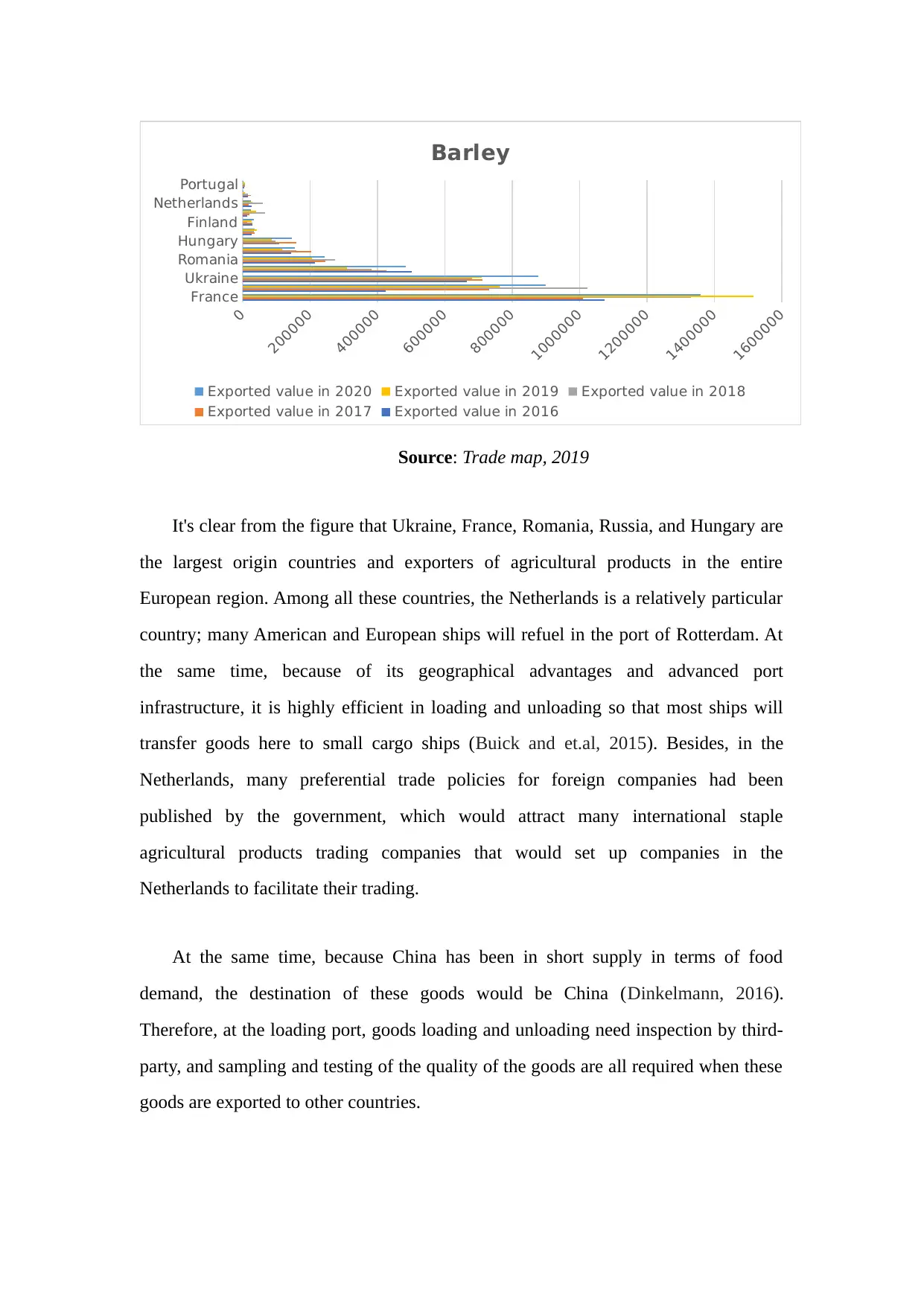

Barley

Exported value in 2020 Exported value in 2019 Exported value in 2018

Exported value in 2017 Exported value in 2016

Source: Trade map, 2019

It's clear from the figure that Ukraine, France, Romania, Russia, and Hungary are

the largest origin countries and exporters of agricultural products in the entire

European region. Among all these countries, the Netherlands is a relatively particular

country; many American and European ships will refuel in the port of Rotterdam. At

the same time, because of its geographical advantages and advanced port

infrastructure, it is highly efficient in loading and unloading so that most ships will

transfer goods here to small cargo ships (Buick and et.al, 2015). Besides, in the

Netherlands, many preferential trade policies for foreign companies had been

published by the government, which would attract many international staple

agricultural products trading companies that would set up companies in the

Netherlands to facilitate their trading.

At the same time, because China has been in short supply in terms of food

demand, the destination of these goods would be China (Dinkelmann, 2016).

Therefore, at the loading port, goods loading and unloading need inspection by third-

party, and sampling and testing of the quality of the goods are all required when these

goods are exported to other countries.

Ukraine

Romania

Hungary

Finland

Netherlands

Portugal

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

Barley

Exported value in 2020 Exported value in 2019 Exported value in 2018

Exported value in 2017 Exported value in 2016

Source: Trade map, 2019

It's clear from the figure that Ukraine, France, Romania, Russia, and Hungary are

the largest origin countries and exporters of agricultural products in the entire

European region. Among all these countries, the Netherlands is a relatively particular

country; many American and European ships will refuel in the port of Rotterdam. At

the same time, because of its geographical advantages and advanced port

infrastructure, it is highly efficient in loading and unloading so that most ships will

transfer goods here to small cargo ships (Buick and et.al, 2015). Besides, in the

Netherlands, many preferential trade policies for foreign companies had been

published by the government, which would attract many international staple

agricultural products trading companies that would set up companies in the

Netherlands to facilitate their trading.

At the same time, because China has been in short supply in terms of food

demand, the destination of these goods would be China (Dinkelmann, 2016).

Therefore, at the loading port, goods loading and unloading need inspection by third-

party, and sampling and testing of the quality of the goods are all required when these

goods are exported to other countries.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

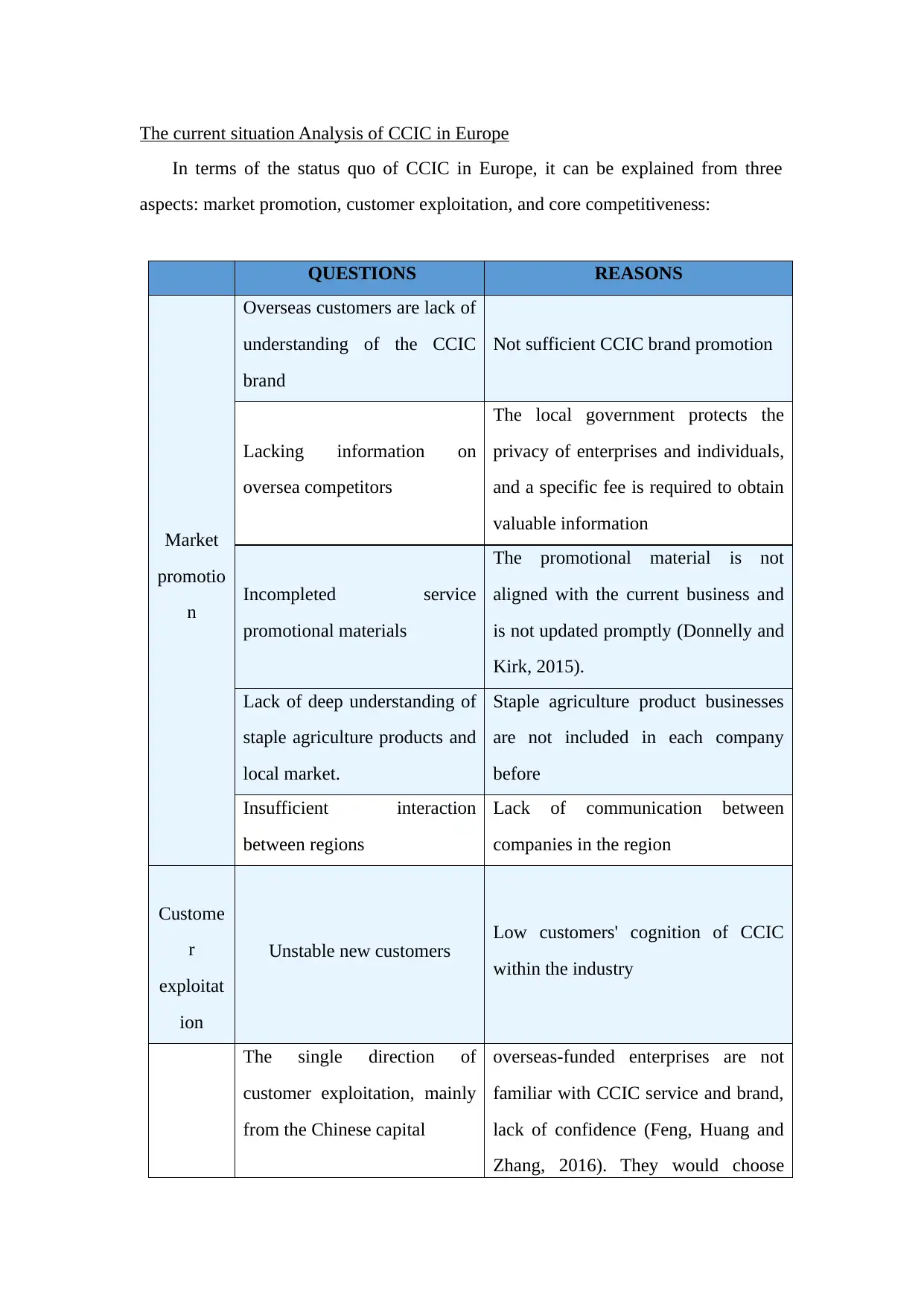

The current situation Analysis of CCIC in Europe

In terms of the status quo of CCIC in Europe, it can be explained from three

aspects: market promotion, customer exploitation, and core competitiveness:

QUESTIONS REASONS

Market

promotio

n

Overseas customers are lack of

understanding of the CCIC

brand

Not sufficient CCIC brand promotion

Lacking information on

oversea competitors

The local government protects the

privacy of enterprises and individuals,

and a specific fee is required to obtain

valuable information

Incompleted service

promotional materials

The promotional material is not

aligned with the current business and

is not updated promptly (Donnelly and

Kirk, 2015).

Lack of deep understanding of

staple agriculture products and

local market.

Staple agriculture product businesses

are not included in each company

before

Insufficient interaction

between regions

Lack of communication between

companies in the region

Custome

r

exploitat

ion

Unstable new customers Low customers' cognition of CCIC

within the industry

The single direction of

customer exploitation, mainly

from the Chinese capital

overseas-funded enterprises are not

familiar with CCIC service and brand,

lack of confidence (Feng, Huang and

Zhang, 2016). They would choose

In terms of the status quo of CCIC in Europe, it can be explained from three

aspects: market promotion, customer exploitation, and core competitiveness:

QUESTIONS REASONS

Market

promotio

n

Overseas customers are lack of

understanding of the CCIC

brand

Not sufficient CCIC brand promotion

Lacking information on

oversea competitors

The local government protects the

privacy of enterprises and individuals,

and a specific fee is required to obtain

valuable information

Incompleted service

promotional materials

The promotional material is not

aligned with the current business and

is not updated promptly (Donnelly and

Kirk, 2015).

Lack of deep understanding of

staple agriculture products and

local market.

Staple agriculture product businesses

are not included in each company

before

Insufficient interaction

between regions

Lack of communication between

companies in the region

Custome

r

exploitat

ion

Unstable new customers Low customers' cognition of CCIC

within the industry

The single direction of

customer exploitation, mainly

from the Chinese capital

overseas-funded enterprises are not

familiar with CCIC service and brand,

lack of confidence (Feng, Huang and

Zhang, 2016). They would choose

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SGS and BV as their leading service

provider at the very beginning.

Core

competit

ion

Unqualified inspector Lacking training for the inspectors, as

well as the field operation

Lack of lab No business that can support the

regular operation of the laboratory

Business analysis of existing and potential customers

Although it is said that the inspection business of staple agriculture products has

not achieved significant growth, the process from zero to one has been realized.

Taking COFCO as an example, COFCO, the primary customer, is now the top five-

grain trader globally. The main destination port of COFCO is China, but like the other

grain crop traders, they will also conduct some local grain procurement trade in

Europe (Hanna, 2016). The following part will mainly introduce its main business

distribution in the European, procurement quantity, procurement varieties, loading and

unloading ports, et al.;

Corn

3313611.

97, 69%

Wheat,

971000,

20%

Rapeseed

, 321700,

7%

Barly,

222000,

5%

Soya,550

0, 0.11%

provider at the very beginning.

Core

competit

ion

Unqualified inspector Lacking training for the inspectors, as

well as the field operation

Lack of lab No business that can support the

regular operation of the laboratory

Business analysis of existing and potential customers

Although it is said that the inspection business of staple agriculture products has

not achieved significant growth, the process from zero to one has been realized.

Taking COFCO as an example, COFCO, the primary customer, is now the top five-

grain trader globally. The main destination port of COFCO is China, but like the other

grain crop traders, they will also conduct some local grain procurement trade in

Europe (Hanna, 2016). The following part will mainly introduce its main business

distribution in the European, procurement quantity, procurement varieties, loading and

unloading ports, et al.;

Corn

3313611.

97, 69%

Wheat,

971000,

20%

Rapeseed

, 321700,

7%

Barly,

222000,

5%

Soya,550

0, 0.11%

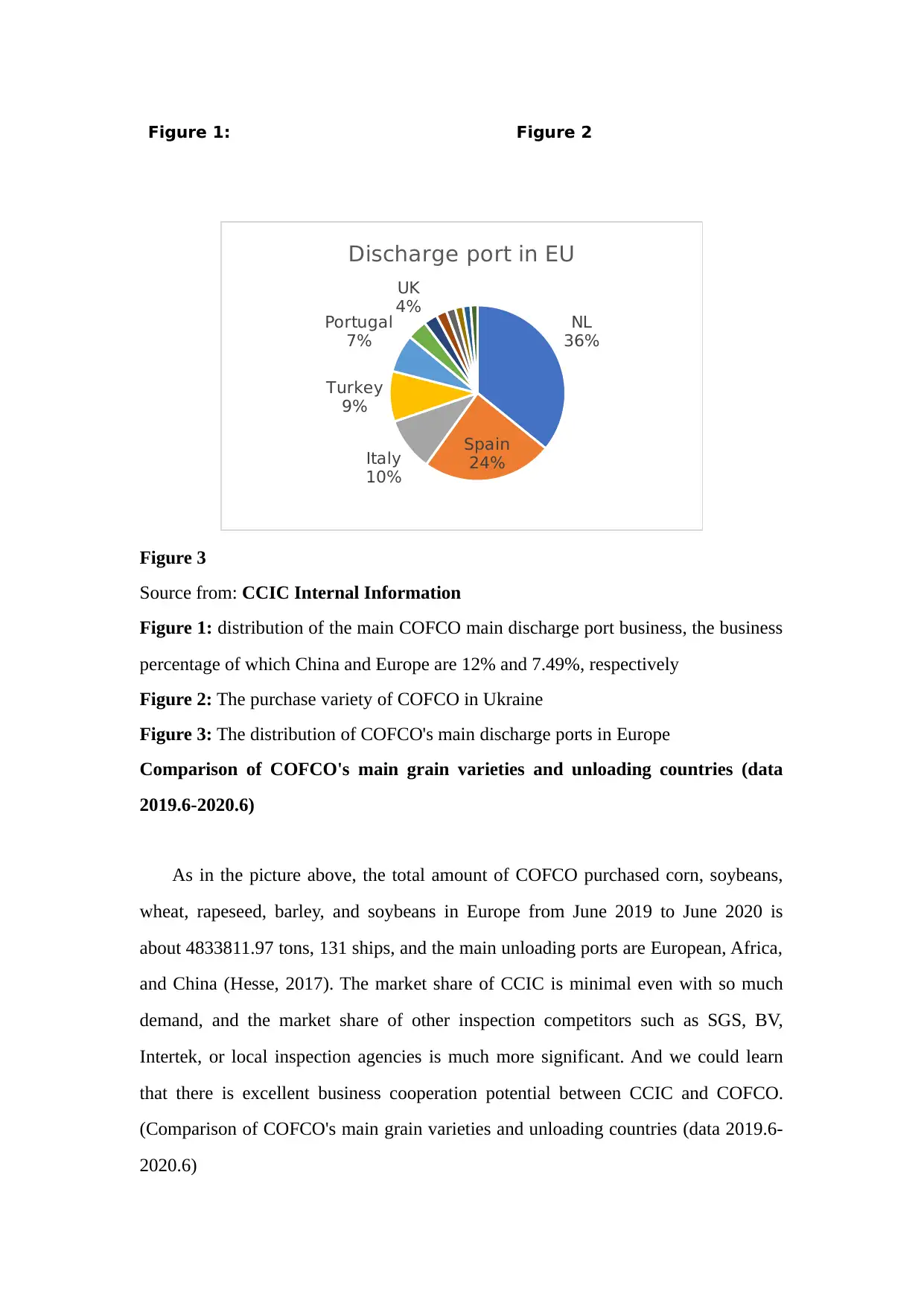

Figure 1: Figure 2

NL

36%

Spain

24%Italy

10%

Turkey

9%

Portugal

7%

UK

4%

Discharge port in EU

Figure 3

Source from: CCIC Internal Information

Figure 1: distribution of the main COFCO main discharge port business, the business

percentage of which China and Europe are 12% and 7.49%, respectively

Figure 2: The purchase variety of COFCO in Ukraine

Figure 3: The distribution of COFCO's main discharge ports in Europe

Comparison of COFCO's main grain varieties and unloading countries (data

2019.6-2020.6)

As in the picture above, the total amount of COFCO purchased corn, soybeans,

wheat, rapeseed, barley, and soybeans in Europe from June 2019 to June 2020 is

about 4833811.97 tons, 131 ships, and the main unloading ports are European, Africa,

and China (Hesse, 2017). The market share of CCIC is minimal even with so much

demand, and the market share of other inspection competitors such as SGS, BV,

Intertek, or local inspection agencies is much more significant. And we could learn

that there is excellent business cooperation potential between CCIC and COFCO.

(Comparison of COFCO's main grain varieties and unloading countries (data 2019.6-

2020.6)

NL

36%

Spain

24%Italy

10%

Turkey

9%

Portugal

7%

UK

4%

Discharge port in EU

Figure 3

Source from: CCIC Internal Information

Figure 1: distribution of the main COFCO main discharge port business, the business

percentage of which China and Europe are 12% and 7.49%, respectively

Figure 2: The purchase variety of COFCO in Ukraine

Figure 3: The distribution of COFCO's main discharge ports in Europe

Comparison of COFCO's main grain varieties and unloading countries (data

2019.6-2020.6)

As in the picture above, the total amount of COFCO purchased corn, soybeans,

wheat, rapeseed, barley, and soybeans in Europe from June 2019 to June 2020 is

about 4833811.97 tons, 131 ships, and the main unloading ports are European, Africa,

and China (Hesse, 2017). The market share of CCIC is minimal even with so much

demand, and the market share of other inspection competitors such as SGS, BV,

Intertek, or local inspection agencies is much more significant. And we could learn

that there is excellent business cooperation potential between CCIC and COFCO.

(Comparison of COFCO's main grain varieties and unloading countries (data 2019.6-

2020.6)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

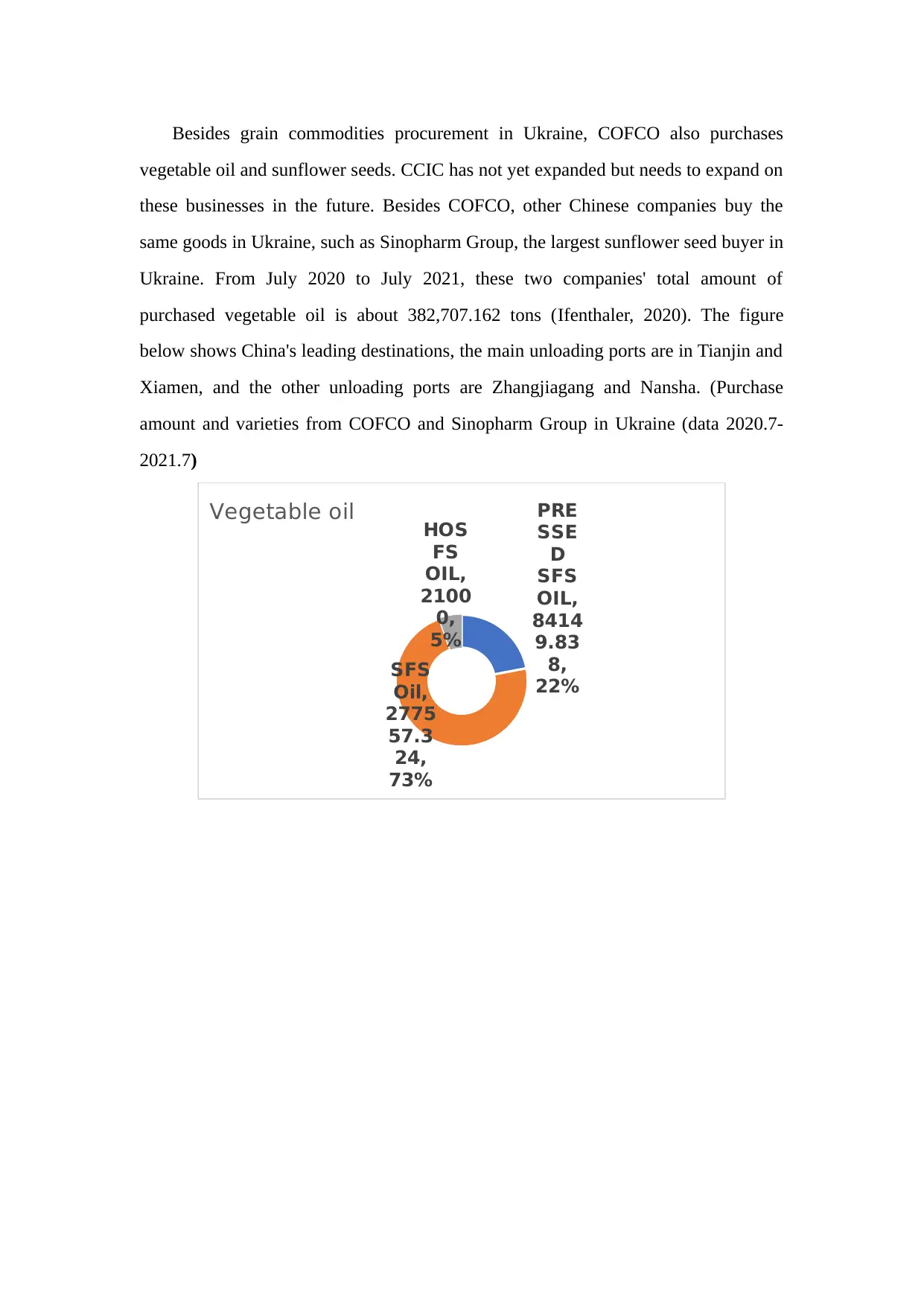

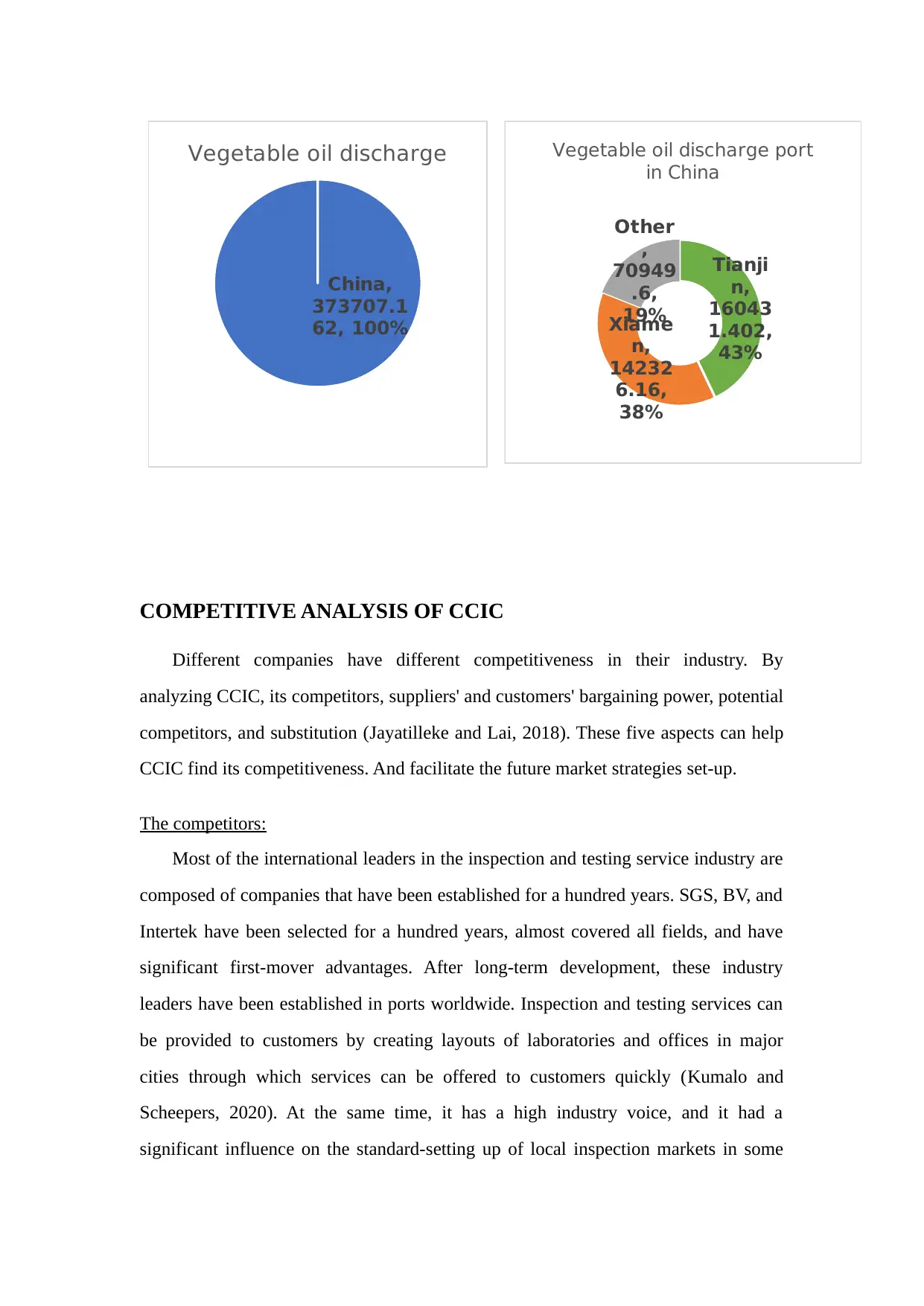

Besides grain commodities procurement in Ukraine, COFCO also purchases

vegetable oil and sunflower seeds. CCIC has not yet expanded but needs to expand on

these businesses in the future. Besides COFCO, other Chinese companies buy the

same goods in Ukraine, such as Sinopharm Group, the largest sunflower seed buyer in

Ukraine. From July 2020 to July 2021, these two companies' total amount of

purchased vegetable oil is about 382,707.162 tons (Ifenthaler, 2020). The figure

below shows China's leading destinations, the main unloading ports are in Tianjin and

Xiamen, and the other unloading ports are Zhangjiagang and Nansha. (Purchase

amount and varieties from COFCO and Sinopharm Group in Ukraine (data 2020.7-

2021.7)

PRE

SSE

D

SFS

OIL,

8414

9.83

8,

22%

SFS

Oil,

2775

57.3

24,

73%

HOS

FS

OIL,

2100

0,

5%

Vegetable oil

vegetable oil and sunflower seeds. CCIC has not yet expanded but needs to expand on

these businesses in the future. Besides COFCO, other Chinese companies buy the

same goods in Ukraine, such as Sinopharm Group, the largest sunflower seed buyer in

Ukraine. From July 2020 to July 2021, these two companies' total amount of

purchased vegetable oil is about 382,707.162 tons (Ifenthaler, 2020). The figure

below shows China's leading destinations, the main unloading ports are in Tianjin and

Xiamen, and the other unloading ports are Zhangjiagang and Nansha. (Purchase

amount and varieties from COFCO and Sinopharm Group in Ukraine (data 2020.7-

2021.7)

PRE

SSE

D

SFS

OIL,

8414

9.83

8,

22%

SFS

Oil,

2775

57.3

24,

73%

HOS

FS

OIL,

2100

0,

5%

Vegetable oil

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

China,

373707.1

62, 100%

Vegetable oil discharge

Tianji

n,

16043

1.402,

43%

Xiame

n,

14232

6.16,

38%

Other

,

70949

.6,

19%

Vegetable oil discharge port

in China

COMPETITIVE ANALYSIS OF CCIC

Different companies have different competitiveness in their industry. By

analyzing CCIC, its competitors, suppliers' and customers' bargaining power, potential

competitors, and substitution (Jayatilleke and Lai, 2018). These five aspects can help

CCIC find its competitiveness. And facilitate the future market strategies set-up.

The competitors:

Most of the international leaders in the inspection and testing service industry are

composed of companies that have been established for a hundred years. SGS, BV, and

Intertek have been selected for a hundred years, almost covered all fields, and have

significant first-mover advantages. After long-term development, these industry

leaders have been established in ports worldwide. Inspection and testing services can

be provided to customers by creating layouts of laboratories and offices in major

cities through which services can be offered to customers quickly (Kumalo and

Scheepers, 2020). At the same time, it has a high industry voice, and it had a

significant influence on the standard-setting up of local inspection markets in some

373707.1

62, 100%

Vegetable oil discharge

Tianji

n,

16043

1.402,

43%

Xiame

n,

14232

6.16,

38%

Other

,

70949

.6,

19%

Vegetable oil discharge port

in China

COMPETITIVE ANALYSIS OF CCIC

Different companies have different competitiveness in their industry. By

analyzing CCIC, its competitors, suppliers' and customers' bargaining power, potential

competitors, and substitution (Jayatilleke and Lai, 2018). These five aspects can help

CCIC find its competitiveness. And facilitate the future market strategies set-up.

The competitors:

Most of the international leaders in the inspection and testing service industry are

composed of companies that have been established for a hundred years. SGS, BV, and

Intertek have been selected for a hundred years, almost covered all fields, and have

significant first-mover advantages. After long-term development, these industry

leaders have been established in ports worldwide. Inspection and testing services can

be provided to customers by creating layouts of laboratories and offices in major

cities through which services can be offered to customers quickly (Kumalo and

Scheepers, 2020). At the same time, it has a high industry voice, and it had a

significant influence on the standard-setting up of local inspection markets in some

developing countries. However, these international giants cannot influence developed

and developing countries like the United States, Canada, China. Because these

countries have a strong awareness of their protection, they may allow such

international third-party testing institutions to enter the testing industry. However,

they will not allow them to occupy a substantial market share and voice in the open

market, which may affect official certification inspection and testing agencies

supported, trusted, and authorized by the government.

CCIC has sufficient authority in the domestic inspection and testing market

because of its particular organization, power, and largest inspection market share.

Such strengths of the organization make them unreplaceable by other international

and foreign inspection agencies (Li and et.al, 2016). However, it is quite the opposite

in the European market because the European inspection market is already in an open

competitive market. As a new international inspection company and to enter the

market, CCIC needs to challenge and break the SGS, BV, the birthplace headquartered

in Europe. Therefore, the company has already become a relatively monopolistic

enterprise. CCIC also requires more time, financial and human investment.

Bargaining power of suppliers:

At present, CCIC's suppliers are small inspection companies or independent

inspectors in the local inspection market. Some of these suppliers have their own

business, while others keep looking for a business. However, these suppliers are all

equipped with professional inspection knowledge, which CCIC lacks in the European

staple agricultural products market. Through the current cooperation with these

suppliers, they need CCIC to entrust their business to increase their income because

CCIC has strong bargaining power over its prices and is dominant (Limba and et.al,

2018). However, it is also necessary to control the price according to the actual

business situation. If the supplier's profit is lower, even with no profit space, it could

also look for other businesses and give up the cooperation with CCIC. Overall, for the

supplier, CCIC is still in a dominant position.

and developing countries like the United States, Canada, China. Because these

countries have a strong awareness of their protection, they may allow such

international third-party testing institutions to enter the testing industry. However,

they will not allow them to occupy a substantial market share and voice in the open

market, which may affect official certification inspection and testing agencies

supported, trusted, and authorized by the government.

CCIC has sufficient authority in the domestic inspection and testing market

because of its particular organization, power, and largest inspection market share.

Such strengths of the organization make them unreplaceable by other international

and foreign inspection agencies (Li and et.al, 2016). However, it is quite the opposite

in the European market because the European inspection market is already in an open

competitive market. As a new international inspection company and to enter the

market, CCIC needs to challenge and break the SGS, BV, the birthplace headquartered

in Europe. Therefore, the company has already become a relatively monopolistic

enterprise. CCIC also requires more time, financial and human investment.

Bargaining power of suppliers:

At present, CCIC's suppliers are small inspection companies or independent

inspectors in the local inspection market. Some of these suppliers have their own

business, while others keep looking for a business. However, these suppliers are all

equipped with professional inspection knowledge, which CCIC lacks in the European

staple agricultural products market. Through the current cooperation with these

suppliers, they need CCIC to entrust their business to increase their income because

CCIC has strong bargaining power over its prices and is dominant (Limba and et.al,

2018). However, it is also necessary to control the price according to the actual

business situation. If the supplier's profit is lower, even with no profit space, it could

also look for other businesses and give up the cooperation with CCIC. Overall, for the

supplier, CCIC is still in a dominant position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.