Impact of CDP on Carbon Emission Minimization in Developed Countries

VerifiedAdded on 2023/06/12

|14

|4057

|52

Report

AI Summary

This report examines the impact of the Carbon Disclosure Project (CDP) on minimizing carbon emissions, primarily focusing on developed countries. It employs the legitimacy theory to assess carbon disclosure practices, highlighting the role of companies in adopting emission-reducing techniques. The research uses secondary data from 2009 to 2015, analyzing companies from Belgium, UK, and Germany. Descriptive statistics and inferential analysis, including t-tests and correlation analysis, are used to evaluate the effectiveness of CDP in promoting carbon emission reduction. The findings indicate varying levels of carbon disclosure among companies and identify areas for future research, particularly concerning non-financial performance and strategic environmental management. Desklib provides a platform to explore similar assignments and access study resources.

Introduction

Climate change have become an issue of concern to both the developed and emerging

economies. The economic growth is important in eradicating poverty but it comes with some

challenges such as increased carbon emission from the companies (Panel, 2013). Development

and expansion of companies in a country lead to creation of job opportunities to the local

population (Katzenbach, and Smith, 2015). Carbon emission have led to great effect on the

climate change such as the global warming. Countries and companies are bringing their efforts

together to reduce the level of carbon emission to the environment (Hansen et al., 2013; Zhang,

Wang and Song, 2013). Developed countries are the high emitters of carbon dioxide gas to the

environment. For instance, the United States’ industrial and commercial sources were reported to

have emitted carbon dioxide gas three times more than the residents in the year 2010 (Nordhaus,

2010). Continued increase of carbon emission led to the emergence of Carbon Disclosure Project

that required the companies to be keeping records of carbon disclosure and reporting the records

within a certain period of time (Ascui and Lovell, 2012; Andrew, and Cortese, 2013). Even

though the companies are keeping records and reporting the carbon emission, they do little in

minimizing the emissions. Reports addressing the climate change challenges considered the

growing markets for products and services’ effects on the companies’ responses to the climate

change (Saka and Oshika, 2014). Despite the efforts and pressure mounted by the non-

governmental organization (CDP) on the companies’ report on carbon emissions, not all

companies respond to the provided emissions and climate change questionnaire on their next

course of action towards combating carbon emissions (Matsumura, Prakash and Vera-Muñoz,

2013). The rising concern from both private and public sectors help the CDP in mounting

pressure and encouraging companies to adopt and mitigate carbon emissions that lead to climate

Climate change have become an issue of concern to both the developed and emerging

economies. The economic growth is important in eradicating poverty but it comes with some

challenges such as increased carbon emission from the companies (Panel, 2013). Development

and expansion of companies in a country lead to creation of job opportunities to the local

population (Katzenbach, and Smith, 2015). Carbon emission have led to great effect on the

climate change such as the global warming. Countries and companies are bringing their efforts

together to reduce the level of carbon emission to the environment (Hansen et al., 2013; Zhang,

Wang and Song, 2013). Developed countries are the high emitters of carbon dioxide gas to the

environment. For instance, the United States’ industrial and commercial sources were reported to

have emitted carbon dioxide gas three times more than the residents in the year 2010 (Nordhaus,

2010). Continued increase of carbon emission led to the emergence of Carbon Disclosure Project

that required the companies to be keeping records of carbon disclosure and reporting the records

within a certain period of time (Ascui and Lovell, 2012; Andrew, and Cortese, 2013). Even

though the companies are keeping records and reporting the carbon emission, they do little in

minimizing the emissions. Reports addressing the climate change challenges considered the

growing markets for products and services’ effects on the companies’ responses to the climate

change (Saka and Oshika, 2014). Despite the efforts and pressure mounted by the non-

governmental organization (CDP) on the companies’ report on carbon emissions, not all

companies respond to the provided emissions and climate change questionnaire on their next

course of action towards combating carbon emissions (Matsumura, Prakash and Vera-Muñoz,

2013). The rising concern from both private and public sectors help the CDP in mounting

pressure and encouraging companies to adopt and mitigate carbon emissions that lead to climate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

change. This research is then aimed at assessing the effects of CDP towards minimizing carbon

emissions.

Summary of literature review

This research adopted legitimacy theory in the examination of carbon disclosure by both private

and public sectors. No theory has come clear in explaining corporate social responsibility

disclosure practices until when legitimacy theory came about and had wide dependence by the

researchers (Fernando, and Lawrence, 2014). Environmental and social disclosure can easily be

explained currently by using legitimacy theory (Deegan, 2014). Due to legitimacy ability of

providing disclosing strategies, legitimacy theory is preferred over other theories (Bakker, Raab,

and Milward, 2012). The strategies identified by the legitimacy theory can be adopted by the

organizations which might legitimize the existence of the organizations hence could be

empirically tested (Maier, Meyer and Steinbereithner, 2016). Agency theory on the other hand

provides the assumption details of the relationship between business agents and principals

(Westley et al., 2013). Through the adopted legitimacy theory, the existing problems in the

carbon disclosure can be somewhat resolved with ease and keeping all the set goals at check.

Business organizations and companies are the major sources of carbon emissions as in the

previous reviews (Huisingh, Zhang, Moore, Qiao and Li, 2015; Böttcher, and Müller, 2015). The

so referred companies are supposed to adopt new techniques that are aimed at minimizing carbon

emissions and keep it at the lowest level possible. The climate change made the companies and

other business organizations suffer some significant risks whose effects are felt in the value of

the organizations’ investments of shareholders (Okereke, Wittneben and Bowen, 2012). The

earlier researches show that there is existence of correlation between the share price and the

environmental performance (Eccles, Ioannou and Serafeim, 2014; Edwards, 2014). Performance

emissions.

Summary of literature review

This research adopted legitimacy theory in the examination of carbon disclosure by both private

and public sectors. No theory has come clear in explaining corporate social responsibility

disclosure practices until when legitimacy theory came about and had wide dependence by the

researchers (Fernando, and Lawrence, 2014). Environmental and social disclosure can easily be

explained currently by using legitimacy theory (Deegan, 2014). Due to legitimacy ability of

providing disclosing strategies, legitimacy theory is preferred over other theories (Bakker, Raab,

and Milward, 2012). The strategies identified by the legitimacy theory can be adopted by the

organizations which might legitimize the existence of the organizations hence could be

empirically tested (Maier, Meyer and Steinbereithner, 2016). Agency theory on the other hand

provides the assumption details of the relationship between business agents and principals

(Westley et al., 2013). Through the adopted legitimacy theory, the existing problems in the

carbon disclosure can be somewhat resolved with ease and keeping all the set goals at check.

Business organizations and companies are the major sources of carbon emissions as in the

previous reviews (Huisingh, Zhang, Moore, Qiao and Li, 2015; Böttcher, and Müller, 2015). The

so referred companies are supposed to adopt new techniques that are aimed at minimizing carbon

emissions and keep it at the lowest level possible. The climate change made the companies and

other business organizations suffer some significant risks whose effects are felt in the value of

the organizations’ investments of shareholders (Okereke, Wittneben and Bowen, 2012). The

earlier researches show that there is existence of correlation between the share price and the

environmental performance (Eccles, Ioannou and Serafeim, 2014; Edwards, 2014). Performance

evaluation in conjunction with performance based incentives are used to protect shareholders’

interests. The levels of carbon emissions is almost unmanageable due to the companies’

managers’ lack of sufficient experience to manage emissions. As a result, the set target have

been difficult to be achieved.

Further studies on financial performance exhibited targets and incentives effects without

including the non-financial performance (Sierzchula, Bakker, Maat and van Wee, 2014.). Being

that carbon emissions and climate change is a bother to all the sectors, non-financial performance

and target operations was the identified gap. Furthermore, future research should be on the

relationship between non-financial performance and the environmental performance. Strategic

importance still remain hanging and sidelined in the firms’ management and operations since

firms are not quite familiar with it. Challenging targets might lead to increase in the number of

targets completed and less weight given to environment related targets.

Hypothesis development

Seminal articles have been covered in legitimacy theory on the control and separation of

ownership. Society can operate in the funny manner by revoking the contract awarded to an

organization if the society feel unsatisfied with organizations’ services (Marcuse, 2013). The

behavior of the agents can be bonded with the guide of principals’ interest related to incentive

performance and setting targets (Fayezi, O'Loughlin and Zutshi, 2012). Legitimacy theory plays

a vital role in explaining environmental and social disclosures in regards to carbon emissions. In

the hypothesis development, it is important to consider the advantages of legitimacy theory that

is not in other theories. One such advantage is providing disclosure strategies that companies

adopt to make their existence legitimate. Slacks are created due to available information

asymmetry that is targeted by the agents. In regards to aforementioned theory in the operational

interests. The levels of carbon emissions is almost unmanageable due to the companies’

managers’ lack of sufficient experience to manage emissions. As a result, the set target have

been difficult to be achieved.

Further studies on financial performance exhibited targets and incentives effects without

including the non-financial performance (Sierzchula, Bakker, Maat and van Wee, 2014.). Being

that carbon emissions and climate change is a bother to all the sectors, non-financial performance

and target operations was the identified gap. Furthermore, future research should be on the

relationship between non-financial performance and the environmental performance. Strategic

importance still remain hanging and sidelined in the firms’ management and operations since

firms are not quite familiar with it. Challenging targets might lead to increase in the number of

targets completed and less weight given to environment related targets.

Hypothesis development

Seminal articles have been covered in legitimacy theory on the control and separation of

ownership. Society can operate in the funny manner by revoking the contract awarded to an

organization if the society feel unsatisfied with organizations’ services (Marcuse, 2013). The

behavior of the agents can be bonded with the guide of principals’ interest related to incentive

performance and setting targets (Fayezi, O'Loughlin and Zutshi, 2012). Legitimacy theory plays

a vital role in explaining environmental and social disclosures in regards to carbon emissions. In

the hypothesis development, it is important to consider the advantages of legitimacy theory that

is not in other theories. One such advantage is providing disclosure strategies that companies

adopt to make their existence legitimate. Slacks are created due to available information

asymmetry that is targeted by the agents. In regards to aforementioned theory in the operational

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

proxies, slack formed the dependent variables (DV) while the incentives provided by the

managers and budgetary process in setting easy targets are referred to in the past researches. In

order to understand carbon emissions, there is dire need for incorporating slack literature in the

operationalization and its application in carbon emissions. Independent variable in this research

will be information asymmetry even though there is their decrease with time. The numbers in the

organization for the past years in which no targets have been set are collected to measure the

information asymmetry on carbon emissions. Greater performance have the effects of greater

completion and the effects are moderated using the performance incentives. Managers in their sit

in the management role of the organization know the potentials of the organizations than the

shareholders or investors. Inverse proportionality exist between information asymmetry and the

created slacks by the managers.

Data collection

In order to exhaust the companies and countries’ response to climate change due to carbon

disclosure, electronic methods was applied to obtain CDP data from their database which

covered the period of six years from 2009 to 2015. In that regards therefore, the data used in this

research were secondary and covered a total population of 5,054 companies from various

countries such as China, Colombia, France, Mexico, South Korea, United Kingdom, USA,

Australia, Canada etc. the data consisted of bot categorical and numerical variables which led to

both categorical and numerical data. It was in the aim of CDP for all the companies from all

countries to comply and report their actions towards carbon disclosure. As a result therefore, this

research took a sample of companies from three developed countries i.e. Belgium, UK and

Germany. The sample size used was 30 companies from the three stated countries and have their

efforts evaluated in the period of the past seven years from 2009 to 2015. From the entire data

managers and budgetary process in setting easy targets are referred to in the past researches. In

order to understand carbon emissions, there is dire need for incorporating slack literature in the

operationalization and its application in carbon emissions. Independent variable in this research

will be information asymmetry even though there is their decrease with time. The numbers in the

organization for the past years in which no targets have been set are collected to measure the

information asymmetry on carbon emissions. Greater performance have the effects of greater

completion and the effects are moderated using the performance incentives. Managers in their sit

in the management role of the organization know the potentials of the organizations than the

shareholders or investors. Inverse proportionality exist between information asymmetry and the

created slacks by the managers.

Data collection

In order to exhaust the companies and countries’ response to climate change due to carbon

disclosure, electronic methods was applied to obtain CDP data from their database which

covered the period of six years from 2009 to 2015. In that regards therefore, the data used in this

research were secondary and covered a total population of 5,054 companies from various

countries such as China, Colombia, France, Mexico, South Korea, United Kingdom, USA,

Australia, Canada etc. the data consisted of bot categorical and numerical variables which led to

both categorical and numerical data. It was in the aim of CDP for all the companies from all

countries to comply and report their actions towards carbon disclosure. As a result therefore, this

research took a sample of companies from three developed countries i.e. Belgium, UK and

Germany. The sample size used was 30 companies from the three stated countries and have their

efforts evaluated in the period of the past seven years from 2009 to 2015. From the entire data

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

set, thirty samples were randomly selected basing particularly on the three developed countries

which covered a relatively wider range of companies.

The retrieved data were in excel data files and were organized and prepared in the same software

for analysis. Descriptive and inferential statistical analysis were conducted to leverage the

characteristics and the companies’ response towards minimizing carbon disclosure in their daily

activities in the covered period.

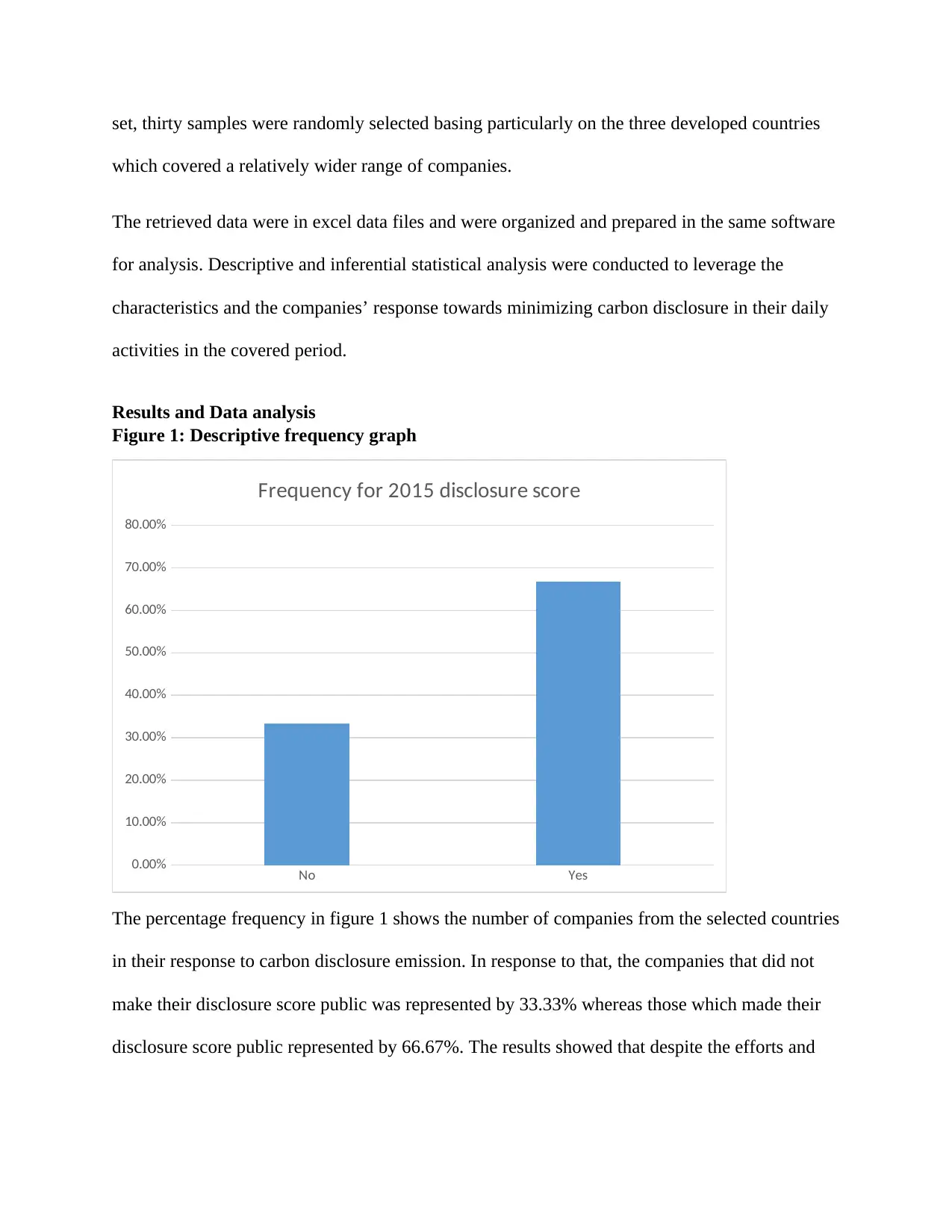

Results and Data analysis

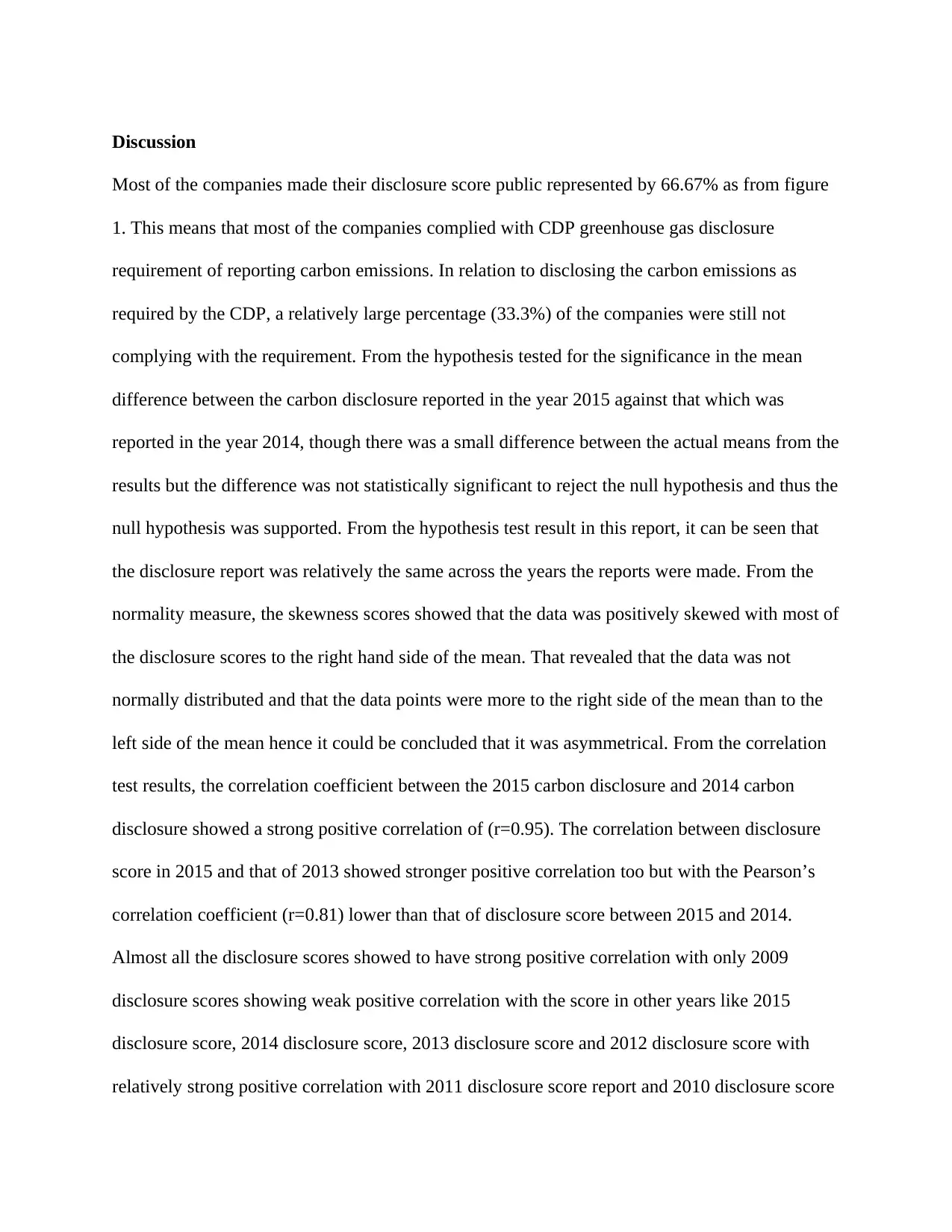

Figure 1: Descriptive frequency graph

No Yes

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Frequency for 2015 disclosure score

The percentage frequency in figure 1 shows the number of companies from the selected countries

in their response to carbon disclosure emission. In response to that, the companies that did not

make their disclosure score public was represented by 33.33% whereas those which made their

disclosure score public represented by 66.67%. The results showed that despite the efforts and

which covered a relatively wider range of companies.

The retrieved data were in excel data files and were organized and prepared in the same software

for analysis. Descriptive and inferential statistical analysis were conducted to leverage the

characteristics and the companies’ response towards minimizing carbon disclosure in their daily

activities in the covered period.

Results and Data analysis

Figure 1: Descriptive frequency graph

No Yes

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Frequency for 2015 disclosure score

The percentage frequency in figure 1 shows the number of companies from the selected countries

in their response to carbon disclosure emission. In response to that, the companies that did not

make their disclosure score public was represented by 33.33% whereas those which made their

disclosure score public represented by 66.67%. The results showed that despite the efforts and

the debates on reporting carbon emission to the environment by the companies, some of the

companies could still defy and not report their carbon emissions to the public.

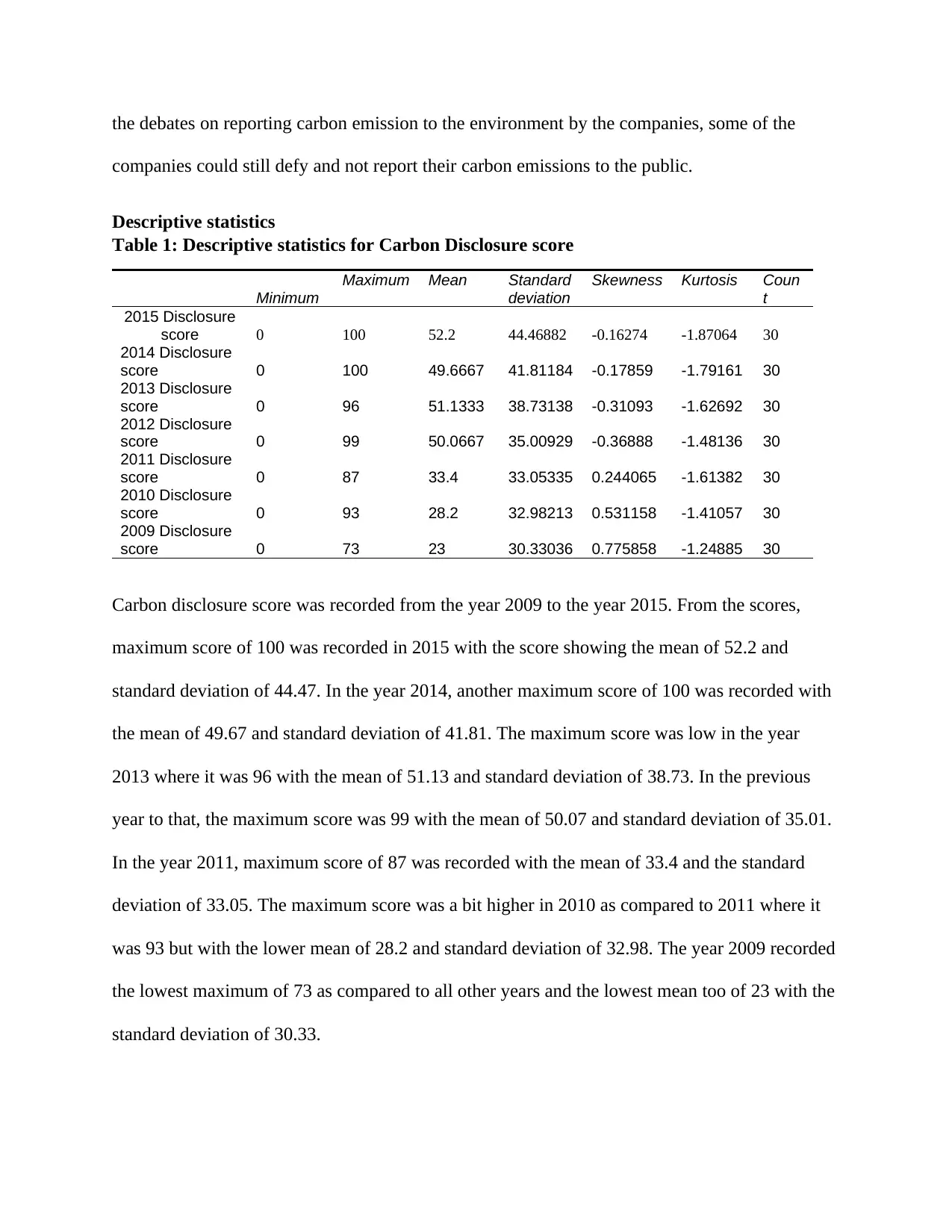

Descriptive statistics

Table 1: Descriptive statistics for Carbon Disclosure score

Minimum

Maximum Mean Standard

deviation

Skewness Kurtosis Coun

t

2015 Disclosure

score 0 100 52.2 44.46882 -0.16274 -1.87064 30

2014 Disclosure

score 0 100 49.6667 41.81184 -0.17859 -1.79161 30

2013 Disclosure

score 0 96 51.1333 38.73138 -0.31093 -1.62692 30

2012 Disclosure

score 0 99 50.0667 35.00929 -0.36888 -1.48136 30

2011 Disclosure

score 0 87 33.4 33.05335 0.244065 -1.61382 30

2010 Disclosure

score 0 93 28.2 32.98213 0.531158 -1.41057 30

2009 Disclosure

score 0 73 23 30.33036 0.775858 -1.24885 30

Carbon disclosure score was recorded from the year 2009 to the year 2015. From the scores,

maximum score of 100 was recorded in 2015 with the score showing the mean of 52.2 and

standard deviation of 44.47. In the year 2014, another maximum score of 100 was recorded with

the mean of 49.67 and standard deviation of 41.81. The maximum score was low in the year

2013 where it was 96 with the mean of 51.13 and standard deviation of 38.73. In the previous

year to that, the maximum score was 99 with the mean of 50.07 and standard deviation of 35.01.

In the year 2011, maximum score of 87 was recorded with the mean of 33.4 and the standard

deviation of 33.05. The maximum score was a bit higher in 2010 as compared to 2011 where it

was 93 but with the lower mean of 28.2 and standard deviation of 32.98. The year 2009 recorded

the lowest maximum of 73 as compared to all other years and the lowest mean too of 23 with the

standard deviation of 30.33.

companies could still defy and not report their carbon emissions to the public.

Descriptive statistics

Table 1: Descriptive statistics for Carbon Disclosure score

Minimum

Maximum Mean Standard

deviation

Skewness Kurtosis Coun

t

2015 Disclosure

score 0 100 52.2 44.46882 -0.16274 -1.87064 30

2014 Disclosure

score 0 100 49.6667 41.81184 -0.17859 -1.79161 30

2013 Disclosure

score 0 96 51.1333 38.73138 -0.31093 -1.62692 30

2012 Disclosure

score 0 99 50.0667 35.00929 -0.36888 -1.48136 30

2011 Disclosure

score 0 87 33.4 33.05335 0.244065 -1.61382 30

2010 Disclosure

score 0 93 28.2 32.98213 0.531158 -1.41057 30

2009 Disclosure

score 0 73 23 30.33036 0.775858 -1.24885 30

Carbon disclosure score was recorded from the year 2009 to the year 2015. From the scores,

maximum score of 100 was recorded in 2015 with the score showing the mean of 52.2 and

standard deviation of 44.47. In the year 2014, another maximum score of 100 was recorded with

the mean of 49.67 and standard deviation of 41.81. The maximum score was low in the year

2013 where it was 96 with the mean of 51.13 and standard deviation of 38.73. In the previous

year to that, the maximum score was 99 with the mean of 50.07 and standard deviation of 35.01.

In the year 2011, maximum score of 87 was recorded with the mean of 33.4 and the standard

deviation of 33.05. The maximum score was a bit higher in 2010 as compared to 2011 where it

was 93 but with the lower mean of 28.2 and standard deviation of 32.98. The year 2009 recorded

the lowest maximum of 73 as compared to all other years and the lowest mean too of 23 with the

standard deviation of 30.33.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

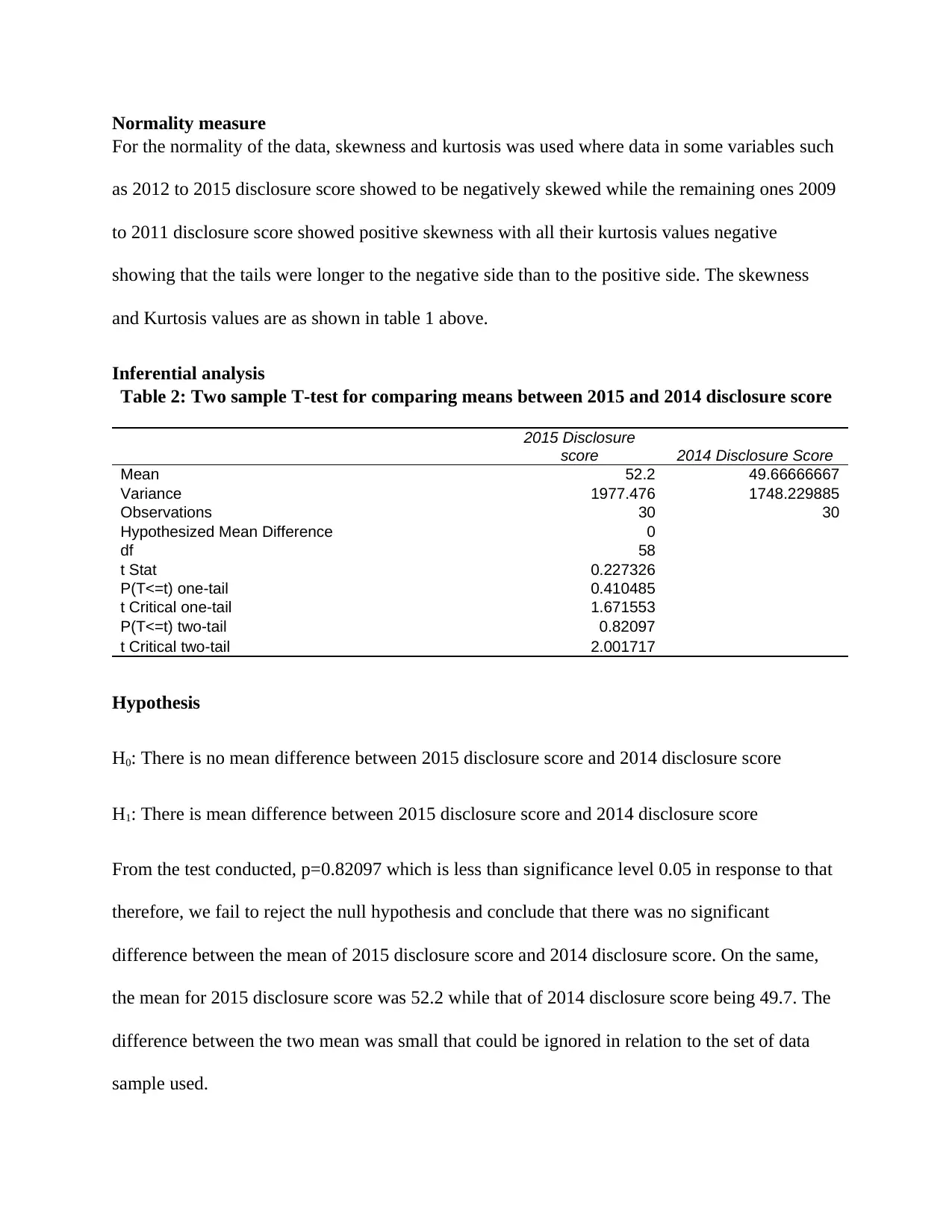

Normality measure

For the normality of the data, skewness and kurtosis was used where data in some variables such

as 2012 to 2015 disclosure score showed to be negatively skewed while the remaining ones 2009

to 2011 disclosure score showed positive skewness with all their kurtosis values negative

showing that the tails were longer to the negative side than to the positive side. The skewness

and Kurtosis values are as shown in table 1 above.

Inferential analysis

Table 2: Two sample T-test for comparing means between 2015 and 2014 disclosure score

2015 Disclosure

score 2014 Disclosure Score

Mean 52.2 49.66666667

Variance 1977.476 1748.229885

Observations 30 30

Hypothesized Mean Difference 0

df 58

t Stat 0.227326

P(T<=t) one-tail 0.410485

t Critical one-tail 1.671553

P(T<=t) two-tail 0.82097

t Critical two-tail 2.001717

Hypothesis

H0: There is no mean difference between 2015 disclosure score and 2014 disclosure score

H1: There is mean difference between 2015 disclosure score and 2014 disclosure score

From the test conducted, p=0.82097 which is less than significance level 0.05 in response to that

therefore, we fail to reject the null hypothesis and conclude that there was no significant

difference between the mean of 2015 disclosure score and 2014 disclosure score. On the same,

the mean for 2015 disclosure score was 52.2 while that of 2014 disclosure score being 49.7. The

difference between the two mean was small that could be ignored in relation to the set of data

sample used.

For the normality of the data, skewness and kurtosis was used where data in some variables such

as 2012 to 2015 disclosure score showed to be negatively skewed while the remaining ones 2009

to 2011 disclosure score showed positive skewness with all their kurtosis values negative

showing that the tails were longer to the negative side than to the positive side. The skewness

and Kurtosis values are as shown in table 1 above.

Inferential analysis

Table 2: Two sample T-test for comparing means between 2015 and 2014 disclosure score

2015 Disclosure

score 2014 Disclosure Score

Mean 52.2 49.66666667

Variance 1977.476 1748.229885

Observations 30 30

Hypothesized Mean Difference 0

df 58

t Stat 0.227326

P(T<=t) one-tail 0.410485

t Critical one-tail 1.671553

P(T<=t) two-tail 0.82097

t Critical two-tail 2.001717

Hypothesis

H0: There is no mean difference between 2015 disclosure score and 2014 disclosure score

H1: There is mean difference between 2015 disclosure score and 2014 disclosure score

From the test conducted, p=0.82097 which is less than significance level 0.05 in response to that

therefore, we fail to reject the null hypothesis and conclude that there was no significant

difference between the mean of 2015 disclosure score and 2014 disclosure score. On the same,

the mean for 2015 disclosure score was 52.2 while that of 2014 disclosure score being 49.7. The

difference between the two mean was small that could be ignored in relation to the set of data

sample used.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

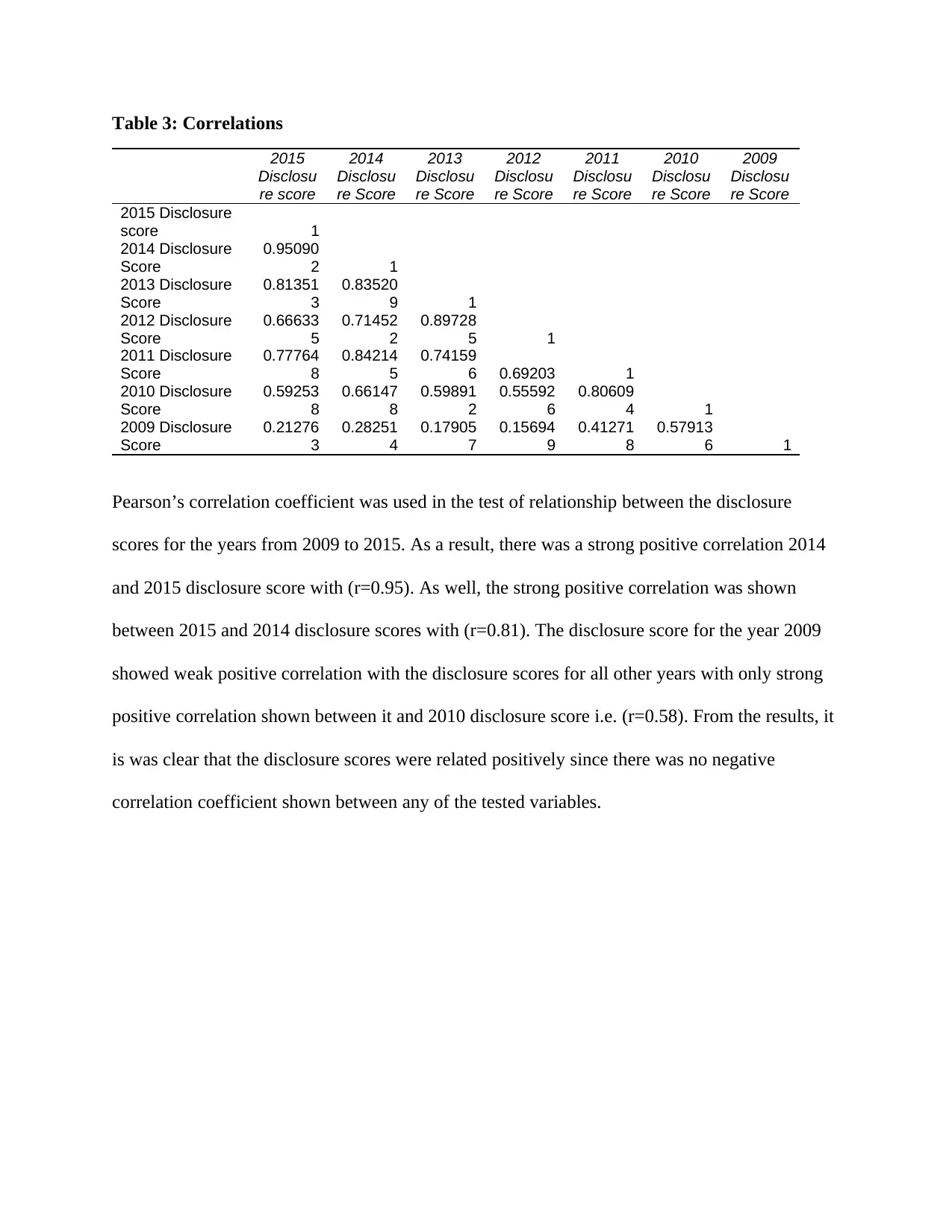

Table 3: Correlations

2015

Disclosu

re score

2014

Disclosu

re Score

2013

Disclosu

re Score

2012

Disclosu

re Score

2011

Disclosu

re Score

2010

Disclosu

re Score

2009

Disclosu

re Score

2015 Disclosure

score 1

2014 Disclosure

Score

0.95090

2 1

2013 Disclosure

Score

0.81351

3

0.83520

9 1

2012 Disclosure

Score

0.66633

5

0.71452

2

0.89728

5 1

2011 Disclosure

Score

0.77764

8

0.84214

5

0.74159

6 0.69203 1

2010 Disclosure

Score

0.59253

8

0.66147

8

0.59891

2

0.55592

6

0.80609

4 1

2009 Disclosure

Score

0.21276

3

0.28251

4

0.17905

7

0.15694

9

0.41271

8

0.57913

6 1

Pearson’s correlation coefficient was used in the test of relationship between the disclosure

scores for the years from 2009 to 2015. As a result, there was a strong positive correlation 2014

and 2015 disclosure score with (r=0.95). As well, the strong positive correlation was shown

between 2015 and 2014 disclosure scores with (r=0.81). The disclosure score for the year 2009

showed weak positive correlation with the disclosure scores for all other years with only strong

positive correlation shown between it and 2010 disclosure score i.e. (r=0.58). From the results, it

is was clear that the disclosure scores were related positively since there was no negative

correlation coefficient shown between any of the tested variables.

2015

Disclosu

re score

2014

Disclosu

re Score

2013

Disclosu

re Score

2012

Disclosu

re Score

2011

Disclosu

re Score

2010

Disclosu

re Score

2009

Disclosu

re Score

2015 Disclosure

score 1

2014 Disclosure

Score

0.95090

2 1

2013 Disclosure

Score

0.81351

3

0.83520

9 1

2012 Disclosure

Score

0.66633

5

0.71452

2

0.89728

5 1

2011 Disclosure

Score

0.77764

8

0.84214

5

0.74159

6 0.69203 1

2010 Disclosure

Score

0.59253

8

0.66147

8

0.59891

2

0.55592

6

0.80609

4 1

2009 Disclosure

Score

0.21276

3

0.28251

4

0.17905

7

0.15694

9

0.41271

8

0.57913

6 1

Pearson’s correlation coefficient was used in the test of relationship between the disclosure

scores for the years from 2009 to 2015. As a result, there was a strong positive correlation 2014

and 2015 disclosure score with (r=0.95). As well, the strong positive correlation was shown

between 2015 and 2014 disclosure scores with (r=0.81). The disclosure score for the year 2009

showed weak positive correlation with the disclosure scores for all other years with only strong

positive correlation shown between it and 2010 disclosure score i.e. (r=0.58). From the results, it

is was clear that the disclosure scores were related positively since there was no negative

correlation coefficient shown between any of the tested variables.

Discussion

Most of the companies made their disclosure score public represented by 66.67% as from figure

1. This means that most of the companies complied with CDP greenhouse gas disclosure

requirement of reporting carbon emissions. In relation to disclosing the carbon emissions as

required by the CDP, a relatively large percentage (33.3%) of the companies were still not

complying with the requirement. From the hypothesis tested for the significance in the mean

difference between the carbon disclosure reported in the year 2015 against that which was

reported in the year 2014, though there was a small difference between the actual means from the

results but the difference was not statistically significant to reject the null hypothesis and thus the

null hypothesis was supported. From the hypothesis test result in this report, it can be seen that

the disclosure report was relatively the same across the years the reports were made. From the

normality measure, the skewness scores showed that the data was positively skewed with most of

the disclosure scores to the right hand side of the mean. That revealed that the data was not

normally distributed and that the data points were more to the right side of the mean than to the

left side of the mean hence it could be concluded that it was asymmetrical. From the correlation

test results, the correlation coefficient between the 2015 carbon disclosure and 2014 carbon

disclosure showed a strong positive correlation of (r=0.95). The correlation between disclosure

score in 2015 and that of 2013 showed stronger positive correlation too but with the Pearson’s

correlation coefficient (r=0.81) lower than that of disclosure score between 2015 and 2014.

Almost all the disclosure scores showed to have strong positive correlation with only 2009

disclosure scores showing weak positive correlation with the score in other years like 2015

disclosure score, 2014 disclosure score, 2013 disclosure score and 2012 disclosure score with

relatively strong positive correlation with 2011 disclosure score report and 2010 disclosure score

Most of the companies made their disclosure score public represented by 66.67% as from figure

1. This means that most of the companies complied with CDP greenhouse gas disclosure

requirement of reporting carbon emissions. In relation to disclosing the carbon emissions as

required by the CDP, a relatively large percentage (33.3%) of the companies were still not

complying with the requirement. From the hypothesis tested for the significance in the mean

difference between the carbon disclosure reported in the year 2015 against that which was

reported in the year 2014, though there was a small difference between the actual means from the

results but the difference was not statistically significant to reject the null hypothesis and thus the

null hypothesis was supported. From the hypothesis test result in this report, it can be seen that

the disclosure report was relatively the same across the years the reports were made. From the

normality measure, the skewness scores showed that the data was positively skewed with most of

the disclosure scores to the right hand side of the mean. That revealed that the data was not

normally distributed and that the data points were more to the right side of the mean than to the

left side of the mean hence it could be concluded that it was asymmetrical. From the correlation

test results, the correlation coefficient between the 2015 carbon disclosure and 2014 carbon

disclosure showed a strong positive correlation of (r=0.95). The correlation between disclosure

score in 2015 and that of 2013 showed stronger positive correlation too but with the Pearson’s

correlation coefficient (r=0.81) lower than that of disclosure score between 2015 and 2014.

Almost all the disclosure scores showed to have strong positive correlation with only 2009

disclosure scores showing weak positive correlation with the score in other years like 2015

disclosure score, 2014 disclosure score, 2013 disclosure score and 2012 disclosure score with

relatively strong positive correlation with 2011 disclosure score report and 2010 disclosure score

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

report i.e. (r=0.41 and r=0.58) respectively. This could tell that the disclosure scores were

improving over the latest years from the previous years as this can as well be supported by the

mean disclosure results from the data e.g. 2013 mean disclosure score from the sampled

companies was 51.13 and the disclosure score for the year 2009 had the mean of 23. Large

difference (28.13) of the mean disclosure scores reported in the years showed improvement in

the companies’ report on the carbon disclosure.

improving over the latest years from the previous years as this can as well be supported by the

mean disclosure results from the data e.g. 2013 mean disclosure score from the sampled

companies was 51.13 and the disclosure score for the year 2009 had the mean of 23. Large

difference (28.13) of the mean disclosure scores reported in the years showed improvement in

the companies’ report on the carbon disclosure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Limitations of the study

This research only tested on the correlation and the mean difference between the carbon

disclosure scores for the years 2009 to 2015. The root cause of the mean difference and the

importance of the disclosure values have not been discussed thus remained unclear. In the future

research, it would be important if they would carry out the research on the practical methods that

should be applied by the companies both in public and private sectors to minimize or fully do

away the carbon emissions and control the climate change. Furthermore, after the carbon

disclosure reported by the companies, nothing much seem to be done due to lack of directions to

take since there were no penalties imposed on the companies defaulting to give the carbon

disclosure reports. The report did not cover what the CDP does to the companies that file their

reports every required period whether or not they are rewarded to keep others dedicate their

potential towards meeting the same goal of reducing keeping the carbon disclosure records on

check and thus working towards minimizing the emissions by acquiring environment friendly

sources of energy thus dealing with climate change. This study adopted legitimacy theory which

mentioned of identifying the strategies for the companies to adopt in legitimizing their existence

but did not explicate any of such strategies. Finally, this study identified that the existing theories

had not in any way explained the relationship that exist between non-financial performance and

the environmental performance. This is the gap of knowledge that be focused on for future

research.

Further research

Referring to the limitation identified from this report, further research should address the

importance of the companies’ disclosure score values for clarity. When this is done, the

proportion of the companies that were was reported to have not been disclosing their annual

carbon disclosure data might be drawn and convinced to comply with the CDP requirement by

This research only tested on the correlation and the mean difference between the carbon

disclosure scores for the years 2009 to 2015. The root cause of the mean difference and the

importance of the disclosure values have not been discussed thus remained unclear. In the future

research, it would be important if they would carry out the research on the practical methods that

should be applied by the companies both in public and private sectors to minimize or fully do

away the carbon emissions and control the climate change. Furthermore, after the carbon

disclosure reported by the companies, nothing much seem to be done due to lack of directions to

take since there were no penalties imposed on the companies defaulting to give the carbon

disclosure reports. The report did not cover what the CDP does to the companies that file their

reports every required period whether or not they are rewarded to keep others dedicate their

potential towards meeting the same goal of reducing keeping the carbon disclosure records on

check and thus working towards minimizing the emissions by acquiring environment friendly

sources of energy thus dealing with climate change. This study adopted legitimacy theory which

mentioned of identifying the strategies for the companies to adopt in legitimizing their existence

but did not explicate any of such strategies. Finally, this study identified that the existing theories

had not in any way explained the relationship that exist between non-financial performance and

the environmental performance. This is the gap of knowledge that be focused on for future

research.

Further research

Referring to the limitation identified from this report, further research should address the

importance of the companies’ disclosure score values for clarity. When this is done, the

proportion of the companies that were was reported to have not been disclosing their annual

carbon disclosure data might be drawn and convinced to comply with the CDP requirement by

providing the disclosure reports. Further, future research should be conducted on the practical

methods that should be applied by the companies in both public and private sectors to fully

minimize the carbon emissions by the companies and have climate change under control.

Researches to come in the future should be on encouraging the companies in complying with the

disclosure report as outlined by the CDP. In that regard, researches should be conducted

suggesting penalties that should be imposed on the companies that fail to provide the carbon

emissions disclosure report to prohibit companies from defaulting to give their disclosure report.

methods that should be applied by the companies in both public and private sectors to fully

minimize the carbon emissions by the companies and have climate change under control.

Researches to come in the future should be on encouraging the companies in complying with the

disclosure report as outlined by the CDP. In that regard, researches should be conducted

suggesting penalties that should be imposed on the companies that fail to provide the carbon

emissions disclosure report to prohibit companies from defaulting to give their disclosure report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.