Comprehensive Report: Central Bank Credit Bureau Examination

VerifiedAdded on 2022/08/12

|30

|7597

|19

Report

AI Summary

This report provides a detailed examination of the Central Bank Credit Bureau Examination Department (CBED), outlining its purpose, structure, and operational domains. The report covers key aspects such as planning and monitoring, on-site examination, quality assurance, and risk management, including fraud detection and business continuity planning. It delves into the CBED's role in ensuring financial stability and consumer protection within Oman's banking sector, including licensing requirements, on-site and off-site supervision, and dispute resolution mechanisms. The report analyzes the department's responsibilities, job descriptions, and adherence to the banking law of Oman, providing a comprehensive overview of the CBED's functions and activities. It also includes details on the code of ethics, training, and reporting procedures, reflecting a commitment to transparency and regulatory compliance. This report is a valuable resource for understanding the CBED's role in the financial landscape.

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 1

1 | P a g e

Central

Bank

Credit

Bureau

Examinatio

n

Departmen

t

1 | P a g e

Central

Bank

Credit

Bureau

Examinatio

n

Departmen

t

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 2

Table of Contents

1 General...........................................................................................................................................4

1.01 Purpose.....................................................................................................................................4

1.02 List of Abbreviations............................................................................................................4

1.03 Responsibility for Implementation..................................................................................4

1.04 Custody and Access.............................................................................................................5

1.05 Maintenance and Updating................................................................................................5

1.06 Mission Statement................................................................................................................5

1.07 Introduction of Credit Bureau Examination Department......................................11

1.08 Organization structure......................................................................................................12

1.09 Terms of references...........................................................................................................12

1.10 Job Description.....................................................................................................................13

1.11 Retention Period of Files and Records.........................................................................13

1.12 Acting Responsibility..........................................................................................................13

1.13 Code of Ethics and Professional Standard..................................................................13

1.14 Maintenance of CBED Corresponding..........................................................................15

2 Planning and Monitoring Domain..................................................................................15

2.01 Preparation of Annual Examination Plan.....................................................................15

2.02 Risk Profiling and Examination Strategy.....................................................................15

2.03 Monitoring of other Regulatory Data/ Information..................................................16

2.04 Monitoring of Compliance Status of Examination Report.....................................16

2.05 Finalizing TORs of Limited Scope Examinations.......................................................16

2.06 Acting as Nodal Point for Incoming/ Outgoing Mail...................................................17

2.07 Other Policy Related Matters..........................................................................................17

2.08 Strategic Planning and Budgeting.................................................................................17

2.09 Submission of Quarterly Activity Reports to the Board of Governors..............18

2.10 Training and Development..............................................................................................18

2.11 Serve as Secretariat of DMC...........................................................................................19

3 On-site Examination Domain............................................................................................19

3.01 Pre-Examination Activities...............................................................................................19

3.02 Fieldwork Related Activities............................................................................................20

3.03 Drafting and Finalization of Report...............................................................................20

2 | P a g e

Table of Contents

1 General...........................................................................................................................................4

1.01 Purpose.....................................................................................................................................4

1.02 List of Abbreviations............................................................................................................4

1.03 Responsibility for Implementation..................................................................................4

1.04 Custody and Access.............................................................................................................5

1.05 Maintenance and Updating................................................................................................5

1.06 Mission Statement................................................................................................................5

1.07 Introduction of Credit Bureau Examination Department......................................11

1.08 Organization structure......................................................................................................12

1.09 Terms of references...........................................................................................................12

1.10 Job Description.....................................................................................................................13

1.11 Retention Period of Files and Records.........................................................................13

1.12 Acting Responsibility..........................................................................................................13

1.13 Code of Ethics and Professional Standard..................................................................13

1.14 Maintenance of CBED Corresponding..........................................................................15

2 Planning and Monitoring Domain..................................................................................15

2.01 Preparation of Annual Examination Plan.....................................................................15

2.02 Risk Profiling and Examination Strategy.....................................................................15

2.03 Monitoring of other Regulatory Data/ Information..................................................16

2.04 Monitoring of Compliance Status of Examination Report.....................................16

2.05 Finalizing TORs of Limited Scope Examinations.......................................................16

2.06 Acting as Nodal Point for Incoming/ Outgoing Mail...................................................17

2.07 Other Policy Related Matters..........................................................................................17

2.08 Strategic Planning and Budgeting.................................................................................17

2.09 Submission of Quarterly Activity Reports to the Board of Governors..............18

2.10 Training and Development..............................................................................................18

2.11 Serve as Secretariat of DMC...........................................................................................19

3 On-site Examination Domain............................................................................................19

3.01 Pre-Examination Activities...............................................................................................19

3.02 Fieldwork Related Activities............................................................................................20

3.03 Drafting and Finalization of Report...............................................................................20

2 | P a g e

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 3

4 Quality Assurance Domain................................................................................................20

4.01 Review of Draft Violations & Exceptions and Schedule of Criticized Advances

20

4.02 Exit Meeting..........................................................................................................................21

4.03 Review of Exit Meeting Chart..........................................................................................21

4.04 Review of Examination Report.......................................................................................22

4.05 Review of Other Related Documents...........................................................................22

4.06 Secretarial Support to the Rating Panel......................................................................23

4.07 Maintenance of Risk Register.........................................................................................23

4.08 Secretarial Support to MPBDC........................................................................................23

5 Risk Management, Fraud Detection and Business Continuity Plan..........24

5.01 Risk Management...............................................................................................................24

5.02 Fraud Detection...................................................................................................................24

5.03 Business Continuity Plan..................................................................................................25

6 Appendix 1: Changes to the report..............................................................................26

7 Appendix 2: Interruptions.................................................................................................27

3 | P a g e

4 Quality Assurance Domain................................................................................................20

4.01 Review of Draft Violations & Exceptions and Schedule of Criticized Advances

20

4.02 Exit Meeting..........................................................................................................................21

4.03 Review of Exit Meeting Chart..........................................................................................21

4.04 Review of Examination Report.......................................................................................22

4.05 Review of Other Related Documents...........................................................................22

4.06 Secretarial Support to the Rating Panel......................................................................23

4.07 Maintenance of Risk Register.........................................................................................23

4.08 Secretarial Support to MPBDC........................................................................................23

5 Risk Management, Fraud Detection and Business Continuity Plan..........24

5.01 Risk Management...............................................................................................................24

5.02 Fraud Detection...................................................................................................................24

5.03 Business Continuity Plan..................................................................................................25

6 Appendix 1: Changes to the report..............................................................................26

7 Appendix 2: Interruptions.................................................................................................27

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 4

1 General

1.01Purpose

The fundamental purpose of a credit bureau department is to make sure that the creditors

have the appropriate information to facilitate lending and its related decisions. The department

partners with all institutions which take part in lending including banks, mortgage lenders, credit

card service providers and any other company that deals with financial matters.

1.02List of Abbreviations

i. ACRI- Arab Credit Reporting Initiative

ii. ATM- Automated Teller Machine

iii. CBD- Credit Bureau Department

iv. CBO- Central Bank of Oman

v. MFI- Micro Finance Institutions

vi. MOI- Ministry of Interior

vii. NBCI – National Bureau of Commercial Information

viii. ND- National Identification

ix. ROP- Royal Oman Police

x. SME- Small and Medium Enterprises

xi. WB- World Bank (Monnet, 2016)

4 | P a g e

1 General

1.01Purpose

The fundamental purpose of a credit bureau department is to make sure that the creditors

have the appropriate information to facilitate lending and its related decisions. The department

partners with all institutions which take part in lending including banks, mortgage lenders, credit

card service providers and any other company that deals with financial matters.

1.02List of Abbreviations

i. ACRI- Arab Credit Reporting Initiative

ii. ATM- Automated Teller Machine

iii. CBD- Credit Bureau Department

iv. CBO- Central Bank of Oman

v. MFI- Micro Finance Institutions

vi. MOI- Ministry of Interior

vii. NBCI – National Bureau of Commercial Information

viii. ND- National Identification

ix. ROP- Royal Oman Police

x. SME- Small and Medium Enterprises

xi. WB- World Bank (Monnet, 2016)

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 5

1.03Responsibility for Implementation

Central Bank of Oman (CBO) has a duty and a responsibility of making sure that a constant

structure for the financial progress of Oman has been provided through its Credit Bureau

Department (Dogru, 2017). This will be done in conjunction with any other department which

will be deemed appropriate depending on what has to be done at a given time.

1.04Custody and Access

The custody of information contained herewith and any other related information will be

maintained by the CBO under the department of the Credit Bureau Department. This information

can be accessed by any staff at CBO and any other person who has been granted permission to

access this information by CBO administration.

1.05Maintenance and Updating

This information will be maintained by the CBD at CBO and it will be updated by the same

department in consultation with appropriate government agencies, experts and representatives of

financial institutions where their presence is necessary. This will also be done by the government

through the right ministry so that CBO remains compliant to the law of the state (Wiseman et al,

2019).

1.06Mission Statement

To deliver a constant structure for the financial progress of Oman through efficient,

transparent and effective implementation of financial conversation rate policy and supervision of

the monetary sector.

5 | P a g e

1.03Responsibility for Implementation

Central Bank of Oman (CBO) has a duty and a responsibility of making sure that a constant

structure for the financial progress of Oman has been provided through its Credit Bureau

Department (Dogru, 2017). This will be done in conjunction with any other department which

will be deemed appropriate depending on what has to be done at a given time.

1.04Custody and Access

The custody of information contained herewith and any other related information will be

maintained by the CBO under the department of the Credit Bureau Department. This information

can be accessed by any staff at CBO and any other person who has been granted permission to

access this information by CBO administration.

1.05Maintenance and Updating

This information will be maintained by the CBD at CBO and it will be updated by the same

department in consultation with appropriate government agencies, experts and representatives of

financial institutions where their presence is necessary. This will also be done by the government

through the right ministry so that CBO remains compliant to the law of the state (Wiseman et al,

2019).

1.06Mission Statement

To deliver a constant structure for the financial progress of Oman through efficient,

transparent and effective implementation of financial conversation rate policy and supervision of

the monetary sector.

5 | P a g e

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 6

Supervision Framework

The Central Bank of Oman makes use of both on-site and off-site examination

techniques. All banks have to go through an on-site examination every year which is carried out

after a certain period to establish the condition of the institution in question.

Licensing:

1. Requirements

For an organization to be licensed to operate it has to meet the requirements so that its

operations can run smoothly. This means that from documentation, structural requirements,

financial qualifications and personnel should be met depending on the size and scope of the

organization in question. The larger the organization, the more it has to do and vice versa.

2. Ownership

The ownership of a given organization must be stated clearly with the right supporting

documents. Whether it is owned as a sole proprietorship, a partnership or a corporation, this has

to come out clearly so that when licensing is done, the right license has to be provided. This will

enable the government to know who they are dealing with.

6 | P a g e

Licensing On-Site

Supervision

Off-Site

Supervision

Dispute

Resolution

Supervision Framework

The Central Bank of Oman makes use of both on-site and off-site examination

techniques. All banks have to go through an on-site examination every year which is carried out

after a certain period to establish the condition of the institution in question.

Licensing:

1. Requirements

For an organization to be licensed to operate it has to meet the requirements so that its

operations can run smoothly. This means that from documentation, structural requirements,

financial qualifications and personnel should be met depending on the size and scope of the

organization in question. The larger the organization, the more it has to do and vice versa.

2. Ownership

The ownership of a given organization must be stated clearly with the right supporting

documents. Whether it is owned as a sole proprietorship, a partnership or a corporation, this has

to come out clearly so that when licensing is done, the right license has to be provided. This will

enable the government to know who they are dealing with.

6 | P a g e

Licensing On-Site

Supervision

Off-Site

Supervision

Dispute

Resolution

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 7

3. Management

For a bank to operate effectively then there is a need for it to have the right people in the

management. This is treated as a requirement before the bank is licensed. An organization,

therefore, must prove that it has the people with the right capacity to manage and run it

appropriately before it is licensed (Brown, 2017). The management is the heart of the organization

and its effectiveness will affect the effectiveness of the entire organization.

4. Financial Capacity

For any organization to receive a license that permits it to operate as a bank in Oman it has to

prove that it has financial stability. As a bank, the core business circumnavigates around money

without which the bank loses its importance (Agarwal et al, 2017). This makes it necessary for a

bank that is seeking a license to operate to prove that it is financially stable and it can meet all

the financial obligations which come before it.

On-site Supervision:

In conformation to the statutes, every organization goes through on-site supervision once per

year to establish its condition on various aspects that are deemed necessary at the time of

examination.

1. Consumer Protection

A report has to generate on whether the organization through its actions and non-actions are

fostering high levels of consumer protection. Instances of unwarranted customer exploitation are

7 | P a g e

3. Management

For a bank to operate effectively then there is a need for it to have the right people in the

management. This is treated as a requirement before the bank is licensed. An organization,

therefore, must prove that it has the people with the right capacity to manage and run it

appropriately before it is licensed (Brown, 2017). The management is the heart of the organization

and its effectiveness will affect the effectiveness of the entire organization.

4. Financial Capacity

For any organization to receive a license that permits it to operate as a bank in Oman it has to

prove that it has financial stability. As a bank, the core business circumnavigates around money

without which the bank loses its importance (Agarwal et al, 2017). This makes it necessary for a

bank that is seeking a license to operate to prove that it is financially stable and it can meet all

the financial obligations which come before it.

On-site Supervision:

In conformation to the statutes, every organization goes through on-site supervision once per

year to establish its condition on various aspects that are deemed necessary at the time of

examination.

1. Consumer Protection

A report has to generate on whether the organization through its actions and non-actions are

fostering high levels of consumer protection. Instances of unwarranted customer exploitation are

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 8

checked out if they do exist (Li, 2016). Abidance to the laws on customer protection is also

checked out to ensure that all customers are getting what is stipulated by the law.

2. Information security CIA

Measures that have been taken by the organization to protect customer and employee

information which is private are checked out. This aims at ensuring that at no instance does

information which should have remained private and confidential get leaked. Information on

what the organization has done to collect this data so that the general security issues of

information is collected.

3. Compliance

Data on compliance by an organization is collected. When it comes to compliance, the main

area of focus is compliance by law especially when it comes to the setting up and organization of

the premise. This information is collected to determine whether the organization has done as it

should do in terms of providing an environment from which people can work (Ball, 2018). This

will also aim at fostering compliance with the law and other key rules and regulations.

4. Workplace safety

When carrying out the on-site supervision, information on workplace safety of a given place

is collected. This will help in determining whether the premises of a given organization are safe

for the workers and customers. This is done with a close reference to the outlined workplace

safety standards which an organization should adhere to. This is aimed at ensuring that the

workers, customers and other people who visit such a premise are safe.

8 | P a g e

checked out if they do exist (Li, 2016). Abidance to the laws on customer protection is also

checked out to ensure that all customers are getting what is stipulated by the law.

2. Information security CIA

Measures that have been taken by the organization to protect customer and employee

information which is private are checked out. This aims at ensuring that at no instance does

information which should have remained private and confidential get leaked. Information on

what the organization has done to collect this data so that the general security issues of

information is collected.

3. Compliance

Data on compliance by an organization is collected. When it comes to compliance, the main

area of focus is compliance by law especially when it comes to the setting up and organization of

the premise. This information is collected to determine whether the organization has done as it

should do in terms of providing an environment from which people can work (Ball, 2018). This

will also aim at fostering compliance with the law and other key rules and regulations.

4. Workplace safety

When carrying out the on-site supervision, information on workplace safety of a given place

is collected. This will help in determining whether the premises of a given organization are safe

for the workers and customers. This is done with a close reference to the outlined workplace

safety standards which an organization should adhere to. This is aimed at ensuring that the

workers, customers and other people who visit such a premise are safe.

8 | P a g e

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 9

Offsite Supervision:

The banking surveillance department is responsible for Offsite supervision.

1. Statistical Returns

Information on the prudential returns for the banks is collected during the exercise. This is

used to measure the financial health of the organization being supervised. This makes it possible

for ongoing supervision of these organizations (Gama et al, 2017). This information also reveals

warning signs that a certain organization is not on the right track for appropriate corrective

measures.

2. Compliance Returns

Data about compliance that an organization has done in comparison to what it should be

doing is collected. This becomes crucial is determining to what extent such organizations are

abiding by the law. This is done so that appropriate corrective measures can be taken to ensure

that all organizations under the supervision of the central bank are complying with the law.

Compliance with working conditions, health and safety environment is also determined (Roberts,

2016).

3. Laws

Apart from the national and international laws which an organization is expected to comply

with, other self-established laws that guide the operation of a given organization are also taken

into consideration. The appropriateness of these laws and general compliance to the general rule

of law is determined through collected data to allow the supervising bank to take the right steps

towards getting things done in the right manner (Kelchen, 2016).

9 | P a g e

Offsite Supervision:

The banking surveillance department is responsible for Offsite supervision.

1. Statistical Returns

Information on the prudential returns for the banks is collected during the exercise. This is

used to measure the financial health of the organization being supervised. This makes it possible

for ongoing supervision of these organizations (Gama et al, 2017). This information also reveals

warning signs that a certain organization is not on the right track for appropriate corrective

measures.

2. Compliance Returns

Data about compliance that an organization has done in comparison to what it should be

doing is collected. This becomes crucial is determining to what extent such organizations are

abiding by the law. This is done so that appropriate corrective measures can be taken to ensure

that all organizations under the supervision of the central bank are complying with the law.

Compliance with working conditions, health and safety environment is also determined (Roberts,

2016).

3. Laws

Apart from the national and international laws which an organization is expected to comply

with, other self-established laws that guide the operation of a given organization are also taken

into consideration. The appropriateness of these laws and general compliance to the general rule

of law is determined through collected data to allow the supervising bank to take the right steps

towards getting things done in the right manner (Kelchen, 2016).

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 10

Dispute Resolution

Information on the process followed to resolve conflicts whenever they arise is collected and

measured against the national standards. The collected information is aimed at establishing

whether the organization has a dispute resolution plan in place which is operational.

i. Dispute resolution plan

The information that is collected to determine whether the organization has a dispute

resolution plan with a keen focus on the contents of the dispute resolution plan. This aims at

establishing whether the plan meets the required standards (Mungiria, 2019).

ii. Complaint procedure

Data that is collected aims at establishing whether an organization has a well-established

process through which complaints can be launched and a dispute resolved as per the

requirements. The aspect of whether this procedure is well known by the employees or it is not

well known so that it can be applied by the employees (Dressel, 2018).

iii. Complains committee

A committee that receives the complaints and addresses them as per the requirements.

Question of whether the membership on such a committee has an appropriate representation and

they are functioning appropriately (Bogart, 2017).

iv. Uniformity in the complaints handling

There is a need for the organization to make sure that when handling complaints and solving

disputes there is some sort of uniformity so that all people are treated equally (Silvestre, 2017).

10 | P a g e

Dispute Resolution

Information on the process followed to resolve conflicts whenever they arise is collected and

measured against the national standards. The collected information is aimed at establishing

whether the organization has a dispute resolution plan in place which is operational.

i. Dispute resolution plan

The information that is collected to determine whether the organization has a dispute

resolution plan with a keen focus on the contents of the dispute resolution plan. This aims at

establishing whether the plan meets the required standards (Mungiria, 2019).

ii. Complaint procedure

Data that is collected aims at establishing whether an organization has a well-established

process through which complaints can be launched and a dispute resolved as per the

requirements. The aspect of whether this procedure is well known by the employees or it is not

well known so that it can be applied by the employees (Dressel, 2018).

iii. Complains committee

A committee that receives the complaints and addresses them as per the requirements.

Question of whether the membership on such a committee has an appropriate representation and

they are functioning appropriately (Bogart, 2017).

iv. Uniformity in the complaints handling

There is a need for the organization to make sure that when handling complaints and solving

disputes there is some sort of uniformity so that all people are treated equally (Silvestre, 2017).

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 11

This makes them feel that they are highly valued and therefore they will end up delivering their

best because of the respect and equality accorded to them whether they are complaining or they

are being complained about.

1.07Introduction of Credit Bureau Examination

Department

Credit Bureau Examination Department is a department under the Central Bank of which

takes part in the examination and ensures that the right standards have been adhered to. It was

established under the guidance of the banking law of Oman (Ott, 2018). This department makes

sure that the banks, mortgage companies and all forms of organizations which offer credit

facilities have provided such facilities as it should be (Ling-Yun et al, 2016). The department also

makes sure that the clients are aware of the existence of such service providers so that they can

make the right decisions.

11 | P a g e

This makes them feel that they are highly valued and therefore they will end up delivering their

best because of the respect and equality accorded to them whether they are complaining or they

are being complained about.

1.07Introduction of Credit Bureau Examination

Department

Credit Bureau Examination Department is a department under the Central Bank of which

takes part in the examination and ensures that the right standards have been adhered to. It was

established under the guidance of the banking law of Oman (Ott, 2018). This department makes

sure that the banks, mortgage companies and all forms of organizations which offer credit

facilities have provided such facilities as it should be (Ling-Yun et al, 2016). The department also

makes sure that the clients are aware of the existence of such service providers so that they can

make the right decisions.

11 | P a g e

Running Header: CENTRAL BANK CREDIT BUREAU EXAMINATION 12

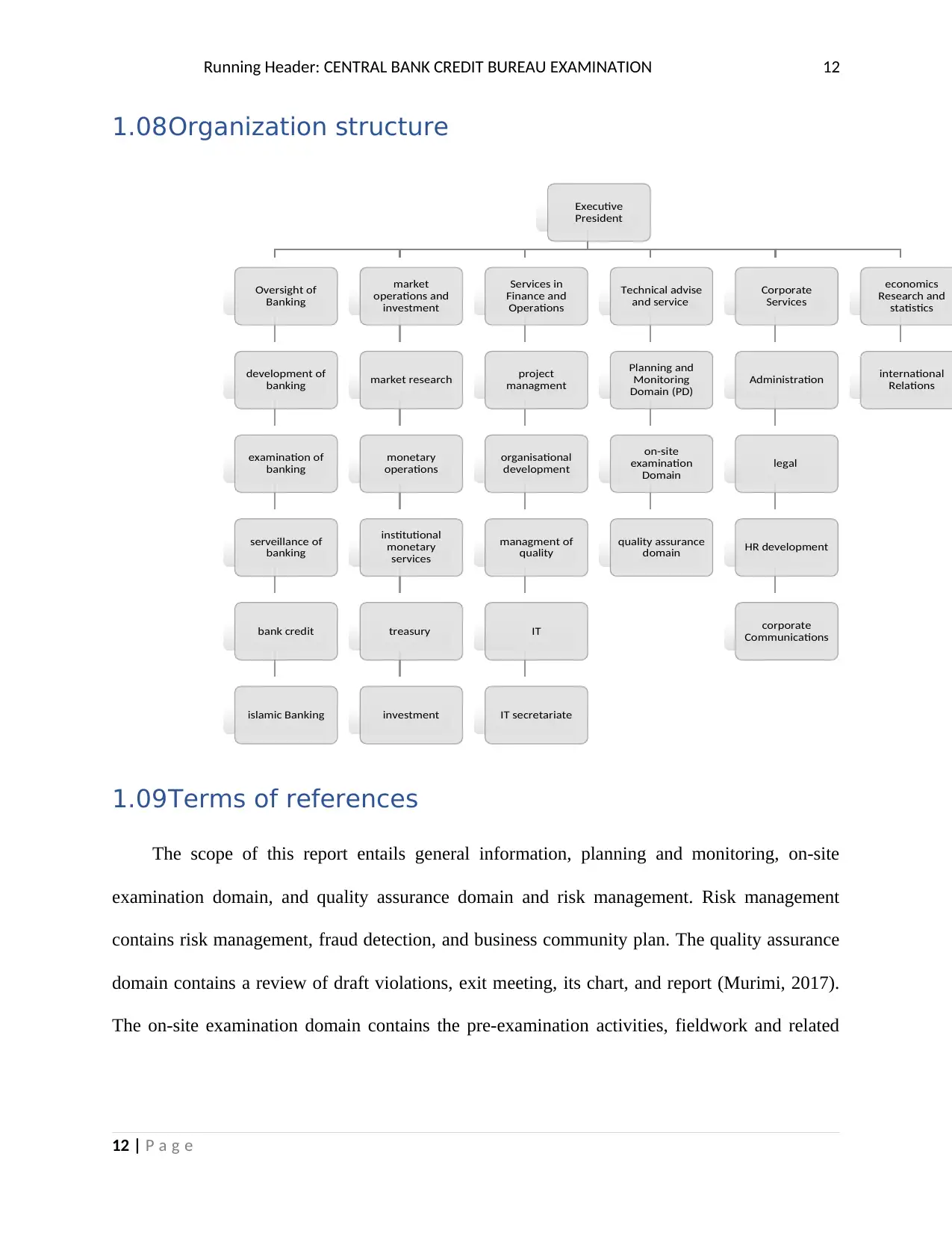

1.08Organization structure

1.09Terms of references

The scope of this report entails general information, planning and monitoring, on-site

examination domain, and quality assurance domain and risk management. Risk management

contains risk management, fraud detection, and business community plan. The quality assurance

domain contains a review of draft violations, exit meeting, its chart, and report (Murimi, 2017).

The on-site examination domain contains the pre-examination activities, fieldwork and related

12 | P a g e

Executive

President

Oversight of

Banking

development of

banking

examination of

banking

serveillance of

banking

bank credit

islamic Banking

market

operations and

investment

market research

monetary

operations

institutional

monetary

services

treasury

investment

Services in

Finance and

Operations

project

managment

organisational

development

managment of

quality

IT

IT secretariate

Technical advise

and service

Planning and

Monitoring

Domain (PD)

on-site

examination

Domain

quality assurance

domain

Corporate

Services

Administration

legal

HR development

corporate

Communications

economics

Research and

statistics

international

Relations

1.08Organization structure

1.09Terms of references

The scope of this report entails general information, planning and monitoring, on-site

examination domain, and quality assurance domain and risk management. Risk management

contains risk management, fraud detection, and business community plan. The quality assurance

domain contains a review of draft violations, exit meeting, its chart, and report (Murimi, 2017).

The on-site examination domain contains the pre-examination activities, fieldwork and related

12 | P a g e

Executive

President

Oversight of

Banking

development of

banking

examination of

banking

serveillance of

banking

bank credit

islamic Banking

market

operations and

investment

market research

monetary

operations

institutional

monetary

services

treasury

investment

Services in

Finance and

Operations

project

managment

organisational

development

managment of

quality

IT

IT secretariate

Technical advise

and service

Planning and

Monitoring

Domain (PD)

on-site

examination

Domain

quality assurance

domain

Corporate

Services

Administration

legal

HR development

corporate

Communications

economics

Research and

statistics

international

Relations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.