Economics of Business: Centrica Plc vs. Southern Energy Plc Analysis

VerifiedAdded on 2020/02/03

|16

|4090

|242

Report

AI Summary

This report presents a comparative financial analysis of Centrica Plc and Southern Energy Plc, examining their performance from 2006 to 2016. The analysis covers key financial metrics such as revenue, gross profit, net income, earnings per share, return on equity, and return on invested capital. The report evaluates the business strategies employed by both companies, highlighting trends in revenue growth, gross profit margins, and net profit margins. It discusses the impact of external factors and internal strategies on their financial outcomes, including the effects of fluctuating oil prices, debt burdens, and strategic decisions related to cost management and investment. The report also delves into the earning per share and provides insights into the factors influencing the profitability and financial stability of both companies, offering a comprehensive overview of their economic performance and strategic approaches within the energy sector. The report concludes by evaluating the effectiveness of business strategies employed by each company and providing a detailed financial comparison.

Economics of the Business Environment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Overview of Organization................................................................................................................3

Analayzing the factors that affect the financial performance of Centrica Plc and Southern

Energy Plc ...................................................................................................................................3

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

Overview of Organization................................................................................................................3

Analayzing the factors that affect the financial performance of Centrica Plc and Southern

Energy Plc ...................................................................................................................................3

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

In today's time there are many fluctuation in economic environment they may be

favorable and unfavorable. Unfavorable condition in business will need some strategies for their

development and growth of economy. Therefore, firm need to understand all market situation

which are rising externally through this, they can set up their business easily in competitive

market situation and will reach out to their ultimate goals. To understand economics of business

environment is very difficult task because they have to consist of all factors which are impact on

their working style. Centrica Plc main competitor is SSE plc therefore, their competition is very

high and they consist of different strategies for understanding market situation. In this report it

consist of performance of firm to its competitor from 2006 to 2016 through this, they can

analysis properly and can set market with macro context.

OVERVIEW OF ORGANIZATION

Analayzing the factors that affect the financial performance of Centrica Plc and Southern

Energy Plc

Centrica Plc is public limited company at United Kingdom and it main aim is to supply

electricity and gas to businesses and consumer. Therefore, it consist of externals factors for

setting up different strategies within organization for maximizing in sale and generating more

energy for UK service users and firms. Thus, organization is involving of new ideas and some

innovative techniques for attracting their customers (Oil and gas sector of UK, 2016). They

consist of small and large scale plants for producing enough electricity.

Scottish Southern Energy Plc is public limited company and its headquarter is in Perth,

United Kingdom. They are delivering products which consist of electricity, natural gas and

broadband to houses and business. It is one of the main constituent of FTSE 100 index. This

business organization is highly involved in the generation and supply of electricity gas. Hence,

other energy related services include gas storage, exploration and production, contracting,

connections and metering. Hence, it is one of the sixth largest firm which has dominated the

energy sector to the large extent. Thus, it is one main rival firms of Centrica Plc

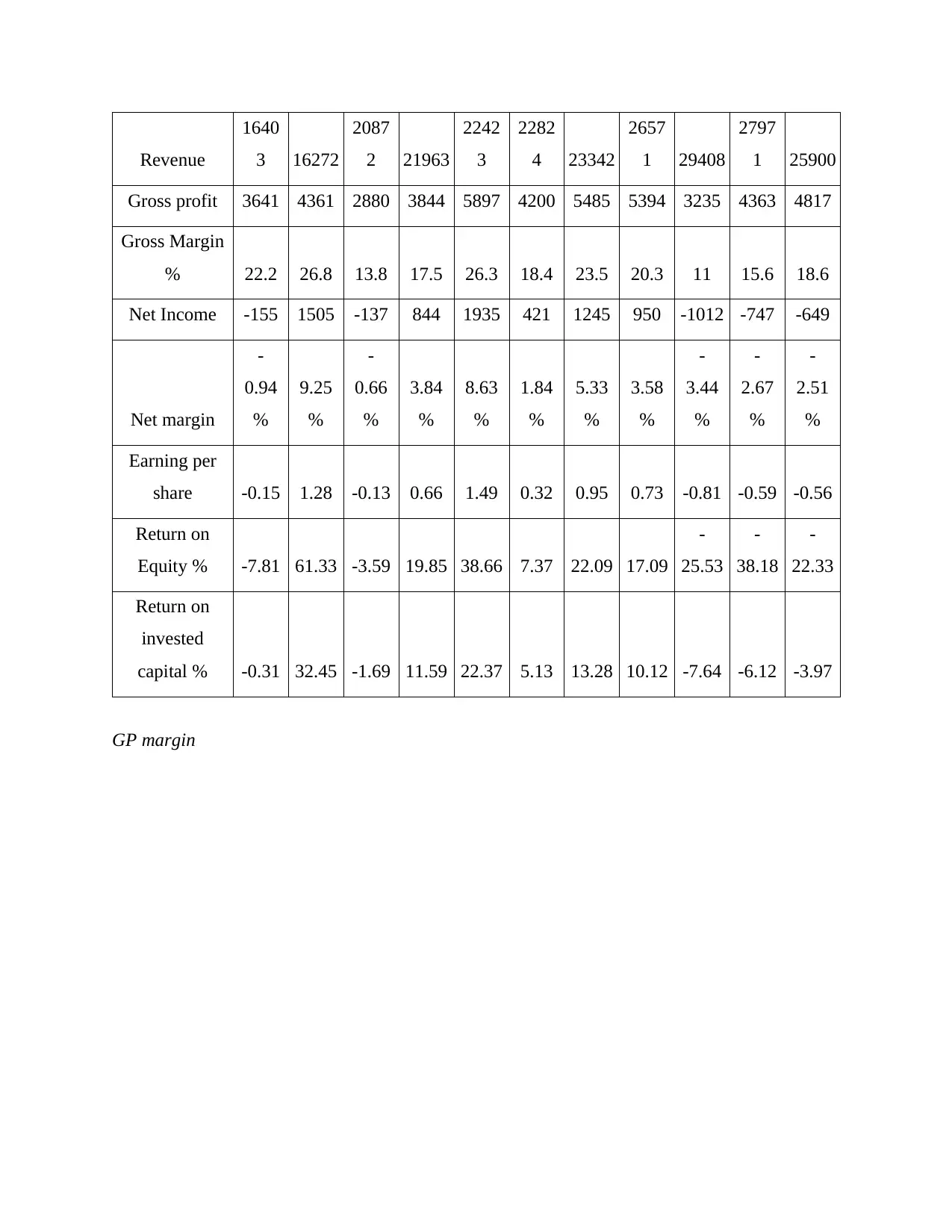

Financial performance of Centrica Plc from 2006 to 2016 are as follows:

Year 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

In today's time there are many fluctuation in economic environment they may be

favorable and unfavorable. Unfavorable condition in business will need some strategies for their

development and growth of economy. Therefore, firm need to understand all market situation

which are rising externally through this, they can set up their business easily in competitive

market situation and will reach out to their ultimate goals. To understand economics of business

environment is very difficult task because they have to consist of all factors which are impact on

their working style. Centrica Plc main competitor is SSE plc therefore, their competition is very

high and they consist of different strategies for understanding market situation. In this report it

consist of performance of firm to its competitor from 2006 to 2016 through this, they can

analysis properly and can set market with macro context.

OVERVIEW OF ORGANIZATION

Analayzing the factors that affect the financial performance of Centrica Plc and Southern

Energy Plc

Centrica Plc is public limited company at United Kingdom and it main aim is to supply

electricity and gas to businesses and consumer. Therefore, it consist of externals factors for

setting up different strategies within organization for maximizing in sale and generating more

energy for UK service users and firms. Thus, organization is involving of new ideas and some

innovative techniques for attracting their customers (Oil and gas sector of UK, 2016). They

consist of small and large scale plants for producing enough electricity.

Scottish Southern Energy Plc is public limited company and its headquarter is in Perth,

United Kingdom. They are delivering products which consist of electricity, natural gas and

broadband to houses and business. It is one of the main constituent of FTSE 100 index. This

business organization is highly involved in the generation and supply of electricity gas. Hence,

other energy related services include gas storage, exploration and production, contracting,

connections and metering. Hence, it is one of the sixth largest firm which has dominated the

energy sector to the large extent. Thus, it is one main rival firms of Centrica Plc

Financial performance of Centrica Plc from 2006 to 2016 are as follows:

Year 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Revenue

1640

3 16272

2087

2 21963

2242

3

2282

4 23342

2657

1 29408

2797

1 25900

Gross profit 3641 4361 2880 3844 5897 4200 5485 5394 3235 4363 4817

Gross Margin

% 22.2 26.8 13.8 17.5 26.3 18.4 23.5 20.3 11 15.6 18.6

Net Income -155 1505 -137 844 1935 421 1245 950 -1012 -747 -649

Net margin

-

0.94

%

9.25

%

-

0.66

%

3.84

%

8.63

%

1.84

%

5.33

%

3.58

%

-

3.44

%

-

2.67

%

-

2.51

%

Earning per

share -0.15 1.28 -0.13 0.66 1.49 0.32 0.95 0.73 -0.81 -0.59 -0.56

Return on

Equity % -7.81 61.33 -3.59 19.85 38.66 7.37 22.09 17.09

-

25.53

-

38.18

-

22.33

Return on

invested

capital % -0.31 32.45 -1.69 11.59 22.37 5.13 13.28 10.12 -7.64 -6.12 -3.97

GP margin

1640

3 16272

2087

2 21963

2242

3

2282

4 23342

2657

1 29408

2797

1 25900

Gross profit 3641 4361 2880 3844 5897 4200 5485 5394 3235 4363 4817

Gross Margin

% 22.2 26.8 13.8 17.5 26.3 18.4 23.5 20.3 11 15.6 18.6

Net Income -155 1505 -137 844 1935 421 1245 950 -1012 -747 -649

Net margin

-

0.94

%

9.25

%

-

0.66

%

3.84

%

8.63

%

1.84

%

5.33

%

3.58

%

-

3.44

%

-

2.67

%

-

2.51

%

Earning per

share -0.15 1.28 -0.13 0.66 1.49 0.32 0.95 0.73 -0.81 -0.59 -0.56

Return on

Equity % -7.81 61.33 -3.59 19.85 38.66 7.37 22.09 17.09

-

25.53

-

38.18

-

22.33

Return on

invested

capital % -0.31 32.45 -1.69 11.59 22.37 5.13 13.28 10.12 -7.64 -6.12 -3.97

GP margin

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ROE

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

G P m argin %

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

G P m argin %

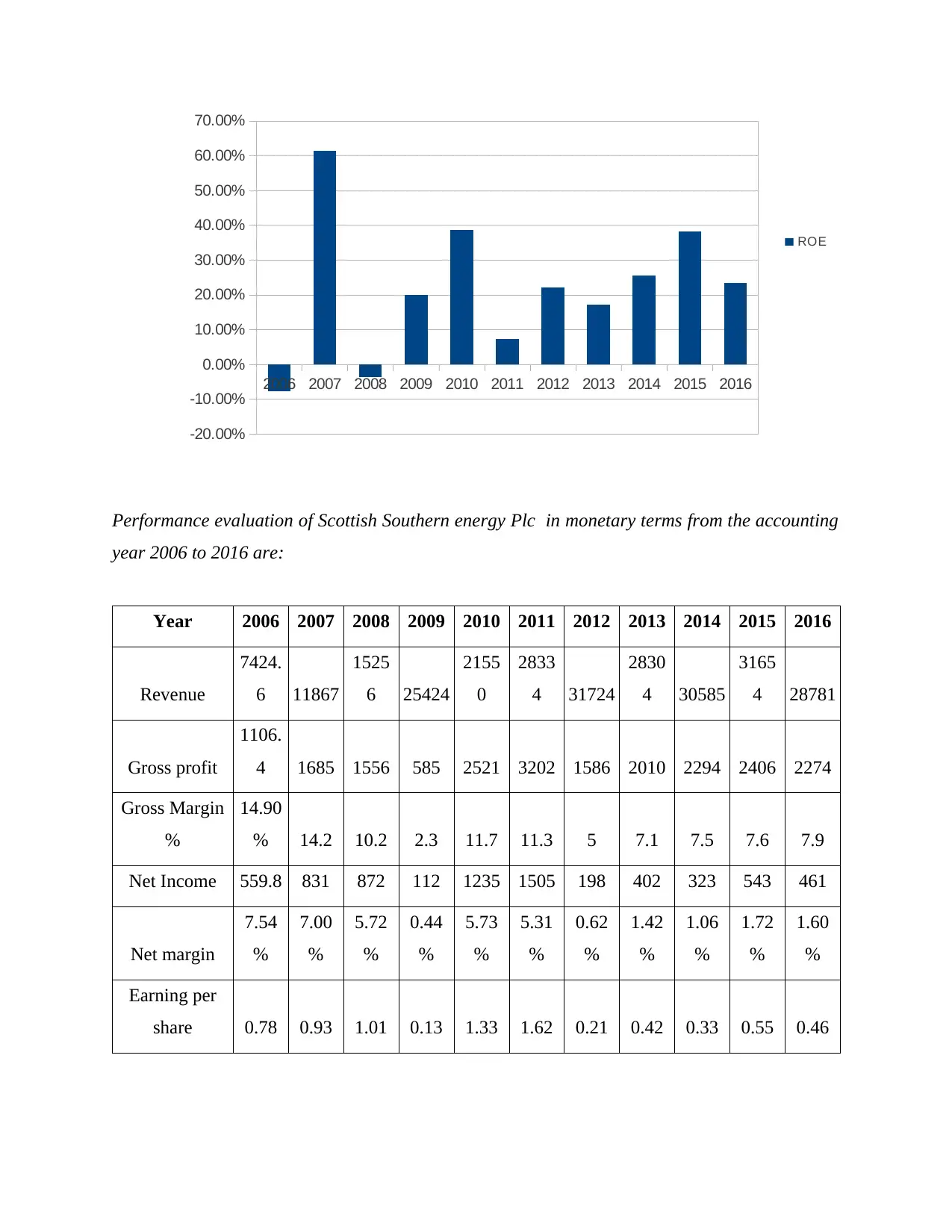

Performance evaluation of Scottish Southern energy Plc in monetary terms from the accounting

year 2006 to 2016 are:

Year 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Revenue

7424.

6 11867

1525

6 25424

2155

0

2833

4 31724

2830

4 30585

3165

4 28781

Gross profit

1106.

4 1685 1556 585 2521 3202 1586 2010 2294 2406 2274

Gross Margin

%

14.90

% 14.2 10.2 2.3 11.7 11.3 5 7.1 7.5 7.6 7.9

Net Income 559.8 831 872 112 1235 1505 198 402 323 543 461

Net margin

7.54

%

7.00

%

5.72

%

0.44

%

5.73

%

5.31

%

0.62

%

1.42

%

1.06

%

1.72

%

1.60

%

Earning per

share 0.78 0.93 1.01 0.13 1.33 1.62 0.21 0.42 0.33 0.55 0.46

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

ROE

year 2006 to 2016 are:

Year 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Revenue

7424.

6 11867

1525

6 25424

2155

0

2833

4 31724

2830

4 30585

3165

4 28781

Gross profit

1106.

4 1685 1556 585 2521 3202 1586 2010 2294 2406 2274

Gross Margin

%

14.90

% 14.2 10.2 2.3 11.7 11.3 5 7.1 7.5 7.6 7.9

Net Income 559.8 831 872 112 1235 1505 198 402 323 543 461

Net margin

7.54

%

7.00

%

5.72

%

0.44

%

5.73

%

5.31

%

0.62

%

1.42

%

1.06

%

1.72

%

1.60

%

Earning per

share 0.78 0.93 1.01 0.13 1.33 1.62 0.21 0.42 0.33 0.55 0.46

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

ROE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

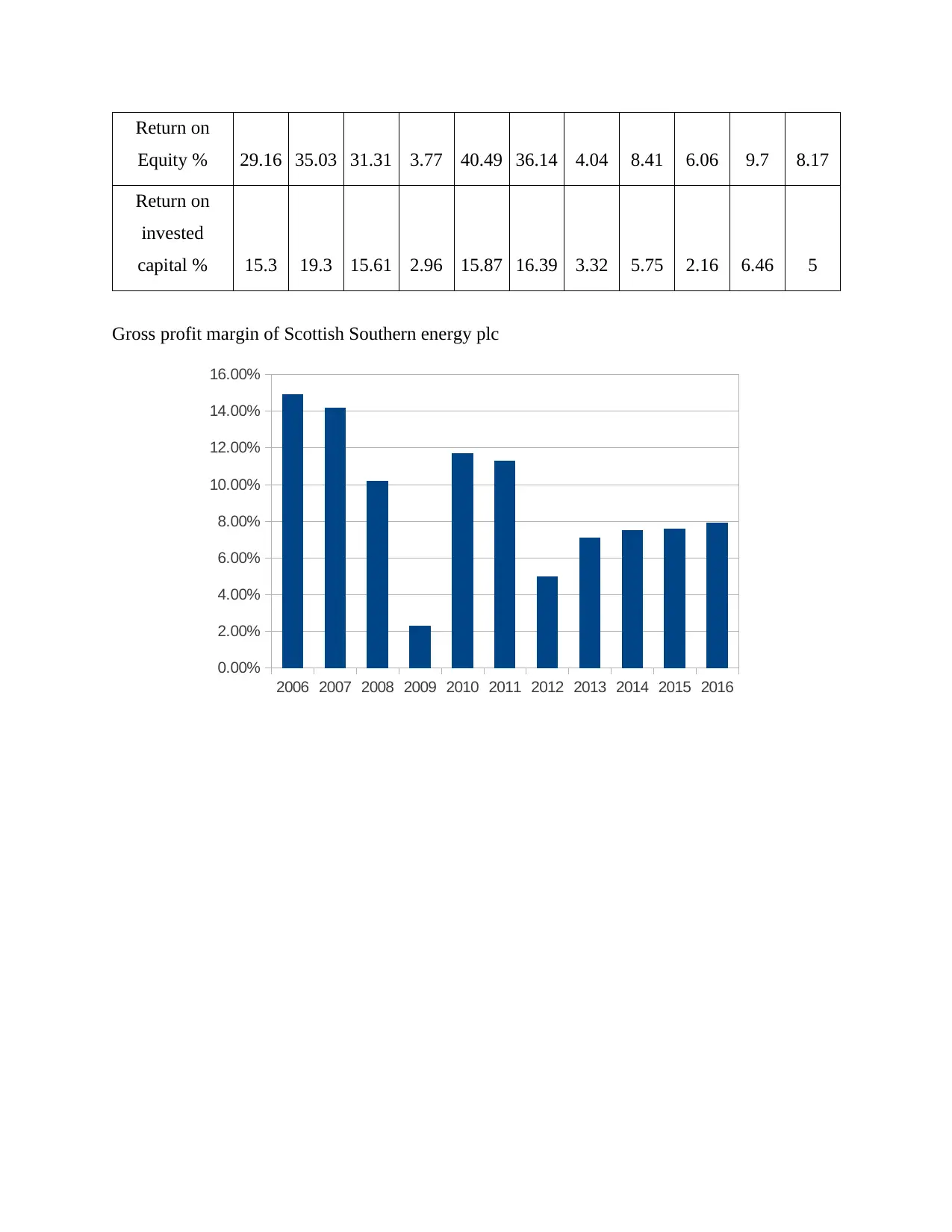

Return on

Equity % 29.16 35.03 31.31 3.77 40.49 36.14 4.04 8.41 6.06 9.7 8.17

Return on

invested

capital % 15.3 19.3 15.61 2.96 15.87 16.39 3.32 5.75 2.16 6.46 5

Gross profit margin of Scottish Southern energy plc

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Equity % 29.16 35.03 31.31 3.77 40.49 36.14 4.04 8.41 6.06 9.7 8.17

Return on

invested

capital % 15.3 19.3 15.61 2.96 15.87 16.39 3.32 5.75 2.16 6.46 5

Gross profit margin of Scottish Southern energy plc

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

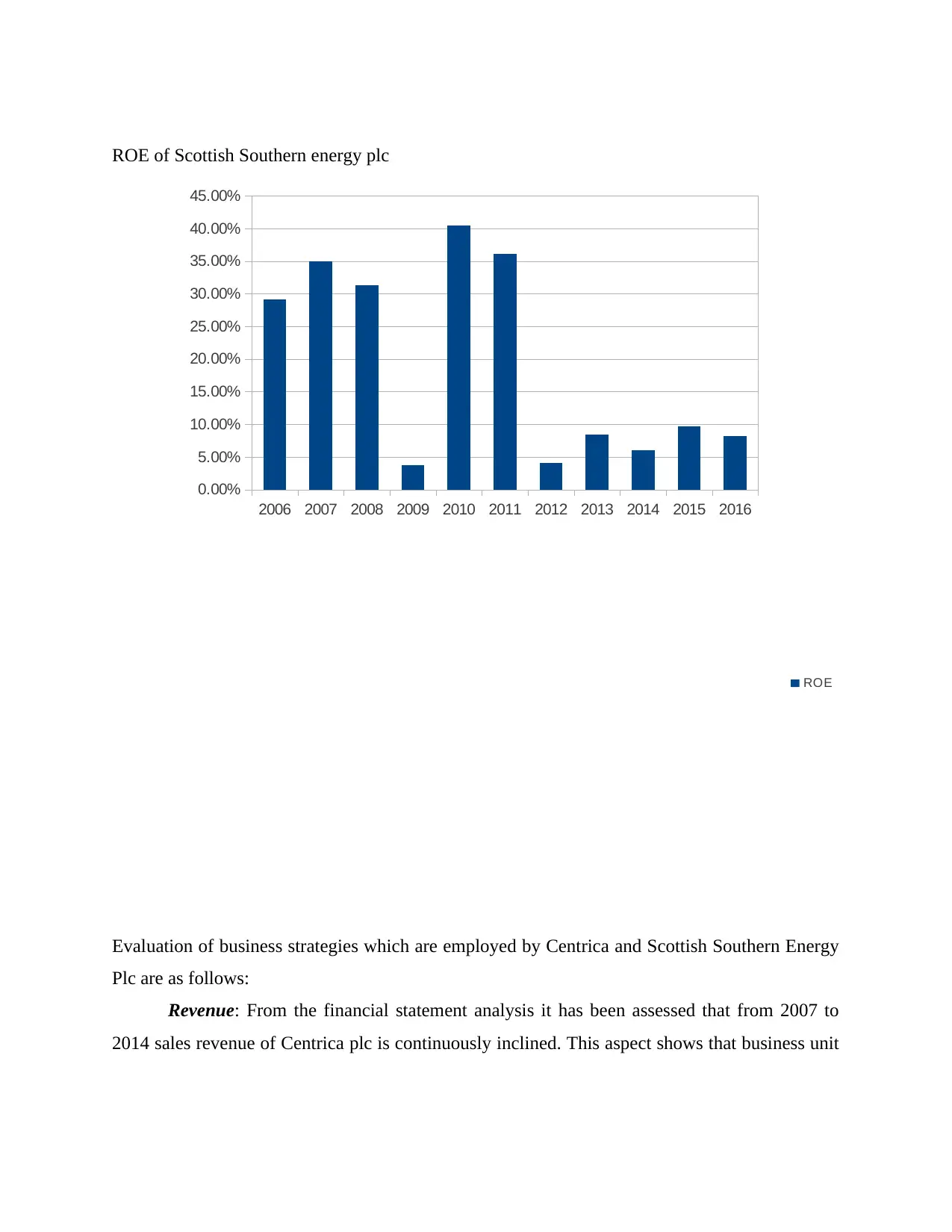

ROE of Scottish Southern energy plc

Evaluation of business strategies which are employed by Centrica and Scottish Southern Energy

Plc are as follows:

Revenue: From the financial statement analysis it has been assessed that from 2007 to

2014 sales revenue of Centrica plc is continuously inclined. This aspect shows that business unit

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

ROE

Evaluation of business strategies which are employed by Centrica and Scottish Southern Energy

Plc are as follows:

Revenue: From the financial statement analysis it has been assessed that from 2007 to

2014 sales revenue of Centrica plc is continuously inclined. This aspect shows that business unit

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

ROE

has employed sound strategic and policy framework. However, on the critical note, in 2015 and

2016 sales revenue of the firm declined irrespective the fact that economic condition of the

country is good (Hamilton and Webster, 2015). On the contrary to it, high level of growth has

been identified in the sales revenue of Southern energy plc. In 2006, revenue of the firm was

£7427.6, whereas at the end of accounting year 2015 such element accounts for the amount of

£31654. In 2016, sales revenue of the firm decreased because price per barrel falls.

Hence, crisis which takes place in the accounting year 2015 and 2016 affected the sales

revenue and profit margin of the firms operated in the oil and gas sector in the negative direction.

Thus, due to the lack of having sound strategic framework Centrica Plc failed to cope with the

situation of crisis. In contrast to this, at the end of accounting year 2015 sales revenue of

Southern energy Plc was £31654. Thus, by taking into consideration such aspect it can be said

that business unit has managed its financial more effectively and efficiently (Solaymani and

et.al., 2015). Along with this, in 2016 sales performance of Southern energy Plc was good as

compared to the rival firm. It shows that business strategies adopted by the firm is high

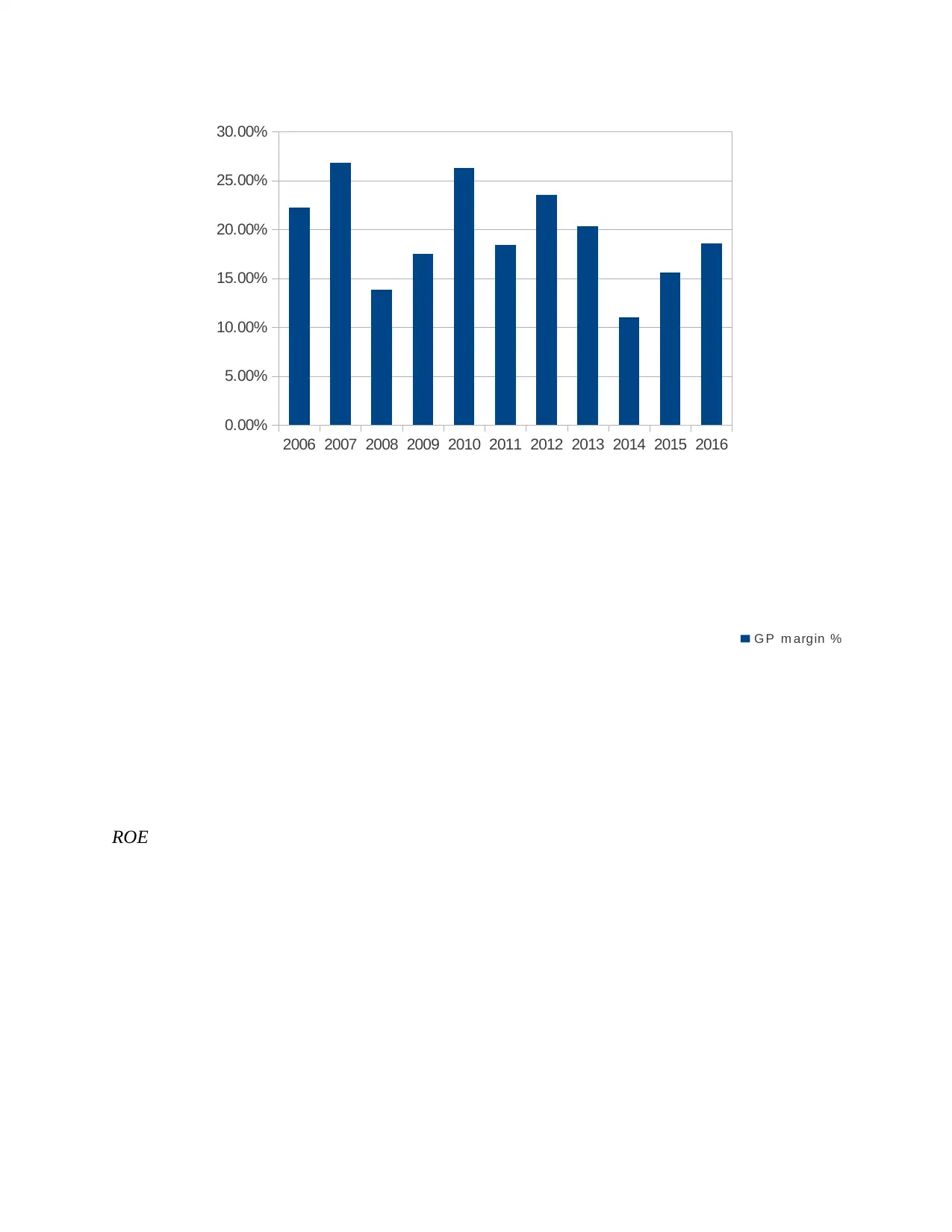

Gross profit (GP) %: It presents the extent to which business unit has managed its direct

expenses from the sales revenue attained by it during the year. Hence, by dividing the gross

profit from net sales business organization and their stakeholders can assess the extent to which

growth takes place in the monetary aspect of firm. From, 2006 to 2016 GP margin of the firm is

showing fluctuating trend in the performance level. During such period most of the time GP

margin decreased irrespective the fact that sales revenue inclined. The reason behind this

company failed to manage the expenses of direct nature more effectively and efficiently. On the

contrary to it, GP margin of Southern Energy plc dropped to the large extent during the last 11

years. In the financial year 2009 gross profit margin of the firm was 2% which is highly lower as

compared to other years. Hence, during this period business unit incurred high level of expenses

for the extraction of oil. High drilling cost is also one of the main factors due to which GP of the

firm reduced significantly. Hence, failure of management in relation to the development of

effectual strategies is one of the main micro factors that impacted the performance of firm in the

negative direction (Richert, Rogers and Burton, 2015). Hence, overall view of the firms

performance entail that Southern energy Plc failed to manage the direct expenses in an effectual

way.

2016 sales revenue of the firm declined irrespective the fact that economic condition of the

country is good (Hamilton and Webster, 2015). On the contrary to it, high level of growth has

been identified in the sales revenue of Southern energy plc. In 2006, revenue of the firm was

£7427.6, whereas at the end of accounting year 2015 such element accounts for the amount of

£31654. In 2016, sales revenue of the firm decreased because price per barrel falls.

Hence, crisis which takes place in the accounting year 2015 and 2016 affected the sales

revenue and profit margin of the firms operated in the oil and gas sector in the negative direction.

Thus, due to the lack of having sound strategic framework Centrica Plc failed to cope with the

situation of crisis. In contrast to this, at the end of accounting year 2015 sales revenue of

Southern energy Plc was £31654. Thus, by taking into consideration such aspect it can be said

that business unit has managed its financial more effectively and efficiently (Solaymani and

et.al., 2015). Along with this, in 2016 sales performance of Southern energy Plc was good as

compared to the rival firm. It shows that business strategies adopted by the firm is high

Gross profit (GP) %: It presents the extent to which business unit has managed its direct

expenses from the sales revenue attained by it during the year. Hence, by dividing the gross

profit from net sales business organization and their stakeholders can assess the extent to which

growth takes place in the monetary aspect of firm. From, 2006 to 2016 GP margin of the firm is

showing fluctuating trend in the performance level. During such period most of the time GP

margin decreased irrespective the fact that sales revenue inclined. The reason behind this

company failed to manage the expenses of direct nature more effectively and efficiently. On the

contrary to it, GP margin of Southern Energy plc dropped to the large extent during the last 11

years. In the financial year 2009 gross profit margin of the firm was 2% which is highly lower as

compared to other years. Hence, during this period business unit incurred high level of expenses

for the extraction of oil. High drilling cost is also one of the main factors due to which GP of the

firm reduced significantly. Hence, failure of management in relation to the development of

effectual strategies is one of the main micro factors that impacted the performance of firm in the

negative direction (Richert, Rogers and Burton, 2015). Hence, overall view of the firms

performance entail that Southern energy Plc failed to manage the direct expenses in an effectual

way.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit (NP) % This measure provides deeper insight about the extent to which

business unit has fund to distribute among the shareholders. Along with this, it also provides

deeper insight about the firms ability in relation to the management of indirect expenses. During

the period of 11 years five times Centrica Plc suffered from the situation of negative return. This

aspect presents that company has incurred high level of expenses in comparison to the other

years. Thus, it reflects that higher management fails to exert effectual control on the expenditure

level during this period. Hence, after facing such critical situation business unit has taken

decision in relation to the reduction of job level to maintain the expenditure.

Along with this, depressed oil prices are also one of the significant factors due to which

net profit margin of the firm was affected in the negative direction. Further, company has also

made its efforts in relation to cutting the prices with the aim to cope up with the price level.

Unfortunately, management failed to manage the expenses that is resulted into lower or negative

profit margin in the last 10 years. Hence, due to the external pressure in terms of reducing the

price of barrel and other crisis Centrica Plc has taken several decisions with the aim to improve

its position in the market. Hence, by taking into account such aspect business enterprise has

taken decision in relation to the cutting down dividend and reducing the level of capital

expenditure (Sadaghiani and et.al., 2015). Thus, it is highly required for the business

organization to change the portfolio mix to the large extent. This in turn helps company in

improving its financial position and performance level to the large extent.

On the other hand, net profitability margin of Southern Energy Plc reduced from 7.54%

to 1.60% at the end of accounting year 2016. Hence, from the financial report it has been

assessed that with the aim to cope with the critical business situations company has undertaken

number of research projects in relation to the renewable energy options including biomass, solar,

wind etc. (Financial statement of Southern Energy Plc, 2009). Further, in 2009, Southern Energy

Plc started projects in relation to finding the most economical ways to perform the

manufacturing aspects or operations. Hence, due to this net profitability aspect of the firm

decreased to the significant level.

Along with this, debt burden is another significant factors due to which profit margin of

the firm declined. Moreover, in the period of 2009 business unit required billion of dollar to

build and maintain smarter, robust transmission and distribution system. In addition to this, to

business unit has fund to distribute among the shareholders. Along with this, it also provides

deeper insight about the firms ability in relation to the management of indirect expenses. During

the period of 11 years five times Centrica Plc suffered from the situation of negative return. This

aspect presents that company has incurred high level of expenses in comparison to the other

years. Thus, it reflects that higher management fails to exert effectual control on the expenditure

level during this period. Hence, after facing such critical situation business unit has taken

decision in relation to the reduction of job level to maintain the expenditure.

Along with this, depressed oil prices are also one of the significant factors due to which

net profit margin of the firm was affected in the negative direction. Further, company has also

made its efforts in relation to cutting the prices with the aim to cope up with the price level.

Unfortunately, management failed to manage the expenses that is resulted into lower or negative

profit margin in the last 10 years. Hence, due to the external pressure in terms of reducing the

price of barrel and other crisis Centrica Plc has taken several decisions with the aim to improve

its position in the market. Hence, by taking into account such aspect business enterprise has

taken decision in relation to the cutting down dividend and reducing the level of capital

expenditure (Sadaghiani and et.al., 2015). Thus, it is highly required for the business

organization to change the portfolio mix to the large extent. This in turn helps company in

improving its financial position and performance level to the large extent.

On the other hand, net profitability margin of Southern Energy Plc reduced from 7.54%

to 1.60% at the end of accounting year 2016. Hence, from the financial report it has been

assessed that with the aim to cope with the critical business situations company has undertaken

number of research projects in relation to the renewable energy options including biomass, solar,

wind etc. (Financial statement of Southern Energy Plc, 2009). Further, in 2009, Southern Energy

Plc started projects in relation to finding the most economical ways to perform the

manufacturing aspects or operations. Hence, due to this net profitability aspect of the firm

decreased to the significant level.

Along with this, debt burden is another significant factors due to which profit margin of

the firm declined. Moreover, in the period of 2009 business unit required billion of dollar to

build and maintain smarter, robust transmission and distribution system. In addition to this, to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expand the grid operations business unit had taken decision to raise debt. Hence high debt and

interest expense is one of the main factors due to which both Centrica and Southern Plc failed to

maintain high level of profit margin especially in the period of 2009. Thus, debt burden is the

main causes behind the decreasing trend in the profit margin (Betz and et.al., 2015). Moreover,

debt instrument such as bank loan and debentures impose fixed periodical financial burden in

front of the firm in terms of interest payment. Thus, it is recommended to the business

organization to undertake limited projects at one time. In this way, by taking the significant

measures or actions both Centrica plc and Southern energy plc would become able to meet the

objectives of themselves and their stakeholders to the large extent.

Earning per share: The amount or proportion of net earnings that Centrica Plc distribute

or allocate to their investors on each holding is called earnings per share (EPS). It is an indicator

of profitability which can be determined by dividing the residual earnings to the number of

outstanding shares. Investors often use this ratio to examine the possibility of return on their

investment in the company. With reference to Centrica Plc, in 2007, growth in net profitability

was the main reason for positive EPS of 1.28. In this year, although revenue dropped down but

still effective control over cost assist management to maximize their net earnings and deliver

more return to the organization (Lamorgese, Geneletti and Partidario, 2015). However,

thereafter, in 2009, EPS got decreased to -0.13 due to adverse market conditions and financial

crisis. As per the chart presented, it can be seen that in the year 2005, Centrica Plc’s net earnings

was only £672m which got improved in 2007 to £1122m but still, in 2009, it came down to

£1111m. In this, year, adjusted EPS remained unchanged to 21.7 pence due to more issuance of

shares as it grown up by 22%. However, in 2007, EPS indicates strong performance because of

favorable commodity prices that driven more revenue and return to the Centrica Plc. As a result,

it became able to deliver better return to their investors (McChlery and et.al., 2015). However, its

Total Shareholder return (TSR) showed an exceptional performance in comparison to FTSE 100

Index as company has outperformed the FTSE Index beyond 20% over a period of 5 year.

However, 2010, stipulated growth in basic EPS and adjusted EPS to 25.2 and 1.49 pence even

after 22% increase in average number of shares. But at the end of the period, its performance

came down because of lower EPS -0.56 whilst adjusted EPS dropped down by 4%.

interest expense is one of the main factors due to which both Centrica and Southern Plc failed to

maintain high level of profit margin especially in the period of 2009. Thus, debt burden is the

main causes behind the decreasing trend in the profit margin (Betz and et.al., 2015). Moreover,

debt instrument such as bank loan and debentures impose fixed periodical financial burden in

front of the firm in terms of interest payment. Thus, it is recommended to the business

organization to undertake limited projects at one time. In this way, by taking the significant

measures or actions both Centrica plc and Southern energy plc would become able to meet the

objectives of themselves and their stakeholders to the large extent.

Earning per share: The amount or proportion of net earnings that Centrica Plc distribute

or allocate to their investors on each holding is called earnings per share (EPS). It is an indicator

of profitability which can be determined by dividing the residual earnings to the number of

outstanding shares. Investors often use this ratio to examine the possibility of return on their

investment in the company. With reference to Centrica Plc, in 2007, growth in net profitability

was the main reason for positive EPS of 1.28. In this year, although revenue dropped down but

still effective control over cost assist management to maximize their net earnings and deliver

more return to the organization (Lamorgese, Geneletti and Partidario, 2015). However,

thereafter, in 2009, EPS got decreased to -0.13 due to adverse market conditions and financial

crisis. As per the chart presented, it can be seen that in the year 2005, Centrica Plc’s net earnings

was only £672m which got improved in 2007 to £1122m but still, in 2009, it came down to

£1111m. In this, year, adjusted EPS remained unchanged to 21.7 pence due to more issuance of

shares as it grown up by 22%. However, in 2007, EPS indicates strong performance because of

favorable commodity prices that driven more revenue and return to the Centrica Plc. As a result,

it became able to deliver better return to their investors (McChlery and et.al., 2015). However, its

Total Shareholder return (TSR) showed an exceptional performance in comparison to FTSE 100

Index as company has outperformed the FTSE Index beyond 20% over a period of 5 year.

However, 2010, stipulated growth in basic EPS and adjusted EPS to 25.2 and 1.49 pence even

after 22% increase in average number of shares. But at the end of the period, its performance

came down because of lower EPS -0.56 whilst adjusted EPS dropped down by 4%.

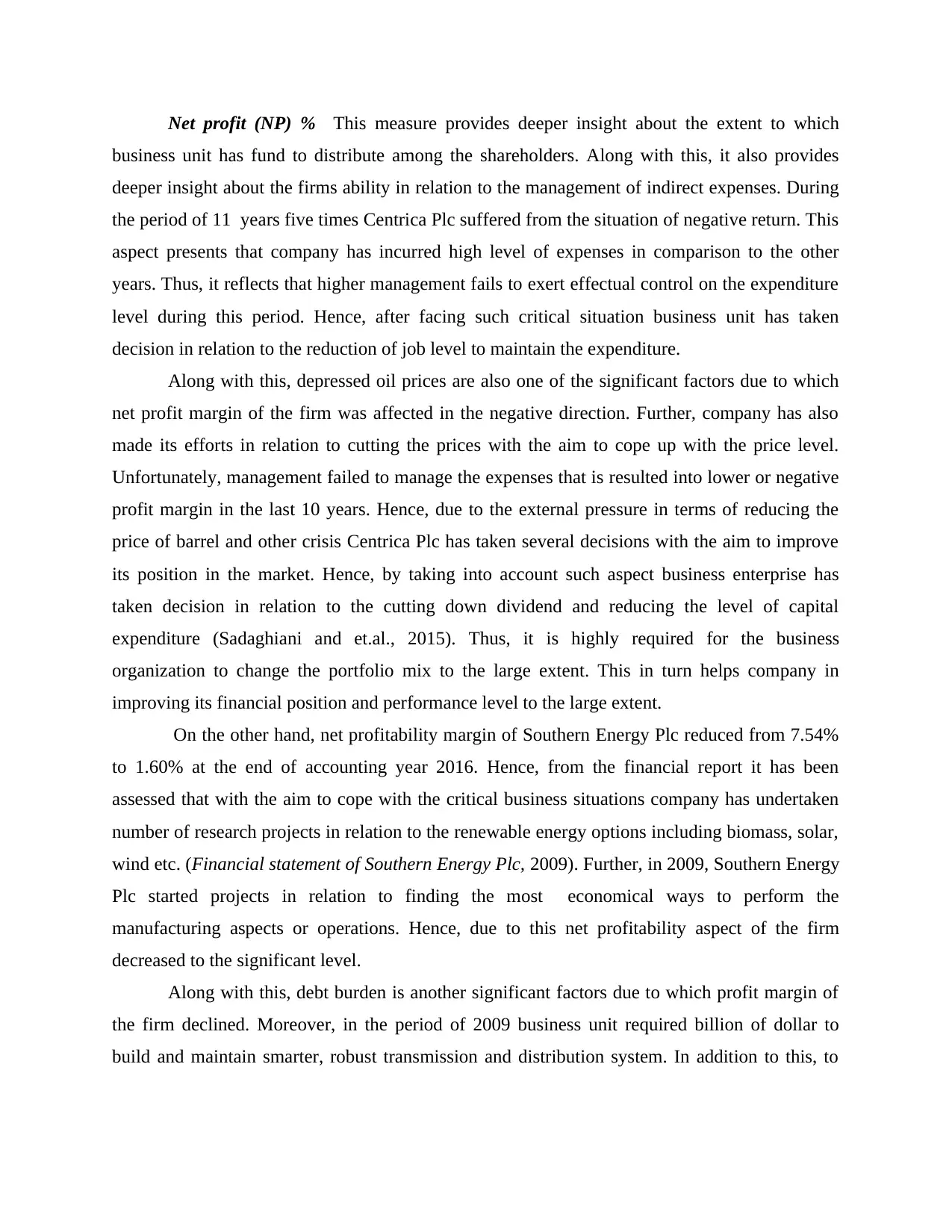

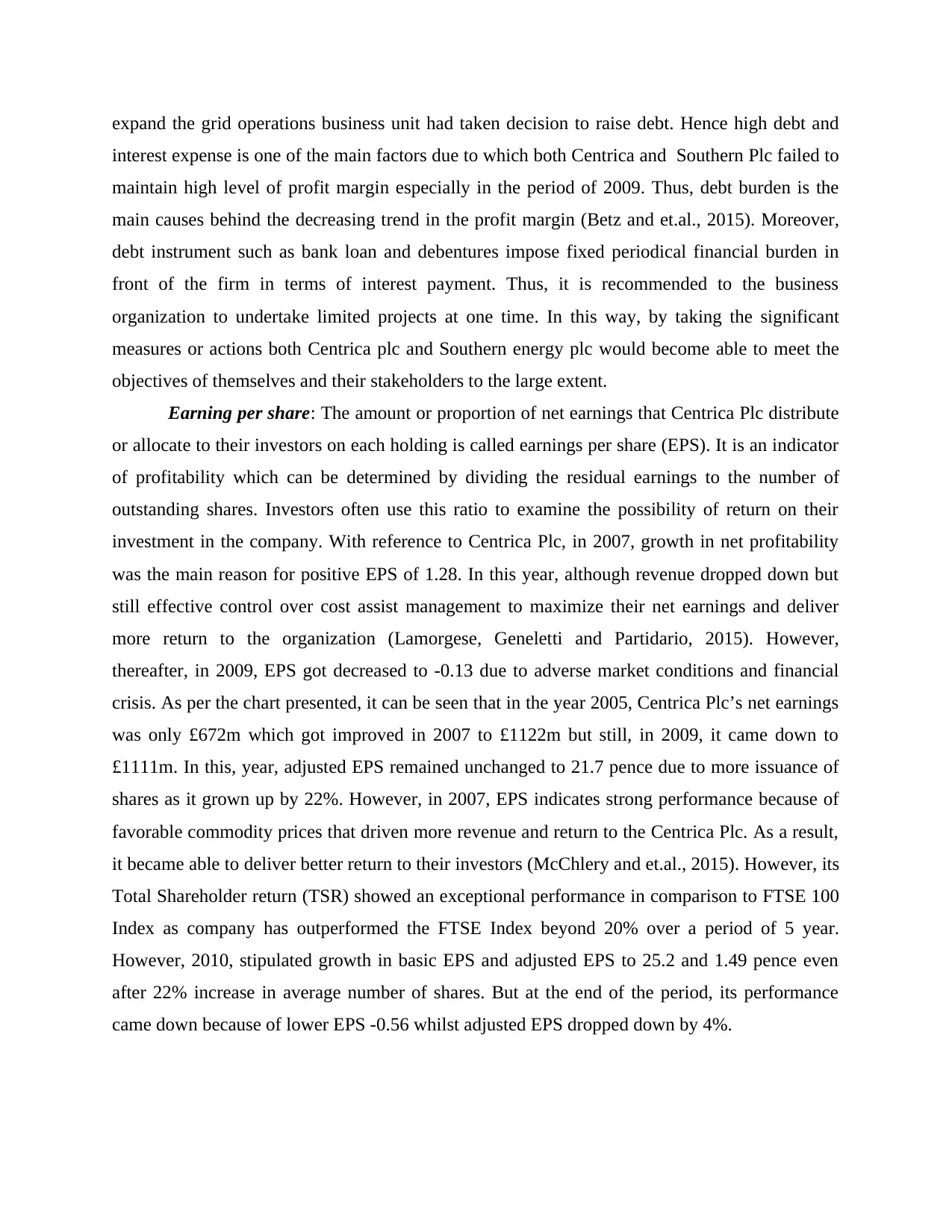

Falling in oil and gas price decreased operating profit by 12% and decreased adjusted

EPS to 17.2p which was 25.9 p in 2013. Its TSR also showed underperformance as in

comparison to FTSE 100, it got reduced by 12.5% in a period of three year. However, on the

other hand, SSE’s EPS showed a rising trend till 2008, but, in 2009, it got decreased to 0.13 in

2009 due to financial instability

and crisis which declined its

product prices for rendered

utility services. It indicates

outturn growth of 3.6% p.a

higher than inflation rate and

showed excellent performance.

However, in 2015, growth in

dividend and net earnings to £543m demonstrates that company performed well in this year. On

full vesting, its EPS is equal to RPI + 8% however, on 25% vesting it is around RPI. Efficient

delivery of energy and utility services, disciplined

investment, strong financial commitment and achieving

EPS to the minimum level of inflation also enable SSE to

reward investors and fulfill their return expectations.

Return on equity: It is a profitability measure which

helps to examine that how much proportion of profitability

firm generated on their investor’s equity capital. In other words, it indicates that how effectively

business equity is managed to generate more and more return in the business. In the year 2006,

Centrica Plc’s ROE showed negative return of 7.81% however, its competitors, SSE’s ROE was

comparatively greater to 29.16%. In the micro-conditions, skilled and talented personnel and

strong managerial decisions to achieve high growth in the market were the reasons behind

favorable ROE in SSE (Sonesson and et.al., 2016). On the contrary, in 2007, Centrica’s ROE got

enhanced to 61.33 higher than that of SSE’s ROE of 35.03 positive. It becomes possible mainly

EPS to 17.2p which was 25.9 p in 2013. Its TSR also showed underperformance as in

comparison to FTSE 100, it got reduced by 12.5% in a period of three year. However, on the

other hand, SSE’s EPS showed a rising trend till 2008, but, in 2009, it got decreased to 0.13 in

2009 due to financial instability

and crisis which declined its

product prices for rendered

utility services. It indicates

outturn growth of 3.6% p.a

higher than inflation rate and

showed excellent performance.

However, in 2015, growth in

dividend and net earnings to £543m demonstrates that company performed well in this year. On

full vesting, its EPS is equal to RPI + 8% however, on 25% vesting it is around RPI. Efficient

delivery of energy and utility services, disciplined

investment, strong financial commitment and achieving

EPS to the minimum level of inflation also enable SSE to

reward investors and fulfill their return expectations.

Return on equity: It is a profitability measure which

helps to examine that how much proportion of profitability

firm generated on their investor’s equity capital. In other words, it indicates that how effectively

business equity is managed to generate more and more return in the business. In the year 2006,

Centrica Plc’s ROE showed negative return of 7.81% however, its competitors, SSE’s ROE was

comparatively greater to 29.16%. In the micro-conditions, skilled and talented personnel and

strong managerial decisions to achieve high growth in the market were the reasons behind

favorable ROE in SSE (Sonesson and et.al., 2016). On the contrary, in 2007, Centrica’s ROE got

enhanced to 61.33 higher than that of SSE’s ROE of 35.03 positive. It becomes possible mainly

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.