Applied Econometrics: Analysis of CEO Salaries and Firm Performance

VerifiedAdded on 2023/03/20

|18

|4047

|93

Report

AI Summary

This report applies econometric techniques to analyze CEO salaries, focusing on factors influencing compensation and firm performance. Task 1 utilizes multiple regression models to assess the impact of variables like return on equity, sales, and industry sectors on CEO salaries. The analysis includes hypothesis testing, such as ANOVA, to determine significant differences in salaries across sectors. Task 2 employs panel data estimators to analyze production functions, discussing the strengths and weaknesses of different estimators and comparing findings with theoretical predictions. The report includes literature reviews, research methodologies, and detailed interpretations of statistical results, such as p-values, R-squared, and tests for heteroskedasticity and multicollinearity. The report also explores percentage changes in CEO salaries over time using multiple regression models. The conclusion summarizes the key findings and implications of the econometric analysis.

Applied Econometrics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

4. Findings...................................................................................................................................4

1. Estimating level of significance @ 5% pertaining to the salaries of two CEO operating in

different sector such as industrial and financial..........................................................................4

2. Assessing 3 multiple regression models to identify the factors that may explain the CEO

salary in 1990...............................................................................................................................5

3. Explaining percentage change in CEO salary over 1989-90 using 3 multiple regression

model...........................................................................................................................................9

4.................................................................................................................................................13

TASK 2..........................................................................................................................................14

a. Specifying and estimating production function using 3 different panel-data estimators.......14

b. Discussing strengths and weaknesses of each panel-data estimator......................................16

c. Identifying preferred estimator and comparing findings with theoretical predictions and

empirical findings......................................................................................................................16

d. Conclusion.............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

4. Findings...................................................................................................................................4

1. Estimating level of significance @ 5% pertaining to the salaries of two CEO operating in

different sector such as industrial and financial..........................................................................4

2. Assessing 3 multiple regression models to identify the factors that may explain the CEO

salary in 1990...............................................................................................................................5

3. Explaining percentage change in CEO salary over 1989-90 using 3 multiple regression

model...........................................................................................................................................9

4.................................................................................................................................................13

TASK 2..........................................................................................................................................14

a. Specifying and estimating production function using 3 different panel-data estimators.......14

b. Discussing strengths and weaknesses of each panel-data estimator......................................16

c. Identifying preferred estimator and comparing findings with theoretical predictions and

empirical findings......................................................................................................................16

d. Conclusion.............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Econometrics is the branch of economics that is highly concerned with the use of and

application of mathematical models in the context of concerned problem or issue. In the present

times, business units lay high level of emphasis on undertaking statistical methods or tools and

techniques for discovering suitable information from economic data set. The present report is

based on different case situations which will provide deeper insight about the manner in which

multiple regression and panel estimation model assists in evaluating the concerned data set.

TASK 1

1. Introduction

In the current times, CEO’s salary determination becomes the major issue which is facing

by the business units. At the time of appointing CEO, several aspects are considered by the

business unit such as skills, experience in the concerned field etc. Hence, this task will provide

deeper insight about the factors that have an influence on CEO’s salary determination. Further, it

also entails the manner in which regression as well as post-estimation tests assist in making

evaluation of hypotheses and thereby making decisions.

2. Literature review

According to the views of Bragaw and Misangyi (2017) high level of relationship takes

place between pay and performance of CEO. Moreover, the main motive of business unit is to

maximize the wealth of shareholders to a great extent. Hence, this is one of the main factors from

which aspect of CEO’s salary determination are highly influenced. On the other side, Hou, Priem

and Goranova (2017) benchmark is the major factors that closely impact the level of CEO

compensation. In other words, it can be depicted that salary or compensation of CEO is highly

competitive and in line with the offerings of similar companies. Further, investors’ confidence on

concerned CEO also has greater impact on the salary of CEO. Moreover, investors usually gives

priority to the CEO who maximizes their wealth and returns as well.

3. Research methodology

Econometrics is the branch of economics that is highly concerned with the use of and

application of mathematical models in the context of concerned problem or issue. In the present

times, business units lay high level of emphasis on undertaking statistical methods or tools and

techniques for discovering suitable information from economic data set. The present report is

based on different case situations which will provide deeper insight about the manner in which

multiple regression and panel estimation model assists in evaluating the concerned data set.

TASK 1

1. Introduction

In the current times, CEO’s salary determination becomes the major issue which is facing

by the business units. At the time of appointing CEO, several aspects are considered by the

business unit such as skills, experience in the concerned field etc. Hence, this task will provide

deeper insight about the factors that have an influence on CEO’s salary determination. Further, it

also entails the manner in which regression as well as post-estimation tests assist in making

evaluation of hypotheses and thereby making decisions.

2. Literature review

According to the views of Bragaw and Misangyi (2017) high level of relationship takes

place between pay and performance of CEO. Moreover, the main motive of business unit is to

maximize the wealth of shareholders to a great extent. Hence, this is one of the main factors from

which aspect of CEO’s salary determination are highly influenced. On the other side, Hou, Priem

and Goranova (2017) benchmark is the major factors that closely impact the level of CEO

compensation. In other words, it can be depicted that salary or compensation of CEO is highly

competitive and in line with the offerings of similar companies. Further, investors’ confidence on

concerned CEO also has greater impact on the salary of CEO. Moreover, investors usually gives

priority to the CEO who maximizes their wealth and returns as well.

3. Research methodology

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the current study, 209 observations related to the CEO salary has been use to assess the

factors that have impact on the salary structure of chief executive officer. In this, regression test

of statistics has been applied using stata to assess the impact of different variables on CEO’s

salary. In addition to this post-estimation tests have also been conducted to ascertain the

suitability of variables undertaken.

4. Findings

1. Estimating level of significance @ 5% pertaining to the salaries of two CEO operating in

different sector such as industrial and financial

Null hypothesis (H0): There is no significant difference takes place in the mean value of CEO’s

salary operating in industrial and financial sector.

Alternative hypothesis (H1): There is a significant difference takes place in the mean value of

CEO’s salary operating in industrial and financial sector.

.

Total 391732982 208 1883331.64

Residual 389750161 206 1891991.07

indus#finance 0 0

finance 654.319657 1 654.319657 0.00 0.9852

indus 1742789.68 1 1742789.68 0.92 0.3383

Model 1982821.25 2 991410.626 0.52 0.5929

Source Partial SS df MS F Prob > F

Root MSE = 1375.5 Adj R-squared = -0.0046

Number of obs = 209 R-squared = 0.0051

. anova salary indus## finance

Total 391732982 208 1883331.64

Residual 391732982 208 1883331.64

Model 0 0

Source Partial SS df MS F Prob > F

Root MSE = 1372.35 Adj R-squared = 0.0000

Number of obs = 209 R-squared = 0.0000

. anova salary

factors that have impact on the salary structure of chief executive officer. In this, regression test

of statistics has been applied using stata to assess the impact of different variables on CEO’s

salary. In addition to this post-estimation tests have also been conducted to ascertain the

suitability of variables undertaken.

4. Findings

1. Estimating level of significance @ 5% pertaining to the salaries of two CEO operating in

different sector such as industrial and financial

Null hypothesis (H0): There is no significant difference takes place in the mean value of CEO’s

salary operating in industrial and financial sector.

Alternative hypothesis (H1): There is a significant difference takes place in the mean value of

CEO’s salary operating in industrial and financial sector.

.

Total 391732982 208 1883331.64

Residual 389750161 206 1891991.07

indus#finance 0 0

finance 654.319657 1 654.319657 0.00 0.9852

indus 1742789.68 1 1742789.68 0.92 0.3383

Model 1982821.25 2 991410.626 0.52 0.5929

Source Partial SS df MS F Prob > F

Root MSE = 1375.5 Adj R-squared = -0.0046

Number of obs = 209 R-squared = 0.0051

. anova salary indus## finance

Total 391732982 208 1883331.64

Residual 391732982 208 1883331.64

Model 0 0

Source Partial SS df MS F Prob > F

Root MSE = 1372.35 Adj R-squared = 0.0000

Number of obs = 209 R-squared = 0.0000

. anova salary

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Applying Two-way ANOVA test on data set, it has found that p value is greater than 0.05

in the context of both industrial and financial sector. By taking into such outcome, it can be

depicted that null hypothesis is accepted. In accordance with such aspect, salaries of CEO

working in industrial and financial sector are moving in the similar direction.

2. Assessing 3 multiple regression models to identify the factors that may explain the CEO salary in

1990

Model 1- CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷𝟐sales + 𝜺𝒊

Model 2: CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷𝟐sales + 𝜷3ros + 𝜺𝒊

Model 3: CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷2ros + 𝜷3indus + 𝜷4consprod + 𝜷4finance + 𝜷5utility +𝜺𝒊

Model 1- CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷𝟐sales + 𝜺𝒊

_cons 830.6313 223.9049 3.71 0.000 389.1924 1272.07

roe 19.63097 11.07655 1.77 0.078 -2.20697 41.46891

sales .0163416 .0088736 1.84 0.067 -.0011532 .0338363

salary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 391732982 208 1883331.64 Root MSE = 1358.7

Adj R-squared = 0.0197

Residual 380305470 206 1846143.06 R-squared = 0.0292

Model 11427511.8 2 5713755.89 Prob > F = 0.0474

F( 2, 206) = 3.09

Source SS df MS Number of obs = 209

. regress salary sales roe

Interpretation: the above depicted table shows that value r square accounts for .02

respectively. This aspect shows that dependent variable such as salary of CEO will not be

affected significantly if changes take place in the independent variable. Further, p value under

each category is greater than standard limit such as 0.05. By taking into account such aspect, it

can be depicted that null hypothesis is true and other one is rejected. In accordance with the

in the context of both industrial and financial sector. By taking into such outcome, it can be

depicted that null hypothesis is accepted. In accordance with such aspect, salaries of CEO

working in industrial and financial sector are moving in the similar direction.

2. Assessing 3 multiple regression models to identify the factors that may explain the CEO salary in

1990

Model 1- CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷𝟐sales + 𝜺𝒊

Model 2: CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷𝟐sales + 𝜷3ros + 𝜺𝒊

Model 3: CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷2ros + 𝜷3indus + 𝜷4consprod + 𝜷4finance + 𝜷5utility +𝜺𝒊

Model 1- CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷𝟐sales + 𝜺𝒊

_cons 830.6313 223.9049 3.71 0.000 389.1924 1272.07

roe 19.63097 11.07655 1.77 0.078 -2.20697 41.46891

sales .0163416 .0088736 1.84 0.067 -.0011532 .0338363

salary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 391732982 208 1883331.64 Root MSE = 1358.7

Adj R-squared = 0.0197

Residual 380305470 206 1846143.06 R-squared = 0.0292

Model 11427511.8 2 5713755.89 Prob > F = 0.0474

F( 2, 206) = 3.09

Source SS df MS Number of obs = 209

. regress salary sales roe

Interpretation: the above depicted table shows that value r square accounts for .02

respectively. This aspect shows that dependent variable such as salary of CEO will not be

affected significantly if changes take place in the independent variable. Further, p value under

each category is greater than standard limit such as 0.05. By taking into account such aspect, it

can be depicted that null hypothesis is true and other one is rejected. In accordance with the

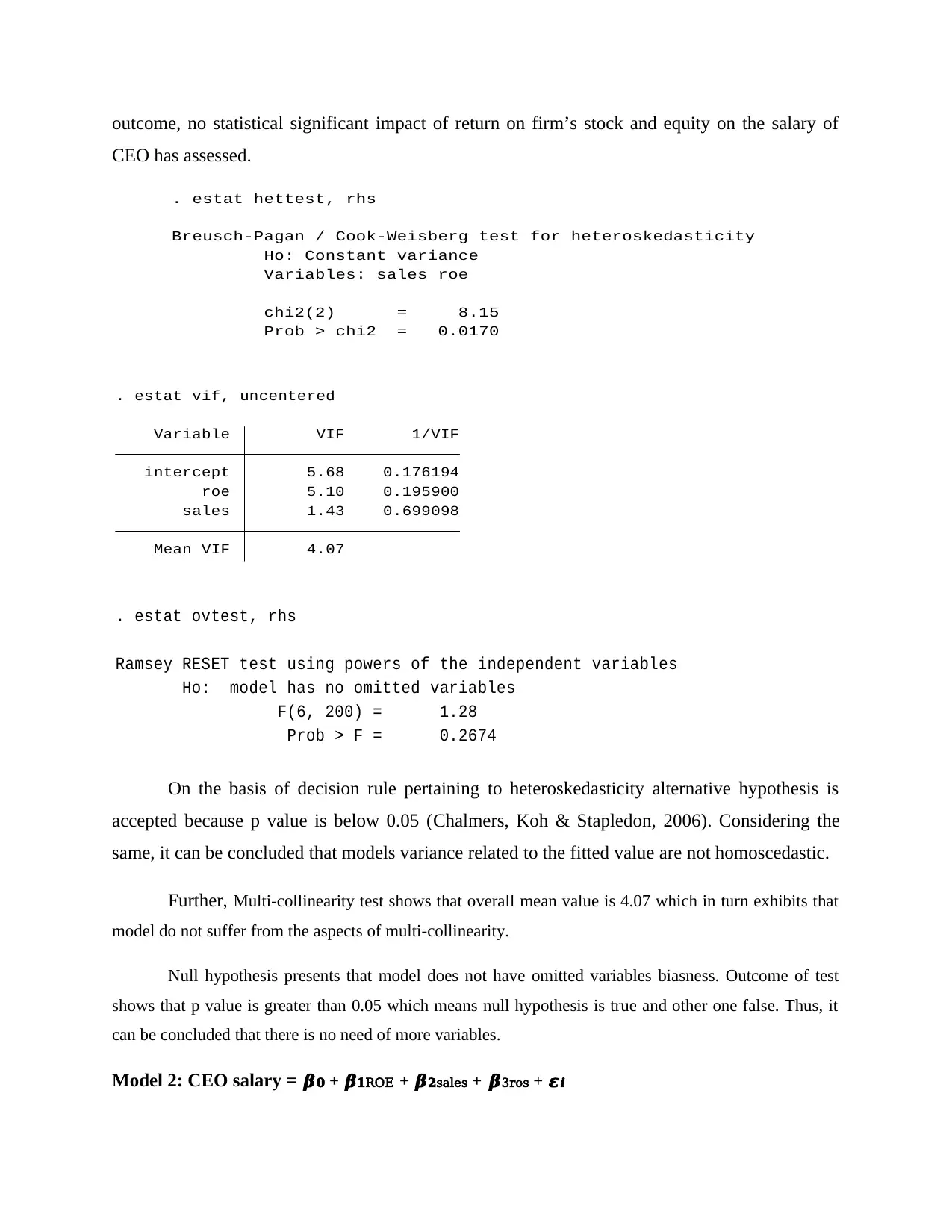

outcome, no statistical significant impact of return on firm’s stock and equity on the salary of

CEO has assessed.

Prob > chi2 = 0.0170

chi2(2) = 8.15

Variables: sales roe

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

Mean VIF 4.07

sales 1.43 0.699098

roe 5.10 0.195900

intercept 5.68 0.176194

Variable VIF 1/VIF

. estat vif, uncentered

Prob > F = 0.2674

F(6, 200) = 1.28

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

On the basis of decision rule pertaining to heteroskedasticity alternative hypothesis is

accepted because p value is below 0.05 (Chalmers, Koh & Stapledon, 2006). Considering the

same, it can be concluded that models variance related to the fitted value are not homoscedastic.

Further, Multi-collinearity test shows that overall mean value is 4.07 which in turn exhibits that

model do not suffer from the aspects of multi-collinearity.

Null hypothesis presents that model does not have omitted variables biasness. Outcome of test

shows that p value is greater than 0.05 which means null hypothesis is true and other one false. Thus, it

can be concluded that there is no need of more variables.

Model 2: CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷𝟐sales + 𝜷3ros + 𝜺𝒊

CEO has assessed.

Prob > chi2 = 0.0170

chi2(2) = 8.15

Variables: sales roe

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

Mean VIF 4.07

sales 1.43 0.699098

roe 5.10 0.195900

intercept 5.68 0.176194

Variable VIF 1/VIF

. estat vif, uncentered

Prob > F = 0.2674

F(6, 200) = 1.28

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

On the basis of decision rule pertaining to heteroskedasticity alternative hypothesis is

accepted because p value is below 0.05 (Chalmers, Koh & Stapledon, 2006). Considering the

same, it can be concluded that models variance related to the fitted value are not homoscedastic.

Further, Multi-collinearity test shows that overall mean value is 4.07 which in turn exhibits that

model do not suffer from the aspects of multi-collinearity.

Null hypothesis presents that model does not have omitted variables biasness. Outcome of test

shows that p value is greater than 0.05 which means null hypothesis is true and other one false. Thus, it

can be concluded that there is no need of more variables.

Model 2: CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷𝟐sales + 𝜷3ros + 𝜺𝒊

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

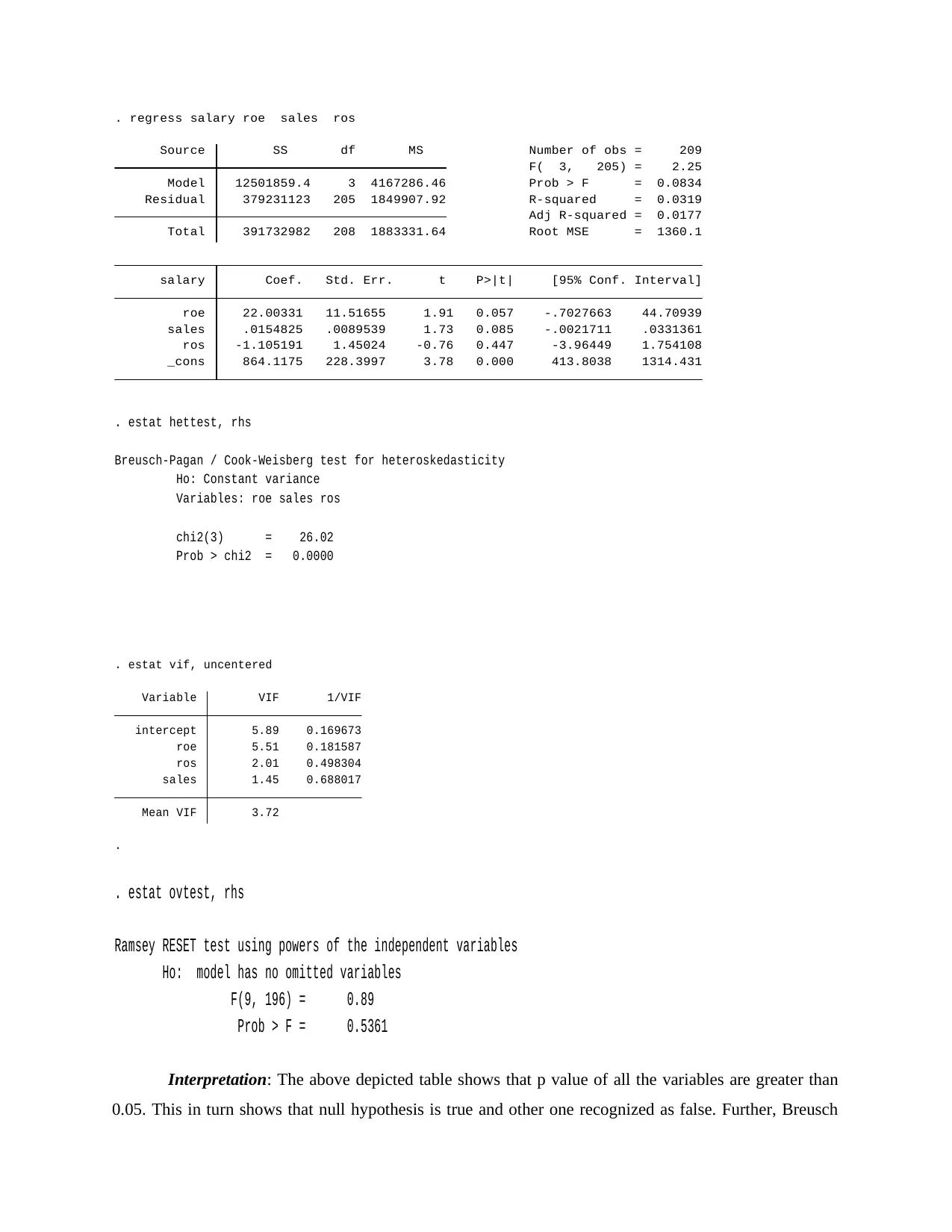

_cons 864.1175 228.3997 3.78 0.000 413.8038 1314.431

ros -1.105191 1.45024 -0.76 0.447 -3.96449 1.754108

sales .0154825 .0089539 1.73 0.085 -.0021711 .0331361

roe 22.00331 11.51655 1.91 0.057 -.7027663 44.70939

salary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 391732982 208 1883331.64 Root MSE = 1360.1

Adj R-squared = 0.0177

Residual 379231123 205 1849907.92 R-squared = 0.0319

Model 12501859.4 3 4167286.46 Prob > F = 0.0834

F( 3, 205) = 2.25

Source SS df MS Number of obs = 209

. regress salary roe sales ros

Prob > chi2 = 0.0000

chi2(3) = 26.02

Variables: roe sales ros

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

.

Mean VIF 3.72

sales 1.45 0.688017

ros 2.01 0.498304

roe 5.51 0.181587

intercept 5.89 0.169673

Variable VIF 1/VIF

. estat vif, uncentered

Prob > F = 0.5361

F(9, 196) = 0.89

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

Interpretation: The above depicted table shows that p value of all the variables are greater than

0.05. This in turn shows that null hypothesis is true and other one recognized as false. Further, Breusch

ros -1.105191 1.45024 -0.76 0.447 -3.96449 1.754108

sales .0154825 .0089539 1.73 0.085 -.0021711 .0331361

roe 22.00331 11.51655 1.91 0.057 -.7027663 44.70939

salary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 391732982 208 1883331.64 Root MSE = 1360.1

Adj R-squared = 0.0177

Residual 379231123 205 1849907.92 R-squared = 0.0319

Model 12501859.4 3 4167286.46 Prob > F = 0.0834

F( 3, 205) = 2.25

Source SS df MS Number of obs = 209

. regress salary roe sales ros

Prob > chi2 = 0.0000

chi2(3) = 26.02

Variables: roe sales ros

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

.

Mean VIF 3.72

sales 1.45 0.688017

ros 2.01 0.498304

roe 5.51 0.181587

intercept 5.89 0.169673

Variable VIF 1/VIF

. estat vif, uncentered

Prob > F = 0.5361

F(9, 196) = 0.89

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

Interpretation: The above depicted table shows that p value of all the variables are greater than

0.05. This in turn shows that null hypothesis is true and other one recognized as false. Further, Breusch

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pagnan test model presents that p value is below the standard limit such as 0.05 which in turn shows that

alternative hypothesis is appropriate over null (Brick, Palmon & Wald, 2006). Mean as per multi-

collinearity test accounts for 3.72 significantly. This in turn exhibits that model does not suffering from

multi-collinearity. Ramsey test model shows that p>0.05 that means model does not suffer from any

errors.

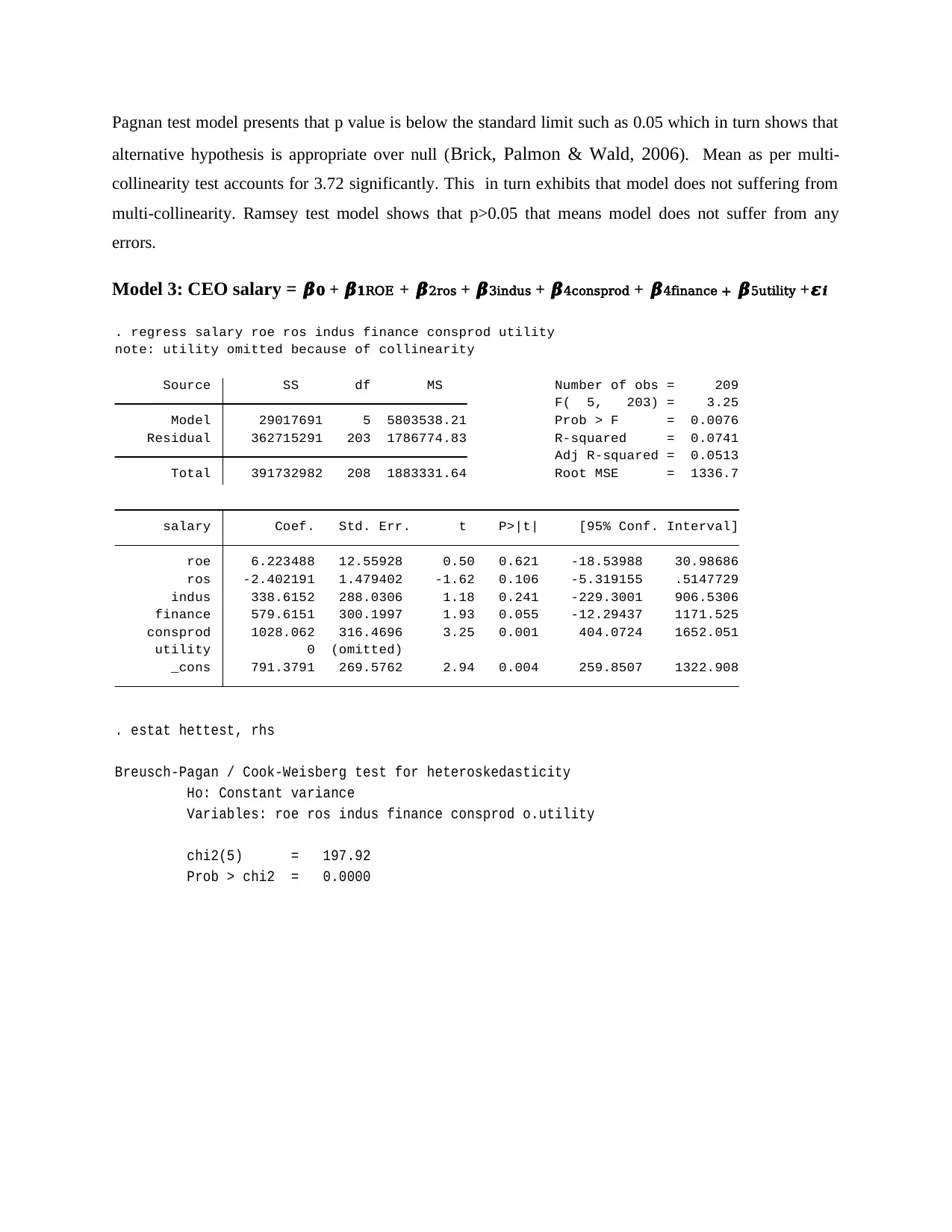

Model 3: CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷2ros + 𝜷3indus + 𝜷4consprod + 𝜷4finance + 𝜷5utility +𝜺𝒊

_cons 791.3791 269.5762 2.94 0.004 259.8507 1322.908

utility 0 (omitted)

consprod 1028.062 316.4696 3.25 0.001 404.0724 1652.051

finance 579.6151 300.1997 1.93 0.055 -12.29437 1171.525

indus 338.6152 288.0306 1.18 0.241 -229.3001 906.5306

ros -2.402191 1.479402 -1.62 0.106 -5.319155 .5147729

roe 6.223488 12.55928 0.50 0.621 -18.53988 30.98686

salary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 391732982 208 1883331.64 Root MSE = 1336.7

Adj R-squared = 0.0513

Residual 362715291 203 1786774.83 R-squared = 0.0741

Model 29017691 5 5803538.21 Prob > F = 0.0076

F( 5, 203) = 3.25

Source SS df MS Number of obs = 209

note: utility omitted because of collinearity

. regress salary roe ros indus finance consprod utility

Prob > chi2 = 0.0000

chi2(5) = 197.92

Variables: roe ros indus finance consprod o.utility

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

alternative hypothesis is appropriate over null (Brick, Palmon & Wald, 2006). Mean as per multi-

collinearity test accounts for 3.72 significantly. This in turn exhibits that model does not suffering from

multi-collinearity. Ramsey test model shows that p>0.05 that means model does not suffer from any

errors.

Model 3: CEO salary = 𝜷𝟎 + 𝜷𝟏ROE + 𝜷2ros + 𝜷3indus + 𝜷4consprod + 𝜷4finance + 𝜷5utility +𝜺𝒊

_cons 791.3791 269.5762 2.94 0.004 259.8507 1322.908

utility 0 (omitted)

consprod 1028.062 316.4696 3.25 0.001 404.0724 1652.051

finance 579.6151 300.1997 1.93 0.055 -12.29437 1171.525

indus 338.6152 288.0306 1.18 0.241 -229.3001 906.5306

ros -2.402191 1.479402 -1.62 0.106 -5.319155 .5147729

roe 6.223488 12.55928 0.50 0.621 -18.53988 30.98686

salary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 391732982 208 1883331.64 Root MSE = 1336.7

Adj R-squared = 0.0513

Residual 362715291 203 1786774.83 R-squared = 0.0741

Model 29017691 5 5803538.21 Prob > F = 0.0076

F( 5, 203) = 3.25

Source SS df MS Number of obs = 209

note: utility omitted because of collinearity

. regress salary roe ros indus finance consprod utility

Prob > chi2 = 0.0000

chi2(5) = 197.92

Variables: roe ros indus finance consprod o.utility

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

.

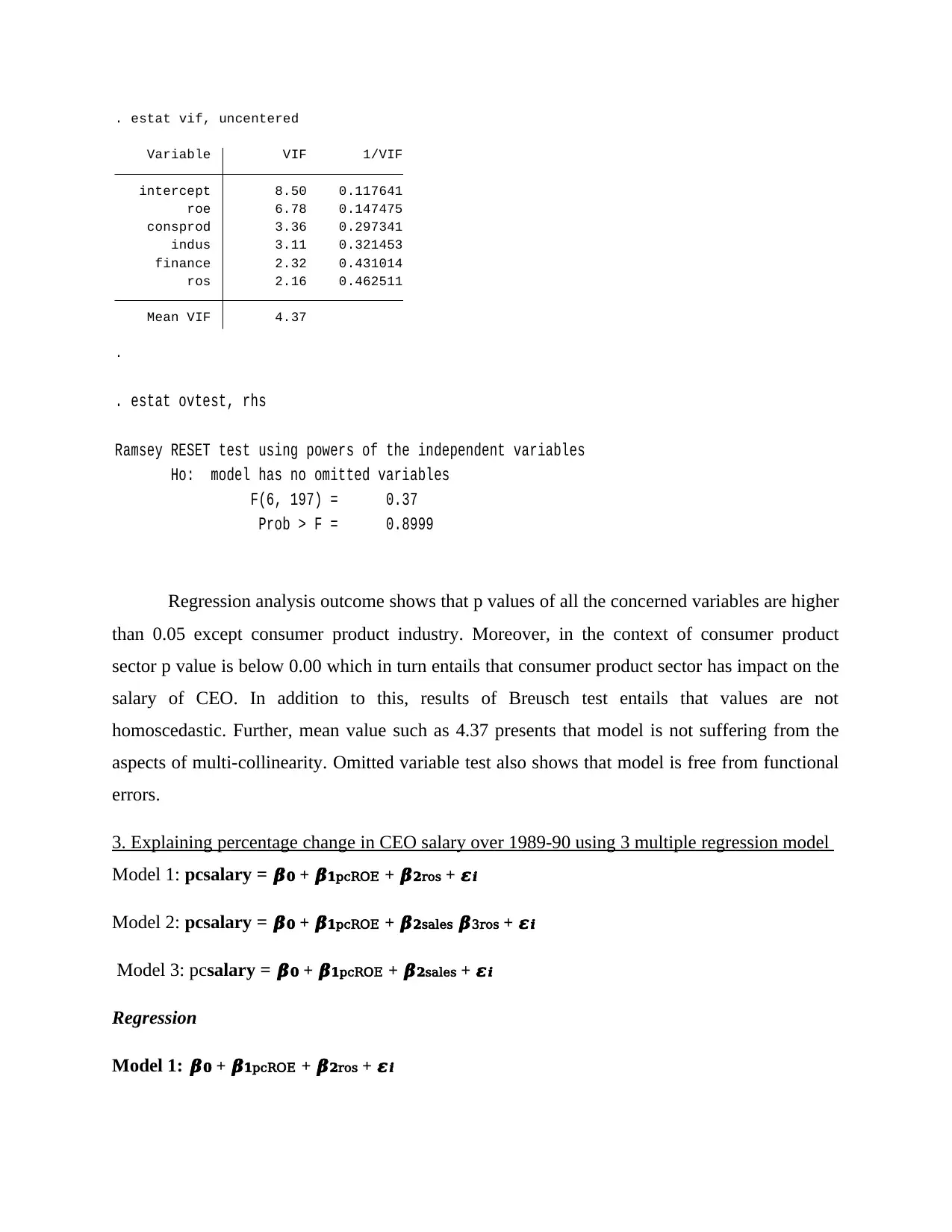

Mean VIF 4.37

ros 2.16 0.462511

finance 2.32 0.431014

indus 3.11 0.321453

consprod 3.36 0.297341

roe 6.78 0.147475

intercept 8.50 0.117641

Variable VIF 1/VIF

. estat vif, uncentered

Prob > F = 0.8999

F(6, 197) = 0.37

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

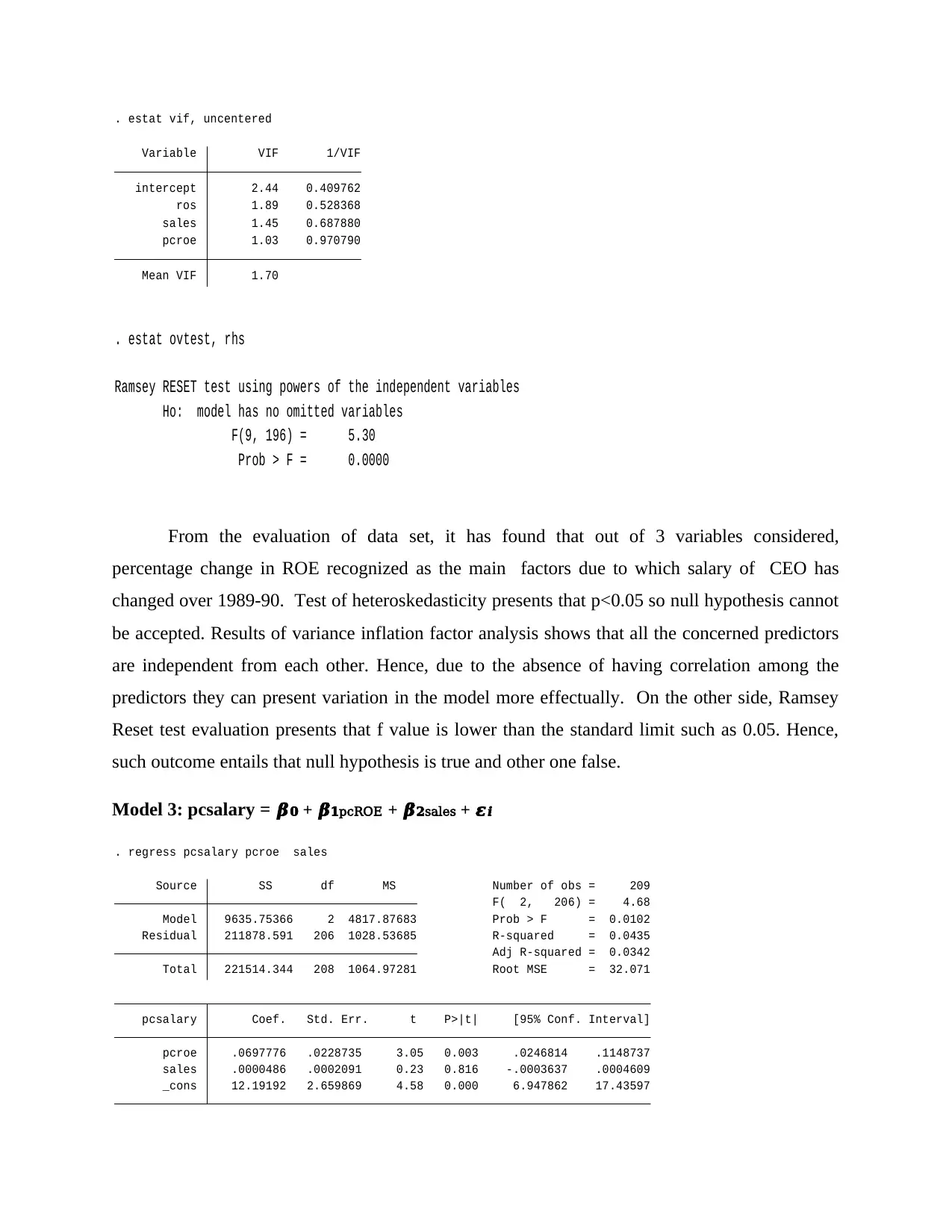

Regression analysis outcome shows that p values of all the concerned variables are higher

than 0.05 except consumer product industry. Moreover, in the context of consumer product

sector p value is below 0.00 which in turn entails that consumer product sector has impact on the

salary of CEO. In addition to this, results of Breusch test entails that values are not

homoscedastic. Further, mean value such as 4.37 presents that model is not suffering from the

aspects of multi-collinearity. Omitted variable test also shows that model is free from functional

errors.

3. Explaining percentage change in CEO salary over 1989-90 using 3 multiple regression model

Model 1: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐ros + 𝜺𝒊

Model 2: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐sales 𝜷3ros + 𝜺𝒊

Model 3: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐sales + 𝜺𝒊

Regression

Model 1: 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐ros + 𝜺𝒊

Mean VIF 4.37

ros 2.16 0.462511

finance 2.32 0.431014

indus 3.11 0.321453

consprod 3.36 0.297341

roe 6.78 0.147475

intercept 8.50 0.117641

Variable VIF 1/VIF

. estat vif, uncentered

Prob > F = 0.8999

F(6, 197) = 0.37

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

Regression analysis outcome shows that p values of all the concerned variables are higher

than 0.05 except consumer product industry. Moreover, in the context of consumer product

sector p value is below 0.00 which in turn entails that consumer product sector has impact on the

salary of CEO. In addition to this, results of Breusch test entails that values are not

homoscedastic. Further, mean value such as 4.37 presents that model is not suffering from the

aspects of multi-collinearity. Omitted variable test also shows that model is free from functional

errors.

3. Explaining percentage change in CEO salary over 1989-90 using 3 multiple regression model

Model 1: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐ros + 𝜺𝒊

Model 2: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐sales 𝜷3ros + 𝜺𝒊

Model 3: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐sales + 𝜺𝒊

Regression

Model 1: 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐ros + 𝜺𝒊

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

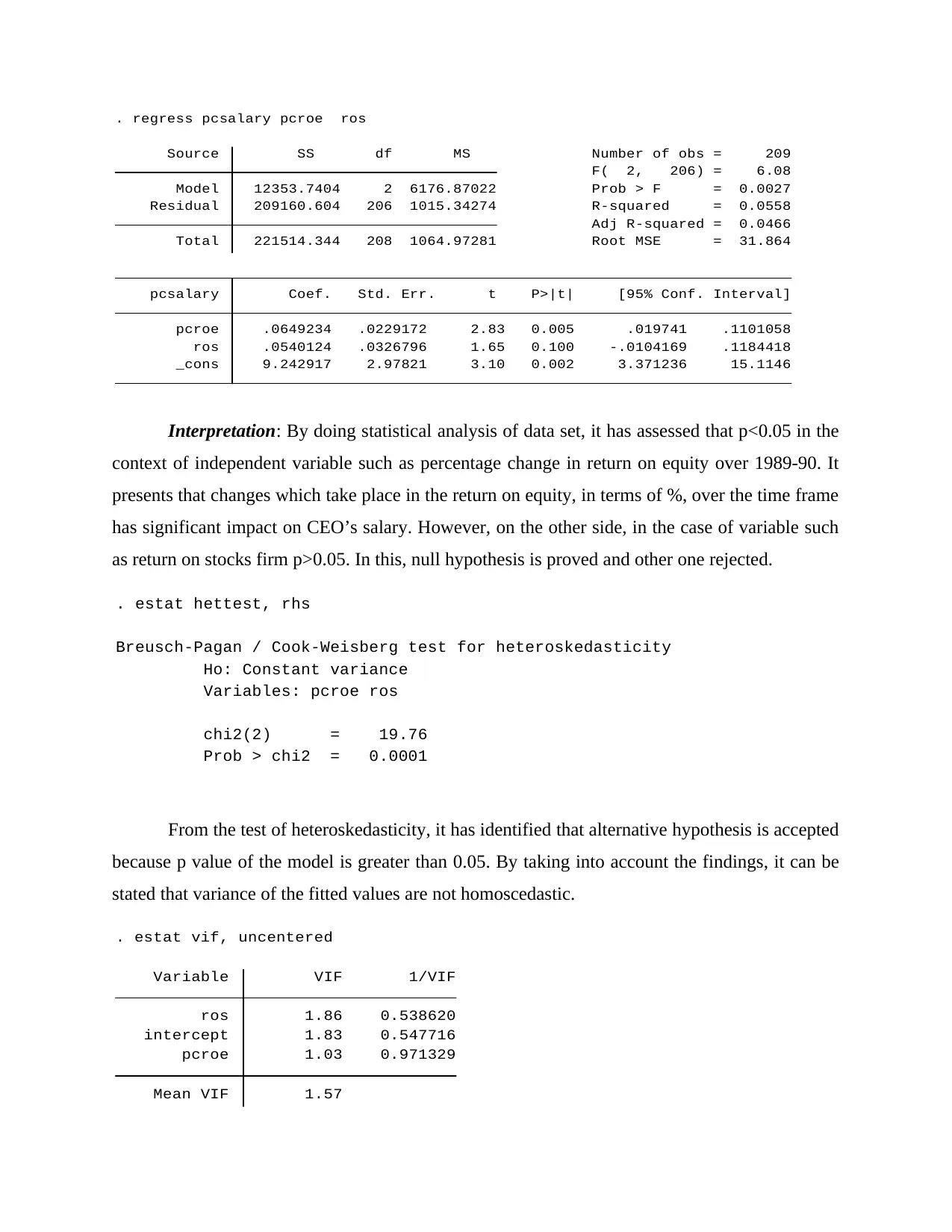

_cons 9.242917 2.97821 3.10 0.002 3.371236 15.1146

ros .0540124 .0326796 1.65 0.100 -.0104169 .1184418

pcroe .0649234 .0229172 2.83 0.005 .019741 .1101058

pcsalary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 221514.344 208 1064.97281 Root MSE = 31.864

Adj R-squared = 0.0466

Residual 209160.604 206 1015.34274 R-squared = 0.0558

Model 12353.7404 2 6176.87022 Prob > F = 0.0027

F( 2, 206) = 6.08

Source SS df MS Number of obs = 209

. regress pcsalary pcroe ros

Interpretation: By doing statistical analysis of data set, it has assessed that p<0.05 in the

context of independent variable such as percentage change in return on equity over 1989-90. It

presents that changes which take place in the return on equity, in terms of %, over the time frame

has significant impact on CEO’s salary. However, on the other side, in the case of variable such

as return on stocks firm p>0.05. In this, null hypothesis is proved and other one rejected.

Prob > chi2 = 0.0001

chi2(2) = 19.76

Variables: pcroe ros

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

From the test of heteroskedasticity, it has identified that alternative hypothesis is accepted

because p value of the model is greater than 0.05. By taking into account the findings, it can be

stated that variance of the fitted values are not homoscedastic.

Mean VIF 1.57

pcroe 1.03 0.971329

intercept 1.83 0.547716

ros 1.86 0.538620

Variable VIF 1/VIF

. estat vif, uncentered

ros .0540124 .0326796 1.65 0.100 -.0104169 .1184418

pcroe .0649234 .0229172 2.83 0.005 .019741 .1101058

pcsalary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 221514.344 208 1064.97281 Root MSE = 31.864

Adj R-squared = 0.0466

Residual 209160.604 206 1015.34274 R-squared = 0.0558

Model 12353.7404 2 6176.87022 Prob > F = 0.0027

F( 2, 206) = 6.08

Source SS df MS Number of obs = 209

. regress pcsalary pcroe ros

Interpretation: By doing statistical analysis of data set, it has assessed that p<0.05 in the

context of independent variable such as percentage change in return on equity over 1989-90. It

presents that changes which take place in the return on equity, in terms of %, over the time frame

has significant impact on CEO’s salary. However, on the other side, in the case of variable such

as return on stocks firm p>0.05. In this, null hypothesis is proved and other one rejected.

Prob > chi2 = 0.0001

chi2(2) = 19.76

Variables: pcroe ros

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

From the test of heteroskedasticity, it has identified that alternative hypothesis is accepted

because p value of the model is greater than 0.05. By taking into account the findings, it can be

stated that variance of the fitted values are not homoscedastic.

Mean VIF 1.57

pcroe 1.03 0.971329

intercept 1.83 0.547716

ros 1.86 0.538620

Variable VIF 1/VIF

. estat vif, uncentered

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

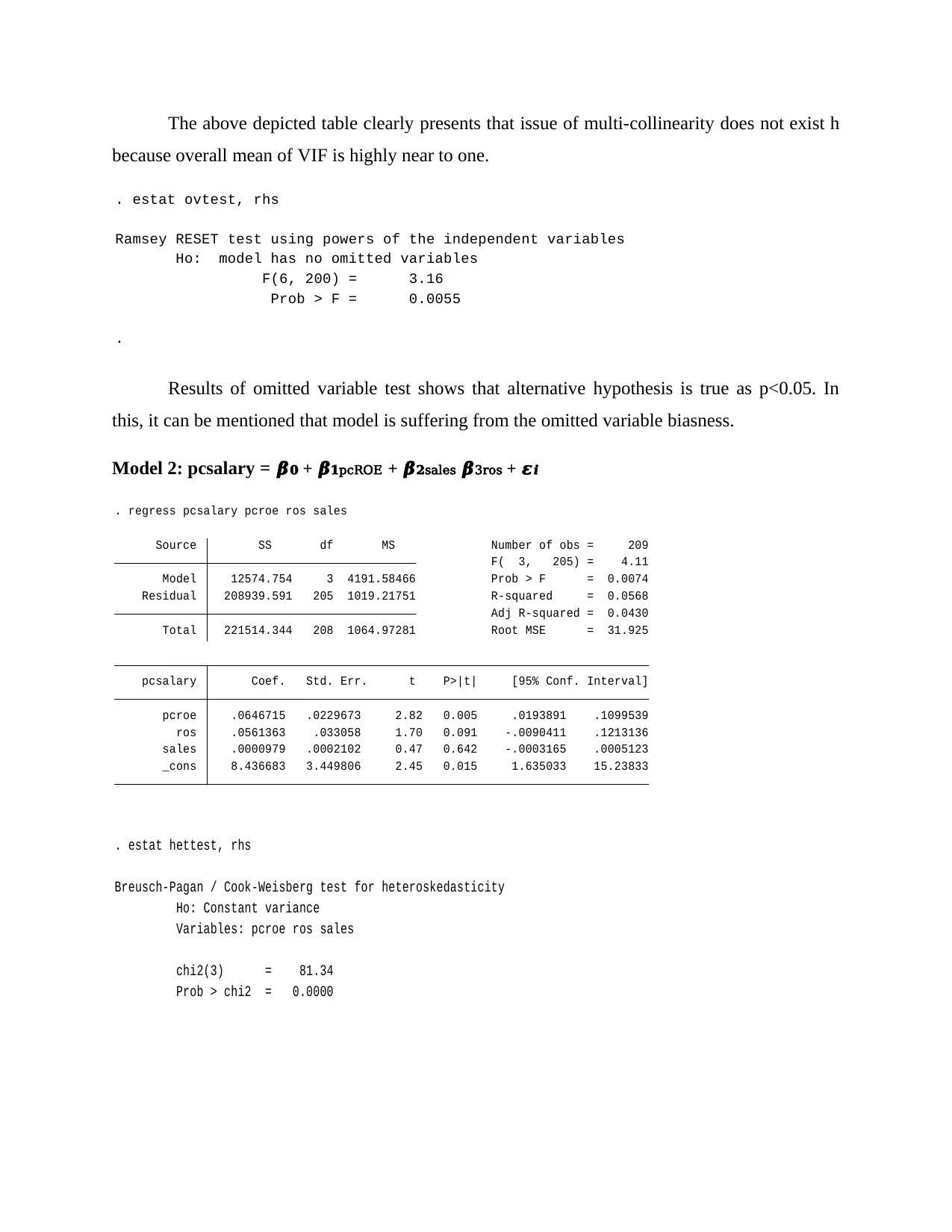

The above depicted table clearly presents that issue of multi-collinearity does not exist h

because overall mean of VIF is highly near to one.

.

Prob > F = 0.0055

F(6, 200) = 3.16

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

Results of omitted variable test shows that alternative hypothesis is true as p<0.05. In

this, it can be mentioned that model is suffering from the omitted variable biasness.

Model 2: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐sales 𝜷3ros + 𝜺𝒊

_cons 8.436683 3.449806 2.45 0.015 1.635033 15.23833

sales .0000979 .0002102 0.47 0.642 -.0003165 .0005123

ros .0561363 .033058 1.70 0.091 -.0090411 .1213136

pcroe .0646715 .0229673 2.82 0.005 .0193891 .1099539

pcsalary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 221514.344 208 1064.97281 Root MSE = 31.925

Adj R-squared = 0.0430

Residual 208939.591 205 1019.21751 R-squared = 0.0568

Model 12574.754 3 4191.58466 Prob > F = 0.0074

F( 3, 205) = 4.11

Source SS df MS Number of obs = 209

. regress pcsalary pcroe ros sales

Prob > chi2 = 0.0000

chi2(3) = 81.34

Variables: pcroe ros sales

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

because overall mean of VIF is highly near to one.

.

Prob > F = 0.0055

F(6, 200) = 3.16

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

Results of omitted variable test shows that alternative hypothesis is true as p<0.05. In

this, it can be mentioned that model is suffering from the omitted variable biasness.

Model 2: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐sales 𝜷3ros + 𝜺𝒊

_cons 8.436683 3.449806 2.45 0.015 1.635033 15.23833

sales .0000979 .0002102 0.47 0.642 -.0003165 .0005123

ros .0561363 .033058 1.70 0.091 -.0090411 .1213136

pcroe .0646715 .0229673 2.82 0.005 .0193891 .1099539

pcsalary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 221514.344 208 1064.97281 Root MSE = 31.925

Adj R-squared = 0.0430

Residual 208939.591 205 1019.21751 R-squared = 0.0568

Model 12574.754 3 4191.58466 Prob > F = 0.0074

F( 3, 205) = 4.11

Source SS df MS Number of obs = 209

. regress pcsalary pcroe ros sales

Prob > chi2 = 0.0000

chi2(3) = 81.34

Variables: pcroe ros sales

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. estat hettest, rhs

Mean VIF 1.70

pcroe 1.03 0.970790

sales 1.45 0.687880

ros 1.89 0.528368

intercept 2.44 0.409762

Variable VIF 1/VIF

. estat vif, uncentered

Prob > F = 0.0000

F(9, 196) = 5.30

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

From the evaluation of data set, it has found that out of 3 variables considered,

percentage change in ROE recognized as the main factors due to which salary of CEO has

changed over 1989-90. Test of heteroskedasticity presents that p<0.05 so null hypothesis cannot

be accepted. Results of variance inflation factor analysis shows that all the concerned predictors

are independent from each other. Hence, due to the absence of having correlation among the

predictors they can present variation in the model more effectually. On the other side, Ramsey

Reset test evaluation presents that f value is lower than the standard limit such as 0.05. Hence,

such outcome entails that null hypothesis is true and other one false.

Model 3: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐sales + 𝜺𝒊

_cons 12.19192 2.659869 4.58 0.000 6.947862 17.43597

sales .0000486 .0002091 0.23 0.816 -.0003637 .0004609

pcroe .0697776 .0228735 3.05 0.003 .0246814 .1148737

pcsalary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 221514.344 208 1064.97281 Root MSE = 32.071

Adj R-squared = 0.0342

Residual 211878.591 206 1028.53685 R-squared = 0.0435

Model 9635.75366 2 4817.87683 Prob > F = 0.0102

F( 2, 206) = 4.68

Source SS df MS Number of obs = 209

. regress pcsalary pcroe sales

pcroe 1.03 0.970790

sales 1.45 0.687880

ros 1.89 0.528368

intercept 2.44 0.409762

Variable VIF 1/VIF

. estat vif, uncentered

Prob > F = 0.0000

F(9, 196) = 5.30

Ho: model has no omitted variables

Ramsey RESET test using powers of the independent variables

. estat ovtest, rhs

From the evaluation of data set, it has found that out of 3 variables considered,

percentage change in ROE recognized as the main factors due to which salary of CEO has

changed over 1989-90. Test of heteroskedasticity presents that p<0.05 so null hypothesis cannot

be accepted. Results of variance inflation factor analysis shows that all the concerned predictors

are independent from each other. Hence, due to the absence of having correlation among the

predictors they can present variation in the model more effectually. On the other side, Ramsey

Reset test evaluation presents that f value is lower than the standard limit such as 0.05. Hence,

such outcome entails that null hypothesis is true and other one false.

Model 3: pcsalary = 𝜷𝟎 + 𝜷𝟏pcROE + 𝜷𝟐sales + 𝜺𝒊

_cons 12.19192 2.659869 4.58 0.000 6.947862 17.43597

sales .0000486 .0002091 0.23 0.816 -.0003637 .0004609

pcroe .0697776 .0228735 3.05 0.003 .0246814 .1148737

pcsalary Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 221514.344 208 1064.97281 Root MSE = 32.071

Adj R-squared = 0.0342

Residual 211878.591 206 1028.53685 R-squared = 0.0435

Model 9635.75366 2 4817.87683 Prob > F = 0.0102

F( 2, 206) = 4.68

Source SS df MS Number of obs = 209

. regress pcsalary pcroe sales

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.