Certificate IV Accounting: BAS/IAS Activity Statement Tasks

VerifiedAdded on 2020/04/21

|38

|6787

|103

Homework Assignment

AI Summary

This document presents a comprehensive solution to an assessment focusing on the FNSBKG404 unit, which is part of the FNS40615 Certificate IV in Accounting. The assignment addresses the skills and knowledge required to carry out business activity statements (BAS) and instalment activity statements (IAS) tasks. The solution covers key aspects such as identifying individual compliance requirements, researching and documenting legislative and organizational requirements, applying GST implications, reporting on payroll activities, and completing and reconciling activity statements. The document answers specific questions related to tax obligations, GST implications, payroll reporting, PAYG installments, and the tasks involved in completing and reconciling activity statements. It emphasizes the importance of adhering to current legislation, regulations, and industry codes of practice, including the Tax Agent Services Act (TASA) and the Australian Taxation Office (ATO) requirements.

ASSESSMENT

Qualification: FNS40615 Certificate IV in Accounting

Unit of Competency: FNSBKG404 Carry out business activity and instalment

activity statement tasks

Student Name:

Student ID:

Assessment Due Date:

Qualification: FNS40615 Certificate IV in Accounting

Unit of Competency: FNSBKG404 Carry out business activity and instalment

activity statement tasks

Student Name:

Student ID:

Assessment Due Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

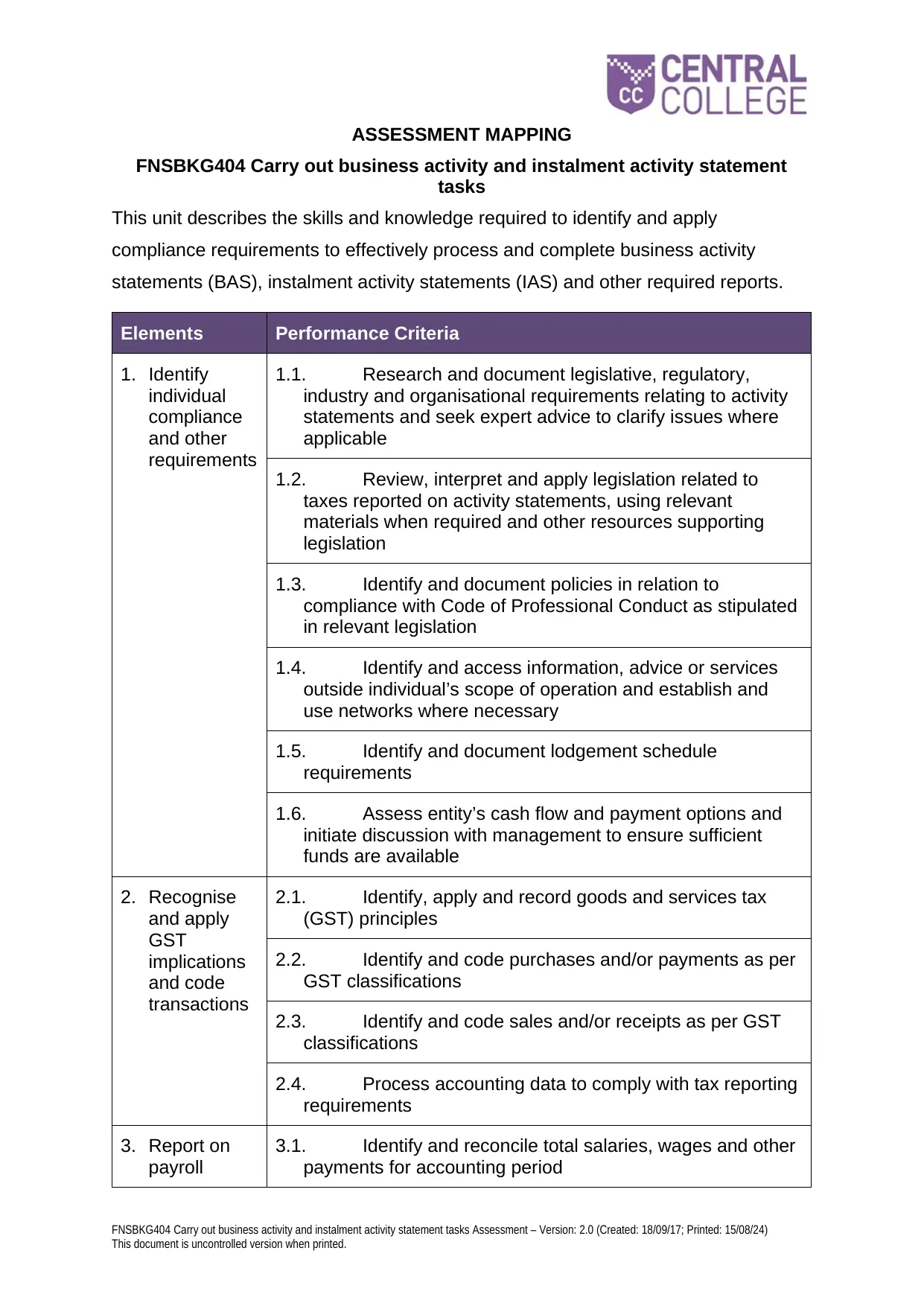

ASSESSMENT MAPPING

FNSBKG404 Carry out business activity and instalment activity statement

tasks

This unit describes the skills and knowledge required to identify and apply

compliance requirements to effectively process and complete business activity

statements (BAS), instalment activity statements (IAS) and other required reports.

Elements Performance Criteria

1. Identify

individual

compliance

and other

requirements

1.1. Research and document legislative, regulatory,

industry and organisational requirements relating to activity

statements and seek expert advice to clarify issues where

applicable

1.2. Review, interpret and apply legislation related to

taxes reported on activity statements, using relevant

materials when required and other resources supporting

legislation

1.3. Identify and document policies in relation to

compliance with Code of Professional Conduct as stipulated

in relevant legislation

1.4. Identify and access information, advice or services

outside individual’s scope of operation and establish and

use networks where necessary

1.5. Identify and document lodgement schedule

requirements

1.6. Assess entity’s cash flow and payment options and

initiate discussion with management to ensure sufficient

funds are available

2. Recognise

and apply

GST

implications

and code

transactions

2.1. Identify, apply and record goods and services tax

(GST) principles

2.2. Identify and code purchases and/or payments as per

GST classifications

2.3. Identify and code sales and/or receipts as per GST

classifications

2.4. Process accounting data to comply with tax reporting

requirements

3. Report on

payroll

3.1. Identify and reconcile total salaries, wages and other

payments for accounting period

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

FNSBKG404 Carry out business activity and instalment activity statement

tasks

This unit describes the skills and knowledge required to identify and apply

compliance requirements to effectively process and complete business activity

statements (BAS), instalment activity statements (IAS) and other required reports.

Elements Performance Criteria

1. Identify

individual

compliance

and other

requirements

1.1. Research and document legislative, regulatory,

industry and organisational requirements relating to activity

statements and seek expert advice to clarify issues where

applicable

1.2. Review, interpret and apply legislation related to

taxes reported on activity statements, using relevant

materials when required and other resources supporting

legislation

1.3. Identify and document policies in relation to

compliance with Code of Professional Conduct as stipulated

in relevant legislation

1.4. Identify and access information, advice or services

outside individual’s scope of operation and establish and

use networks where necessary

1.5. Identify and document lodgement schedule

requirements

1.6. Assess entity’s cash flow and payment options and

initiate discussion with management to ensure sufficient

funds are available

2. Recognise

and apply

GST

implications

and code

transactions

2.1. Identify, apply and record goods and services tax

(GST) principles

2.2. Identify and code purchases and/or payments as per

GST classifications

2.3. Identify and code sales and/or receipts as per GST

classifications

2.4. Process accounting data to comply with tax reporting

requirements

3. Report on

payroll

3.1. Identify and reconcile total salaries, wages and other

payments for accounting period

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

activities and

amounts

withheld

3.2. Identify and reconcile amounts withheld from salaries

and wages for accounting period in conjunction with payroll

department if applicable

3.3. Identify and reconcile amounts withheld from other

payments for accounting period in conjunction with other

departments if applicable

3.4. Verify or calculate pay as you go (PAYG) instalment

amount where applicable, or calculate for other payments

where applicable

4. Complete

and

reconcile

activity

statement

4.1. Generate, review and validate activity statement

reports, identify any errors and correct bookkeeping entries

where required

4.2. Make adjustments for previous quarters, months or

year-end where necessary

4.3. Complete BAS and/or IAS return in accordance with

current statutory, legislative, regulatory and organisational

schedule

4.4. Reconcile figures completed on BAS and/or IAS form

with journal entries, financial statements, GST and other

control accounts

5. Identify

individual

compliance

and other

requirements

5.1. Check activity statement and ensure sign off by

appropriate person as identified by statutory, legislative and

regulatory requirements

5.2. Lodge activity statement in accordance with

statutory, legislative and regulatory requirements

5.3. Process and record payments and refunds as

required

Performance Evidence

Evidence of the ability to:

research, critically evaluate and apply any changes to current or new legislative

or professional conduct requirements relevant to the preparation of activity

statements

identify financial transactions required to prepare activity statements and apply

goods and services tax (GST) principles and classifications

prepare both business activity statements (BAS) and instalment activity

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

amounts

withheld

3.2. Identify and reconcile amounts withheld from salaries

and wages for accounting period in conjunction with payroll

department if applicable

3.3. Identify and reconcile amounts withheld from other

payments for accounting period in conjunction with other

departments if applicable

3.4. Verify or calculate pay as you go (PAYG) instalment

amount where applicable, or calculate for other payments

where applicable

4. Complete

and

reconcile

activity

statement

4.1. Generate, review and validate activity statement

reports, identify any errors and correct bookkeeping entries

where required

4.2. Make adjustments for previous quarters, months or

year-end where necessary

4.3. Complete BAS and/or IAS return in accordance with

current statutory, legislative, regulatory and organisational

schedule

4.4. Reconcile figures completed on BAS and/or IAS form

with journal entries, financial statements, GST and other

control accounts

5. Identify

individual

compliance

and other

requirements

5.1. Check activity statement and ensure sign off by

appropriate person as identified by statutory, legislative and

regulatory requirements

5.2. Lodge activity statement in accordance with

statutory, legislative and regulatory requirements

5.3. Process and record payments and refunds as

required

Performance Evidence

Evidence of the ability to:

research, critically evaluate and apply any changes to current or new legislative

or professional conduct requirements relevant to the preparation of activity

statements

identify financial transactions required to prepare activity statements and apply

goods and services tax (GST) principles and classifications

prepare both business activity statements (BAS) and instalment activity

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

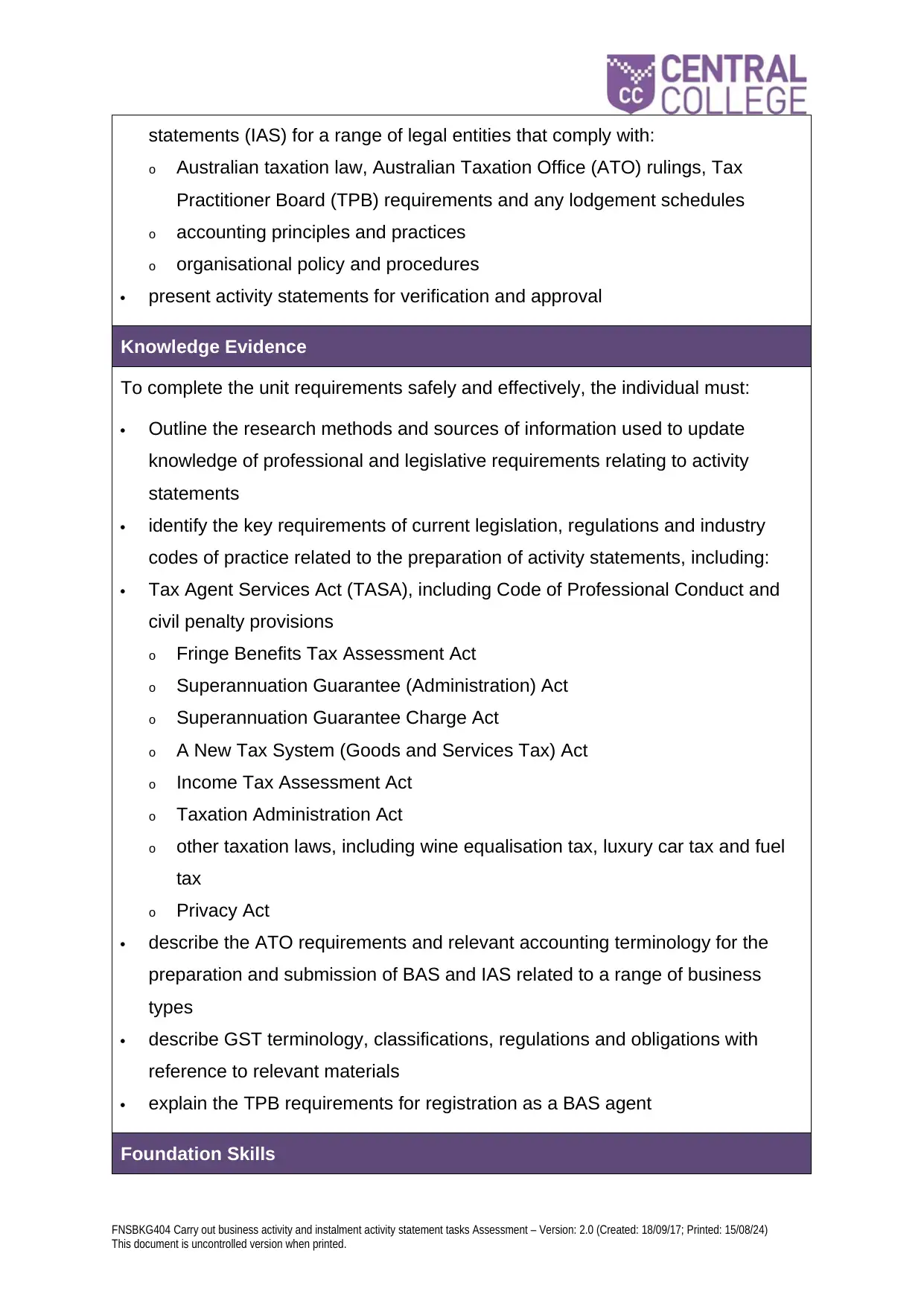

statements (IAS) for a range of legal entities that comply with:

o Australian taxation law, Australian Taxation Office (ATO) rulings, Tax

Practitioner Board (TPB) requirements and any lodgement schedules

o accounting principles and practices

o organisational policy and procedures

present activity statements for verification and approval

Knowledge Evidence

To complete the unit requirements safely and effectively, the individual must:

Outline the research methods and sources of information used to update

knowledge of professional and legislative requirements relating to activity

statements

identify the key requirements of current legislation, regulations and industry

codes of practice related to the preparation of activity statements, including:

Tax Agent Services Act (TASA), including Code of Professional Conduct and

civil penalty provisions

o Fringe Benefits Tax Assessment Act

o Superannuation Guarantee (Administration) Act

o Superannuation Guarantee Charge Act

o A New Tax System (Goods and Services Tax) Act

o Income Tax Assessment Act

o Taxation Administration Act

o other taxation laws, including wine equalisation tax, luxury car tax and fuel

tax

o Privacy Act

describe the ATO requirements and relevant accounting terminology for the

preparation and submission of BAS and IAS related to a range of business

types

describe GST terminology, classifications, regulations and obligations with

reference to relevant materials

explain the TPB requirements for registration as a BAS agent

Foundation Skills

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

o Australian taxation law, Australian Taxation Office (ATO) rulings, Tax

Practitioner Board (TPB) requirements and any lodgement schedules

o accounting principles and practices

o organisational policy and procedures

present activity statements for verification and approval

Knowledge Evidence

To complete the unit requirements safely and effectively, the individual must:

Outline the research methods and sources of information used to update

knowledge of professional and legislative requirements relating to activity

statements

identify the key requirements of current legislation, regulations and industry

codes of practice related to the preparation of activity statements, including:

Tax Agent Services Act (TASA), including Code of Professional Conduct and

civil penalty provisions

o Fringe Benefits Tax Assessment Act

o Superannuation Guarantee (Administration) Act

o Superannuation Guarantee Charge Act

o A New Tax System (Goods and Services Tax) Act

o Income Tax Assessment Act

o Taxation Administration Act

o other taxation laws, including wine equalisation tax, luxury car tax and fuel

tax

o Privacy Act

describe the ATO requirements and relevant accounting terminology for the

preparation and submission of BAS and IAS related to a range of business

types

describe GST terminology, classifications, regulations and obligations with

reference to relevant materials

explain the TPB requirements for registration as a BAS agent

Foundation Skills

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

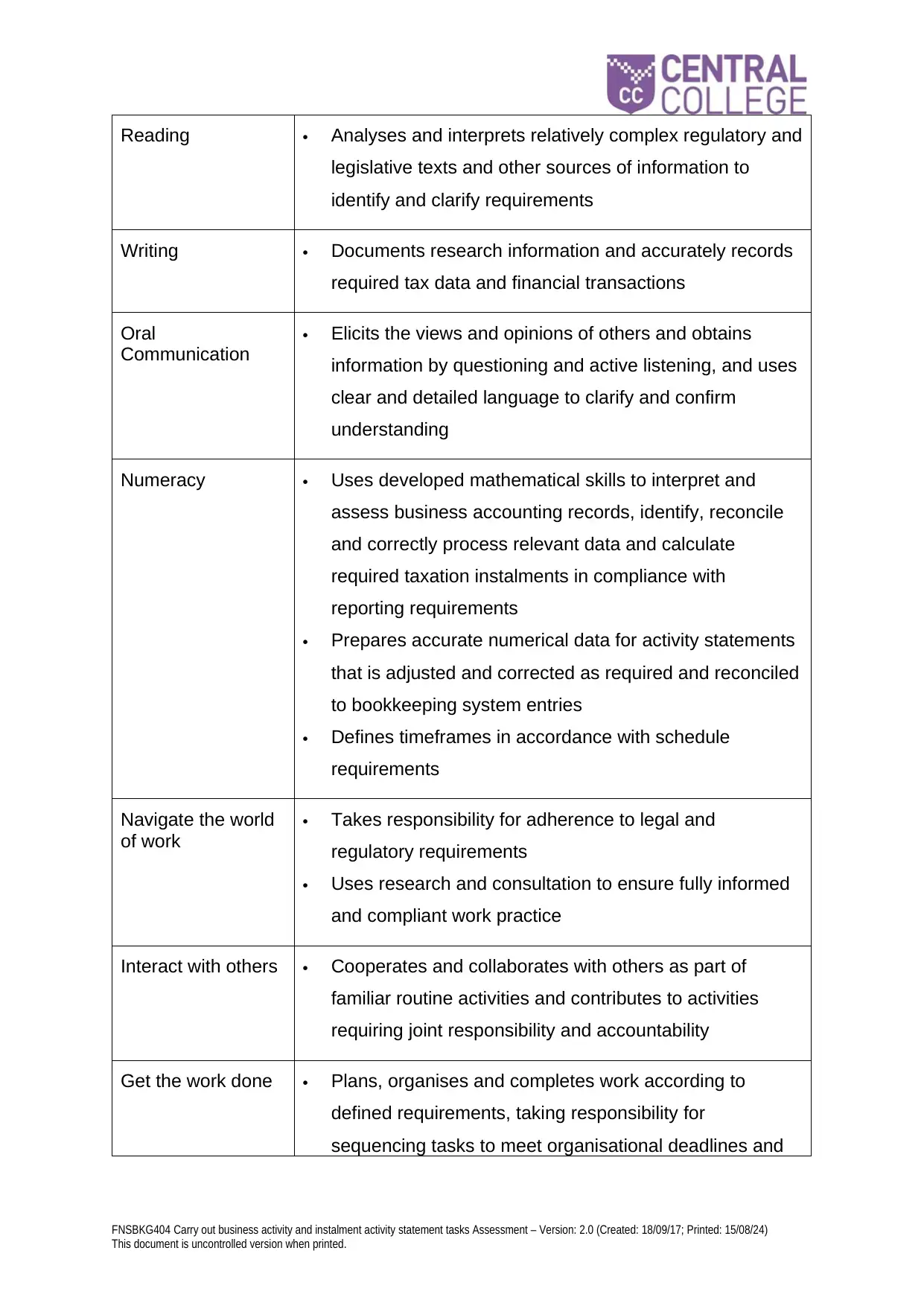

Reading Analyses and interprets relatively complex regulatory and

legislative texts and other sources of information to

identify and clarify requirements

Writing Documents research information and accurately records

required tax data and financial transactions

Oral

Communication

Elicits the views and opinions of others and obtains

information by questioning and active listening, and uses

clear and detailed language to clarify and confirm

understanding

Numeracy Uses developed mathematical skills to interpret and

assess business accounting records, identify, reconcile

and correctly process relevant data and calculate

required taxation instalments in compliance with

reporting requirements

Prepares accurate numerical data for activity statements

that is adjusted and corrected as required and reconciled

to bookkeeping system entries

Defines timeframes in accordance with schedule

requirements

Navigate the world

of work

Takes responsibility for adherence to legal and

regulatory requirements

Uses research and consultation to ensure fully informed

and compliant work practice

Interact with others Cooperates and collaborates with others as part of

familiar routine activities and contributes to activities

requiring joint responsibility and accountability

Get the work done Plans, organises and completes work according to

defined requirements, taking responsibility for

sequencing tasks to meet organisational deadlines and

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

legislative texts and other sources of information to

identify and clarify requirements

Writing Documents research information and accurately records

required tax data and financial transactions

Oral

Communication

Elicits the views and opinions of others and obtains

information by questioning and active listening, and uses

clear and detailed language to clarify and confirm

understanding

Numeracy Uses developed mathematical skills to interpret and

assess business accounting records, identify, reconcile

and correctly process relevant data and calculate

required taxation instalments in compliance with

reporting requirements

Prepares accurate numerical data for activity statements

that is adjusted and corrected as required and reconciled

to bookkeeping system entries

Defines timeframes in accordance with schedule

requirements

Navigate the world

of work

Takes responsibility for adherence to legal and

regulatory requirements

Uses research and consultation to ensure fully informed

and compliant work practice

Interact with others Cooperates and collaborates with others as part of

familiar routine activities and contributes to activities

requiring joint responsibility and accountability

Get the work done Plans, organises and completes work according to

defined requirements, taking responsibility for

sequencing tasks to meet organisational deadlines and

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

legislative requirements

Uses systematic, analytical processes in complex,

routine and non-routine situations, gathering information

and identifying and evaluating potential solutions

Uses digital tools to conduct research, design work

processes and to complete work tasks

ASSESSMENT INFORMATION:

To be deemed competent for this unit of competency, you are required to

satisfactorily complete two (2) assessments:

Assessment 1: Written questions

Assessment 2: Skills Assessment

Assessment Instructions

Your assessment will be required to be typed in Arial font size 12 only. You will

provide your completed assessment for all of questions in one document and MUST

be uploaded into MOODLE (No other method of submission will be accepted).

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

Uses systematic, analytical processes in complex,

routine and non-routine situations, gathering information

and identifying and evaluating potential solutions

Uses digital tools to conduct research, design work

processes and to complete work tasks

ASSESSMENT INFORMATION:

To be deemed competent for this unit of competency, you are required to

satisfactorily complete two (2) assessments:

Assessment 1: Written questions

Assessment 2: Skills Assessment

Assessment Instructions

Your assessment will be required to be typed in Arial font size 12 only. You will

provide your completed assessment for all of questions in one document and MUST

be uploaded into MOODLE (No other method of submission will be accepted).

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

You are required to professionally format your document including spell-check and

indicating each Task answer [e.g. Task 1 (a.) then the answer, Task 1 (b.) then the

answer etc.] according to this Assignment requirement. You may lose marks if you

have not spell-checked your document (as this is a professional formatting

requirement, a business skill).

This assessment can be completed in one of several ways. Assessment candidates

may identify unit requirement within their own work environment or organisation, or

with reference to a scenario provided by the trainer/assessor.

Be sure to properly reference your sources of information using the Harvard

referencing system. For more information go to:-

Student Handbook - latest version

Ask your Trainer/Assessor to provide you with this information

In order to determine if you are addressing this assignment adequately in terms of

competency/comprehension (prior to due date) a draft copy of your assessment

should be discussed during class time in consultation with your

Trainer/Assessor. For this feedback/ support from your Trainer/Assessor, you will

need to bring to class your “draft copy” with any evidence of the research you have

conducted to produce the assessment.

If, as a student you feel you have special needs that require your Trainer/Assessor to

apply a reasonable adjustment – please discuss this with your Trainer/Assessor at

the beginning of the subject studies.

Your Assignment must:

a. Be of a professional standard (spelling, grammar, punctuation)

b. Size 12, Arial Font

c. 1.5 Spacing

d. All pages must have a Header/Footer with the following details:

o Name

o Student ID

o The course & unit of competency

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

indicating each Task answer [e.g. Task 1 (a.) then the answer, Task 1 (b.) then the

answer etc.] according to this Assignment requirement. You may lose marks if you

have not spell-checked your document (as this is a professional formatting

requirement, a business skill).

This assessment can be completed in one of several ways. Assessment candidates

may identify unit requirement within their own work environment or organisation, or

with reference to a scenario provided by the trainer/assessor.

Be sure to properly reference your sources of information using the Harvard

referencing system. For more information go to:-

Student Handbook - latest version

Ask your Trainer/Assessor to provide you with this information

In order to determine if you are addressing this assignment adequately in terms of

competency/comprehension (prior to due date) a draft copy of your assessment

should be discussed during class time in consultation with your

Trainer/Assessor. For this feedback/ support from your Trainer/Assessor, you will

need to bring to class your “draft copy” with any evidence of the research you have

conducted to produce the assessment.

If, as a student you feel you have special needs that require your Trainer/Assessor to

apply a reasonable adjustment – please discuss this with your Trainer/Assessor at

the beginning of the subject studies.

Your Assignment must:

a. Be of a professional standard (spelling, grammar, punctuation)

b. Size 12, Arial Font

c. 1.5 Spacing

d. All pages must have a Header/Footer with the following details:

o Name

o Student ID

o The course & unit of competency

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

o Date

o Page numbering

e. Title page

f. Index page

g. Body of work

h. Referencing

How to upload your answered assessment into MOODLE

To upload your assignment into Moodle, follow these steps.

1. Log-in to Moodle and access the subject that you will be submitting the

assignment in.

2. Locate the assessment you will be uploading into by scrolling down to the week

that the assessment is due in and then click on the assessment submission link.

3. Click on the name of the assignment.

4. Click the Browse button.

5. Select the file and click Open.

6. Click the Upload this file button.

7. If you have more than one file, repeat the process (steps 4-6) to attach

additional files up to the assignment's limit.

8. Once happy with your submission click the Send for marking button. The

files are locked and the student can no longer delete, or upload more, files.

Note: The date and time of the submission is recorded when the files are sent for

marking, not when they are first uploaded.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

o Page numbering

e. Title page

f. Index page

g. Body of work

h. Referencing

How to upload your answered assessment into MOODLE

To upload your assignment into Moodle, follow these steps.

1. Log-in to Moodle and access the subject that you will be submitting the

assignment in.

2. Locate the assessment you will be uploading into by scrolling down to the week

that the assessment is due in and then click on the assessment submission link.

3. Click on the name of the assignment.

4. Click the Browse button.

5. Select the file and click Open.

6. Click the Upload this file button.

7. If you have more than one file, repeat the process (steps 4-6) to attach

additional files up to the assignment's limit.

8. Once happy with your submission click the Send for marking button. The

files are locked and the student can no longer delete, or upload more, files.

Note: The date and time of the submission is recorded when the files are sent for

marking, not when they are first uploaded.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

ASSESSMENT 1: WRITTEN QUESTIONS

QUESTIONS

1. What are the three main categories of tax obligations?

Answer: The three main tax obligations for the taxpayer are as follows;

a. Registration

b. Lodgement

c. Reporting and Payment

Irrespective of the type of entity an individual, big organization or SMSF all the

tax payers are required to make an application for the TFN and a large number of

them are required to lodge a yearly tax return.

2. What do you need to do in order to identify individual compliance and other

requirements?

Answer: Obeying to the lawful requirements and obligations or systematically and

preventively protecting the individual taxpayer in the field of taxes is known as the

tax compliance. Government with the help of the tax administrations, usually seek to

reduce their own system of taxation operating cost whereas at the same time

keeping the compliance cost for taxpayers as minimum as possible. In order to attain

this, an equilibrium should be created between the cost borne by the individual in

complying with the regulations of tax and the cost that is shouldered by the revenue

authority in running the system. Enforcing compliance through constant checks,

substantial audits and prosecution is considered as an expensive method of making

sure that adequate compliance is attained where the taxpayer is stimulated to co-

operate and actively comply with the regulations of taxation.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

QUESTIONS

1. What are the three main categories of tax obligations?

Answer: The three main tax obligations for the taxpayer are as follows;

a. Registration

b. Lodgement

c. Reporting and Payment

Irrespective of the type of entity an individual, big organization or SMSF all the

tax payers are required to make an application for the TFN and a large number of

them are required to lodge a yearly tax return.

2. What do you need to do in order to identify individual compliance and other

requirements?

Answer: Obeying to the lawful requirements and obligations or systematically and

preventively protecting the individual taxpayer in the field of taxes is known as the

tax compliance. Government with the help of the tax administrations, usually seek to

reduce their own system of taxation operating cost whereas at the same time

keeping the compliance cost for taxpayers as minimum as possible. In order to attain

this, an equilibrium should be created between the cost borne by the individual in

complying with the regulations of tax and the cost that is shouldered by the revenue

authority in running the system. Enforcing compliance through constant checks,

substantial audits and prosecution is considered as an expensive method of making

sure that adequate compliance is attained where the taxpayer is stimulated to co-

operate and actively comply with the regulations of taxation.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. How would you recognise and apply GST implications and code transactions?

Answer: Recognizing and applying GST implications and code transactions are as

follows;

a. The fundamentals of GST are recognized, applied and recorded.

b. Purchases and payments are recorded, coded in accordance with the GST

classifications and they are split in capital and non-capital as considered

appropriate.

c. Sales and other receipts are recognized and coded according to the GST

classifications

d. Accounting data is processed to adhere with the reporting requirements of

taxation.

4. What do you need to do to report on payroll activities?

Answer: Reporting on payroll activities are as follows;

a. An employer under the payroll activities is required to report to the ATO

regarding all the payments on or prior to the payday, through the payroll

event.

b. When the payment is made through electronic means, the day of payment is

either considered as the date that is stipulated in the electronic transactions or

else no date is specified, the data on which the payment is proposed to be

made in the employees bank account.

c. The report should take into the account the employee, with the amount that is

subjected to withholding in the regular cycle of pay.

d. Total amount of salaries and other types of payments during the period of

accounting are recognized and reconciled.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

Answer: Recognizing and applying GST implications and code transactions are as

follows;

a. The fundamentals of GST are recognized, applied and recorded.

b. Purchases and payments are recorded, coded in accordance with the GST

classifications and they are split in capital and non-capital as considered

appropriate.

c. Sales and other receipts are recognized and coded according to the GST

classifications

d. Accounting data is processed to adhere with the reporting requirements of

taxation.

4. What do you need to do to report on payroll activities?

Answer: Reporting on payroll activities are as follows;

a. An employer under the payroll activities is required to report to the ATO

regarding all the payments on or prior to the payday, through the payroll

event.

b. When the payment is made through electronic means, the day of payment is

either considered as the date that is stipulated in the electronic transactions or

else no date is specified, the data on which the payment is proposed to be

made in the employees bank account.

c. The report should take into the account the employee, with the amount that is

subjected to withholding in the regular cycle of pay.

d. Total amount of salaries and other types of payments during the period of

accounting are recognized and reconciled.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

e. The sum that is to be withhold from the salaries, wages and other payments

during the period of accounting are recognized and reconciled in the

conjunctions with the department of payroll if it is applicable.

5. What do you need to do in order to report on other amounts withheld, PAYG

instalments and taxes?

Answer: The requirements of reporting on the other amount withheld, PAYG

instalments and taxes are as follows;

a. An employer having a branch for PAYG for withholding purpose, the employer

is required to report separately the payroll events for each of the PAYG

withholding branch that is established with the ATO.

b. Amounts that are withheld from other payments during the period of

accounting are recognized and identified and reconciled in accordance with

other subdivisions provided they are applicable.

c. The instalment amount of PAYG should be verified or wherever applicable

should be computed.

d. Instalments amounts must be verified wherever applicable and must be

computed for other taxes.

6. What tasks must be performed when completing and reconciling the activity

statement?

Answer: Tasks that needs to be executed at the time of completing and reconciling

the activity statement are as follows;

a. Activity statement report should be generated whenever required and should

be checked and validated.

b. Errors should be identified and correct bookkeeping entries must be

generated.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

during the period of accounting are recognized and reconciled in the

conjunctions with the department of payroll if it is applicable.

5. What do you need to do in order to report on other amounts withheld, PAYG

instalments and taxes?

Answer: The requirements of reporting on the other amount withheld, PAYG

instalments and taxes are as follows;

a. An employer having a branch for PAYG for withholding purpose, the employer

is required to report separately the payroll events for each of the PAYG

withholding branch that is established with the ATO.

b. Amounts that are withheld from other payments during the period of

accounting are recognized and identified and reconciled in accordance with

other subdivisions provided they are applicable.

c. The instalment amount of PAYG should be verified or wherever applicable

should be computed.

d. Instalments amounts must be verified wherever applicable and must be

computed for other taxes.

6. What tasks must be performed when completing and reconciling the activity

statement?

Answer: Tasks that needs to be executed at the time of completing and reconciling

the activity statement are as follows;

a. Activity statement report should be generated whenever required and should

be checked and validated.

b. Errors should be identified and correct bookkeeping entries must be

generated.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

c. Adjustment for previous quarter should be made, or months or end of the year

whenever it is necessary.

d. BAS and IAS return must be completed in compliance with the up to date

statutory, regulatory and legislative organisational schedule.

e. Figures must be completed on the BAS and IAS form and must be reconciled

with the journal entries profit and loss statement, GST and other forms of

control accounts.

7. What tasks are required when lodging an activity statement?

Answer: Task required at the time of lodging activity statements are as follows;

a. Activity statement must be checked and signed off by an appropriate

individual as identified by the statutory legislation and regulations

requirements

b. Activity statements must be dispatched in compliance with the statutory

requirements, legislative and regulatory requirements.

c. Payment or any form of refund that is processed must be recorded.

8. What steps are involved in completing a BAS reconciliation?

Answer: Steps involved in completed BAS reconciliation are as follows;

Step 1: Preparing the information: Under this step the taxpayer is required to

reconcile their books of accounts to make sure that all the information is correct and

up to date.

Step 2: Entering Missing Transactions: An individual is required to record any

missing transaction for which they have receipts and invoices. For each of the

missing transactions the taxpayer will be needing a date, total sum of the

transaction, amount of GST and description.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

whenever it is necessary.

d. BAS and IAS return must be completed in compliance with the up to date

statutory, regulatory and legislative organisational schedule.

e. Figures must be completed on the BAS and IAS form and must be reconciled

with the journal entries profit and loss statement, GST and other forms of

control accounts.

7. What tasks are required when lodging an activity statement?

Answer: Task required at the time of lodging activity statements are as follows;

a. Activity statement must be checked and signed off by an appropriate

individual as identified by the statutory legislation and regulations

requirements

b. Activity statements must be dispatched in compliance with the statutory

requirements, legislative and regulatory requirements.

c. Payment or any form of refund that is processed must be recorded.

8. What steps are involved in completing a BAS reconciliation?

Answer: Steps involved in completed BAS reconciliation are as follows;

Step 1: Preparing the information: Under this step the taxpayer is required to

reconcile their books of accounts to make sure that all the information is correct and

up to date.

Step 2: Entering Missing Transactions: An individual is required to record any

missing transaction for which they have receipts and invoices. For each of the

missing transactions the taxpayer will be needing a date, total sum of the

transaction, amount of GST and description.

FNSBKG404 Carry out business activity and instalment activity statement tasks Assessment – Version: 2.0 (Created: 18/09/17; Printed: 15/08/24)

This document is uncontrolled version when printed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.