AAMC Training Group: FNS40815 Finance & Mortgage Broking Assessment

VerifiedAdded on 2023/05/31

|16

|5746

|377

Homework Assignment

AI Summary

This document presents a comprehensive solution to the FNS40815 Certificate IV in Finance & Mortgage Broking assessment, specifically for the Acc/FP Stream. It encompasses various tasks including a cover sheet, a third-party observer checklist, and short answer questions related to responsible lending scenarios. The assessment covers five units of competency: Apply principles of professional practice, Comply with legislation and industry codes, Manage personal work priorities, Prospect for new clients, and Design and produce business documents. The document includes a third-party declarer checklist and reference, along with detailed instructions for completion. Task 2 features short answer questions based on a responsible lending scenario, requiring analysis of initial inquiries, verification of information, and compliance with relevant financial regulations. The provided solution aims to assist students in understanding and completing their assessment successfully.

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all

tasks and this cover sheet via the AAMC Training Group portal. Your assessment

tasks must be uploaded in an electronic format i.e. Word, Excel, PDF or Scan. Please see

the step-by-step instructions in your Member Area on how to upload assessments.

Student details

Course name FNS40815 Certificate IV in Finance and Mortgage Broking (Acc&FP Stream)

Assessment name FNS40815 Acc/FP Stream Assessment

Surname Given name

Address Postcode

Email

Phone Phone (other)

Current occupation

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment submission

to AAMC Training is your own work and NOT the result of plagiarism or excessive collaboration,

and that all material used from any third party has been identified and referenced appropriately.

AAMC Training may conduct independent evaluation checks and contact your supervisor to

discuss your assessment.

Checklist of attachments:

☐ Task 1 -Third party observer checklist and reference

☐ Task 2 - Short Answer questions

Please indicate style of course undertaken:

☐ Face to face – Trainer’s name: ☐ Correspondence ☐ Online

Once your assessment has been successfully uploaded it will be pending review with your

nominated course assessor. Your assessor will mark your assessment and you will receive an

email advising you if you have been assessed as satisfactory. If you are marked as not yet

satisfactory you will be contacted and asked to provide additional information or re-visit the

assessment and re-upload your amended case study or written tasks.

Please contact our head office if you need assistance with your assessment:

Office: +61 8 9344 4088 Fax: +61 8 9344 4188 Email: info@aamctraining.edu.au

Assessment V2.2 © AAMC Training Group A1

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all

tasks and this cover sheet via the AAMC Training Group portal. Your assessment

tasks must be uploaded in an electronic format i.e. Word, Excel, PDF or Scan. Please see

the step-by-step instructions in your Member Area on how to upload assessments.

Student details

Course name FNS40815 Certificate IV in Finance and Mortgage Broking (Acc&FP Stream)

Assessment name FNS40815 Acc/FP Stream Assessment

Surname Given name

Address Postcode

Phone Phone (other)

Current occupation

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment submission

to AAMC Training is your own work and NOT the result of plagiarism or excessive collaboration,

and that all material used from any third party has been identified and referenced appropriately.

AAMC Training may conduct independent evaluation checks and contact your supervisor to

discuss your assessment.

Checklist of attachments:

☐ Task 1 -Third party observer checklist and reference

☐ Task 2 - Short Answer questions

Please indicate style of course undertaken:

☐ Face to face – Trainer’s name: ☐ Correspondence ☐ Online

Once your assessment has been successfully uploaded it will be pending review with your

nominated course assessor. Your assessor will mark your assessment and you will receive an

email advising you if you have been assessed as satisfactory. If you are marked as not yet

satisfactory you will be contacted and asked to provide additional information or re-visit the

assessment and re-upload your amended case study or written tasks.

Please contact our head office if you need assistance with your assessment:

Office: +61 8 9344 4088 Fax: +61 8 9344 4188 Email: info@aamctraining.edu.au

Assessment V2.2 © AAMC Training Group A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

FNS40815 Acc/FP Stream Assessment

This assessment encompasses the following five units of competency:

FNSINC401 Apply principles of professional practice to work in the financial services

industry

FNSFMK505 – Comply with legislation and industry codes of practice

BSBWOR501 – Manage personal work priorities and professional development

FNSSAM403 - Prospect for new clients

BSBITU306 – Design and produce business documents

The following are requirements to complete and submit this assessment:

Task 1 -Third Party Observer checklist and reference

Task 2 - Short answer questions

A2 © AAMC Training Group Assessment V2.2

FNS40815 Acc/FP Stream Assessment

This assessment encompasses the following five units of competency:

FNSINC401 Apply principles of professional practice to work in the financial services

industry

FNSFMK505 – Comply with legislation and industry codes of practice

BSBWOR501 – Manage personal work priorities and professional development

FNSSAM403 - Prospect for new clients

BSBITU306 – Design and produce business documents

The following are requirements to complete and submit this assessment:

Task 1 -Third Party Observer checklist and reference

Task 2 - Short answer questions

A2 © AAMC Training Group Assessment V2.2

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

Task 1: Third Party Declarer Checklist

Instructions for Third Party Declarer

You have been approached to provide evidence on behalf of an applicant (candidate) wishing to

obtain Recognition of Prior Learning (RPL) for BSBITU306 – Design and produce business

documents and FNSSAM403 – Prospect for new clients.

BSBITU306 – Design and produce business documents

This unit describes the performance outcomes, skills and knowledge required to design and

produce various business documents and publications. It includes selecting and using a range of

functions on a variety of computer applications.

FNSSAM403 – Prospect for new clients

This unit describes the skills and knowledge required to identify and contact potential client

prospects using networks, leads and research skills as well as cold calling. Initial contact may

happen over the phone or email, in person, at conferences and presentations, or through a variety

of networking opportunities.

The evidence you are to provide is based on your assessment of the applicant’s ability to work to

a satisfactory level of performance in these areas.

Before you agree to act as a Third Party assessor please beware that you need to:

Have a sound understanding of business processes.

Be employed in a business capacity for at least three years.

For the purpose of this exercise, your main role is to complete the following competency

checklist. Basically the candidate is seeking verification from you for this unit of competence.

It is important that you answer fairly and honestly. If you are not confident that the candidate

possesses skills and knowledge in particular areas listed please do not tick these items.

In addition to completing the competency checklists, you will need to:

Sign the statement to confirm your answers are true and correct.

Provide a written reference for the applicant. Please note that a sample referee template

has been provided which you can use to help with the written reference.

Applicants should be able to display knowledge and skills of the following points. The third party

declarer must indicate competency by checking the boxes in each column if the applicant is

competent.

Assessment V2.2 © AAMC Training Group A3

Task 1: Third Party Declarer Checklist

Instructions for Third Party Declarer

You have been approached to provide evidence on behalf of an applicant (candidate) wishing to

obtain Recognition of Prior Learning (RPL) for BSBITU306 – Design and produce business

documents and FNSSAM403 – Prospect for new clients.

BSBITU306 – Design and produce business documents

This unit describes the performance outcomes, skills and knowledge required to design and

produce various business documents and publications. It includes selecting and using a range of

functions on a variety of computer applications.

FNSSAM403 – Prospect for new clients

This unit describes the skills and knowledge required to identify and contact potential client

prospects using networks, leads and research skills as well as cold calling. Initial contact may

happen over the phone or email, in person, at conferences and presentations, or through a variety

of networking opportunities.

The evidence you are to provide is based on your assessment of the applicant’s ability to work to

a satisfactory level of performance in these areas.

Before you agree to act as a Third Party assessor please beware that you need to:

Have a sound understanding of business processes.

Be employed in a business capacity for at least three years.

For the purpose of this exercise, your main role is to complete the following competency

checklist. Basically the candidate is seeking verification from you for this unit of competence.

It is important that you answer fairly and honestly. If you are not confident that the candidate

possesses skills and knowledge in particular areas listed please do not tick these items.

In addition to completing the competency checklists, you will need to:

Sign the statement to confirm your answers are true and correct.

Provide a written reference for the applicant. Please note that a sample referee template

has been provided which you can use to help with the written reference.

Applicants should be able to display knowledge and skills of the following points. The third party

declarer must indicate competency by checking the boxes in each column if the applicant is

competent.

Assessment V2.2 © AAMC Training Group A3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

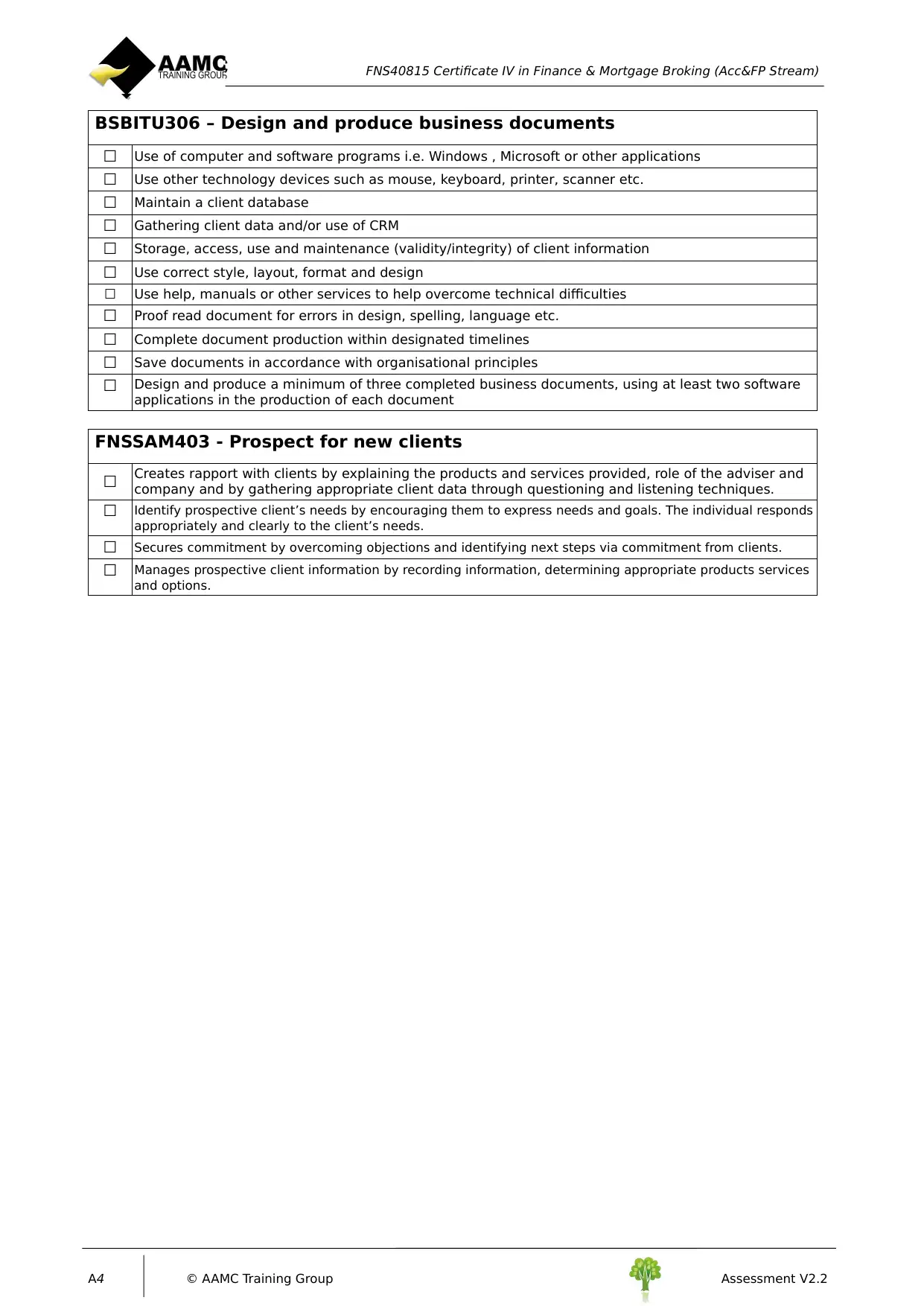

BSBITU306 – Design and produce business documents

☐ Use of computer and software programs i.e. Windows , Microsoft or other applications

☐ Use other technology devices such as mouse, keyboard, printer, scanner etc.

☐ Maintain a client database

☐ Gathering client data and/or use of CRM

☐ Storage, access, use and maintenance (validity/integrity) of client information

☐ Use correct style, layout, format and design

☐ Use help, manuals or other services to help overcome technical difficulties

☐ Proof read document for errors in design, spelling, language etc.

☐ Complete document production within designated timelines

☐ Save documents in accordance with organisational principles

☐ Design and produce a minimum of three completed business documents, using at least two software

applications in the production of each document

FNSSAM403 - Prospect for new clients

☐ Creates rapport with clients by explaining the products and services provided, role of the adviser and

company and by gathering appropriate client data through questioning and listening techniques.

☐ Identify prospective client’s needs by encouraging them to express needs and goals. The individual responds

appropriately and clearly to the client’s needs.

☐ Secures commitment by overcoming objections and identifying next steps via commitment from clients.

☐ Manages prospective client information by recording information, determining appropriate products services

and options.

A4 © AAMC Training Group Assessment V2.2

BSBITU306 – Design and produce business documents

☐ Use of computer and software programs i.e. Windows , Microsoft or other applications

☐ Use other technology devices such as mouse, keyboard, printer, scanner etc.

☐ Maintain a client database

☐ Gathering client data and/or use of CRM

☐ Storage, access, use and maintenance (validity/integrity) of client information

☐ Use correct style, layout, format and design

☐ Use help, manuals or other services to help overcome technical difficulties

☐ Proof read document for errors in design, spelling, language etc.

☐ Complete document production within designated timelines

☐ Save documents in accordance with organisational principles

☐ Design and produce a minimum of three completed business documents, using at least two software

applications in the production of each document

FNSSAM403 - Prospect for new clients

☐ Creates rapport with clients by explaining the products and services provided, role of the adviser and

company and by gathering appropriate client data through questioning and listening techniques.

☐ Identify prospective client’s needs by encouraging them to express needs and goals. The individual responds

appropriately and clearly to the client’s needs.

☐ Secures commitment by overcoming objections and identifying next steps via commitment from clients.

☐ Manages prospective client information by recording information, determining appropriate products services

and options.

A4 © AAMC Training Group Assessment V2.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

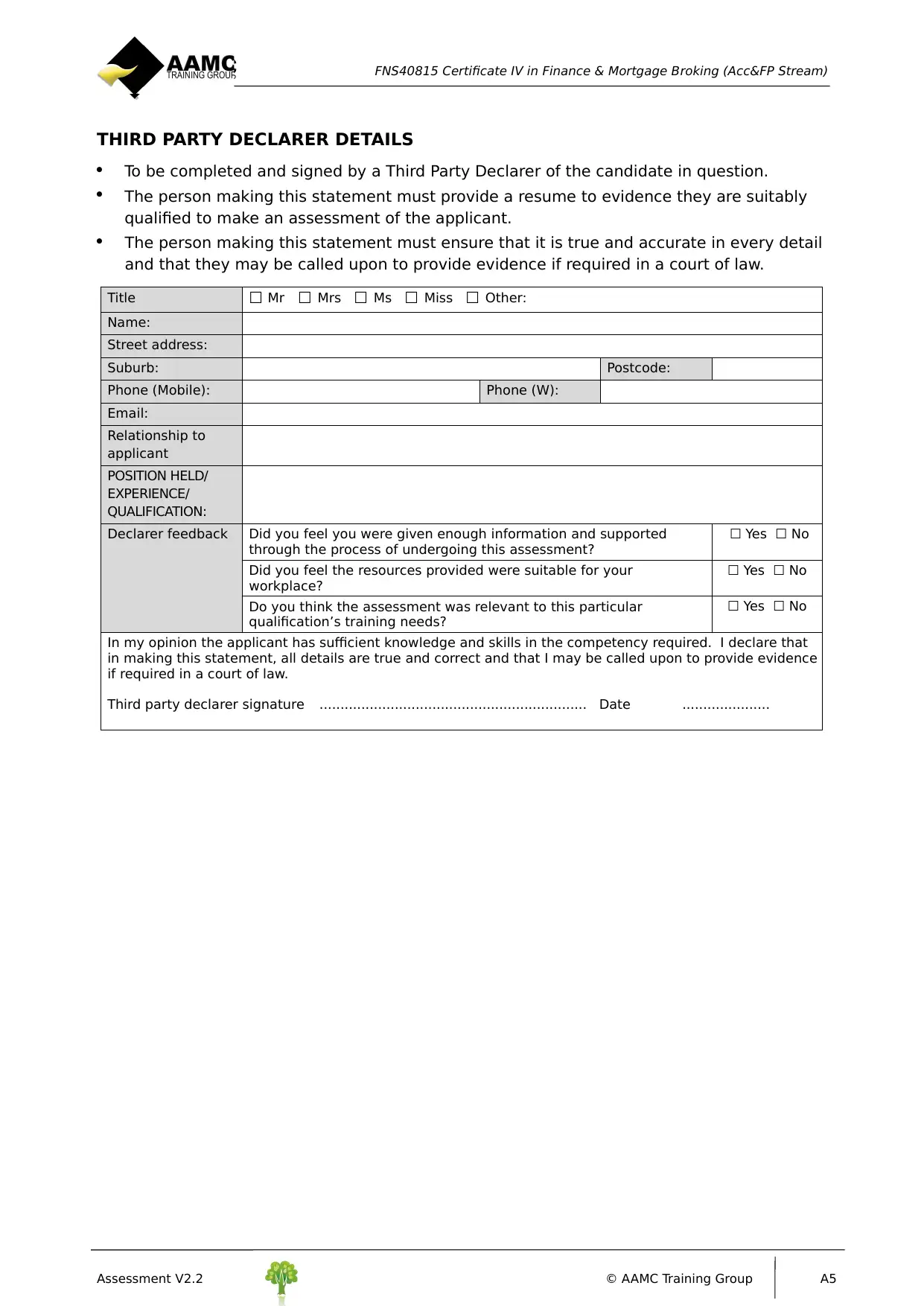

THIRD PARTY DECLARER DETAILS

To be completed and signed by a Third Party Declarer of the candidate in question.

The person making this statement must provide a resume to evidence they are suitably

qualified to make an assessment of the applicant.

The person making this statement must ensure that it is true and accurate in every detail

and that they may be called upon to provide evidence if required in a court of law.

Title ☐ Mr ☐ Mrs ☐ Ms ☐ Miss ☐ Other:

Name:

Street address:

Suburb: Postcode:

Phone (Mobile): Phone (W):

Email:

Relationship to

applicant

POSITION HELD/

EXPERIENCE/

QUALIFICATION:

Declarer feedback Did you feel you were given enough information and supported

through the process of undergoing this assessment?

☐ Yes ☐ No

Did you feel the resources provided were suitable for your

workplace?

☐ Yes ☐ No

Do you think the assessment was relevant to this particular

qualification’s training needs?

☐ Yes ☐ No

In my opinion the applicant has sufficient knowledge and skills in the competency required. I declare that

in making this statement, all details are true and correct and that I may be called upon to provide evidence

if required in a court of law.

Third party declarer signature ................................................................ Date .....................

Assessment V2.2 © AAMC Training Group A5

THIRD PARTY DECLARER DETAILS

To be completed and signed by a Third Party Declarer of the candidate in question.

The person making this statement must provide a resume to evidence they are suitably

qualified to make an assessment of the applicant.

The person making this statement must ensure that it is true and accurate in every detail

and that they may be called upon to provide evidence if required in a court of law.

Title ☐ Mr ☐ Mrs ☐ Ms ☐ Miss ☐ Other:

Name:

Street address:

Suburb: Postcode:

Phone (Mobile): Phone (W):

Email:

Relationship to

applicant

POSITION HELD/

EXPERIENCE/

QUALIFICATION:

Declarer feedback Did you feel you were given enough information and supported

through the process of undergoing this assessment?

☐ Yes ☐ No

Did you feel the resources provided were suitable for your

workplace?

☐ Yes ☐ No

Do you think the assessment was relevant to this particular

qualification’s training needs?

☐ Yes ☐ No

In my opinion the applicant has sufficient knowledge and skills in the competency required. I declare that

in making this statement, all details are true and correct and that I may be called upon to provide evidence

if required in a court of law.

Third party declarer signature ................................................................ Date .....................

Assessment V2.2 © AAMC Training Group A5

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

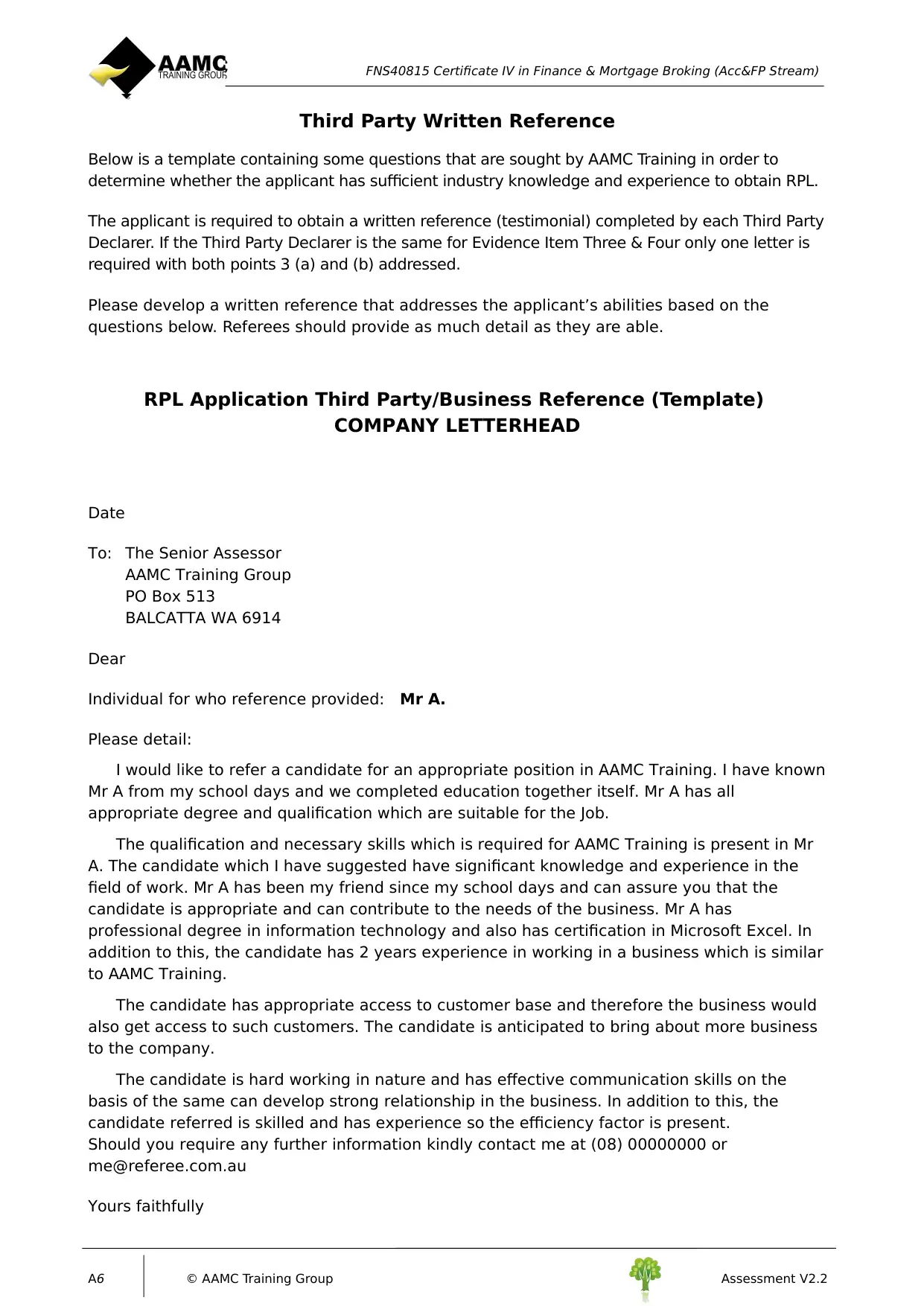

Third Party Written Reference

Below is a template containing some questions that are sought by AAMC Training in order to

determine whether the applicant has sufficient industry knowledge and experience to obtain RPL.

The applicant is required to obtain a written reference (testimonial) completed by each Third Party

Declarer. If the Third Party Declarer is the same for Evidence Item Three & Four only one letter is

required with both points 3 (a) and (b) addressed.

Please develop a written reference that addresses the applicant’s abilities based on the

questions below. Referees should provide as much detail as they are able.

RPL Application Third Party/Business Reference (Template)

COMPANY LETTERHEAD

Date

To: The Senior Assessor

AAMC Training Group

PO Box 513

BALCATTA WA 6914

Dear

Individual for who reference provided: Mr A.

Please detail:

I would like to refer a candidate for an appropriate position in AAMC Training. I have known

Mr A from my school days and we completed education together itself. Mr A has all

appropriate degree and qualification which are suitable for the Job.

The qualification and necessary skills which is required for AAMC Training is present in Mr

A. The candidate which I have suggested have significant knowledge and experience in the

field of work. Mr A has been my friend since my school days and can assure you that the

candidate is appropriate and can contribute to the needs of the business. Mr A has

professional degree in information technology and also has certification in Microsoft Excel. In

addition to this, the candidate has 2 years experience in working in a business which is similar

to AAMC Training.

The candidate has appropriate access to customer base and therefore the business would

also get access to such customers. The candidate is anticipated to bring about more business

to the company.

The candidate is hard working in nature and has effective communication skills on the

basis of the same can develop strong relationship in the business. In addition to this, the

candidate referred is skilled and has experience so the efficiency factor is present.

Should you require any further information kindly contact me at (08) 00000000 or

me@referee.com.au

Yours faithfully

A6 © AAMC Training Group Assessment V2.2

Third Party Written Reference

Below is a template containing some questions that are sought by AAMC Training in order to

determine whether the applicant has sufficient industry knowledge and experience to obtain RPL.

The applicant is required to obtain a written reference (testimonial) completed by each Third Party

Declarer. If the Third Party Declarer is the same for Evidence Item Three & Four only one letter is

required with both points 3 (a) and (b) addressed.

Please develop a written reference that addresses the applicant’s abilities based on the

questions below. Referees should provide as much detail as they are able.

RPL Application Third Party/Business Reference (Template)

COMPANY LETTERHEAD

Date

To: The Senior Assessor

AAMC Training Group

PO Box 513

BALCATTA WA 6914

Dear

Individual for who reference provided: Mr A.

Please detail:

I would like to refer a candidate for an appropriate position in AAMC Training. I have known

Mr A from my school days and we completed education together itself. Mr A has all

appropriate degree and qualification which are suitable for the Job.

The qualification and necessary skills which is required for AAMC Training is present in Mr

A. The candidate which I have suggested have significant knowledge and experience in the

field of work. Mr A has been my friend since my school days and can assure you that the

candidate is appropriate and can contribute to the needs of the business. Mr A has

professional degree in information technology and also has certification in Microsoft Excel. In

addition to this, the candidate has 2 years experience in working in a business which is similar

to AAMC Training.

The candidate has appropriate access to customer base and therefore the business would

also get access to such customers. The candidate is anticipated to bring about more business

to the company.

The candidate is hard working in nature and has effective communication skills on the

basis of the same can develop strong relationship in the business. In addition to this, the

candidate referred is skilled and has experience so the efficiency factor is present.

Should you require any further information kindly contact me at (08) 00000000 or

me@referee.com.au

Yours faithfully

A6 © AAMC Training Group Assessment V2.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

A Referee

Job Title

Task 2: Short answers

Answers to the following questions and scenarios may be found in the first module (Financial

Services Professional Practice, Legislation and Codes of Practice) of the learning guide from

the end of Section 2 to Section 8. You may also wish to refer to the relevant legislation via the

internet such as the ASIC National Consumer Protection Act 2009.

1. RESPONSIBLE LENDING SCENARIO

Scenario 1: Mustapha has just been told that come 1st July he would be stepping up as

the new Assistant Manager. On telling his partner Jenny the good news, she suggested

they start looking to buy a house as they’d probably be able to afford one. Excited, they

call a local finance broker who was previously referred to them by a friend.

The finance broker congratulated Mustapha on his imminent promotion and asked if they

would answer some questions to help determine how much they could borrow. Mustapha

and Jenny agreed to provide the required financial information. Mustapha and Jenny are

good savers and have sufficient funds to possibly cover for a 10 per cent deposit.

Jenny is cautious and felt a fixed rate loan would be better so they could budget

effectively. Mustapha felt no reason to disagree so the broker worked out a loan amount

based on the introductory rate which was fixed for the first six months. Mustapha’s

increased salary meant they could borrow a lot more than before. Jenny’s income varied

as she works casual at the local store. The broker asked Jenny how many hours she

worked on average to determine their combined income.

The broker signed and dated the preliminary assessment with today’s date. She then gave

Mustapha & Jenny a copy.

a. Explain the importance of making initial enquiries about a customer and verifying this

information.

The process of initial enquiry can be viewed as a very important function for a business and

the reasons for the same is stated below:

The initial enquiry of a needs of the customers would help the brokers to effectively

determine the credit requirement and also the capacity of the borrower, serviceability

preferences of the borrower and would ultimately result in a proper lending process.

On the basis of the initial enquiry, brokers can effectively give suggestions to the client

regarding the product which is to be choosen and also regarding the term period of the

loan which will be most suitable for the client.

Initial enquiry also helps the management to have health communication process with the

brokers and instruct them as to exactly what they are looking for and this therefore makes

the whole lendiong process more efficienct in nature.

b. Module 1, Section 2 of the learning guide covers responsible lending conduct

obligations in detail. Considering what a broker should cover in terms of responsible

Assessment V2.2 © AAMC Training Group A7

A Referee

Job Title

Task 2: Short answers

Answers to the following questions and scenarios may be found in the first module (Financial

Services Professional Practice, Legislation and Codes of Practice) of the learning guide from

the end of Section 2 to Section 8. You may also wish to refer to the relevant legislation via the

internet such as the ASIC National Consumer Protection Act 2009.

1. RESPONSIBLE LENDING SCENARIO

Scenario 1: Mustapha has just been told that come 1st July he would be stepping up as

the new Assistant Manager. On telling his partner Jenny the good news, she suggested

they start looking to buy a house as they’d probably be able to afford one. Excited, they

call a local finance broker who was previously referred to them by a friend.

The finance broker congratulated Mustapha on his imminent promotion and asked if they

would answer some questions to help determine how much they could borrow. Mustapha

and Jenny agreed to provide the required financial information. Mustapha and Jenny are

good savers and have sufficient funds to possibly cover for a 10 per cent deposit.

Jenny is cautious and felt a fixed rate loan would be better so they could budget

effectively. Mustapha felt no reason to disagree so the broker worked out a loan amount

based on the introductory rate which was fixed for the first six months. Mustapha’s

increased salary meant they could borrow a lot more than before. Jenny’s income varied

as she works casual at the local store. The broker asked Jenny how many hours she

worked on average to determine their combined income.

The broker signed and dated the preliminary assessment with today’s date. She then gave

Mustapha & Jenny a copy.

a. Explain the importance of making initial enquiries about a customer and verifying this

information.

The process of initial enquiry can be viewed as a very important function for a business and

the reasons for the same is stated below:

The initial enquiry of a needs of the customers would help the brokers to effectively

determine the credit requirement and also the capacity of the borrower, serviceability

preferences of the borrower and would ultimately result in a proper lending process.

On the basis of the initial enquiry, brokers can effectively give suggestions to the client

regarding the product which is to be choosen and also regarding the term period of the

loan which will be most suitable for the client.

Initial enquiry also helps the management to have health communication process with the

brokers and instruct them as to exactly what they are looking for and this therefore makes

the whole lendiong process more efficienct in nature.

b. Module 1, Section 2 of the learning guide covers responsible lending conduct

obligations in detail. Considering what a broker should cover in terms of responsible

Assessment V2.2 © AAMC Training Group A7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

lending, list at least five (5) things that the finance broker failed to provide/discuss in

Scenario 1 interview.

1 The broker did not make sufficient enquiries with the clients and certainly ot all

information is avalibale with the broker.

2 The broker failed to provide proper guidance to the clients and help them fet to a

decision. The case shows that there is a confusion between the client and his wife

and the former prefers a variable interest credit while the latter prefers fixed

interest rate credit. The broker should have guided them to get to a healthy

conclusion regarding the choice of credit facility.

3 The borker did not verify the financial status of the clients and therefore it can be

said that the broker is not efficient.

4 The broker did not conduct the prelimary assessment of the credit facility which

the client wants and the broker has also failed to comply with the relevant

documents.

5 The broker did not provide credit guide, fact find and Quote in his assessment.

Scenario 2: Mal and Corinne are seeking your advice in relation to refinancing their loan

after speaking with some friends who have a more flexible loan product and a better rate

with their lender.

c. Highlight the factors Mal and Corinne should consider before making the decision to

switch or refinance their loan.

The factors which are to be considered by Mal and Corinne before taking any decisions

regarding switch or refinance of loan is shown below:

Interest rate of the loan

Numerous fees related to the loan such as entry, exit and ongoing fees

Flexibility of the loan

Term period of the loan

Insurance on the mortgage part of the loan

Security against rise in interest rate.

2. CONSUMER PROTECTION

Scenario:

Stephen was a floor and wall tiler who earned $1,200 a week. He spent $600 a week on

expenses. He went to a lender to get a home loan of $200,000. Stephen needed a loan

with an average interest rate that he could pay off over the medium term.

Instead, he was offered a loan for $500,000 with a high fixed interest rate and therefore

repayments that he could not readily afford. As he was experiencing hardship, Stephen

sought an injunction against the lender collecting his mortgage repayments. Stephen then

A8 © AAMC Training Group Assessment V2.2

lending, list at least five (5) things that the finance broker failed to provide/discuss in

Scenario 1 interview.

1 The broker did not make sufficient enquiries with the clients and certainly ot all

information is avalibale with the broker.

2 The broker failed to provide proper guidance to the clients and help them fet to a

decision. The case shows that there is a confusion between the client and his wife

and the former prefers a variable interest credit while the latter prefers fixed

interest rate credit. The broker should have guided them to get to a healthy

conclusion regarding the choice of credit facility.

3 The borker did not verify the financial status of the clients and therefore it can be

said that the broker is not efficient.

4 The broker did not conduct the prelimary assessment of the credit facility which

the client wants and the broker has also failed to comply with the relevant

documents.

5 The broker did not provide credit guide, fact find and Quote in his assessment.

Scenario 2: Mal and Corinne are seeking your advice in relation to refinancing their loan

after speaking with some friends who have a more flexible loan product and a better rate

with their lender.

c. Highlight the factors Mal and Corinne should consider before making the decision to

switch or refinance their loan.

The factors which are to be considered by Mal and Corinne before taking any decisions

regarding switch or refinance of loan is shown below:

Interest rate of the loan

Numerous fees related to the loan such as entry, exit and ongoing fees

Flexibility of the loan

Term period of the loan

Insurance on the mortgage part of the loan

Security against rise in interest rate.

2. CONSUMER PROTECTION

Scenario:

Stephen was a floor and wall tiler who earned $1,200 a week. He spent $600 a week on

expenses. He went to a lender to get a home loan of $200,000. Stephen needed a loan

with an average interest rate that he could pay off over the medium term.

Instead, he was offered a loan for $500,000 with a high fixed interest rate and therefore

repayments that he could not readily afford. As he was experiencing hardship, Stephen

sought an injunction against the lender collecting his mortgage repayments. Stephen then

A8 © AAMC Training Group Assessment V2.2

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

sought compensation for the loss and damage he had suffered for being put into an

unsuitable loan.

a. Describe what you think will happen under the consumer protection provisions of the

responsible lending obligations.

As per the provisions of Consumer protection Act, the consumer can file for the

consumer remedy provision allows him to seek compensation for any loss or damage

which can be suffered by the client from the advisor.

b. What Penalties can be incurred? (Refer Learning Guide Module 1, Section 2)

The penalties which can be incurred are given below:

Criminal Penalties will apply for any misconducts and the same can include

imprisonment.

Fine would be applicable as civil liability

Infringement Notice would be applicable to ASIC

Consumer remedies which can include compensation.

3. DISCLOSURE AND PRESCRIBED DOCUMENTS

(Please note this relates to Finance/Mortgage Broking under the NCCP Act 2009

and not Financial Planning)

a. What document should a credit representative or Australian Credit Licence holder provide

to a client to explain about the services they offer? List some of the information contained

in this document.

Credit Guide: The credit guide can effectively provide information relating to the broker

and also hios profile. Credit guide also provide information relating to responsiblew

lending and resolution of disputes in a business. The credit guide also contains

assistance of the credit and summary of assessment.

b. In your OWN words, explain why is it important for a business to have a sufficient

complaint’s handling system? In your answer explain the essential steps in handling

and resolving a customer complaint. The Commonwealth Ombudsman has a good

Better Practice Guide to Complaint Handling publication on their website.

According to me, effective complaint handling process can bring bring about a

reduction the overall compliants which the business receives from the clients. The

reduction in the compliants of the business would result in enhanced customer

satisfaction and this will also attract new customer to the business.

The essential steps which needs to be followed for the purpose of ensuring that the

compliants of the customers are effectively handled:

Assessment V2.2 © AAMC Training Group A9

sought compensation for the loss and damage he had suffered for being put into an

unsuitable loan.

a. Describe what you think will happen under the consumer protection provisions of the

responsible lending obligations.

As per the provisions of Consumer protection Act, the consumer can file for the

consumer remedy provision allows him to seek compensation for any loss or damage

which can be suffered by the client from the advisor.

b. What Penalties can be incurred? (Refer Learning Guide Module 1, Section 2)

The penalties which can be incurred are given below:

Criminal Penalties will apply for any misconducts and the same can include

imprisonment.

Fine would be applicable as civil liability

Infringement Notice would be applicable to ASIC

Consumer remedies which can include compensation.

3. DISCLOSURE AND PRESCRIBED DOCUMENTS

(Please note this relates to Finance/Mortgage Broking under the NCCP Act 2009

and not Financial Planning)

a. What document should a credit representative or Australian Credit Licence holder provide

to a client to explain about the services they offer? List some of the information contained

in this document.

Credit Guide: The credit guide can effectively provide information relating to the broker

and also hios profile. Credit guide also provide information relating to responsiblew

lending and resolution of disputes in a business. The credit guide also contains

assistance of the credit and summary of assessment.

b. In your OWN words, explain why is it important for a business to have a sufficient

complaint’s handling system? In your answer explain the essential steps in handling

and resolving a customer complaint. The Commonwealth Ombudsman has a good

Better Practice Guide to Complaint Handling publication on their website.

According to me, effective complaint handling process can bring bring about a

reduction the overall compliants which the business receives from the clients. The

reduction in the compliants of the business would result in enhanced customer

satisfaction and this will also attract new customer to the business.

The essential steps which needs to be followed for the purpose of ensuring that the

compliants of the customers are effectively handled:

Assessment V2.2 © AAMC Training Group A9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

The first and foremost step is to effectively listen to what the customer has to say and

full undivided attention is to be provided. The management should respond in calm

and polite way in order to ensure that the customers are not offended further.

The person who is handling the compliants after listening to the client should

empathize with the client and understand the position in which the client stands. This

will help in creating a strong bond between the two. This will also allow the business

effectively resolve the issues which the client faces.

The next step is to offer a solution which would address every concern of the client and

in many cases, the solution would not be the same that the client wants but the same

needs to be negotiated with the client in a polite manner.

After the client has agreed to the solution, the management need to take the

necessary steps for carrying out the solution

One the complaint of the client is solved, the management needs to follow up whether

the client is statisfied with the solution or not.

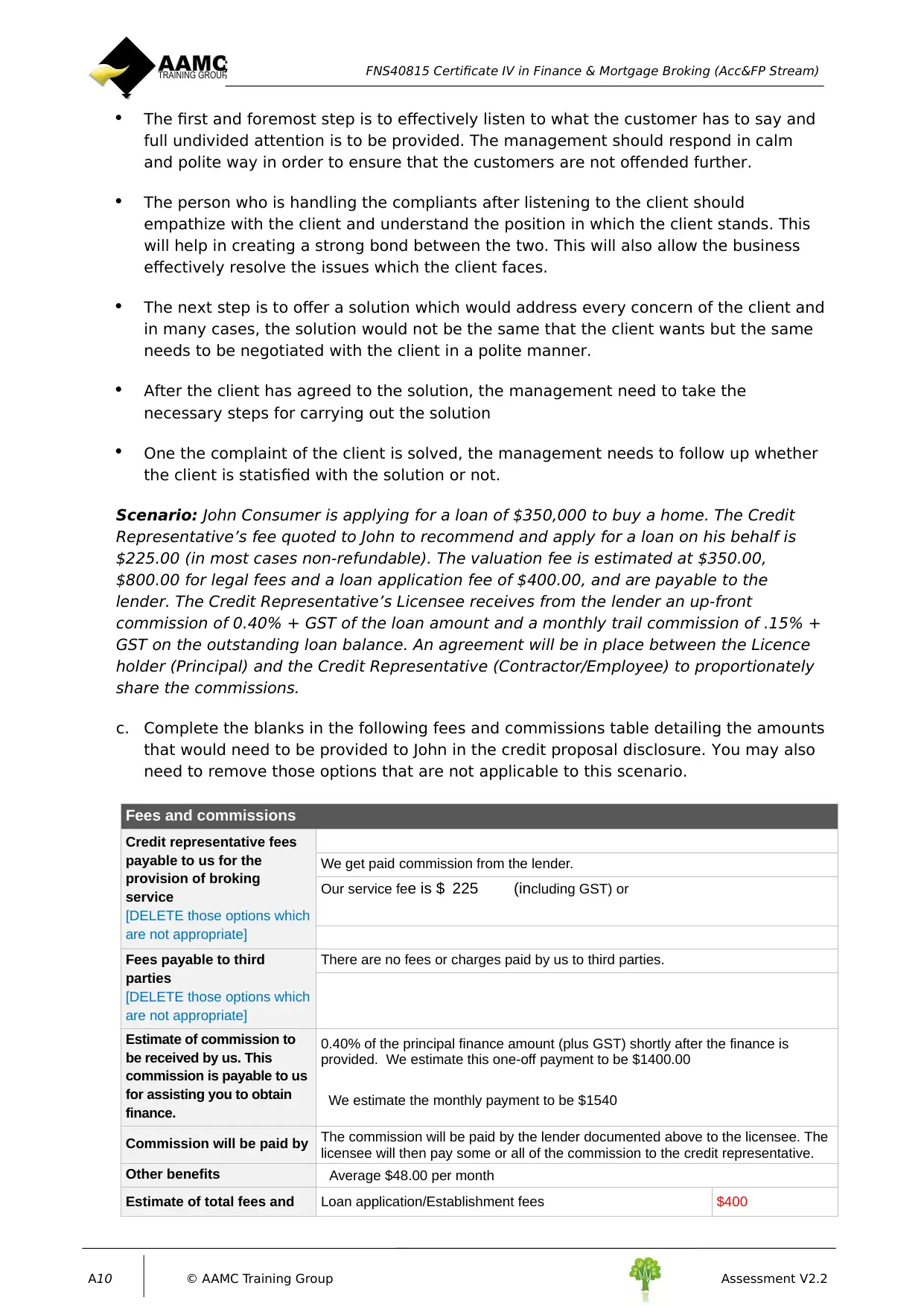

Scenario: John Consumer is applying for a loan of $350,000 to buy a home. The Credit

Representative’s fee quoted to John to recommend and apply for a loan on his behalf is

$225.00 (in most cases non-refundable). The valuation fee is estimated at $350.00,

$800.00 for legal fees and a loan application fee of $400.00, and are payable to the

lender. The Credit Representative’s Licensee receives from the lender an up-front

commission of 0.40% + GST of the loan amount and a monthly trail commission of .15% +

GST on the outstanding loan balance. An agreement will be in place between the Licence

holder (Principal) and the Credit Representative (Contractor/Employee) to proportionately

share the commissions.

c. Complete the blanks in the following fees and commissions table detailing the amounts

that would need to be provided to John in the credit proposal disclosure. You may also

need to remove those options that are not applicable to this scenario.

Fees and commissions

Credit representative fees

payable to us for the

provision of broking

service

[DELETE those options which

are not appropriate]

We get paid commission from the lender.

Our service fee is $ 225 (including GST) or

Fees payable to third

parties

[DELETE those options which

are not appropriate]

There are no fees or charges paid by us to third parties.

Estimate of commission to

be received by us. This

commission is payable to us

for assisting you to obtain

finance.

0.40% of the principal finance amount (plus GST) shortly after the finance is

provided. We estimate this one-off payment to be $1400.00

We estimate the monthly payment to be $1540

Commission will be paid by The commission will be paid by the lender documented above to the licensee. The

licensee will then pay some or all of the commission to the credit representative.

Other benefits Average $48.00 per month

Estimate of total fees and Loan application/Establishment fees $400

A10 © AAMC Training Group Assessment V2.2

The first and foremost step is to effectively listen to what the customer has to say and

full undivided attention is to be provided. The management should respond in calm

and polite way in order to ensure that the customers are not offended further.

The person who is handling the compliants after listening to the client should

empathize with the client and understand the position in which the client stands. This

will help in creating a strong bond between the two. This will also allow the business

effectively resolve the issues which the client faces.

The next step is to offer a solution which would address every concern of the client and

in many cases, the solution would not be the same that the client wants but the same

needs to be negotiated with the client in a polite manner.

After the client has agreed to the solution, the management need to take the

necessary steps for carrying out the solution

One the complaint of the client is solved, the management needs to follow up whether

the client is statisfied with the solution or not.

Scenario: John Consumer is applying for a loan of $350,000 to buy a home. The Credit

Representative’s fee quoted to John to recommend and apply for a loan on his behalf is

$225.00 (in most cases non-refundable). The valuation fee is estimated at $350.00,

$800.00 for legal fees and a loan application fee of $400.00, and are payable to the

lender. The Credit Representative’s Licensee receives from the lender an up-front

commission of 0.40% + GST of the loan amount and a monthly trail commission of .15% +

GST on the outstanding loan balance. An agreement will be in place between the Licence

holder (Principal) and the Credit Representative (Contractor/Employee) to proportionately

share the commissions.

c. Complete the blanks in the following fees and commissions table detailing the amounts

that would need to be provided to John in the credit proposal disclosure. You may also

need to remove those options that are not applicable to this scenario.

Fees and commissions

Credit representative fees

payable to us for the

provision of broking

service

[DELETE those options which

are not appropriate]

We get paid commission from the lender.

Our service fee is $ 225 (including GST) or

Fees payable to third

parties

[DELETE those options which

are not appropriate]

There are no fees or charges paid by us to third parties.

Estimate of commission to

be received by us. This

commission is payable to us

for assisting you to obtain

finance.

0.40% of the principal finance amount (plus GST) shortly after the finance is

provided. We estimate this one-off payment to be $1400.00

We estimate the monthly payment to be $1540

Commission will be paid by The commission will be paid by the lender documented above to the licensee. The

licensee will then pay some or all of the commission to the credit representative.

Other benefits Average $48.00 per month

Estimate of total fees and Loan application/Establishment fees $400

A10 © AAMC Training Group Assessment V2.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

charges payable to the

financier in relation to

applying for the finance.

These fees are payable by

you.

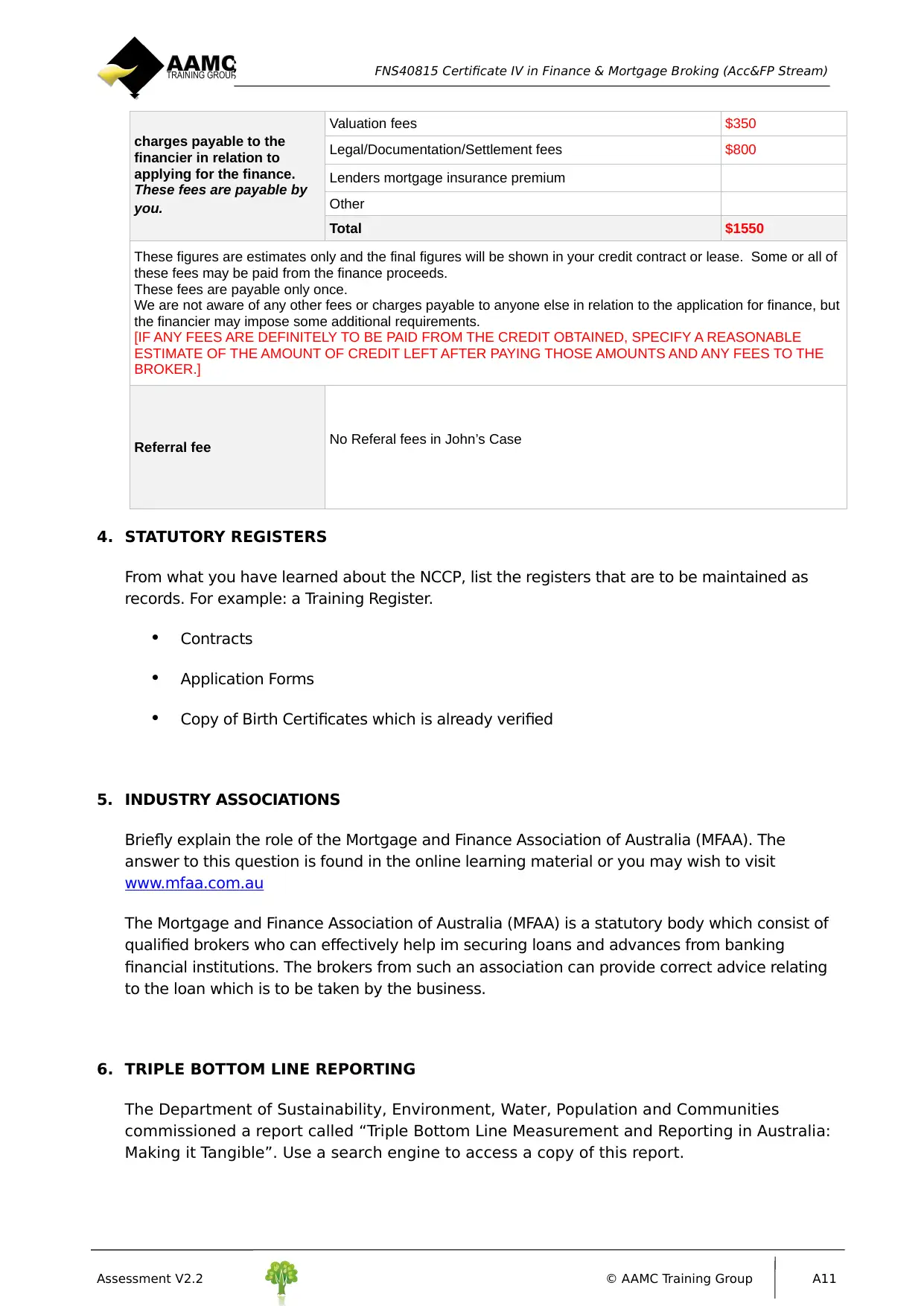

Valuation fees $350

Legal/Documentation/Settlement fees $800

Lenders mortgage insurance premium

Other

Total $1550

These figures are estimates only and the final figures will be shown in your credit contract or lease. Some or all of

these fees may be paid from the finance proceeds.

These fees are payable only once.

We are not aware of any other fees or charges payable to anyone else in relation to the application for finance, but

the financier may impose some additional requirements.

[IF ANY FEES ARE DEFINITELY TO BE PAID FROM THE CREDIT OBTAINED, SPECIFY A REASONABLE

ESTIMATE OF THE AMOUNT OF CREDIT LEFT AFTER PAYING THOSE AMOUNTS AND ANY FEES TO THE

BROKER.]

Referral fee No Referal fees in John’s Case

4. STATUTORY REGISTERS

From what you have learned about the NCCP, list the registers that are to be maintained as

records. For example: a Training Register.

Contracts

Application Forms

Copy of Birth Certificates which is already verified

5. INDUSTRY ASSOCIATIONS

Briefly explain the role of the Mortgage and Finance Association of Australia (MFAA). The

answer to this question is found in the online learning material or you may wish to visit

www.mfaa.com.au

The Mortgage and Finance Association of Australia (MFAA) is a statutory body which consist of

qualified brokers who can effectively help im securing loans and advances from banking

financial institutions. The brokers from such an association can provide correct advice relating

to the loan which is to be taken by the business.

6. TRIPLE BOTTOM LINE REPORTING

The Department of Sustainability, Environment, Water, Population and Communities

commissioned a report called “Triple Bottom Line Measurement and Reporting in Australia:

Making it Tangible”. Use a search engine to access a copy of this report.

Assessment V2.2 © AAMC Training Group A11

charges payable to the

financier in relation to

applying for the finance.

These fees are payable by

you.

Valuation fees $350

Legal/Documentation/Settlement fees $800

Lenders mortgage insurance premium

Other

Total $1550

These figures are estimates only and the final figures will be shown in your credit contract or lease. Some or all of

these fees may be paid from the finance proceeds.

These fees are payable only once.

We are not aware of any other fees or charges payable to anyone else in relation to the application for finance, but

the financier may impose some additional requirements.

[IF ANY FEES ARE DEFINITELY TO BE PAID FROM THE CREDIT OBTAINED, SPECIFY A REASONABLE

ESTIMATE OF THE AMOUNT OF CREDIT LEFT AFTER PAYING THOSE AMOUNTS AND ANY FEES TO THE

BROKER.]

Referral fee No Referal fees in John’s Case

4. STATUTORY REGISTERS

From what you have learned about the NCCP, list the registers that are to be maintained as

records. For example: a Training Register.

Contracts

Application Forms

Copy of Birth Certificates which is already verified

5. INDUSTRY ASSOCIATIONS

Briefly explain the role of the Mortgage and Finance Association of Australia (MFAA). The

answer to this question is found in the online learning material or you may wish to visit

www.mfaa.com.au

The Mortgage and Finance Association of Australia (MFAA) is a statutory body which consist of

qualified brokers who can effectively help im securing loans and advances from banking

financial institutions. The brokers from such an association can provide correct advice relating

to the loan which is to be taken by the business.

6. TRIPLE BOTTOM LINE REPORTING

The Department of Sustainability, Environment, Water, Population and Communities

commissioned a report called “Triple Bottom Line Measurement and Reporting in Australia:

Making it Tangible”. Use a search engine to access a copy of this report.

Assessment V2.2 © AAMC Training Group A11

FNS40815 Certificate IV in Finance & Mortgage Broking (Acc&FP Stream)

After reading the report please express in your own words the five broad categories that

capture the current diverse state of play in performance measurement and reporting in

Australia.

1. Wait and See can be identified as the category where the companies are satisfied with the presenty

scenario and can bring about communication and accountability.

2. Establish a commitment with the stakeholders s that openness and transparency can be maintained.

3. The business ne3eds to seek alignment between shateholder’s expectation and corporate staretegy

and the same can be started from the scratch. This approach requires establiushing a new

management system which is a long process.

4. The management needs to focus on sustainability and partnership principles so that the same cam be

embedded in the management system.

5. Some companies which are mostly in private ownership often define the commitment to their

sustainability practices.

6.

7. SUSTAINABLE BANKING

Sustainability is not confined to our larger financial institutions like CBA, NAB and IAG. It is

also being embraced by smaller institutions such as Maleny Credit Union (MCU)

Sustainable Banking. MCU began operations in 1984 as a community based credit union

located in Maleny, Queensland.

The MCU Board of Directors is committed to long-term sustainability and believes the

credit union has social and environmental obligations in addition to providing sound

financial management. MCU practices "triple bottom line" reporting as a way of measuring

progress and ensuring accountability against its sustainability targets.

Review the MCU website and detail how MCU practices socially responsible investment.

MCU practices socially responsible investment by following the steps:

Providing loans to members for sustainale environment purposes

Enabling donations from the members of local, national and global organization

Providing assistance to micro finace groups.

8. TEAM WORK AND ORGANISATIONAL PLANNING

You have recently been employed as a Mortgage Broker in a medium-sized Mortgage

Broking practice. You are in charge of a small team of inexperienced mortgage brokers and

Administration support staff. You discover that morale in the firm is low because:

People are unable to distinguish between tasks that require them to work

autonomously from those that require them to work as part of a team.

There is a lack of communication about team activities.

Due to the relative inexperience of the team, the image of the firm internally and

externally is not very good.

A12 © AAMC Training Group Assessment V2.2

After reading the report please express in your own words the five broad categories that

capture the current diverse state of play in performance measurement and reporting in

Australia.

1. Wait and See can be identified as the category where the companies are satisfied with the presenty

scenario and can bring about communication and accountability.

2. Establish a commitment with the stakeholders s that openness and transparency can be maintained.

3. The business ne3eds to seek alignment between shateholder’s expectation and corporate staretegy

and the same can be started from the scratch. This approach requires establiushing a new

management system which is a long process.

4. The management needs to focus on sustainability and partnership principles so that the same cam be

embedded in the management system.

5. Some companies which are mostly in private ownership often define the commitment to their

sustainability practices.

6.

7. SUSTAINABLE BANKING

Sustainability is not confined to our larger financial institutions like CBA, NAB and IAG. It is

also being embraced by smaller institutions such as Maleny Credit Union (MCU)

Sustainable Banking. MCU began operations in 1984 as a community based credit union

located in Maleny, Queensland.

The MCU Board of Directors is committed to long-term sustainability and believes the

credit union has social and environmental obligations in addition to providing sound

financial management. MCU practices "triple bottom line" reporting as a way of measuring

progress and ensuring accountability against its sustainability targets.

Review the MCU website and detail how MCU practices socially responsible investment.

MCU practices socially responsible investment by following the steps:

Providing loans to members for sustainale environment purposes

Enabling donations from the members of local, national and global organization

Providing assistance to micro finace groups.

8. TEAM WORK AND ORGANISATIONAL PLANNING

You have recently been employed as a Mortgage Broker in a medium-sized Mortgage

Broking practice. You are in charge of a small team of inexperienced mortgage brokers and

Administration support staff. You discover that morale in the firm is low because:

People are unable to distinguish between tasks that require them to work

autonomously from those that require them to work as part of a team.

There is a lack of communication about team activities.

Due to the relative inexperience of the team, the image of the firm internally and

externally is not very good.

A12 © AAMC Training Group Assessment V2.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.