Certificate IV in Finance Assignment

VerifiedAdded on 2020/02/23

|43

|12219

|44

Homework Assignment

AI Summary

This assignment for the Certificate IV in Finance and Mortgage Broking includes various tasks related to financial assessments, client interactions, and mortgage recommendations. Students are required to analyze case studies, complete client information collection tools, and provide detailed proposals based on the financial situations of clients. The assignment emphasizes understanding responsible lending obligations and the necessary documentation for mortgage applications.

Assignment

Certificate IV in Finance and Mortgage Broking

(CIVMBv1_AS_A2)

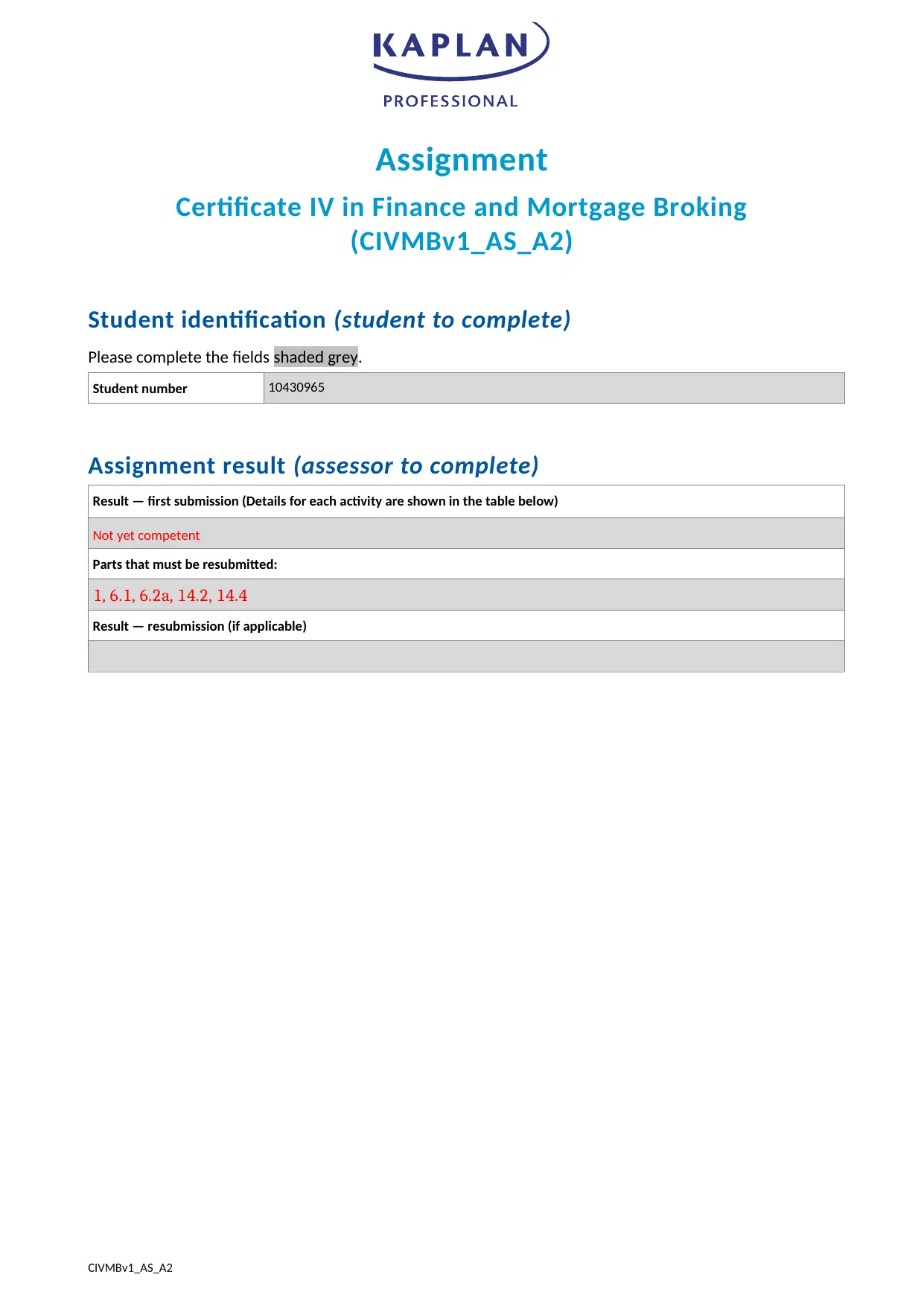

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10430965

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Not yet competent

Parts that must be resubmitted:

1, 6.1, 6.2a, 14.2, 14.4

Result — resubmission (if applicable)

CIVMBv1_AS_A2

Certificate IV in Finance and Mortgage Broking

(CIVMBv1_AS_A2)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10430965

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Not yet competent

Parts that must be resubmitted:

1, 6.1, 6.2a, 14.2, 14.4

Result — resubmission (if applicable)

CIVMBv1_AS_A2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

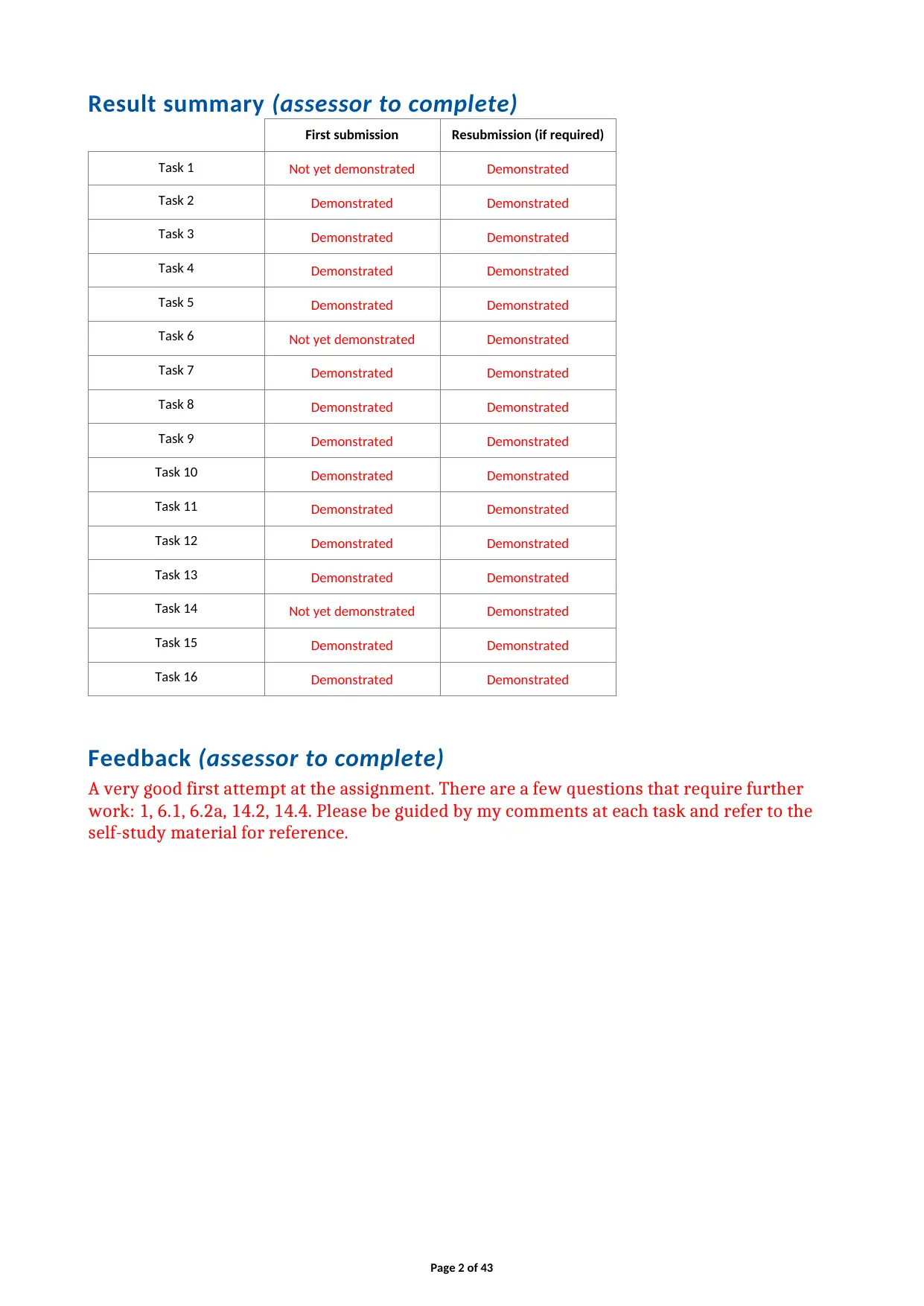

Result summary (assessor to complete)

First submission Resubmission (if required)

Task 1 Not yet demonstrated Demonstrated

Task 2 Demonstrated Demonstrated

Task 3 Demonstrated Demonstrated

Task 4 Demonstrated Demonstrated

Task 5 Demonstrated Demonstrated

Task 6 Not yet demonstrated Demonstrated

Task 7 Demonstrated Demonstrated

Task 8 Demonstrated Demonstrated

Task 9 Demonstrated Demonstrated

Task 10 Demonstrated Demonstrated

Task 11 Demonstrated Demonstrated

Task 12 Demonstrated Demonstrated

Task 13 Demonstrated Demonstrated

Task 14 Not yet demonstrated Demonstrated

Task 15 Demonstrated Demonstrated

Task 16 Demonstrated Demonstrated

Feedback (assessor to complete)

A very good first attempt at the assignment. There are a few questions that require further

work: 1, 6.1, 6.2a, 14.2, 14.4. Please be guided by my comments at each task and refer to the

self-study material for reference.

Page 2 of 43

First submission Resubmission (if required)

Task 1 Not yet demonstrated Demonstrated

Task 2 Demonstrated Demonstrated

Task 3 Demonstrated Demonstrated

Task 4 Demonstrated Demonstrated

Task 5 Demonstrated Demonstrated

Task 6 Not yet demonstrated Demonstrated

Task 7 Demonstrated Demonstrated

Task 8 Demonstrated Demonstrated

Task 9 Demonstrated Demonstrated

Task 10 Demonstrated Demonstrated

Task 11 Demonstrated Demonstrated

Task 12 Demonstrated Demonstrated

Task 13 Demonstrated Demonstrated

Task 14 Not yet demonstrated Demonstrated

Task 15 Demonstrated Demonstrated

Task 16 Demonstrated Demonstrated

Feedback (assessor to complete)

A very good first attempt at the assignment. There are a few questions that require further

work: 1, 6.1, 6.2a, 14.2, 14.4. Please be guided by my comments at each task and refer to the

self-study material for reference.

Page 2 of 43

Before you begin

Read everything in this document before you start your assignment for Certificate IV in Finance and

Mortgage Broking.

About this document

This document includes the following parts:

• Instructions for completing and submitting this assignment

• Results and feedback

• Section 1: Case study 1 — Malcolm and Susan Johnson

• Section 2: Case study 2 — John Simpson

• Appendix 1: Fact Finder

Instructions for completing and submitting this assignment

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete the

assignment within your enrolment period. Your study plan is in the KapLearn Certificate IV in Finance and

Mortgage Broking subject room.

Completing the assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1B_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

The assignment

This assignment is split into 16 Tasks, over 3 Sections. To finish this assignment, you must complete all

16 tasks.

The information and data you need to complete Sections 1 & 2 is presented in case studies at the beginning

of those sections.

Page 3 of 43

Read everything in this document before you start your assignment for Certificate IV in Finance and

Mortgage Broking.

About this document

This document includes the following parts:

• Instructions for completing and submitting this assignment

• Results and feedback

• Section 1: Case study 1 — Malcolm and Susan Johnson

• Section 2: Case study 2 — John Simpson

• Appendix 1: Fact Finder

Instructions for completing and submitting this assignment

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete the

assignment within your enrolment period. Your study plan is in the KapLearn Certificate IV in Finance and

Mortgage Broking subject room.

Completing the assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1B_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

The assignment

This assignment is split into 16 Tasks, over 3 Sections. To finish this assignment, you must complete all

16 tasks.

The information and data you need to complete Sections 1 & 2 is presented in case studies at the beginning

of those sections.

Page 3 of 43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the Client Information Collection Tool in Appendix 1, assumptions are permitted although

they must not be in conflict with the information provided in the Case Study.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements, or to calculate any service fees

that may be applicable.

Page 4 of 43

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the Client Information Collection Tool in Appendix 1, assumptions are permitted although

they must not be in conflict with the information provided in the Case Study.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements, or to calculate any service fees

that may be applicable.

Page 4 of 43

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Submitting the assignment

You must submit your completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed

all parts and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Certificate IV in Finance and

Mortgage Broking subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 5 of 43

You must submit your completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed

all parts and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Certificate IV in Finance and

Mortgage Broking subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 5 of 43

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 6 of 43

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 6 of 43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 1: Case study 1 — Malcolm and Susan Johnson

Background

Malcolm and Susan Johnson are a young couple about to buy their first home. They have been married for

five years and during that time have rented an apartment while also saving for their own home.

They have been looking at properties for the last month and one has really caught their eye, although the

bathroom and ensuite could do with a little work. They had planned on shopping around the various

lenders themselves to find the most appropriate loan for their needs, but as they both work, they have little

time to do the research necessary. And, as they both admit, they have limited knowledge of the loan

products available and might have difficulty in evaluating the options.

They have not paid a deposit at this stage.

On a suggestion from Susan’s brother (one of your former clients) they have contacted you about the loan.

Following is a summary of the details of the property they wish to purchase, the couple’s financial and

employment details, and the loan features they require.

The property

Address: Unit 12, 43 Seaside Parade, Coastville, <Your State>

Purchase price: $490,000

Description: 2 bedroom strata title unit

Agent details: Steven Allstone

Phone: 8282 1113

Mobile: 0412 880 088

The couple

Current address: Unit 12, 22 Wentworth Lane, Highville, <Your State>

Malcolm and Susan have lived there 5 years

Home phone: 9001 2121

Funds position

Purchase price: $490,000

Estimated costs: $20,000

Total required: $510,000

Loan: $430,000

Own contribution: $80,000

Page 7 of 43

Background

Malcolm and Susan Johnson are a young couple about to buy their first home. They have been married for

five years and during that time have rented an apartment while also saving for their own home.

They have been looking at properties for the last month and one has really caught their eye, although the

bathroom and ensuite could do with a little work. They had planned on shopping around the various

lenders themselves to find the most appropriate loan for their needs, but as they both work, they have little

time to do the research necessary. And, as they both admit, they have limited knowledge of the loan

products available and might have difficulty in evaluating the options.

They have not paid a deposit at this stage.

On a suggestion from Susan’s brother (one of your former clients) they have contacted you about the loan.

Following is a summary of the details of the property they wish to purchase, the couple’s financial and

employment details, and the loan features they require.

The property

Address: Unit 12, 43 Seaside Parade, Coastville, <Your State>

Purchase price: $490,000

Description: 2 bedroom strata title unit

Agent details: Steven Allstone

Phone: 8282 1113

Mobile: 0412 880 088

The couple

Current address: Unit 12, 22 Wentworth Lane, Highville, <Your State>

Malcolm and Susan have lived there 5 years

Home phone: 9001 2121

Funds position

Purchase price: $490,000

Estimated costs: $20,000

Total required: $510,000

Loan: $430,000

Own contribution: $80,000

Page 7 of 43

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assets

Capital Bank savings account (joint) $92,000

Capital Bank cheque account (joint) $1,600

Holden Commodore SS, eight years old (Malcolm) $25,000

Suzuki Baleno, seven years old (Susan) $9,000

Superannuation — Capital Bank (Malcolm) $28,000

Superannuation — Capital Bank (Susan) $62,000

Household effects (insured value) $40,000

Liabilities

Capital Bank personal loan (Malcolm) $3,600

(repayments $180 p.m.)

Capital Bank Visa card (Malcolm) $200

(limit $2,000)

Capital Bank Visa card (Susan) $600

(limit $3,000)

All debts have been repaid according to arrangements. In relation to the credit card debt, the minimum

monthly commitment should be calculated at 3% of the credit limit.

Income/employment

Malcolm (date of birth 21/2/86)

Position: Team leader (full time)

Employer: ACME Limited

101 City Rd, Westside, <Your State>

Phone: 9800 1111

Income (gross): $55,000 p.a., net monthly income: $3,705

Employer contact: Alison Johnson, HR Manager

Length of service: 10 years

Driver’s licence: 8855KL

Email: malcolmj@acme.com.au

Page 8 of 43

Capital Bank savings account (joint) $92,000

Capital Bank cheque account (joint) $1,600

Holden Commodore SS, eight years old (Malcolm) $25,000

Suzuki Baleno, seven years old (Susan) $9,000

Superannuation — Capital Bank (Malcolm) $28,000

Superannuation — Capital Bank (Susan) $62,000

Household effects (insured value) $40,000

Liabilities

Capital Bank personal loan (Malcolm) $3,600

(repayments $180 p.m.)

Capital Bank Visa card (Malcolm) $200

(limit $2,000)

Capital Bank Visa card (Susan) $600

(limit $3,000)

All debts have been repaid according to arrangements. In relation to the credit card debt, the minimum

monthly commitment should be calculated at 3% of the credit limit.

Income/employment

Malcolm (date of birth 21/2/86)

Position: Team leader (full time)

Employer: ACME Limited

101 City Rd, Westside, <Your State>

Phone: 9800 1111

Income (gross): $55,000 p.a., net monthly income: $3,705

Employer contact: Alison Johnson, HR Manager

Length of service: 10 years

Driver’s licence: 8855KL

Email: malcolmj@acme.com.au

Page 8 of 43

Susan (date of birth 8/10/87)

Position: Accountant (full time)

Employer: Phones R Us

804 High Street, City East, <Your State>

Phone: 9910 2033

Income (gross): $91,000 p.a., net monthly income: $5,629

Employer contact: Stan Adams, HR Manager

Length of service: 12 years

Driver’s licence: 17016C

Email: sjohnson@phonesrus.com.au

Interest income

Approximately $40 per month from $12,000, remaining in savings account after home loan deposit. Interest

4% p.a.

Solicitor’s details

Jones and Co

22 High Street, City East, <Your State>

Phone: 8281 1382

Fax: 8290 1800

The loan requirements

• 30-year term

• Premium Option home loan

• standard variable interest rate @ 5.57%

• proposed settlement date — 6 weeks time

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• funds access via card

• offset facility.

Page 9 of 43

Position: Accountant (full time)

Employer: Phones R Us

804 High Street, City East, <Your State>

Phone: 9910 2033

Income (gross): $91,000 p.a., net monthly income: $5,629

Employer contact: Stan Adams, HR Manager

Length of service: 12 years

Driver’s licence: 17016C

Email: sjohnson@phonesrus.com.au

Interest income

Approximately $40 per month from $12,000, remaining in savings account after home loan deposit. Interest

4% p.a.

Solicitor’s details

Jones and Co

22 High Street, City East, <Your State>

Phone: 8281 1382

Fax: 8290 1800

The loan requirements

• 30-year term

• Premium Option home loan

• standard variable interest rate @ 5.57%

• proposed settlement date — 6 weeks time

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• funds access via card

• offset facility.

Page 9 of 43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assignment tasks (student to complete)

Task 1 — Initial disclosures

Following a personal introduction, and before you begin gathering information about the clients’ existing

financial situation or needs, there are certain disclosures you are required to make as a finance broker

regarding the way you are remunerated and the range and limitation of your services.

Identify and describe three (3) of these disclosures. (200 words)

Student response to Task 1

The three disclosures prior to the gathering the information from the client are:

1. How the intermediary is to be paid: The process that would be used for the payment to the

intermediaries is to be laid down so that the client has adequate knowledge about the mode of

payment and how it would reduce the time.

2. Who the intermediary represents: It is essential to reveal the client about who the intermediary

represents so that the client has knowledge about whom they are paying the money and does not

go missing.

3. Who the intermediary pays for the referrals: The referrals are paid by the intermediary to the

individuals who are making the referrals and bringing in new clients.

The three disclosures that requires to be mentioned are:

1. Credit Guide: It provides primary data regarding the broker to the consumer. The time of providing

the credit guide is dependent upon the kind of entity the broker is and the what credit operations,

the broker engages in but would be specifically before initiating in the credit operations of the

consumers.

2. Quote: Quote describes the consumers about the anticipated costs before making use of the

services if the fee of the consumer is charged. Before initiating the credit assistance, a quote

requires to be given to the consumers and the consumer requires to accept the quote by signing

the quote.

3. Proposal Document: A proposal document provides the cost to the consumers of making use of the

services that are inclusive of the commission of the broker that they may receive. A proposal

document requires to be given to the consumer during the same time of credit assistance given to a

consumer.

Page 10 of 43

Task 1 — Initial disclosures

Following a personal introduction, and before you begin gathering information about the clients’ existing

financial situation or needs, there are certain disclosures you are required to make as a finance broker

regarding the way you are remunerated and the range and limitation of your services.

Identify and describe three (3) of these disclosures. (200 words)

Student response to Task 1

The three disclosures prior to the gathering the information from the client are:

1. How the intermediary is to be paid: The process that would be used for the payment to the

intermediaries is to be laid down so that the client has adequate knowledge about the mode of

payment and how it would reduce the time.

2. Who the intermediary represents: It is essential to reveal the client about who the intermediary

represents so that the client has knowledge about whom they are paying the money and does not

go missing.

3. Who the intermediary pays for the referrals: The referrals are paid by the intermediary to the

individuals who are making the referrals and bringing in new clients.

The three disclosures that requires to be mentioned are:

1. Credit Guide: It provides primary data regarding the broker to the consumer. The time of providing

the credit guide is dependent upon the kind of entity the broker is and the what credit operations,

the broker engages in but would be specifically before initiating in the credit operations of the

consumers.

2. Quote: Quote describes the consumers about the anticipated costs before making use of the

services if the fee of the consumer is charged. Before initiating the credit assistance, a quote

requires to be given to the consumers and the consumer requires to accept the quote by signing

the quote.

3. Proposal Document: A proposal document provides the cost to the consumers of making use of the

services that are inclusive of the commission of the broker that they may receive. A proposal

document requires to be given to the consumer during the same time of credit assistance given to a

consumer.

Page 10 of 43

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessor feedback: Resubmission required?

You have correctly identified the documents to be provided to the

client at different stages however the question asks you to identify

and describe three disclosures you should make prior to gathering

information from client, not the documents. What disclosures

particularly are included in the Credit Guide? Topic 3.1 page 20 may

also assist.

Refer to MFAA Code Of Practice 2014 on its website and ASIC website:

http://asic.gov.au/regulatory-resources/credit/responsible-lending/

responsible-lending-disclosure-obligations-overview-for-credit-

licensees-and-representatives/

Yes

Task 2 — Gathering and documenting client information

Complete the Client Information Collection Tool located at the end of the assignment in Appendix 1 using

the information provided in Case Study 1.

Note: Any assumptions you make should be listed, and not be in conflict with the case study information

already provided.

You have demonstrated that you are competent regards to this Task.

Page 11 of 43

You have correctly identified the documents to be provided to the

client at different stages however the question asks you to identify

and describe three disclosures you should make prior to gathering

information from client, not the documents. What disclosures

particularly are included in the Credit Guide? Topic 3.1 page 20 may

also assist.

Refer to MFAA Code Of Practice 2014 on its website and ASIC website:

http://asic.gov.au/regulatory-resources/credit/responsible-lending/

responsible-lending-disclosure-obligations-overview-for-credit-

licensees-and-representatives/

Yes

Task 2 — Gathering and documenting client information

Complete the Client Information Collection Tool located at the end of the assignment in Appendix 1 using

the information provided in Case Study 1.

Note: Any assumptions you make should be listed, and not be in conflict with the case study information

already provided.

You have demonstrated that you are competent regards to this Task.

Page 11 of 43

Task 3 — Assessing the clients’ situation

1. Based on the information provided in the case study and using the tools available to you

(e.g. loan calculators, including those available on lenders’ websites), provide an assessment of

the clients’ borrowing ability and ability to service the loan they require.

Consider and comment on issues such as:

• borrowing ability in relation to the loan required

• deposit requirements for the loan required

• repayment ability based on the loan required

• likelihood that the clients will be able to meet their financial obligations

• do they require Lenders Mortgage Insurance (LMI), and if so, how much will it cost

• any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions. (750 words)

Student response to Task 3: Question 1

The borrowing capability of Malcolm and Susan cam ne understood easily by assessing their asset and

liabilities statement. It is known that the couple has been married for over 5 years and has being living in a

rented house. They are in the idea of purchasing their own house and therefore has been looking for

various options of loan. They wants to purchase a property that is situated in 43 Seaside Parade Coastville

that has a cost of $490,000 and the Gant name is Steven Allstone. It is seen that the price of the property is

$490,000 and the anticipated costs associated to the property is $20,000 and thus the total cost comes to

$510,000. The amount of loan they want to receive is $430,000 and they have the idea of making a down

payment of $80,000.

The asset consists of $92,000 in the savings account of capital bank which has a value of $1,600 in the

cheque account of capital bank, superannuation of value of $90,000 for the couple as a both. They have

two cars for each of the couple with a value of $34,000 and value of household comprising of $40,000 and

the liabilities consists of the personal loan of $3600 and an outstanding credit card amount of of $800 for

the couple. Malcolm is working in ACME Ltd as a team leader and has annual income of $55,000 and Susan

is an accountant in Phones r Us with an annual salary of $91,000. It has been observed that the total annual

salary of the couple as a whole is $146,000 and the loan interest of 5.575 that results to $2460 per month

and therefore the amount can be paid with ease by the couple. The down payment value of $80,000 can be

paid easily by the couple by observing their annual salary along with the savings account balance and the

superannuation that they possess. The ability of borrowing for the couple is accurate in accordance to their

income as they can bring forth the down payment payment of $80,000 and the rest of the balance can be

taken as a loan as they have the ability to pay for the interest in a simpler manner.

The requirements of deposits of the required loan consists of the identity proof of the person who is taking

the loan, their proof of address, photo, salary slip and government witnessed guarantors, authenticity proof

of the property, collateral securities and and the bank statement of the person who is undertaking the loan.

The ability of repayment is on the basis of the amount of loan required is simple for the couple as they

have adequate bank balance along with the superannuation and their salary is quite good for the

repayment of the loan. It is observed that they have been married for more than 5 years and have been

working for over 12 years so it is estimated that as they are young they have the ability to work for a longer

period of time unless they are down with sickness or any accidents and therefore by looking at the tenure

of loan which has been 30 years, they can pay for their loan in an easy manner. It is even seen that the rate

of interest falls along with the duration of the loan and repayment and therefore the accrued interest along

with the amount of principal annually would be around $2460 per month, which is pretty moderate on

comparison to their monthly income.

The couple have the ability to meet their financial obligations easily as they have a steady income rate

along with the benefit of being young which provides them with the chance to raise their income in the

Page 12 of 43

1. Based on the information provided in the case study and using the tools available to you

(e.g. loan calculators, including those available on lenders’ websites), provide an assessment of

the clients’ borrowing ability and ability to service the loan they require.

Consider and comment on issues such as:

• borrowing ability in relation to the loan required

• deposit requirements for the loan required

• repayment ability based on the loan required

• likelihood that the clients will be able to meet their financial obligations

• do they require Lenders Mortgage Insurance (LMI), and if so, how much will it cost

• any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions. (750 words)

Student response to Task 3: Question 1

The borrowing capability of Malcolm and Susan cam ne understood easily by assessing their asset and

liabilities statement. It is known that the couple has been married for over 5 years and has being living in a

rented house. They are in the idea of purchasing their own house and therefore has been looking for

various options of loan. They wants to purchase a property that is situated in 43 Seaside Parade Coastville

that has a cost of $490,000 and the Gant name is Steven Allstone. It is seen that the price of the property is

$490,000 and the anticipated costs associated to the property is $20,000 and thus the total cost comes to

$510,000. The amount of loan they want to receive is $430,000 and they have the idea of making a down

payment of $80,000.

The asset consists of $92,000 in the savings account of capital bank which has a value of $1,600 in the

cheque account of capital bank, superannuation of value of $90,000 for the couple as a both. They have

two cars for each of the couple with a value of $34,000 and value of household comprising of $40,000 and

the liabilities consists of the personal loan of $3600 and an outstanding credit card amount of of $800 for

the couple. Malcolm is working in ACME Ltd as a team leader and has annual income of $55,000 and Susan

is an accountant in Phones r Us with an annual salary of $91,000. It has been observed that the total annual

salary of the couple as a whole is $146,000 and the loan interest of 5.575 that results to $2460 per month

and therefore the amount can be paid with ease by the couple. The down payment value of $80,000 can be

paid easily by the couple by observing their annual salary along with the savings account balance and the

superannuation that they possess. The ability of borrowing for the couple is accurate in accordance to their

income as they can bring forth the down payment payment of $80,000 and the rest of the balance can be

taken as a loan as they have the ability to pay for the interest in a simpler manner.

The requirements of deposits of the required loan consists of the identity proof of the person who is taking

the loan, their proof of address, photo, salary slip and government witnessed guarantors, authenticity proof

of the property, collateral securities and and the bank statement of the person who is undertaking the loan.

The ability of repayment is on the basis of the amount of loan required is simple for the couple as they

have adequate bank balance along with the superannuation and their salary is quite good for the

repayment of the loan. It is observed that they have been married for more than 5 years and have been

working for over 12 years so it is estimated that as they are young they have the ability to work for a longer

period of time unless they are down with sickness or any accidents and therefore by looking at the tenure

of loan which has been 30 years, they can pay for their loan in an easy manner. It is even seen that the rate

of interest falls along with the duration of the loan and repayment and therefore the accrued interest along

with the amount of principal annually would be around $2460 per month, which is pretty moderate on

comparison to their monthly income.

The couple have the ability to meet their financial obligations easily as they have a steady income rate

along with the benefit of being young which provides them with the chance to raise their income in the

Page 12 of 43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 43

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.