FNS40815 Certificate IV in Finance Assignment 1: Dowell Scenario

VerifiedAdded on 2020/04/07

|10

|2670

|33

Homework Assignment

AI Summary

This document presents a completed finance assignment based on a provided scenario involving a couple, the Dowells, seeking to refinance their existing mortgage and purchase an investment property. The assignment includes a completed fact find document, a product recommendation with justification, a list of supporting documents, a loan costing sheet, a loan servicing calculation (NSR), and a completed ANZ loan application form with accompanying documents. The scenario provides detailed information about the clients' financial situation, including income, assets, debts, and investment goals. The assignment requires the student to apply their knowledge of mortgage broking principles to assess the clients' needs, recommend a suitable loan product, and complete the necessary documentation for a loan application. The solution demonstrates the practical application of financial concepts and loan origination processes.

ASSI

© 2017 The National Finance V

To be completed by the

Trainee

You must include this page with your Assignment 1

submission

Alternatively you can retype the details as a front page to your

Assignment

Trainee name

Trainee Postal Address

Trainee Daytime Phone numbers

Trainee Email address

I state that this Assignment contains no material which has been written by another person.

I make this statement with the understanding that my assessment may be compromised if

found to be otherwise. Signed Date

Submissions can be mailed to NFI, P.O. Box 1354, Capalaba B.C. Qld 4157 OR

Email to assessments@financeinstitute.com.au (if emailing you must adhere to the emailing

size rules)

OFFICE USE ONLY BELOW

HERE

Date received by NFI Date received by Assessor

Name of Assessor

Date assessed

Competent

Not Yet Competent

Mark

Assessor’s Comments:

.................................................................................................

.............................................................................................................................

......

...........................................................................................................................

........

.............................................................................................................................

......

Further action required (if applicable)

© 2017 The National Finance V

To be completed by the

Trainee

You must include this page with your Assignment 1

submission

Alternatively you can retype the details as a front page to your

Assignment

Trainee name

Trainee Postal Address

Trainee Daytime Phone numbers

Trainee Email address

I state that this Assignment contains no material which has been written by another person.

I make this statement with the understanding that my assessment may be compromised if

found to be otherwise. Signed Date

Submissions can be mailed to NFI, P.O. Box 1354, Capalaba B.C. Qld 4157 OR

Email to assessments@financeinstitute.com.au (if emailing you must adhere to the emailing

size rules)

OFFICE USE ONLY BELOW

HERE

Date received by NFI Date received by Assessor

Name of Assessor

Date assessed

Competent

Not Yet Competent

Mark

Assessor’s Comments:

.................................................................................................

.............................................................................................................................

......

...........................................................................................................................

........

.............................................................................................................................

......

Further action required (if applicable)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ASSI

© 2017 The National Finance V

T

ask

Using the information contained in the Scenario below, please complete the following 6

tasks. You must complete each task for your submission to be assessed. Omission of any of

these 6 tasks will be regarded as ‘Working Towards Competency’ and you will then be

required to resubmit in full.

1. Complete the Fact Find document on these clients – using the form in

Appendix 14.

We have not included all supplementary information on these clients so you

will need to

create your own “improvised” answers for inclusion in the Fact Find

document.

Trainees who already have access to their own version of a Fact Find template

may use

their own form as an alternative to that provided in Appendix 14.

2. Recommend a product for the clients and explain your reasons for

recommendation

3. List the supporting documents that would be needed to support the loan

4. Complete loan costing sheet *

5. Complete a loan servicing calculation (NSR) *

6. Complete a loan application form (an ANZ loan application form has been

provided for you, which you must use) and complete all of the

accompanying documents as provided for you. Your answer to this

Activity should be prepared as if you were

submitting a real full loan application to the

lender.

Please note: If there is information required on the ANZ application form that is not

supplied, please improvise. The application should be completed as neatly as

possible to ensure ease of review. It is to be submitted to NFI as if NFI is the lender

and you were an accredited broker (but you do not need to make up “dummy”

supporting documents eg. rates notice, etc.). If you do not submit in a professional

manner, your assessment will not be marked.

* The fees and charges required in order to complete this assignment correctly (ie.

Estimate of

Costs worksheet) can be found in Unit 7 (use your own state-specific section at the

back of Unit

7) and the instructions for how to complete the NSR form are in Unit 8. A Lenders

Mortgage

Insurance Chart (for your LMI calculation if applicable) is found in Unit 7. Trainees

should ensure they source their fees and charges from these units. There are also

sample documents to follow in Units 7 and 8.

S

cenario

Clients: Mary Jane

Dowell

DL No.: 4167384

DOB: 06/06/65 Australian Passport No.: L93214773

John James Dowell

DL No.: 4378691

© 2017 The National Finance V

T

ask

Using the information contained in the Scenario below, please complete the following 6

tasks. You must complete each task for your submission to be assessed. Omission of any of

these 6 tasks will be regarded as ‘Working Towards Competency’ and you will then be

required to resubmit in full.

1. Complete the Fact Find document on these clients – using the form in

Appendix 14.

We have not included all supplementary information on these clients so you

will need to

create your own “improvised” answers for inclusion in the Fact Find

document.

Trainees who already have access to their own version of a Fact Find template

may use

their own form as an alternative to that provided in Appendix 14.

2. Recommend a product for the clients and explain your reasons for

recommendation

3. List the supporting documents that would be needed to support the loan

4. Complete loan costing sheet *

5. Complete a loan servicing calculation (NSR) *

6. Complete a loan application form (an ANZ loan application form has been

provided for you, which you must use) and complete all of the

accompanying documents as provided for you. Your answer to this

Activity should be prepared as if you were

submitting a real full loan application to the

lender.

Please note: If there is information required on the ANZ application form that is not

supplied, please improvise. The application should be completed as neatly as

possible to ensure ease of review. It is to be submitted to NFI as if NFI is the lender

and you were an accredited broker (but you do not need to make up “dummy”

supporting documents eg. rates notice, etc.). If you do not submit in a professional

manner, your assessment will not be marked.

* The fees and charges required in order to complete this assignment correctly (ie.

Estimate of

Costs worksheet) can be found in Unit 7 (use your own state-specific section at the

back of Unit

7) and the instructions for how to complete the NSR form are in Unit 8. A Lenders

Mortgage

Insurance Chart (for your LMI calculation if applicable) is found in Unit 7. Trainees

should ensure they source their fees and charges from these units. There are also

sample documents to follow in Units 7 and 8.

S

cenario

Clients: Mary Jane

Dowell

DL No.: 4167384

DOB: 06/06/65 Australian Passport No.: L93214773

John James Dowell

DL No.: 4378691

ASSI

© 2017 The National Finance V

DOB: 03/05/67 Australian Passport No.: L8078972

Current Address: 46 Collins Street, North Ryde

NSW 2113

Time there, 2.6 years

Phone 0411 123 456

Previous Address: 37 Maple Street, Gladesville

NSW 2111

Time there, 4 years.

Children: 2 children aged 7 and 9 Scenario Continued overleaf

….

© 2017 The National Finance V

DOB: 03/05/67 Australian Passport No.: L8078972

Current Address: 46 Collins Street, North Ryde

NSW 2113

Time there, 2.6 years

Phone 0411 123 456

Previous Address: 37 Maple Street, Gladesville

NSW 2111

Time there, 4 years.

Children: 2 children aged 7 and 9 Scenario Continued overleaf

….

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSIGNMENT 1

© 2017 The National Finance V

Existing Property: Own Home valued at

$995,000

Current outstanding loan balance $180,000

(with CBA) Loan Repayments $1,080 per month

Cash: The clients have $12,000 cash in the

bank. Credit Cards: CBA Visa - $5,000 limit

(balance $2,000)

Westpac MasterCard - $5,000 limit (balance $1,500)

Mr Dowell works at the Parramatta Council as the tourism manager and earns $115,000

p.a. He has worked there for 8 years.

Mrs Dowell is a primary school teacher at Ryde Primary School and earns $64,000 p.a. She

has worked there for the past 3 years after having several years of home duties.

The Dowells own two cars – a 2014 Ford Falcon worth $18,000 unencumbered and a 2015

Land Cruiser worth $30,000 subject to finance of $20,000 ($450 per month).

The Dowells have a 36 month Interest Free loan from GE for a sound/movie system for

$3,000. The minimum monthly payment is 5%.

You interviewed Mr and Mrs Dowell at your office after some initial telephone conversations

previously. They both spoke good English as they are permanent Australians for 20 years

and they expressed their excitement at buying their second property. They are aware they

will need to visit the new lender branch to complete a Customer Identification Procedure

prior to finance approval from the lender. They have not yet enquired into an exact payout

figure from CBA.

The clients wish to refinance their current loan and purchase an

investment property.

The investment property is an established 2 bedroom unit in a residential block of 4 at 45

(Lot 4) Jones

Rd, North Ryde and is valued at

$685,000.

Rental Income of $650 per week is expected and the body corporate expense will be just

$35 per week. They have made an offer on the unit at the asking price, have put down a

$1000 cash deposit, and the offer has been accepted with settlement in 60 days.

Title particulars: Lot 4, Folio 3871, Vol.

1821.

The solicitors they will be using are Henderson & Partners, ph

1234 567 890

Scenario Continued overleaf ….

© 2017 The National Finance V

Existing Property: Own Home valued at

$995,000

Current outstanding loan balance $180,000

(with CBA) Loan Repayments $1,080 per month

Cash: The clients have $12,000 cash in the

bank. Credit Cards: CBA Visa - $5,000 limit

(balance $2,000)

Westpac MasterCard - $5,000 limit (balance $1,500)

Mr Dowell works at the Parramatta Council as the tourism manager and earns $115,000

p.a. He has worked there for 8 years.

Mrs Dowell is a primary school teacher at Ryde Primary School and earns $64,000 p.a. She

has worked there for the past 3 years after having several years of home duties.

The Dowells own two cars – a 2014 Ford Falcon worth $18,000 unencumbered and a 2015

Land Cruiser worth $30,000 subject to finance of $20,000 ($450 per month).

The Dowells have a 36 month Interest Free loan from GE for a sound/movie system for

$3,000. The minimum monthly payment is 5%.

You interviewed Mr and Mrs Dowell at your office after some initial telephone conversations

previously. They both spoke good English as they are permanent Australians for 20 years

and they expressed their excitement at buying their second property. They are aware they

will need to visit the new lender branch to complete a Customer Identification Procedure

prior to finance approval from the lender. They have not yet enquired into an exact payout

figure from CBA.

The clients wish to refinance their current loan and purchase an

investment property.

The investment property is an established 2 bedroom unit in a residential block of 4 at 45

(Lot 4) Jones

Rd, North Ryde and is valued at

$685,000.

Rental Income of $650 per week is expected and the body corporate expense will be just

$35 per week. They have made an offer on the unit at the asking price, have put down a

$1000 cash deposit, and the offer has been accepted with settlement in 60 days.

Title particulars: Lot 4, Folio 3871, Vol.

1821.

The solicitors they will be using are Henderson & Partners, ph

1234 567 890

Scenario Continued overleaf ….

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ASSIGNMENT 1

© 2017 The National Finance V

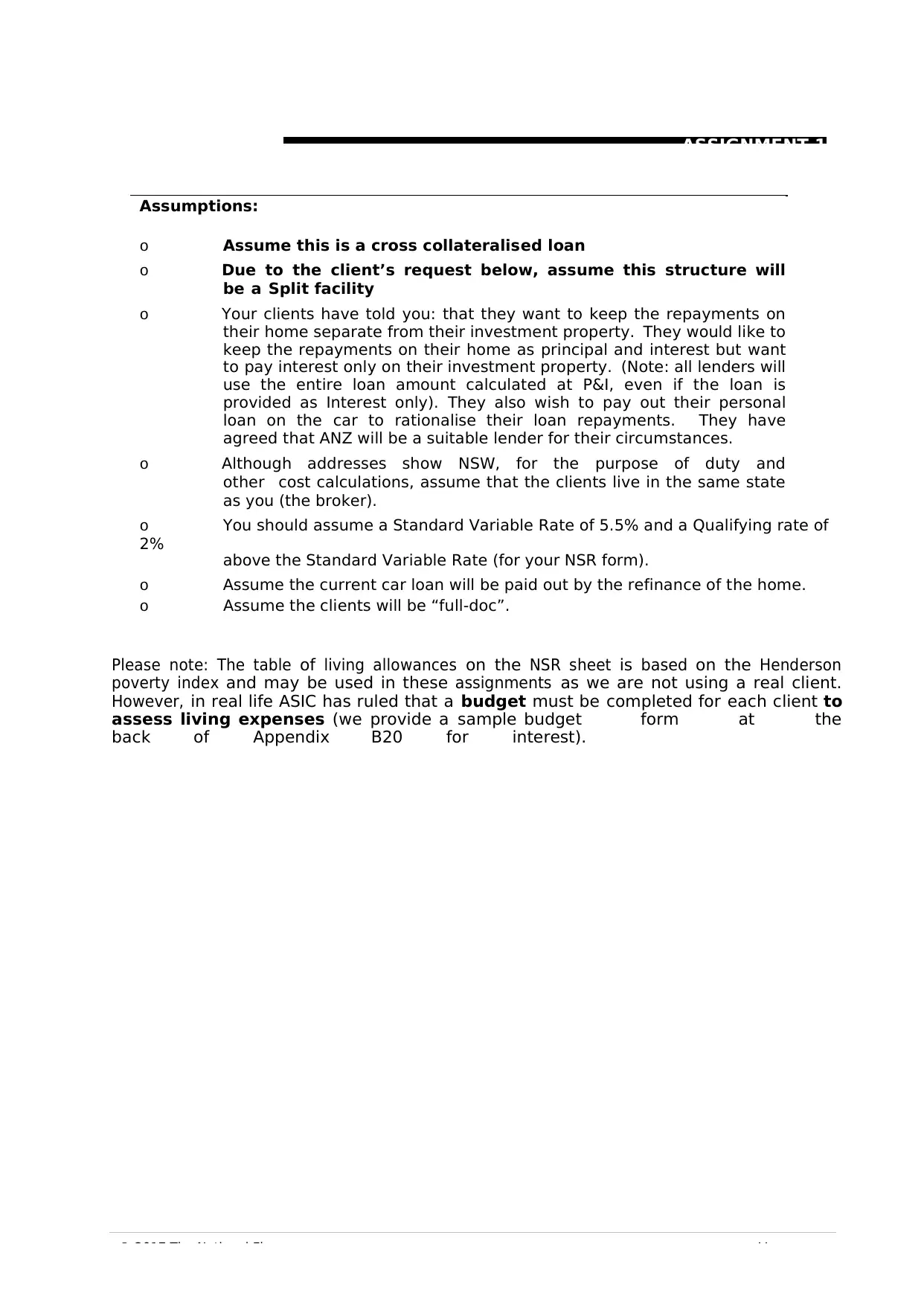

Assumptions:

o Assume this is a cross collateralised loan

o Due to the client’s request below, assume this structure will

be a Split facility

o Your clients have told you: that they want to keep the repayments on

their home separate from their investment property. They would like to

keep the repayments on their home as principal and interest but want

to pay interest only on their investment property. (Note: all lenders will

use the entire loan amount calculated at P&I, even if the loan is

provided as Interest only). They also wish to pay out their personal

loan on the car to rationalise their loan repayments. They have

agreed that ANZ will be a suitable lender for their circumstances.

o Although addresses show NSW, for the purpose of duty and

other cost calculations, assume that the clients live in the same state

as you (the broker).

o You should assume a Standard Variable Rate of 5.5% and a Qualifying rate of

2%

above the Standard Variable Rate (for your NSR form).

o Assume the current car loan will be paid out by the refinance of the home.

o Assume the clients will be “full-doc”.

Please note: The table of living allowances on the NSR sheet is based on the Henderson

poverty index and may be used in these assignments as we are not using a real client.

However, in real life ASIC has ruled that a budget must be completed for each client to

assess living expenses (we provide a sample budget form at the

back of Appendix B20 for interest).

© 2017 The National Finance V

Assumptions:

o Assume this is a cross collateralised loan

o Due to the client’s request below, assume this structure will

be a Split facility

o Your clients have told you: that they want to keep the repayments on

their home separate from their investment property. They would like to

keep the repayments on their home as principal and interest but want

to pay interest only on their investment property. (Note: all lenders will

use the entire loan amount calculated at P&I, even if the loan is

provided as Interest only). They also wish to pay out their personal

loan on the car to rationalise their loan repayments. They have

agreed that ANZ will be a suitable lender for their circumstances.

o Although addresses show NSW, for the purpose of duty and

other cost calculations, assume that the clients live in the same state

as you (the broker).

o You should assume a Standard Variable Rate of 5.5% and a Qualifying rate of

2%

above the Standard Variable Rate (for your NSR form).

o Assume the current car loan will be paid out by the refinance of the home.

o Assume the clients will be “full-doc”.

Please note: The table of living allowances on the NSR sheet is based on the Henderson

poverty index and may be used in these assignments as we are not using a real client.

However, in real life ASIC has ruled that a budget must be completed for each client to

assess living expenses (we provide a sample budget form at the

back of Appendix B20 for interest).

© 2017 The National Finance V

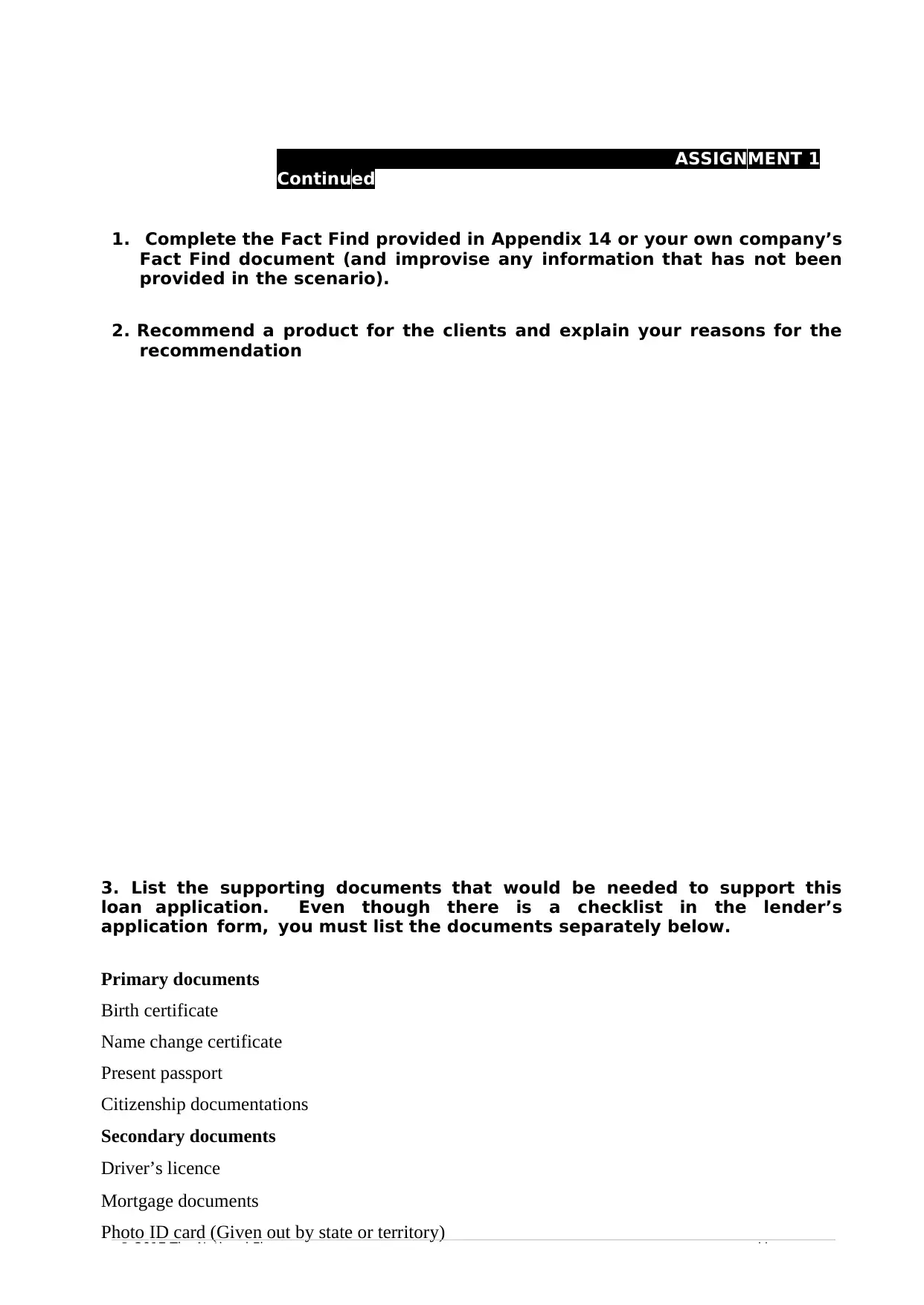

ASSIGNMENT 1

Continued

1. Complete the Fact Find provided in Appendix 14 or your own company’s

Fact Find document (and improvise any information that has not been

provided in the scenario).

2. Recommend a product for the clients and explain your reasons for the

recommendation

3. List the supporting documents that would be needed to support this

loan application. Even though there is a checklist in the lender’s

application form, you must list the documents separately below.

Primary documents

Birth certificate

Name change certificate

Present passport

Citizenship documentations

Secondary documents

Driver’s licence

Mortgage documents

Photo ID card (Given out by state or territory)

ASSIGNMENT 1

Continued

1. Complete the Fact Find provided in Appendix 14 or your own company’s

Fact Find document (and improvise any information that has not been

provided in the scenario).

2. Recommend a product for the clients and explain your reasons for the

recommendation

3. List the supporting documents that would be needed to support this

loan application. Even though there is a checklist in the lender’s

application form, you must list the documents separately below.

Primary documents

Birth certificate

Name change certificate

Present passport

Citizenship documentations

Secondary documents

Driver’s licence

Mortgage documents

Photo ID card (Given out by state or territory)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

© 2017 The National Finance V

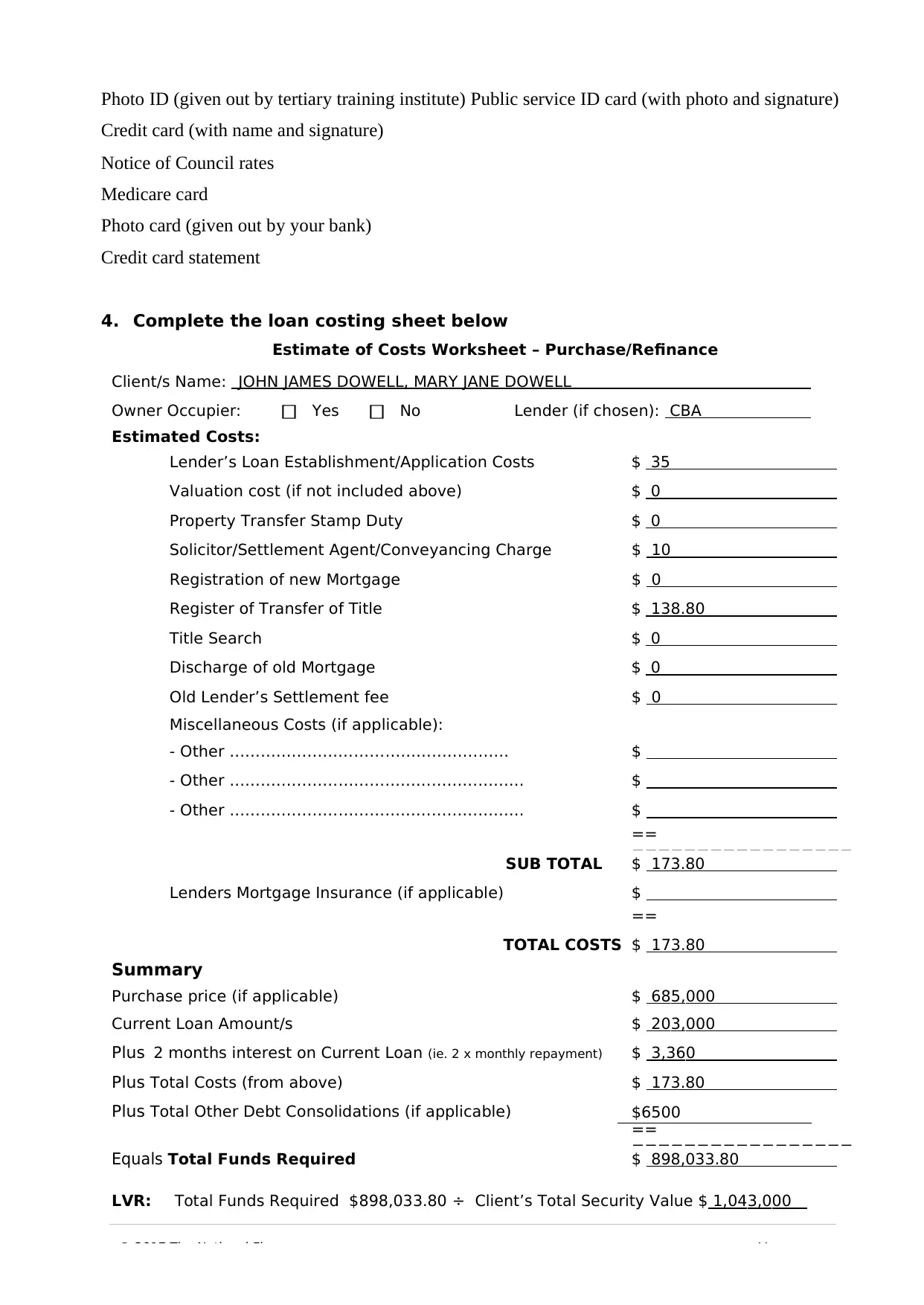

Photo ID (given out by tertiary training institute) Public service ID card (with photo and signature)

Credit card (with name and signature)

Notice of Council rates

Medicare card

Photo card (given out by your bank)

Credit card statement

4. Complete the loan costing sheet below

Estimate of Costs Worksheet – Purchase/Refinance

Client/s Name: JOHN JAMES DOWELL, MARY JANE DOWELL

Owner Occupier: Yes No Lender (if chosen): CBA

Estimated Costs:

Lender’s Loan Establishment/Application Costs $ 35

Valuation cost (if not included above) $ 0

Property Transfer Stamp Duty $ 0

Solicitor/Settlement Agent/Conveyancing Charge $ 10

Registration of new Mortgage $ 0

Register of Transfer of Title $ 138.80

Title Search $ 0

Discharge of old Mortgage $ 0

Old Lender’s Settlement fee $ 0

Miscellaneous Costs (if applicable):

- Other ……………………………………………… $

- Other ………………………………………………… $

- Other ………………………………………………… $

==

=================

SUB TOTAL $ 173.80

Lenders Mortgage Insurance (if applicable) $

==

=================

TOTAL COSTS $ 173.80

Summary

Purchase price (if applicable) $ 685,000

Current Loan Amount/s $ 203,000

Plus 2 months interest on Current Loan (ie. 2 x monthly repayment) $ 3,360

Plus Total Costs (from above) $ 173.80

Plus Total Other Debt Consolidations (if applicable) $6500

==

=================

Equals Total Funds Required $ 898,033.80

LVR: Total Funds Required $898,033.80 ÷ Client’s Total Security Value $ 1,043,000

Photo ID (given out by tertiary training institute) Public service ID card (with photo and signature)

Credit card (with name and signature)

Notice of Council rates

Medicare card

Photo card (given out by your bank)

Credit card statement

4. Complete the loan costing sheet below

Estimate of Costs Worksheet – Purchase/Refinance

Client/s Name: JOHN JAMES DOWELL, MARY JANE DOWELL

Owner Occupier: Yes No Lender (if chosen): CBA

Estimated Costs:

Lender’s Loan Establishment/Application Costs $ 35

Valuation cost (if not included above) $ 0

Property Transfer Stamp Duty $ 0

Solicitor/Settlement Agent/Conveyancing Charge $ 10

Registration of new Mortgage $ 0

Register of Transfer of Title $ 138.80

Title Search $ 0

Discharge of old Mortgage $ 0

Old Lender’s Settlement fee $ 0

Miscellaneous Costs (if applicable):

- Other ……………………………………………… $

- Other ………………………………………………… $

- Other ………………………………………………… $

==

=================

SUB TOTAL $ 173.80

Lenders Mortgage Insurance (if applicable) $

==

=================

TOTAL COSTS $ 173.80

Summary

Purchase price (if applicable) $ 685,000

Current Loan Amount/s $ 203,000

Plus 2 months interest on Current Loan (ie. 2 x monthly repayment) $ 3,360

Plus Total Costs (from above) $ 173.80

Plus Total Other Debt Consolidations (if applicable) $6500

==

=================

Equals Total Funds Required $ 898,033.80

LVR: Total Funds Required $898,033.80 ÷ Client’s Total Security Value $ 1,043,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

© 2017 The National Finance V

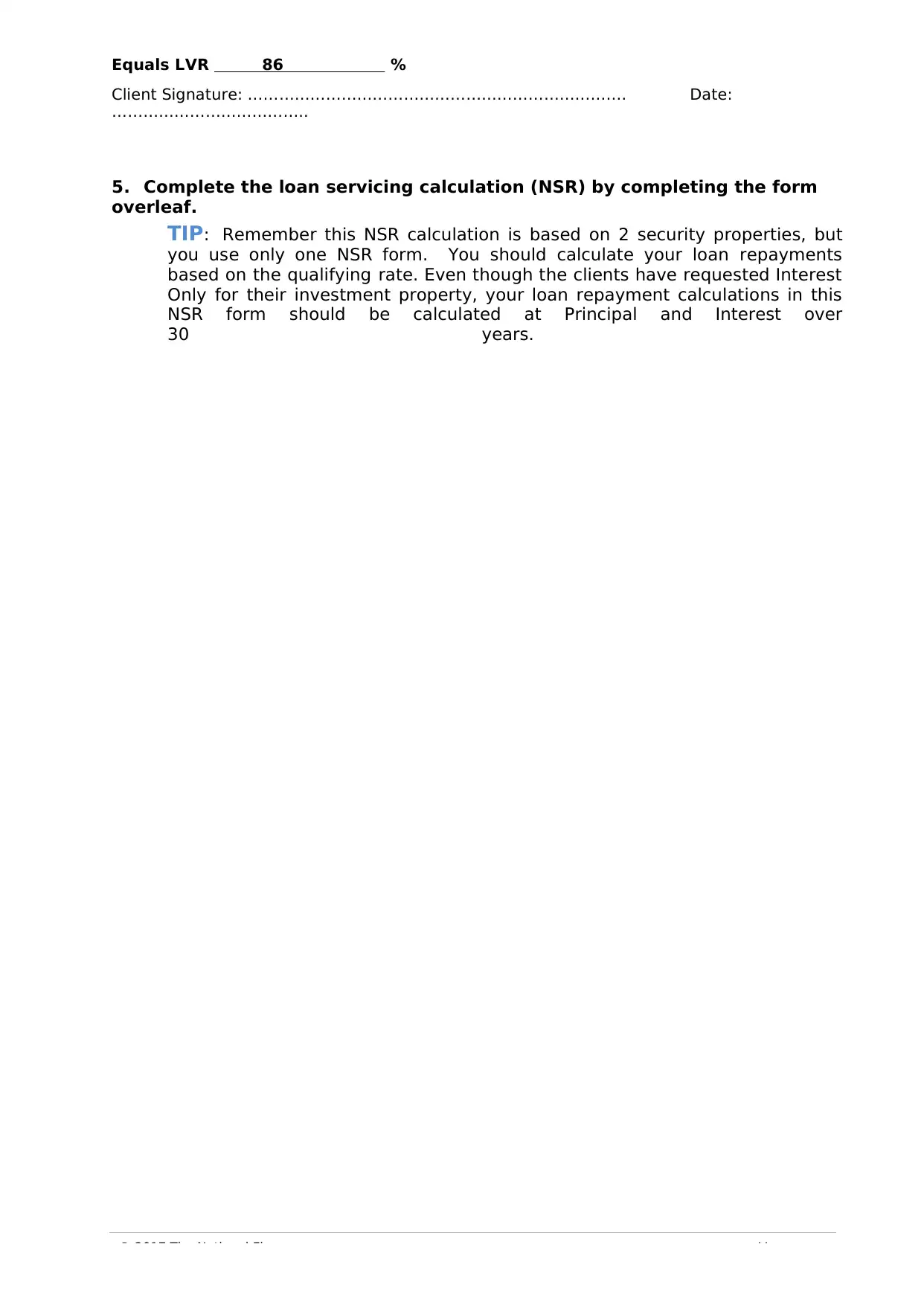

Equals LVR 86 %

Client Signature: ………………………………………………………………. Date:

………………………………..

5. Complete the loan servicing calculation (NSR) by completing the form

overleaf.

TIP: Remember this NSR calculation is based on 2 security properties, but

you use only one NSR form. You should calculate your loan repayments

based on the qualifying rate. Even though the clients have requested Interest

Only for their investment property, your loan repayment calculations in this

NSR form should be calculated at Principal and Interest over

30 years.

Equals LVR 86 %

Client Signature: ………………………………………………………………. Date:

………………………………..

5. Complete the loan servicing calculation (NSR) by completing the form

overleaf.

TIP: Remember this NSR calculation is based on 2 security properties, but

you use only one NSR form. You should calculate your loan repayments

based on the qualifying rate. Even though the clients have requested Interest

Only for their investment property, your loan repayment calculations in this

NSR form should be calculated at Principal and Interest over

30 years.

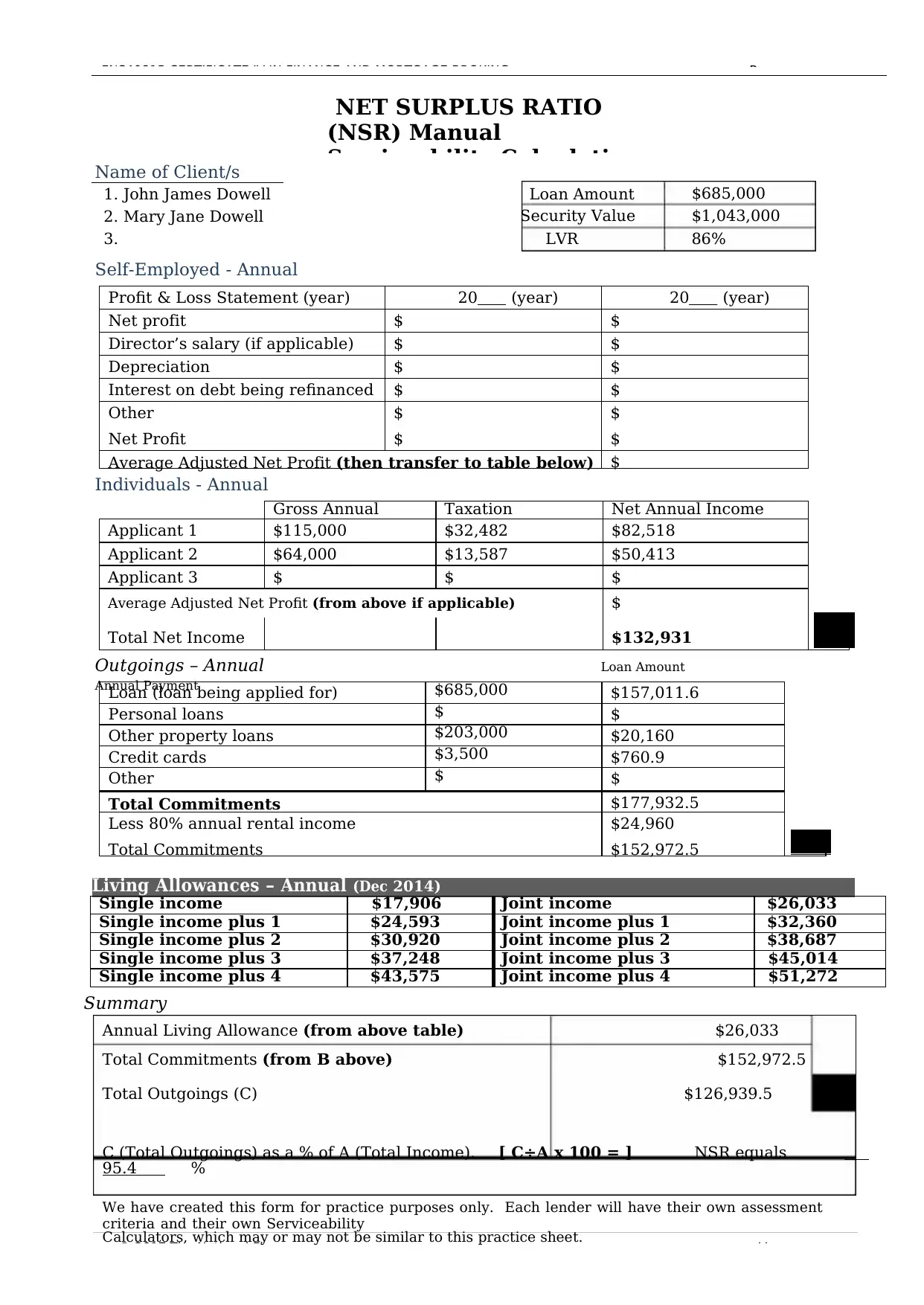

PageFNS40815 CERTIFICATE IV IN FINANCE AND MORTGAGE BROKING –

Profit & Loss Statement (year) 20 (year) 20 (year)

Net profit $ $

Director’s salary (if applicable) $ $

Depreciation $ $

Interest on debt being refinanced $ $

Other

Net Profit

$

$

$

$

Average Adjusted Net Profit (then transfer to table below) $

Gross Annual

Income

Taxation Net Annual Income

Applicant 1 $115,000 $32,482 $82,518

Applicant 2 $64,000 $13,587 $50,413

Applicant 3 $ $ $

Average Adjusted Net Profit (from above if applicable) $

$132,931Total Net Income A

Loan (loan being applied for) $685,000 $157,011.6

Personal loans $ $

Other property loans $203,000 $20,160

Credit cards $3,500 $760.9

Other $ $

Total Commitments $177,932.5

Less 80% annual rental income

Total Commitments

$24,960

$152,972.5 B

© 2017 The National Finance V

NET SURPLUS RATIO

(NSR) Manual

Serviceability Calculation

Name of Client/s

1. John James Dowell Loan Amount $685,000

2. Mary Jane Dowell Security Value $1,043,000

3. LVR 86%

Self-Employed - Annual

Individuals - Annual

Outgoings – Annual Loan Amount

Annual Payment

Living Allowances – Annual (Dec 2014)

Single income $17,906 Joint income $26,033

Single income plus 1 $24,593 Joint income plus 1 $32,360

Single income plus 2 $30,920 Joint income plus 2 $38,687

Single income plus 3 $37,248 Joint income plus 3 $45,014

Single income plus 4 $43,575 Joint income plus 4 $51,272

Summary

Annual Living Allowance (from above table) $26,033

Total Commitments (from B above) $152,972.5

Total Outgoings (C) $126,939.5

C

C (Total Outgoings) as a % of A (Total Income). [ C÷A x 100 = ] NSR equals

95.4 %

We have created this form for practice purposes only. Each lender will have their own assessment

criteria and their own Serviceability

Calculators, which may or may not be similar to this practice sheet.

Profit & Loss Statement (year) 20 (year) 20 (year)

Net profit $ $

Director’s salary (if applicable) $ $

Depreciation $ $

Interest on debt being refinanced $ $

Other

Net Profit

$

$

$

$

Average Adjusted Net Profit (then transfer to table below) $

Gross Annual

Income

Taxation Net Annual Income

Applicant 1 $115,000 $32,482 $82,518

Applicant 2 $64,000 $13,587 $50,413

Applicant 3 $ $ $

Average Adjusted Net Profit (from above if applicable) $

$132,931Total Net Income A

Loan (loan being applied for) $685,000 $157,011.6

Personal loans $ $

Other property loans $203,000 $20,160

Credit cards $3,500 $760.9

Other $ $

Total Commitments $177,932.5

Less 80% annual rental income

Total Commitments

$24,960

$152,972.5 B

© 2017 The National Finance V

NET SURPLUS RATIO

(NSR) Manual

Serviceability Calculation

Name of Client/s

1. John James Dowell Loan Amount $685,000

2. Mary Jane Dowell Security Value $1,043,000

3. LVR 86%

Self-Employed - Annual

Individuals - Annual

Outgoings – Annual Loan Amount

Annual Payment

Living Allowances – Annual (Dec 2014)

Single income $17,906 Joint income $26,033

Single income plus 1 $24,593 Joint income plus 1 $32,360

Single income plus 2 $30,920 Joint income plus 2 $38,687

Single income plus 3 $37,248 Joint income plus 3 $45,014

Single income plus 4 $43,575 Joint income plus 4 $51,272

Summary

Annual Living Allowance (from above table) $26,033

Total Commitments (from B above) $152,972.5

Total Outgoings (C) $126,939.5

C

C (Total Outgoings) as a % of A (Total Income). [ C÷A x 100 = ] NSR equals

95.4 %

We have created this form for practice purposes only. Each lender will have their own assessment

criteria and their own Serviceability

Calculators, which may or may not be similar to this practice sheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PageFNS40815 CERTIFICATE IV IN FINANCE AND MORTGAGE BROKING –

© 2017 The National Finance V

6. Complete the lender’s application form (a blank ANZ loan application form

has been provided for you) and the other documents as provided for you.

Your answer to this Activity should be prepared as if you were submitting a

real full loan application to the lender. Remember you must treat this as a

cross-collateralised loan structure.

Please note: If there is information required on the application that is not

supplied please improvise. The application should be completed as neatly as

possible to ensure ease of review. Tax charts, an LMI table and sundry forms can

be found in your course content. You do not need to create any “dummy”

supporting documents (eg. documents that your client would typically provide to

you in a real submission, eg. rates notices), just ensure you list them where

required.

For this question you must include the following 5 completed forms (all

have been provided for you):

- Lending Checklist

- Summary of product choice

- Privacy Act, Disclosure and Consent

- Loan Application Cover Sheet

- ANZ Application form

TIPS:

Use the LMI table provided in Unit 7 to calculate your LMI and don’t forget

LMI stamp

duty.

Page 6 of the ANZ form is where you show your split facility structure

On page 9 of the ANZ form Assets and Liabilities should be shown as

current / pre-

settlement but Income and Expenses are to be shown as proposed / post

settlement

© 2017 The National Finance V

6. Complete the lender’s application form (a blank ANZ loan application form

has been provided for you) and the other documents as provided for you.

Your answer to this Activity should be prepared as if you were submitting a

real full loan application to the lender. Remember you must treat this as a

cross-collateralised loan structure.

Please note: If there is information required on the application that is not

supplied please improvise. The application should be completed as neatly as

possible to ensure ease of review. Tax charts, an LMI table and sundry forms can

be found in your course content. You do not need to create any “dummy”

supporting documents (eg. documents that your client would typically provide to

you in a real submission, eg. rates notices), just ensure you list them where

required.

For this question you must include the following 5 completed forms (all

have been provided for you):

- Lending Checklist

- Summary of product choice

- Privacy Act, Disclosure and Consent

- Loan Application Cover Sheet

- ANZ Application form

TIPS:

Use the LMI table provided in Unit 7 to calculate your LMI and don’t forget

LMI stamp

duty.

Page 6 of the ANZ form is where you show your split facility structure

On page 9 of the ANZ form Assets and Liabilities should be shown as

current / pre-

settlement but Income and Expenses are to be shown as proposed / post

settlement

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.