Financial Analysis: CFFA, Perpetuity Valuation & PE Ratio Report

VerifiedAdded on 2022/11/14

|8

|983

|66

Report

AI Summary

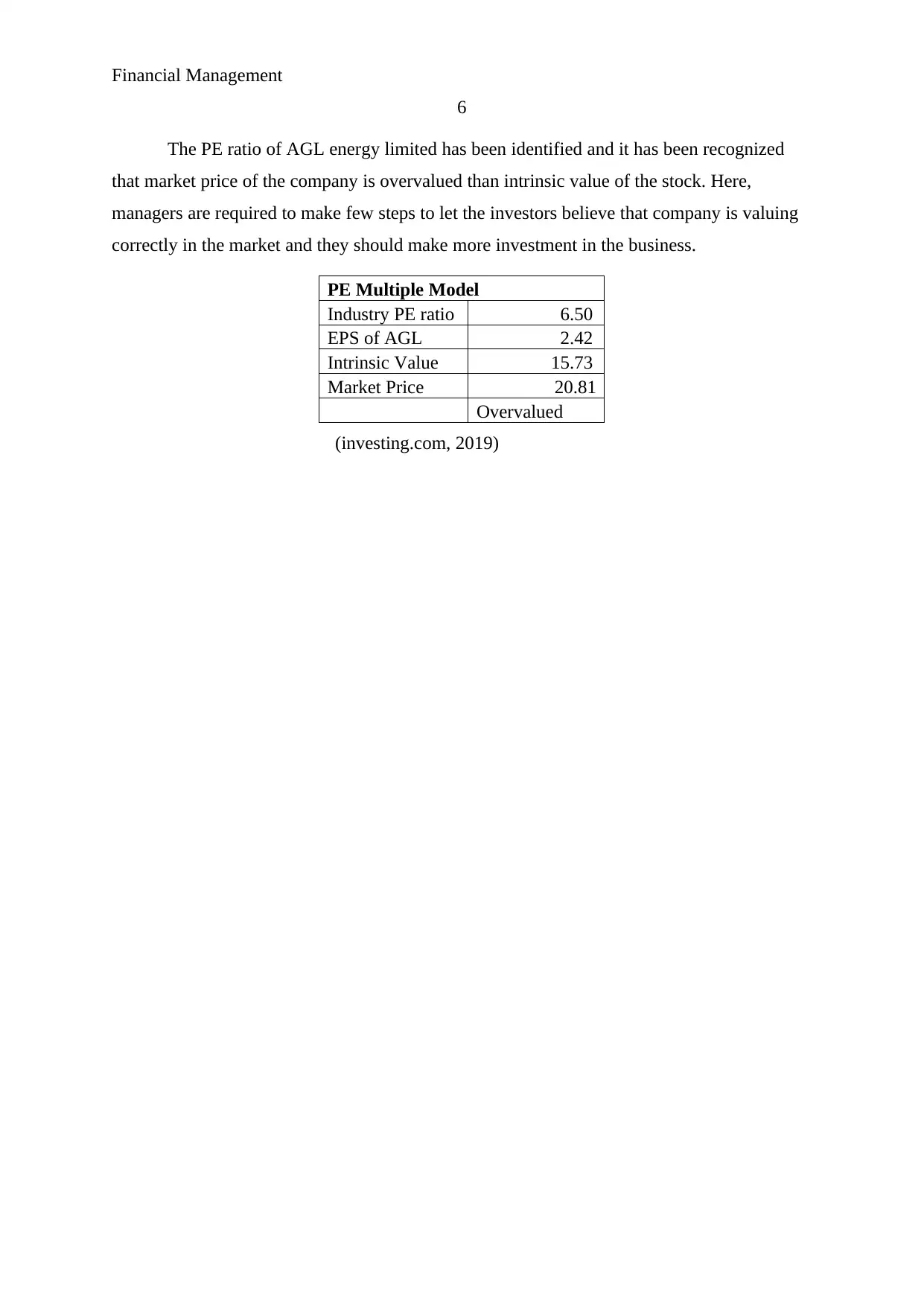

This report provides a detailed analysis of financial management concepts, focusing on Cash Flow From Assets (CFFA), perpetuity valuation, and Price-to-Earnings (PE) ratio. It includes the calculation of CFFA for XYZ Limited using balance sheet and income statement data, followed by an explanation of present value of perpetuity with an example. The report also discusses the significance of PE ratio in determining a company's worth, particularly in the context of AGL Energy Limited, where the market price is compared to the intrinsic value, alongside recommendations for managers to address overvaluation. Desklib offers a variety of study resources, including past papers and solved assignments, to support students in mastering complex financial topics.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.