Tax Law 30 June 2019 Seminar 6: Capital Gains Tax (CGT) Analysis

VerifiedAdded on 2022/09/11

|11

|2039

|13

Homework Assignment

AI Summary

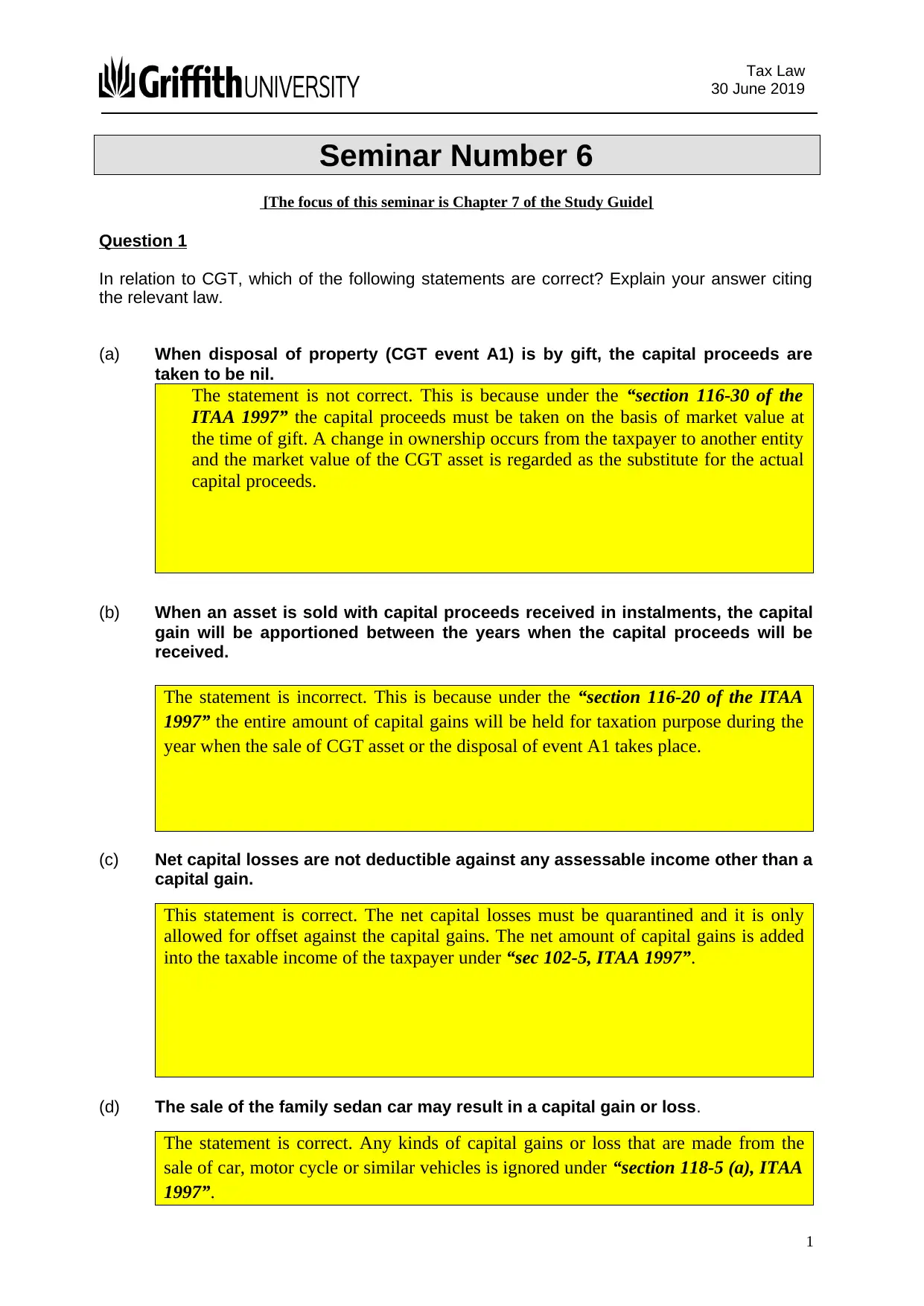

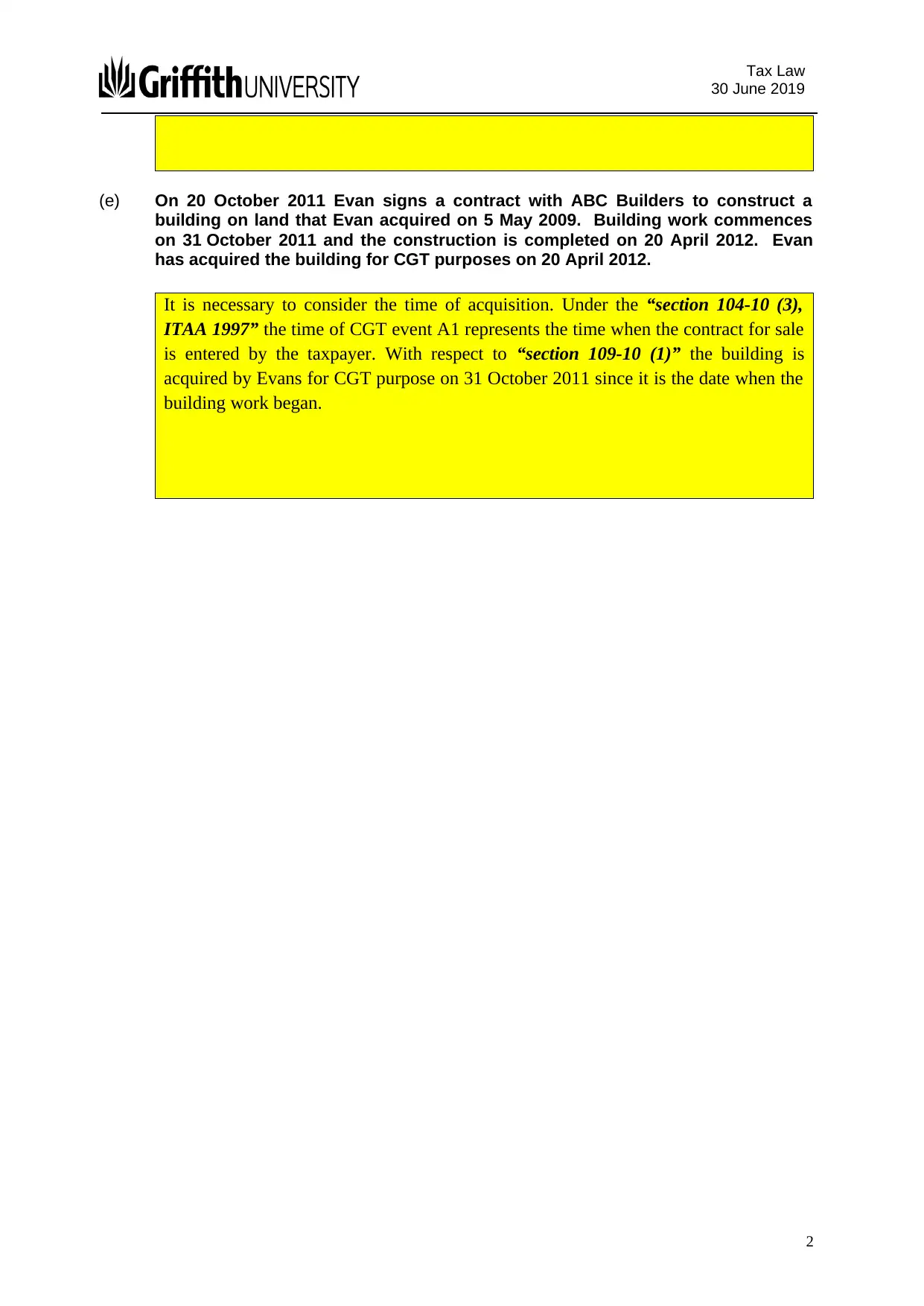

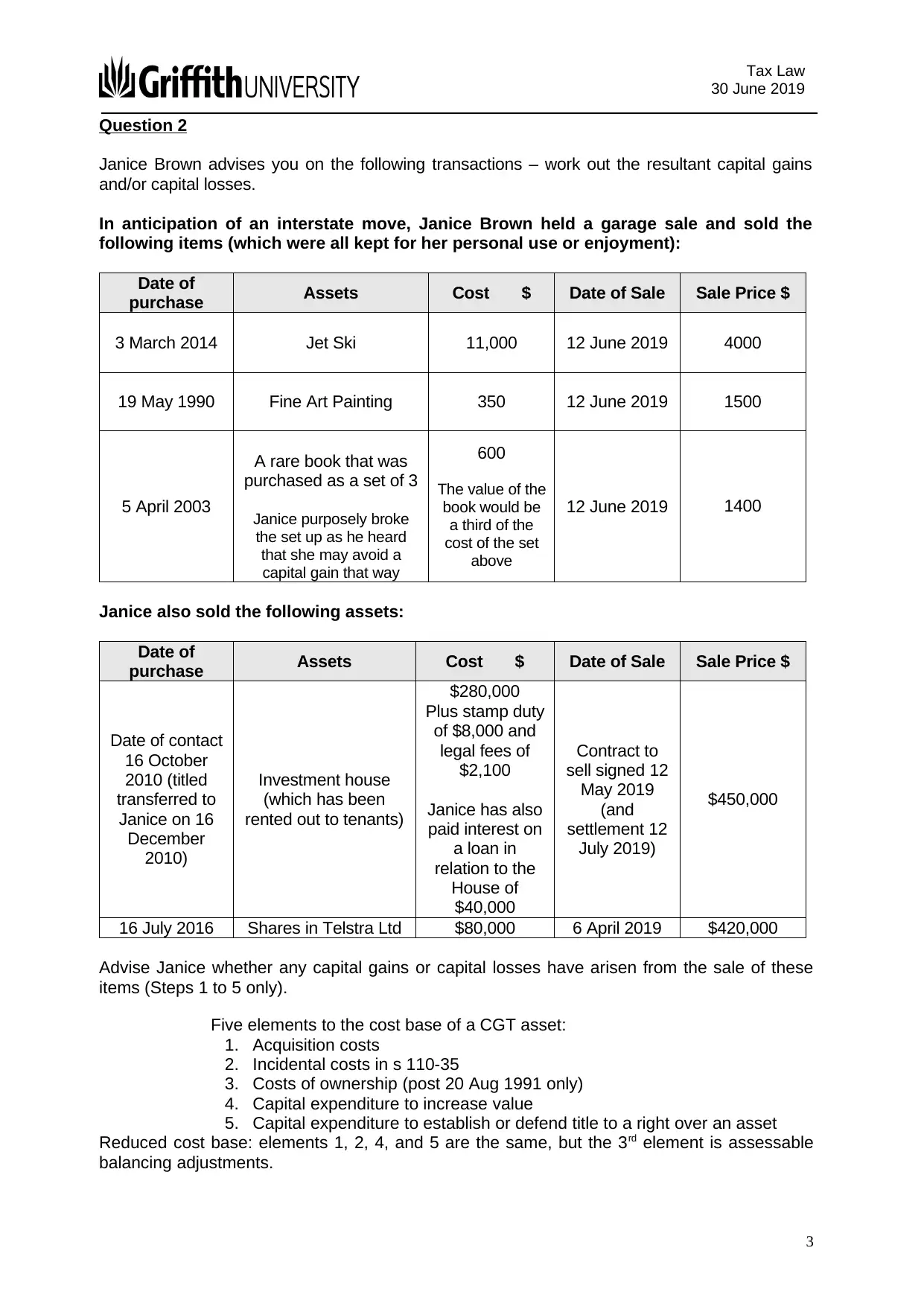

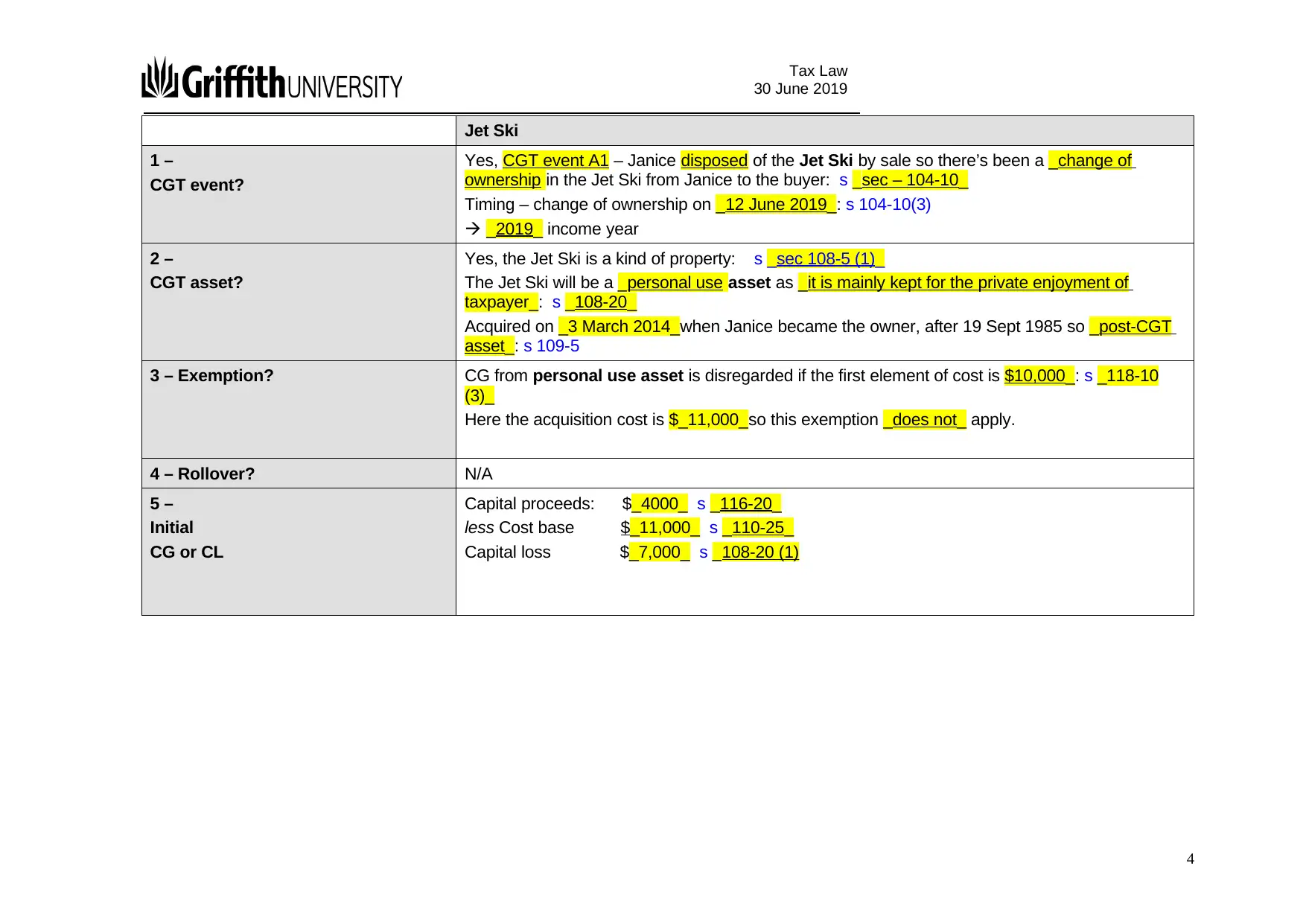

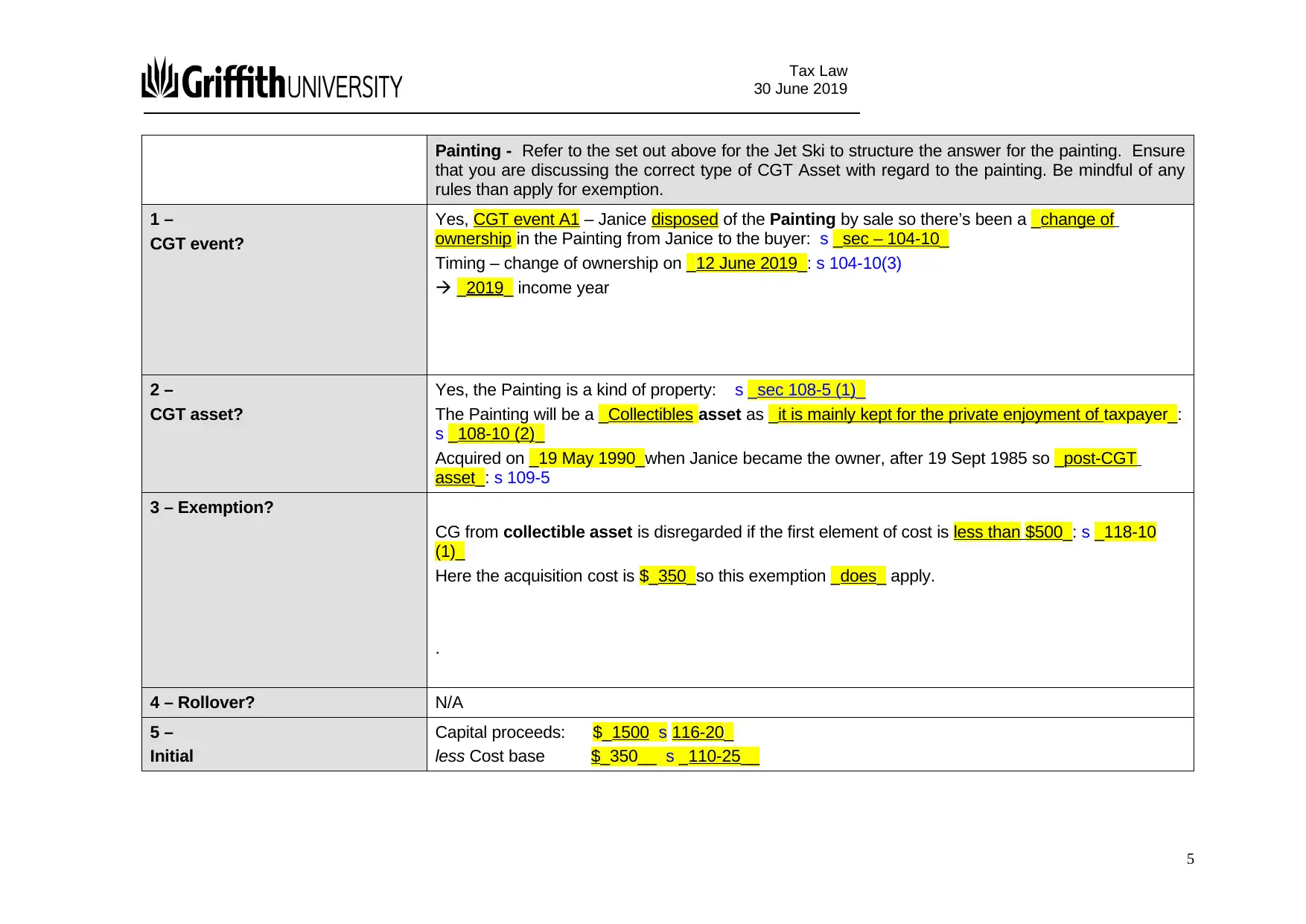

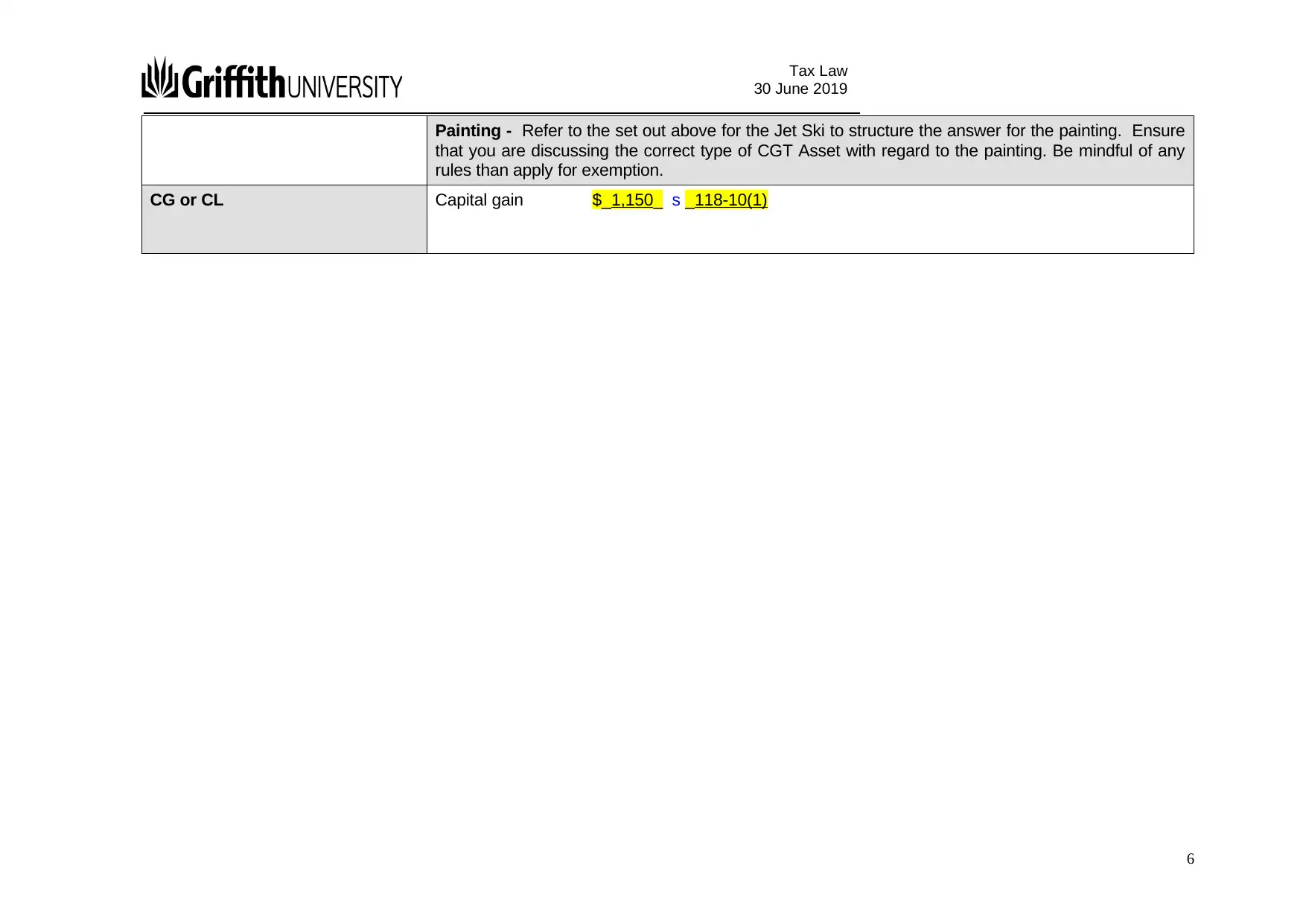

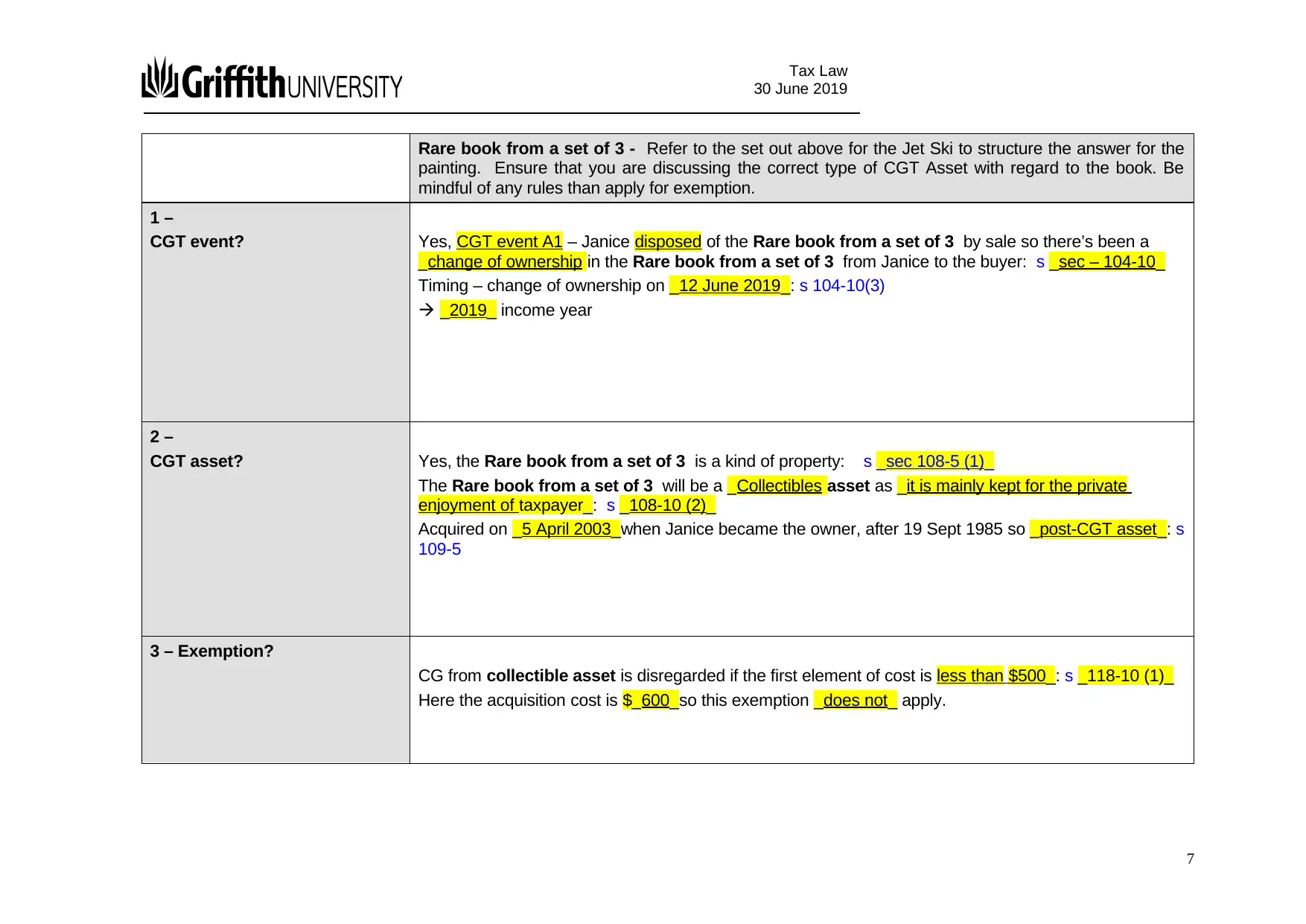

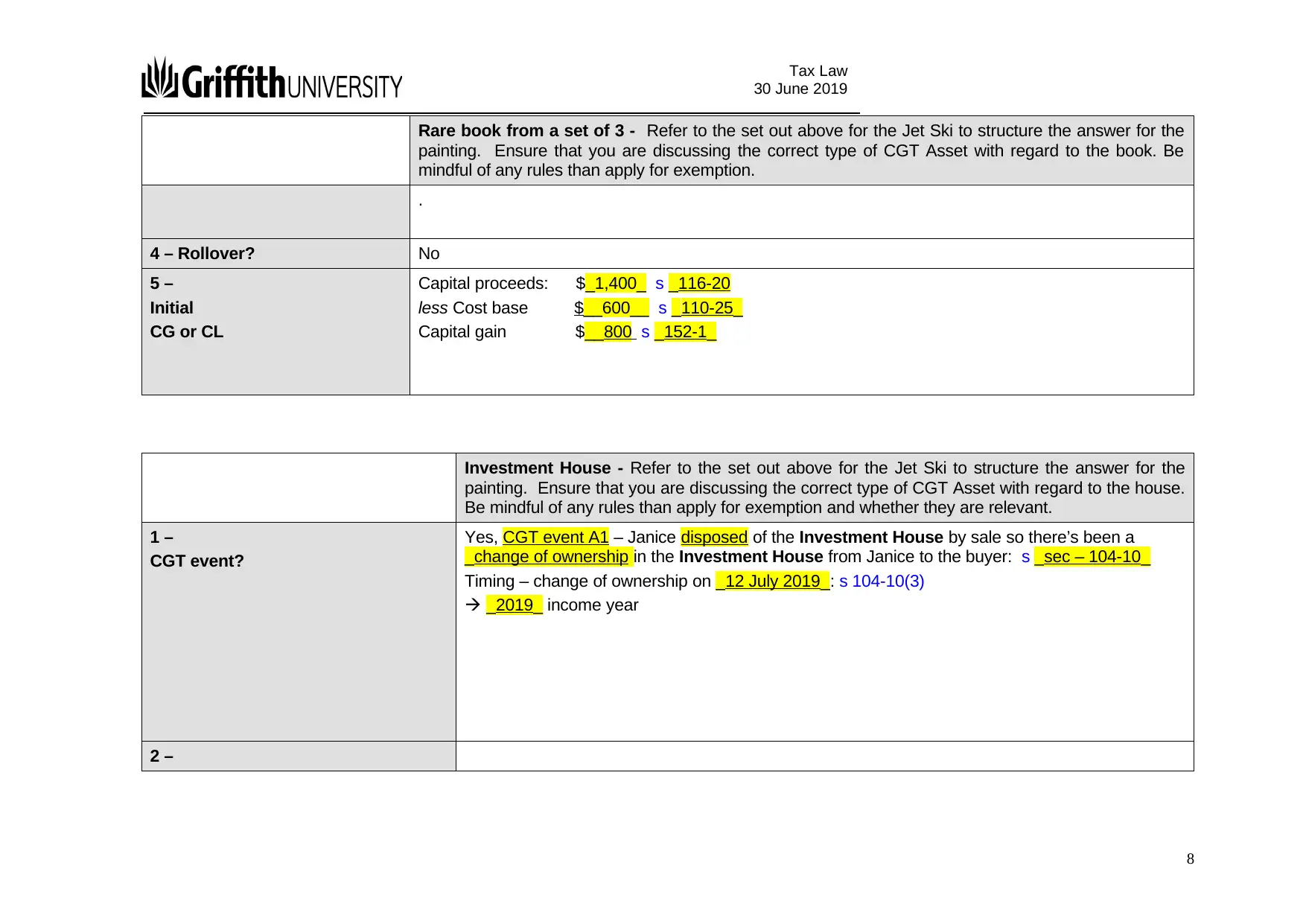

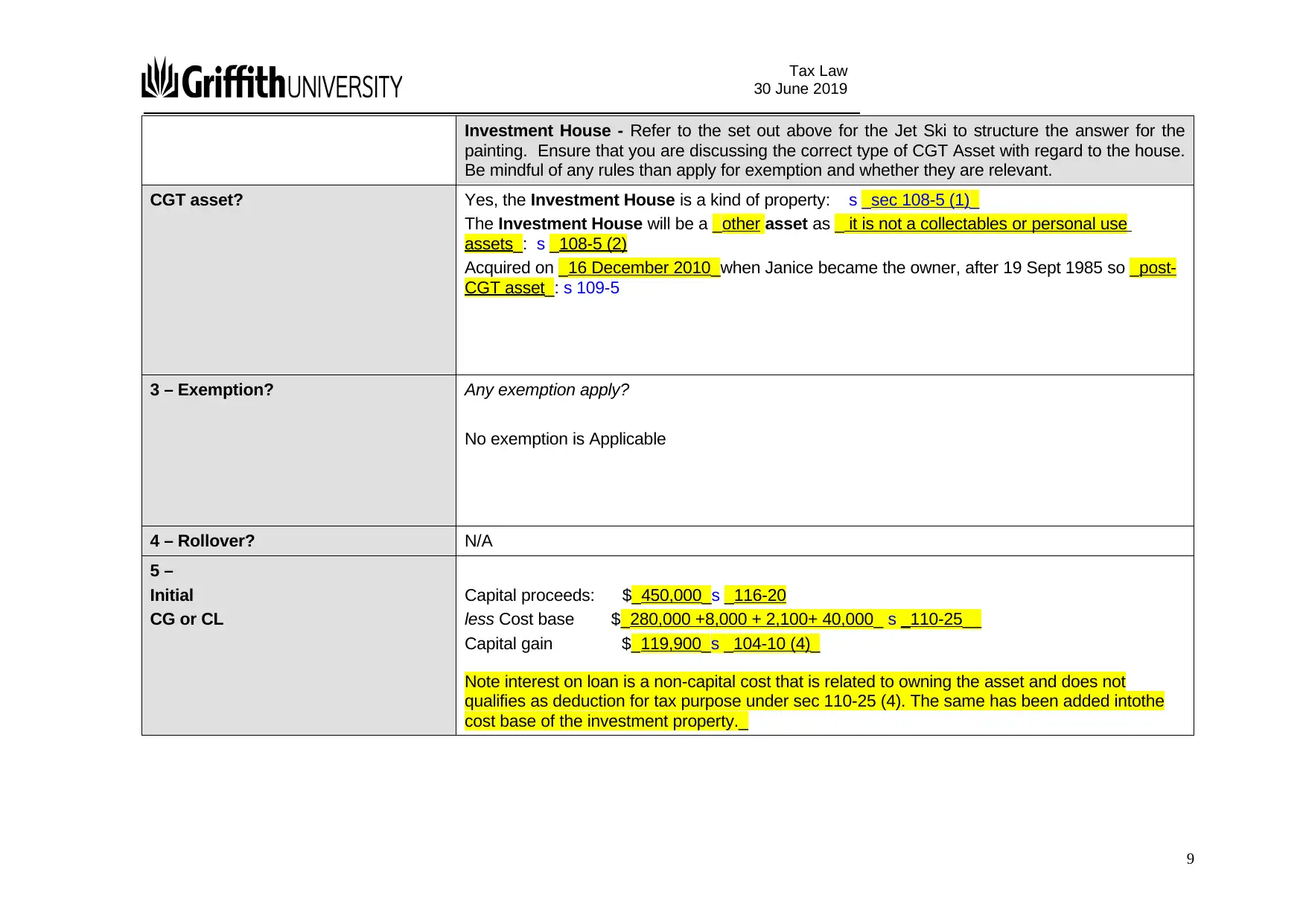

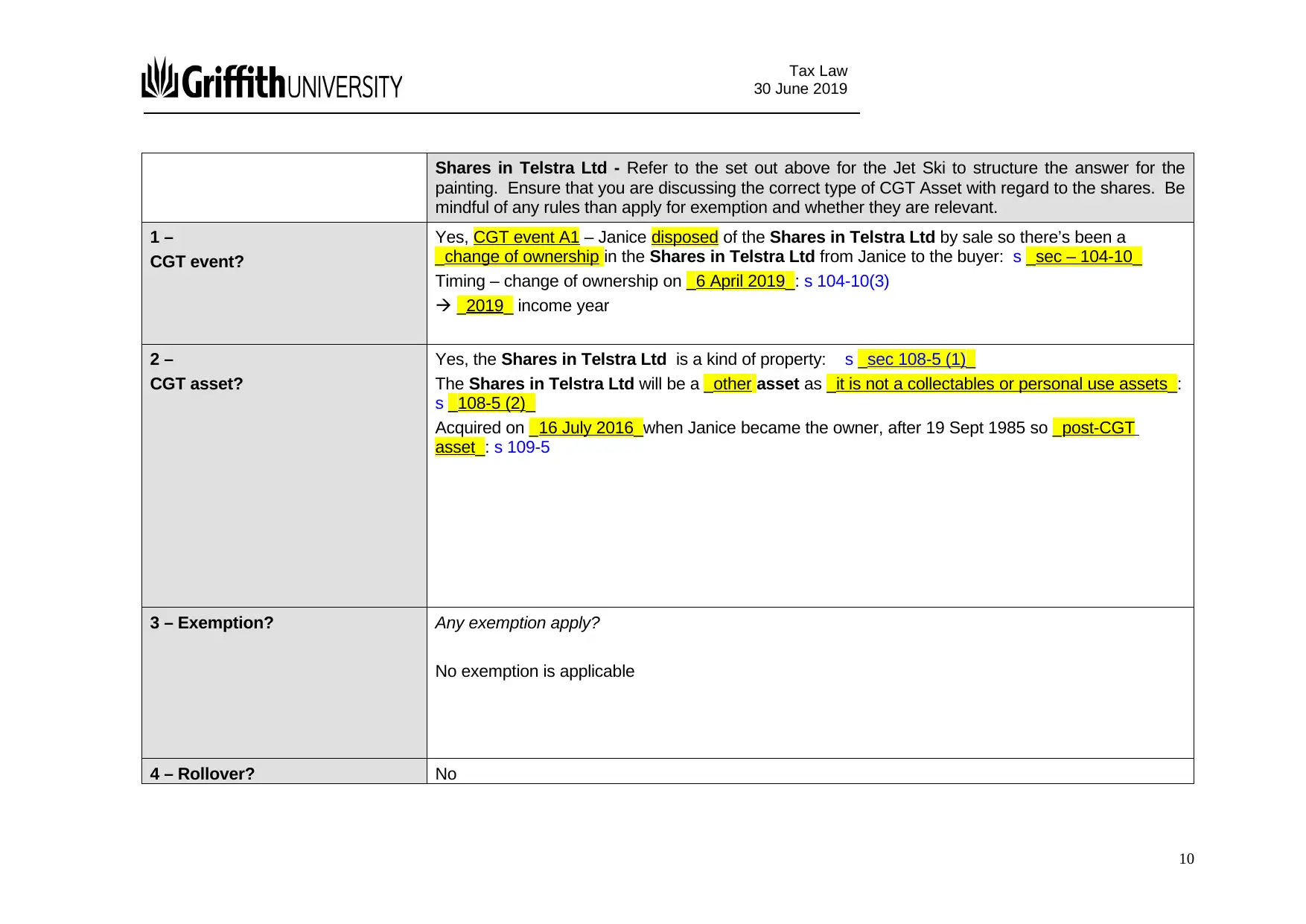

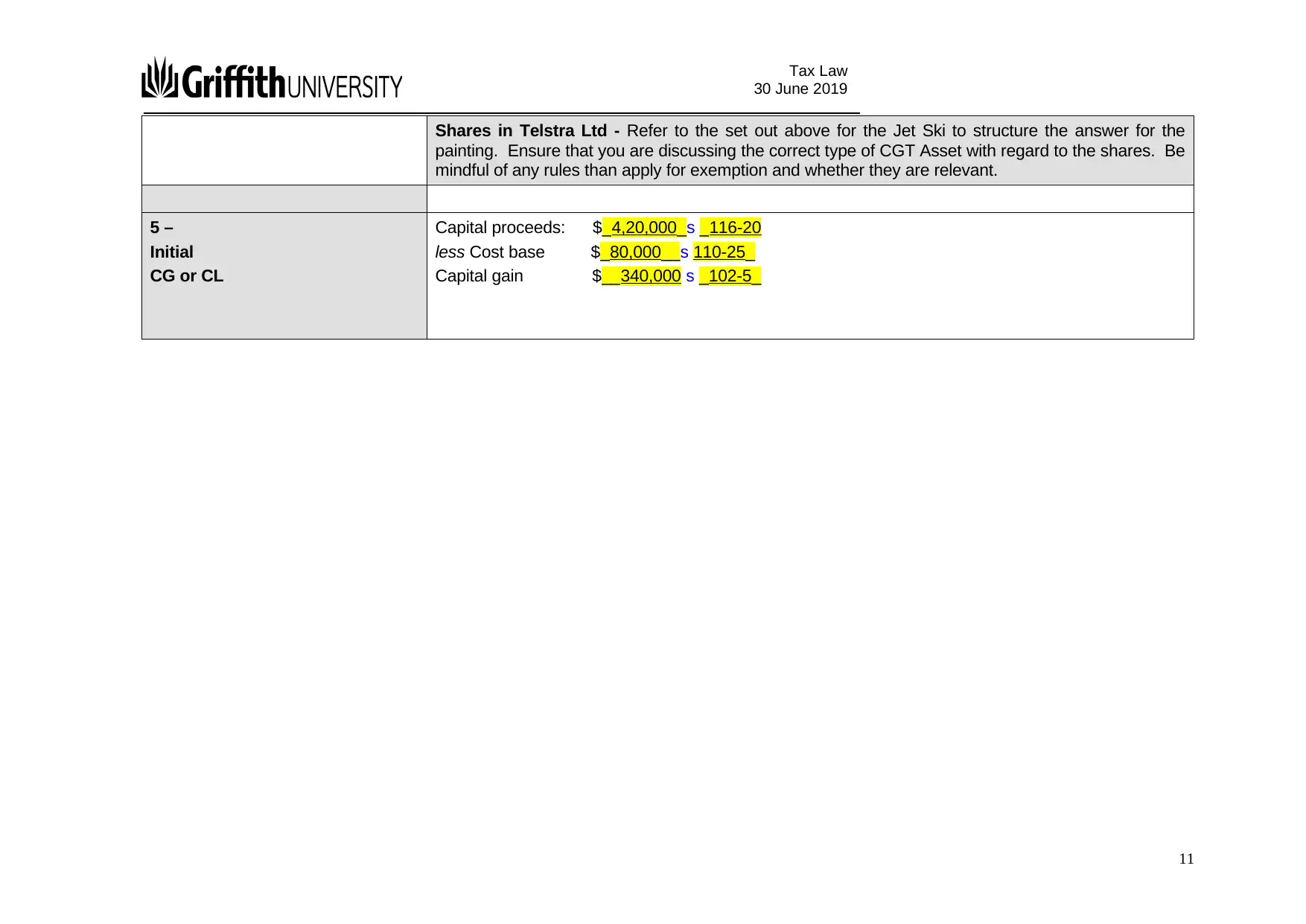

This document presents a comprehensive solution to a tax law assignment, specifically focusing on Capital Gains Tax (CGT) and its application to various scenarios. The solution addresses two main questions. The first question involves evaluating the correctness of several statements related to CGT, providing explanations and citing relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997). The second question requires the calculation of capital gains and losses arising from the sale of various assets, including a jet ski, painting, rare book, investment house, and shares. The analysis involves determining CGT events, identifying CGT assets, considering exemptions, and calculating capital gains or losses based on the cost base and capital proceeds. The solution provides step-by-step calculations and explanations for each asset, ensuring a clear understanding of the CGT implications. The document highlights the relevant sections of the ITAA 1997 and provides a detailed breakdown of each transaction to determine the resultant capital gains or losses.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.