Taxation Law Assignment: CGT Event Analysis and Tax Calculation

VerifiedAdded on 2022/08/20

|7

|872

|15

Homework Assignment

AI Summary

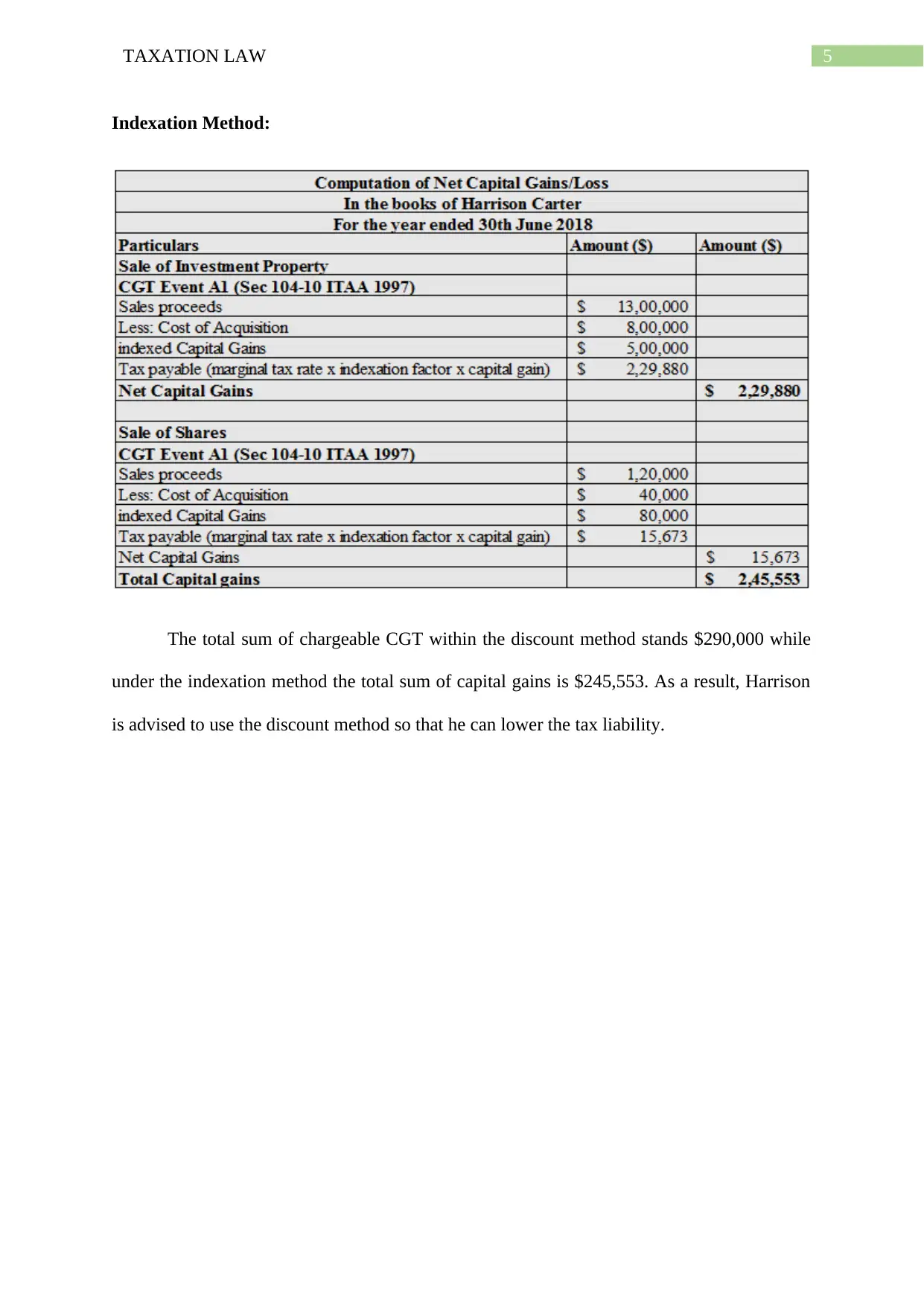

This document presents a detailed analysis of a Taxation Law assignment, focusing on Capital Gains Tax (CGT) events. The assignment explores scenarios involving the sale of investment property and a share portfolio, analyzing the timing of CGT events based on relevant legislation and case law, including references to the Income Tax Assessment Act 1997 (ITAA 1997) and the case of FCT v Sara Lee Household & Body Care P/L (2000). The solution calculates tax liabilities using both the discount and indexation methods, providing recommendations for minimizing tax obligations. The document includes references to key legal texts and provides a comprehensive understanding of CGT principles and their practical application in the given case study.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.