Taxation Law: CGT Event Analysis and Fringe Benefit Implications

VerifiedAdded on 2023/06/04

|13

|3550

|340

Report

AI Summary

This report provides a comprehensive analysis of Capital Gains Tax (CGT) events and fringe benefits under Australian Taxation Law. It examines various scenarios, including the sale of a vacant land, theft of an antique bed, sale of a painting, and transactions involving shares in different companies, determining the capital gains or losses and their eligibility for discount capital gains. The report also addresses the classification of a violin as a personal use asset and its tax implications. Furthermore, it delves into the effects of fringe benefits, specifically focusing on the provision of a car by an employer and its implications under the Fringe Benefits Tax Assessment Act 1986 (FBTAA 1986), referencing relevant case laws and legislative sections to support the analysis.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1:................................................................................................................2

(a) Block of vacant land:........................................................................................................2

(b) Antique bed:.....................................................................................................................2

(c) Painting:............................................................................................................................4

(d) Shares:..............................................................................................................................5

i) Common Bank Limited:.................................................................................................5

ii) PHB Iron Ore Limited:..................................................................................................5

iii) Young Kids Learning Limited:....................................................................................6

iv) Share Build Limited:.....................................................................................................6

(e) Violin:...............................................................................................................................7

Answer to Question 2:................................................................................................................8

Part (a):...................................................................................................................................8

Part (b):.................................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Answer to Question 1:................................................................................................................2

(a) Block of vacant land:........................................................................................................2

(b) Antique bed:.....................................................................................................................2

(c) Painting:............................................................................................................................4

(d) Shares:..............................................................................................................................5

i) Common Bank Limited:.................................................................................................5

ii) PHB Iron Ore Limited:..................................................................................................5

iii) Young Kids Learning Limited:....................................................................................6

iv) Share Build Limited:.....................................................................................................6

(e) Violin:...............................................................................................................................7

Answer to Question 2:................................................................................................................8

Part (a):...................................................................................................................................8

Part (b):.................................................................................................................................10

References:...............................................................................................................................11

2TAXATION LAW

Answer to Question 1:

(a) Block of vacant land:

The selling of land could be adjudged as CGT event and in accordance with “Section

108-5 of ITAA 1997”; the land could be termed as CGT asset. When this is the case, the land

sale triggers the event A1, which takes place at the time of signing the contract on 3rd June of

the current tax year, which complies with “Section 104-10 of ITAA 1997”. The capital

proceeds from this sale include $320,000 and the fact that $20,000 is payable on 3rd January

of the next year is not relevant in this case. The overall cost base is obtained as $120,000,

which is computed by adding all the amounts together mentioned as follows:

According to “Section 110-25(2) of ITAA 1997”, acquisition is identified as the first

component of the asset base, which is $100,000 (Barkoczy 2016).

In accordance with “Section 110-25(4) of ITAA 1997”, rates and land taxes are

identified as the third component of the asset base amounting to $20,000, since the

acquisition of land was made after 20th August 1991.

This implies the existence of capital gain due to the fact that overall cost base has not

been more compared to the capital proceeds. Therefore, the capital gain would be $200,000

($320,000 - $120,000). This amount is deemed to be an eligible discount capital gain

mentioned under “Section 115-25(1) of ITAA 1997” (Braithwaite 2017).

(b) Antique bed:

According to the provided information, the antique bed is stolen and this is considered

as CGT asset. According to “Section 104-20(1) of ITAA 1997”, this incident triggers the

event C1. This incident has occurred at the time of obtaining compensation proceeds from the

insurance firm. The issue here is to evaluate whether the antique bed would be collectible.

Answer to Question 1:

(a) Block of vacant land:

The selling of land could be adjudged as CGT event and in accordance with “Section

108-5 of ITAA 1997”; the land could be termed as CGT asset. When this is the case, the land

sale triggers the event A1, which takes place at the time of signing the contract on 3rd June of

the current tax year, which complies with “Section 104-10 of ITAA 1997”. The capital

proceeds from this sale include $320,000 and the fact that $20,000 is payable on 3rd January

of the next year is not relevant in this case. The overall cost base is obtained as $120,000,

which is computed by adding all the amounts together mentioned as follows:

According to “Section 110-25(2) of ITAA 1997”, acquisition is identified as the first

component of the asset base, which is $100,000 (Barkoczy 2016).

In accordance with “Section 110-25(4) of ITAA 1997”, rates and land taxes are

identified as the third component of the asset base amounting to $20,000, since the

acquisition of land was made after 20th August 1991.

This implies the existence of capital gain due to the fact that overall cost base has not

been more compared to the capital proceeds. Therefore, the capital gain would be $200,000

($320,000 - $120,000). This amount is deemed to be an eligible discount capital gain

mentioned under “Section 115-25(1) of ITAA 1997” (Braithwaite 2017).

(b) Antique bed:

According to the provided information, the antique bed is stolen and this is considered

as CGT asset. According to “Section 104-20(1) of ITAA 1997”, this incident triggers the

event C1. This incident has occurred at the time of obtaining compensation proceeds from the

insurance firm. The issue here is to evaluate whether the antique bed would be collectible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

This would rely on the nature of the item and the purpose of the client at the time of

purchasing the same (Daniel et al. 2016). In this situation, as the name implies, the antique

bed could be classified as an antique item, as laid out in “Section 108-10(2) of ITAA 1997”.

Moreover, it is noteworthy to mention that the antique bed would be used for personal

purpose, which fulfils both limbs of the definition that it is collectible. Hence, there should

not be disregard of any capital gains and losses due to the fact that the cost base of the asset is

higher than $500, which is line with “Section 118-10(1) of ITAA 1997”.

Moreover, “Section 116-25 of ITAA 1997” states the substitution rule of market value

are not included for C1 event and therefore, capital proceeds are identified as $11,000.

However, there is no relevancy of the market value of $25,000 in this scenario. On the other

hand, the overall cost base is identified as $5,000. The calculation is conducted by taking into

consideration all the following amounts:

As mentioned in “Section 110-25(2) of ITAA 1997”, acquisition is the initial cost

base component, which is provided as $3,500.

According to “Section 110-25(5) of ITAA 1997”, expense incurred for increasing the

value of the asset is the fourth asset base component, which is given as $1,500.

This implies that the capital gain would be $6,000 ($11,000 - $6,000) and this is

considered to be eligible discount capital gain, as stated in “Section 115-25(1) of ITAA

1997”. Moreover, “Section 114-1 of ITAA 1997”, emphasises on applying indexation to the

cost due to the purchase of antique bed before 21st September 1999. In the third quarter of the

year 1986, the index number was 77.6 at the time of purchasing the bed. However, in the last

quarter of 1986, the index number was 79.8 after conduction of alterations (Frecknall-Hughes

and Kirchler 2015). “Section 960-275 of ITAA 1997” states that the index number at the time

the bed was stolen was 123.4 and it fell under the third quarter of the year 1999. Thus, the

This would rely on the nature of the item and the purpose of the client at the time of

purchasing the same (Daniel et al. 2016). In this situation, as the name implies, the antique

bed could be classified as an antique item, as laid out in “Section 108-10(2) of ITAA 1997”.

Moreover, it is noteworthy to mention that the antique bed would be used for personal

purpose, which fulfils both limbs of the definition that it is collectible. Hence, there should

not be disregard of any capital gains and losses due to the fact that the cost base of the asset is

higher than $500, which is line with “Section 118-10(1) of ITAA 1997”.

Moreover, “Section 116-25 of ITAA 1997” states the substitution rule of market value

are not included for C1 event and therefore, capital proceeds are identified as $11,000.

However, there is no relevancy of the market value of $25,000 in this scenario. On the other

hand, the overall cost base is identified as $5,000. The calculation is conducted by taking into

consideration all the following amounts:

As mentioned in “Section 110-25(2) of ITAA 1997”, acquisition is the initial cost

base component, which is provided as $3,500.

According to “Section 110-25(5) of ITAA 1997”, expense incurred for increasing the

value of the asset is the fourth asset base component, which is given as $1,500.

This implies that the capital gain would be $6,000 ($11,000 - $6,000) and this is

considered to be eligible discount capital gain, as stated in “Section 115-25(1) of ITAA

1997”. Moreover, “Section 114-1 of ITAA 1997”, emphasises on applying indexation to the

cost due to the purchase of antique bed before 21st September 1999. In the third quarter of the

year 1986, the index number was 77.6 at the time of purchasing the bed. However, in the last

quarter of 1986, the index number was 79.8 after conduction of alterations (Frecknall-Hughes

and Kirchler 2015). “Section 960-275 of ITAA 1997” states that the index number at the time

the bed was stolen was 123.4 and it fell under the third quarter of the year 1999. Thus, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

index factor amounts to 1.590 (4/77.6) and 1.546 (4/79.8), as per “Section 960-275(5) of

ITAA 1997”. Hence, the indexed cost base is computed by considering the below-stated

amounts:

First cost base component: $3,500 x 1.590 = $5,565

Fourth cost base component: $1,500 x 1.546 = $2,319

Therefore, the total amount of the index cost base would be $7,884 ($5,565 + $2,319).

This signifies the existence of capital gain, since the indexed cost base does not exceed the

capital proceeds. Hence, the capital gain amounts to $3,116 ($11,000 - $7,884).

(c) Painting:

In this case, the issue is to ascertain whether the painting is collectible. More

precisely, an artwork would rely on the purpose or nature of the owner at the time of purchase

(Hashimzade and Epifantseva 2017). As per the provided situation, the client bought the item

from a renowned artist of Australia and later on, the painting was sold due to rise in value

after the demise of the artist. Thus, it could be used that the purchase is not used for personal

enjoyment; instead, it was conducted for investment purpose (Higgins 2014). As a result, the

painting could not be adjudged as collectible. The painting sale could be identified as CGT

event, which belongs within disposals, mentioned under “Section 104-A of ITAA 1997”. In

this case, painting could be classified under a part of the client’s property, which is then

considered as a CGT asset.

When the painting was disposed, the event A1 is triggered, which falls under “Section

104-10(1) of ITAA 1997”. The overall cost base is identified as $2,000 and the capital

proceeds have been $125,000 and therefore, the capital gain would be $125,000 ($123,000 -

$2,000). However, it is to be noted that the painting was bought on 2nd May 1985, which was

prior to 20th September 1985. As a result, it would fall under Pre-CGT asset, due to which

index factor amounts to 1.590 (4/77.6) and 1.546 (4/79.8), as per “Section 960-275(5) of

ITAA 1997”. Hence, the indexed cost base is computed by considering the below-stated

amounts:

First cost base component: $3,500 x 1.590 = $5,565

Fourth cost base component: $1,500 x 1.546 = $2,319

Therefore, the total amount of the index cost base would be $7,884 ($5,565 + $2,319).

This signifies the existence of capital gain, since the indexed cost base does not exceed the

capital proceeds. Hence, the capital gain amounts to $3,116 ($11,000 - $7,884).

(c) Painting:

In this case, the issue is to ascertain whether the painting is collectible. More

precisely, an artwork would rely on the purpose or nature of the owner at the time of purchase

(Hashimzade and Epifantseva 2017). As per the provided situation, the client bought the item

from a renowned artist of Australia and later on, the painting was sold due to rise in value

after the demise of the artist. Thus, it could be used that the purchase is not used for personal

enjoyment; instead, it was conducted for investment purpose (Higgins 2014). As a result, the

painting could not be adjudged as collectible. The painting sale could be identified as CGT

event, which belongs within disposals, mentioned under “Section 104-A of ITAA 1997”. In

this case, painting could be classified under a part of the client’s property, which is then

considered as a CGT asset.

When the painting was disposed, the event A1 is triggered, which falls under “Section

104-10(1) of ITAA 1997”. The overall cost base is identified as $2,000 and the capital

proceeds have been $125,000 and therefore, the capital gain would be $125,000 ($123,000 -

$2,000). However, it is to be noted that the painting was bought on 2nd May 1985, which was

prior to 20th September 1985. As a result, it would fall under Pre-CGT asset, due to which

5TAXATION LAW

capital gain would be disregarded, in accordance with “Section 104-10(5) of ITAA 1997”

(Littlewood and Elliffe 2017).

(d) Shares:

i) Common Bank Limited:

Since share in an organisation is a CGT asset, as per “Section 108-5 of ITAA 1997”, the

selling of shares would lead to ownership change of shares. This would trigger A1 event in

compliance with “Section 104-10(1) of ITAA 1997”. This change is evident, after the sale of

shares on 4th July. Moreover, indexation is not applicable to the cost base, as the shares were

bought after 21st September 1999 (McGregor-Lowndes 2016). In this situation, the capital

proceeds denote the money received by or entitled to the taxpayer in relation to the event

occurrence, which are obtained as $47,000 ($47 x 1,000). On the other hand, the overall cost

base is obtained as $16.300 by taking into consideration the following amounts:

As per “Section 110-25(2) of ITAA 1997”, acquisition cost is the initial cost base

component, which is $15,000 ($15 x 1,000).

“Section 110-35 of ITAA 1997” cites that brokerage fees are the second cost base

component, which is $550.

Another component of the cost base is stamp duty cost, which is $750, as per the

above section.

Hence, the capital gain of the client would be $30,700 and this is considered as eligible

discount capital gain, as per “Section 115-25(1) of ITAA 1997”.

ii) PHB Iron Ore Limited:

The case is similar to that of Common Bank Limited, in which the ownership has

changed after selling the shares on 14th February. The capital proceeds have been $62,500

capital gain would be disregarded, in accordance with “Section 104-10(5) of ITAA 1997”

(Littlewood and Elliffe 2017).

(d) Shares:

i) Common Bank Limited:

Since share in an organisation is a CGT asset, as per “Section 108-5 of ITAA 1997”, the

selling of shares would lead to ownership change of shares. This would trigger A1 event in

compliance with “Section 104-10(1) of ITAA 1997”. This change is evident, after the sale of

shares on 4th July. Moreover, indexation is not applicable to the cost base, as the shares were

bought after 21st September 1999 (McGregor-Lowndes 2016). In this situation, the capital

proceeds denote the money received by or entitled to the taxpayer in relation to the event

occurrence, which are obtained as $47,000 ($47 x 1,000). On the other hand, the overall cost

base is obtained as $16.300 by taking into consideration the following amounts:

As per “Section 110-25(2) of ITAA 1997”, acquisition cost is the initial cost base

component, which is $15,000 ($15 x 1,000).

“Section 110-35 of ITAA 1997” cites that brokerage fees are the second cost base

component, which is $550.

Another component of the cost base is stamp duty cost, which is $750, as per the

above section.

Hence, the capital gain of the client would be $30,700 and this is considered as eligible

discount capital gain, as per “Section 115-25(1) of ITAA 1997”.

ii) PHB Iron Ore Limited:

The case is similar to that of Common Bank Limited, in which the ownership has

changed after selling the shares on 14th February. The capital proceeds have been $62,500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

($25 x 2,500); however, the overall cost base is $32,500 by taking into consideration the

following amounts:

Acquisition cost is the initial cost base component, which is $30,000 ($12 x 2,500).

Brokerage fees are the second cost base component, which is $1,000.

Another component of the cost base is stamp duty cost, which is $1,500, as per the

above section.

Hence, the capital gain made is $30,000 ($62,500 - $32,500), which is an eligible

discount capital gain.

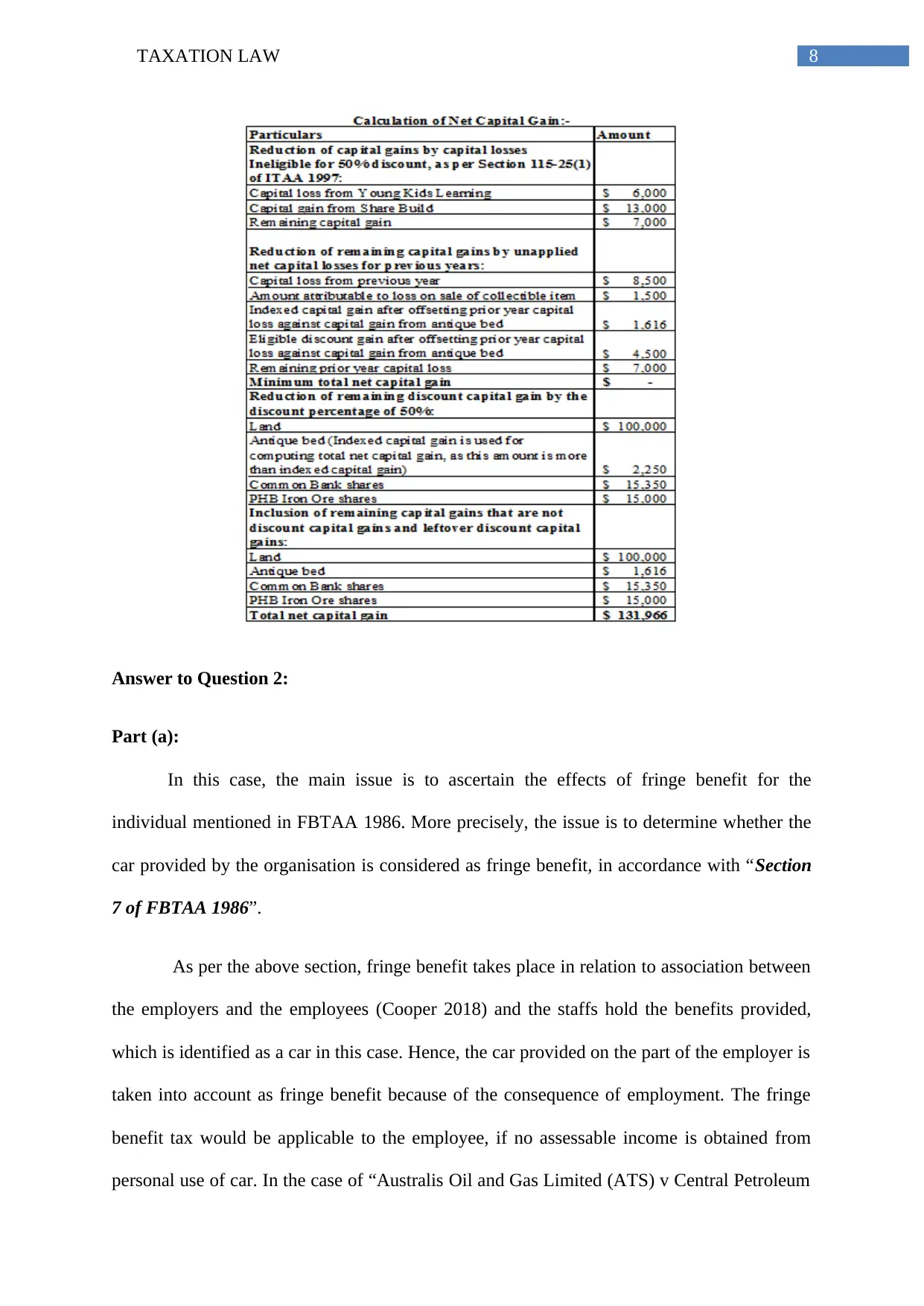

iii) Young Kids Learning Limited:

The situation, in this case, is identical to the above situation until the change of

ownership; however, capital loss is suffered by the client. The capital proceeds have been

$600 ($0.5 x 1,200), while the overall cost base is $6,150 by considering the following

amounts:

Acquisition cost is the initial cost base component, which is $6,000 ($5 x 1,200).

Brokerage fees are the second cost base component, which is $1,000.

Another component of the cost base is stamp duty cost, which is $1,500, as per the

above section (Russell 2016).

Hence, the capital loss suffered is $6,000 ($600 - $6,600), which is an eligible discount

capital gain.

iv) Share Build Limited:

The case is similar to that of Common Bank Limited, in which the ownership has

changed after selling the shares on 22nd January. The capital proceeds have been $25,000

($2.5 x 10,000) and the overall cost base is $11,900 by considering the following amounts:

($25 x 2,500); however, the overall cost base is $32,500 by taking into consideration the

following amounts:

Acquisition cost is the initial cost base component, which is $30,000 ($12 x 2,500).

Brokerage fees are the second cost base component, which is $1,000.

Another component of the cost base is stamp duty cost, which is $1,500, as per the

above section.

Hence, the capital gain made is $30,000 ($62,500 - $32,500), which is an eligible

discount capital gain.

iii) Young Kids Learning Limited:

The situation, in this case, is identical to the above situation until the change of

ownership; however, capital loss is suffered by the client. The capital proceeds have been

$600 ($0.5 x 1,200), while the overall cost base is $6,150 by considering the following

amounts:

Acquisition cost is the initial cost base component, which is $6,000 ($5 x 1,200).

Brokerage fees are the second cost base component, which is $1,000.

Another component of the cost base is stamp duty cost, which is $1,500, as per the

above section (Russell 2016).

Hence, the capital loss suffered is $6,000 ($600 - $6,600), which is an eligible discount

capital gain.

iv) Share Build Limited:

The case is similar to that of Common Bank Limited, in which the ownership has

changed after selling the shares on 22nd January. The capital proceeds have been $25,000

($2.5 x 10,000) and the overall cost base is $11,900 by considering the following amounts:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Acquisition cost is the initial cost base component, which is $10,000 ($51 x 10,000).

Brokerage fees are the second cost base component, which is $900.

Another component of the cost base is stamp duty cost, which is $1,100, as per the

above section.

Hence, the capital loss suffered is $13,000 ($25,000 - $12,000). However, this is not an

eligible discount gain, as shares were bought in July of the existing tax year and they were

sold in the same year not withholding for at least 12 months, as per “Section 115-40 of ITAA

1997” (Wu 2018).

(e) Violin:

According to the facts provided, the client is interested in accumulating musical

instruments and they are for personal enjoyment only. Therefore, the violin is classified as

personal use asset, in accordance with “Section 108-20(2) of ITAA 1997”. This sale would

trigger A1 event due to ownership change. As the cost acquisition of violin is $5,500 is lower

than $10,000, one particular law is applicable, according to which the capital gain of $6,500

($12,000 - $5,500) would not be considered.

For calculating the total capital gain, the following considerations are made:

Acquisition cost is the initial cost base component, which is $10,000 ($51 x 10,000).

Brokerage fees are the second cost base component, which is $900.

Another component of the cost base is stamp duty cost, which is $1,100, as per the

above section.

Hence, the capital loss suffered is $13,000 ($25,000 - $12,000). However, this is not an

eligible discount gain, as shares were bought in July of the existing tax year and they were

sold in the same year not withholding for at least 12 months, as per “Section 115-40 of ITAA

1997” (Wu 2018).

(e) Violin:

According to the facts provided, the client is interested in accumulating musical

instruments and they are for personal enjoyment only. Therefore, the violin is classified as

personal use asset, in accordance with “Section 108-20(2) of ITAA 1997”. This sale would

trigger A1 event due to ownership change. As the cost acquisition of violin is $5,500 is lower

than $10,000, one particular law is applicable, according to which the capital gain of $6,500

($12,000 - $5,500) would not be considered.

For calculating the total capital gain, the following considerations are made:

8TAXATION LAW

Answer to Question 2:

Part (a):

In this case, the main issue is to ascertain the effects of fringe benefit for the

individual mentioned in FBTAA 1986. More precisely, the issue is to determine whether the

car provided by the organisation is considered as fringe benefit, in accordance with “Section

7 of FBTAA 1986”.

As per the above section, fringe benefit takes place in relation to association between

the employers and the employees (Cooper 2018) and the staffs hold the benefits provided,

which is identified as a car in this case. Hence, the car provided on the part of the employer is

taken into account as fringe benefit because of the consequence of employment. The fringe

benefit tax would be applicable to the employee, if no assessable income is obtained from

personal use of car. In the case of “Australis Oil and Gas Limited (ATS) v Central Petroleum

Answer to Question 2:

Part (a):

In this case, the main issue is to ascertain the effects of fringe benefit for the

individual mentioned in FBTAA 1986. More precisely, the issue is to determine whether the

car provided by the organisation is considered as fringe benefit, in accordance with “Section

7 of FBTAA 1986”.

As per the above section, fringe benefit takes place in relation to association between

the employers and the employees (Cooper 2018) and the staffs hold the benefits provided,

which is identified as a car in this case. Hence, the car provided on the part of the employer is

taken into account as fringe benefit because of the consequence of employment. The fringe

benefit tax would be applicable to the employee, if no assessable income is obtained from

personal use of car. In the case of “Australis Oil and Gas Limited (ATS) v Central Petroleum

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Limited (CPL) 2015”, it has been found that a declaration is made about the non-

infringement of the British and French parts of the European patent number EP 1 523 218

(Butler and Calcott 2018).

The fringe benefit expense is mentioned in “Subsection B22A of FBTAA 1986”. This

expense signifies the amount spent by the employee and this is to be reimbursed by the

employer. The expense might include costs from official and personal reasons. Generally, if

an employee incurs any cost for meeting the obligations of the employer, the amount is to be

reimbursed to the employee as fringe benefit expense payment. Therefore, the amount

reimbursed to the employee is taxable (Woellner et al. 2016).

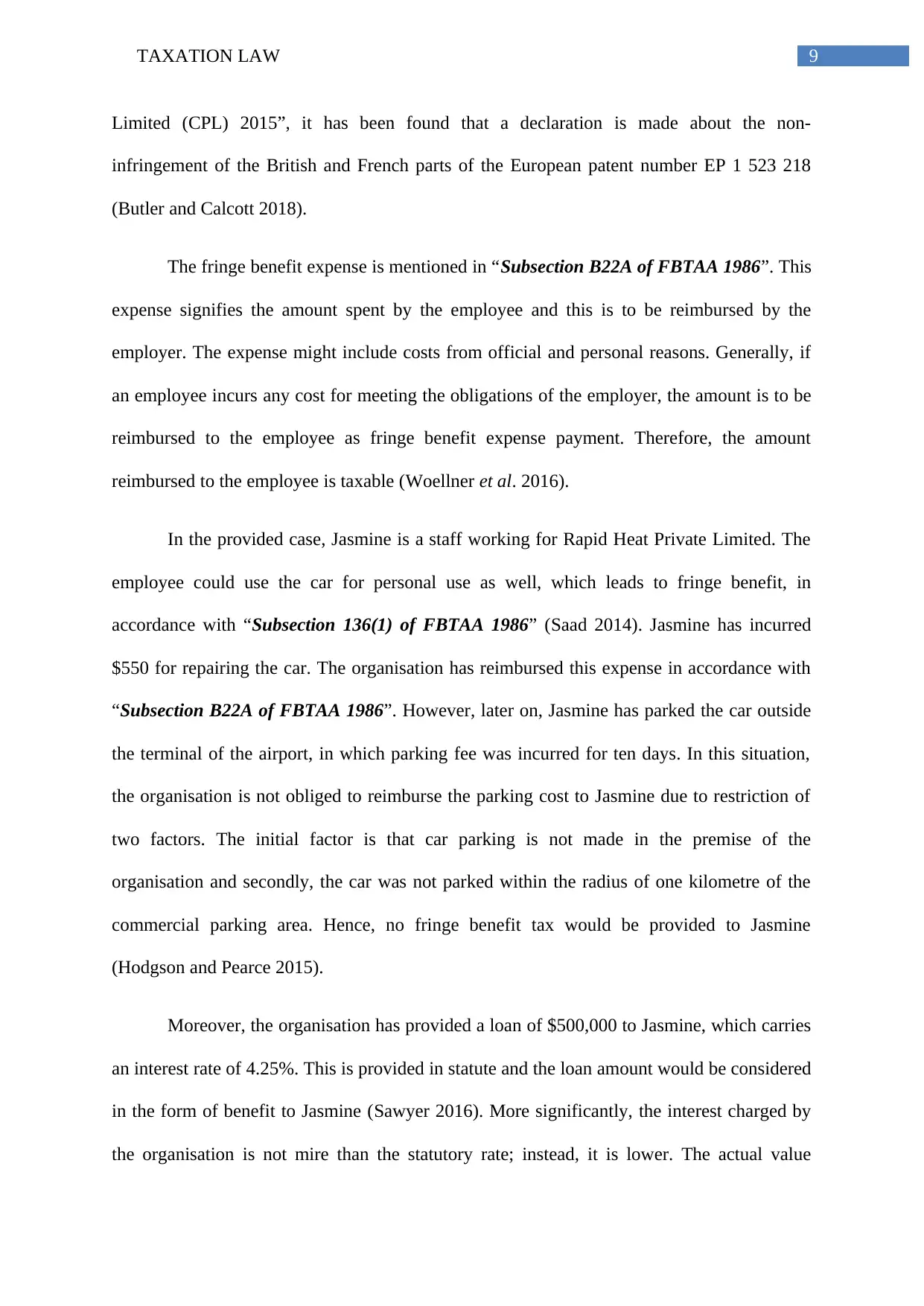

In the provided case, Jasmine is a staff working for Rapid Heat Private Limited. The

employee could use the car for personal use as well, which leads to fringe benefit, in

accordance with “Subsection 136(1) of FBTAA 1986” (Saad 2014). Jasmine has incurred

$550 for repairing the car. The organisation has reimbursed this expense in accordance with

“Subsection B22A of FBTAA 1986”. However, later on, Jasmine has parked the car outside

the terminal of the airport, in which parking fee was incurred for ten days. In this situation,

the organisation is not obliged to reimburse the parking cost to Jasmine due to restriction of

two factors. The initial factor is that car parking is not made in the premise of the

organisation and secondly, the car was not parked within the radius of one kilometre of the

commercial parking area. Hence, no fringe benefit tax would be provided to Jasmine

(Hodgson and Pearce 2015).

Moreover, the organisation has provided a loan of $500,000 to Jasmine, which carries

an interest rate of 4.25%. This is provided in statute and the loan amount would be considered

in the form of benefit to Jasmine (Sawyer 2016). More significantly, the interest charged by

the organisation is not mire than the statutory rate; instead, it is lower. The actual value

Limited (CPL) 2015”, it has been found that a declaration is made about the non-

infringement of the British and French parts of the European patent number EP 1 523 218

(Butler and Calcott 2018).

The fringe benefit expense is mentioned in “Subsection B22A of FBTAA 1986”. This

expense signifies the amount spent by the employee and this is to be reimbursed by the

employer. The expense might include costs from official and personal reasons. Generally, if

an employee incurs any cost for meeting the obligations of the employer, the amount is to be

reimbursed to the employee as fringe benefit expense payment. Therefore, the amount

reimbursed to the employee is taxable (Woellner et al. 2016).

In the provided case, Jasmine is a staff working for Rapid Heat Private Limited. The

employee could use the car for personal use as well, which leads to fringe benefit, in

accordance with “Subsection 136(1) of FBTAA 1986” (Saad 2014). Jasmine has incurred

$550 for repairing the car. The organisation has reimbursed this expense in accordance with

“Subsection B22A of FBTAA 1986”. However, later on, Jasmine has parked the car outside

the terminal of the airport, in which parking fee was incurred for ten days. In this situation,

the organisation is not obliged to reimburse the parking cost to Jasmine due to restriction of

two factors. The initial factor is that car parking is not made in the premise of the

organisation and secondly, the car was not parked within the radius of one kilometre of the

commercial parking area. Hence, no fringe benefit tax would be provided to Jasmine

(Hodgson and Pearce 2015).

Moreover, the organisation has provided a loan of $500,000 to Jasmine, which carries

an interest rate of 4.25%. This is provided in statute and the loan amount would be considered

in the form of benefit to Jasmine (Sawyer 2016). More significantly, the interest charged by

the organisation is not mire than the statutory rate; instead, it is lower. The actual value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

related to loan fringe benefit includes the variation between interest, which could have risen

at the application of statutory rate and the actual rate could be applied under “Section 4 of

FBTAA 1986”.

Part (b):

According to FBTAA 1986, the individual incurring tax needs to maintain the cost

details and claim deduction, which is allowed constituting portion of assessable salary and

identifying the consequences of the same (Tan, Braithwaite and Reinhart 2016). A taxpayer is

enabled to assure cost findings, which are caused due to the range of developing assessable

pay.

In other situation, if Jasmine utilised the leftover loan amount of $50,000 to acquire

shares, instead of providing the shares to her husband, she could claim deduction, as per

“Section 8-1 of ITAA 1997”. Hence, as the remaining loan amount was provided to her

husband purchasing shares and due to such consequence, the individual is entitled for

claiming deduction relating to loan, which could have been deductible, as per “Section 8-1 of

ITAA 1997” (Tang and Wan 2015).

related to loan fringe benefit includes the variation between interest, which could have risen

at the application of statutory rate and the actual rate could be applied under “Section 4 of

FBTAA 1986”.

Part (b):

According to FBTAA 1986, the individual incurring tax needs to maintain the cost

details and claim deduction, which is allowed constituting portion of assessable salary and

identifying the consequences of the same (Tan, Braithwaite and Reinhart 2016). A taxpayer is

enabled to assure cost findings, which are caused due to the range of developing assessable

pay.

In other situation, if Jasmine utilised the leftover loan amount of $50,000 to acquire

shares, instead of providing the shares to her husband, she could claim deduction, as per

“Section 8-1 of ITAA 1997”. Hence, as the remaining loan amount was provided to her

husband purchasing shares and due to such consequence, the individual is entitled for

claiming deduction relating to loan, which could have been deductible, as per “Section 8-1 of

ITAA 1997” (Tang and Wan 2015).

11TAXATION LAW

References:

Barkoczy, S., 2016. Core tax legislation and study guide. OUP Catalogue.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Cooper, R., 2018. Recent changes to fringe benefits. TAXtalk, 2018(71), pp.52-55.

Daniel, P., Keen, M., Świstak, A. and Thuronyi, V. eds., 2016. International Taxation and

the Extractive Industries: Resources Without Borders. Taylor & Francis.

Frecknall-Hughes, J. and Kirchler, E., 2015. Towards a general theory of tax practice. Social

& Legal Studies, 24(2), pp.289-312.

Hashimzade, N. and Epifantseva, Y. eds., 2017. The Routledge Companion to Tax Avoidance

Research. Routledge.

Higgins, T., 2014. Income contingent loans: Theory, practice and prospects. Springer.

Hodgson, H. and Pearce, P., 2015. TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), p.819.

Littlewood, M. and Elliffe, C. eds., 2017. Capital Gains Taxation: A Comparative Analysis of

Key Issues. Edward Elgar Publishing.

McGregor-Lowndes, M., 2016. Lawyers, reform and regulation in the Australian third

sector. Third Sector Review, 22(2), p.33.

References:

Barkoczy, S., 2016. Core tax legislation and study guide. OUP Catalogue.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Cooper, R., 2018. Recent changes to fringe benefits. TAXtalk, 2018(71), pp.52-55.

Daniel, P., Keen, M., Świstak, A. and Thuronyi, V. eds., 2016. International Taxation and

the Extractive Industries: Resources Without Borders. Taylor & Francis.

Frecknall-Hughes, J. and Kirchler, E., 2015. Towards a general theory of tax practice. Social

& Legal Studies, 24(2), pp.289-312.

Hashimzade, N. and Epifantseva, Y. eds., 2017. The Routledge Companion to Tax Avoidance

Research. Routledge.

Higgins, T., 2014. Income contingent loans: Theory, practice and prospects. Springer.

Hodgson, H. and Pearce, P., 2015. TravelSmart or travel tax breaks: is the fringe benefits tax

a barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), p.819.

Littlewood, M. and Elliffe, C. eds., 2017. Capital Gains Taxation: A Comparative Analysis of

Key Issues. Edward Elgar Publishing.

McGregor-Lowndes, M., 2016. Lawyers, reform and regulation in the Australian third

sector. Third Sector Review, 22(2), p.33.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.