Comprehensive Report on Taxation Theory, Practice & Law: CGT & FBT

VerifiedAdded on 2023/06/07

|13

|2845

|375

Report

AI Summary

This report provides a legal analysis of Capital Gains Tax (CGT) consequences related to the disposal of capital assets, assuming the taxpayer isn't involved in trading these assets as a business. It covers various assets including vacant land, antique beds, paintings, shares, and violins, detailing CGT implications based on purchase dates and threshold values. The report also examines Fringe Benefit Tax (FBT) implications for car fringe benefits, loan fringe benefits, and expense fringe benefits provided to an employee, Jasmine, by her employer, Rapid Heat Pty Ltd, calculating FBT payable amounts. The report further explores potential tax deductions related to loan usage and concludes with a discussion on how certain actions can increase tax deductions.

Taxation Theory, Practice & Law

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

A legal advice is required to be extended to the client for the relevant Capital Gains Tax (CGT)

consequences that would be occurred because of the disposal of the capital assets of taxpayer.

Further, the assumption has been made that taxpayer does not involve in running a business of

trading these capital assets and hence, the taxation implication is applicable here is to treat the

given proceeds not to assessable income under s. 6-5 ITAA 1997 (Gilders, et. al., 2015). This is

because the taxpayer is producing the capital proceeds from the disposal of capital assets and

these are not taxable. Thus, the only potential tax liability is related to the capital gains or loss

realised by the taxpayer.

Asset: Vacant Land Block

Taxpayer who has sold pre-CGT assets is exempted from CGT liability (s. 149 (10) ITAA 1997)

(Austlii, 2018 a). It is because the pre-CGT assets are those which have been purchased earlier

than September 20, 1985 when there was no CGT implication (Deutsch, et.al., 2015). Therefore,

any asset which does not belong to pre-CGT asset will be held taken for capital gains/loss and

thus, CGT liabilities would potentially result (Coleman, 2016).

Further, the selling of capital assets as per the given underlying situation is categorised under A1

CGT events. This includes the procedure that cost base (sum of associated costs of the asset) will

be deducted from the net income generated from sale so as to get the net capital gains/loss

(s.110-25, ITAA 1997). The cost base is comprised of the below highlighted elements (s.110-

25(1), ITAA 1997) (Austlii, 2018 b).

1) Cost incurred to purchase asset

2) Incidental costs like stamp duty, legal fees when the asset purchase or sale is done.

3) Cost for retaining the ownership (Taxes and interest cost if loan assumed for purchase of

asset)

4) Cost for enhancing of preserving the net worth of asset (capital expenses)

5) Cost for protecting the title of asset (capital expenses)

1

A legal advice is required to be extended to the client for the relevant Capital Gains Tax (CGT)

consequences that would be occurred because of the disposal of the capital assets of taxpayer.

Further, the assumption has been made that taxpayer does not involve in running a business of

trading these capital assets and hence, the taxation implication is applicable here is to treat the

given proceeds not to assessable income under s. 6-5 ITAA 1997 (Gilders, et. al., 2015). This is

because the taxpayer is producing the capital proceeds from the disposal of capital assets and

these are not taxable. Thus, the only potential tax liability is related to the capital gains or loss

realised by the taxpayer.

Asset: Vacant Land Block

Taxpayer who has sold pre-CGT assets is exempted from CGT liability (s. 149 (10) ITAA 1997)

(Austlii, 2018 a). It is because the pre-CGT assets are those which have been purchased earlier

than September 20, 1985 when there was no CGT implication (Deutsch, et.al., 2015). Therefore,

any asset which does not belong to pre-CGT asset will be held taken for capital gains/loss and

thus, CGT liabilities would potentially result (Coleman, 2016).

Further, the selling of capital assets as per the given underlying situation is categorised under A1

CGT events. This includes the procedure that cost base (sum of associated costs of the asset) will

be deducted from the net income generated from sale so as to get the net capital gains/loss

(s.110-25, ITAA 1997). The cost base is comprised of the below highlighted elements (s.110-

25(1), ITAA 1997) (Austlii, 2018 b).

1) Cost incurred to purchase asset

2) Incidental costs like stamp duty, legal fees when the asset purchase or sale is done.

3) Cost for retaining the ownership (Taxes and interest cost if loan assumed for purchase of

asset)

4) Cost for enhancing of preserving the net worth of asset (capital expenses)

5) Cost for protecting the title of asset (capital expenses)

1

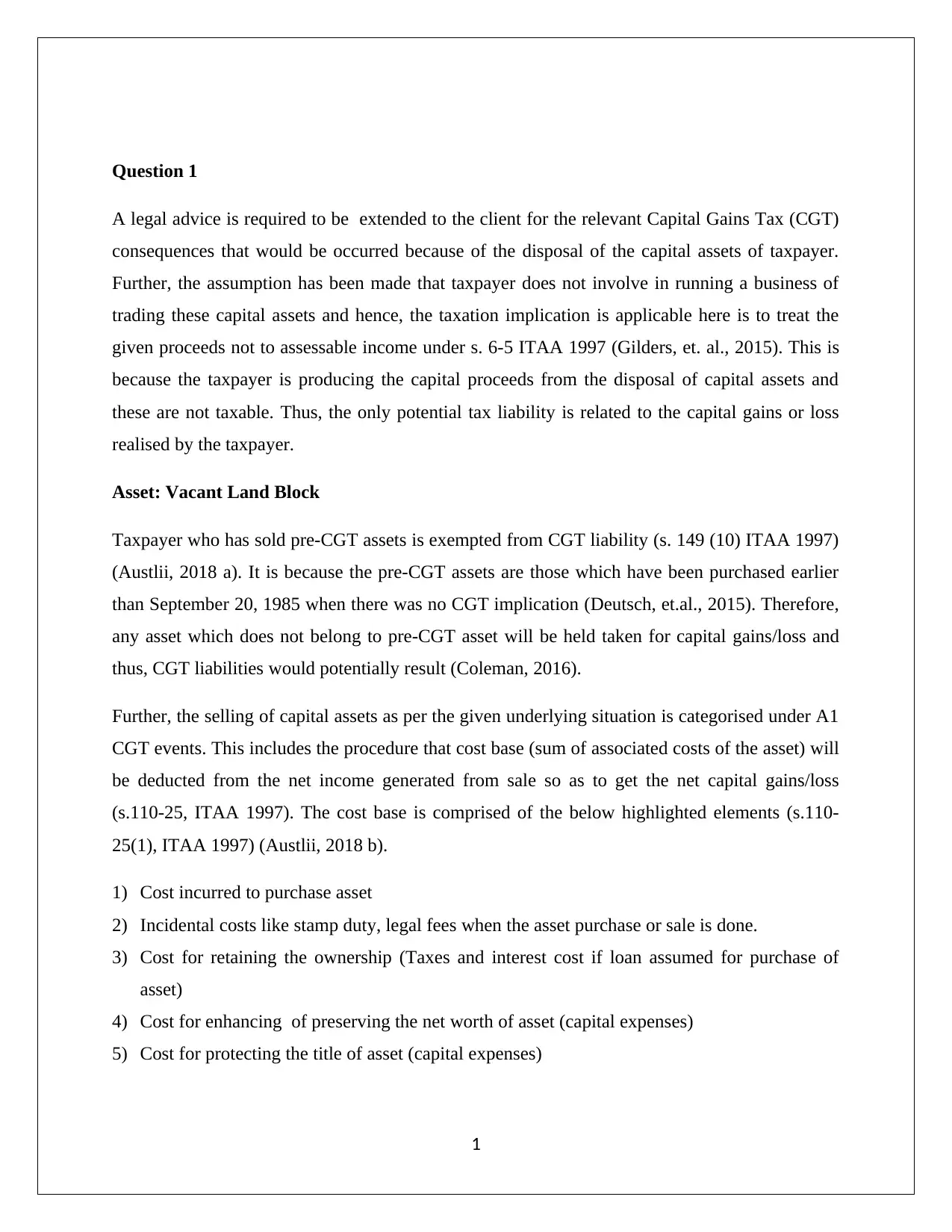

It may be possible that there are some capital losses from last years that are unbalanced and

hence, it would be essential to adjust theses capital losses from the derived capital gains.

The capital assets which are held by taxpayer for a period higher than one complete income year

yields long term capital gains/losses and Division 115 ITAA 1997 would provide a rebate of

50% on capital gains before CGT consequences are levied.

TR 94/29 implies that income from sale will be used for capital gains/losses computation for the

given year in which the taxpayer has signed the agreement of sale of asset (ATO, 1994). There

will be no effect of the fact that the income is expected to receive in next year and in actual the

taxpayer did not get the income from sale.

Block of Land

Asset: Antique Bed

Collectables in their ambit also include the antique items and the capital gains derived from sale

will only be subject to CGT liability when the buying has been done for more than $500 on

behalf of the taxpayer (Barkoczy, 2017). Taxpayer has been bought the antique bed for $3500 on

July 21, 1986 clearly this is not a pre-CGT asset and is purchased higher than the threshold value

of $500.

2

hence, it would be essential to adjust theses capital losses from the derived capital gains.

The capital assets which are held by taxpayer for a period higher than one complete income year

yields long term capital gains/losses and Division 115 ITAA 1997 would provide a rebate of

50% on capital gains before CGT consequences are levied.

TR 94/29 implies that income from sale will be used for capital gains/losses computation for the

given year in which the taxpayer has signed the agreement of sale of asset (ATO, 1994). There

will be no effect of the fact that the income is expected to receive in next year and in actual the

taxpayer did not get the income from sale.

Block of Land

Asset: Antique Bed

Collectables in their ambit also include the antique items and the capital gains derived from sale

will only be subject to CGT liability when the buying has been done for more than $500 on

behalf of the taxpayer (Barkoczy, 2017). Taxpayer has been bought the antique bed for $3500 on

July 21, 1986 clearly this is not a pre-CGT asset and is purchased higher than the threshold value

of $500.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

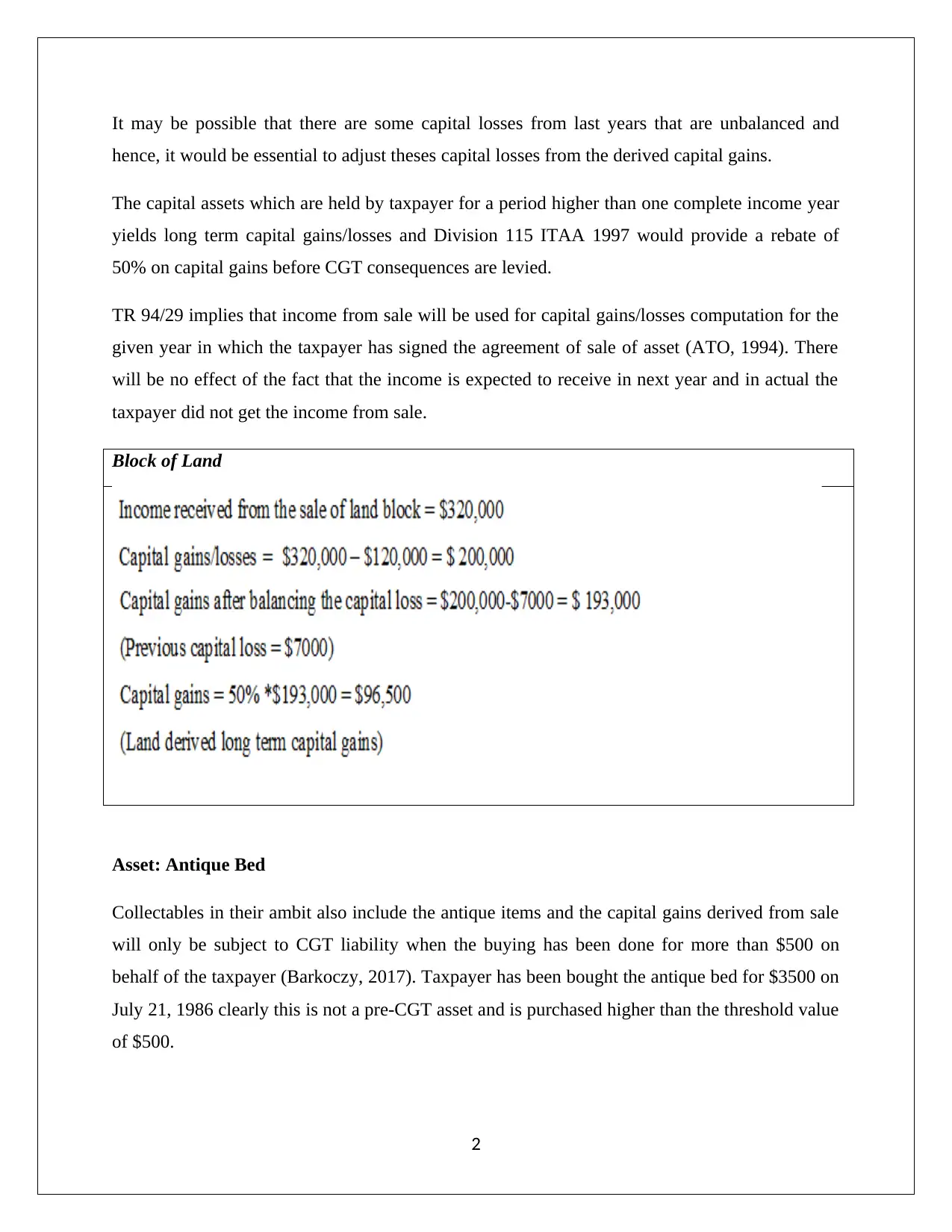

Therefore, the capital asset sale will be taken for CGT. The sale of collectable (antique bed) is

also a capital event A1.The taxpayer’s antique bed is stolen and she has received the claim from

insurance amount and hence, this amount will be assumed to be the sale proceeds from antique

bed for computation of capital gains/losses.

Antique Bed

Asset: Painting

The painting is pre-CGT asset since the taxpayer has made the purchase of painting on May, 2.

1985 that is prior to September 20, 1985 (s. 149(10), ITAA 1997). The capital proceeds will not

contribute to the total taxable capital gains of taxpayer and therefore, CGT liability will be

exempted in this case (Wilmot, 2014).

Asset: Shares

The shares are not classified as pre-CGT assets because taxpayer has been made the purchase of

shares after September 19, 1985 (s. 149(10), ITAA 1997). Also, the shares disposal will be

termed as capital event A1 and cost base and capital gains/loss is computed below. Further,

3

also a capital event A1.The taxpayer’s antique bed is stolen and she has received the claim from

insurance amount and hence, this amount will be assumed to be the sale proceeds from antique

bed for computation of capital gains/losses.

Antique Bed

Asset: Painting

The painting is pre-CGT asset since the taxpayer has made the purchase of painting on May, 2.

1985 that is prior to September 20, 1985 (s. 149(10), ITAA 1997). The capital proceeds will not

contribute to the total taxable capital gains of taxpayer and therefore, CGT liability will be

exempted in this case (Wilmot, 2014).

Asset: Shares

The shares are not classified as pre-CGT assets because taxpayer has been made the purchase of

shares after September 19, 1985 (s. 149(10), ITAA 1997). Also, the shares disposal will be

termed as capital event A1 and cost base and capital gains/loss is computed below. Further,

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

based on the underlying holding period of each of these shares, capital gains concession as

highlighted in s.115-25 ITAA 1997 has been applied (Deutsch, et.al., 2015).

Three shares have generated long term capital gains and as a result of this, the capital gains will

be granted 50% rebate. While no rebate will be applicable for Share Built because it has

generated short term capital gains (Sadiq, et.al., 2015).

4

highlighted in s.115-25 ITAA 1997 has been applied (Deutsch, et.al., 2015).

Three shares have generated long term capital gains and as a result of this, the capital gains will

be granted 50% rebate. While no rebate will be applicable for Share Built because it has

generated short term capital gains (Sadiq, et.al., 2015).

4

Asset: Violin

It is essential to determine whether violin is a personal use asset or collectable. There are

sufficient witness present to conclude that violin is not a collectable and belongs to personal use

asset of taxpayer (Coleman, 2016).

She is a collector of musical instruments.

She collects various violins for the collection.

She plays violin regularly.

She plays is very well and plays for entertainment.

Based on above, it would be fair to say that violin is personal asset. Also, she has made the

payment for purchase after September 19, 1985 and this does not belong to pre-CGT asset

(Gilders, et. al., 2015). Moreover, the imperative condition for CGT application for personal

asset is that the payment for purchase of the asset must be greater than the threshold amount.

The threshold amount is $10,000. Taxpayer has made the payment of $5,500 which implies that

the amount of purchase does not cross the threshold value and hence, the CGT will be exempted

in case of sale of violin.

Capital gains/losses

The final computation table would be made that would represent the CGT consequences of the

taxpayer for year ending June 30, 2018.

Block of vacant land $96,500

Antique bed $2,250

Painting -

Shares $40,350

Violin -

Net capital gains = $139,100

5

It is essential to determine whether violin is a personal use asset or collectable. There are

sufficient witness present to conclude that violin is not a collectable and belongs to personal use

asset of taxpayer (Coleman, 2016).

She is a collector of musical instruments.

She collects various violins for the collection.

She plays violin regularly.

She plays is very well and plays for entertainment.

Based on above, it would be fair to say that violin is personal asset. Also, she has made the

payment for purchase after September 19, 1985 and this does not belong to pre-CGT asset

(Gilders, et. al., 2015). Moreover, the imperative condition for CGT application for personal

asset is that the payment for purchase of the asset must be greater than the threshold amount.

The threshold amount is $10,000. Taxpayer has made the payment of $5,500 which implies that

the amount of purchase does not cross the threshold value and hence, the CGT will be exempted

in case of sale of violin.

Capital gains/losses

The final computation table would be made that would represent the CGT consequences of the

taxpayer for year ending June 30, 2018.

Block of vacant land $96,500

Antique bed $2,250

Painting -

Shares $40,350

Violin -

Net capital gains = $139,100

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2

(a) The fringe benefit is extended to employee when the employer provides personal benefits to

their employee but not in the form of cash. The Fringe Benefit Tax (FBT) is separate from

personal income tax and is applied on the employer. The various factors associated with the

fringe benefits are discussed in Fringe Benefits Assessment Act 1986. It is also important to

see that employee who receives and uses the benefits is free for FBT liability which means

he/she does not need to pay the FBT payable amount.

There are host of personal benefits which the employer provides to employee in the form of

fringe benefits. However, the respective fringe benefits in the present scenarios are discussed

below (Barkoczy, 2017).

“Car Fringe Benefits”

As the name suggests, the employer provides a vehicle (car) to employee so that the employee

can travel through the car for personal works. When the scope of use of car is increased from

office work to personal work then only car fringe benefit has been given to employee from

employer as per the outlines of s.7, FBTAA 1986.

Jasmine is an employee of Rapid Heat Pty Ltd. On May 1, 2017, Rapid Heat provides car to

Jasmine that she can travel for personal work as well as for office work. It will be fair to say that

employer has provides car fringe benefits to Jasmine and the FBT liability will be resulted on

employer. The employer has also given the expenses ($550) which are occurred because of the

repairing (minor) on car when the car was at garage. There is zero participation on behalf of

Jasmine while purchasing the car on May 1, 2017 and thus, the amount of $33,000 has been

given by employer only. The FBT liability for car fringe benefit requires the following factors

which are highlighted below.

Base Value

6

(a) The fringe benefit is extended to employee when the employer provides personal benefits to

their employee but not in the form of cash. The Fringe Benefit Tax (FBT) is separate from

personal income tax and is applied on the employer. The various factors associated with the

fringe benefits are discussed in Fringe Benefits Assessment Act 1986. It is also important to

see that employee who receives and uses the benefits is free for FBT liability which means

he/she does not need to pay the FBT payable amount.

There are host of personal benefits which the employer provides to employee in the form of

fringe benefits. However, the respective fringe benefits in the present scenarios are discussed

below (Barkoczy, 2017).

“Car Fringe Benefits”

As the name suggests, the employer provides a vehicle (car) to employee so that the employee

can travel through the car for personal works. When the scope of use of car is increased from

office work to personal work then only car fringe benefit has been given to employee from

employer as per the outlines of s.7, FBTAA 1986.

Jasmine is an employee of Rapid Heat Pty Ltd. On May 1, 2017, Rapid Heat provides car to

Jasmine that she can travel for personal work as well as for office work. It will be fair to say that

employer has provides car fringe benefits to Jasmine and the FBT liability will be resulted on

employer. The employer has also given the expenses ($550) which are occurred because of the

repairing (minor) on car when the car was at garage. There is zero participation on behalf of

Jasmine while purchasing the car on May 1, 2017 and thus, the amount of $33,000 has been

given by employer only. The FBT liability for car fringe benefit requires the following factors

which are highlighted below.

Base Value

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is also termed as capital value of car and will be computed based on the buying cost and

associated expenses which are paid by employer during the utilization of car by employee.

Base value ¿( $ 33000−$ 550)=$ 32 , 450

Statutory %

This percentage will be flat 20% when the car is purchased after the threshold year which is

2011. Here also, car is purchased after threshold year which is on 2017 and hence, the applicable

statutory % is 20%.

Available car days

It has been assumed that employee has started using the car on the same day on which the car has

provided to employee.

Starting day: May 1, 2017

Till: 31 March, 2018

Available days = 335 days

Moreover, the noteworthy aspect is that car is at garage for repairing and these five days will not

reduce the net available days because the car is sent only for minor repairing not for major

repairs (Nethercott, Richardson and Devos, 2016). Furthermore, Jasmine went out of city and

she parked the car at airport for ten days, here the net available days will not reduce by 10 days

as she had the availability towards the car. Therefore,

The net available days will be 335 days.

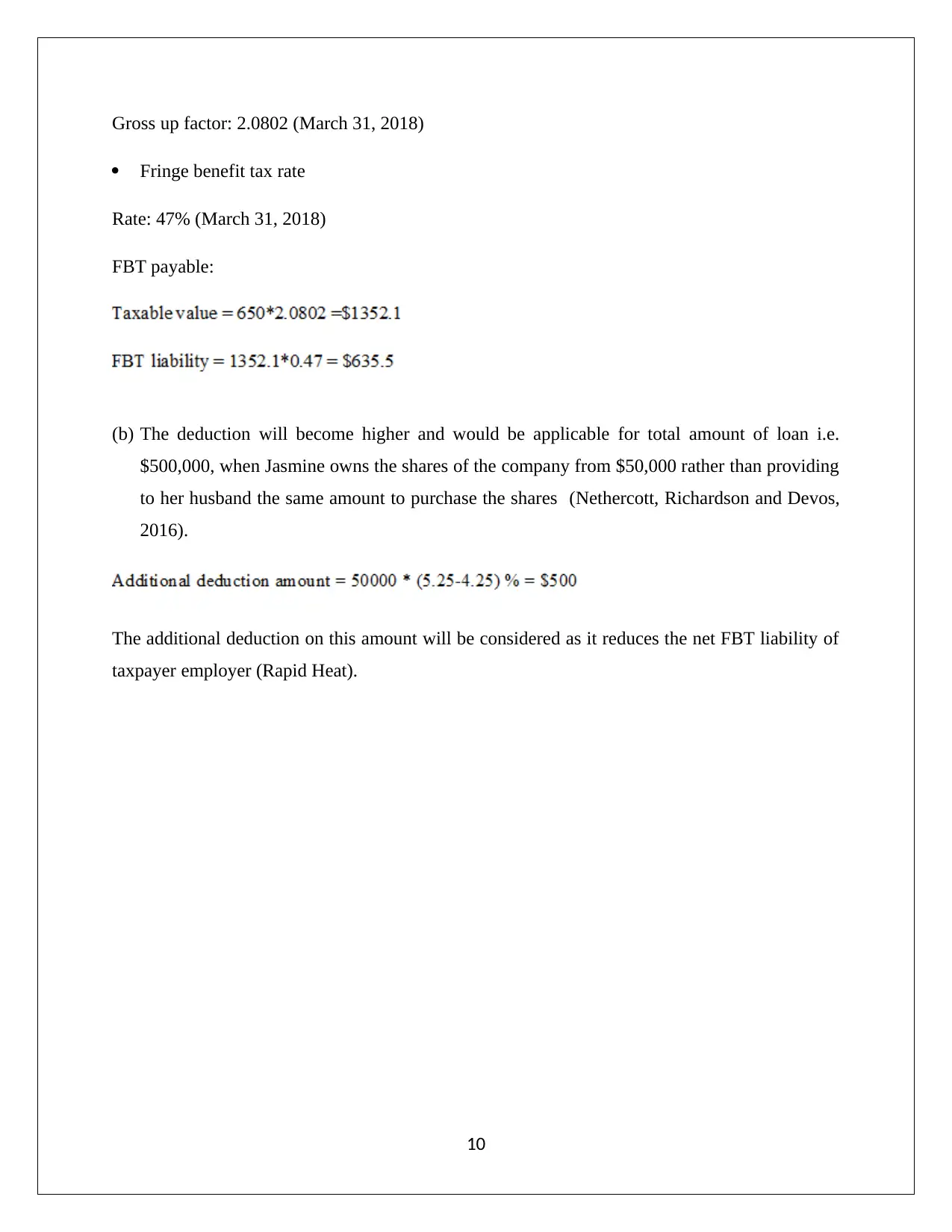

Gross up factor

Car: TYPE I Goods (Under Goods and Service Act 1999)

Gross up factor: 2.0802 (March 31, 2018)

Fringe benefit tax rate

Rate: 47% (March 31, 2018)

7

associated expenses which are paid by employer during the utilization of car by employee.

Base value ¿( $ 33000−$ 550)=$ 32 , 450

Statutory %

This percentage will be flat 20% when the car is purchased after the threshold year which is

2011. Here also, car is purchased after threshold year which is on 2017 and hence, the applicable

statutory % is 20%.

Available car days

It has been assumed that employee has started using the car on the same day on which the car has

provided to employee.

Starting day: May 1, 2017

Till: 31 March, 2018

Available days = 335 days

Moreover, the noteworthy aspect is that car is at garage for repairing and these five days will not

reduce the net available days because the car is sent only for minor repairing not for major

repairs (Nethercott, Richardson and Devos, 2016). Furthermore, Jasmine went out of city and

she parked the car at airport for ten days, here the net available days will not reduce by 10 days

as she had the availability towards the car. Therefore,

The net available days will be 335 days.

Gross up factor

Car: TYPE I Goods (Under Goods and Service Act 1999)

Gross up factor: 2.0802 (March 31, 2018)

Fringe benefit tax rate

Rate: 47% (March 31, 2018)

7

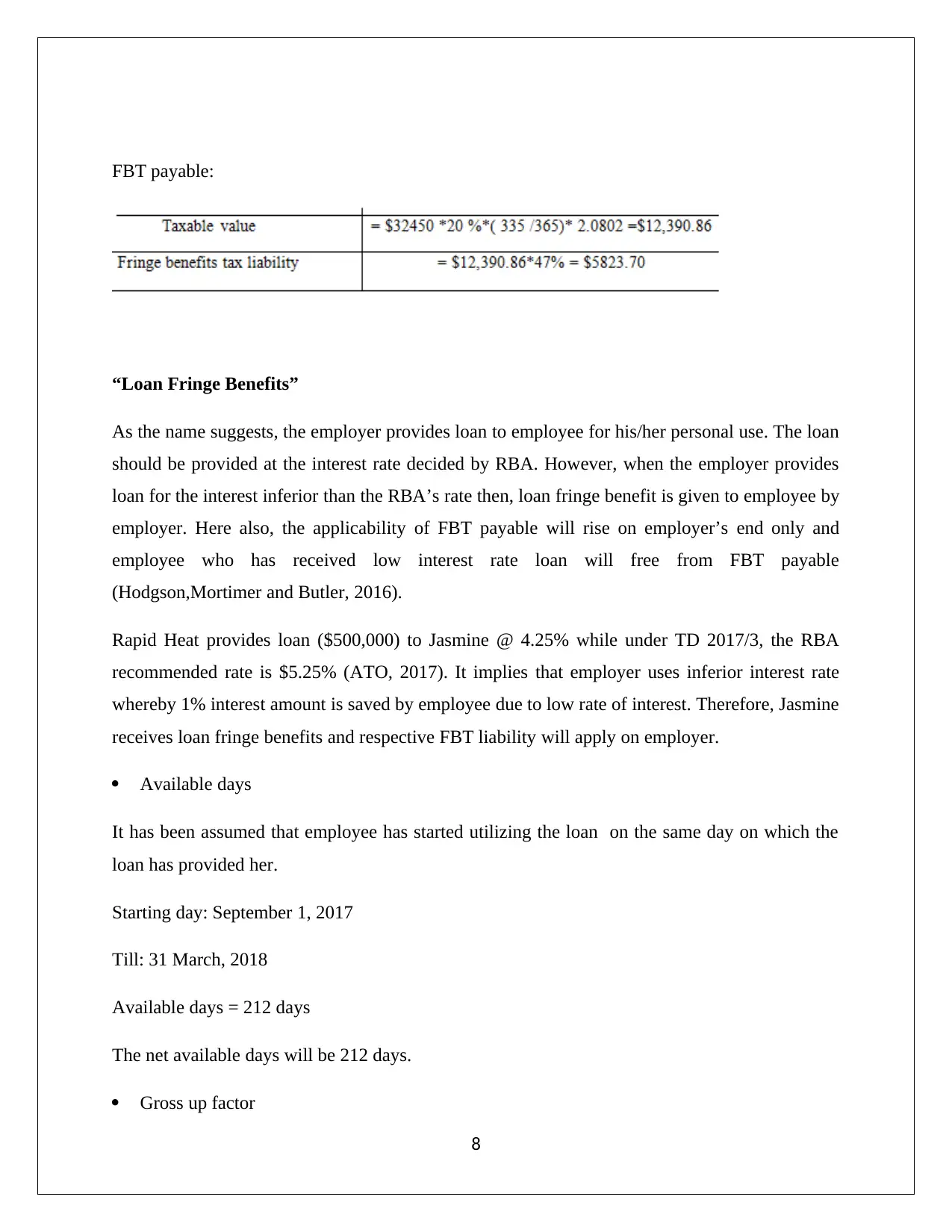

FBT payable:

“Loan Fringe Benefits”

As the name suggests, the employer provides loan to employee for his/her personal use. The loan

should be provided at the interest rate decided by RBA. However, when the employer provides

loan for the interest inferior than the RBA’s rate then, loan fringe benefit is given to employee by

employer. Here also, the applicability of FBT payable will rise on employer’s end only and

employee who has received low interest rate loan will free from FBT payable

(Hodgson,Mortimer and Butler, 2016).

Rapid Heat provides loan ($500,000) to Jasmine @ 4.25% while under TD 2017/3, the RBA

recommended rate is $5.25% (ATO, 2017). It implies that employer uses inferior interest rate

whereby 1% interest amount is saved by employee due to low rate of interest. Therefore, Jasmine

receives loan fringe benefits and respective FBT liability will apply on employer.

Available days

It has been assumed that employee has started utilizing the loan on the same day on which the

loan has provided her.

Starting day: September 1, 2017

Till: 31 March, 2018

Available days = 212 days

The net available days will be 212 days.

Gross up factor

8

“Loan Fringe Benefits”

As the name suggests, the employer provides loan to employee for his/her personal use. The loan

should be provided at the interest rate decided by RBA. However, when the employer provides

loan for the interest inferior than the RBA’s rate then, loan fringe benefit is given to employee by

employer. Here also, the applicability of FBT payable will rise on employer’s end only and

employee who has received low interest rate loan will free from FBT payable

(Hodgson,Mortimer and Butler, 2016).

Rapid Heat provides loan ($500,000) to Jasmine @ 4.25% while under TD 2017/3, the RBA

recommended rate is $5.25% (ATO, 2017). It implies that employer uses inferior interest rate

whereby 1% interest amount is saved by employee due to low rate of interest. Therefore, Jasmine

receives loan fringe benefits and respective FBT liability will apply on employer.

Available days

It has been assumed that employee has started utilizing the loan on the same day on which the

loan has provided her.

Starting day: September 1, 2017

Till: 31 March, 2018

Available days = 212 days

The net available days will be 212 days.

Gross up factor

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

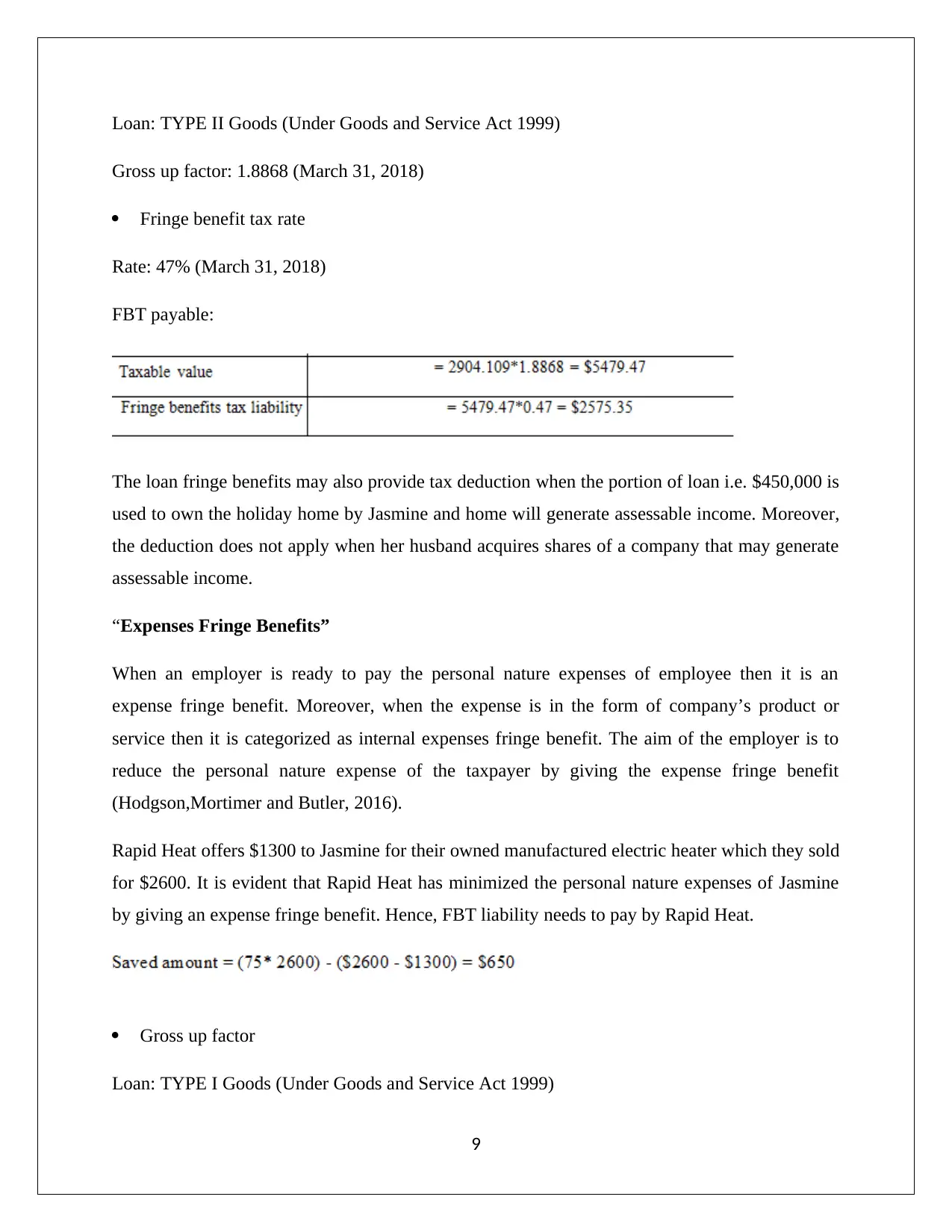

Loan: TYPE II Goods (Under Goods and Service Act 1999)

Gross up factor: 1.8868 (March 31, 2018)

Fringe benefit tax rate

Rate: 47% (March 31, 2018)

FBT payable:

The loan fringe benefits may also provide tax deduction when the portion of loan i.e. $450,000 is

used to own the holiday home by Jasmine and home will generate assessable income. Moreover,

the deduction does not apply when her husband acquires shares of a company that may generate

assessable income.

“Expenses Fringe Benefits”

When an employer is ready to pay the personal nature expenses of employee then it is an

expense fringe benefit. Moreover, when the expense is in the form of company’s product or

service then it is categorized as internal expenses fringe benefit. The aim of the employer is to

reduce the personal nature expense of the taxpayer by giving the expense fringe benefit

(Hodgson,Mortimer and Butler, 2016).

Rapid Heat offers $1300 to Jasmine for their owned manufactured electric heater which they sold

for $2600. It is evident that Rapid Heat has minimized the personal nature expenses of Jasmine

by giving an expense fringe benefit. Hence, FBT liability needs to pay by Rapid Heat.

Gross up factor

Loan: TYPE I Goods (Under Goods and Service Act 1999)

9

Gross up factor: 1.8868 (March 31, 2018)

Fringe benefit tax rate

Rate: 47% (March 31, 2018)

FBT payable:

The loan fringe benefits may also provide tax deduction when the portion of loan i.e. $450,000 is

used to own the holiday home by Jasmine and home will generate assessable income. Moreover,

the deduction does not apply when her husband acquires shares of a company that may generate

assessable income.

“Expenses Fringe Benefits”

When an employer is ready to pay the personal nature expenses of employee then it is an

expense fringe benefit. Moreover, when the expense is in the form of company’s product or

service then it is categorized as internal expenses fringe benefit. The aim of the employer is to

reduce the personal nature expense of the taxpayer by giving the expense fringe benefit

(Hodgson,Mortimer and Butler, 2016).

Rapid Heat offers $1300 to Jasmine for their owned manufactured electric heater which they sold

for $2600. It is evident that Rapid Heat has minimized the personal nature expenses of Jasmine

by giving an expense fringe benefit. Hence, FBT liability needs to pay by Rapid Heat.

Gross up factor

Loan: TYPE I Goods (Under Goods and Service Act 1999)

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross up factor: 2.0802 (March 31, 2018)

Fringe benefit tax rate

Rate: 47% (March 31, 2018)

FBT payable:

(b) The deduction will become higher and would be applicable for total amount of loan i.e.

$500,000, when Jasmine owns the shares of the company from $50,000 rather than providing

to her husband the same amount to purchase the shares (Nethercott, Richardson and Devos,

2016).

The additional deduction on this amount will be considered as it reduces the net FBT liability of

taxpayer employer (Rapid Heat).

10

Fringe benefit tax rate

Rate: 47% (March 31, 2018)

FBT payable:

(b) The deduction will become higher and would be applicable for total amount of loan i.e.

$500,000, when Jasmine owns the shares of the company from $50,000 rather than providing

to her husband the same amount to purchase the shares (Nethercott, Richardson and Devos,

2016).

The additional deduction on this amount will be considered as it reduces the net FBT liability of

taxpayer employer (Rapid Heat).

10

References

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 25 September 2018)

ATO, (2017) Taxation Determination –TD 2017/3 [Online].

http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD%2FTD20173%2FNAT%2FATO

%2F00001%22 (Accessed: 25 September 2018)

Austlii, (2018 a) Income Tax Assessment Act 1997- SECT 149.10 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s149.10.html (Accessed: 25

September 2018)

Austlii, (2018 b) Income Tax Assessment Act 1997- SECT 110.25.General Rules About Cost

Base [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html (Accessed: 25

September 2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

11

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 25 September 2018)

ATO, (2017) Taxation Determination –TD 2017/3 [Online].

http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD%2FTD20173%2FNAT%2FATO

%2F00001%22 (Accessed: 25 September 2018)

Austlii, (2018 a) Income Tax Assessment Act 1997- SECT 149.10 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s149.10.html (Accessed: 25

September 2018)

Austlii, (2018 b) Income Tax Assessment Act 1997- SECT 110.25.General Rules About Cost

Base [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html (Accessed: 25

September 2018)

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.