CLWM4100 Taxation Law Assessment: CGT, Capital Gains and Losses Report

VerifiedAdded on 2022/08/21

|7

|1064

|11

Report

AI Summary

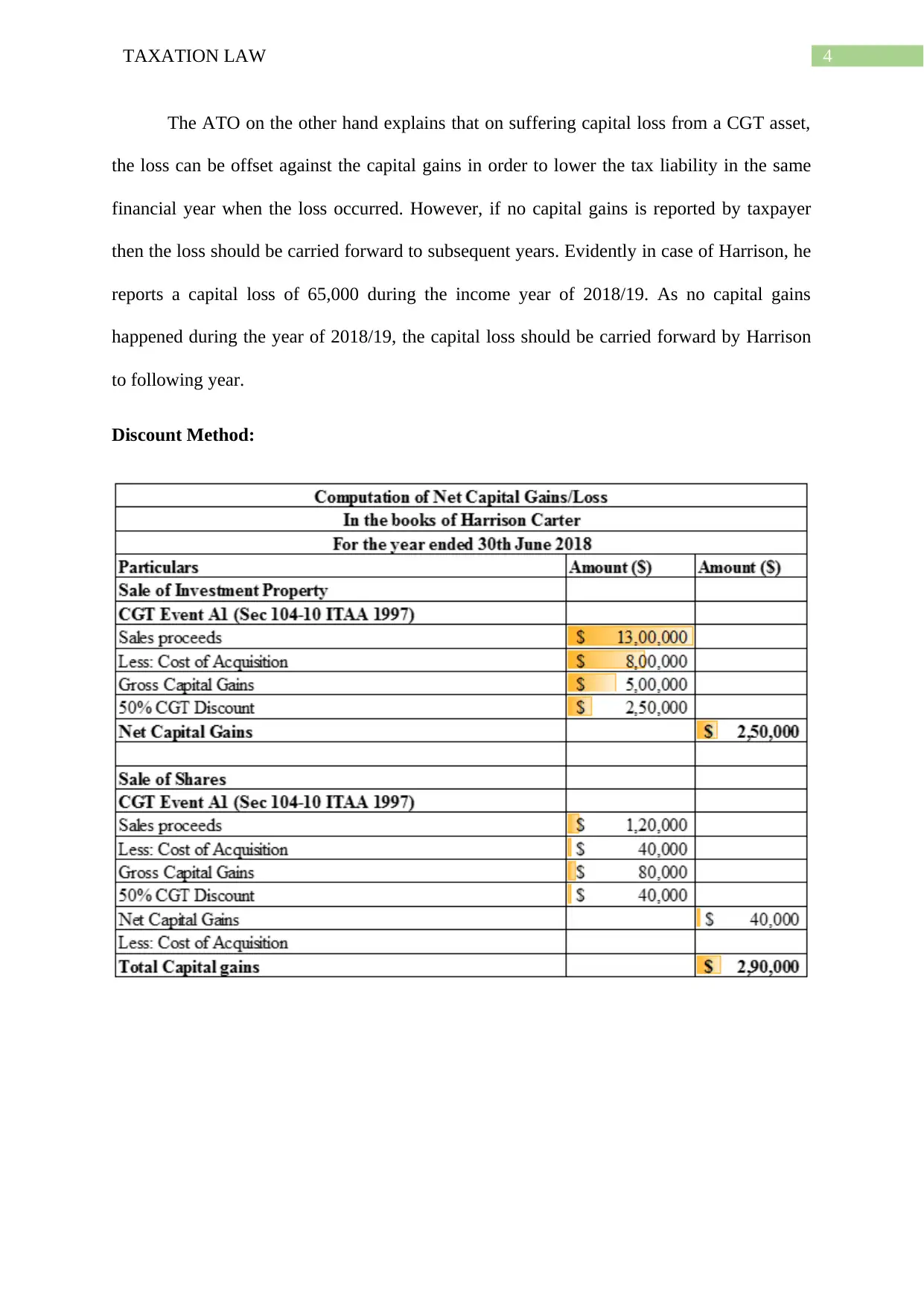

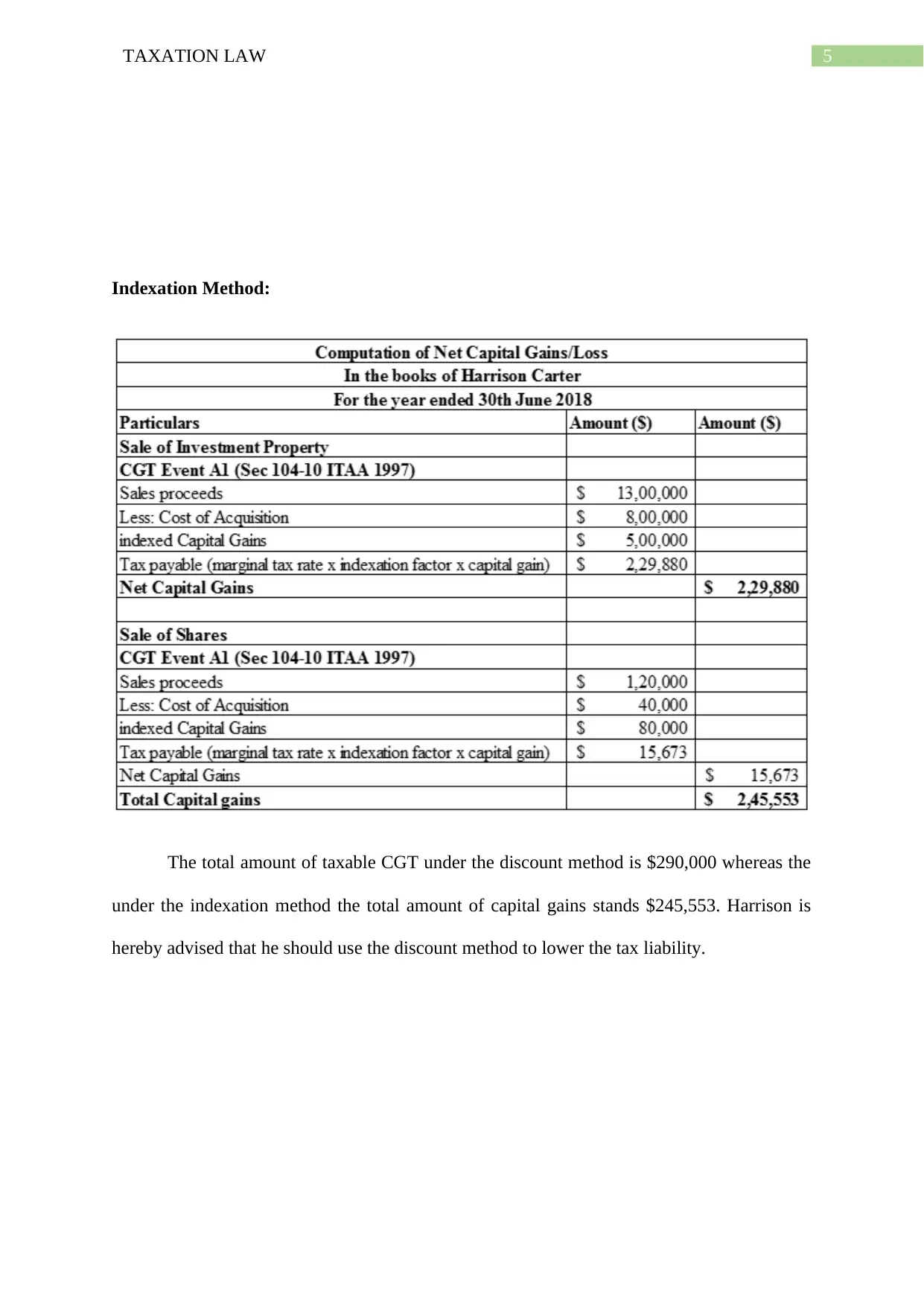

This report addresses a taxation law case study, focusing on the timing of a CGT event and the calculation of capital gains and losses. Part 1 explains the timing of a CGT event, referencing relevant sections of the ITAA 1997 and case law. Part 2 advises on the net capital gains or losses to be included in Harrison Carter's tax return for the years ending 2018 and 2019, including calculations using both discount and indexation methods. The report analyzes the sale of an investment property and the acquisition of shares, determining the applicable CGT event dates. It also covers the offsetting of capital losses. The report concludes with a recommendation on the most advantageous method for calculating capital gains to minimize tax liability. The report provides a comprehensive analysis of CGT implications for an Australian resident.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.