Corporate Accounting & Reporting: CGU & Goodwill Impairment Loss

VerifiedAdded on 2023/06/16

|8

|1328

|317

Report

AI Summary

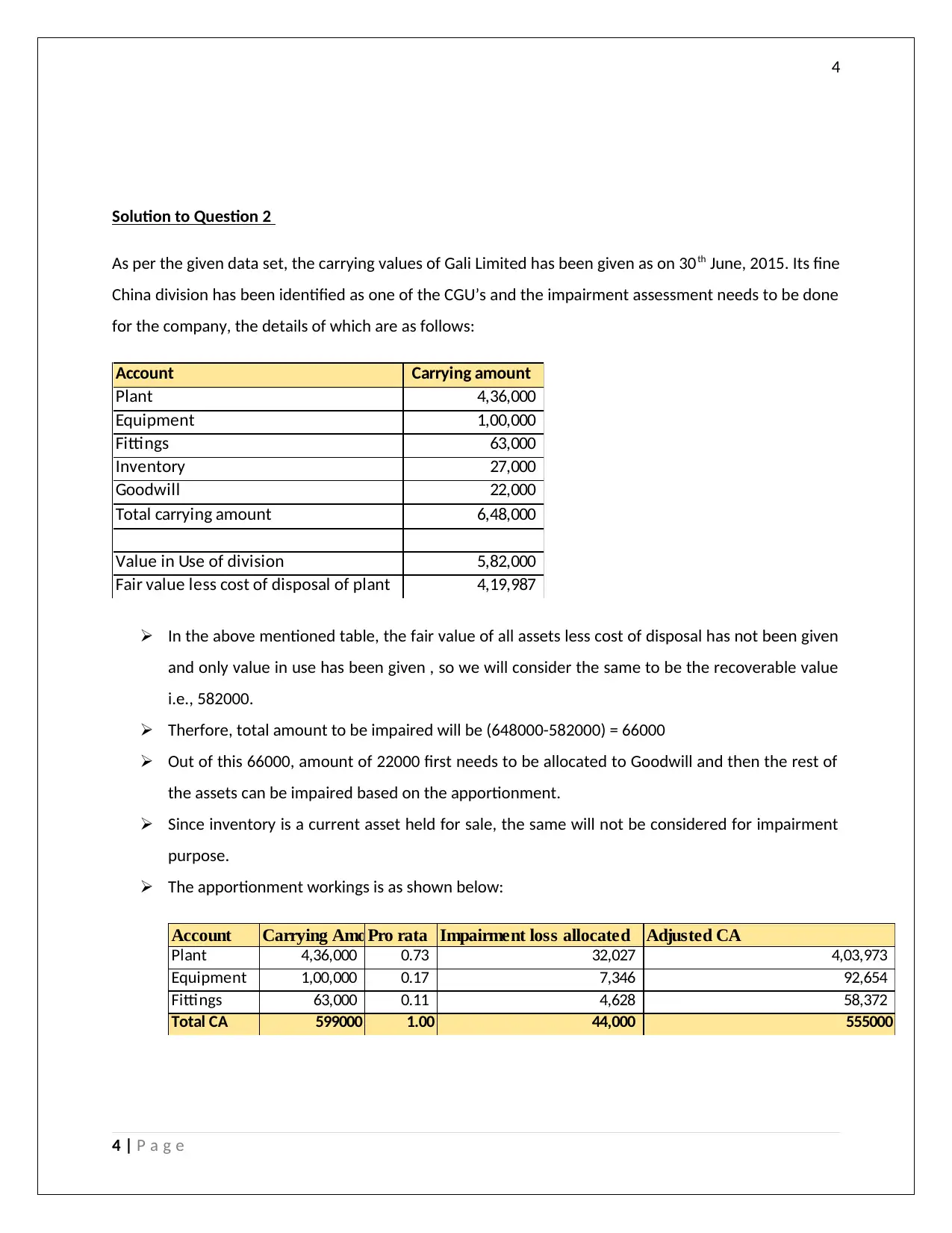

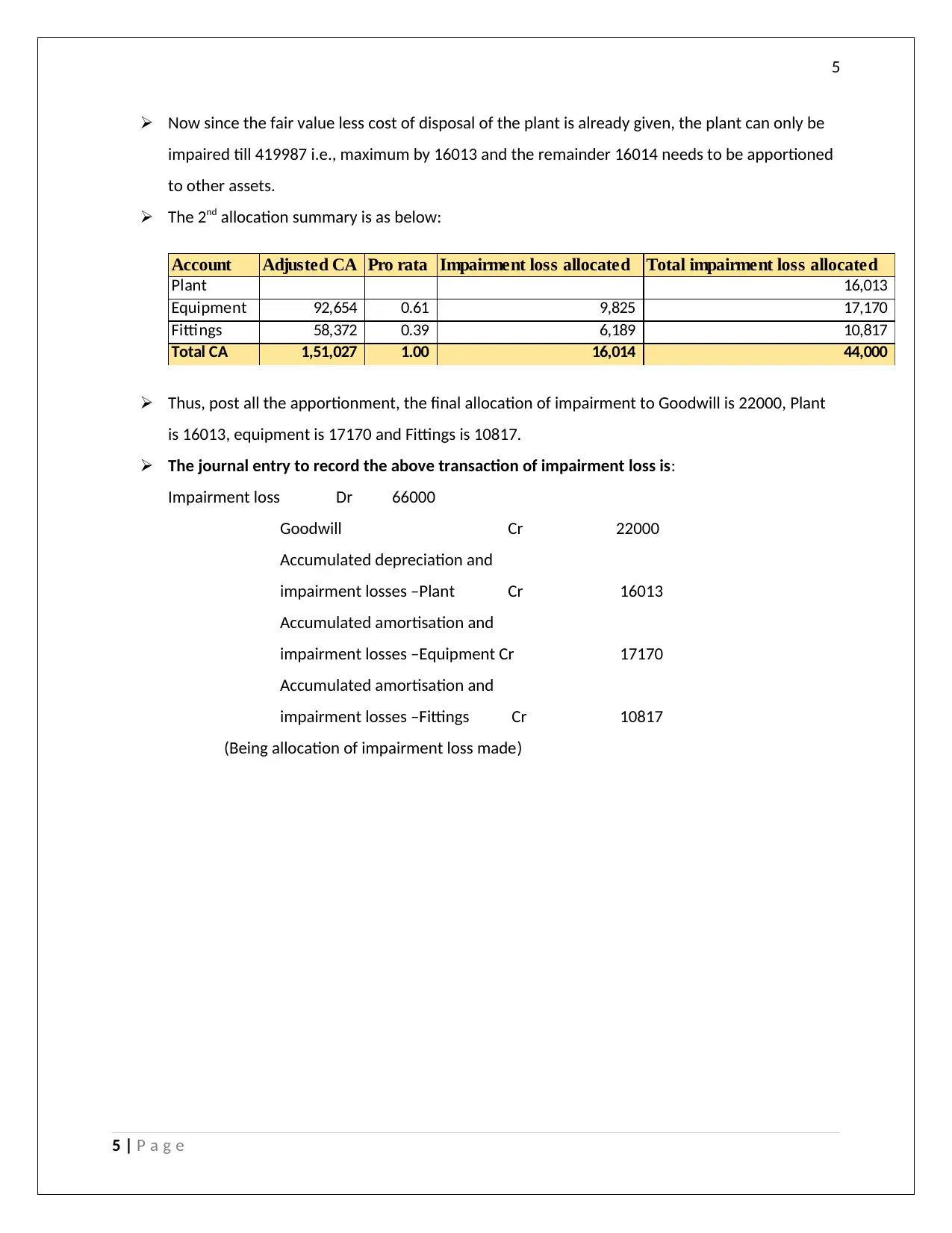

This report provides a detailed analysis of impairment loss in corporate accounting and reporting, focusing on the application of IAS 36 and the specific considerations for Cash Generating Units (CGUs) including goodwill. It addresses the recognition, measurement, and allocation of impairment losses, particularly in the context of CGUs. The report includes a solution to a specific question involving Gali Limited's fine China division, demonstrating the step-by-step process of calculating and allocating impairment losses across various assets, including plant, equipment, fittings, inventory, and goodwill. The analysis emphasizes the importance of accurate valuation and the proper disclosure of management's estimates and assumptions in financial statements. The report concludes by summarizing the key considerations for impairment assessment and disclosure requirements.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.