Corporate Accounting: Detailed Report on Impairment Loss in CGUs

VerifiedAdded on 2023/04/23

|8

|1329

|103

Report

AI Summary

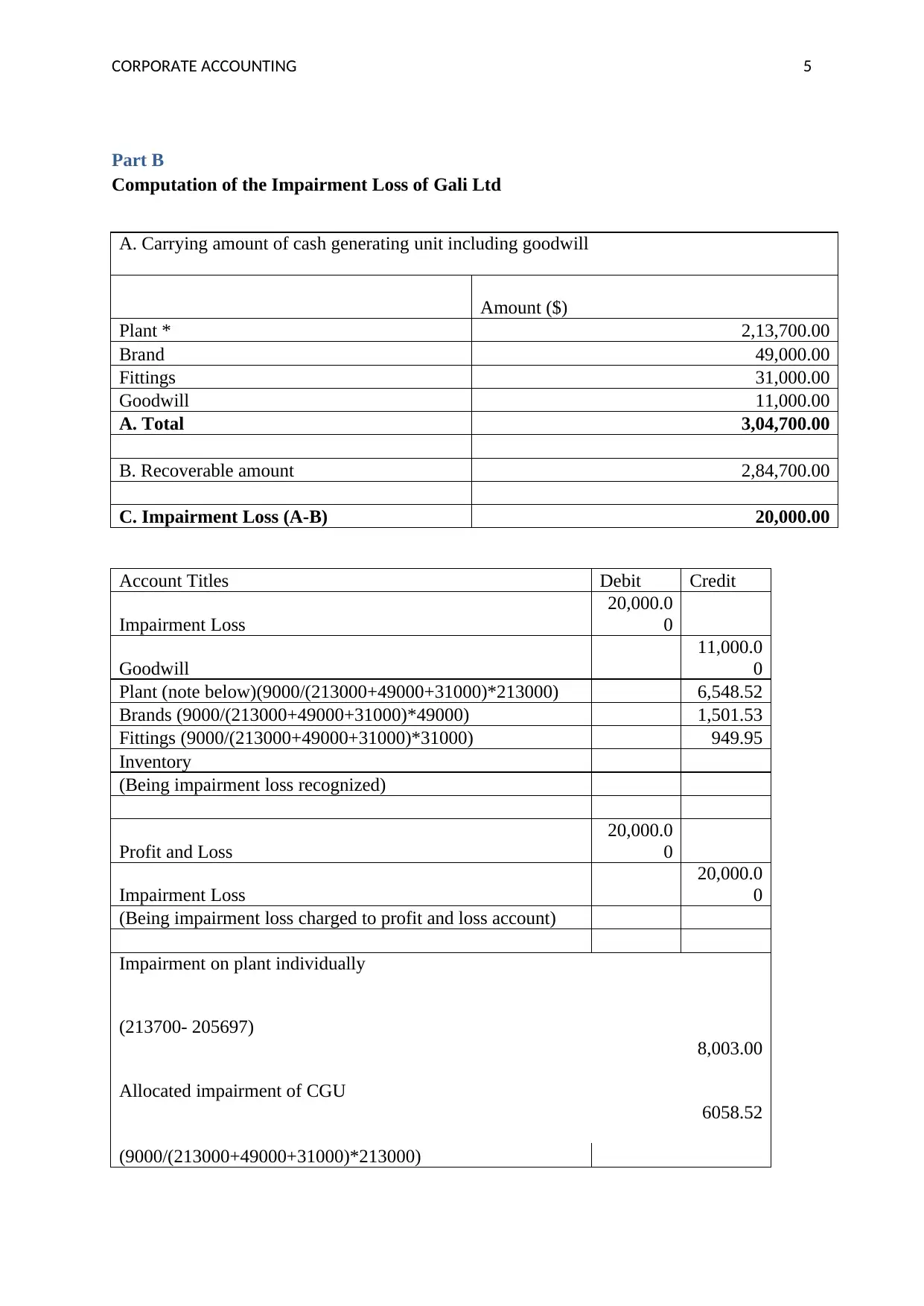

This report provides a comprehensive analysis of impairment loss in the context of cash generating units (CGUs), focusing on the relevant accounting standards and practical applications. It begins by defining impairment loss and its purpose, emphasizing the importance of revaluating assets to reflect their realizable value and prevent overvaluation in financial statements. The report distinguishes between impairment testing for individual assets and CGUs, highlighting the complexities involved in the latter. It discusses the allocation of goodwill in CGUs and the subsequent allocation of impairment loss to other assets based on their carrying amounts. A practical computation of impairment loss for Gali Ltd is included, demonstrating the application of these principles. The report concludes by reiterating the significance of impairment loss computation for accurate asset valuation and financial reporting. Desklib provides access to similar solved assignments and study resources.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.