Accounting for Impairment Loss: Analysis of Cash Generating Units

VerifiedAdded on 2023/06/11

|9

|1830

|485

Report

AI Summary

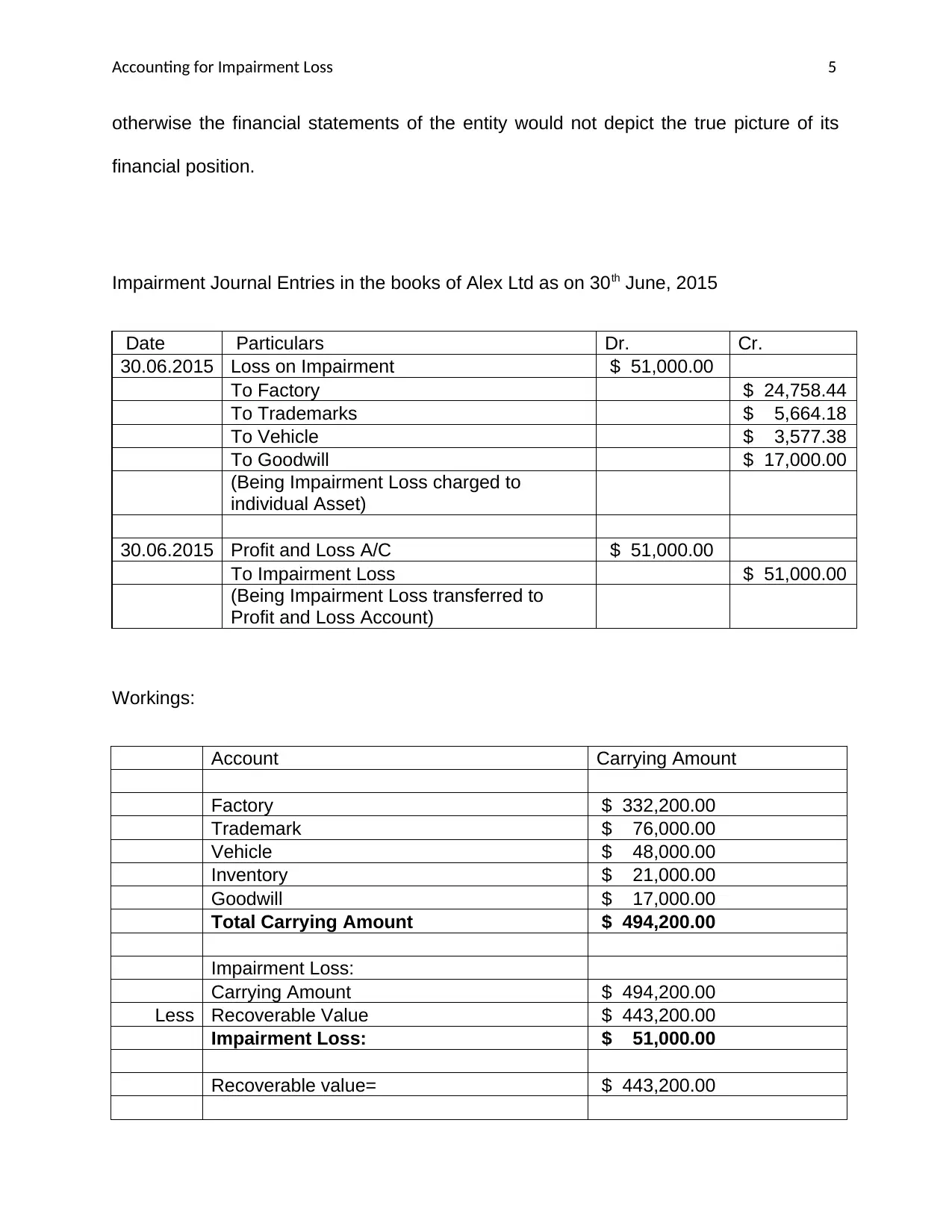

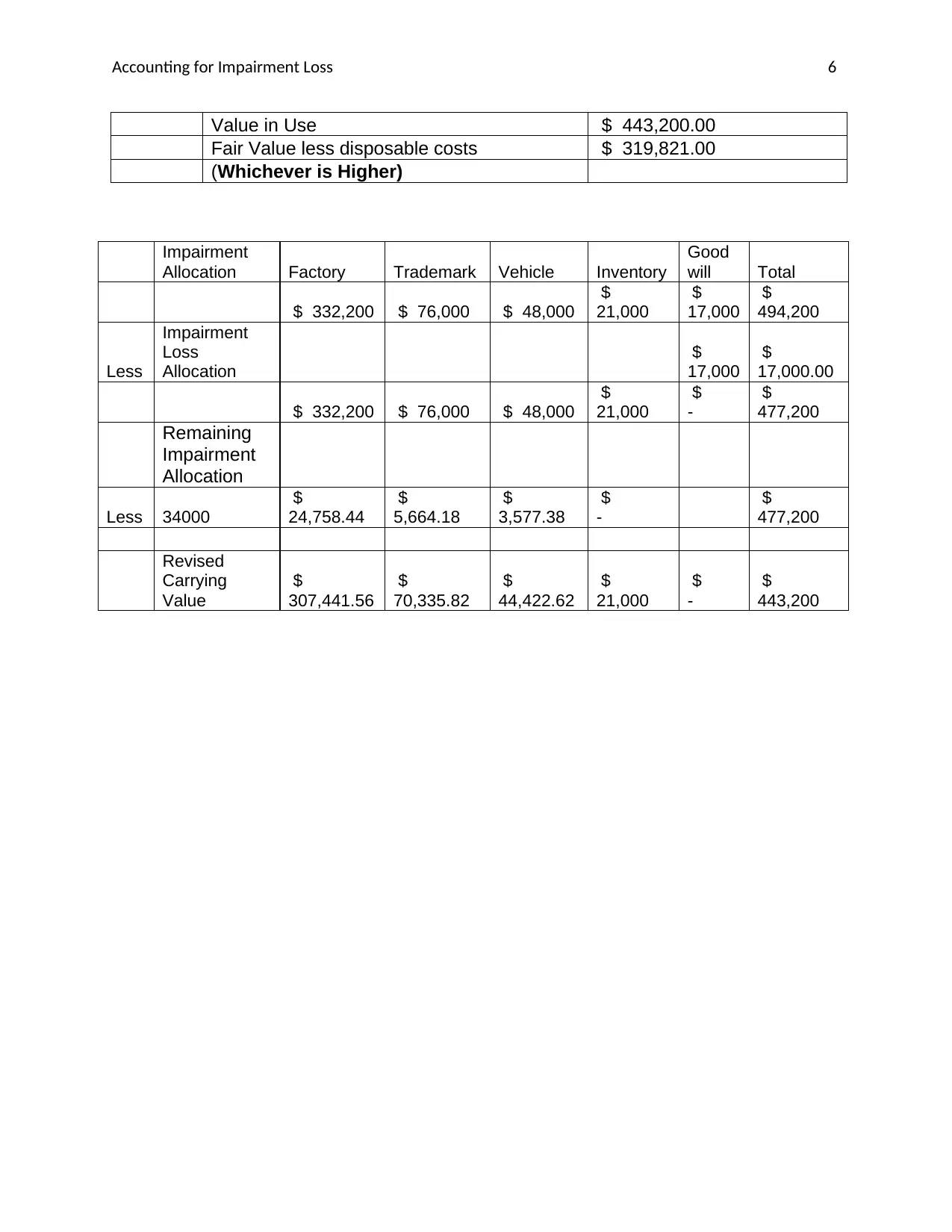

This report provides an overview of accounting for impairment loss on cash-generating units (CGUs) as per AASB 136 and IAS 36. It discusses the indicators of impairment, determination of recoverable value, and allocation of impairment loss. The report also covers specific judgments for identifying CGUs, the treatment of goodwill, and the annual impairment testing requirements for certain assets. Furthermore, it explains the journal entries for recording impairment loss and includes a practical example with calculations. The report concludes by emphasizing the importance of complying with accounting standards to accurately reflect the financial position of an entity. It also includes a discussion of disclosures that are required regarding impairment of loss like goodwill amount per CGU, impairment amount, method of valuation used for determining value in use and fair value, assumptions used to value the assets and the sensitivity analysis, if any, applied.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.