Accounting for Business: Challenger Ltd Financial Statement Analysis

VerifiedAdded on 2021/05/31

|15

|2510

|18

Report

AI Summary

This report provides a comprehensive financial analysis of Challenger Ltd, focusing on its performance evaluation through ratio analysis. The assignment computes and analyzes key financial ratios such as current ratio, quick ratio, net profit margin, return on equity, and return on assets for Challenger Ltd. Furthermore, the report conducts a comparative study, benchmarking Challenger Ltd against BBVA Group and Alliance Trust, both operating within the same industry. The analysis covers data from 2016 and 2017, highlighting the company's liquidity, profitability, and efficiency, and provides insights into its financial strengths and weaknesses relative to its competitors. The report concludes with a discussion on the implications of these findings and offers a comparative perspective on the financial health of the three companies, drawing conclusions based on the computed ratios and their trends.

Running head: ACCOUNTING FOR BUSINESS

ACCOUNTING FOR BUSINESS

Name of the Student:

Name of the University:

Student ID:

Company’s Name:

Author’s Note:

ACCOUNTING FOR BUSINESS

Name of the Student:

Name of the University:

Student ID:

Company’s Name:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING FOR BUSINESS

Executive Summary

The main purpose of this assignment is to analyze the financial statement of Challenger ltd and

also comment on the performance of the business. The assignment will be computing significant

ratio which are related to the performance of the business and analyze the same. The assignment

will also be comparing the different ratios which are computed for measuring the performance of

the business with other companies which belong to the same industry. The companies which are

selected for the purpose of comparison are BBVA Group and Alliance Trust ltd.

ACCOUNTING FOR BUSINESS

Executive Summary

The main purpose of this assignment is to analyze the financial statement of Challenger ltd and

also comment on the performance of the business. The assignment will be computing significant

ratio which are related to the performance of the business and analyze the same. The assignment

will also be comparing the different ratios which are computed for measuring the performance of

the business with other companies which belong to the same industry. The companies which are

selected for the purpose of comparison are BBVA Group and Alliance Trust ltd.

2

ACCOUNTING FOR BUSINESS

Table of Contents

1. Introduction..............................................................................................................................3

1.1 Purpose..............................................................................................................................3

1.2 Scope.................................................................................................................................3

1.3 Limitation..........................................................................................................................3

2.0 Company Overview...................................................................................................................3

3.0 Ratio Analysis............................................................................................................................4

3.1 Current Ratio.........................................................................................................................5

3.2 Quick Ratio............................................................................................................................6

3.3 Net Profit Margin...................................................................................................................6

3.4 Return on Equity....................................................................................................................7

3.5 Return on Assets....................................................................................................................7

Analysis and Comparison between Challenger ltd, BBVA Group and Alliance Trust...................8

Reference.......................................................................................................................................10

Appendix........................................................................................................................................12

ACCOUNTING FOR BUSINESS

Table of Contents

1. Introduction..............................................................................................................................3

1.1 Purpose..............................................................................................................................3

1.2 Scope.................................................................................................................................3

1.3 Limitation..........................................................................................................................3

2.0 Company Overview...................................................................................................................3

3.0 Ratio Analysis............................................................................................................................4

3.1 Current Ratio.........................................................................................................................5

3.2 Quick Ratio............................................................................................................................6

3.3 Net Profit Margin...................................................................................................................6

3.4 Return on Equity....................................................................................................................7

3.5 Return on Assets....................................................................................................................7

Analysis and Comparison between Challenger ltd, BBVA Group and Alliance Trust...................8

Reference.......................................................................................................................................10

Appendix........................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING FOR BUSINESS

1. Introduction

1.1 Purpose

The main purpose of the assignment is to analyze the financial reports of Challenger ltd for

the purpose of evaluating financial performance of the company. In addition to this, the

assignment will be containing ratio which are to be computed and then analysis the performance

of the company in comparison with other similar companies belonging to similar industry (Luo

et al., 2015).

1.2 Scope

The scope of this assignment is compute the key financial ratios which are associated with

the business. The ratios which are computed have some significance and are considered to be

financial indicators of performance in a business. The assignment will be conducting a

comparative study between Challenger ltd and BBVA Group ltd and Alliance Trust which

operates in the same industry as Challenger ltd.

1.3 Limitation

The limitation which the assignment faces is that the ratio which are considered for this

assignment are limited for comparison purposes and it makes the scope of the assignment a bit

narrow. The ratios which are computed is for the last two years for which the analysis is to b e

undertaken.

2.0 Company Overview

Challenger ltd is a company which operates in Australia and is engaged in managing

investments for its customers. The company has its headquarters in Sydney, Australia. In other

ACCOUNTING FOR BUSINESS

1. Introduction

1.1 Purpose

The main purpose of the assignment is to analyze the financial reports of Challenger ltd for

the purpose of evaluating financial performance of the company. In addition to this, the

assignment will be containing ratio which are to be computed and then analysis the performance

of the company in comparison with other similar companies belonging to similar industry (Luo

et al., 2015).

1.2 Scope

The scope of this assignment is compute the key financial ratios which are associated with

the business. The ratios which are computed have some significance and are considered to be

financial indicators of performance in a business. The assignment will be conducting a

comparative study between Challenger ltd and BBVA Group ltd and Alliance Trust which

operates in the same industry as Challenger ltd.

1.3 Limitation

The limitation which the assignment faces is that the ratio which are considered for this

assignment are limited for comparison purposes and it makes the scope of the assignment a bit

narrow. The ratios which are computed is for the last two years for which the analysis is to b e

undertaken.

2.0 Company Overview

Challenger ltd is a company which operates in Australia and is engaged in managing

investments for its customers. The company has its headquarters in Sydney, Australia. In other

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING FOR BUSINESS

words, the company provides financial security to individuals when they are unable to earn

income or when such individuals retire. The various plans of the management of the company is

to provide a platform where individual can save their incomes and when such persons retire they

can have a steady flow of income as per their requirement. Challenger has been developing over

the years and the business of the company has expanded. In addition to this, the company is

considered to be one of the largest fund managing companies in Australia as per current year’s

estimates. The total assets of the company which is generated is shown in the annual reports of

the business which comes to about $ 70 billion. This shows that the company is improving its

business performances in order to expand the market further and gain competitive advantage for

the business.

3.0 Ratio Analysis

Ratio analysis is a popular technique which is used by businesses to analyze the

performance of the company in terms of profitability, solvency, Efficiency. Various decision-

making process are based on the analysis and findings which are obtained from this analysis (Al

Karim & Alam, 2013). The ratios which are considered for this analysis are considered to

financial indicators of the performance of the business (Nirajini & Priya, 2013). A figure below

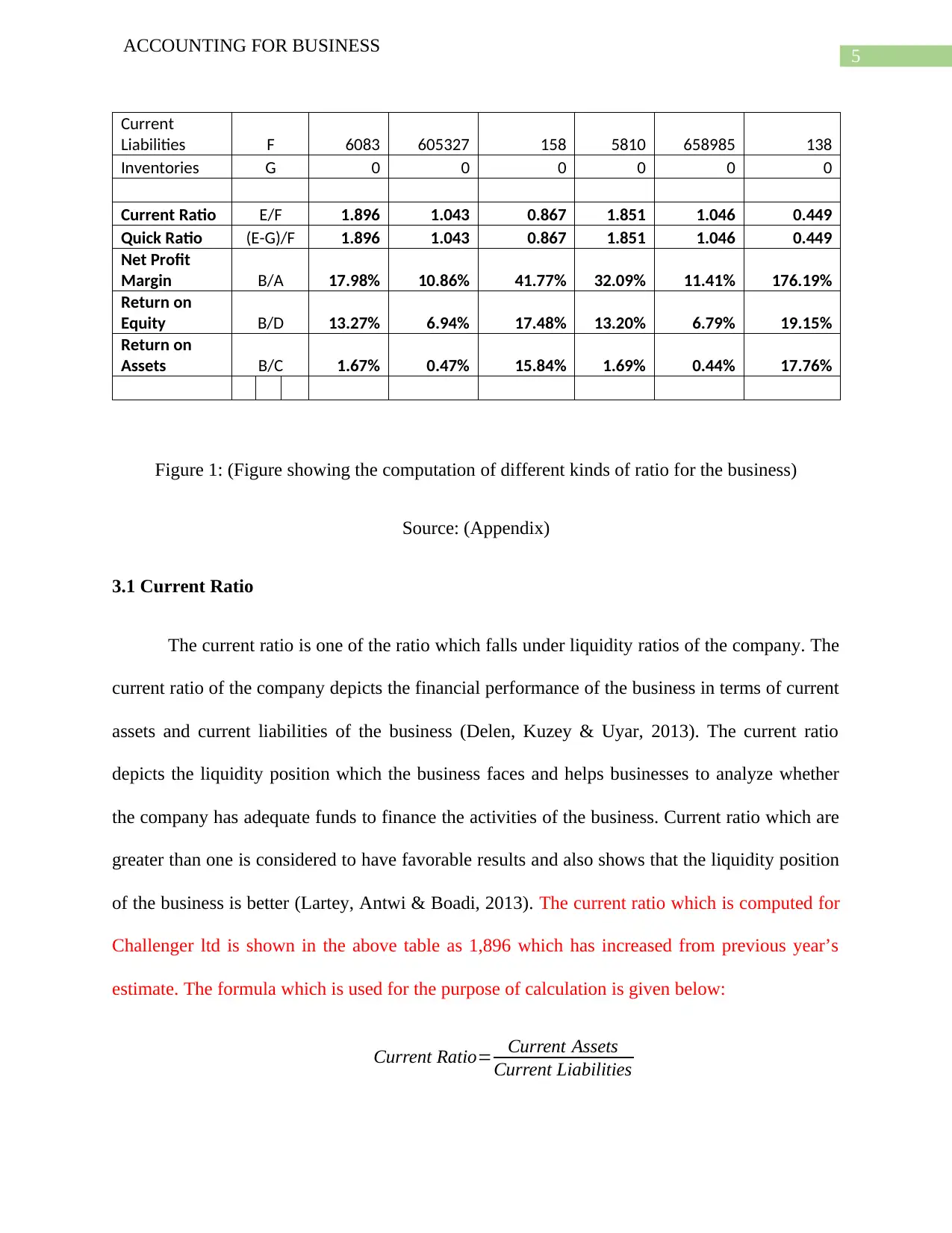

shows the table in which the computation of different ratios is calculated below:

2017 2016

Particulars

Formula

s

Challeng

er

BBVA

Group

Alliance

Trust

Challeng

er

BBVA

Group

Alliance

Trust

Revenue A 2140.3 29630 1130 1104.4 28175 357

Net Profit B 384.9 3218 472 354.4 3215 629

Total Assets C 23011 690059 2979 20978 731856 3541

Total Equity D 2901 46344 2700 2684 47364 3284

Current Assets E 11532 631516 137 10756 689158 62

ACCOUNTING FOR BUSINESS

words, the company provides financial security to individuals when they are unable to earn

income or when such individuals retire. The various plans of the management of the company is

to provide a platform where individual can save their incomes and when such persons retire they

can have a steady flow of income as per their requirement. Challenger has been developing over

the years and the business of the company has expanded. In addition to this, the company is

considered to be one of the largest fund managing companies in Australia as per current year’s

estimates. The total assets of the company which is generated is shown in the annual reports of

the business which comes to about $ 70 billion. This shows that the company is improving its

business performances in order to expand the market further and gain competitive advantage for

the business.

3.0 Ratio Analysis

Ratio analysis is a popular technique which is used by businesses to analyze the

performance of the company in terms of profitability, solvency, Efficiency. Various decision-

making process are based on the analysis and findings which are obtained from this analysis (Al

Karim & Alam, 2013). The ratios which are considered for this analysis are considered to

financial indicators of the performance of the business (Nirajini & Priya, 2013). A figure below

shows the table in which the computation of different ratios is calculated below:

2017 2016

Particulars

Formula

s

Challeng

er

BBVA

Group

Alliance

Trust

Challeng

er

BBVA

Group

Alliance

Trust

Revenue A 2140.3 29630 1130 1104.4 28175 357

Net Profit B 384.9 3218 472 354.4 3215 629

Total Assets C 23011 690059 2979 20978 731856 3541

Total Equity D 2901 46344 2700 2684 47364 3284

Current Assets E 11532 631516 137 10756 689158 62

5

ACCOUNTING FOR BUSINESS

Current

Liabilities F 6083 605327 158 5810 658985 138

Inventories G 0 0 0 0 0 0

Current Ratio E/F 1.896 1.043 0.867 1.851 1.046 0.449

Quick Ratio (E-G)/F 1.896 1.043 0.867 1.851 1.046 0.449

Net Profit

Margin B/A 17.98% 10.86% 41.77% 32.09% 11.41% 176.19%

Return on

Equity B/D 13.27% 6.94% 17.48% 13.20% 6.79% 19.15%

Return on

Assets B/C 1.67% 0.47% 15.84% 1.69% 0.44% 17.76%

Figure 1: (Figure showing the computation of different kinds of ratio for the business)

Source: (Appendix)

3.1 Current Ratio

The current ratio is one of the ratio which falls under liquidity ratios of the company. The

current ratio of the company depicts the financial performance of the business in terms of current

assets and current liabilities of the business (Delen, Kuzey & Uyar, 2013). The current ratio

depicts the liquidity position which the business faces and helps businesses to analyze whether

the company has adequate funds to finance the activities of the business. Current ratio which are

greater than one is considered to have favorable results and also shows that the liquidity position

of the business is better (Lartey, Antwi & Boadi, 2013). The current ratio which is computed for

Challenger ltd is shown in the above table as 1,896 which has increased from previous year’s

estimate. The formula which is used for the purpose of calculation is given below:

Current Ratio= Current Assets

Current Liabilities

ACCOUNTING FOR BUSINESS

Current

Liabilities F 6083 605327 158 5810 658985 138

Inventories G 0 0 0 0 0 0

Current Ratio E/F 1.896 1.043 0.867 1.851 1.046 0.449

Quick Ratio (E-G)/F 1.896 1.043 0.867 1.851 1.046 0.449

Net Profit

Margin B/A 17.98% 10.86% 41.77% 32.09% 11.41% 176.19%

Return on

Equity B/D 13.27% 6.94% 17.48% 13.20% 6.79% 19.15%

Return on

Assets B/C 1.67% 0.47% 15.84% 1.69% 0.44% 17.76%

Figure 1: (Figure showing the computation of different kinds of ratio for the business)

Source: (Appendix)

3.1 Current Ratio

The current ratio is one of the ratio which falls under liquidity ratios of the company. The

current ratio of the company depicts the financial performance of the business in terms of current

assets and current liabilities of the business (Delen, Kuzey & Uyar, 2013). The current ratio

depicts the liquidity position which the business faces and helps businesses to analyze whether

the company has adequate funds to finance the activities of the business. Current ratio which are

greater than one is considered to have favorable results and also shows that the liquidity position

of the business is better (Lartey, Antwi & Boadi, 2013). The current ratio which is computed for

Challenger ltd is shown in the above table as 1,896 which has increased from previous year’s

estimate. The formula which is used for the purpose of calculation is given below:

Current Ratio= Current Assets

Current Liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING FOR BUSINESS

3.2 Quick Ratio

Quick ratio of a company also falls under the purview of liquidity ratio of the business.

This ratio is similar to current ratio which is computed by the company. The quick ratio

considers quick assets which are cash balance, debtors and similar other assets and quick

liabilities for the purpose of computation. The quick ratio of the business depicts the liquidity

position of the business as to whether the business is able to meet the short-term financing

requirements of the business or not. In other words, the ratio is a measure of the ability of the

company to meet its current short-term obligations. The quick ratio of Challenger ltd which is

shown in the above table comes to 1.896 which is same as the current ratio of the company. The

formula which is used for the purpose of calculation is shown below:

Quick Ratio= Current Assets−Inventories

Current Liabilities

3.3 Net Profit Margin

The net profit margin ratio shows the relationship between net profit which is generated

by the company and the sales revenue which is generated by the business. The main purpose of

the ratio is to analyze how much net profit can be earned for a particular level of sale (Rehman,

2013). This is considered to be an important ratio as it is an important financial indicator of the

performance of the business. The net profit margin for Challenger ltd which is shown in the table

above table which is 17.98% % which has significantly reduced from previous years estimate.

The formula which is used is given below:

ACCOUNTING FOR BUSINESS

3.2 Quick Ratio

Quick ratio of a company also falls under the purview of liquidity ratio of the business.

This ratio is similar to current ratio which is computed by the company. The quick ratio

considers quick assets which are cash balance, debtors and similar other assets and quick

liabilities for the purpose of computation. The quick ratio of the business depicts the liquidity

position of the business as to whether the business is able to meet the short-term financing

requirements of the business or not. In other words, the ratio is a measure of the ability of the

company to meet its current short-term obligations. The quick ratio of Challenger ltd which is

shown in the above table comes to 1.896 which is same as the current ratio of the company. The

formula which is used for the purpose of calculation is shown below:

Quick Ratio= Current Assets−Inventories

Current Liabilities

3.3 Net Profit Margin

The net profit margin ratio shows the relationship between net profit which is generated

by the company and the sales revenue which is generated by the business. The main purpose of

the ratio is to analyze how much net profit can be earned for a particular level of sale (Rehman,

2013). This is considered to be an important ratio as it is an important financial indicator of the

performance of the business. The net profit margin for Challenger ltd which is shown in the table

above table which is 17.98% % which has significantly reduced from previous years estimate.

The formula which is used is given below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING FOR BUSINESS

Net Profit Margin= Net Profit

Revenue Generated

3.4 Return on Equity

The return on equity refers to the return which is expected by the shareholders as returns

they will be getting for the investments made by them. Return on Equity (ROE) is considered to

be one of the financial indicators which are used by potential investors for taking investment

decisions in the shares and securities of the company (Heikal et al., 2014). In addition to this, the

level of ROE is also a system which can display that the company is performing well. the return

of equity which is computed is shown in the table which is given above is 13.27 % which has

slightly fallen from the previous year’s estimate. The formula which is used is given below:

Return on Equity ( ROE ) = Net Profit

Total Shareholders Equity

3.5 Return on Assets

The return on assets ratio shows the relationship between total assets of the business with

the returns which are earned by the business. In other words, it shows the revenue which the

business can earn while employing the assets of the business (Baños-Caballero, García-Teruel &

Martínez-Solano, 2014). This is also noted by the potential stakeholders as such ratio provides

information about the different activities of the business. Return on assets ratio signifies whether

the assets which are possessed by the business are applied in a favorable manner or not. The

formula which is used is given below:

ACCOUNTING FOR BUSINESS

Net Profit Margin= Net Profit

Revenue Generated

3.4 Return on Equity

The return on equity refers to the return which is expected by the shareholders as returns

they will be getting for the investments made by them. Return on Equity (ROE) is considered to

be one of the financial indicators which are used by potential investors for taking investment

decisions in the shares and securities of the company (Heikal et al., 2014). In addition to this, the

level of ROE is also a system which can display that the company is performing well. the return

of equity which is computed is shown in the table which is given above is 13.27 % which has

slightly fallen from the previous year’s estimate. The formula which is used is given below:

Return on Equity ( ROE ) = Net Profit

Total Shareholders Equity

3.5 Return on Assets

The return on assets ratio shows the relationship between total assets of the business with

the returns which are earned by the business. In other words, it shows the revenue which the

business can earn while employing the assets of the business (Baños-Caballero, García-Teruel &

Martínez-Solano, 2014). This is also noted by the potential stakeholders as such ratio provides

information about the different activities of the business. Return on assets ratio signifies whether

the assets which are possessed by the business are applied in a favorable manner or not. The

formula which is used is given below:

8

ACCOUNTING FOR BUSINESS

Returnon Assets ( ROA ) = Net Profit

Total Assets

Analysis and Comparison between Challenger ltd, BBVA Group and Alliance Trust

The companies which are selected for the purpose of conducting an analysis and

comparison with Challenger ltd are BBVA Group and Alliance Trust. As per figure 1, which

shows the significant ratios which are calculated for the analysis part for 2017 and 2016. The

current ratio as shown in figure 1, is much better of Challenger ltd than its rival companies which

suggest that the liquidity position of the company is secure and the company can effectively

finance any projects. The current ratio for the year 2017 for challengers ltd, BBVA Group and

Alliance Trust are computed to be 1.896, 1.043 and 0.876 respectively. The current ratio is most

adverse in case of Alliance trust which signifies that the company is facing certain liquidity

crisis. In comparison with 2016 estimates as calculated the current ratio has reduced slightly for

BBVA Group and slightly improved for Alliance trust as well as Challenger ltd. The quick ratio

of all three companies show similar results as current which suggest that the current ratio

estimates are also quick ratio estimates for all the three companies. This also suggested that all

the businesses does not have any inventories therefore the quick assets of the business does not

changes as current assets which are taken into consideration for calculation of quick assets does

not change. The net profit margin of Challenger ltd, BBVA Group and Alliance Trust for the

year 2017 show results as 17.98%, 10.86% and 41.77% respectively. The net profit margin of

Alliance Trust shows abnormal amounts of profits for both 2016 and 2017 which is more than

Challenger ltd and BBVA Group. The net profit margin of Challenger ltd has reduced from

previous year which was 32.8% which suggest that the cost which is associated with production

has increased and therefore the profits of the company has fallen (Ongore & Kusa, 2013). The

ACCOUNTING FOR BUSINESS

Returnon Assets ( ROA ) = Net Profit

Total Assets

Analysis and Comparison between Challenger ltd, BBVA Group and Alliance Trust

The companies which are selected for the purpose of conducting an analysis and

comparison with Challenger ltd are BBVA Group and Alliance Trust. As per figure 1, which

shows the significant ratios which are calculated for the analysis part for 2017 and 2016. The

current ratio as shown in figure 1, is much better of Challenger ltd than its rival companies which

suggest that the liquidity position of the company is secure and the company can effectively

finance any projects. The current ratio for the year 2017 for challengers ltd, BBVA Group and

Alliance Trust are computed to be 1.896, 1.043 and 0.876 respectively. The current ratio is most

adverse in case of Alliance trust which signifies that the company is facing certain liquidity

crisis. In comparison with 2016 estimates as calculated the current ratio has reduced slightly for

BBVA Group and slightly improved for Alliance trust as well as Challenger ltd. The quick ratio

of all three companies show similar results as current which suggest that the current ratio

estimates are also quick ratio estimates for all the three companies. This also suggested that all

the businesses does not have any inventories therefore the quick assets of the business does not

changes as current assets which are taken into consideration for calculation of quick assets does

not change. The net profit margin of Challenger ltd, BBVA Group and Alliance Trust for the

year 2017 show results as 17.98%, 10.86% and 41.77% respectively. The net profit margin of

Alliance Trust shows abnormal amounts of profits for both 2016 and 2017 which is more than

Challenger ltd and BBVA Group. The net profit margin of Challenger ltd has reduced from

previous year which was 32.8% which suggest that the cost which is associated with production

has increased and therefore the profits of the company has fallen (Ongore & Kusa, 2013). The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING FOR BUSINESS

net profit margin for both BBVA Group and Alliance trust has reduced from previous year. The

profits of Alliance trust still stand out in the figure 1 as shown above. The return on equity shows

that the estimate has increased slightly from previous year’s results for Challenger ltd and BBVA

Group. The return on equity for Alliance trust has however reduced from previous year. As the

profitability of Alliance Trust is significantly more than Challenger ltd and BBVA Group, it is

quite natural that the return on equity for the company is much better than its competitors which

shows that the company is meeting the needs of the shareholders of the company effectively.

The return on assets estimates show that Alliance Trust has the best estimates in the comparative

study and the estimates of Challenger ltd and BBVA Group is no where near the results of

Alliance trust which shows that the company has a better return on assets.

ACCOUNTING FOR BUSINESS

net profit margin for both BBVA Group and Alliance trust has reduced from previous year. The

profits of Alliance trust still stand out in the figure 1 as shown above. The return on equity shows

that the estimate has increased slightly from previous year’s results for Challenger ltd and BBVA

Group. The return on equity for Alliance trust has however reduced from previous year. As the

profitability of Alliance Trust is significantly more than Challenger ltd and BBVA Group, it is

quite natural that the return on equity for the company is much better than its competitors which

shows that the company is meeting the needs of the shareholders of the company effectively.

The return on assets estimates show that Alliance Trust has the best estimates in the comparative

study and the estimates of Challenger ltd and BBVA Group is no where near the results of

Alliance trust which shows that the company has a better return on assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING FOR BUSINESS

Reference

Al Karim, R., & Alam, T. (2013). An evaluation of financial performance of private commercial

banks in Bangladesh: Ratio analysis. Journal of Business Studies Quarterly, 5(2), 65.

Baños-Caballero, S., García-Teruel, P. J., & Martínez-Solano, P. (2014). Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), 332-338.

Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), 3970-3983.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets (ROA),

return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current ratio

(CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Lartey, V. C., Antwi, S., & Boadi, E. K. (2013). The relationship between liquidity and

profitability of listed banks in Ghana. International Journal of Business and Social

Science, 4(3).

Luo, D., Dong, H., Luo, H., Xian, Y., Wan, J., Guo, X., & Wu, Y. (2015). The application of

stable isotope ratio analysis to determine the geographical origin of wheat. Food

chemistry, 174, 197-201.

ACCOUNTING FOR BUSINESS

Reference

Al Karim, R., & Alam, T. (2013). An evaluation of financial performance of private commercial

banks in Bangladesh: Ratio analysis. Journal of Business Studies Quarterly, 5(2), 65.

Baños-Caballero, S., García-Teruel, P. J., & Martínez-Solano, P. (2014). Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), 332-338.

Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), 3970-3983.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets (ROA),

return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current ratio

(CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Lartey, V. C., Antwi, S., & Boadi, E. K. (2013). The relationship between liquidity and

profitability of listed banks in Ghana. International Journal of Business and Social

Science, 4(3).

Luo, D., Dong, H., Luo, H., Xian, Y., Wan, J., Guo, X., & Wu, Y. (2015). The application of

stable isotope ratio analysis to determine the geographical origin of wheat. Food

chemistry, 174, 197-201.

11

ACCOUNTING FOR BUSINESS

Nirajini, A., & Priya, K. B. (2013). Impact of capital structure on financial performance of the

listed trading companies in Sri Lanka. International Journal of Scientific and Research

Publications, 3(5), 35-43.

Ongore, V. O., & Kusa, G. B. (2013). Determinants of financial performance of commercial

banks in Kenya. International Journal of Economics and Financial Issues, 3(1), 237.

Rehman, S. S. F. U. (2013). Relationship between financial leverage and financial performance:

Empirical evidence of listed sugar companies of Pakistan. Global Journal of Management

and Business Research.

ACCOUNTING FOR BUSINESS

Nirajini, A., & Priya, K. B. (2013). Impact of capital structure on financial performance of the

listed trading companies in Sri Lanka. International Journal of Scientific and Research

Publications, 3(5), 35-43.

Ongore, V. O., & Kusa, G. B. (2013). Determinants of financial performance of commercial

banks in Kenya. International Journal of Economics and Financial Issues, 3(1), 237.

Rehman, S. S. F. U. (2013). Relationship between financial leverage and financial performance:

Empirical evidence of listed sugar companies of Pakistan. Global Journal of Management

and Business Research.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.