Challenges in Accounting within Global Finance: A Comprehensive Report

VerifiedAdded on 2020/03/16

|14

|2948

|261

Report

AI Summary

This report delves into the intricate challenges of accounting within the context of global finance. It highlights the increasing complexities faced by financial professionals due to globalization, including the need to navigate diverse international regulations, currencies, and taxation policies. The report emphasizes the importance of understanding global trends, adapting accounting practices, and identifying key challenges to ensure accurate financial reporting and effective decision-making. It covers topics such as green accounting and harmonization while also addressing the ethical and moral considerations that accountants encounter in a globalized environment. The methodology includes both qualitative and quantitative research approaches, incorporating direct observation, questionnaires, and interviews to gather comprehensive data and analyze the behaviors and perceptions of accountants. The paper aims to provide insights into the challenges and potential solutions for global finance accounting, offering valuable strategies for companies to optimize their operations and maintain a competitive edge.

Running head: CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Name of the Student:

Name of the University:

Author Note:

CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Executive Summary

Finance accounting is one of the most important aspects of business operations that help

organizations to make decisions regarding budget and cost structure. Accounting helps an

organization to effectively understand its position in the industry and their internal situation

based on economic condition and this facilitates it key decision making strategies. Financial

accounting in the global context has become a very tricky and challenging aspect in the business

operations of today simply because companies have to bear in mind a lot of rules and regulations

from various countries across the globe. These challenges need to be correctly and efficiently

identified and solutions need to be come up with. The following report would like to take a

deeper look into these problems and try to provide ways that would help to do away with the

challenges and make the accounting process smoother.

Executive Summary

Finance accounting is one of the most important aspects of business operations that help

organizations to make decisions regarding budget and cost structure. Accounting helps an

organization to effectively understand its position in the industry and their internal situation

based on economic condition and this facilitates it key decision making strategies. Financial

accounting in the global context has become a very tricky and challenging aspect in the business

operations of today simply because companies have to bear in mind a lot of rules and regulations

from various countries across the globe. These challenges need to be correctly and efficiently

identified and solutions need to be come up with. The following report would like to take a

deeper look into these problems and try to provide ways that would help to do away with the

challenges and make the accounting process smoother.

2CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Table of Contents

Introduction......................................................................................................................................3

Project objective..............................................................................................................................3

Project scope....................................................................................................................................4

Literature review..............................................................................................................................4

Green accounting:........................................................................................................................6

Harmonisation:.............................................................................................................................6

Literature gap...................................................................................................................................6

Hypothesis.......................................................................................................................................7

Research design...............................................................................................................................7

Qualitative research:....................................................................................................................7

Quantitative research:..................................................................................................................8

Research limitations.........................................................................................................................9

Time schedule..................................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................3

Project objective..............................................................................................................................3

Project scope....................................................................................................................................4

Literature review..............................................................................................................................4

Green accounting:........................................................................................................................6

Harmonisation:.............................................................................................................................6

Literature gap...................................................................................................................................6

Hypothesis.......................................................................................................................................7

Research design...............................................................................................................................7

Qualitative research:....................................................................................................................7

Quantitative research:..................................................................................................................8

Research limitations.........................................................................................................................9

Time schedule..................................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Introduction

The primary functions of financing have always been trying to control costs, making and

maintaining proper budgets. Finance department of any organization is laden with the task of

planning a budget which will dictate the financial transactions and operations of the companies.

Another important role of finance is internal auditing. This is an essential aspect of business

running, which ensures the organisations are operating in a correct manner (Burns & Needles,

2014). However, in the age of globalization, as organizations are expanding rapidly and are

operating business overseas the finance departments and auditing firms are being faced with new

and more intricate challenges every day. Their tasks and responsibilities transcend from being

burdened with simple capital structure making to profit repatriation policies of the company’s

subsidiaries. Capital budgeting decisions should reflect not just the divisional differences, but

also has to show the complicacies that arise due to the different currencies, exchange rates,

taxation policies and the different laws and regulations in different countries (Prencipe, Bar-

Yosef & Dekker, 2014). The companies’ incentive system must be able to assess, acknowledge

and reward the actions and operations of the managers who work under different economic and

financial settings across the globe. This paper will be aimed at 3xamining the role of the

accounting strategies in the environment of globalization and try to identify the challenges that

are faced by the accounting firms.

Project objective

The prime objectives of this paper are:

To understand the impact of global trends in the globalization setting

To observe the changing accounting practices in today’s integrated world, and

Introduction

The primary functions of financing have always been trying to control costs, making and

maintaining proper budgets. Finance department of any organization is laden with the task of

planning a budget which will dictate the financial transactions and operations of the companies.

Another important role of finance is internal auditing. This is an essential aspect of business

running, which ensures the organisations are operating in a correct manner (Burns & Needles,

2014). However, in the age of globalization, as organizations are expanding rapidly and are

operating business overseas the finance departments and auditing firms are being faced with new

and more intricate challenges every day. Their tasks and responsibilities transcend from being

burdened with simple capital structure making to profit repatriation policies of the company’s

subsidiaries. Capital budgeting decisions should reflect not just the divisional differences, but

also has to show the complicacies that arise due to the different currencies, exchange rates,

taxation policies and the different laws and regulations in different countries (Prencipe, Bar-

Yosef & Dekker, 2014). The companies’ incentive system must be able to assess, acknowledge

and reward the actions and operations of the managers who work under different economic and

financial settings across the globe. This paper will be aimed at 3xamining the role of the

accounting strategies in the environment of globalization and try to identify the challenges that

are faced by the accounting firms.

Project objective

The prime objectives of this paper are:

To understand the impact of global trends in the globalization setting

To observe the changing accounting practices in today’s integrated world, and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

To indentify the key challenges of accounting in today’s global economy

Project scope

The paper would try and identify the challenges of accounting in global finance and then

go on to give probable solutions that would help firms to execute auditing and accounting for the

global companies in a smoother way. The paper, once completed would have a scope of

delivering new strategies to the global companies that would make global finance accounting

easier and devoid of complicated hassle.

Literature review

The rise of the ideas and theories on globalization has brought with it many other

dimensions and new parameters were introduced which had a significant impact on the

accounting practices as well as the accountants in the globally functioning organizations (Rathee

& Kapil, 2015). Compared to the traditional accounting, modern auditing and financial

accounting firms have taken on new identities and new roadways have opened up. While the

traditional form of accounting was concerned with simple auditing and financial management,

modern financial accounting has sprouted new branches and a lot more aspects have been

included in the whole process, some of which are corporate governance, anti-corruption laws,

regulation standards, accountability in large multinational corporations (MNCs) and many more

(Bebbington, Unerman & O'Dwyer, 2014). The factor that makes all of these even more

complicated is the fact that, all these parameters have to be adhered to under different laws and

regulations in every country, hence no uniform code of conduct or action plan cannot be devised

easily. Accounting is a neutral take on the financial and economic conditions of a given

organization or industry. The economic powers and factors that are at play in the setting of

different countries all are incorporated in these financial reflections (Johnson, 2014). The

To indentify the key challenges of accounting in today’s global economy

Project scope

The paper would try and identify the challenges of accounting in global finance and then

go on to give probable solutions that would help firms to execute auditing and accounting for the

global companies in a smoother way. The paper, once completed would have a scope of

delivering new strategies to the global companies that would make global finance accounting

easier and devoid of complicated hassle.

Literature review

The rise of the ideas and theories on globalization has brought with it many other

dimensions and new parameters were introduced which had a significant impact on the

accounting practices as well as the accountants in the globally functioning organizations (Rathee

& Kapil, 2015). Compared to the traditional accounting, modern auditing and financial

accounting firms have taken on new identities and new roadways have opened up. While the

traditional form of accounting was concerned with simple auditing and financial management,

modern financial accounting has sprouted new branches and a lot more aspects have been

included in the whole process, some of which are corporate governance, anti-corruption laws,

regulation standards, accountability in large multinational corporations (MNCs) and many more

(Bebbington, Unerman & O'Dwyer, 2014). The factor that makes all of these even more

complicated is the fact that, all these parameters have to be adhered to under different laws and

regulations in every country, hence no uniform code of conduct or action plan cannot be devised

easily. Accounting is a neutral take on the financial and economic conditions of a given

organization or industry. The economic powers and factors that are at play in the setting of

different countries all are incorporated in these financial reflections (Johnson, 2014). The

5CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

accounting practices and the outcomes give an organization the necessary insight to make vital

economic and budgeting decisions.

The figures that are presented by the accounting departments of the organizations, shape

the decision making process of the companies. Internal audits help companies to understand and

identify the areas or countries which would offer them cheap but skilled labors. Knowledge like

this is important to make decisions which would enable companies to curb costs and increase

their profit margin (Gereffi & Fernandez-Stark, 2016).

If the companies wish to stay ahead of the competition in the fierce market conditions of

today’s world, they must make the right decisions that would enable them to optimize their

operations which would keep them on top of the industry. To make these decisions, it is vital for

the organizations to keep innovating and be creative about the operations in order to be

sustainable (Ebrahim, Battilana & Mair, 2014). While making the decisions it must be kept in

mind that the organization has all the necessary information that are generated by the accounting

department.

Even excluding the aspect of globalization, there a number of other factors that affect the

role of accounting in organizations. The advent of modern technology and its applications have

affected every aspect of business operations, including management and financial auditing. In the

era of free information and technology, the ideas about how products and services are delivered

to the consumers have changed drastically, forever altering the business operations of every

organization.

Evolving market competition has prompted organizations to adopt new methods of

management accounting which comprises of innovative ways like Just In Time (JIT), Total

accounting practices and the outcomes give an organization the necessary insight to make vital

economic and budgeting decisions.

The figures that are presented by the accounting departments of the organizations, shape

the decision making process of the companies. Internal audits help companies to understand and

identify the areas or countries which would offer them cheap but skilled labors. Knowledge like

this is important to make decisions which would enable companies to curb costs and increase

their profit margin (Gereffi & Fernandez-Stark, 2016).

If the companies wish to stay ahead of the competition in the fierce market conditions of

today’s world, they must make the right decisions that would enable them to optimize their

operations which would keep them on top of the industry. To make these decisions, it is vital for

the organizations to keep innovating and be creative about the operations in order to be

sustainable (Ebrahim, Battilana & Mair, 2014). While making the decisions it must be kept in

mind that the organization has all the necessary information that are generated by the accounting

department.

Even excluding the aspect of globalization, there a number of other factors that affect the

role of accounting in organizations. The advent of modern technology and its applications have

affected every aspect of business operations, including management and financial auditing. In the

era of free information and technology, the ideas about how products and services are delivered

to the consumers have changed drastically, forever altering the business operations of every

organization.

Evolving market competition has prompted organizations to adopt new methods of

management accounting which comprises of innovative ways like Just In Time (JIT), Total

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Quality Management (TQM) and other similar methods. Previously, organizations were only

faced with competition from local or at most, the national markets, but today every company has

to overcome the obstacles that are created by overseas companies as well (Stauffer, 2015).

There are several trends that are practiced in managerial accounting processes in the

context of glob al organizations.

Green accounting: With the threats of global warming and environmental pollution becoming

apparent every day, it is increasingly becoming a popular concept of a business organization that

will take care and maintain a balance between the environment and the operations. It has become

of paramount necessity to keep its operations clean and environment friendly if an organization

aims to keep a good relation with every customer and even the governmental bodies of the

country it is operating in (O'Connor, Sexton & Smart, 2013). this new aspect and requirement of

the customers have put accounting and analytics departments in an even more challenging

position as they are tasked with coming up with a budget and economic plan that would enable

the companies to attain Green GNP (Bodie, 2013). Investing in projects and other areas which

facilitate protection of the environment has become one of the key features of every global

organization.

Harmonization: In a time where many companies run several businesses in many countries, it is

very important to have a uniform accounting measure and process for every organization which

would help every company to keep track of their own financial operations more easily. It prime

objective of international harmonization is to make the different financial information from

different countries comparable so that companies can efficiently assess their own performances

in every country and identify where they need to work on.

Quality Management (TQM) and other similar methods. Previously, organizations were only

faced with competition from local or at most, the national markets, but today every company has

to overcome the obstacles that are created by overseas companies as well (Stauffer, 2015).

There are several trends that are practiced in managerial accounting processes in the

context of glob al organizations.

Green accounting: With the threats of global warming and environmental pollution becoming

apparent every day, it is increasingly becoming a popular concept of a business organization that

will take care and maintain a balance between the environment and the operations. It has become

of paramount necessity to keep its operations clean and environment friendly if an organization

aims to keep a good relation with every customer and even the governmental bodies of the

country it is operating in (O'Connor, Sexton & Smart, 2013). this new aspect and requirement of

the customers have put accounting and analytics departments in an even more challenging

position as they are tasked with coming up with a budget and economic plan that would enable

the companies to attain Green GNP (Bodie, 2013). Investing in projects and other areas which

facilitate protection of the environment has become one of the key features of every global

organization.

Harmonization: In a time where many companies run several businesses in many countries, it is

very important to have a uniform accounting measure and process for every organization which

would help every company to keep track of their own financial operations more easily. It prime

objective of international harmonization is to make the different financial information from

different countries comparable so that companies can efficiently assess their own performances

in every country and identify where they need to work on.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Literature gap

Although the previous work has been successful in identifying the different challenges

that create an obstacle while accounting for finance in a global context, the work is mainly

focused upon the statistical interpretation of the data. The ethical and moral grounds of the issues

have been barely talked about in depth, even though these issues are just as important to

understand how the behavioral pattern of the accountants are affected. This research would be

more concerned with the ethical aspects of operating a business in the global context and

financial accounting under the setting of a globalized era which makes the accountants face

situations of moral dilemma. This particular gap will be aimed to be solved in the following

paper.

Hypothesis

Null Hypothesis: The challenges faced by accounting in global finance are going to help

the business organizations if properly met with

Alternative hypothesis: The challenges faced by accounting in global finance are not

helpful for organizations even if they are met with the right solutions

Research design

A number of tools and methods can be used to make sure that the research reaches its

desired goal of identifying the challenges of global finance accounting. Two different types of

research methods are given most importance in a broader sense:

Qualitative research: This is a set of methods that are non-numerical in nature and are used for

social science researches. These methods target specific populations and help to interpret the

collected data that gives a comprehensive idea about the social life. Qualitative research methods

Literature gap

Although the previous work has been successful in identifying the different challenges

that create an obstacle while accounting for finance in a global context, the work is mainly

focused upon the statistical interpretation of the data. The ethical and moral grounds of the issues

have been barely talked about in depth, even though these issues are just as important to

understand how the behavioral pattern of the accountants are affected. This research would be

more concerned with the ethical aspects of operating a business in the global context and

financial accounting under the setting of a globalized era which makes the accountants face

situations of moral dilemma. This particular gap will be aimed to be solved in the following

paper.

Hypothesis

Null Hypothesis: The challenges faced by accounting in global finance are going to help

the business organizations if properly met with

Alternative hypothesis: The challenges faced by accounting in global finance are not

helpful for organizations even if they are met with the right solutions

Research design

A number of tools and methods can be used to make sure that the research reaches its

desired goal of identifying the challenges of global finance accounting. Two different types of

research methods are given most importance in a broader sense:

Qualitative research: This is a set of methods that are non-numerical in nature and are used for

social science researches. These methods target specific populations and help to interpret the

collected data that gives a comprehensive idea about the social life. Qualitative research methods

8CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

help researchers to derive behavioral pattern from the results of the surveys, which help to

predict actions and behavior of the individuals and organizations in the future. This type of

research helps the researchers identify the parameters and the attributes that shape the general

behavior of the subjects and the population behavioral pattern is derived based on that

approximation (Liamputtong, 2013). The qualitative methods that are to be used in the current

research have been selected to be:

Direct observation: This is the simplest method of qualitative research which involves the

researcher to observe the activity of the subjects without interfering in the process. The research

at hand would be employing the researcher to first understand how the accountants of the global

companies operate and what are the methods and tools that are used as well as the limitations of

those methods.

Questionnaire: The accountants will be given a set of questions that will talk about different

issues that they face while working: the issues regarding international laws and regulations and

the drawbacks of the current methods of global finance accounting.

Interviews: The research will then be followed by in depth interviews which would help the

researcher to understand the issues each individual faces while working as a management

accountant in global organizations.

It must be remembered that qualitative data can be tampered with very easily and may

yield biased results. Moreover, since this type of research method is the primary focus of this

paper, these will be used extensively and a behavioral pattern will be tried to retrieve by trying to

understand how the accountants react to certain situations (Clemence, Doise & Lorenzi-Cioldi,

2014).

help researchers to derive behavioral pattern from the results of the surveys, which help to

predict actions and behavior of the individuals and organizations in the future. This type of

research helps the researchers identify the parameters and the attributes that shape the general

behavior of the subjects and the population behavioral pattern is derived based on that

approximation (Liamputtong, 2013). The qualitative methods that are to be used in the current

research have been selected to be:

Direct observation: This is the simplest method of qualitative research which involves the

researcher to observe the activity of the subjects without interfering in the process. The research

at hand would be employing the researcher to first understand how the accountants of the global

companies operate and what are the methods and tools that are used as well as the limitations of

those methods.

Questionnaire: The accountants will be given a set of questions that will talk about different

issues that they face while working: the issues regarding international laws and regulations and

the drawbacks of the current methods of global finance accounting.

Interviews: The research will then be followed by in depth interviews which would help the

researcher to understand the issues each individual faces while working as a management

accountant in global organizations.

It must be remembered that qualitative data can be tampered with very easily and may

yield biased results. Moreover, since this type of research method is the primary focus of this

paper, these will be used extensively and a behavioral pattern will be tried to retrieve by trying to

understand how the accountants react to certain situations (Clemence, Doise & Lorenzi-Cioldi,

2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Quantitative research: This type of research method deals with statistical interpretations of the

gathered data through using mathematical tools which categorize answers and coming up with

definitive patterns which back up the qualitative results. This research method deals with

numerical data and the results are solidified by computational techniques. Specific conditions

and phenomenon are given logical explanation through scientific research.

The current research would take and apply a number of quantitative research methods to observe

and identify a pattern that the accountants feel are the biggest challenges in global financial

accounting process. In many cases, secondary data are the only source of collected data which

form the basis for quantitative research analysis. Surveys are also used to gather data which

would provide with the necessary parameters to calculate and analyze. The accountants and the

organizations will be asked to provide data regarding the biggest and the most frequent issues

that they have faced while making internal audits or managerial accounting, in order to

understand and decipher a pattern for the problems and the most difficult part of the process (Elo

et al., 2014). The statistical results will be immensely helpful in terms of establishing the

assumptions in a firmer way.

Research limitations

The biggest limitation of the research is, which is a problem for almost every survey ever,

is that the sample population size is too small (Brinkmann, 2014). While it may be easier to

calculate the smaller size of data, the opinions and perspectives of every individual cannot be

known from just a few. Small sample size can often lead to results being riddled with

misinterpretations and laden with false conclusions (Geppert, Matten & Williams, 2016). On the

other hand, it is virtually and physically impossible for any research to survey entire populations

Quantitative research: This type of research method deals with statistical interpretations of the

gathered data through using mathematical tools which categorize answers and coming up with

definitive patterns which back up the qualitative results. This research method deals with

numerical data and the results are solidified by computational techniques. Specific conditions

and phenomenon are given logical explanation through scientific research.

The current research would take and apply a number of quantitative research methods to observe

and identify a pattern that the accountants feel are the biggest challenges in global financial

accounting process. In many cases, secondary data are the only source of collected data which

form the basis for quantitative research analysis. Surveys are also used to gather data which

would provide with the necessary parameters to calculate and analyze. The accountants and the

organizations will be asked to provide data regarding the biggest and the most frequent issues

that they have faced while making internal audits or managerial accounting, in order to

understand and decipher a pattern for the problems and the most difficult part of the process (Elo

et al., 2014). The statistical results will be immensely helpful in terms of establishing the

assumptions in a firmer way.

Research limitations

The biggest limitation of the research is, which is a problem for almost every survey ever,

is that the sample population size is too small (Brinkmann, 2014). While it may be easier to

calculate the smaller size of data, the opinions and perspectives of every individual cannot be

known from just a few. Small sample size can often lead to results being riddled with

misinterpretations and laden with false conclusions (Geppert, Matten & Williams, 2016). On the

other hand, it is virtually and physically impossible for any research to survey entire populations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

and collect data from everyone on the planet. The problem of random sampling will always

remain and the current research is not devoid of the same problems.

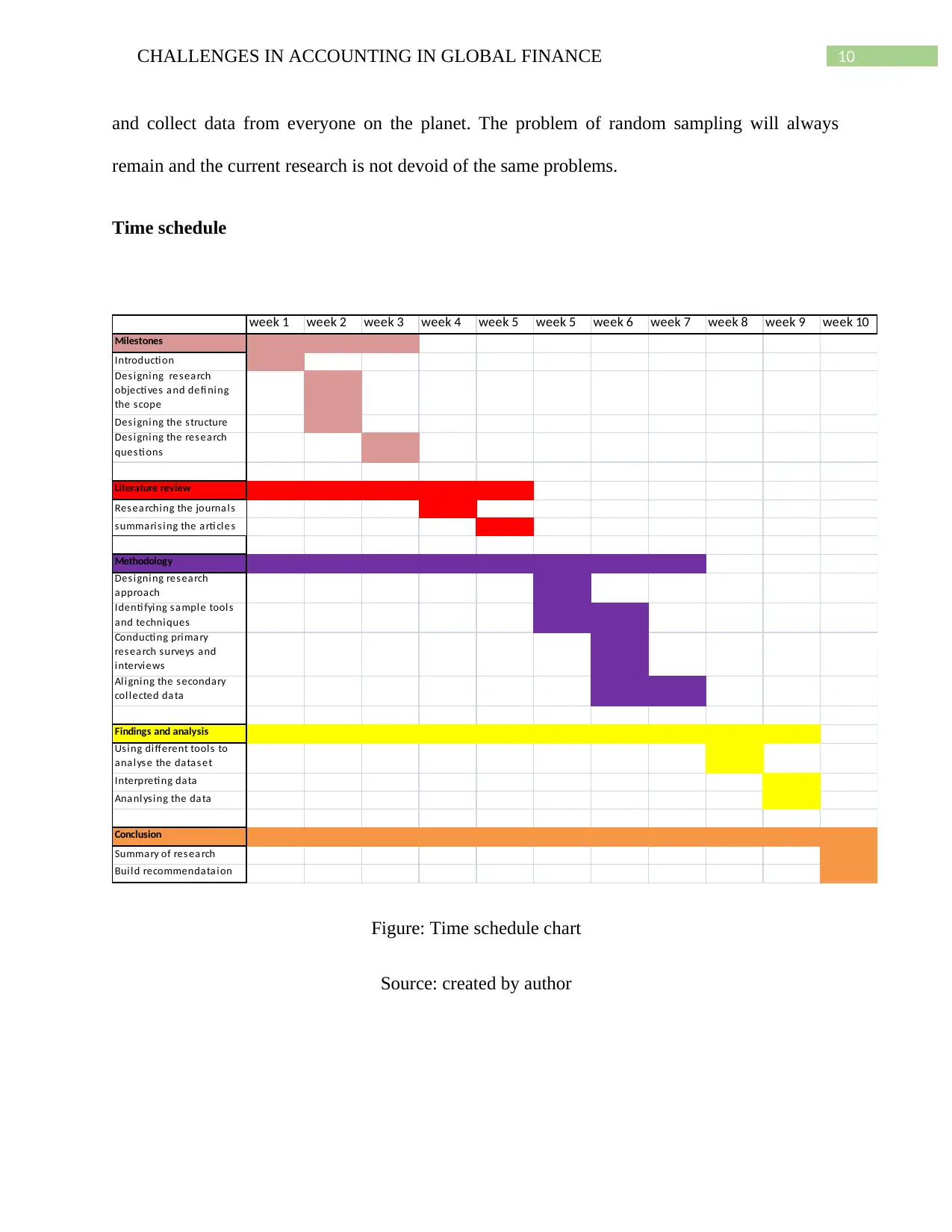

Time schedule

week 1 week 2 week 3 week 4 week 5 week 5 week 6 week 7 week 8 week 9 week 10

Milestones

Introducti on

Des i gni ng resea rch

objecti ves and defi ni ng

the scope

Des i gni ng the structure

Des i gni ng the res ea rch

questi ons

Literature review

Res ea rchi ng the journa l s

summari s i ng the arti cl es

Methodology

Des i gni ng res ea rch

approach

Identi fyi ng sa mpl e tool s

and techni ques

Conducti ng pri mary

res earch surveys and

i ntervi ews

Al i gni ng the s econdary

col l ected da ta

Findings and analysis

Usi ng di fferent tool s to

ana l yse the data set

Interpreti ng data

Ana nl ysi ng the data

Conclusion

Summary of res ea rch

Bui l d recommendata i on

Figure: Time schedule chart

Source: created by author

and collect data from everyone on the planet. The problem of random sampling will always

remain and the current research is not devoid of the same problems.

Time schedule

week 1 week 2 week 3 week 4 week 5 week 5 week 6 week 7 week 8 week 9 week 10

Milestones

Introducti on

Des i gni ng resea rch

objecti ves and defi ni ng

the scope

Des i gni ng the structure

Des i gni ng the res ea rch

questi ons

Literature review

Res ea rchi ng the journa l s

summari s i ng the arti cl es

Methodology

Des i gni ng res ea rch

approach

Identi fyi ng sa mpl e tool s

and techni ques

Conducti ng pri mary

res earch surveys and

i ntervi ews

Al i gni ng the s econdary

col l ected da ta

Findings and analysis

Usi ng di fferent tool s to

ana l yse the data set

Interpreti ng data

Ana nl ysi ng the data

Conclusion

Summary of res ea rch

Bui l d recommendata i on

Figure: Time schedule chart

Source: created by author

11CHALLENGES IN ACCOUNTING IN GLOBAL FINANCE

Conclusion

From the above discussion it can be concluded that the problems faced by the global

companies in the context of financial accounting are very much an issue and the current research

would come in handy to identifying the most important and biggest problems. The research has

selected the methods in such a way that will facilitate in this regard and would most definitely

help to come up with probable solutions that would be of use to reduce the challenges. In the era

of globalization, companies have to adhere to a lot of aspects and in order to maintain a good

position in the industry and a good reputation, every single of these aspects have to be met.

Conclusion

From the above discussion it can be concluded that the problems faced by the global

companies in the context of financial accounting are very much an issue and the current research

would come in handy to identifying the most important and biggest problems. The research has

selected the methods in such a way that will facilitate in this regard and would most definitely

help to come up with probable solutions that would be of use to reduce the challenges. In the era

of globalization, companies have to adhere to a lot of aspects and in order to maintain a good

position in the industry and a good reputation, every single of these aspects have to be met.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.