Financial Management Report: Champion, Claudia & Alliance Co.

VerifiedAdded on 2022/10/28

|13

|2386

|20

Report

AI Summary

This comprehensive financial management report analyzes three distinct portfolios: Champion Co., Claudia Co., and Alliance Co. The report begins with Champion Co., calculating annual after-tax cash flow, net present value (NPV), and sensitivity analysis for an equipment investment. It then moves on to Claudia Co., detailing the cash conversion cycle (CCC) calculation, including Days Inventory Outstanding (DIO), Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO), along with a discussion of overtrading and strategies to mitigate it. Finally, the report assesses Alliance Co., calculating the current market value of a bond and the weighted average cost of capital (WACC). The analysis includes detailed workings, financial ratios, and strategic recommendations for each company's financial decisions. The report concludes with a reflection on the interplay of risk, uncertainty, and the impact of financial decisions on profitability.

Module Name: Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Portfolio 1: Champion Co................................................................................................................3

Task (i).........................................................................................................................................3

Annual after-tax cash flow.......................................................................................................3

Net Present value.....................................................................................................................5

Comments................................................................................................................................5

Task (ii)........................................................................................................................................6

Task (iii).......................................................................................................................................6

Portfolio 2: Claudia Co....................................................................................................................6

Task (a)........................................................................................................................................6

Task (b)........................................................................................................................................7

Task (c)........................................................................................................................................9

Task (d)......................................................................................................................................10

Task (e)......................................................................................................................................10

Portfolio 3: Alliance Co.................................................................................................................11

Task (i).......................................................................................................................................11

Task (b):.....................................................................................................................................11

Task (c)......................................................................................................................................11

References......................................................................................................................................13

2

Portfolio 1: Champion Co................................................................................................................3

Task (i).........................................................................................................................................3

Annual after-tax cash flow.......................................................................................................3

Net Present value.....................................................................................................................5

Comments................................................................................................................................5

Task (ii)........................................................................................................................................6

Task (iii).......................................................................................................................................6

Portfolio 2: Claudia Co....................................................................................................................6

Task (a)........................................................................................................................................6

Task (b)........................................................................................................................................7

Task (c)........................................................................................................................................9

Task (d)......................................................................................................................................10

Task (e)......................................................................................................................................10

Portfolio 3: Alliance Co.................................................................................................................11

Task (i).......................................................................................................................................11

Task (b):.....................................................................................................................................11

Task (c)......................................................................................................................................11

References......................................................................................................................................13

2

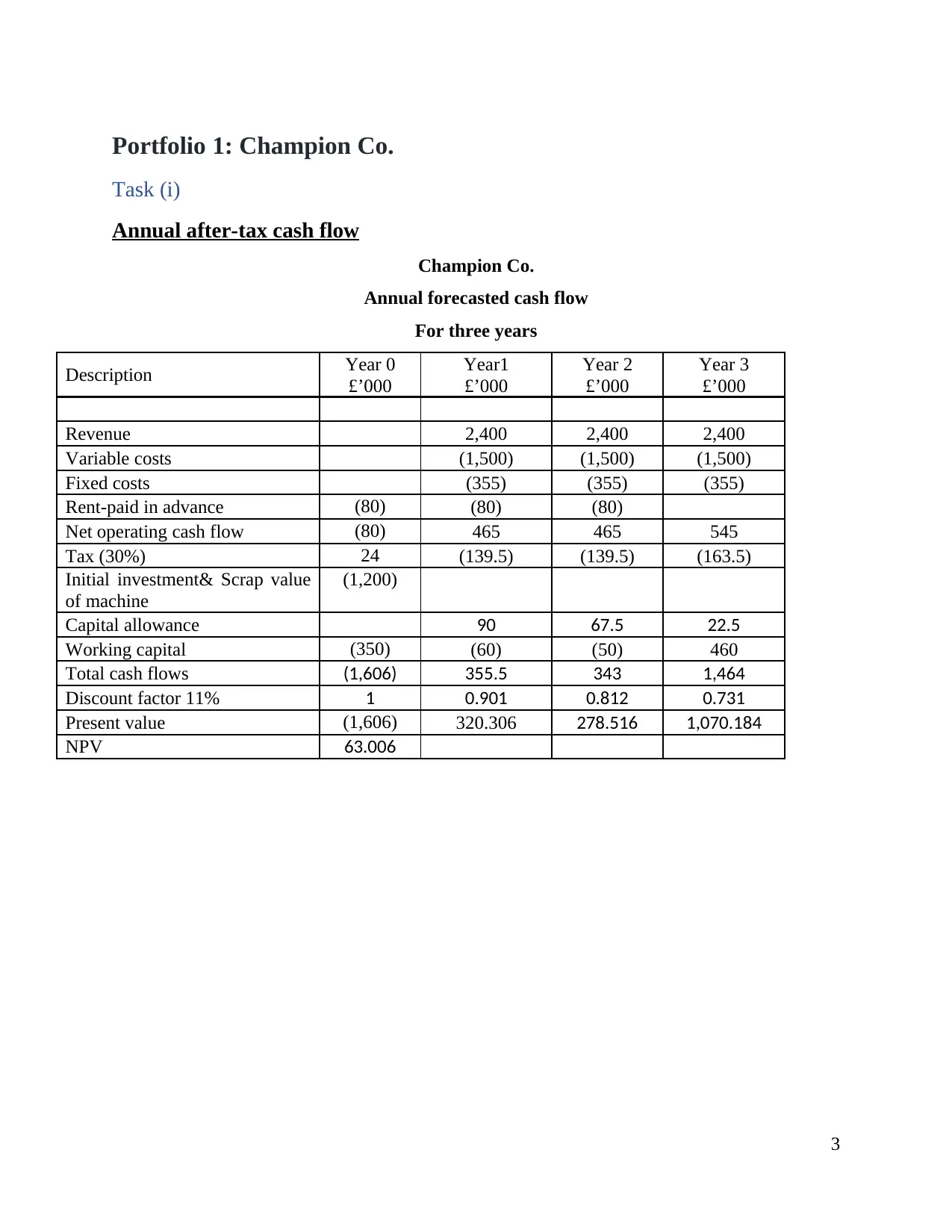

Portfolio 1: Champion Co.

Task (i)

Annual after-tax cash flow

Champion Co.

Annual forecasted cash flow

For three years

Description Year 0

£’000

Year1

£’000

Year 2

£’000

Year 3

£’000

Revenue 2,400 2,400 2,400

Variable costs (1,500) (1,500) (1,500)

Fixed costs (355) (355) (355)

Rent-paid in advance (80) (80) (80)

Net operating cash flow (80) 465 465 545

Tax (30%) 24 (139.5) (139.5) (163.5)

Initial investment& Scrap value

of machine

(1,200)

Capital allowance 90 67.5 22.5

Working capital (350) (60) (50) 460

Total cash flows (1,606) 355.5 343 1,464

Discount factor 11% 1 0.901 0.812 0.731

Present value (1,606) 320.306 278.516 1,070.184

NPV 63.006

3

Task (i)

Annual after-tax cash flow

Champion Co.

Annual forecasted cash flow

For three years

Description Year 0

£’000

Year1

£’000

Year 2

£’000

Year 3

£’000

Revenue 2,400 2,400 2,400

Variable costs (1,500) (1,500) (1,500)

Fixed costs (355) (355) (355)

Rent-paid in advance (80) (80) (80)

Net operating cash flow (80) 465 465 545

Tax (30%) 24 (139.5) (139.5) (163.5)

Initial investment& Scrap value

of machine

(1,200)

Capital allowance 90 67.5 22.5

Working capital (350) (60) (50) 460

Total cash flows (1,606) 355.5 343 1,464

Discount factor 11% 1 0.901 0.812 0.731

Present value (1,606) 320.306 278.516 1,070.184

NPV 63.006

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

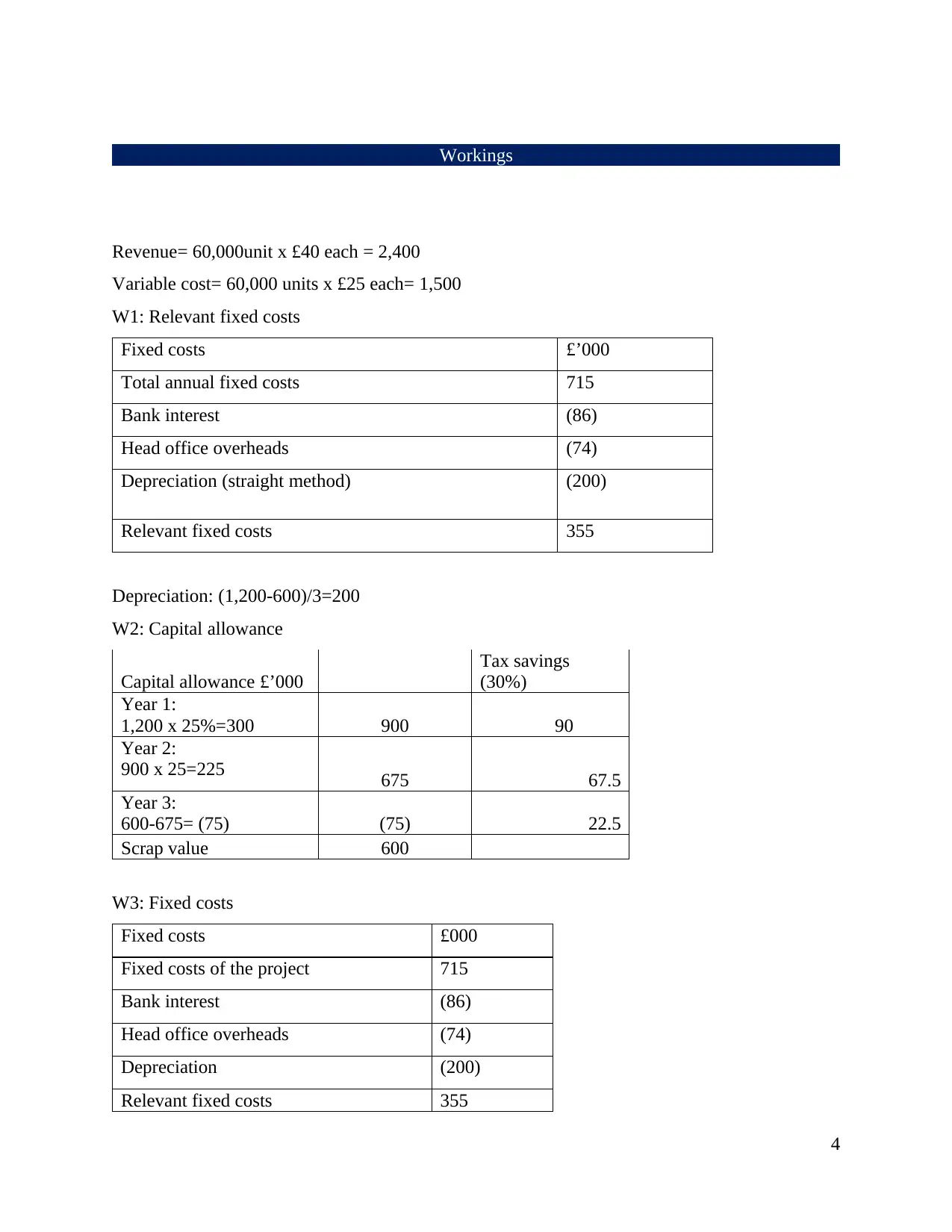

Workings

Revenue= 60,000unit x £40 each = 2,400

Variable cost= 60,000 units x £25 each= 1,500

W1: Relevant fixed costs

Fixed costs £’000

Total annual fixed costs 715

Bank interest (86)

Head office overheads (74)

Depreciation (straight method) (200)

Relevant fixed costs 355

Depreciation: (1,200-600)/3=200

W2: Capital allowance

Capital allowance £’000

Tax savings

(30%)

Year 1:

1,200 x 25%=300 900 90

Year 2:

900 x 25=225 675 67.5

Year 3:

600-675= (75) (75) 22.5

Scrap value 600

W3: Fixed costs

Fixed costs £000

Fixed costs of the project 715

Bank interest (86)

Head office overheads (74)

Depreciation (200)

Relevant fixed costs 355

4

Revenue= 60,000unit x £40 each = 2,400

Variable cost= 60,000 units x £25 each= 1,500

W1: Relevant fixed costs

Fixed costs £’000

Total annual fixed costs 715

Bank interest (86)

Head office overheads (74)

Depreciation (straight method) (200)

Relevant fixed costs 355

Depreciation: (1,200-600)/3=200

W2: Capital allowance

Capital allowance £’000

Tax savings

(30%)

Year 1:

1,200 x 25%=300 900 90

Year 2:

900 x 25=225 675 67.5

Year 3:

600-675= (75) (75) 22.5

Scrap value 600

W3: Fixed costs

Fixed costs £000

Fixed costs of the project 715

Bank interest (86)

Head office overheads (74)

Depreciation (200)

Relevant fixed costs 355

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Present value

Net Present value is an investment appraisal technique which compares current cash inflow with

current cash outflow. Basically, this appraisal technique is based on time value of money. Net

present value of the equipment has been calculated below:

Net Present Value = Sum of present value of net cash inflow – Initial Capital Investment

(Chandra, 2018). As NPV is positive, this equipment can be procured.

Sensitivity of annual sales unit =Present value of after tax-tax contribution= (40-25)

x60,000units=900,000x0.70x2.44=1,537.2

Sensitivity margin= ((NPV/PV of after -tax contribution) x100=63.006/1,537.2 x100=4.09%

Sensitivity of sales proceed of the equipment = PV of after sales proceed =

600,000x0.7x0.731=307,020

Sensitivity to sales proceed = 63,006/307,020x100=20.52%

Comments

If the annual sales decreases from this quantity, then the company can not gain positive cash

flow from this equipment. Here if we assume that the entity can not able to manage to sell 60,000

quantity per annum rather it can sale 50,000. Then the entire cash flow and Net present value

will be changed. On the other hand, the company has assumed that it can gain 50% of the cost of

the equipment after three years but in real life it is quite difficult because after usage an

equipment’s capability of producing more products decreases. And due to this, there is high

chance that the company will not be able to sell at 50% of the cost value. Assume, the company

can sell the equipment at 300,000and it can sell 50,000 quantity annually. Then NPV will

become,

From the above hypothetical calculation, it is clear that if the company can not manage to sell the

budgeted quantity, then the net present value will become negative. This may also impact the

cash flow during the useful life of the equipment.

5

Net Present value is an investment appraisal technique which compares current cash inflow with

current cash outflow. Basically, this appraisal technique is based on time value of money. Net

present value of the equipment has been calculated below:

Net Present Value = Sum of present value of net cash inflow – Initial Capital Investment

(Chandra, 2018). As NPV is positive, this equipment can be procured.

Sensitivity of annual sales unit =Present value of after tax-tax contribution= (40-25)

x60,000units=900,000x0.70x2.44=1,537.2

Sensitivity margin= ((NPV/PV of after -tax contribution) x100=63.006/1,537.2 x100=4.09%

Sensitivity of sales proceed of the equipment = PV of after sales proceed =

600,000x0.7x0.731=307,020

Sensitivity to sales proceed = 63,006/307,020x100=20.52%

Comments

If the annual sales decreases from this quantity, then the company can not gain positive cash

flow from this equipment. Here if we assume that the entity can not able to manage to sell 60,000

quantity per annum rather it can sale 50,000. Then the entire cash flow and Net present value

will be changed. On the other hand, the company has assumed that it can gain 50% of the cost of

the equipment after three years but in real life it is quite difficult because after usage an

equipment’s capability of producing more products decreases. And due to this, there is high

chance that the company will not be able to sell at 50% of the cost value. Assume, the company

can sell the equipment at 300,000and it can sell 50,000 quantity annually. Then NPV will

become,

From the above hypothetical calculation, it is clear that if the company can not manage to sell the

budgeted quantity, then the net present value will become negative. This may also impact the

cash flow during the useful life of the equipment.

5

Task (ii)

As per the given value of Champion, the company will incur negative cash flow at the first year

because at this year, the company will have to purchase the equipment, and this will engage 1.2

million amounts of money. And in the third year, the company will be incurring highest amount

of cash flow because in that year the company is assuming that it can recover the scrap value and

investment in working capital. But after analysing the hypothetical values of scrap value and

Sales amount, it can be concluded that the company should analysis the market again based on

real data value. Otherwise, there is high chance of getting negative cash flow and negative net

present value.

Task (iii)

Risk describes a situation where there is a half chance of being successful on the other hand

uncertainty refers to the condition of the situation where an investor is not sure about the

outcome. Normally these two terms are interrelated but first one describes about a situation and

the second describes about the condition of the situation. For example, Investor is investing in a

project but the project risky. And the reason of risk is that the investor is not sure about whether

he will get outcome from the project. This insecurity is uncertainty.

Methods to incorporate risk or uncertainty are:

1. Certainty Equivalent Method: In this method, cash flows are adjusted with reflective project

risk.

2. Risk-adjusted discount rate method: Under this method, differential project risk is considered

by changing the discount rate of the project’s average rate of return.

Portfolio 2: Claudia Co.

Task (a)

Cash Conversion cycle is basically a metric which provides the minimum time to the company

within which the company can convert its investment in working capital into cash. Here working

capital means inventory, accounts receivables, accrued revenue etc. There are some key points of

Cash conversion cycle:

It expresses the length of time within which a company will recover its investment in the

working capital.

6

As per the given value of Champion, the company will incur negative cash flow at the first year

because at this year, the company will have to purchase the equipment, and this will engage 1.2

million amounts of money. And in the third year, the company will be incurring highest amount

of cash flow because in that year the company is assuming that it can recover the scrap value and

investment in working capital. But after analysing the hypothetical values of scrap value and

Sales amount, it can be concluded that the company should analysis the market again based on

real data value. Otherwise, there is high chance of getting negative cash flow and negative net

present value.

Task (iii)

Risk describes a situation where there is a half chance of being successful on the other hand

uncertainty refers to the condition of the situation where an investor is not sure about the

outcome. Normally these two terms are interrelated but first one describes about a situation and

the second describes about the condition of the situation. For example, Investor is investing in a

project but the project risky. And the reason of risk is that the investor is not sure about whether

he will get outcome from the project. This insecurity is uncertainty.

Methods to incorporate risk or uncertainty are:

1. Certainty Equivalent Method: In this method, cash flows are adjusted with reflective project

risk.

2. Risk-adjusted discount rate method: Under this method, differential project risk is considered

by changing the discount rate of the project’s average rate of return.

Portfolio 2: Claudia Co.

Task (a)

Cash Conversion cycle is basically a metric which provides the minimum time to the company

within which the company can convert its investment in working capital into cash. Here working

capital means inventory, accounts receivables, accrued revenue etc. There are some key points of

Cash conversion cycle:

It expresses the length of time within which a company will recover its investment in the

working capital.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This metric considers the time which is required by a company to sell its inventory. Also,

the time is required to collect cash from trade receivables, and the time within which the

company can pay the bill without incurring any penalties.

Cash Conversion cycle is not same for all types of business rather it differs from industry

to industry.

Cash Conversion cycle is important in determining the requirement for working capital. Because

it provides the basis of assuming the required working capital. Through the days determined, a

company can easily make plan whether to continue current strategy or the strategy needs to be

changed.

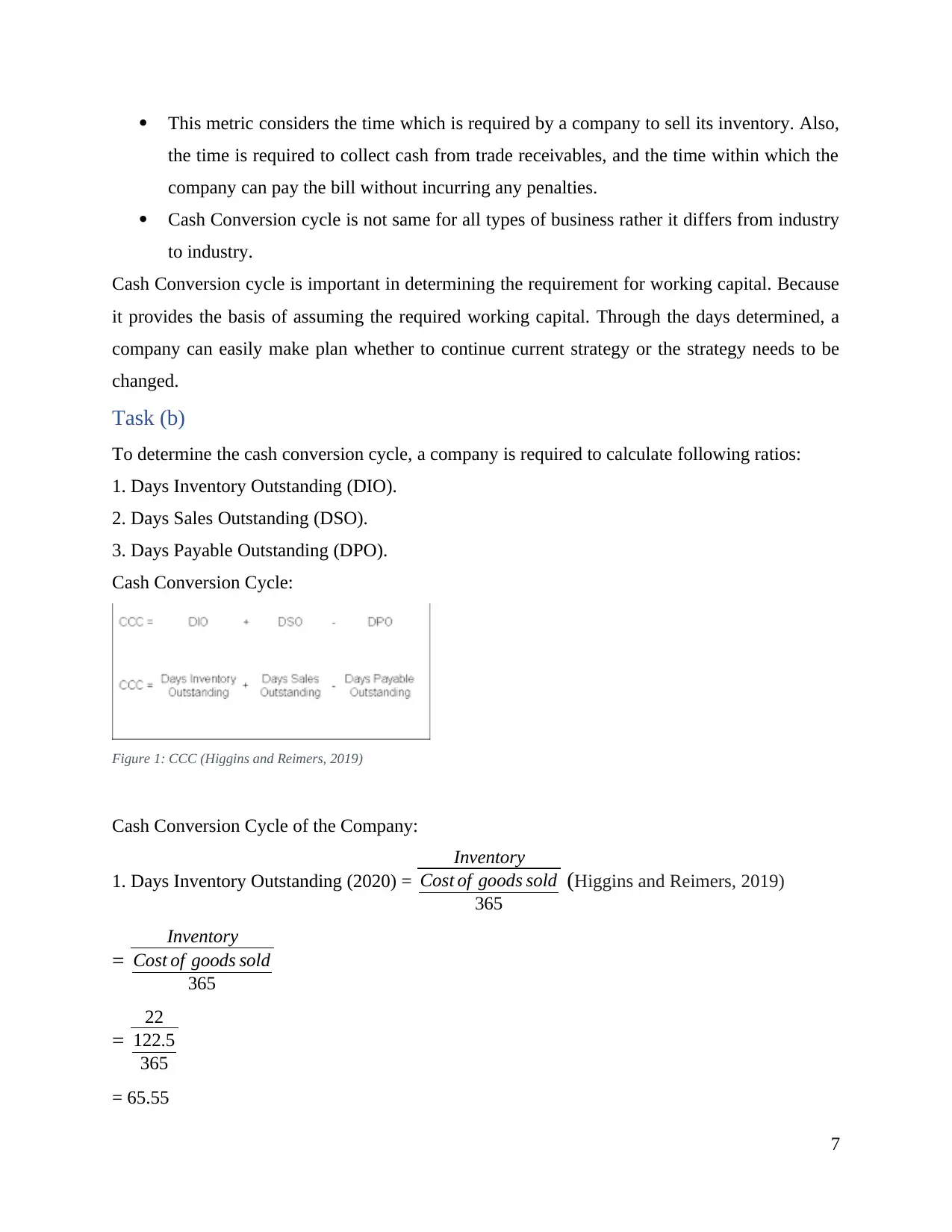

Task (b)

To determine the cash conversion cycle, a company is required to calculate following ratios:

1. Days Inventory Outstanding (DIO).

2. Days Sales Outstanding (DSO).

3. Days Payable Outstanding (DPO).

Cash Conversion Cycle:

Figure 1: CCC (Higgins and Reimers, 2019)

Cash Conversion Cycle of the Company:

1. Days Inventory Outstanding (2020) =

Inventory

Cost of goods sold

365

(Higgins and Reimers, 2019)

=

Inventory

Cost of goods sold

365

=

22

122.5

365

= 65.55

7

the time is required to collect cash from trade receivables, and the time within which the

company can pay the bill without incurring any penalties.

Cash Conversion cycle is not same for all types of business rather it differs from industry

to industry.

Cash Conversion cycle is important in determining the requirement for working capital. Because

it provides the basis of assuming the required working capital. Through the days determined, a

company can easily make plan whether to continue current strategy or the strategy needs to be

changed.

Task (b)

To determine the cash conversion cycle, a company is required to calculate following ratios:

1. Days Inventory Outstanding (DIO).

2. Days Sales Outstanding (DSO).

3. Days Payable Outstanding (DPO).

Cash Conversion Cycle:

Figure 1: CCC (Higgins and Reimers, 2019)

Cash Conversion Cycle of the Company:

1. Days Inventory Outstanding (2020) =

Inventory

Cost of goods sold

365

(Higgins and Reimers, 2019)

=

Inventory

Cost of goods sold

365

=

22

122.5

365

= 65.55

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 66 days.

Days Inventory Outstanding (2019) =

Inventory

Cost of goods sold

365

=

Inventory

Cost of goods sold

365

=

9.5

80.3

365

= 43 days.

Here, in the year 2019, DIO was less than that of the year 2020.

Working:

Average Inventory = (Inventory of 2020 + Inventory of 2019)/2

= (22+9.5)/2

= 15.75 million.

Cost of goods sold:

2019 2020

Revenue 89 131

Gross Profit 8.7 8.5

Cost of Goods Sold 80.3 122.5

2. Days Sales Outstanding (2020) =

Trade Receivables

Revenue

365

(Fabozzi and Peterson, 2018)

=

21 million

131 million

365

= 58.51 days.

Days Sales Outstanding (2019) =

Trade Receivables

Revenue

365

=

10.08 million

89 million

365

8

Days Inventory Outstanding (2019) =

Inventory

Cost of goods sold

365

=

Inventory

Cost of goods sold

365

=

9.5

80.3

365

= 43 days.

Here, in the year 2019, DIO was less than that of the year 2020.

Working:

Average Inventory = (Inventory of 2020 + Inventory of 2019)/2

= (22+9.5)/2

= 15.75 million.

Cost of goods sold:

2019 2020

Revenue 89 131

Gross Profit 8.7 8.5

Cost of Goods Sold 80.3 122.5

2. Days Sales Outstanding (2020) =

Trade Receivables

Revenue

365

(Fabozzi and Peterson, 2018)

=

21 million

131 million

365

= 58.51 days.

Days Sales Outstanding (2019) =

Trade Receivables

Revenue

365

=

10.08 million

89 million

365

8

= 44.29 days.

Here, in the year 2019, DSO was less than that of the year 2020.

Working:

Average Trade Receivables = (Trade Receivables at 2020 + Trade Receivables at 2019)/2

= (21+10.8)/2

= 15.9 million.

3. Days Payable Outstanding (2020) =

Trade Payables

Cost of goods sold

365

(Van Horne James, 2016)

=

20.5

122.5

365

= 61.08 Days.

Days Payable Outstanding (2019) =

Trade Payables

Cost of goods sold

365

= 8.2

80.3

365

= 37.27 Days.

Here, in the year 2019, DPO was less than that of the year 2020.

Cash Conversion Cycle (2020) = 66+59-61=64 days.

Cash Conversion Cycle (2019) = 43+44-37=50 days

The Cash Conversion Cycle is more than one month in both the years and it is below average of

the industry. The company need to reduce the days in trade receivables unless it will be difficult

for the company to operate day to day operation.

Task (c)

Year 2019 2020

Current Ratio 1.65 times 1.27 times

Quick Ratio 0.89 times 0.63 times

Sales/Net working capital 11 times 14 times

Turnover increase 47%

Non-current assets increase 12%

Inventory increase 131%

Receivable increase 94%

9

Here, in the year 2019, DSO was less than that of the year 2020.

Working:

Average Trade Receivables = (Trade Receivables at 2020 + Trade Receivables at 2019)/2

= (21+10.8)/2

= 15.9 million.

3. Days Payable Outstanding (2020) =

Trade Payables

Cost of goods sold

365

(Van Horne James, 2016)

=

20.5

122.5

365

= 61.08 Days.

Days Payable Outstanding (2019) =

Trade Payables

Cost of goods sold

365

= 8.2

80.3

365

= 37.27 Days.

Here, in the year 2019, DPO was less than that of the year 2020.

Cash Conversion Cycle (2020) = 66+59-61=64 days.

Cash Conversion Cycle (2019) = 43+44-37=50 days

The Cash Conversion Cycle is more than one month in both the years and it is below average of

the industry. The company need to reduce the days in trade receivables unless it will be difficult

for the company to operate day to day operation.

Task (c)

Year 2019 2020

Current Ratio 1.65 times 1.27 times

Quick Ratio 0.89 times 0.63 times

Sales/Net working capital 11 times 14 times

Turnover increase 47%

Non-current assets increase 12%

Inventory increase 131%

Receivable increase 94%

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Payable increase 150%

Overdraft increase 212%

Current Ratio:

2019: 20.5/12.4=1.65

2020: 43/33.6=1.27

Quick Ratio= (current assets-inventory)/current liabilities

2019: (20.5-9.5)/12.4=0.89

2020: (43-22)/33.6=0.63

Sales/Net working capital

2019: 89/ (20.5-12.4) =10.98

2020:131/ (43-33.6) = 13.93

Turnover increase: [(131/89) – 1x100]

Non-current assets increase: [(40.8/36.4)-1x100]

Inventory increase: [(22/9.5)-1x100]

Receivable increase: [(21/10.8)-1x100]

Payable increase: [(20.5/8.2)-1x100]

Overdraft increase: [(13.1/4.2)-1x100]

Overtrading means buying excessive and selling excessive stocks either by broker or investor.

From the given table, it can be understood that there is huge change in equity between 2019 and

2020. In the year 2020, 26.90 million equity and liabilities have been raised by the company.

And this is reasoning the company as incurred 7 million profit where operating profit was 8.5

million. The company has incurred higher finance cost due to overtrading.

Task (d)

Different Strategies to financing Working Capital:

1. A company can take advance from its customers.

2. It can negotiate with its trade payables to increase the credit period.

3. To finance the working capital the company can take bank overdraft.

4. Nowadays, several commercial banks are giving short term loan to the companies to finance

their working capital.

10

Overdraft increase 212%

Current Ratio:

2019: 20.5/12.4=1.65

2020: 43/33.6=1.27

Quick Ratio= (current assets-inventory)/current liabilities

2019: (20.5-9.5)/12.4=0.89

2020: (43-22)/33.6=0.63

Sales/Net working capital

2019: 89/ (20.5-12.4) =10.98

2020:131/ (43-33.6) = 13.93

Turnover increase: [(131/89) – 1x100]

Non-current assets increase: [(40.8/36.4)-1x100]

Inventory increase: [(22/9.5)-1x100]

Receivable increase: [(21/10.8)-1x100]

Payable increase: [(20.5/8.2)-1x100]

Overdraft increase: [(13.1/4.2)-1x100]

Overtrading means buying excessive and selling excessive stocks either by broker or investor.

From the given table, it can be understood that there is huge change in equity between 2019 and

2020. In the year 2020, 26.90 million equity and liabilities have been raised by the company.

And this is reasoning the company as incurred 7 million profit where operating profit was 8.5

million. The company has incurred higher finance cost due to overtrading.

Task (d)

Different Strategies to financing Working Capital:

1. A company can take advance from its customers.

2. It can negotiate with its trade payables to increase the credit period.

3. To finance the working capital the company can take bank overdraft.

4. Nowadays, several commercial banks are giving short term loan to the companies to finance

their working capital.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task (e)

Overtrading is a common incident in case of rapidly growing companies. To avoid overtrading,

Claudia can follow following strategies:

1. Can take lease or can purchase fixed assets on hire price.

2. Can bring more capital to the company.

3. They need to cut the unnecessary costs.

4. They need to be very cost effective and cost efficiency.

Portfolio 3: Alliance Co

Task (i)

Current Market Value of Bond:

I × [ 1− 1

(1+ Kd)n

Kd

+ MV

(1+ Kd)n ] (Brigham and Houston, 2021)

Here,

I = 20 Million * 8% = 1.60 Million.

Kd = 10% - (0.10*30%) = 7%.

n = 6 years

MV = 20 million

1.6 × [ 1− 1

(1+0.07)6

0.07

+ 20

(1+0.07)6 ]

= 7.62 + 13.33

= 20.96 Million.

Task (b):

Current weighted Average Cost:

Amount Weight

Share capital 20.00 18%

Reserves 60.00 55%

Bond A 20.00 18%

Bank Loan 10.00 9%

110.00 100%

11

Overtrading is a common incident in case of rapidly growing companies. To avoid overtrading,

Claudia can follow following strategies:

1. Can take lease or can purchase fixed assets on hire price.

2. Can bring more capital to the company.

3. They need to cut the unnecessary costs.

4. They need to be very cost effective and cost efficiency.

Portfolio 3: Alliance Co

Task (i)

Current Market Value of Bond:

I × [ 1− 1

(1+ Kd)n

Kd

+ MV

(1+ Kd)n ] (Brigham and Houston, 2021)

Here,

I = 20 Million * 8% = 1.60 Million.

Kd = 10% - (0.10*30%) = 7%.

n = 6 years

MV = 20 million

1.6 × [ 1− 1

(1+0.07)6

0.07

+ 20

(1+0.07)6 ]

= 7.62 + 13.33

= 20.96 Million.

Task (b):

Current weighted Average Cost:

Amount Weight

Share capital 20.00 18%

Reserves 60.00 55%

Bond A 20.00 18%

Bank Loan 10.00 9%

110.00 100%

11

WACC = 0.15*18% + 0.15*55% + 0.07*9% + 0.04*9% = 12%.

Here, Cost of Equity = 15%.

Cost of equity = Cost of reserve = 15%.

Cost of bond A = (0.10 – 0.10*30%) = 7%

Cost of bank Loan = LIBOR + 1% = 3% + 1% = 4%.

Task (c)

In the prior section, weighted average cost of capital of the company has already been calculated.

It seems that the cost of capital is not so high, but it can be compared with rate of return. Suppose

the rate of return is 16%, then the company’s cost capital is effective that the company has

managed to earn higher than the cost of capital. If the company raises more debt than the cost of

capital will be increased, and it will increase the finance cost. Though in the market, there is a

prediction of increasing the interest rate by 4%. Due to this increases the finance cost will also be

increased and in spite of having higher operating profit the company may incur low profit after

tax.

12

Here, Cost of Equity = 15%.

Cost of equity = Cost of reserve = 15%.

Cost of bond A = (0.10 – 0.10*30%) = 7%

Cost of bank Loan = LIBOR + 1% = 3% + 1% = 4%.

Task (c)

In the prior section, weighted average cost of capital of the company has already been calculated.

It seems that the cost of capital is not so high, but it can be compared with rate of return. Suppose

the rate of return is 16%, then the company’s cost capital is effective that the company has

managed to earn higher than the cost of capital. If the company raises more debt than the cost of

capital will be increased, and it will increase the finance cost. Though in the market, there is a

prediction of increasing the interest rate by 4%. Due to this increases the finance cost will also be

increased and in spite of having higher operating profit the company may incur low profit after

tax.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.