Impact of Lending Condition Changes on Real Estate Borrowing Costs

VerifiedAdded on 2023/01/18

|12

|3370

|82

Report

AI Summary

This report critically assesses the impact of changes in lending conditions on real estate borrowing costs, analyzing the roles of financial institutions, government regulations, and economic factors. It examines the effects of lending condition variations on real estate transactions and property investments, considering the implications of the 2008 financial crisis and subsequent policy implementations. The report explores the impact of rising interest rates, inflation, and employment on borrowing costs, and it highlights the importance of effective policies to avoid future financial crises. By utilizing secondary data sources, the report provides a detailed overview of the challenges faced by both lenders and borrowers, emphasizing the need for flexible and effective lending policies to stabilize economies and prevent adverse impacts on individuals and the global market. The analysis also covers the evolution of lending practices, including the impact of subprime mortgages and the role of government-sponsored entities, concluding with an emphasis on the importance of extra due diligence and the re-examination of lending metrics to mitigate risks.

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 1

CHANGES IN LENDING CONDITIONS AND ITS IMPACT ON REAL ESTATE

BORROWINGS

The Name Of The Class (Course)

Professor (Tutor)

The Name Of The School (University)

The City And State Where It Is Located

The Date

CHANGES IN LENDING CONDITIONS AND ITS IMPACT ON REAL ESTATE

BORROWINGS

The Name Of The Class (Course)

Professor (Tutor)

The Name Of The School (University)

The City And State Where It Is Located

The Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 2

EXECUTIVE SUMMARY

This report is based on assessment of variations in lending conditions that have influenced the

real estate borrowings. It also takes account of the combined role financial institutions and

government authorities in the implementation of effective policies and procedures to avoid

adverse circumstances in future. Furthermore, the assessment is also focused on the hurdles

that are faced by both lending institutions and borrowers, which acts a significant element for

every economy. The analysis also includes several other factors that are taken into

consideration by making use of secondary data sources in order to reflect a detailed view for

better understanding of recent variations in lending conditions.

EXECUTIVE SUMMARY

This report is based on assessment of variations in lending conditions that have influenced the

real estate borrowings. It also takes account of the combined role financial institutions and

government authorities in the implementation of effective policies and procedures to avoid

adverse circumstances in future. Furthermore, the assessment is also focused on the hurdles

that are faced by both lending institutions and borrowers, which acts a significant element for

every economy. The analysis also includes several other factors that are taken into

consideration by making use of secondary data sources in order to reflect a detailed view for

better understanding of recent variations in lending conditions.

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 3

IMPACT OF CHANGES IN LENDING CONDITIONS ON REAL ESTATE BORROWING

COSTS

The financial institutions have played a significant role in relation to real estate borrowing

costs, as these institutions lend the properties by imposing variable interest rates based on

existing economic conditions. It is also worth noticing that lending conditions also have a

major impact on varying behaviour of transactions and property investments. However, the

government regulators have also taken account of global financial crisis by implementing

measures to regulate mortgage in order to reduce debt to income and loan to value ratios

accordingly (Johnson and Li, 2013). These measures were introduced by keeping in view that

it might provide assistance in stabilizing house pricing and housing demand (Fang and

Munneke, 2017). On the other hand, the effectiveness of such policies cannot be determined

with the help of an empirical approach, rather a dynamic and comprehensive approach proves

helpful in evaluating the effectiveness. By taking account of national statistics and

government reports, it is also evident that the initiative was taken into consideration by

announcing a comprehensive real estate program to regulate mortgage lending through large

financial institutions (Peng, 2018).

Financial Debt Crisis

However, there was a major collapse of investment bank known as Lehman Brothers as they

exposed themselves to excessive risk due to which financial crisis came into existence. There

were also significant bailouts of several other financial institutions due to the implementation

of stringent fiscal and monetary policies to prevent further collapse to world’s financial

system. In 2008, this major collapse led to the economic downturn due to which strict lending

conditions were imposed in relation to real estate borrowing (Luque, 2017). There were

massive mortgage approval rates due to which housing prices also increased by a greater

IMPACT OF CHANGES IN LENDING CONDITIONS ON REAL ESTATE BORROWING

COSTS

The financial institutions have played a significant role in relation to real estate borrowing

costs, as these institutions lend the properties by imposing variable interest rates based on

existing economic conditions. It is also worth noticing that lending conditions also have a

major impact on varying behaviour of transactions and property investments. However, the

government regulators have also taken account of global financial crisis by implementing

measures to regulate mortgage in order to reduce debt to income and loan to value ratios

accordingly (Johnson and Li, 2013). These measures were introduced by keeping in view that

it might provide assistance in stabilizing house pricing and housing demand (Fang and

Munneke, 2017). On the other hand, the effectiveness of such policies cannot be determined

with the help of an empirical approach, rather a dynamic and comprehensive approach proves

helpful in evaluating the effectiveness. By taking account of national statistics and

government reports, it is also evident that the initiative was taken into consideration by

announcing a comprehensive real estate program to regulate mortgage lending through large

financial institutions (Peng, 2018).

Financial Debt Crisis

However, there was a major collapse of investment bank known as Lehman Brothers as they

exposed themselves to excessive risk due to which financial crisis came into existence. There

were also significant bailouts of several other financial institutions due to the implementation

of stringent fiscal and monetary policies to prevent further collapse to world’s financial

system. In 2008, this major collapse led to the economic downturn due to which strict lending

conditions were imposed in relation to real estate borrowing (Luque, 2017). There were

massive mortgage approval rates due to which housing prices also increased by a greater

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 4

proportion and this rapid increase in delinquency rates also gave rise to the devaluation of

financial instruments i.e. mortgage backed securities. Hence, those financial institutions who

have made large investments started to face a liquidity crisis due to a reduction in value of

financial instruments (Hoesli and Reka, 2015). The federal government took a significant

initiative after this collapse and made an investment of almost $85 billion due to which there

was a massive rise in borrowing costs and lending conditions were re-considered by

government authorities to reduce such incidents in future. However, the recent changes in

lending conditions also have an impact on borrowing costs as it can still be seen across the

globe by taking account of rising interest rates and inflation due to revised and stringent

policies imposed by various economies. Furthermore, variation in lending conditions has also

affected employment and if effective measures are not taken then it can further deteriorate the

existing economic conditions. The real estate borrowing crisis has also played vital role in a

reduction of consumer wealth, failure of key business operations, and inefficiency in

economic activity leading to great recession. In 2006, financial crisis also provided easier

access to subprime borrowers due to which the housing prices escalated further (Pavlov and

Wachter, 2010). Hence, it became difficult for the individuals to repay the principal amount

of loan at higher interest rates, and financial institutions also faced problems in offering lower

interest rates due to a rise in bankruptcy cases.

REAL ESTATE BORROWING COSTS AND LENDING SITUATION

In addition to this, the primary reason of increase in borrowing costs was that the financial

institutions began to lend a higher amount of loan at lower interest rates initially, but later on

housing prices began to fluctuate and relaxation in lending conditions also gave rise to the

real estate bubble. The consumers were facing higher amount of debts due to which they had

to sell their properties below fair value and based upon the existing conditions in market.

Such incidents led to a rise in debt-ratio and significant losses had to be borne by both real

proportion and this rapid increase in delinquency rates also gave rise to the devaluation of

financial instruments i.e. mortgage backed securities. Hence, those financial institutions who

have made large investments started to face a liquidity crisis due to a reduction in value of

financial instruments (Hoesli and Reka, 2015). The federal government took a significant

initiative after this collapse and made an investment of almost $85 billion due to which there

was a massive rise in borrowing costs and lending conditions were re-considered by

government authorities to reduce such incidents in future. However, the recent changes in

lending conditions also have an impact on borrowing costs as it can still be seen across the

globe by taking account of rising interest rates and inflation due to revised and stringent

policies imposed by various economies. Furthermore, variation in lending conditions has also

affected employment and if effective measures are not taken then it can further deteriorate the

existing economic conditions. The real estate borrowing crisis has also played vital role in a

reduction of consumer wealth, failure of key business operations, and inefficiency in

economic activity leading to great recession. In 2006, financial crisis also provided easier

access to subprime borrowers due to which the housing prices escalated further (Pavlov and

Wachter, 2010). Hence, it became difficult for the individuals to repay the principal amount

of loan at higher interest rates, and financial institutions also faced problems in offering lower

interest rates due to a rise in bankruptcy cases.

REAL ESTATE BORROWING COSTS AND LENDING SITUATION

In addition to this, the primary reason of increase in borrowing costs was that the financial

institutions began to lend a higher amount of loan at lower interest rates initially, but later on

housing prices began to fluctuate and relaxation in lending conditions also gave rise to the

real estate bubble. The consumers were facing higher amount of debts due to which they had

to sell their properties below fair value and based upon the existing conditions in market.

Such incidents led to a rise in debt-ratio and significant losses had to be borne by both real

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 5

estate owners and financial institutions. It also had a major influence on those ventures that

were expected to give higher returns in future, but banks were not able to generate sufficient

returns for stakeholders due to liquidity crisis and present lending conditions in the market. It

is also argued that financial agreements including collateralized debt obligations and

mortgage-backed securities also reflected an increase because it derived the value from

increased housing prices and mortgage payments (Giambona, Golec and Schwienbacher,

2013). However, this financial innovation allowed the shareholders and banks to make large

investments in the US housing market. Hence, financial institutions faced significant losses

who made huge investments in real estate properties during a fall in housing prices across the

globe. The lenders were also allowed to enter foreclosure due to a presence of financial

incentive due to lower housing prices in comparison to mortgage. Based on national

statistics, the real estate owners have lost a significant amount of wealth approximately up to

$4.2 trillion from home equity (Peng, 2018). However, ratio of losses and debts also

increased in relation to other loans because financial crisis also affected the rest of the parts

of economy. Further to this, US regulatory authorities have also placed emphasis on

deregulation in order to encourage business that has resulted in reduced disclosure of

information and monitoring of activities with regard to recent policies undertaken by

evolving financial institutions. However, if the general public is not allowed to have an

access to detailed information, then real estate owners can face an adverse impact while

making effective decisions due to lack of credible information. It is evident that policy

makers were not able to recognise the role of hedge funds and investment banks, which is

also referred to as shadow banking system.

The experts believe that these institutions have become as significant as commercial

depository banks in terms of lending credit to economy, but they may be subject to different

regulations (Lee, 2017). Despite this, central banks have encouraged lending institutions to

estate owners and financial institutions. It also had a major influence on those ventures that

were expected to give higher returns in future, but banks were not able to generate sufficient

returns for stakeholders due to liquidity crisis and present lending conditions in the market. It

is also argued that financial agreements including collateralized debt obligations and

mortgage-backed securities also reflected an increase because it derived the value from

increased housing prices and mortgage payments (Giambona, Golec and Schwienbacher,

2013). However, this financial innovation allowed the shareholders and banks to make large

investments in the US housing market. Hence, financial institutions faced significant losses

who made huge investments in real estate properties during a fall in housing prices across the

globe. The lenders were also allowed to enter foreclosure due to a presence of financial

incentive due to lower housing prices in comparison to mortgage. Based on national

statistics, the real estate owners have lost a significant amount of wealth approximately up to

$4.2 trillion from home equity (Peng, 2018). However, ratio of losses and debts also

increased in relation to other loans because financial crisis also affected the rest of the parts

of economy. Further to this, US regulatory authorities have also placed emphasis on

deregulation in order to encourage business that has resulted in reduced disclosure of

information and monitoring of activities with regard to recent policies undertaken by

evolving financial institutions. However, if the general public is not allowed to have an

access to detailed information, then real estate owners can face an adverse impact while

making effective decisions due to lack of credible information. It is evident that policy

makers were not able to recognise the role of hedge funds and investment banks, which is

also referred to as shadow banking system.

The experts believe that these institutions have become as significant as commercial

depository banks in terms of lending credit to economy, but they may be subject to different

regulations (Lee, 2017). Despite this, central banks have encouraged lending institutions to

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 6

restore faith in commercial paper markets due to their importance in terms of funding

business activities. The government authorities have also focused on implementation of

economic stimulus programs by assuming other financial commitments. It came into

consideration that such huge financial crisis was avoidable but it happened due to breakdown

of corporate governance as the institutions were taking high risk by acting recklessly (Blake,

2016). Nowadays, extra due diligence EDD is performed by lending institutions by staying

focused on profile of customers because it might have an impact on future operations of an

organization. Further, real estate borrowing costs have become an integral factor for every

financial institution due to a relaxation in lending standards by commercial banks.

Additionally, mortgage lenders also focused on relaxation of underwriting standards when

there was competition between mortgage lenders for market share and higher revenues. The

proportion of subprime mortgage also increased due to competitive pressures preceding

financial debt crisis. However, government sponsored enterprises and US investment banks

focused on expansion of lending conditions in order to catch up with private lending

institutions. It was discovered by financial crisis inquiry commission that the primary reason

of financial crisis was not only related to affordable housing policies, although inefficient

policies of government authorities had an impact on real estate borrowing costs across the

globe. Based on SEC’s report, the severity of such crisis can also be determined by fraud

incidents that amounted to a total of almost $2 trillion in relation to 13 million substandard

loans. However, it came into existence due to the acquisition of loan by government-

sponsored entities on a large scale.

Besides, government officials have performed several investigations on subprime mortgages

because they also contributed to the rise in borrowing costs. This increase can also be tied to

floating rate debt or short-term loan holders because their interest rate will be higher in

comparison to fixed rate mortgages (Downs, Sebastian and Woltering, 2016). By taking

restore faith in commercial paper markets due to their importance in terms of funding

business activities. The government authorities have also focused on implementation of

economic stimulus programs by assuming other financial commitments. It came into

consideration that such huge financial crisis was avoidable but it happened due to breakdown

of corporate governance as the institutions were taking high risk by acting recklessly (Blake,

2016). Nowadays, extra due diligence EDD is performed by lending institutions by staying

focused on profile of customers because it might have an impact on future operations of an

organization. Further, real estate borrowing costs have become an integral factor for every

financial institution due to a relaxation in lending standards by commercial banks.

Additionally, mortgage lenders also focused on relaxation of underwriting standards when

there was competition between mortgage lenders for market share and higher revenues. The

proportion of subprime mortgage also increased due to competitive pressures preceding

financial debt crisis. However, government sponsored enterprises and US investment banks

focused on expansion of lending conditions in order to catch up with private lending

institutions. It was discovered by financial crisis inquiry commission that the primary reason

of financial crisis was not only related to affordable housing policies, although inefficient

policies of government authorities had an impact on real estate borrowing costs across the

globe. Based on SEC’s report, the severity of such crisis can also be determined by fraud

incidents that amounted to a total of almost $2 trillion in relation to 13 million substandard

loans. However, it came into existence due to the acquisition of loan by government-

sponsored entities on a large scale.

Besides, government officials have performed several investigations on subprime mortgages

because they also contributed to the rise in borrowing costs. This increase can also be tied to

floating rate debt or short-term loan holders because their interest rate will be higher in

comparison to fixed rate mortgages (Downs, Sebastian and Woltering, 2016). By taking

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 7

account of purchasing power parity theory, it is also evident that rise in borrowing costs can

have an impact on it as the individuals will face issues while making an acquisition of houses.

Hence, government authorities should introduce flexible but effective policies for lending

institutions so that such financial issues can be avoided in future because continuity of such

incidents can adversely affect future prospects of an economy and world at large. In 2017,

significant changes were made in lending conditions in order to minimize the number of

interest-only lending under which lending institutions issued loans to the borrowers. This

reduction allowed the individuals to borrow for 80% of a property’s value and most of the

investors will now be required to raise approximately 20% as down payment for property

acquisition.

Recent Variations In Conditions Related To Lending

Moreover, further restrictions are also imposed in which the government wants that lenders

should re-examine their metrics with regard to serviceability. The lenders use this in order to

define the ability of an acquirer as if he will be able to repay interest and principal amount

according to the loan agreement between both parties by taking account of individual’s

expenses and level of income (Raya and Kucel, 2015). Hence, recent changes in lending

conditions require financial institutions to give an assurance that their metrics have the ability

to meet existing market conditions in relation to real estate borrowing costs. However, by

considering the high-risk loans, it can place significant amount of risk on both borrower and

lender, as the borrower might go bankrupt on his payment schedule, and lending institution

may have to record bad debts that cannot be recovered later. This will also affect the

statement of financial position of any organization due to significant property losses, and

lending institution’s goodwill will also be exposed to higher risk in comparison to the rest of

competitors operating in same market segment. Despite this, it is clear that each home loan

has a principal behind it, which represents total sum of loan or principal that has to be repaid

account of purchasing power parity theory, it is also evident that rise in borrowing costs can

have an impact on it as the individuals will face issues while making an acquisition of houses.

Hence, government authorities should introduce flexible but effective policies for lending

institutions so that such financial issues can be avoided in future because continuity of such

incidents can adversely affect future prospects of an economy and world at large. In 2017,

significant changes were made in lending conditions in order to minimize the number of

interest-only lending under which lending institutions issued loans to the borrowers. This

reduction allowed the individuals to borrow for 80% of a property’s value and most of the

investors will now be required to raise approximately 20% as down payment for property

acquisition.

Recent Variations In Conditions Related To Lending

Moreover, further restrictions are also imposed in which the government wants that lenders

should re-examine their metrics with regard to serviceability. The lenders use this in order to

define the ability of an acquirer as if he will be able to repay interest and principal amount

according to the loan agreement between both parties by taking account of individual’s

expenses and level of income (Raya and Kucel, 2015). Hence, recent changes in lending

conditions require financial institutions to give an assurance that their metrics have the ability

to meet existing market conditions in relation to real estate borrowing costs. However, by

considering the high-risk loans, it can place significant amount of risk on both borrower and

lender, as the borrower might go bankrupt on his payment schedule, and lending institution

may have to record bad debts that cannot be recovered later. This will also affect the

statement of financial position of any organization due to significant property losses, and

lending institution’s goodwill will also be exposed to higher risk in comparison to the rest of

competitors operating in same market segment. Despite this, it is clear that each home loan

has a principal behind it, which represents total sum of loan or principal that has to be repaid

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 8

to lending institution. However, payment structure is simple in traditional mortgage system in

which real estate owners are required to make payments each month that will result in a

reduction of principal amount (LaCour-Little, 2001). Hence, interest amount is only paid on

the remaining principal each month, and these type of borrowings are referred to as principal

and interest home loans. On the other hand, interest only lending varies from traditional

mortgage system, which requires the real estate owner to repay the interest amount only

instead of principal. It means that the total sum of principal amount does not decrease for a

duration of interest only time span (Park, Matkin and Marlowe, 2016). There may be several

reasons for which the investors might prefer this option as loans are normally used by the

borrowers in order to avoid an influence on their monthly outflows. It can usually provide

assistance when it comes to the management of diverse portfolios, which will ultimately help

in generating positive cash flows (Downs and Xu, 2014). The investors can also make

savings by making an investment in another venture from which they can generate sufficient

returns through which they can also claim tax-incentives. However, once the interest only

time period comes to an end, the principal amount still has to be repaid as the real estate

owner has to make repayments for the remaining timeline of loan and investors can also face

difficulties due to inefficient preparation.

Market Reports And Analysis

Based upon analysis, government authorities and lending institutions should devise

reasonable measures for borrowers before allowing them to enter into any loan agreement

because pre-cautionary measures can allow the banks to make effective policies by focusing

on its liquidity position and customer profile. Besides, the market reports on mortgage

represents that the outstanding value of residential loans has increased by 3.3% in comparison

to previous year and the value of gross mortgage advances have reflected an increase of

almost 5.5% respectively (Marketresearch.com, 2019). However, the ratio of lending to home

to lending institution. However, payment structure is simple in traditional mortgage system in

which real estate owners are required to make payments each month that will result in a

reduction of principal amount (LaCour-Little, 2001). Hence, interest amount is only paid on

the remaining principal each month, and these type of borrowings are referred to as principal

and interest home loans. On the other hand, interest only lending varies from traditional

mortgage system, which requires the real estate owner to repay the interest amount only

instead of principal. It means that the total sum of principal amount does not decrease for a

duration of interest only time span (Park, Matkin and Marlowe, 2016). There may be several

reasons for which the investors might prefer this option as loans are normally used by the

borrowers in order to avoid an influence on their monthly outflows. It can usually provide

assistance when it comes to the management of diverse portfolios, which will ultimately help

in generating positive cash flows (Downs and Xu, 2014). The investors can also make

savings by making an investment in another venture from which they can generate sufficient

returns through which they can also claim tax-incentives. However, once the interest only

time period comes to an end, the principal amount still has to be repaid as the real estate

owner has to make repayments for the remaining timeline of loan and investors can also face

difficulties due to inefficient preparation.

Market Reports And Analysis

Based upon analysis, government authorities and lending institutions should devise

reasonable measures for borrowers before allowing them to enter into any loan agreement

because pre-cautionary measures can allow the banks to make effective policies by focusing

on its liquidity position and customer profile. Besides, the market reports on mortgage

represents that the outstanding value of residential loans has increased by 3.3% in comparison

to previous year and the value of gross mortgage advances have reflected an increase of

almost 5.5% respectively (Marketresearch.com, 2019). However, the ratio of lending to home

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 9

movers has reduced by 0.9 percentage points as a basic component of lending for the

acquisition of real estate. It can be argued by taking account of these statistics that there is

still requirement for making enhancement in lending policies, as the banks should involve

regulatory authorities that can provide assistance in retaining liquidity position because it is

vital to avoid going concern issues in the long term.

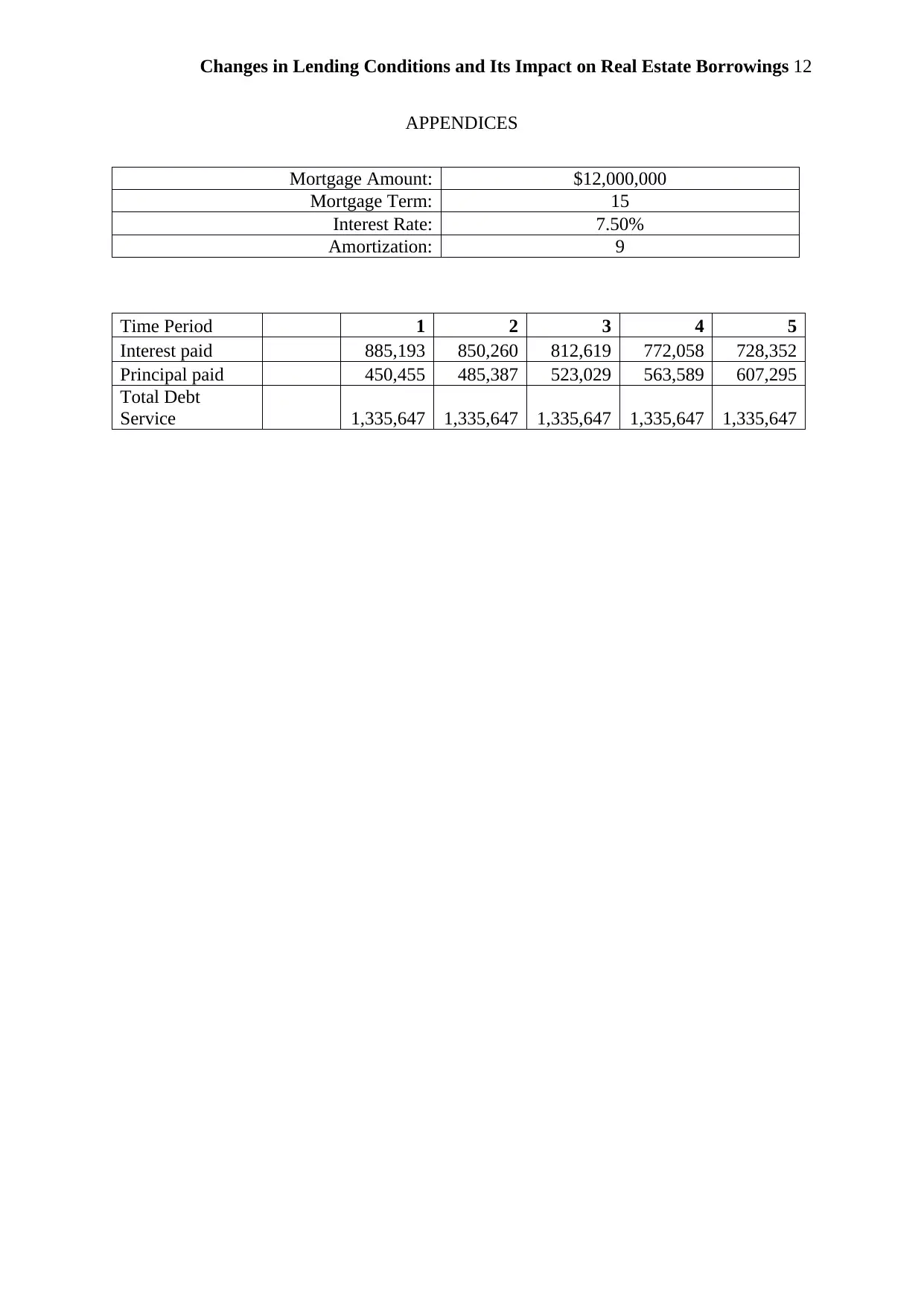

CALCULATION AND EXPLANATION

As per the appendices, the total sum of mortgage amount is considered to be as $12m,

mortgage term is 15 years, the interest rate is 7.50% and amortization is 9 respectively.

Hence, the net principal and interest amount reflects a fall with the passage of time due to

timely repayments by borrowers. However, total amount of debt service will remain constant

after each payment of interest and principal amount. Besides, if the anticipated holding period

is effectively agreed and managed between borrower and lending institution, then the whole

amount of loan can be repaid on an agreed schedule, which will prove beneficial for both

parties due to timely settlement of cash flows. Furthermore, the interest amount can also be

varied based on existing conditions in real estate sector, and overall economy.

Hence, it can be concluded that rising interest rates can adversely affect both economy, and

lending institutions. Besides, it will also have an impact on purchasing power of borrowers as

per purchasing power parity theory. The financial institutions should take account of interest

rate policies because it acts as a key indicator in relation to real estate borrowings. In existing

scenario, the interest rate on principal amount of mortgage appears to be slightly normal and

if payments are made as per agreed schedule, then it will allow borrowers to avoid

bankruptcy issues. In the end, lending conditions should be flexible to encourage the

proportion of safe borrowings, and it will also increase the profits of an organization.

movers has reduced by 0.9 percentage points as a basic component of lending for the

acquisition of real estate. It can be argued by taking account of these statistics that there is

still requirement for making enhancement in lending policies, as the banks should involve

regulatory authorities that can provide assistance in retaining liquidity position because it is

vital to avoid going concern issues in the long term.

CALCULATION AND EXPLANATION

As per the appendices, the total sum of mortgage amount is considered to be as $12m,

mortgage term is 15 years, the interest rate is 7.50% and amortization is 9 respectively.

Hence, the net principal and interest amount reflects a fall with the passage of time due to

timely repayments by borrowers. However, total amount of debt service will remain constant

after each payment of interest and principal amount. Besides, if the anticipated holding period

is effectively agreed and managed between borrower and lending institution, then the whole

amount of loan can be repaid on an agreed schedule, which will prove beneficial for both

parties due to timely settlement of cash flows. Furthermore, the interest amount can also be

varied based on existing conditions in real estate sector, and overall economy.

Hence, it can be concluded that rising interest rates can adversely affect both economy, and

lending institutions. Besides, it will also have an impact on purchasing power of borrowers as

per purchasing power parity theory. The financial institutions should take account of interest

rate policies because it acts as a key indicator in relation to real estate borrowings. In existing

scenario, the interest rate on principal amount of mortgage appears to be slightly normal and

if payments are made as per agreed schedule, then it will allow borrowers to avoid

bankruptcy issues. In the end, lending conditions should be flexible to encourage the

proportion of safe borrowings, and it will also increase the profits of an organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 10

REFERENCES

Pavlov, A. and Wachter, S. (2010). Subprime Lending and Real Estate Prices. Real Estate

Economics, 39(1), pp.1-17.

Fang, L. and Munneke, H. (2017). Gender Equality in Mortgage Lending. Real Estate

Economics.

Luque, J. (2017). Cross-Border Residential Lending: Theory and Evidence from the

European Sovereign Debt Crisis. Real Estate Economics.

LaCour-Little, M., Yu, W. and Sun, L. (2013). The Role of Home Equity Lending in the

Recent Mortgage Crisis. Real Estate Economics, 42(1), pp.153-189.

Johnson, K. and Li, G. (2013). Are Adjustable-Rate Mortgage Borrowers Borrowing

Constrained?. Real Estate Economics, 42(2), pp.457-471.

Downs, D. and Xu, P. (2014). Commercial Real Estate, Distress and Financial Resolution:

Portfolio Lending Versus Securitization. The Journal of Real Estate Finance and Economics,

51(2), pp.254-287.

Blake, T. (2016). Commuting Costs and Geographic Sorting in the Housing Market. Real

Estate Economics.

Raya, J. and Kucel, A. (2015). Did Housing Taxation Contribute to Increase Riskier

Borrowing?. The Journal of Real Estate Finance and Economics, 53(1), pp.90-113.

Marketresearch.com. (2019). Credit & Loans Market Research Reports & Credit & Loans

Industry Analysis | MarketResearch.com. [online] Available at:

https://www.marketresearch.com/Service-Industries-c1598/Financial-Services-c83/Credit-

Loans-c415/ [Accessed 14 Apr. 2019].

REFERENCES

Pavlov, A. and Wachter, S. (2010). Subprime Lending and Real Estate Prices. Real Estate

Economics, 39(1), pp.1-17.

Fang, L. and Munneke, H. (2017). Gender Equality in Mortgage Lending. Real Estate

Economics.

Luque, J. (2017). Cross-Border Residential Lending: Theory and Evidence from the

European Sovereign Debt Crisis. Real Estate Economics.

LaCour-Little, M., Yu, W. and Sun, L. (2013). The Role of Home Equity Lending in the

Recent Mortgage Crisis. Real Estate Economics, 42(1), pp.153-189.

Johnson, K. and Li, G. (2013). Are Adjustable-Rate Mortgage Borrowers Borrowing

Constrained?. Real Estate Economics, 42(2), pp.457-471.

Downs, D. and Xu, P. (2014). Commercial Real Estate, Distress and Financial Resolution:

Portfolio Lending Versus Securitization. The Journal of Real Estate Finance and Economics,

51(2), pp.254-287.

Blake, T. (2016). Commuting Costs and Geographic Sorting in the Housing Market. Real

Estate Economics.

Raya, J. and Kucel, A. (2015). Did Housing Taxation Contribute to Increase Riskier

Borrowing?. The Journal of Real Estate Finance and Economics, 53(1), pp.90-113.

Marketresearch.com. (2019). Credit & Loans Market Research Reports & Credit & Loans

Industry Analysis | MarketResearch.com. [online] Available at:

https://www.marketresearch.com/Service-Industries-c1598/Financial-Services-c83/Credit-

Loans-c415/ [Accessed 14 Apr. 2019].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 11

Lee, K. (2017). Borrowing Constraints and the Tenure Choice of Young Households. Konkuk

Research Institute of Real Estate and Urban Studies, 10(1), pp.205-223.

Peng, L. (2018). Benchmarking Local Commercial Real Estate Returns: Statistics Meets

Economics. Real Estate Economics.

Park, Y., Matkin, D. and Marlowe, J. (2016). Internal Control Deficiencies and Municipal

Borrowing Costs. Public Budgeting & Finance, 37(1), pp.88-111.

Peng, L. (2018). Benchmarking Local Commercial Real Estate Returns: Statistics Meets

Economics. Real Estate Economics.

Giambona, E., Golec, J. and Schwienbacher, A. (2013). Debt Capacity of Real Estate

Collateral. Real Estate Economics, 42(3), pp.578-605.

Hoesli, M. and Reka, K. (2015). Contagion Channels between Real Estate and Financial

Markets. Real Estate Economics, 43(1), pp.101-138.

Downs, D., Sebastian, S. and Woltering, R. (2016). Real Estate Fund Openings and

Cannibalization. Real Estate Economics, 45(4), pp.791-828.

Lee, K. (2017). Borrowing Constraints and the Tenure Choice of Young Households. Konkuk

Research Institute of Real Estate and Urban Studies, 10(1), pp.205-223.

Peng, L. (2018). Benchmarking Local Commercial Real Estate Returns: Statistics Meets

Economics. Real Estate Economics.

Park, Y., Matkin, D. and Marlowe, J. (2016). Internal Control Deficiencies and Municipal

Borrowing Costs. Public Budgeting & Finance, 37(1), pp.88-111.

Peng, L. (2018). Benchmarking Local Commercial Real Estate Returns: Statistics Meets

Economics. Real Estate Economics.

Giambona, E., Golec, J. and Schwienbacher, A. (2013). Debt Capacity of Real Estate

Collateral. Real Estate Economics, 42(3), pp.578-605.

Hoesli, M. and Reka, K. (2015). Contagion Channels between Real Estate and Financial

Markets. Real Estate Economics, 43(1), pp.101-138.

Downs, D., Sebastian, S. and Woltering, R. (2016). Real Estate Fund Openings and

Cannibalization. Real Estate Economics, 45(4), pp.791-828.

Changes in Lending Conditions and Its Impact on Real Estate Borrowings 12

APPENDICES

Mortgage Amount: $12,000,000

Mortgage Term: 15

Interest Rate: 7.50%

Amortization: 9

Time Period 1 2 3 4 5

Interest paid 885,193 850,260 812,619 772,058 728,352

Principal paid 450,455 485,387 523,029 563,589 607,295

Total Debt

Service 1,335,647 1,335,647 1,335,647 1,335,647 1,335,647

APPENDICES

Mortgage Amount: $12,000,000

Mortgage Term: 15

Interest Rate: 7.50%

Amortization: 9

Time Period 1 2 3 4 5

Interest paid 885,193 850,260 812,619 772,058 728,352

Principal paid 450,455 485,387 523,029 563,589 607,295

Total Debt

Service 1,335,647 1,335,647 1,335,647 1,335,647 1,335,647

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.