GreenEarth Corporation: Charlotte Mills Valuation & Acquisition

VerifiedAdded on 2023/04/20

|10

|1985

|318

Case Study

AI Summary

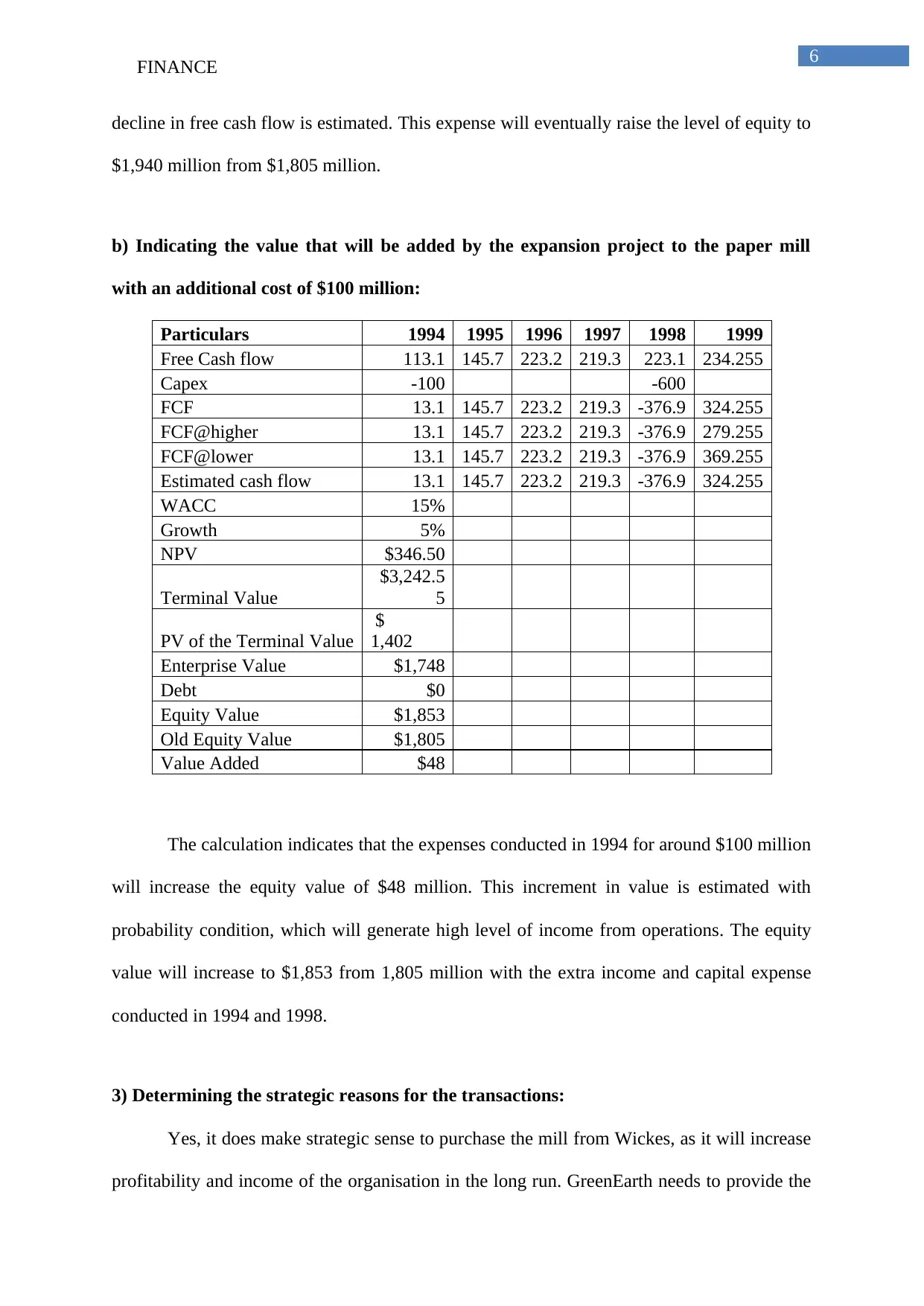

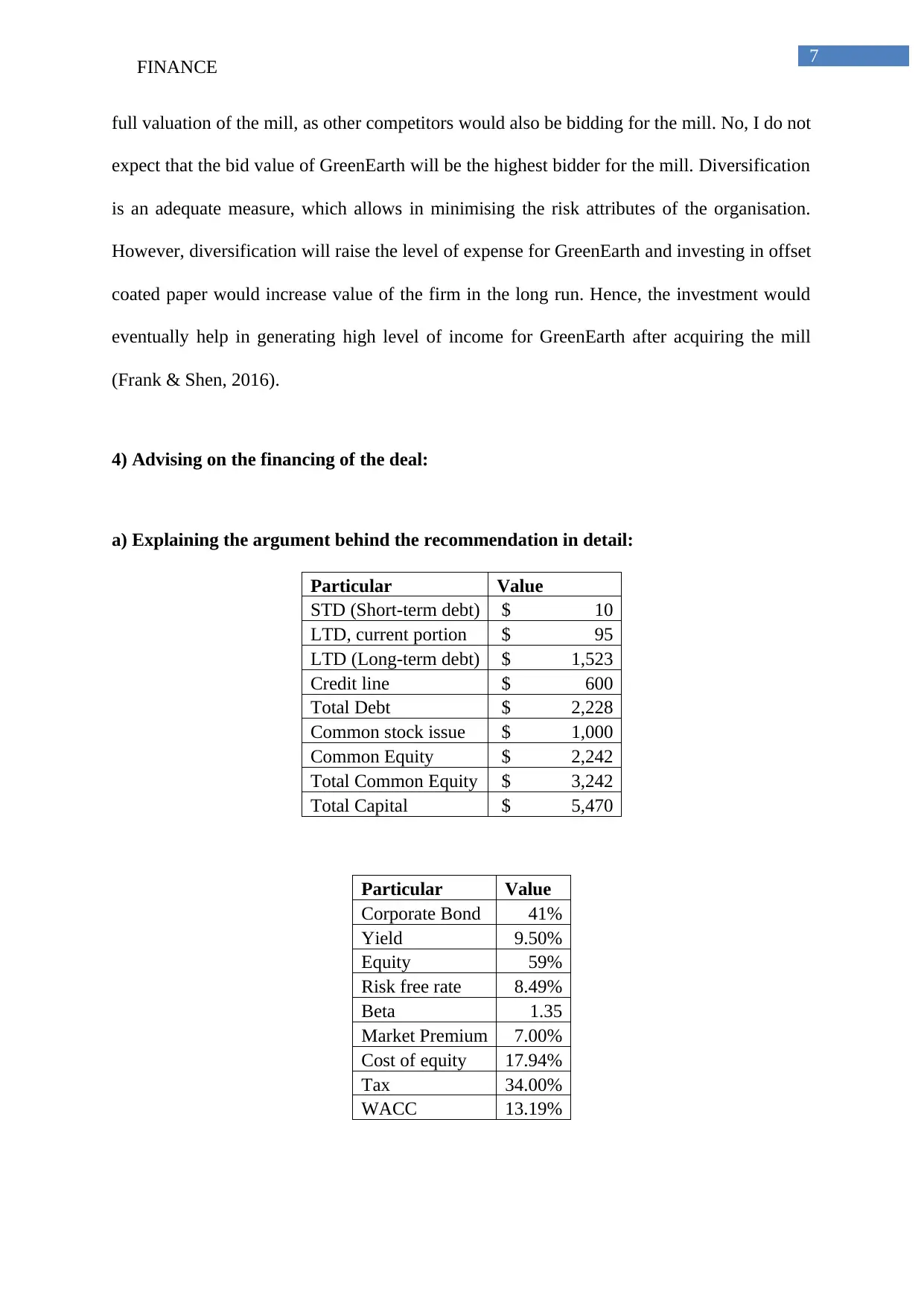

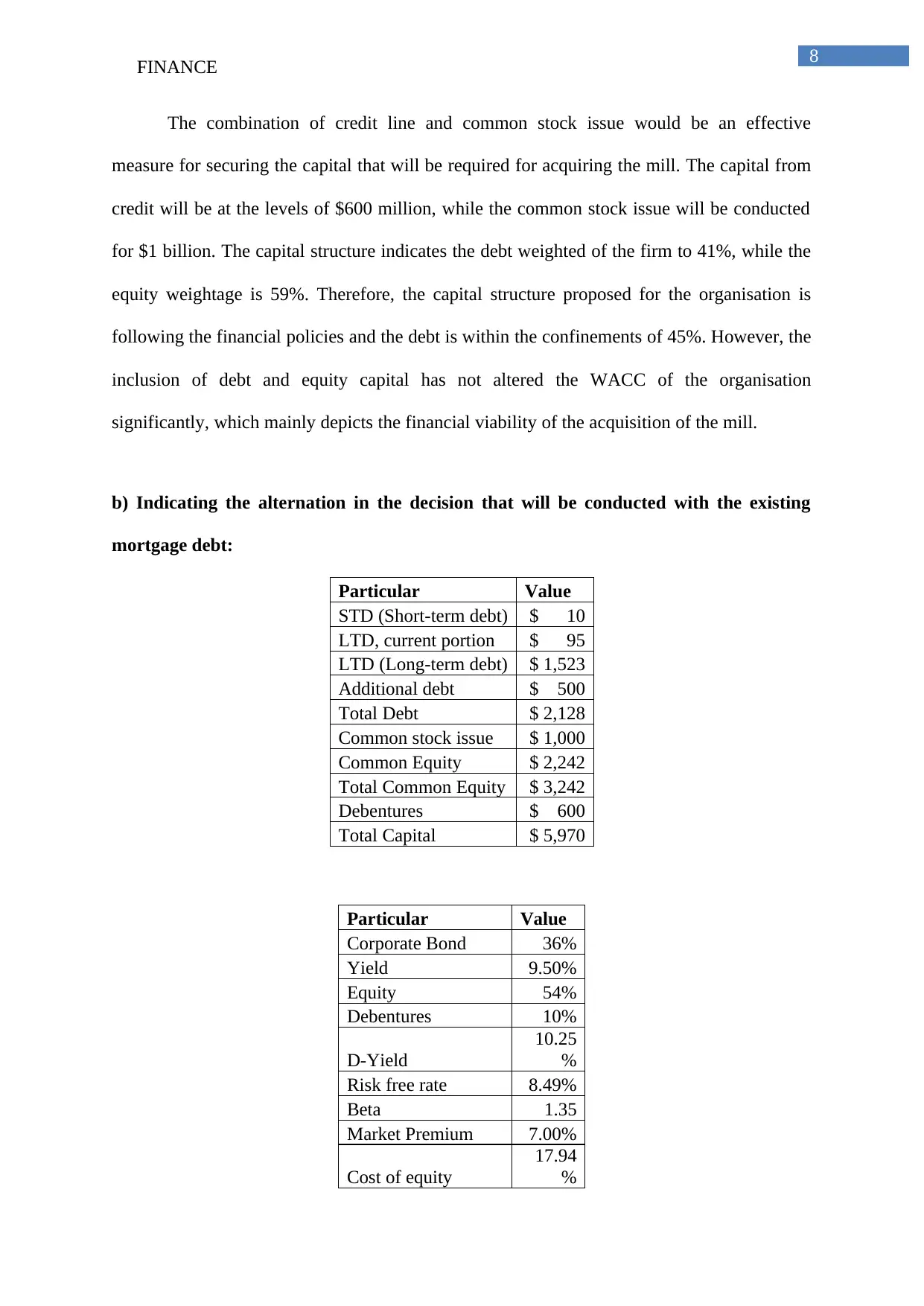

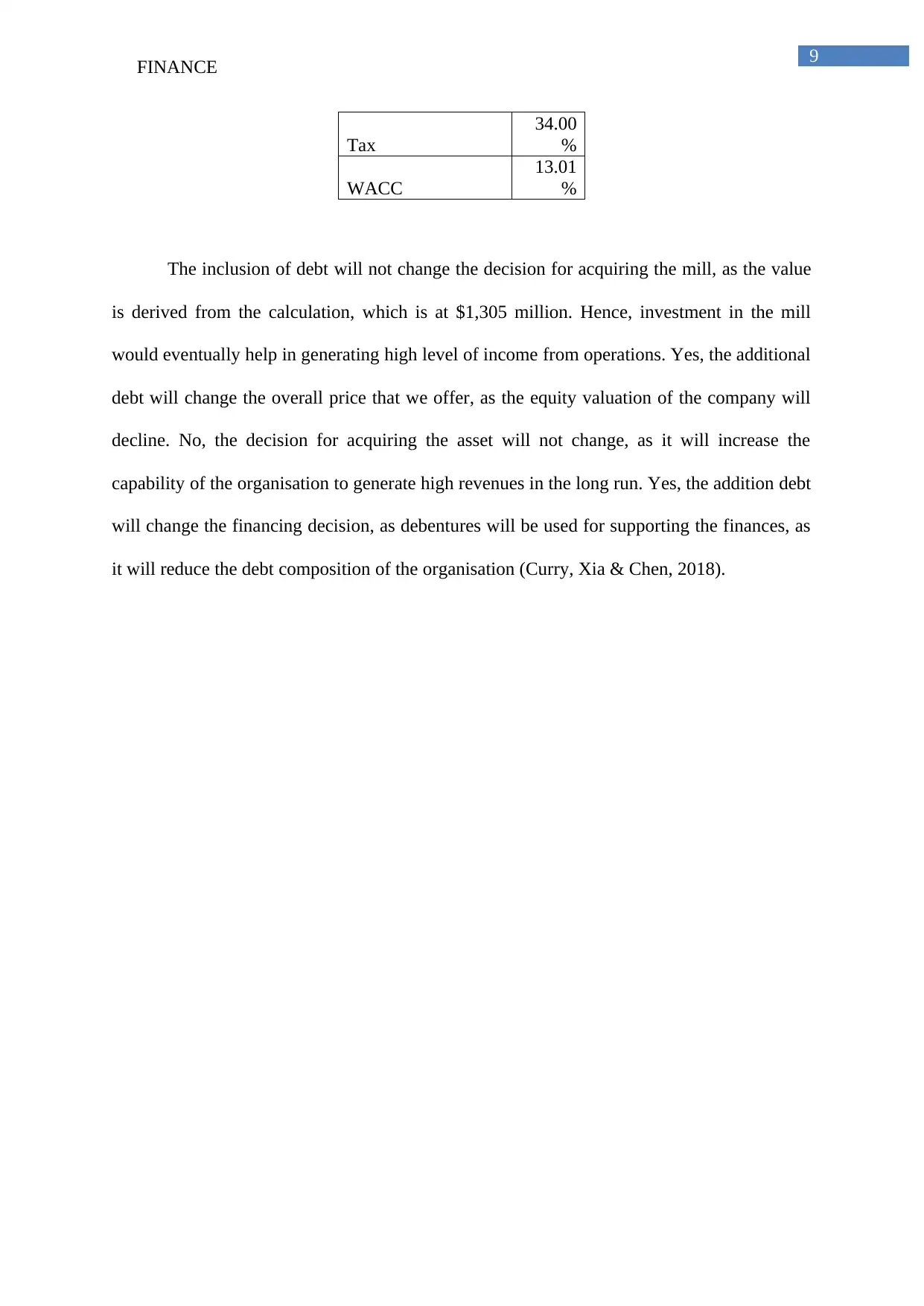

This case study provides a comprehensive financial analysis of GreenEarth Corporation's potential acquisition of Charlotte Mills. It begins by estimating the valuation of Charlotte Mills, evaluating the components of WACC, and determining the impact of tax basis changes. It then assesses the value of the scenario after five years, considering expansion projects and additional costs. The study also explores the strategic reasons for the transaction and advises on the financing of the deal, recommending a combination of credit line and common stock issue. Furthermore, it examines the potential impact of existing mortgage debt and debentures on the financing decision. The analysis includes detailed calculations of free cash flow, NPV, terminal value, and equity value under various scenarios, providing a robust assessment of the acquisition's financial viability. Desklib offers similar solved assignments and study resources for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.