Comprehensive Valuation Report: 85 Chester Street, Aston, Birmingham

VerifiedAdded on 2021/02/17

|13

|3669

|25

Report

AI Summary

This report provides a comprehensive valuation analysis of a leasehold industrial property located at 85 Chester Street, Aston, Birmingham. The report begins with an introduction to property valuation, focusing on the complexities of leasehold properties and the importance of financial ratios. The main body of the report details the property's features, including its location, layout, and infrastructure. It then delves into the calculation of the Estimated Rental Value (ERV) based on market data, the All Risks Market Yield (ARY), and the Rateable Value of the building, including Small Business Rate Relief (SBRR). The report uses comparable evidence methods and considers factors such as accessibility, floor area, and parking space to determine the property's value. It also includes hypothetical scenarios to illustrate different valuation outcomes, and concludes with a summary of the key findings and a list of references. The report provides a detailed breakdown of the financial aspects of the property valuation process, making it a useful resource for understanding the complexities of commercial real estate valuation.

BUSINESS PLAN

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

The Property...........................................................................................................................1

Estimated Rental Value and All Risks Market Yield.............................................................3

Rateable Value of the building and Rates Payable including SBRR.....................................5

Hypothetical Scenario 1.........................................................................................................8

Hypothetical Scenario 2.........................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

.......................................................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

The Property...........................................................................................................................1

Estimated Rental Value and All Risks Market Yield.............................................................3

Rateable Value of the building and Rates Payable including SBRR.....................................5

Hypothetical Scenario 1.........................................................................................................8

Hypothetical Scenario 2.........................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

.......................................................................................................................................................11

INTRODUCTION

Valuation of leasehold property is the complex concept and it will calculated through

critical financial ratios to measure the value of property (Ball, Lizieri and MacGregor, 2012). It

is direct for freehold property but in case of leasehold property, it more complicated to determine

because of their limited shelf life. It include typical tenure for the different leasehold property

such as 99 years for the residential or commercial property and 30 to 60 years for the industrial

property. This report cover various topics such as Estimated Rental Value (ERV) of the property

and it also include the All Risk Yield (ARY) which used for the valuation of risk related to

investment. In addition, Market Risk Yield (MRY) is the market risk of purchasing property.

MAIN BODY

The Property

Address: 85 Chester Street, Aston, Birmingham, B6 4AE

Rental Price: £ 121,478 per annum exclusive

Tenure: To Let (Leasehold)

Property Type: Industrial / Warehouse

Details: Approx. 8.1m eaves height

Accommodation: Near about 1736 sq m.

1

Valuation of leasehold property is the complex concept and it will calculated through

critical financial ratios to measure the value of property (Ball, Lizieri and MacGregor, 2012). It

is direct for freehold property but in case of leasehold property, it more complicated to determine

because of their limited shelf life. It include typical tenure for the different leasehold property

such as 99 years for the residential or commercial property and 30 to 60 years for the industrial

property. This report cover various topics such as Estimated Rental Value (ERV) of the property

and it also include the All Risk Yield (ARY) which used for the valuation of risk related to

investment. In addition, Market Risk Yield (MRY) is the market risk of purchasing property.

MAIN BODY

The Property

Address: 85 Chester Street, Aston, Birmingham, B6 4AE

Rental Price: £ 121,478 per annum exclusive

Tenure: To Let (Leasehold)

Property Type: Industrial / Warehouse

Details: Approx. 8.1m eaves height

Accommodation: Near about 1736 sq m.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

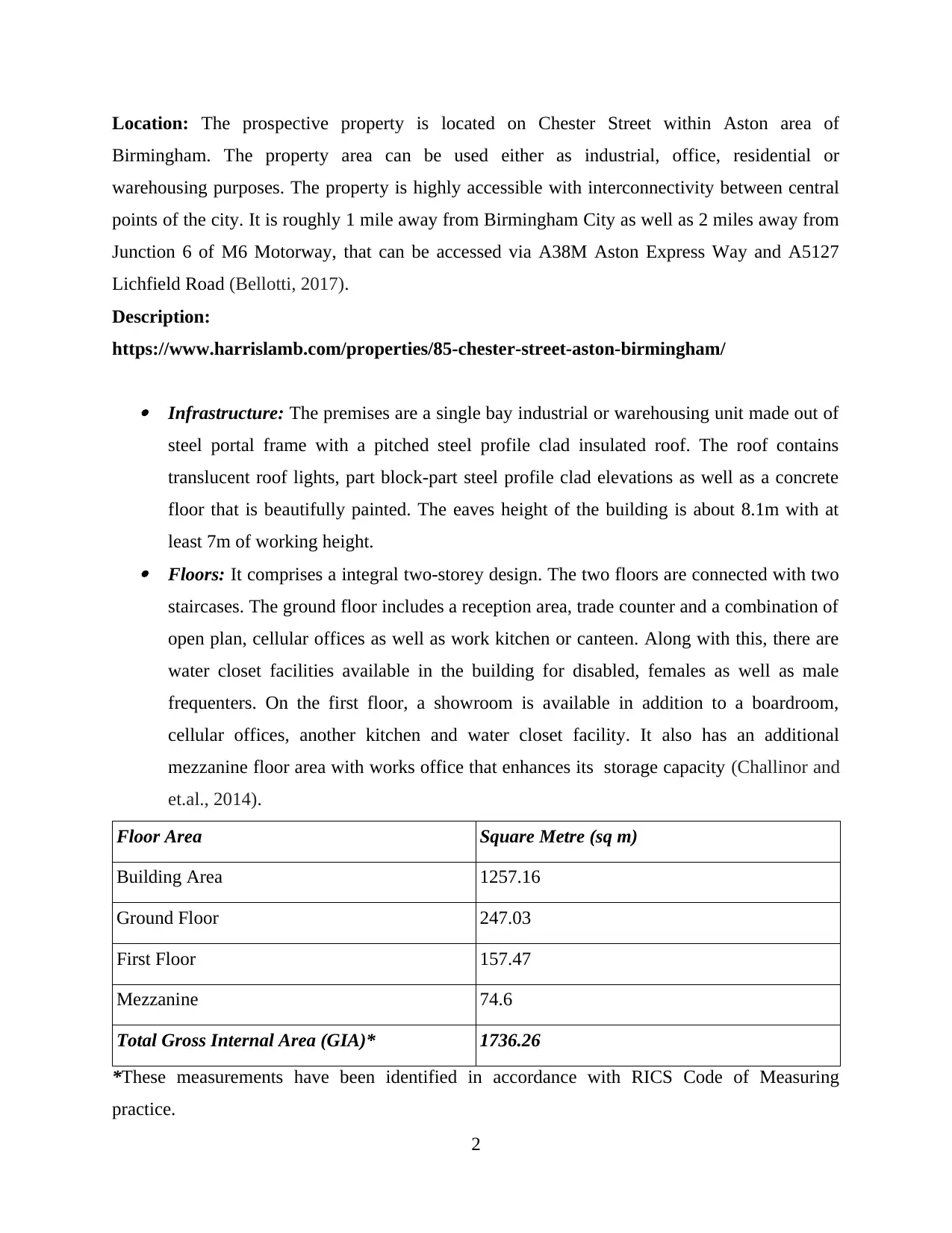

Location: The prospective property is located on Chester Street within Aston area of

Birmingham. The property area can be used either as industrial, office, residential or

warehousing purposes. The property is highly accessible with interconnectivity between central

points of the city. It is roughly 1 mile away from Birmingham City as well as 2 miles away from

Junction 6 of M6 Motorway, that can be accessed via A38M Aston Express Way and A5127

Lichfield Road (Bellotti, 2017).

Description:

https://www.harrislamb.com/properties/85-chester-street-aston-birmingham/

Infrastructure: The premises are a single bay industrial or warehousing unit made out of

steel portal frame with a pitched steel profile clad insulated roof. The roof contains

translucent roof lights, part block-part steel profile clad elevations as well as a concrete

floor that is beautifully painted. The eaves height of the building is about 8.1m with at

least 7m of working height. Floors: It comprises a integral two-storey design. The two floors are connected with two

staircases. The ground floor includes a reception area, trade counter and a combination of

open plan, cellular offices as well as work kitchen or canteen. Along with this, there are

water closet facilities available in the building for disabled, females as well as male

frequenters. On the first floor, a showroom is available in addition to a boardroom,

cellular offices, another kitchen and water closet facility. It also has an additional

mezzanine floor area with works office that enhances its storage capacity (Challinor and

et.al., 2014).

Floor Area Square Metre (sq m)

Building Area 1257.16

Ground Floor 247.03

First Floor 157.47

Mezzanine 74.6

Total Gross Internal Area (GIA)* 1736.26

*These measurements have been identified in accordance with RICS Code of Measuring

practice.

2

Birmingham. The property area can be used either as industrial, office, residential or

warehousing purposes. The property is highly accessible with interconnectivity between central

points of the city. It is roughly 1 mile away from Birmingham City as well as 2 miles away from

Junction 6 of M6 Motorway, that can be accessed via A38M Aston Express Way and A5127

Lichfield Road (Bellotti, 2017).

Description:

https://www.harrislamb.com/properties/85-chester-street-aston-birmingham/

Infrastructure: The premises are a single bay industrial or warehousing unit made out of

steel portal frame with a pitched steel profile clad insulated roof. The roof contains

translucent roof lights, part block-part steel profile clad elevations as well as a concrete

floor that is beautifully painted. The eaves height of the building is about 8.1m with at

least 7m of working height. Floors: It comprises a integral two-storey design. The two floors are connected with two

staircases. The ground floor includes a reception area, trade counter and a combination of

open plan, cellular offices as well as work kitchen or canteen. Along with this, there are

water closet facilities available in the building for disabled, females as well as male

frequenters. On the first floor, a showroom is available in addition to a boardroom,

cellular offices, another kitchen and water closet facility. It also has an additional

mezzanine floor area with works office that enhances its storage capacity (Challinor and

et.al., 2014).

Floor Area Square Metre (sq m)

Building Area 1257.16

Ground Floor 247.03

First Floor 157.47

Mezzanine 74.6

Total Gross Internal Area (GIA)* 1736.26

*These measurements have been identified in accordance with RICS Code of Measuring

practice.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Entrance and Lighting: The building has an excellent sodium lighting system. Thus,

providing a well-lit and comfortable working environment for its occupants. The access

to the building is through two foldable shutter doors.

Additional Features: The premises have a yard and provide ample car parking area

protected by a gate and fence. Currently, 10 designated parking spaces are available on

the property. In addition to this, a suspended ceiling, recessed lighting, air conditioning,

carpet tiles and central heating with gas fire also add to the appeal of the property

(Chang, Christoffersen and Jacobs, 2013).

Estimated Rental Value and All Risks Market Yield

The property has been valued using comparable evidence method. The information

regarding the same has been extracted from online databases, agents, professional press and

other sources. Under this method, important factors are identified that directly affect the

potential income stream of the property and pose to become a restriction on its use. Such factors

include location, size, quality of infrastructure among others. For the aforementioned property,

the following key factors affect it:

Accessibility to major road networks;

Accessibility to site;

Layout of the building including height;

Floor area;

Parking Space.

Since the building is an industrial/warehouse unit with a rental tenure specifically

leasehold, the above mentioned factors are the key areas to be considered when collecting

comparable evidence (Ciaian and et.al., 2012).

Estimated Rental Value (ERV):

Estimated Rental Value is an estimated rent that a given property is expected to reach

based on its characteristics, location, layout, work conditions as well as nearby market

conditions. When deciding to purchase a piece of property or land, ERV is one of the most

important variable to be considered by an investor. In the context of given case scenario, the

Estimated Rental Value is calculated as follows:

Based on the prevailing Market rent in Birmingham, the (ERV) Estimated Rental Value for the

relevant property is arrived that:

3

providing a well-lit and comfortable working environment for its occupants. The access

to the building is through two foldable shutter doors.

Additional Features: The premises have a yard and provide ample car parking area

protected by a gate and fence. Currently, 10 designated parking spaces are available on

the property. In addition to this, a suspended ceiling, recessed lighting, air conditioning,

carpet tiles and central heating with gas fire also add to the appeal of the property

(Chang, Christoffersen and Jacobs, 2013).

Estimated Rental Value and All Risks Market Yield

The property has been valued using comparable evidence method. The information

regarding the same has been extracted from online databases, agents, professional press and

other sources. Under this method, important factors are identified that directly affect the

potential income stream of the property and pose to become a restriction on its use. Such factors

include location, size, quality of infrastructure among others. For the aforementioned property,

the following key factors affect it:

Accessibility to major road networks;

Accessibility to site;

Layout of the building including height;

Floor area;

Parking Space.

Since the building is an industrial/warehouse unit with a rental tenure specifically

leasehold, the above mentioned factors are the key areas to be considered when collecting

comparable evidence (Ciaian and et.al., 2012).

Estimated Rental Value (ERV):

Estimated Rental Value is an estimated rent that a given property is expected to reach

based on its characteristics, location, layout, work conditions as well as nearby market

conditions. When deciding to purchase a piece of property or land, ERV is one of the most

important variable to be considered by an investor. In the context of given case scenario, the

Estimated Rental Value is calculated as follows:

Based on the prevailing Market rent in Birmingham, the (ERV) Estimated Rental Value for the

relevant property is arrived that:

3

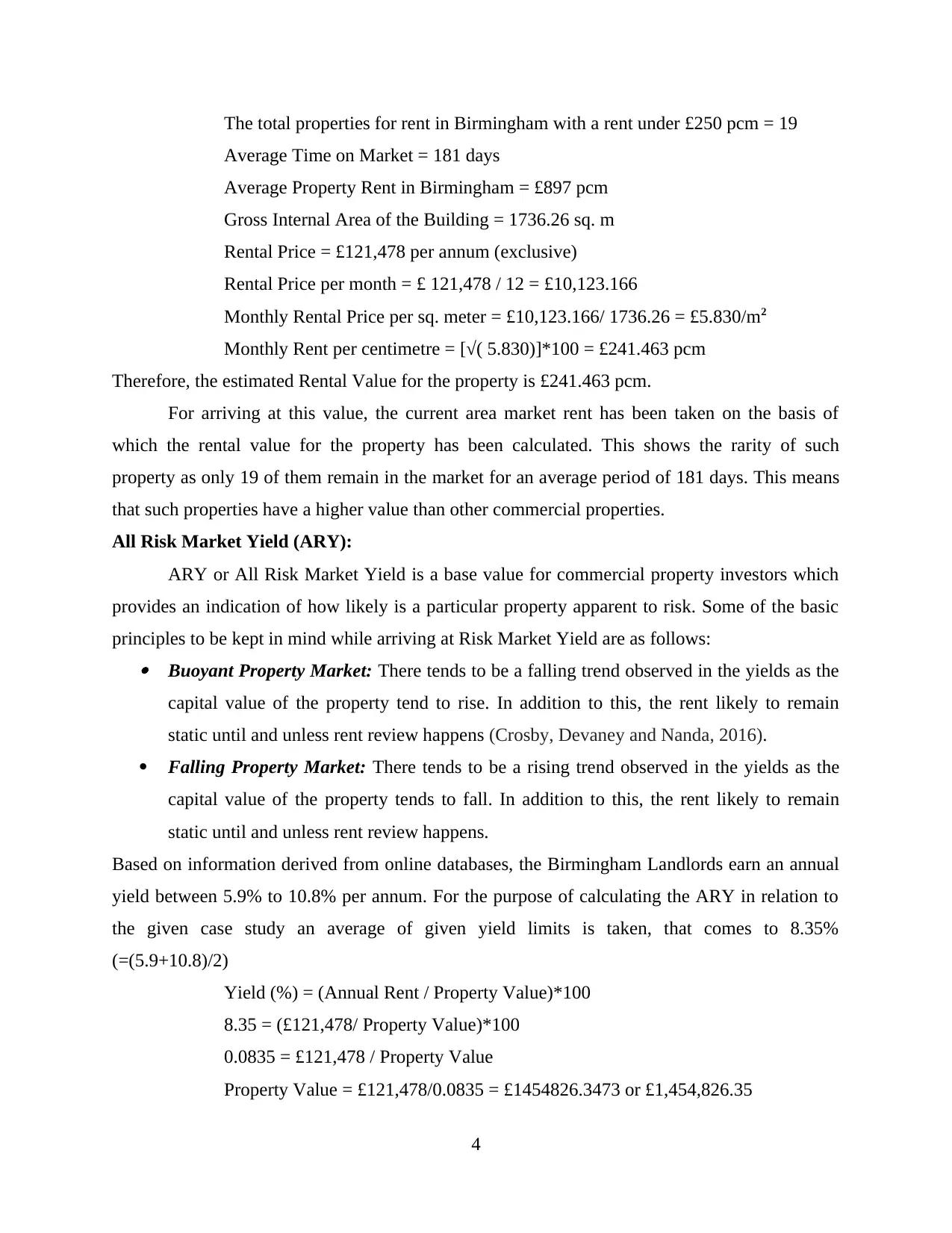

The total properties for rent in Birmingham with a rent under £250 pcm = 19

Average Time on Market = 181 days

Average Property Rent in Birmingham = £897 pcm

Gross Internal Area of the Building = 1736.26 sq. m

Rental Price = £121,478 per annum (exclusive)

Rental Price per month = £ 121,478 / 12 = £10,123.166

Monthly Rental Price per sq. meter = £10,123.166/ 1736.26 = £5.830/m2

Monthly Rent per centimetre = [√( 5.830)]*100 = £241.463 pcm

Therefore, the estimated Rental Value for the property is £241.463 pcm.

For arriving at this value, the current area market rent has been taken on the basis of

which the rental value for the property has been calculated. This shows the rarity of such

property as only 19 of them remain in the market for an average period of 181 days. This means

that such properties have a higher value than other commercial properties.

All Risk Market Yield (ARY):

ARY or All Risk Market Yield is a base value for commercial property investors which

provides an indication of how likely is a particular property apparent to risk. Some of the basic

principles to be kept in mind while arriving at Risk Market Yield are as follows: Buoyant Property Market: There tends to be a falling trend observed in the yields as the

capital value of the property tend to rise. In addition to this, the rent likely to remain

static until and unless rent review happens (Crosby, Devaney and Nanda, 2016).

Falling Property Market: There tends to be a rising trend observed in the yields as the

capital value of the property tends to fall. In addition to this, the rent likely to remain

static until and unless rent review happens.

Based on information derived from online databases, the Birmingham Landlords earn an annual

yield between 5.9% to 10.8% per annum. For the purpose of calculating the ARY in relation to

the given case study an average of given yield limits is taken, that comes to 8.35%

(=(5.9+10.8)/2)

Yield (%) = (Annual Rent / Property Value)*100

8.35 = (£121,478/ Property Value)*100

0.0835 = £121,478 / Property Value

Property Value = £121,478/0.0835 = £1454826.3473 or £1,454,826.35

4

Average Time on Market = 181 days

Average Property Rent in Birmingham = £897 pcm

Gross Internal Area of the Building = 1736.26 sq. m

Rental Price = £121,478 per annum (exclusive)

Rental Price per month = £ 121,478 / 12 = £10,123.166

Monthly Rental Price per sq. meter = £10,123.166/ 1736.26 = £5.830/m2

Monthly Rent per centimetre = [√( 5.830)]*100 = £241.463 pcm

Therefore, the estimated Rental Value for the property is £241.463 pcm.

For arriving at this value, the current area market rent has been taken on the basis of

which the rental value for the property has been calculated. This shows the rarity of such

property as only 19 of them remain in the market for an average period of 181 days. This means

that such properties have a higher value than other commercial properties.

All Risk Market Yield (ARY):

ARY or All Risk Market Yield is a base value for commercial property investors which

provides an indication of how likely is a particular property apparent to risk. Some of the basic

principles to be kept in mind while arriving at Risk Market Yield are as follows: Buoyant Property Market: There tends to be a falling trend observed in the yields as the

capital value of the property tend to rise. In addition to this, the rent likely to remain

static until and unless rent review happens (Crosby, Devaney and Nanda, 2016).

Falling Property Market: There tends to be a rising trend observed in the yields as the

capital value of the property tends to fall. In addition to this, the rent likely to remain

static until and unless rent review happens.

Based on information derived from online databases, the Birmingham Landlords earn an annual

yield between 5.9% to 10.8% per annum. For the purpose of calculating the ARY in relation to

the given case study an average of given yield limits is taken, that comes to 8.35%

(=(5.9+10.8)/2)

Yield (%) = (Annual Rent / Property Value)*100

8.35 = (£121,478/ Property Value)*100

0.0835 = £121,478 / Property Value

Property Value = £121,478/0.0835 = £1454826.3473 or £1,454,826.35

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The property yield figure can be assumed to be any number ranging between the given

limit of prevalent market yield in Birmingham to ascertain a more accurate reflection of risks.

This would indicate how strong a candidate is for a particular property in the role of tenant. It is

important to note that the references provided by tenants, their credit rating also determine the

level of risk. For such a tenant, the risk would be lower. Conversely, those who are likely to

make defaults on rent payments would pose a higher risk.

Rateable Value of the building and Rates Payable including SBRR

Rateable Value of Property is the amount equivalent to the rent at which the property is

expected to be let out to an individual or a corporate entity on a year-to-year basis. It is based on

the assumption that tenant has undertaken all of their responsibility to pay off its obligations in

regards to the rent payments and applicable taxes thereof, cost of repairs, insurance and other

expenses which are required to be incurred so as to maintain the rental property in a perfect

manner. Rateable Value of the Building is usually assessed by the Valuation Office Agency. This

is an agency of HM Revenue and Customs (Jamar, 2017).

Under this valuation, the property's annual rent is calculated if it were available to be let

on rent in the open market at a fixed valuation date. The rate determination criterion includes:

The Rateable Values are based on the valuation date of April 1, 2008. Such a value would

be applicable until March 31, 2017.

The Rateable Values are based on the valuation date of April 1, 2015. Such a value would

be applicable until April 1, 2017.

Rateable Values are subjected to certain reliefs known as Small Business Rate Relief or

SBRR. It is a relief calculated on the Rateable Value (RV) of business in the relevant valuation

time period. Such a rate varies from region to region. It aims to help small businesses,

specifically those which are not entitled to any other kind of relief that is mandatory in nature. As

the commercial property, in the given case scenario, is located in Birmingham, the SBRR for

that region shall be applicable on the properties. For this purpose, only those business qualify

that:

Own a single property with a Rateable Value of less than £15,000 after April 2017.

Own main property and additional properties with their individual Rateable Value of less

than £2,899 and a Combined Rateable Value of less than £19,999.

In the context of given case scenario, the rateable value of the building is:

5

limit of prevalent market yield in Birmingham to ascertain a more accurate reflection of risks.

This would indicate how strong a candidate is for a particular property in the role of tenant. It is

important to note that the references provided by tenants, their credit rating also determine the

level of risk. For such a tenant, the risk would be lower. Conversely, those who are likely to

make defaults on rent payments would pose a higher risk.

Rateable Value of the building and Rates Payable including SBRR

Rateable Value of Property is the amount equivalent to the rent at which the property is

expected to be let out to an individual or a corporate entity on a year-to-year basis. It is based on

the assumption that tenant has undertaken all of their responsibility to pay off its obligations in

regards to the rent payments and applicable taxes thereof, cost of repairs, insurance and other

expenses which are required to be incurred so as to maintain the rental property in a perfect

manner. Rateable Value of the Building is usually assessed by the Valuation Office Agency. This

is an agency of HM Revenue and Customs (Jamar, 2017).

Under this valuation, the property's annual rent is calculated if it were available to be let

on rent in the open market at a fixed valuation date. The rate determination criterion includes:

The Rateable Values are based on the valuation date of April 1, 2008. Such a value would

be applicable until March 31, 2017.

The Rateable Values are based on the valuation date of April 1, 2015. Such a value would

be applicable until April 1, 2017.

Rateable Values are subjected to certain reliefs known as Small Business Rate Relief or

SBRR. It is a relief calculated on the Rateable Value (RV) of business in the relevant valuation

time period. Such a rate varies from region to region. It aims to help small businesses,

specifically those which are not entitled to any other kind of relief that is mandatory in nature. As

the commercial property, in the given case scenario, is located in Birmingham, the SBRR for

that region shall be applicable on the properties. For this purpose, only those business qualify

that:

Own a single property with a Rateable Value of less than £15,000 after April 2017.

Own main property and additional properties with their individual Rateable Value of less

than £2,899 and a Combined Rateable Value of less than £19,999.

In the context of given case scenario, the rateable value of the building is:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

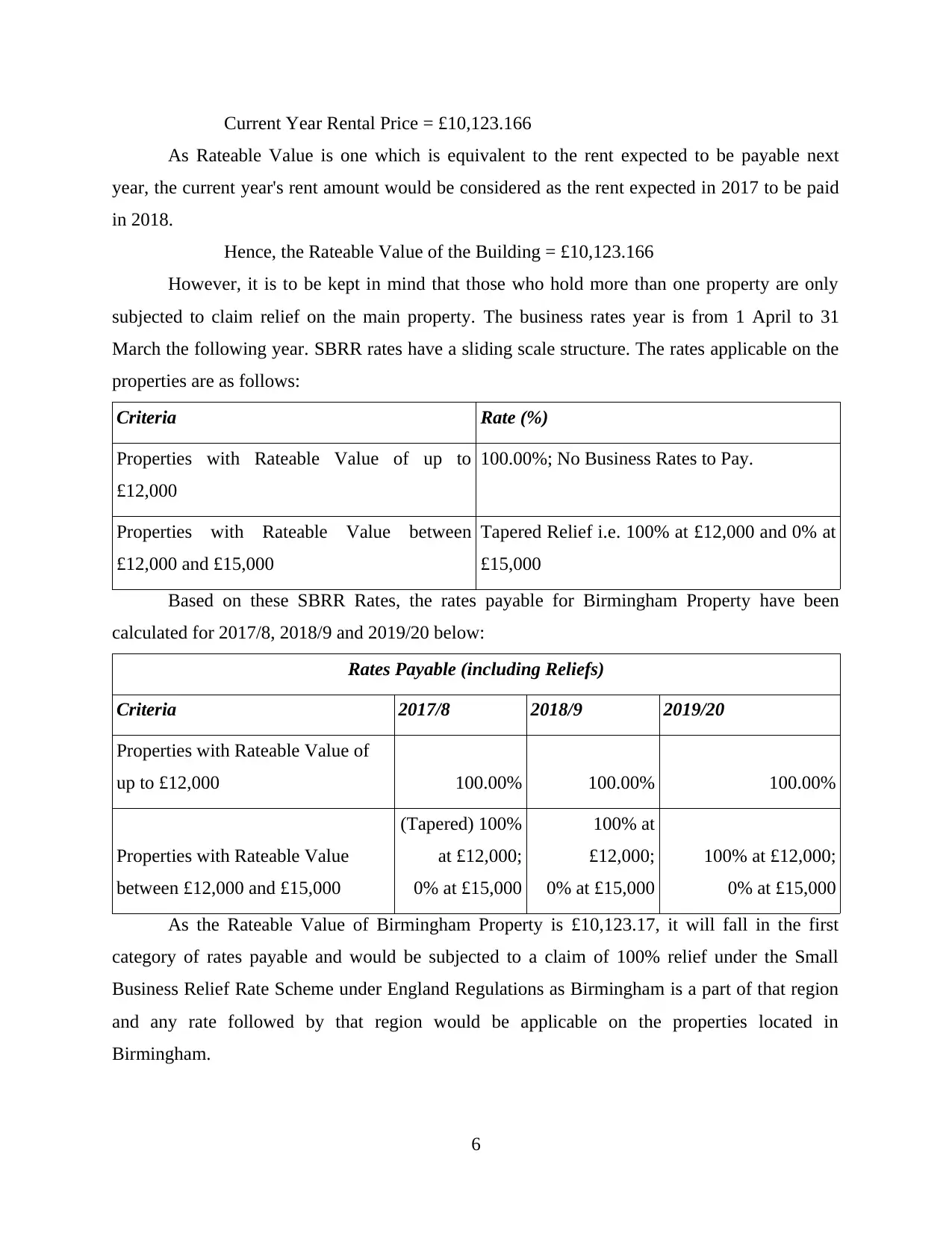

Current Year Rental Price = £10,123.166

As Rateable Value is one which is equivalent to the rent expected to be payable next

year, the current year's rent amount would be considered as the rent expected in 2017 to be paid

in 2018.

Hence, the Rateable Value of the Building = £10,123.166

However, it is to be kept in mind that those who hold more than one property are only

subjected to claim relief on the main property. The business rates year is from 1 April to 31

March the following year. SBRR rates have a sliding scale structure. The rates applicable on the

properties are as follows:

Criteria Rate (%)

Properties with Rateable Value of up to

£12,000

100.00%; No Business Rates to Pay.

Properties with Rateable Value between

£12,000 and £15,000

Tapered Relief i.e. 100% at £12,000 and 0% at

£15,000

Based on these SBRR Rates, the rates payable for Birmingham Property have been

calculated for 2017/8, 2018/9 and 2019/20 below:

Rates Payable (including Reliefs)

Criteria 2017/8 2018/9 2019/20

Properties with Rateable Value of

up to £12,000 100.00% 100.00% 100.00%

Properties with Rateable Value

between £12,000 and £15,000

(Tapered) 100%

at £12,000;

0% at £15,000

100% at

£12,000;

0% at £15,000

100% at £12,000;

0% at £15,000

As the Rateable Value of Birmingham Property is £10,123.17, it will fall in the first

category of rates payable and would be subjected to a claim of 100% relief under the Small

Business Relief Rate Scheme under England Regulations as Birmingham is a part of that region

and any rate followed by that region would be applicable on the properties located in

Birmingham.

6

As Rateable Value is one which is equivalent to the rent expected to be payable next

year, the current year's rent amount would be considered as the rent expected in 2017 to be paid

in 2018.

Hence, the Rateable Value of the Building = £10,123.166

However, it is to be kept in mind that those who hold more than one property are only

subjected to claim relief on the main property. The business rates year is from 1 April to 31

March the following year. SBRR rates have a sliding scale structure. The rates applicable on the

properties are as follows:

Criteria Rate (%)

Properties with Rateable Value of up to

£12,000

100.00%; No Business Rates to Pay.

Properties with Rateable Value between

£12,000 and £15,000

Tapered Relief i.e. 100% at £12,000 and 0% at

£15,000

Based on these SBRR Rates, the rates payable for Birmingham Property have been

calculated for 2017/8, 2018/9 and 2019/20 below:

Rates Payable (including Reliefs)

Criteria 2017/8 2018/9 2019/20

Properties with Rateable Value of

up to £12,000 100.00% 100.00% 100.00%

Properties with Rateable Value

between £12,000 and £15,000

(Tapered) 100%

at £12,000;

0% at £15,000

100% at

£12,000;

0% at £15,000

100% at £12,000;

0% at £15,000

As the Rateable Value of Birmingham Property is £10,123.17, it will fall in the first

category of rates payable and would be subjected to a claim of 100% relief under the Small

Business Relief Rate Scheme under England Regulations as Birmingham is a part of that region

and any rate followed by that region would be applicable on the properties located in

Birmingham.

6

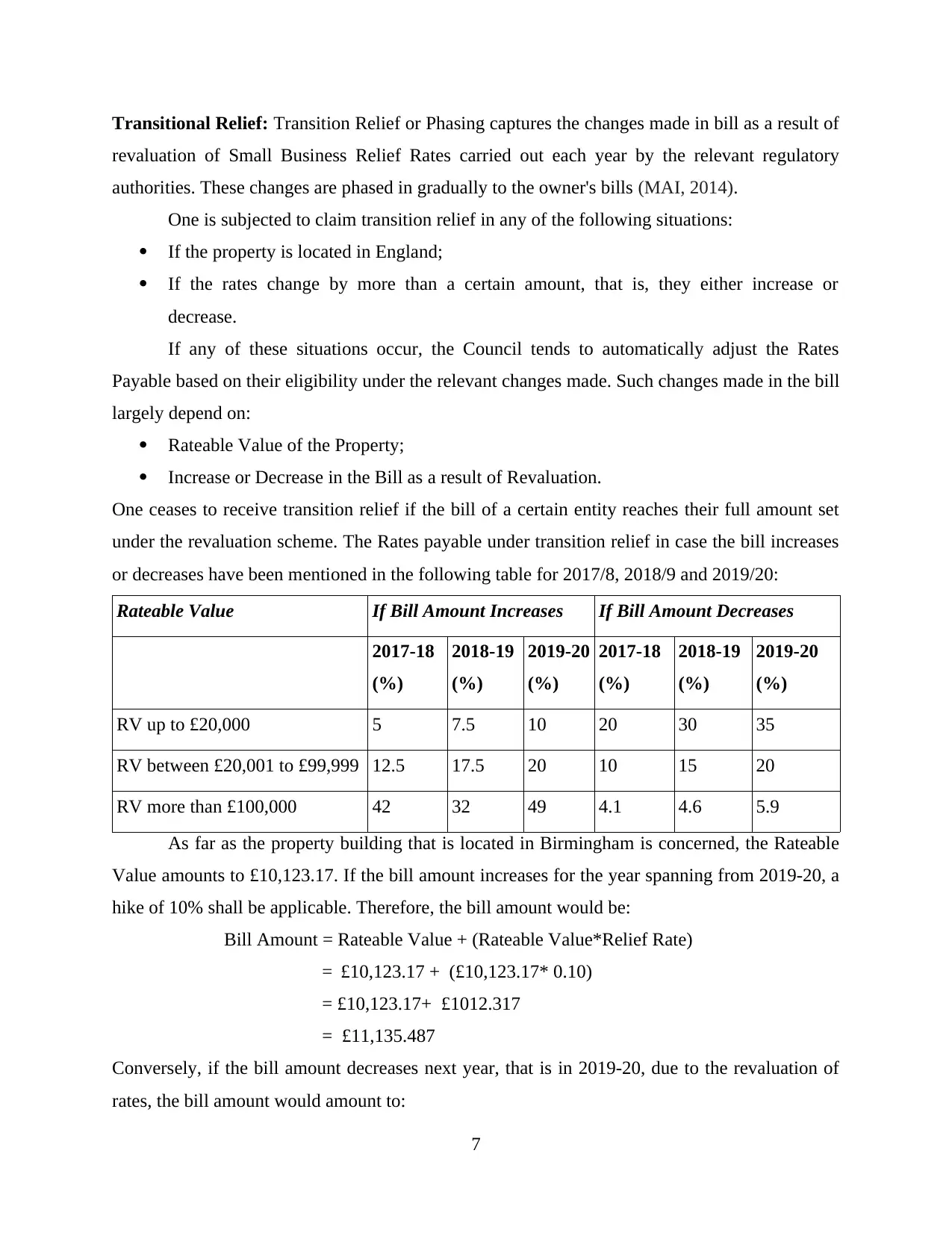

Transitional Relief: Transition Relief or Phasing captures the changes made in bill as a result of

revaluation of Small Business Relief Rates carried out each year by the relevant regulatory

authorities. These changes are phased in gradually to the owner's bills (MAI, 2014).

One is subjected to claim transition relief in any of the following situations:

If the property is located in England;

If the rates change by more than a certain amount, that is, they either increase or

decrease.

If any of these situations occur, the Council tends to automatically adjust the Rates

Payable based on their eligibility under the relevant changes made. Such changes made in the bill

largely depend on:

Rateable Value of the Property;

Increase or Decrease in the Bill as a result of Revaluation.

One ceases to receive transition relief if the bill of a certain entity reaches their full amount set

under the revaluation scheme. The Rates payable under transition relief in case the bill increases

or decreases have been mentioned in the following table for 2017/8, 2018/9 and 2019/20:

Rateable Value If Bill Amount Increases If Bill Amount Decreases

2017-18

(%)

2018-19

(%)

2019-20

(%)

2017-18

(%)

2018-19

(%)

2019-20

(%)

RV up to £20,000 5 7.5 10 20 30 35

RV between £20,001 to £99,999 12.5 17.5 20 10 15 20

RV more than £100,000 42 32 49 4.1 4.6 5.9

As far as the property building that is located in Birmingham is concerned, the Rateable

Value amounts to £10,123.17. If the bill amount increases for the year spanning from 2019-20, a

hike of 10% shall be applicable. Therefore, the bill amount would be:

Bill Amount = Rateable Value + (Rateable Value*Relief Rate)

= £10,123.17 + (£10,123.17* 0.10)

= £10,123.17+ £1012.317

= £11,135.487

Conversely, if the bill amount decreases next year, that is in 2019-20, due to the revaluation of

rates, the bill amount would amount to:

7

revaluation of Small Business Relief Rates carried out each year by the relevant regulatory

authorities. These changes are phased in gradually to the owner's bills (MAI, 2014).

One is subjected to claim transition relief in any of the following situations:

If the property is located in England;

If the rates change by more than a certain amount, that is, they either increase or

decrease.

If any of these situations occur, the Council tends to automatically adjust the Rates

Payable based on their eligibility under the relevant changes made. Such changes made in the bill

largely depend on:

Rateable Value of the Property;

Increase or Decrease in the Bill as a result of Revaluation.

One ceases to receive transition relief if the bill of a certain entity reaches their full amount set

under the revaluation scheme. The Rates payable under transition relief in case the bill increases

or decreases have been mentioned in the following table for 2017/8, 2018/9 and 2019/20:

Rateable Value If Bill Amount Increases If Bill Amount Decreases

2017-18

(%)

2018-19

(%)

2019-20

(%)

2017-18

(%)

2018-19

(%)

2019-20

(%)

RV up to £20,000 5 7.5 10 20 30 35

RV between £20,001 to £99,999 12.5 17.5 20 10 15 20

RV more than £100,000 42 32 49 4.1 4.6 5.9

As far as the property building that is located in Birmingham is concerned, the Rateable

Value amounts to £10,123.17. If the bill amount increases for the year spanning from 2019-20, a

hike of 10% shall be applicable. Therefore, the bill amount would be:

Bill Amount = Rateable Value + (Rateable Value*Relief Rate)

= £10,123.17 + (£10,123.17* 0.10)

= £10,123.17+ £1012.317

= £11,135.487

Conversely, if the bill amount decreases next year, that is in 2019-20, due to the revaluation of

rates, the bill amount would amount to:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

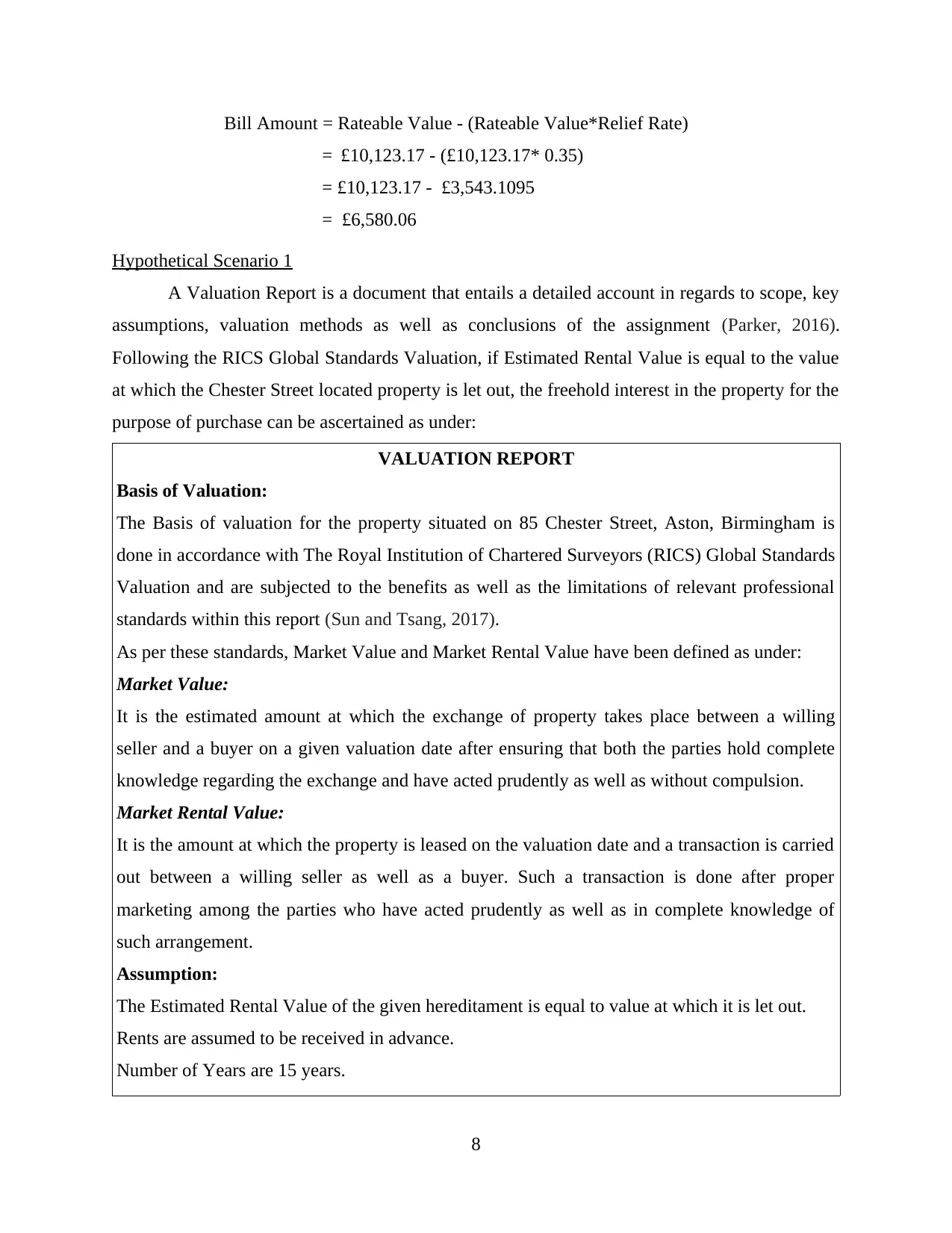

Bill Amount = Rateable Value - (Rateable Value*Relief Rate)

= £10,123.17 - (£10,123.17* 0.35)

= £10,123.17 - £3,543.1095

= £6,580.06

Hypothetical Scenario 1

A Valuation Report is a document that entails a detailed account in regards to scope, key

assumptions, valuation methods as well as conclusions of the assignment (Parker, 2016).

Following the RICS Global Standards Valuation, if Estimated Rental Value is equal to the value

at which the Chester Street located property is let out, the freehold interest in the property for the

purpose of purchase can be ascertained as under:

VALUATION REPORT

Basis of Valuation:

The Basis of valuation for the property situated on 85 Chester Street, Aston, Birmingham is

done in accordance with The Royal Institution of Chartered Surveyors (RICS) Global Standards

Valuation and are subjected to the benefits as well as the limitations of relevant professional

standards within this report (Sun and Tsang, 2017).

As per these standards, Market Value and Market Rental Value have been defined as under:

Market Value:

It is the estimated amount at which the exchange of property takes place between a willing

seller and a buyer on a given valuation date after ensuring that both the parties hold complete

knowledge regarding the exchange and have acted prudently as well as without compulsion.

Market Rental Value:

It is the amount at which the property is leased on the valuation date and a transaction is carried

out between a willing seller as well as a buyer. Such a transaction is done after proper

marketing among the parties who have acted prudently as well as in complete knowledge of

such arrangement.

Assumption:

The Estimated Rental Value of the given hereditament is equal to value at which it is let out.

Rents are assumed to be received in advance.

Number of Years are 15 years.

8

= £10,123.17 - (£10,123.17* 0.35)

= £10,123.17 - £3,543.1095

= £6,580.06

Hypothetical Scenario 1

A Valuation Report is a document that entails a detailed account in regards to scope, key

assumptions, valuation methods as well as conclusions of the assignment (Parker, 2016).

Following the RICS Global Standards Valuation, if Estimated Rental Value is equal to the value

at which the Chester Street located property is let out, the freehold interest in the property for the

purpose of purchase can be ascertained as under:

VALUATION REPORT

Basis of Valuation:

The Basis of valuation for the property situated on 85 Chester Street, Aston, Birmingham is

done in accordance with The Royal Institution of Chartered Surveyors (RICS) Global Standards

Valuation and are subjected to the benefits as well as the limitations of relevant professional

standards within this report (Sun and Tsang, 2017).

As per these standards, Market Value and Market Rental Value have been defined as under:

Market Value:

It is the estimated amount at which the exchange of property takes place between a willing

seller and a buyer on a given valuation date after ensuring that both the parties hold complete

knowledge regarding the exchange and have acted prudently as well as without compulsion.

Market Rental Value:

It is the amount at which the property is leased on the valuation date and a transaction is carried

out between a willing seller as well as a buyer. Such a transaction is done after proper

marketing among the parties who have acted prudently as well as in complete knowledge of

such arrangement.

Assumption:

The Estimated Rental Value of the given hereditament is equal to value at which it is let out.

Rents are assumed to be received in advance.

Number of Years are 15 years.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

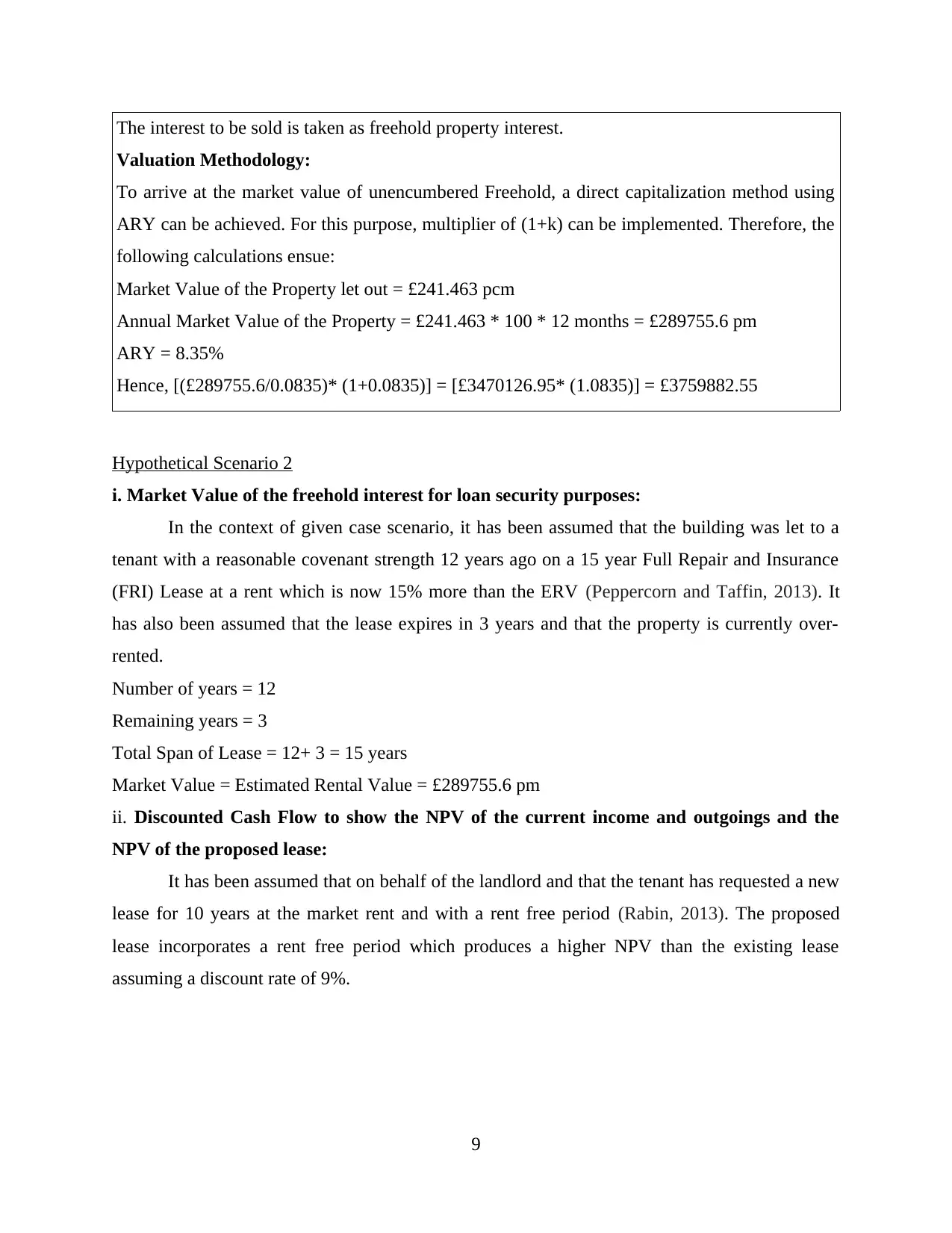

The interest to be sold is taken as freehold property interest.

Valuation Methodology:

To arrive at the market value of unencumbered Freehold, a direct capitalization method using

ARY can be achieved. For this purpose, multiplier of (1+k) can be implemented. Therefore, the

following calculations ensue:

Market Value of the Property let out = £241.463 pcm

Annual Market Value of the Property = £241.463 * 100 * 12 months = £289755.6 pm

ARY = 8.35%

Hence, [(£289755.6/0.0835)* (1+0.0835)] = [£3470126.95* (1.0835)] = £3759882.55

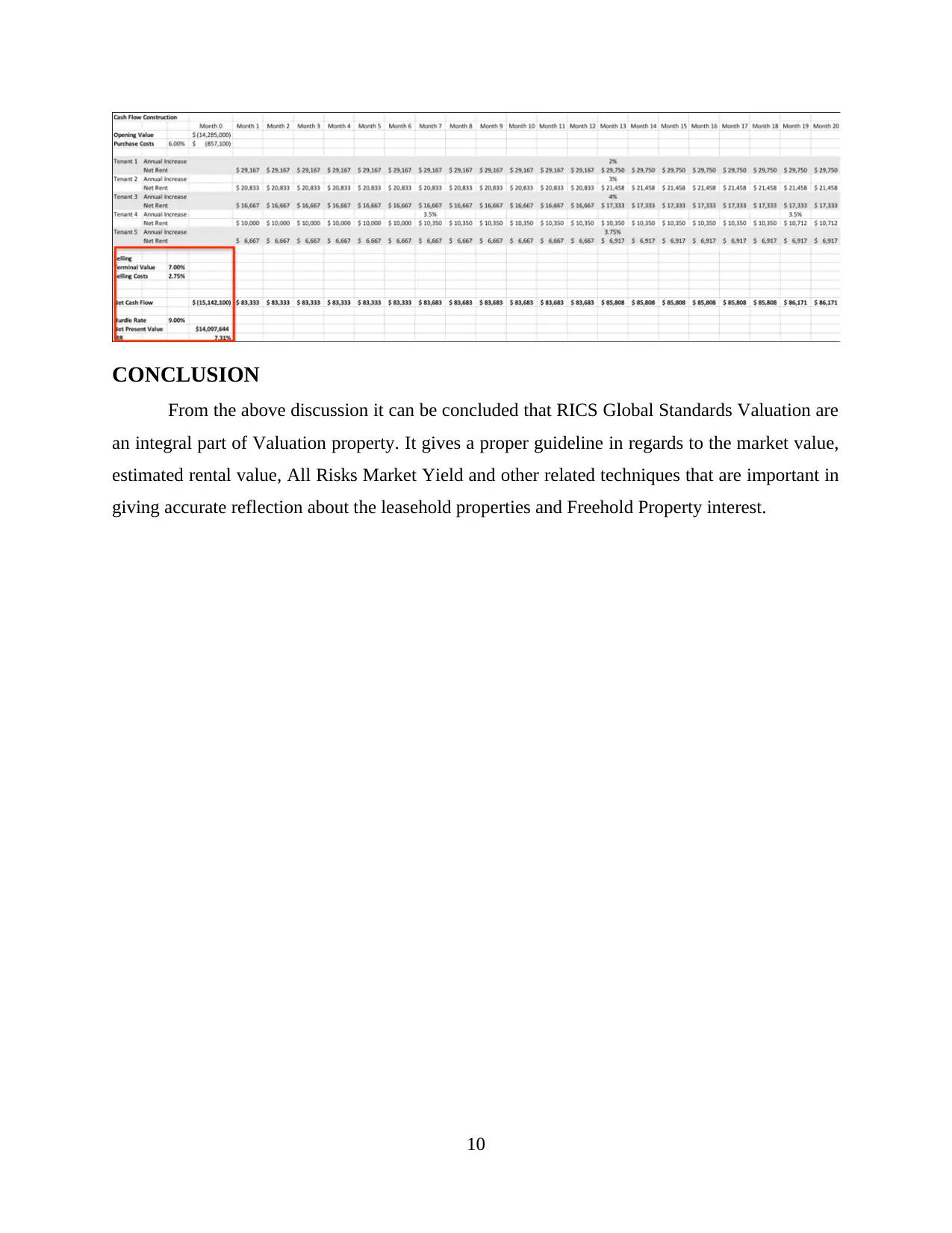

Hypothetical Scenario 2

i. Market Value of the freehold interest for loan security purposes:

In the context of given case scenario, it has been assumed that the building was let to a

tenant with a reasonable covenant strength 12 years ago on a 15 year Full Repair and Insurance

(FRI) Lease at a rent which is now 15% more than the ERV (Peppercorn and Taffin, 2013). It

has also been assumed that the lease expires in 3 years and that the property is currently over-

rented.

Number of years = 12

Remaining years = 3

Total Span of Lease = 12+ 3 = 15 years

Market Value = Estimated Rental Value = £289755.6 pm

ii. Discounted Cash Flow to show the NPV of the current income and outgoings and the

NPV of the proposed lease:

It has been assumed that on behalf of the landlord and that the tenant has requested a new

lease for 10 years at the market rent and with a rent free period (Rabin, 2013). The proposed

lease incorporates a rent free period which produces a higher NPV than the existing lease

assuming a discount rate of 9%.

9

Valuation Methodology:

To arrive at the market value of unencumbered Freehold, a direct capitalization method using

ARY can be achieved. For this purpose, multiplier of (1+k) can be implemented. Therefore, the

following calculations ensue:

Market Value of the Property let out = £241.463 pcm

Annual Market Value of the Property = £241.463 * 100 * 12 months = £289755.6 pm

ARY = 8.35%

Hence, [(£289755.6/0.0835)* (1+0.0835)] = [£3470126.95* (1.0835)] = £3759882.55

Hypothetical Scenario 2

i. Market Value of the freehold interest for loan security purposes:

In the context of given case scenario, it has been assumed that the building was let to a

tenant with a reasonable covenant strength 12 years ago on a 15 year Full Repair and Insurance

(FRI) Lease at a rent which is now 15% more than the ERV (Peppercorn and Taffin, 2013). It

has also been assumed that the lease expires in 3 years and that the property is currently over-

rented.

Number of years = 12

Remaining years = 3

Total Span of Lease = 12+ 3 = 15 years

Market Value = Estimated Rental Value = £289755.6 pm

ii. Discounted Cash Flow to show the NPV of the current income and outgoings and the

NPV of the proposed lease:

It has been assumed that on behalf of the landlord and that the tenant has requested a new

lease for 10 years at the market rent and with a rent free period (Rabin, 2013). The proposed

lease incorporates a rent free period which produces a higher NPV than the existing lease

assuming a discount rate of 9%.

9

CONCLUSION

From the above discussion it can be concluded that RICS Global Standards Valuation are

an integral part of Valuation property. It gives a proper guideline in regards to the market value,

estimated rental value, All Risks Market Yield and other related techniques that are important in

giving accurate reflection about the leasehold properties and Freehold Property interest.

10

From the above discussion it can be concluded that RICS Global Standards Valuation are

an integral part of Valuation property. It gives a proper guideline in regards to the market value,

estimated rental value, All Risks Market Yield and other related techniques that are important in

giving accurate reflection about the leasehold properties and Freehold Property interest.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.