CGE17105 Personal Financial Plan: Cheung Family - UOW College HK

VerifiedAdded on 2023/05/31

|17

|2240

|199

Report

AI Summary

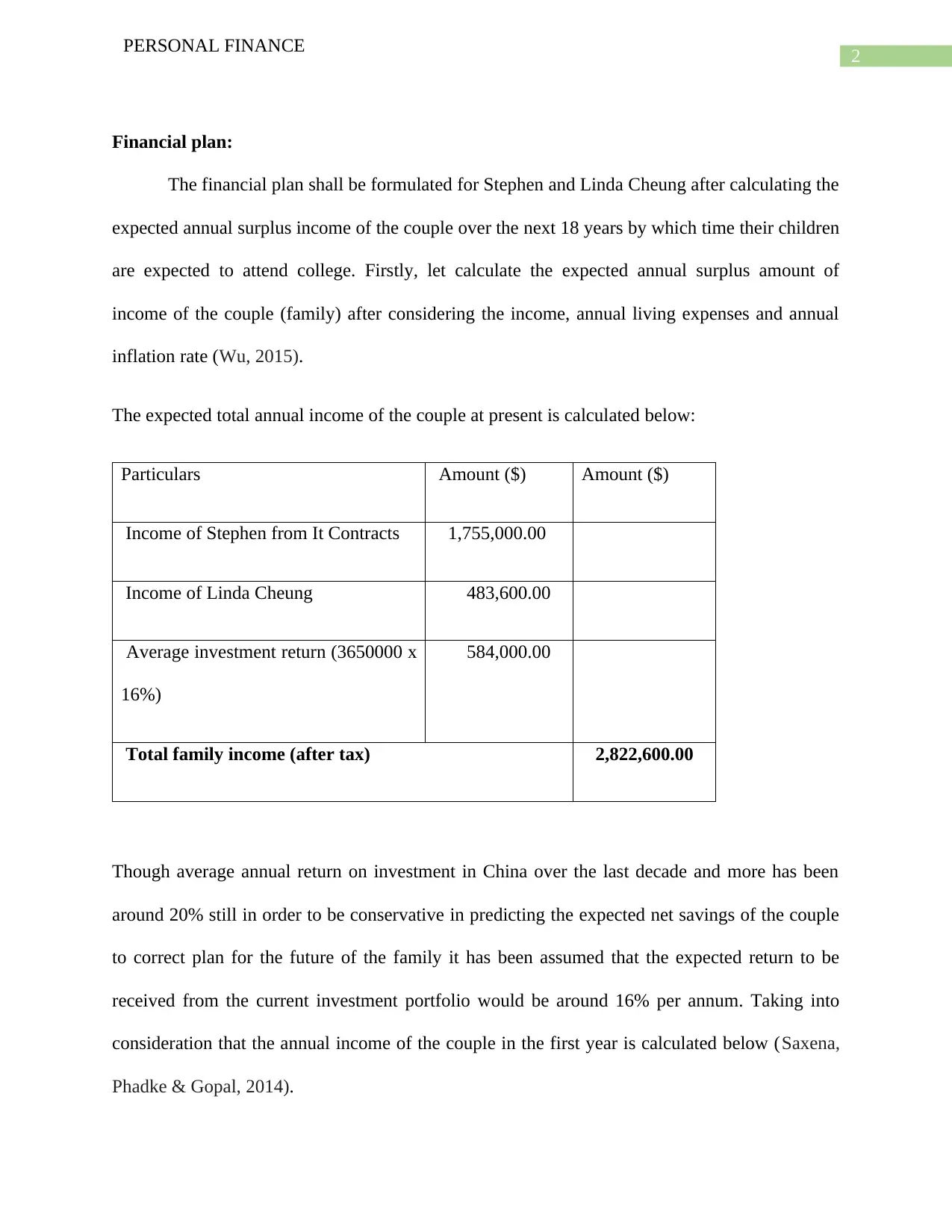

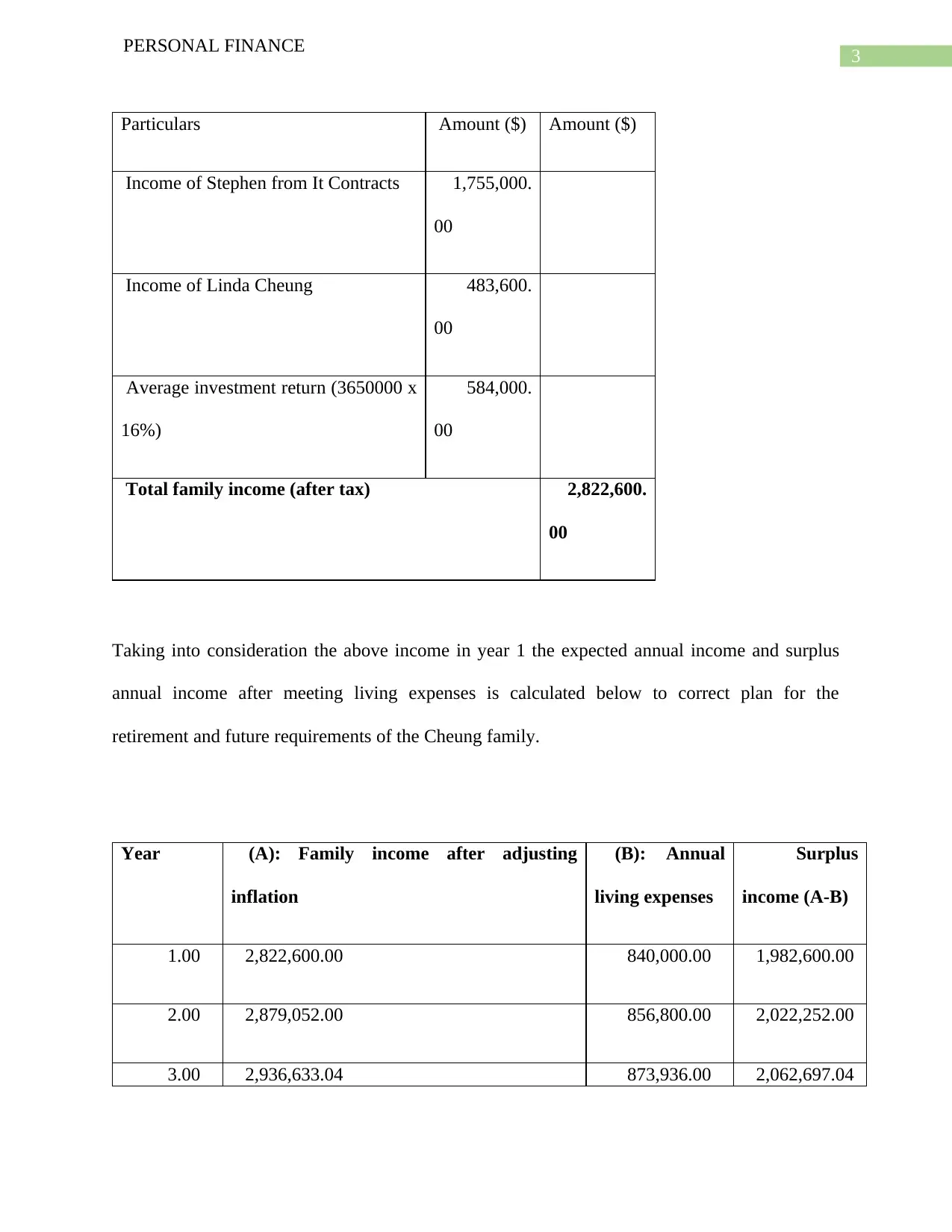

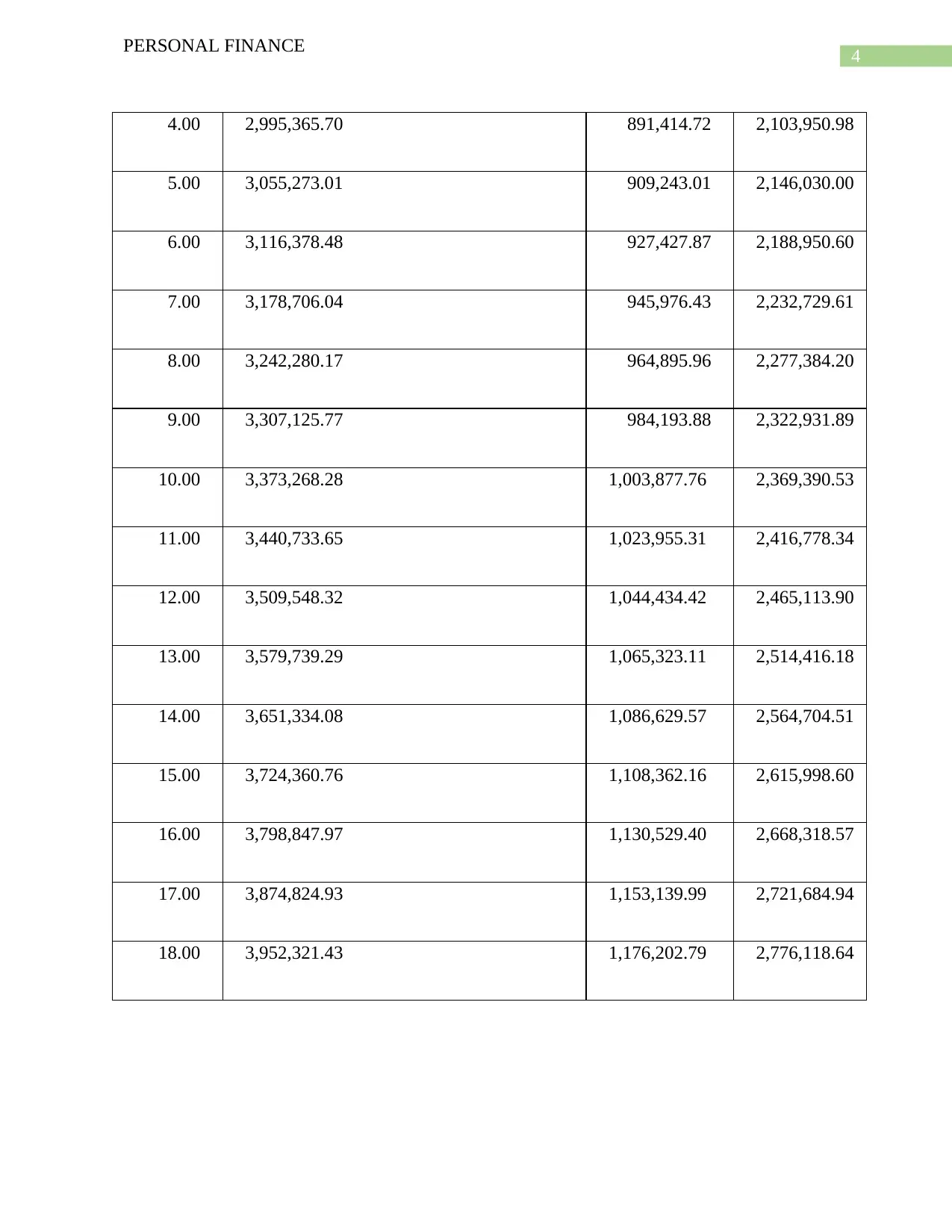

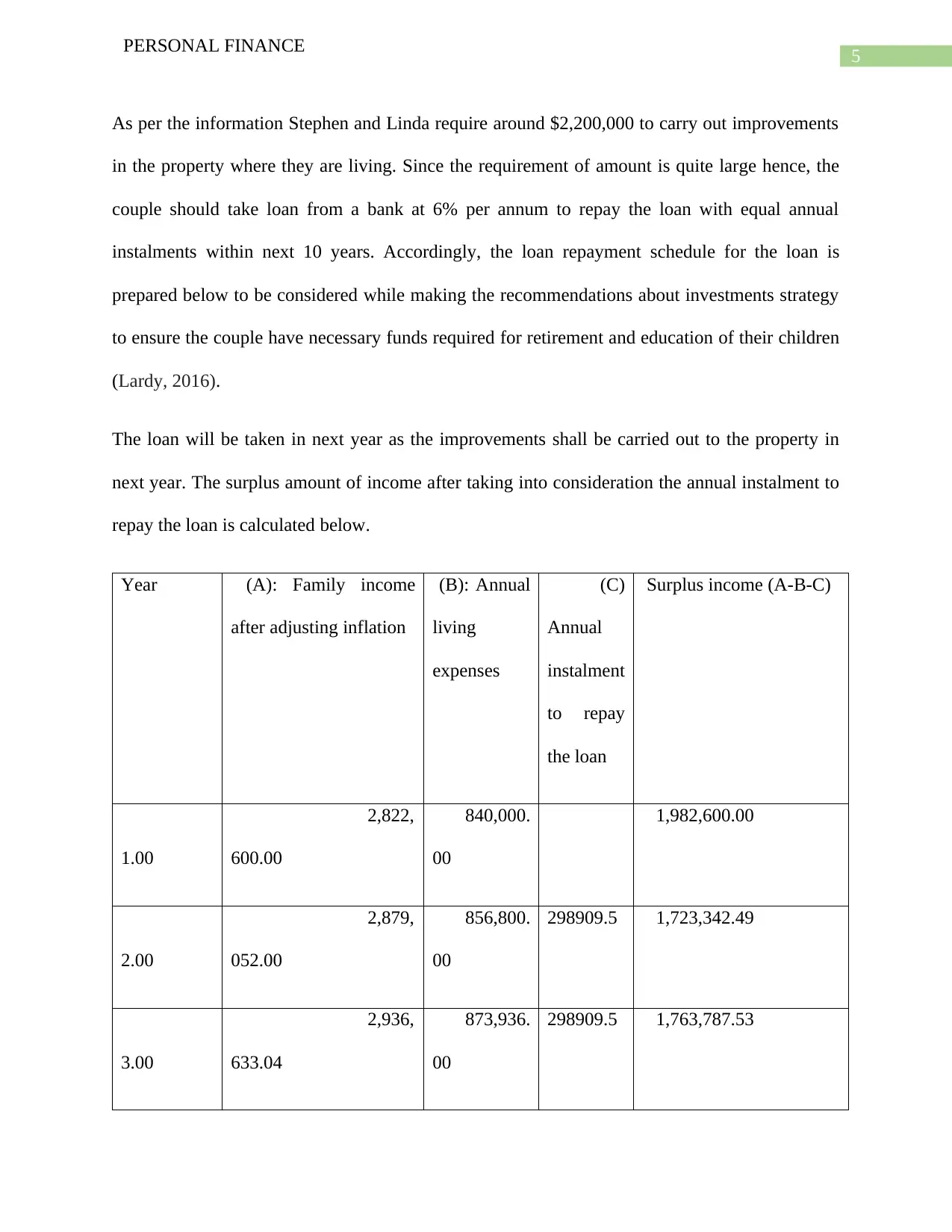

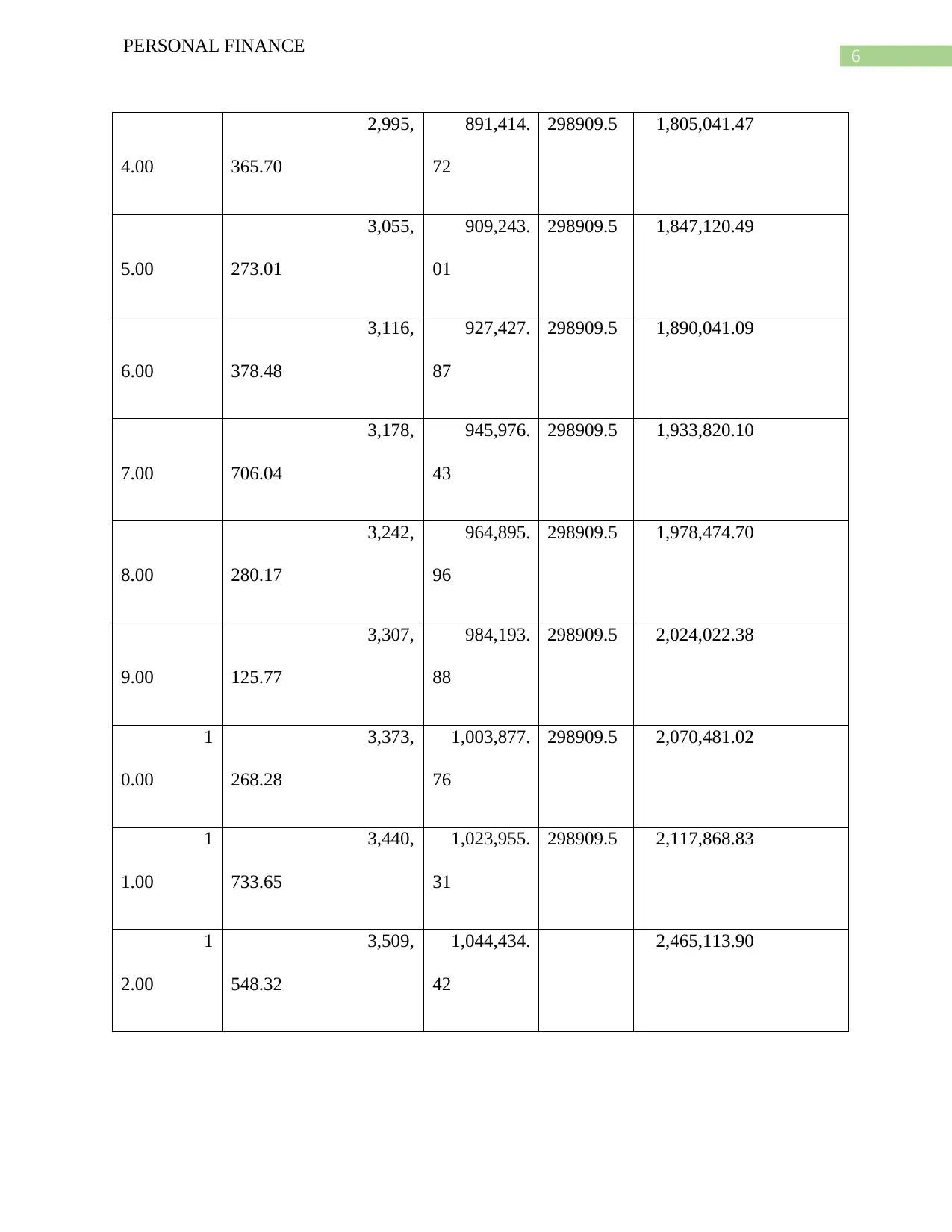

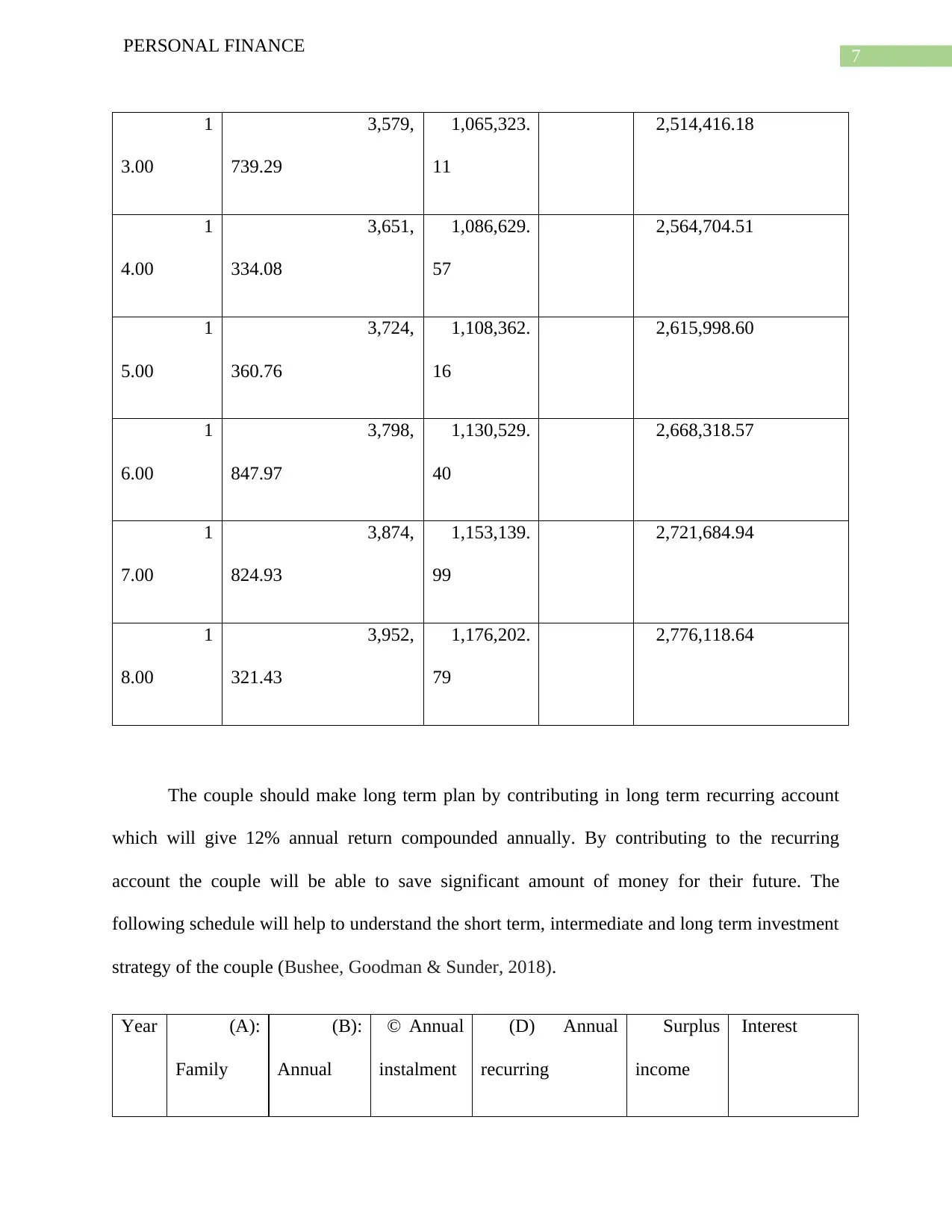

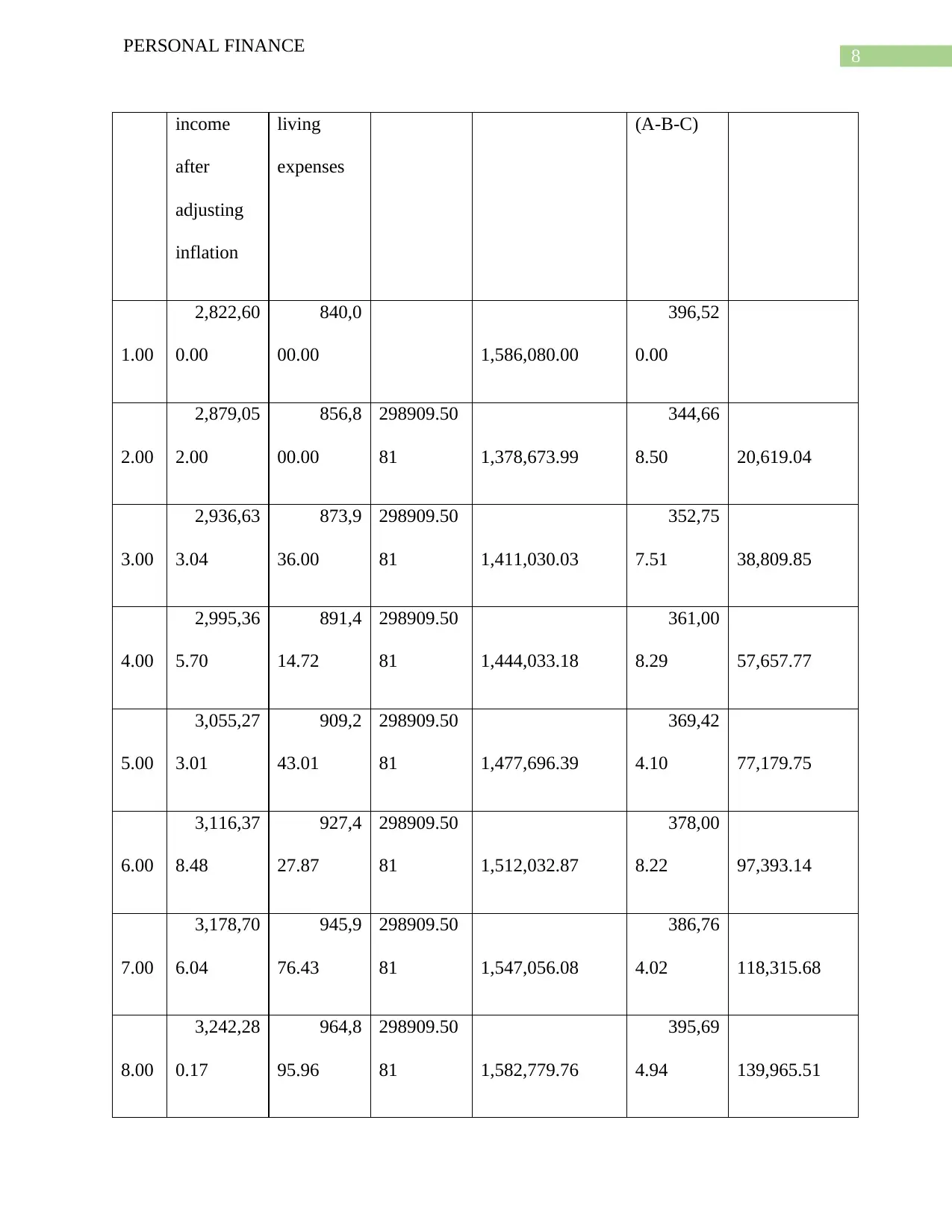

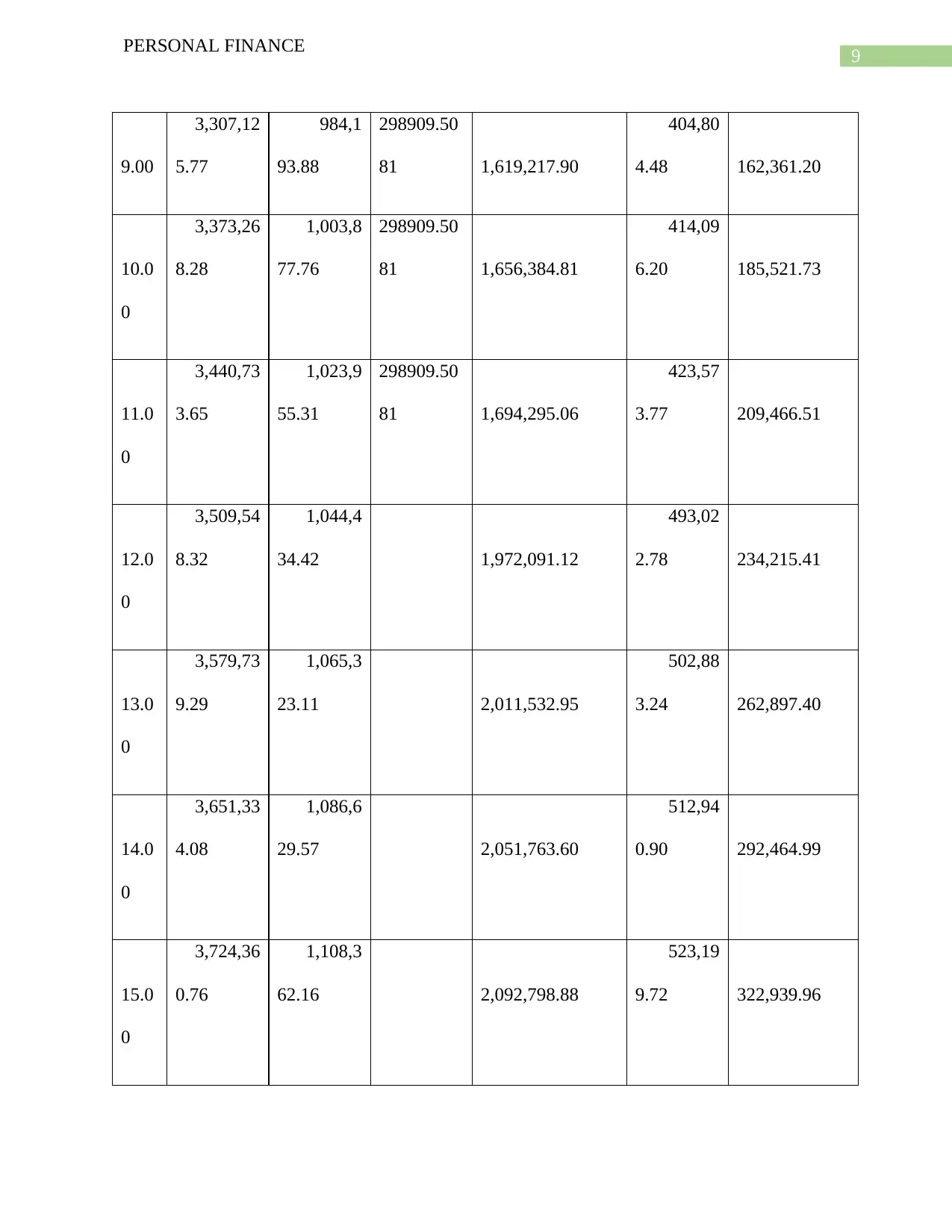

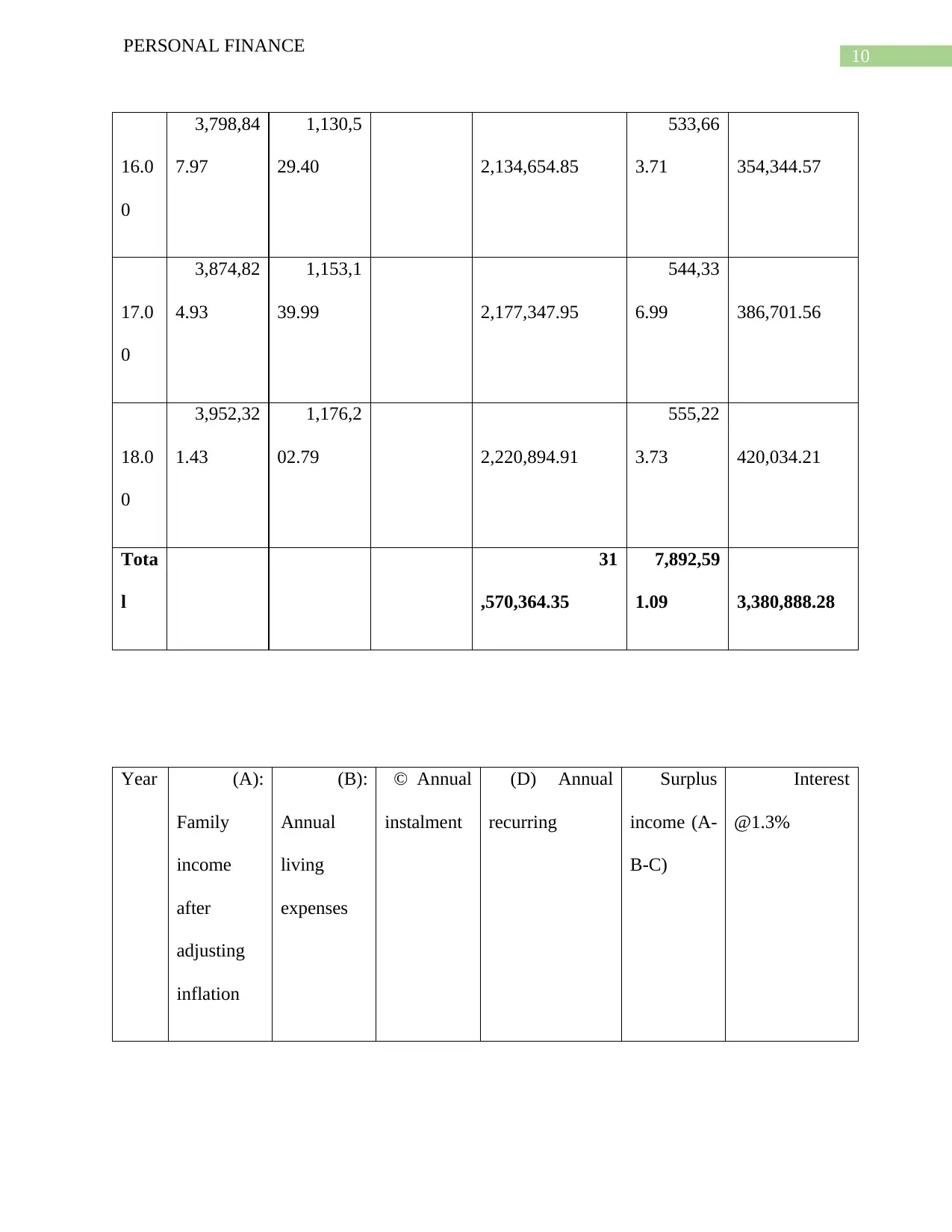

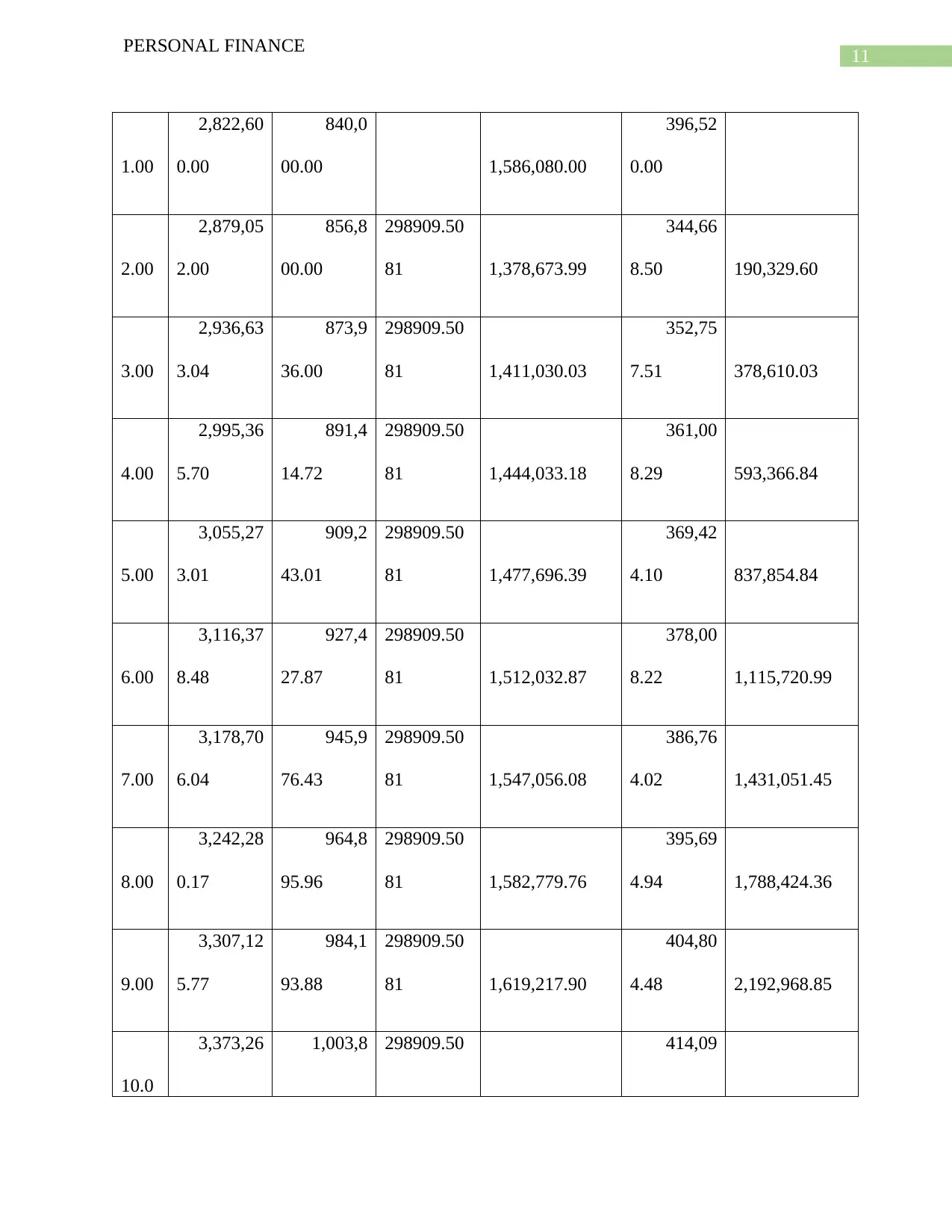

This report provides a comprehensive financial plan for Stephen and Linda Cheung, a couple with two young children, outlining strategies for managing their income, expenses, and investments over the next 18 years until their children attend college. The plan considers their current income from Stephen's IT contracts and Linda's teaching job, alongside their annual living expenses and expected inflation. It includes a loan repayment schedule for property improvements and emphasizes long-term savings through a recurring deposit account with a 12% annual return. The plan recommends investing 80% of their annual surplus in this account to secure funds for their children's education and their own retirement, while also addressing risk tolerance and liquidity considerations. The report concludes with recommendations for loan management and investment strategies to achieve their financial goals.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.